Management Accounting Report: Financial Analysis for Airdri Ltd

VerifiedAdded on 2020/10/23

|20

|5111

|289

Report

AI Summary

This report analyzes the management accounting practices of Airdri Ltd, a small manufacturing company. It covers essential aspects of management accounting, including different systems, reporting methods, and techniques. The report explores cost accounting, inventory management, and job costing systems, as well as methods like cost reporting, budgets, and execution reports. It delves into financial planning, statement analysis, and cost accounting techniques such as absorption and marginal costing. The report also examines the role of management accounting in responding to financial problems and its contribution to sustainable success. The report includes an income statement for the company and discusses how planning tools and budgetary control can help solve problems and support organizations. Finally, the report integrates management accounting within organizational processes.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................3

Explain different methods used for management accounting reporting.....................................5

TASK 2............................................................................................................................................7

Range of management accounting techniques............................................................................7

TASK 3............................................................................................................................................9

Budget as an important control tool............................................................................................9

TASK 4..........................................................................................................................................12

Management accounting to respond to financial problems.......................................................12

An analysis of how in responding to financial problems, management accounting can lead

organisation to sustainable success...........................................................................................13

An evaluation of how planning tools for accounting help to solve problems and support

organisations with sustainable success......................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................3

Explain different methods used for management accounting reporting.....................................5

TASK 2............................................................................................................................................7

Range of management accounting techniques............................................................................7

TASK 3............................................................................................................................................9

Budget as an important control tool............................................................................................9

TASK 4..........................................................................................................................................12

Management accounting to respond to financial problems.......................................................12

An analysis of how in responding to financial problems, management accounting can lead

organisation to sustainable success...........................................................................................13

An evaluation of how planning tools for accounting help to solve problems and support

organisations with sustainable success......................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting that also known as cost accounting, is an process for analysing

or evaluating business cost and operations for prepare financial reports, records and systems to

helps managers in taking appropriate decisions for achieving goals and objectives (Arroyo,

2012). On other hand it is an act of making financial sense and costing data to get useful

information for management and officers within organisation. This report is based on Airdri

which is an small manufacturing company which produce hand dryers and other major

accessories that helps to give suitability to organisation to gain large consumer base. This report

is based on management accounting and their management accounting system. It also includes

methods for management accounting reporting and appropriate tools and techniques for cost

analysis by preparing income statement. Further it includes advantages and disadvantages of

types of planning tools and budgetary control and adaptation of accounting systems to respond

financial problems. Preparation of financial accounts and budgetary control are very important

factors that give important evaluation about stability of an organisation and their future growth.

TASK 1

Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting is an chain of activities that helps in analysing kinds of cost and

operations by preparing internal reports, keeping kinds of records that proved beneficial for

managers in taking important decisions. There are various kinds of roles of management

accounting that are as follows:

Managerial accounting helps managers and other one to take important decisions and it

also provides cost of goods and services in both condition whether product is profitable or not. It

helps in when organisation taking important decisions such as open an new venture and their

important budgetary decisions (Boyns, Edwards and Nikitin, 2013). It helps in comparing actual

decisions with planned performance and evaluation and gives important decisions for critical

evaluation in success of an organisation.

Long term and short term planning:

Management accounting helps in both long term and short term planning while taking

future decisions and plans. It facilitates at time of long term plans, strategic management and

Management accounting that also known as cost accounting, is an process for analysing

or evaluating business cost and operations for prepare financial reports, records and systems to

helps managers in taking appropriate decisions for achieving goals and objectives (Arroyo,

2012). On other hand it is an act of making financial sense and costing data to get useful

information for management and officers within organisation. This report is based on Airdri

which is an small manufacturing company which produce hand dryers and other major

accessories that helps to give suitability to organisation to gain large consumer base. This report

is based on management accounting and their management accounting system. It also includes

methods for management accounting reporting and appropriate tools and techniques for cost

analysis by preparing income statement. Further it includes advantages and disadvantages of

types of planning tools and budgetary control and adaptation of accounting systems to respond

financial problems. Preparation of financial accounts and budgetary control are very important

factors that give important evaluation about stability of an organisation and their future growth.

TASK 1

Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting is an chain of activities that helps in analysing kinds of cost and

operations by preparing internal reports, keeping kinds of records that proved beneficial for

managers in taking important decisions. There are various kinds of roles of management

accounting that are as follows:

Managerial accounting helps managers and other one to take important decisions and it

also provides cost of goods and services in both condition whether product is profitable or not. It

helps in when organisation taking important decisions such as open an new venture and their

important budgetary decisions (Boyns, Edwards and Nikitin, 2013). It helps in comparing actual

decisions with planned performance and evaluation and gives important decisions for critical

evaluation in success of an organisation.

Long term and short term planning:

Management accounting helps in both long term and short term planning while taking

future decisions and plans. It facilitates at time of long term plans, strategic management and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

their accounting and formulation of corporate strategy and at time of study of market trends and

relevancy.

Role in developing management information system:

Management accounting plays very important role at time of developing and taking long

term decisions making for forwarded to managerial staff or personnel at every level of an

organisation for taking important decisions.

Different management accounting system:

Management accounting system emphasis on collecting information and data with help of

external parties in which stakeholders, public regulators and lenders by following accounting

principles (Contrafatto and Burns, 2013). There are some kind of management accounting

system that vary from organisation to organisation and each system should be developed after

analysing needs of management that helps in taking important decisions.

The most basic types of management accounting system are:

Cost accounting system

Inventory management system

Job costing system

Price optimization system

Cost accounting system:

Cost accounting system that also known as product costing system which is an

framework used by organisations for estimation or evaluation of costs of products for

profitability analysis, inventory valuation with controlling cost. Calculation of accurate cost of

products and services are very much crucial with critical for Airdri ltd at time of profitability

operations. There are various kinds of cost accounting system that are fixed cost, variable cost

and opportunity cost with sunk cost that are important part for an organisational growth and

enhancement. With there are various costing techniques in which marginal costing, standard

costing with direct costing etc.. the main advantage of it that it disclose profitable and

unprofitable actions with guide for production policies.

Inventory management system:

Inventory management system helps in track the goods and services by entire supply

chain or by business operations operates under inventory management system (Grötsch, Blome

and Schleper, 2013). In that system it covers from production to retailing, warehousing to

relevancy.

Role in developing management information system:

Management accounting plays very important role at time of developing and taking long

term decisions making for forwarded to managerial staff or personnel at every level of an

organisation for taking important decisions.

Different management accounting system:

Management accounting system emphasis on collecting information and data with help of

external parties in which stakeholders, public regulators and lenders by following accounting

principles (Contrafatto and Burns, 2013). There are some kind of management accounting

system that vary from organisation to organisation and each system should be developed after

analysing needs of management that helps in taking important decisions.

The most basic types of management accounting system are:

Cost accounting system

Inventory management system

Job costing system

Price optimization system

Cost accounting system:

Cost accounting system that also known as product costing system which is an

framework used by organisations for estimation or evaluation of costs of products for

profitability analysis, inventory valuation with controlling cost. Calculation of accurate cost of

products and services are very much crucial with critical for Airdri ltd at time of profitability

operations. There are various kinds of cost accounting system that are fixed cost, variable cost

and opportunity cost with sunk cost that are important part for an organisational growth and

enhancement. With there are various costing techniques in which marginal costing, standard

costing with direct costing etc.. the main advantage of it that it disclose profitable and

unprofitable actions with guide for production policies.

Inventory management system:

Inventory management system helps in track the goods and services by entire supply

chain or by business operations operates under inventory management system (Grötsch, Blome

and Schleper, 2013). In that system it covers from production to retailing, warehousing to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shipping and until movement of stock to end user. It helps in moving of parts of operations for

taking better decisions and invest money at appropriate time frame.

Job costing system:

Job costing is an system that use for assigning and accumulating cost of manufacturing

for an individual unit. It is useful in case of when various items should be produced that are

totally different from each other.

Price optimization system :

Price optimization use for mathematical evaluation or analysis for determine response of

consumers to different prices related to product and services by different channels. It helps in

determination of prices that helps in best meet their objectives and goals for operating profit.

These various management accounting systems are very much essential for an organisation at

time of launching a new product and services with taking crucial decisions. There are some

major benefits of price optimization system that are revenue generate from it helps in give

growth and expansion of a business and gain more insights for the various kinds of pricing

strategies.

Explain different methods used for management accounting reporting.

Managerial which also known as management accounting, that concentrates on receiving

data and information by financial accounting (Hoque, Covaleski and N. Gooneratne, 2013). It

proved useful in preparing financial statements, earning statements and cash flow statements and

also balance sheet which are essential for any organisation in evaluating viability of their project.

There are kinds of methods for evaluating accounting reporting that are as follows:

Cost reporting:

Managerial accounting helps in estimation of price of products and services. It estimates

by completing whole fresh pricing, over head cost and labour cost and any other pricing

considerations. In that entire cost divided into total items created in it, whole data and

information that enables managers in viewing pricing of products and selling cost. It is an

important source for plan and manage income limits of an organisation. The main benefits of

cost reporting that it gives financial confidence and job management with that organisation can

coordinate each and every activity in better way with it supports claims to gain contractual

claims in better way.

Budgets:

taking better decisions and invest money at appropriate time frame.

Job costing system:

Job costing is an system that use for assigning and accumulating cost of manufacturing

for an individual unit. It is useful in case of when various items should be produced that are

totally different from each other.

Price optimization system :

Price optimization use for mathematical evaluation or analysis for determine response of

consumers to different prices related to product and services by different channels. It helps in

determination of prices that helps in best meet their objectives and goals for operating profit.

These various management accounting systems are very much essential for an organisation at

time of launching a new product and services with taking crucial decisions. There are some

major benefits of price optimization system that are revenue generate from it helps in give

growth and expansion of a business and gain more insights for the various kinds of pricing

strategies.

Explain different methods used for management accounting reporting.

Managerial which also known as management accounting, that concentrates on receiving

data and information by financial accounting (Hoque, Covaleski and N. Gooneratne, 2013). It

proved useful in preparing financial statements, earning statements and cash flow statements and

also balance sheet which are essential for any organisation in evaluating viability of their project.

There are kinds of methods for evaluating accounting reporting that are as follows:

Cost reporting:

Managerial accounting helps in estimation of price of products and services. It estimates

by completing whole fresh pricing, over head cost and labour cost and any other pricing

considerations. In that entire cost divided into total items created in it, whole data and

information that enables managers in viewing pricing of products and selling cost. It is an

important source for plan and manage income limits of an organisation. The main benefits of

cost reporting that it gives financial confidence and job management with that organisation can

coordinate each and every activity in better way with it supports claims to gain contractual

claims in better way.

Budgets:

One of most important management accounting tool that is planning of spending on plans

so that spending should be controlled. Budgets are mostly created by utilizing previous financial

plans for accumulating future plans and projections. An organisation spends their money on list

of income and expenditure so that evaluation of each and every factor are very important for

Airdri ltd. The major benefits of budget that it gives control over money and helps in focused on

money goals and objectives so that organisation can control each and every activity in

coordinated way to reach at desirable goals and objectives in better way.

Execution reports:

Management and their accountants avail various spending plans for contrasting income

and expenditure with planned sums (Lavia López and Hiebl, 2014). An organisation after

implementing new budgets and policies bring changes for intended should be analysed and entire

data are listed on report of their performance.

Benefits of management accounting:

There are kinds of advantages of management accounting that are as follows:

It helps in measuring or evaluating actual performance by comparing budgets of an

organisation so that desirable goals should be achieve.

It also helps in management in a way that can maximise return of capital employed which

is an important attribute for an manufacturing organisation.

It enables in preparing budgeting and planning of works and activities by applying

various applications in context of Airdri ltd.

Integration of management accounting system and management reporting within

organisational process:

Management reporting Integration with organisational process

Budget report Budget report is integrate with organisational

process in context of Airdri limited to get

accurate financial stability. In that budget that

helps in predicting income and expenditure of

each term to eliminate risk factor.

Performance report Performance report shows performance level

so that spending should be controlled. Budgets are mostly created by utilizing previous financial

plans for accumulating future plans and projections. An organisation spends their money on list

of income and expenditure so that evaluation of each and every factor are very important for

Airdri ltd. The major benefits of budget that it gives control over money and helps in focused on

money goals and objectives so that organisation can control each and every activity in

coordinated way to reach at desirable goals and objectives in better way.

Execution reports:

Management and their accountants avail various spending plans for contrasting income

and expenditure with planned sums (Lavia López and Hiebl, 2014). An organisation after

implementing new budgets and policies bring changes for intended should be analysed and entire

data are listed on report of their performance.

Benefits of management accounting:

There are kinds of advantages of management accounting that are as follows:

It helps in measuring or evaluating actual performance by comparing budgets of an

organisation so that desirable goals should be achieve.

It also helps in management in a way that can maximise return of capital employed which

is an important attribute for an manufacturing organisation.

It enables in preparing budgeting and planning of works and activities by applying

various applications in context of Airdri ltd.

Integration of management accounting system and management reporting within

organisational process:

Management reporting Integration with organisational process

Budget report Budget report is integrate with organisational

process in context of Airdri limited to get

accurate financial stability. In that budget that

helps in predicting income and expenditure of

each term to eliminate risk factor.

Performance report Performance report shows performance level

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of each individual by smooth functioning of an

individual (Leitner, 2013). It helps in

identifying skills of an individual in taking

appropriate decisions and building strategies.

That provides attributes in analysis of

individual performance.

Inventory and manufacturing report Inventory is an important tool that helps in

evaluation of each attribute such as stock,

income and expenditure with carrying cost of

it.

TASK 2

Range of management accounting techniques.

In management accounting to get desirables outcomes organisation have to apply

different tools and techniques that are as follows;

Financial planning:

The main task of financial planning is to maximise profits and consumer base. Its main

motive to achieve sound financial planning and their coordination (Lukka and Vinnari, 2014).

Therefore it is one of most important tool for achieving goals and objectives in proper way. That

tool use by Airdri limited to record all transactions in proper way to accord with changes.

Financial statement analysis:

Profit and loss accounts and balance sheet consider as an important financial statements

of an organisation. It should be analysed in different periods of time. It enables in analysing

activities of management and growth of business. This can be done through common size

statements, financial accounting and ratio analysis.

Cost accounting:

Cost accounting is one of important tool that helps in cost data by product wise,

department wise, branch wise and many more. It compared with predetermined goals and

objectives, by comparing two cost helps to Airdri limited to decide the factors that helps in bring

difference in cost.

individual (Leitner, 2013). It helps in

identifying skills of an individual in taking

appropriate decisions and building strategies.

That provides attributes in analysis of

individual performance.

Inventory and manufacturing report Inventory is an important tool that helps in

evaluation of each attribute such as stock,

income and expenditure with carrying cost of

it.

TASK 2

Range of management accounting techniques.

In management accounting to get desirables outcomes organisation have to apply

different tools and techniques that are as follows;

Financial planning:

The main task of financial planning is to maximise profits and consumer base. Its main

motive to achieve sound financial planning and their coordination (Lukka and Vinnari, 2014).

Therefore it is one of most important tool for achieving goals and objectives in proper way. That

tool use by Airdri limited to record all transactions in proper way to accord with changes.

Financial statement analysis:

Profit and loss accounts and balance sheet consider as an important financial statements

of an organisation. It should be analysed in different periods of time. It enables in analysing

activities of management and growth of business. This can be done through common size

statements, financial accounting and ratio analysis.

Cost accounting:

Cost accounting is one of important tool that helps in cost data by product wise,

department wise, branch wise and many more. It compared with predetermined goals and

objectives, by comparing two cost helps to Airdri limited to decide the factors that helps in bring

difference in cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

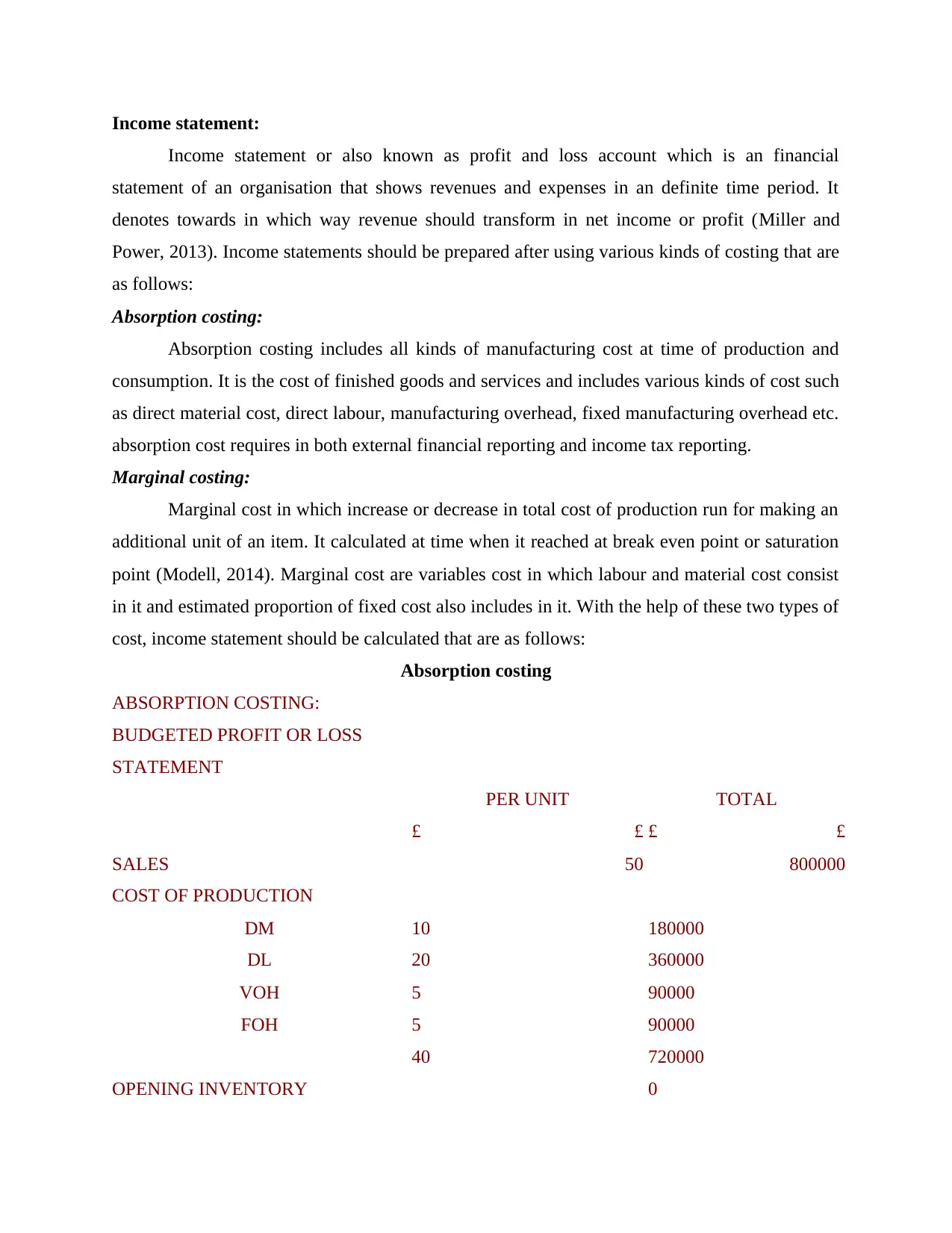

Income statement:

Income statement or also known as profit and loss account which is an financial

statement of an organisation that shows revenues and expenses in an definite time period. It

denotes towards in which way revenue should transform in net income or profit (Miller and

Power, 2013). Income statements should be prepared after using various kinds of costing that are

as follows:

Absorption costing:

Absorption costing includes all kinds of manufacturing cost at time of production and

consumption. It is the cost of finished goods and services and includes various kinds of cost such

as direct material cost, direct labour, manufacturing overhead, fixed manufacturing overhead etc.

absorption cost requires in both external financial reporting and income tax reporting.

Marginal costing:

Marginal cost in which increase or decrease in total cost of production run for making an

additional unit of an item. It calculated at time when it reached at break even point or saturation

point (Modell, 2014). Marginal cost are variables cost in which labour and material cost consist

in it and estimated proportion of fixed cost also includes in it. With the help of these two types of

cost, income statement should be calculated that are as follows:

Absorption costing

ABSORPTION COSTING:

BUDGETED PROFIT OR LOSS

STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

Income statement or also known as profit and loss account which is an financial

statement of an organisation that shows revenues and expenses in an definite time period. It

denotes towards in which way revenue should transform in net income or profit (Miller and

Power, 2013). Income statements should be prepared after using various kinds of costing that are

as follows:

Absorption costing:

Absorption costing includes all kinds of manufacturing cost at time of production and

consumption. It is the cost of finished goods and services and includes various kinds of cost such

as direct material cost, direct labour, manufacturing overhead, fixed manufacturing overhead etc.

absorption cost requires in both external financial reporting and income tax reporting.

Marginal costing:

Marginal cost in which increase or decrease in total cost of production run for making an

additional unit of an item. It calculated at time when it reached at break even point or saturation

point (Modell, 2014). Marginal cost are variables cost in which labour and material cost consist

in it and estimated proportion of fixed cost also includes in it. With the help of these two types of

cost, income statement should be calculated that are as follows:

Absorption costing

ABSORPTION COSTING:

BUDGETED PROFIT OR LOSS

STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

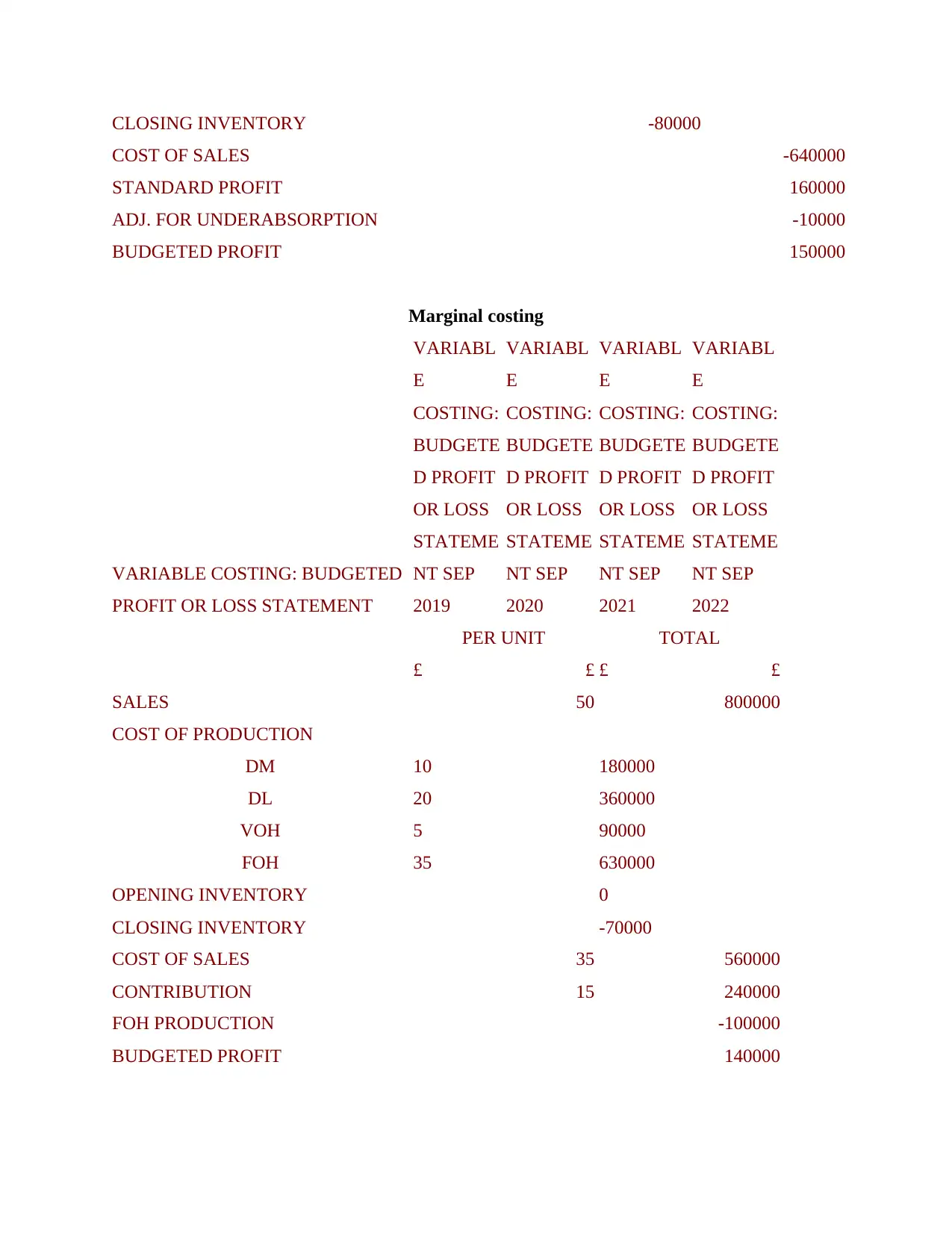

Marginal costing

VARIABLE COSTING: BUDGETED

PROFIT OR LOSS STATEMENT

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2019

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2020

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2021

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2022

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

Marginal costing

VARIABLE COSTING: BUDGETED

PROFIT OR LOSS STATEMENT

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2019

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2020

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2021

VARIABL

E

COSTING:

BUDGETE

D PROFIT

OR LOSS

STATEME

NT SEP

2022

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales=

Fixed cost+

desired

profit/

contribution

per unit

Fixed cost+

desired

profit/

contribution

per unit

Fixed cost+

desired

profit/

contribution

per unit

Interpretation:

from the above calculation it has been summarised that company get net profit by both

the above mentioned method in income statement. By using absorption method organisation sell

minus variable cost on other hand sales minus variable expenses and after all organisation get

great profit ratio which is an important indicator of organisational growth and enhancement. On

other hand sales denotes towards fixed cost plus desired profit and contribution per unit.

Direct variable cost:

Direct variable cost consist of raw materials which increase as total as more units of

production should be manufactured. Cost that are associated with department should be direct or

fixed.

Fixed cost with elements:

Fixed cost+

desired

profit/

contribution

per unit

Fixed cost+

desired

profit/

contribution

per unit

Fixed cost+

desired

profit/

contribution

per unit

Interpretation:

from the above calculation it has been summarised that company get net profit by both

the above mentioned method in income statement. By using absorption method organisation sell

minus variable cost on other hand sales minus variable expenses and after all organisation get

great profit ratio which is an important indicator of organisational growth and enhancement. On

other hand sales denotes towards fixed cost plus desired profit and contribution per unit.

Direct variable cost:

Direct variable cost consist of raw materials which increase as total as more units of

production should be manufactured. Cost that are associated with department should be direct or

fixed.

Fixed cost with elements:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed cost are business expenses that are not rely upon the level of products and services

produced by the business. It should be time related in which major tools consist of interest or

rents that paid per month.

Difference in marginal cost income statement and absorption cost income statement:

There are some differences while preparing income statement of marginal and absorption

that reflect profit through which no sales has been made. That happen due to the fixed cost of

manufacturing overheads on other hand variable statement show loss as no sales.

TASK 3

Budget as an important control tool.

Budget is an quantitative statement, for an definite time period in which includes

planned revenues, expenditure and assets, liabilities and cash flows. It is an process of designing,

implementing and controlling budgets (Nielsen, Mitchell and Nørreklit, 2015). Budget gives an

overview about organisation and its various works and activities to control various works and

activities.

Budgetary control:

Budgetary control is an kind of tool that helps managers to perform in an structured way.

In budgetary control managers evaluates financial goals and objectives by comparing with actual

performance for an organisation. In budget various kinds of planning tools and techniques

includes that are very much crucial and helps in performance of management and their key

members. In that controlling tool managers build kinds of budget and evaluate performance

accordingly, apart from that it helps in giving estimation of future income and expenditure that

helps in making strategies and attain goals. In scenario of Airdri that successfully avails

budgetary control measures that helps in bring estimation of future revenues and cost for

performance evaluation. In budgetary control consist of various tools and techniques that are as

follows:

Forecasting tool:

Forecasting tool is an tool which helps to business to protect their works and activities

from uncertainty. Future activities should be secure by adopting assumptions that totally based

on forecasting of works and activities (Stechemesser and Guenther, 2012). Forecast not actually

implement but estimation should be made with its estimation should based on working in past,

produced by the business. It should be time related in which major tools consist of interest or

rents that paid per month.

Difference in marginal cost income statement and absorption cost income statement:

There are some differences while preparing income statement of marginal and absorption

that reflect profit through which no sales has been made. That happen due to the fixed cost of

manufacturing overheads on other hand variable statement show loss as no sales.

TASK 3

Budget as an important control tool.

Budget is an quantitative statement, for an definite time period in which includes

planned revenues, expenditure and assets, liabilities and cash flows. It is an process of designing,

implementing and controlling budgets (Nielsen, Mitchell and Nørreklit, 2015). Budget gives an

overview about organisation and its various works and activities to control various works and

activities.

Budgetary control:

Budgetary control is an kind of tool that helps managers to perform in an structured way.

In budgetary control managers evaluates financial goals and objectives by comparing with actual

performance for an organisation. In budget various kinds of planning tools and techniques

includes that are very much crucial and helps in performance of management and their key

members. In that controlling tool managers build kinds of budget and evaluate performance

accordingly, apart from that it helps in giving estimation of future income and expenditure that

helps in making strategies and attain goals. In scenario of Airdri that successfully avails

budgetary control measures that helps in bring estimation of future revenues and cost for

performance evaluation. In budgetary control consist of various tools and techniques that are as

follows:

Forecasting tool:

Forecasting tool is an tool which helps to business to protect their works and activities

from uncertainty. Future activities should be secure by adopting assumptions that totally based

on forecasting of works and activities (Stechemesser and Guenther, 2012). Forecast not actually

implement but estimation should be made with its estimation should based on working in past,

nature of an organisation and some other factors. That kind of forecasting methods and tools in

which expert opinion method, delphi method and technique etc.. in case of Airdri apply kinds of

tools to predict their future plans and policies and their advantages and disadvantages are as

follows:

Advantages:

The forecasting tool enables in identification of activities that proved advantageous for an

organisation and it helps in allocation of kinds of resources in effective manner. It helps in accessing needs and wants of consumers and produce products accordingly.

Disadvantages:

Forecasting totally based on past performance of an organisation and sometimes it proved

hazardous for them to reveal all past knowledge and information, in that condition

predication is not accurate.

Forecasting require resources and time for reach at desirable goals and objectives and it

hinders self interest of an organisation.

Fixed budget:

Fixed budget or static budget not change according to change in sales or quantity. It is

most suitable for activities which not fluctuate in future. It is one of most tool for budgetary

control and use for remain fixed in future. In case of Airdri use that tool for activities that not

change in future frequently. So it helps in concentrating works and activities that are important in

nature and not require to update frequently and also save time.

Advantages:

Fixed budget is easy and prepare frequently because these kinds of budgets are easily

track performance of an organisation without any kind of hurdles. It not obligatory to

update it every month. It also enables to organisation for planning to attain future goals and objectives.

Disadvantages:

It is one of most significant kind of budget in which variations not occurred in budget due

to sales or any other factors.

The schedule or framework of that budget based on past works and activities that

sometimes not possible for an organisation.

Flexible budget:

which expert opinion method, delphi method and technique etc.. in case of Airdri apply kinds of

tools to predict their future plans and policies and their advantages and disadvantages are as

follows:

Advantages:

The forecasting tool enables in identification of activities that proved advantageous for an

organisation and it helps in allocation of kinds of resources in effective manner. It helps in accessing needs and wants of consumers and produce products accordingly.

Disadvantages:

Forecasting totally based on past performance of an organisation and sometimes it proved

hazardous for them to reveal all past knowledge and information, in that condition

predication is not accurate.

Forecasting require resources and time for reach at desirable goals and objectives and it

hinders self interest of an organisation.

Fixed budget:

Fixed budget or static budget not change according to change in sales or quantity. It is

most suitable for activities which not fluctuate in future. It is one of most tool for budgetary

control and use for remain fixed in future. In case of Airdri use that tool for activities that not

change in future frequently. So it helps in concentrating works and activities that are important in

nature and not require to update frequently and also save time.

Advantages:

Fixed budget is easy and prepare frequently because these kinds of budgets are easily

track performance of an organisation without any kind of hurdles. It not obligatory to

update it every month. It also enables to organisation for planning to attain future goals and objectives.

Disadvantages:

It is one of most significant kind of budget in which variations not occurred in budget due

to sales or any other factors.

The schedule or framework of that budget based on past works and activities that

sometimes not possible for an organisation.

Flexible budget:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.