Management Accounting Report: Financial Analysis of Airline Scenarios

VerifiedAdded on 2020/05/16

|8

|1727

|81

Report

AI Summary

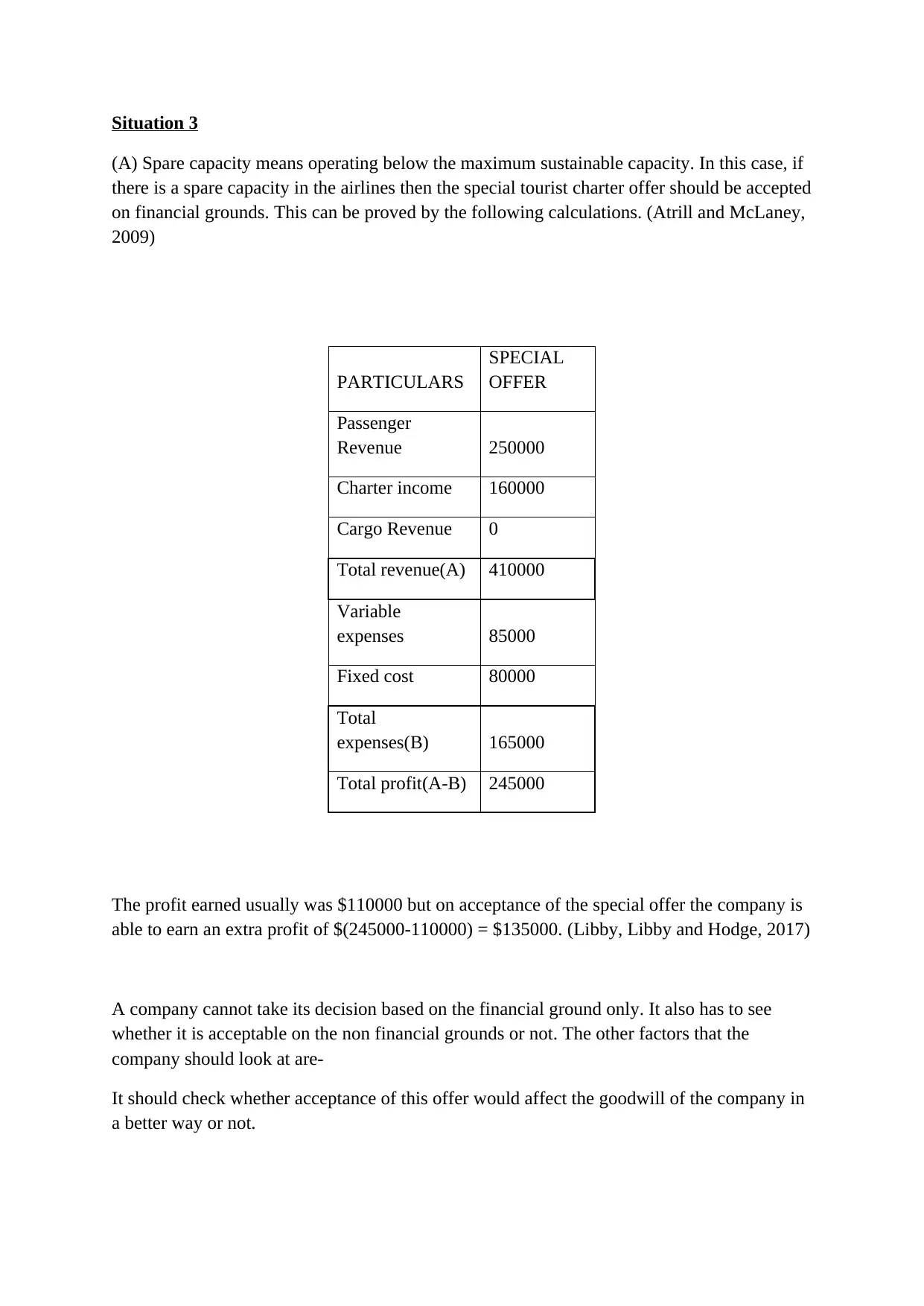

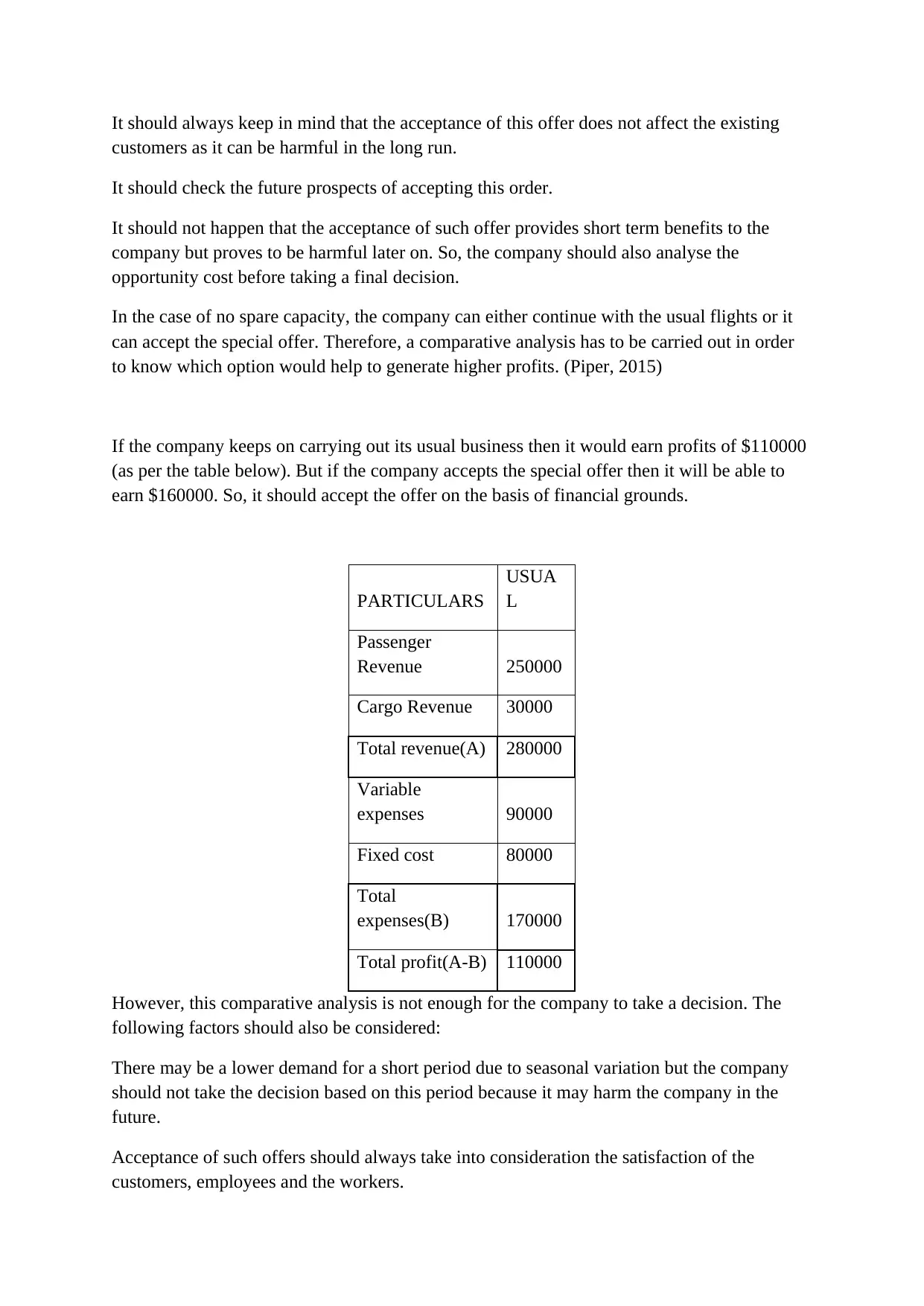

This report analyzes three financial scenarios faced by an airline company using management accounting principles. The first situation evaluates the decision to replace a loader truck with a conveyor belt, considering cash flows both with and without a depreciation tax shield. The second scenario examines the profitability of non-stop versus stop-over flights, highlighting the impact of various costs on overall profit. The third situation addresses the acceptance of a special tourist charter offer, considering both financial and non-financial factors, such as spare capacity and potential impacts on existing customers. The report emphasizes the importance of comprehensive financial analysis, including the consideration of both quantitative and qualitative aspects, for effective decision-making in the airline industry, referencing factors such as industry standards, customer satisfaction, and potential risks.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.