Airline Revenue Management: ANA Group Financial Analysis Report

VerifiedAdded on 2022/08/12

|14

|1852

|12

Report

AI Summary

This report provides a comprehensive financial analysis of ANA Group, a major Japanese airline. It begins with an introduction to airline revenue management and a background of ANA. The core of the report focuses on a detailed financial analysis, evaluating profitability, liquidity, efficiency, and solvency ratios from 2017 to 2018. The analysis includes examination of the company's revenues, broken down by source, and its costs, highlighting factors that influence both. The report also explores the airline's revenue management strategies and offers recommendations for cost reduction and debt management to improve profitability. The report is based on the provided financial data and aims to demonstrate an understanding of airline economics and financial performance.

Running Head: ARLINE REVENUE MANAGEMENT

AIRLINE REVENUE MANAGEMENT

Name of the Student

Name of the University

Author Note

AIRLINE REVENUE MANAGEMENT

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AIRLINE REVENUE MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Background of Company...........................................................................................................2

Financial Analysis of Company.................................................................................................3

Analysis of Revenues and Costs of Company...........................................................................5

Conclusion..................................................................................................................................8

Reference....................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Background of Company...........................................................................................................2

Financial Analysis of Company.................................................................................................3

Analysis of Revenues and Costs of Company...........................................................................5

Conclusion..................................................................................................................................8

Reference....................................................................................................................................9

2AIRLINE REVENUE MANAGEMENT

Introduction

Airlines are held up as epitome of the best practices in the revenue and pricing

management. This industry invests heavily in the development of sophisticated systems for

the forecasting demand, availability and managing of inventory and responding and

monitoring of the prices of competitor in market. Airlines have been leaders in the revenue

and pricing management through investing heavily in the applications of technology for the

higher yields and competitive advantage (Schosser and Wittmer 2015). Hence, this report

aims to discuss activities and business model of ANA Group. Further, analysis will be done

on financial performance of company. Lastly, analysis will be done on costs and revenue of

airline and based on that recommendations will be given on the way airline should manage

them.

Background of Company

All Nippon Airways is the Japanese airline company, headquartered in Tokyo. The

company operates services to forty-nine destinations in Japan and thirty-two destinations in

the international route. ANA is having extensive domestic route network, which covers

entirety of the Japan from Hokkaido in north to the Okinawa in south. The network of

international route extends through the Southeast Asia, Korea, China, US and Western

Europe (Ssl4.eir-parts.net. 2020).

ANA is largest Japanese airline by the number of passengers and its revenue. The

market capitalization of ANA is ¥972.62 billion. The company intends to leverage every

opportunities of business as tailwind that propels it towards the vision of management to

become leading group of airline and ongoing sustainable growth. These opportunities include

rise in demand for the air travel among emerging Asian economies, increasing demand for

Introduction

Airlines are held up as epitome of the best practices in the revenue and pricing

management. This industry invests heavily in the development of sophisticated systems for

the forecasting demand, availability and managing of inventory and responding and

monitoring of the prices of competitor in market. Airlines have been leaders in the revenue

and pricing management through investing heavily in the applications of technology for the

higher yields and competitive advantage (Schosser and Wittmer 2015). Hence, this report

aims to discuss activities and business model of ANA Group. Further, analysis will be done

on financial performance of company. Lastly, analysis will be done on costs and revenue of

airline and based on that recommendations will be given on the way airline should manage

them.

Background of Company

All Nippon Airways is the Japanese airline company, headquartered in Tokyo. The

company operates services to forty-nine destinations in Japan and thirty-two destinations in

the international route. ANA is having extensive domestic route network, which covers

entirety of the Japan from Hokkaido in north to the Okinawa in south. The network of

international route extends through the Southeast Asia, Korea, China, US and Western

Europe (Ssl4.eir-parts.net. 2020).

ANA is largest Japanese airline by the number of passengers and its revenue. The

market capitalization of ANA is ¥972.62 billion. The company intends to leverage every

opportunities of business as tailwind that propels it towards the vision of management to

become leading group of airline and ongoing sustainable growth. These opportunities include

rise in demand for the air travel among emerging Asian economies, increasing demand for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AIRLINE REVENUE MANAGEMENT

the travel to Japan as well as increase in the slots at the Tokyo metropolitan area airports

(Pineda et al. 2018).

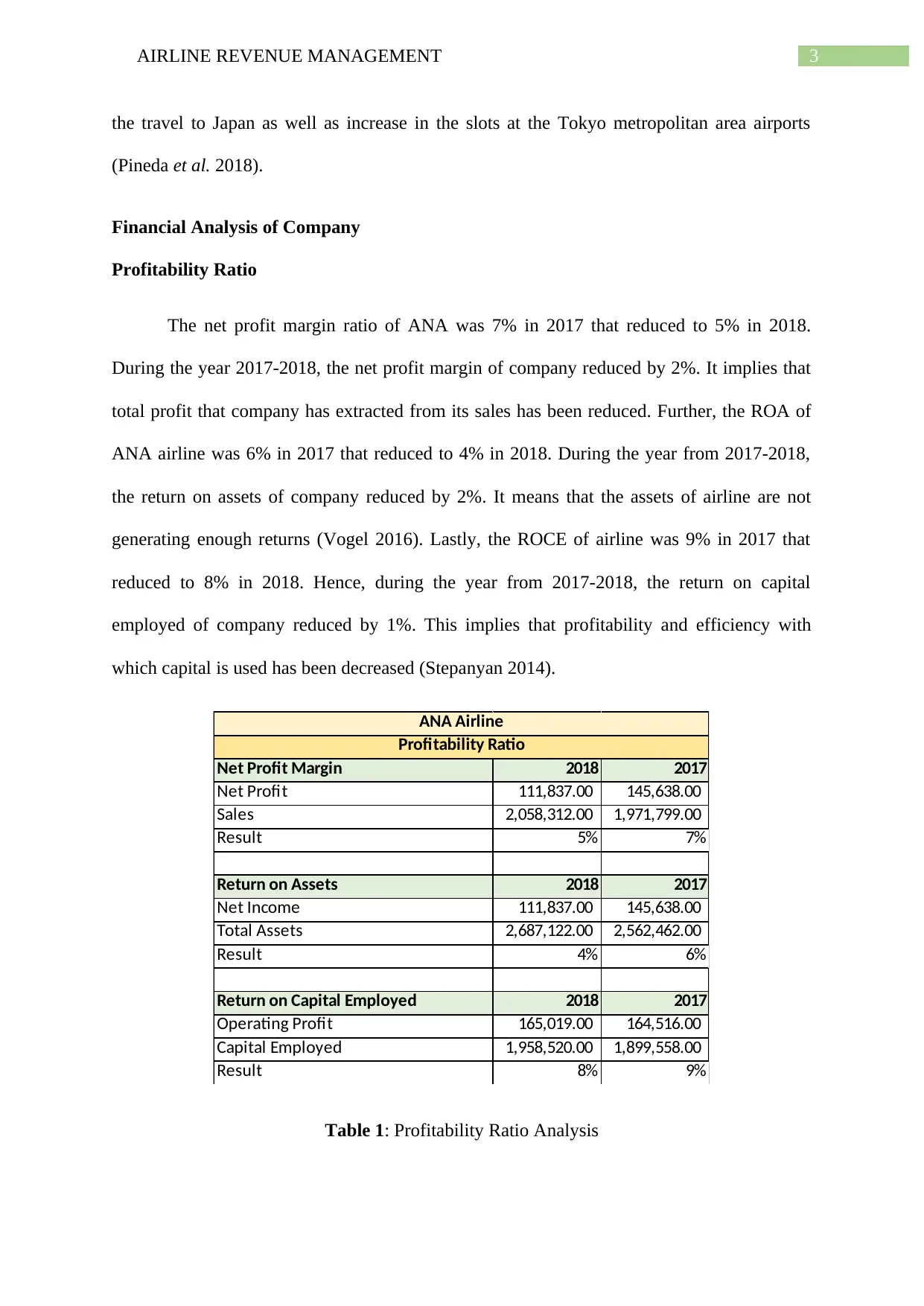

Financial Analysis of Company

Profitability Ratio

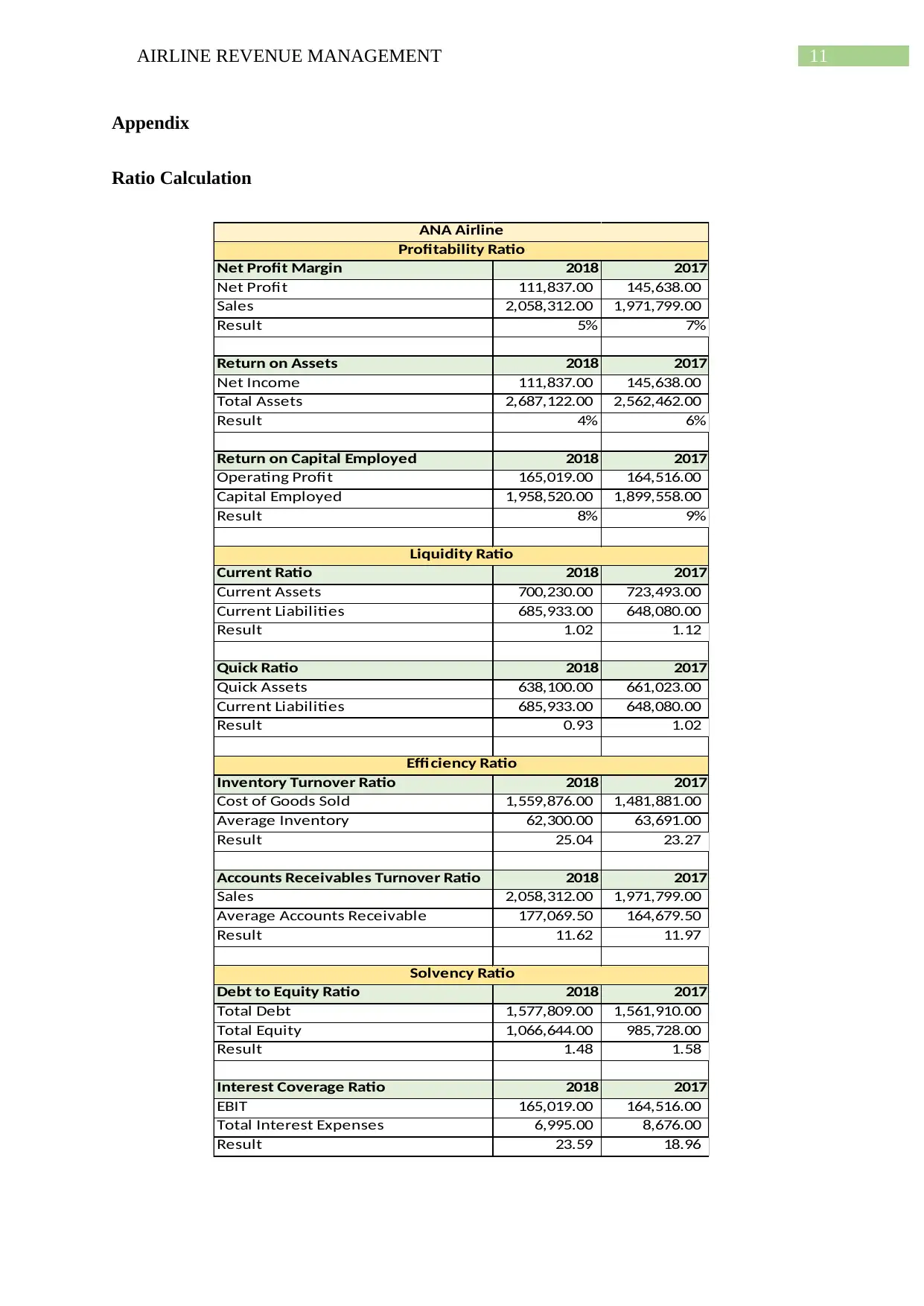

The net profit margin ratio of ANA was 7% in 2017 that reduced to 5% in 2018.

During the year 2017-2018, the net profit margin of company reduced by 2%. It implies that

total profit that company has extracted from its sales has been reduced. Further, the ROA of

ANA airline was 6% in 2017 that reduced to 4% in 2018. During the year from 2017-2018,

the return on assets of company reduced by 2%. It means that the assets of airline are not

generating enough returns (Vogel 2016). Lastly, the ROCE of airline was 9% in 2017 that

reduced to 8% in 2018. Hence, during the year from 2017-2018, the return on capital

employed of company reduced by 1%. This implies that profitability and efficiency with

which capital is used has been decreased (Stepanyan 2014).

Net Profit Margin 2018 2017

Net Profit 111,837.00 145,638.00

Sales 2,058,312.00 1,971,799.00

Result 5% 7%

Return on Assets 2018 2017

Net Income 111,837.00 145,638.00

Total Assets 2,687,122.00 2,562,462.00

Result 4% 6%

Return on Capital Employed 2018 2017

Operating Profit 165,019.00 164,516.00

Capital Employed 1,958,520.00 1,899,558.00

Result 8% 9%

Profitability Ratio

ANA Airline

Table 1: Profitability Ratio Analysis

the travel to Japan as well as increase in the slots at the Tokyo metropolitan area airports

(Pineda et al. 2018).

Financial Analysis of Company

Profitability Ratio

The net profit margin ratio of ANA was 7% in 2017 that reduced to 5% in 2018.

During the year 2017-2018, the net profit margin of company reduced by 2%. It implies that

total profit that company has extracted from its sales has been reduced. Further, the ROA of

ANA airline was 6% in 2017 that reduced to 4% in 2018. During the year from 2017-2018,

the return on assets of company reduced by 2%. It means that the assets of airline are not

generating enough returns (Vogel 2016). Lastly, the ROCE of airline was 9% in 2017 that

reduced to 8% in 2018. Hence, during the year from 2017-2018, the return on capital

employed of company reduced by 1%. This implies that profitability and efficiency with

which capital is used has been decreased (Stepanyan 2014).

Net Profit Margin 2018 2017

Net Profit 111,837.00 145,638.00

Sales 2,058,312.00 1,971,799.00

Result 5% 7%

Return on Assets 2018 2017

Net Income 111,837.00 145,638.00

Total Assets 2,687,122.00 2,562,462.00

Result 4% 6%

Return on Capital Employed 2018 2017

Operating Profit 165,019.00 164,516.00

Capital Employed 1,958,520.00 1,899,558.00

Result 8% 9%

Profitability Ratio

ANA Airline

Table 1: Profitability Ratio Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AIRLINE REVENUE MANAGEMENT

Liquidity Ratio

The current ratio of ANA was 1.12 in 2017 that reduced to 1.02 in 2018. During the

year from 2017-2018, the ratio has been declined by 0.1. This implies that the ability of ANA

in paying its short-term obligations has been decreased over the years. Further, the quick ratio

of company was 1.02 in 2017 that reduced by 0.93 in 2018. During the year from 2017-2018,

the ratio reduced by 0.09. This means that company’s ability for paying its current obligations

with its most liquid assets has been reduced (Öztürk and Serçemeli 2016).

Current Ratio 2018 2017

Current Assets 700,230.00 723,493.00

Current Liabilities 685,933.00 648,080.00

Result 1.02 1.12

Quick Ratio 2018 2017

Quick Assets 638,100.00 661,023.00

Current Liabilities 685,933.00 648,080.00

Result 0.93 1.02

Liquidity Ratio

Table 2: Liquidity Ratio Analysis

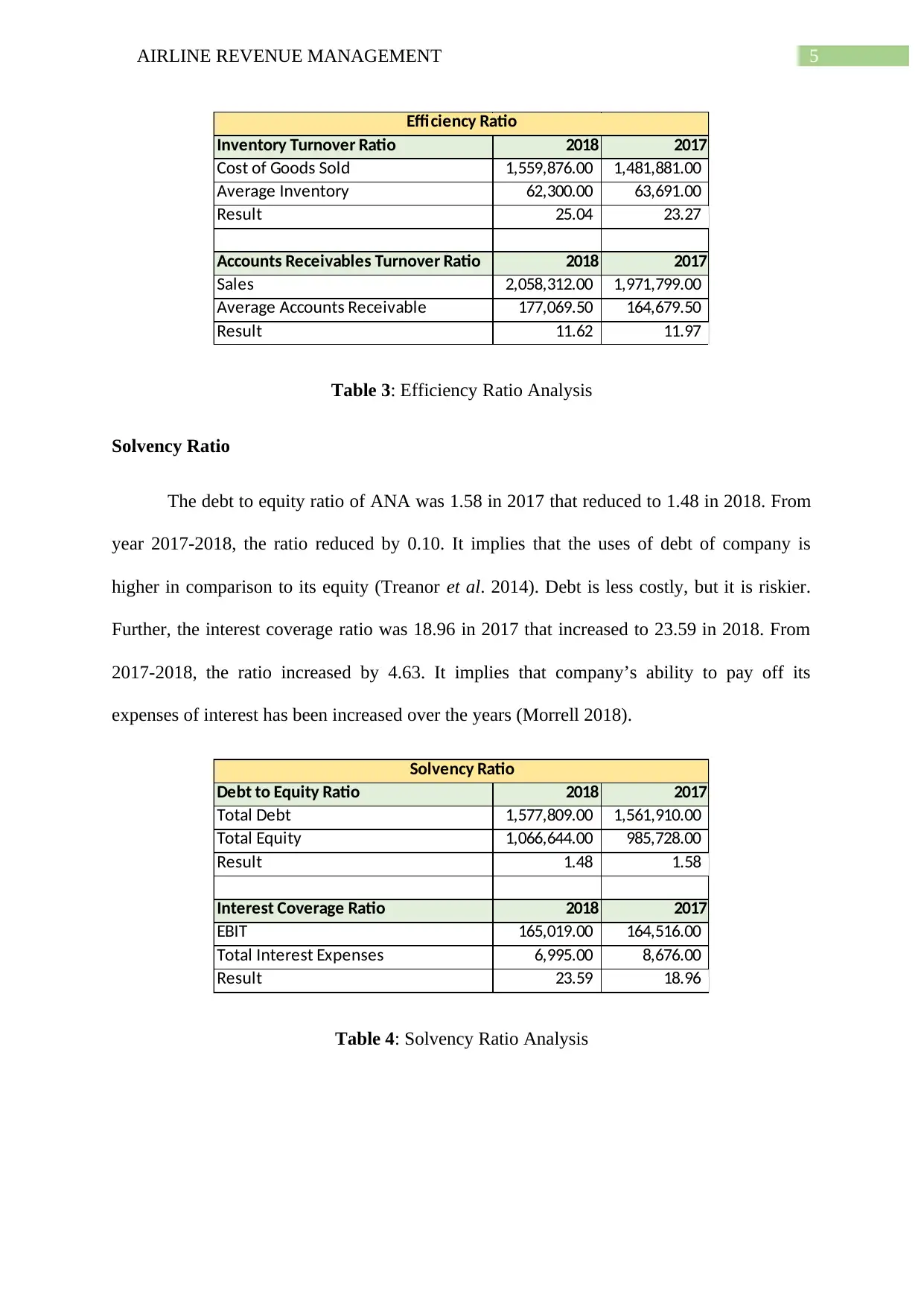

Efficiency Ratio

The inventory turnover ratio of ANA was 23.27 in 2017 that increased to 25.04.

During 2017-2018, the ratio increased by 1.77. It implies that number of times the inventories

consumption during the given period has been increased. The average receivables turnover

ratio of ANA was 11.97 in 2017 that reduced to 11.62 in 2018. From 2017-2018, the ratio

reduced by 0.35. It implies that the efficiency of company in extending credit and collecting

the debts has been reduced (Min and Joo 2016).

Liquidity Ratio

The current ratio of ANA was 1.12 in 2017 that reduced to 1.02 in 2018. During the

year from 2017-2018, the ratio has been declined by 0.1. This implies that the ability of ANA

in paying its short-term obligations has been decreased over the years. Further, the quick ratio

of company was 1.02 in 2017 that reduced by 0.93 in 2018. During the year from 2017-2018,

the ratio reduced by 0.09. This means that company’s ability for paying its current obligations

with its most liquid assets has been reduced (Öztürk and Serçemeli 2016).

Current Ratio 2018 2017

Current Assets 700,230.00 723,493.00

Current Liabilities 685,933.00 648,080.00

Result 1.02 1.12

Quick Ratio 2018 2017

Quick Assets 638,100.00 661,023.00

Current Liabilities 685,933.00 648,080.00

Result 0.93 1.02

Liquidity Ratio

Table 2: Liquidity Ratio Analysis

Efficiency Ratio

The inventory turnover ratio of ANA was 23.27 in 2017 that increased to 25.04.

During 2017-2018, the ratio increased by 1.77. It implies that number of times the inventories

consumption during the given period has been increased. The average receivables turnover

ratio of ANA was 11.97 in 2017 that reduced to 11.62 in 2018. From 2017-2018, the ratio

reduced by 0.35. It implies that the efficiency of company in extending credit and collecting

the debts has been reduced (Min and Joo 2016).

5AIRLINE REVENUE MANAGEMENT

Inventory Turnover Ratio 2018 2017

Cost of Goods Sold 1,559,876.00 1,481,881.00

Average Inventory 62,300.00 63,691.00

Result 25.04 23.27

Accounts Receivables Turnover Ratio 2018 2017

Sales 2,058,312.00 1,971,799.00

Average Accounts Receivable 177,069.50 164,679.50

Result 11.62 11.97

Efficiency Ratio

Table 3: Efficiency Ratio Analysis

Solvency Ratio

The debt to equity ratio of ANA was 1.58 in 2017 that reduced to 1.48 in 2018. From

year 2017-2018, the ratio reduced by 0.10. It implies that the uses of debt of company is

higher in comparison to its equity (Treanor et al. 2014). Debt is less costly, but it is riskier.

Further, the interest coverage ratio was 18.96 in 2017 that increased to 23.59 in 2018. From

2017-2018, the ratio increased by 4.63. It implies that company’s ability to pay off its

expenses of interest has been increased over the years (Morrell 2018).

Debt to Equity Ratio 2018 2017

Total Debt 1,577,809.00 1,561,910.00

Total Equity 1,066,644.00 985,728.00

Result 1.48 1.58

Interest Coverage Ratio 2018 2017

EBIT 165,019.00 164,516.00

Total Interest Expenses 6,995.00 8,676.00

Result 23.59 18.96

Solvency Ratio

Table 4: Solvency Ratio Analysis

Inventory Turnover Ratio 2018 2017

Cost of Goods Sold 1,559,876.00 1,481,881.00

Average Inventory 62,300.00 63,691.00

Result 25.04 23.27

Accounts Receivables Turnover Ratio 2018 2017

Sales 2,058,312.00 1,971,799.00

Average Accounts Receivable 177,069.50 164,679.50

Result 11.62 11.97

Efficiency Ratio

Table 3: Efficiency Ratio Analysis

Solvency Ratio

The debt to equity ratio of ANA was 1.58 in 2017 that reduced to 1.48 in 2018. From

year 2017-2018, the ratio reduced by 0.10. It implies that the uses of debt of company is

higher in comparison to its equity (Treanor et al. 2014). Debt is less costly, but it is riskier.

Further, the interest coverage ratio was 18.96 in 2017 that increased to 23.59 in 2018. From

2017-2018, the ratio increased by 4.63. It implies that company’s ability to pay off its

expenses of interest has been increased over the years (Morrell 2018).

Debt to Equity Ratio 2018 2017

Total Debt 1,577,809.00 1,561,910.00

Total Equity 1,066,644.00 985,728.00

Result 1.48 1.58

Interest Coverage Ratio 2018 2017

EBIT 165,019.00 164,516.00

Total Interest Expenses 6,995.00 8,676.00

Result 23.59 18.96

Solvency Ratio

Table 4: Solvency Ratio Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AIRLINE REVENUE MANAGEMENT

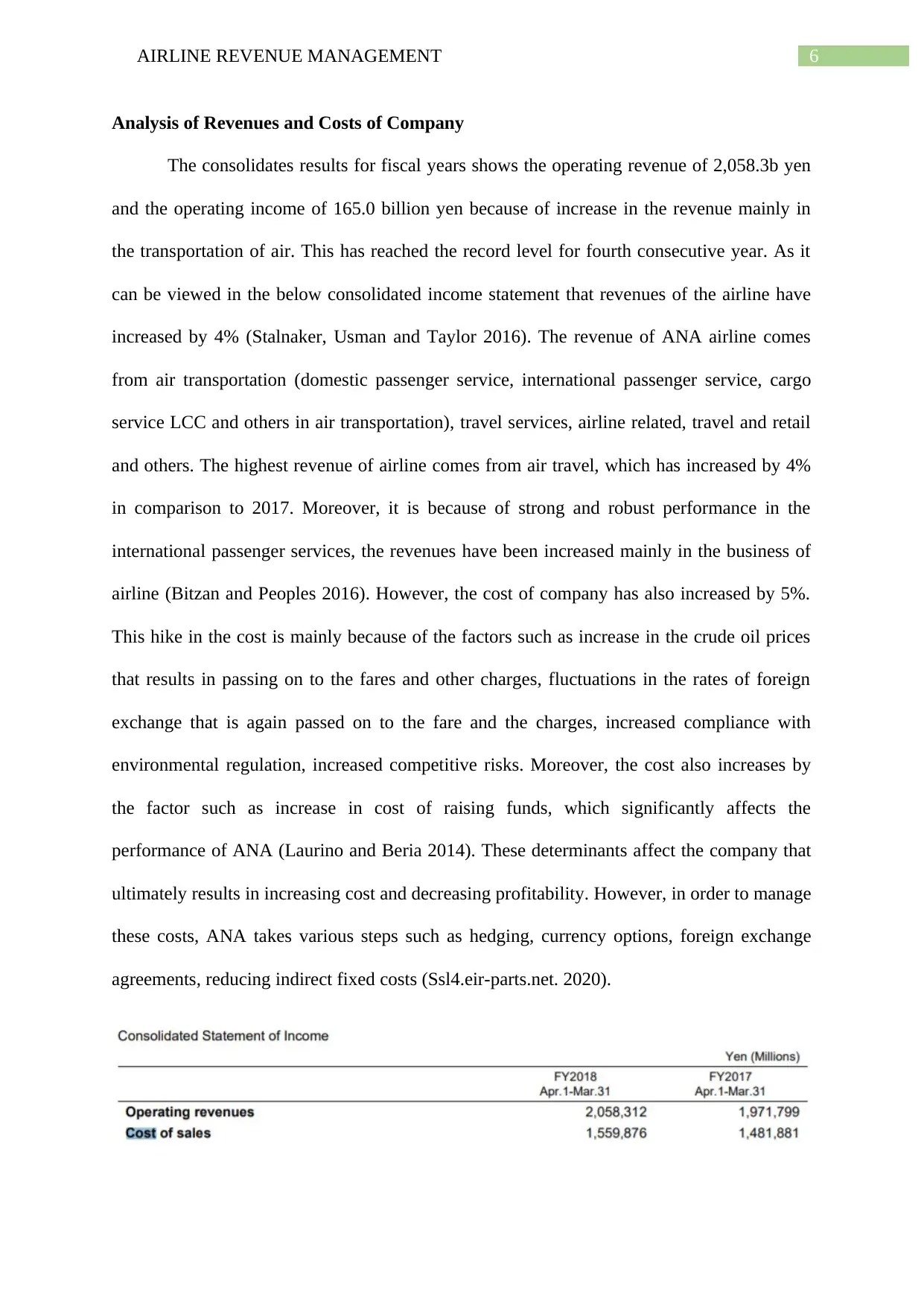

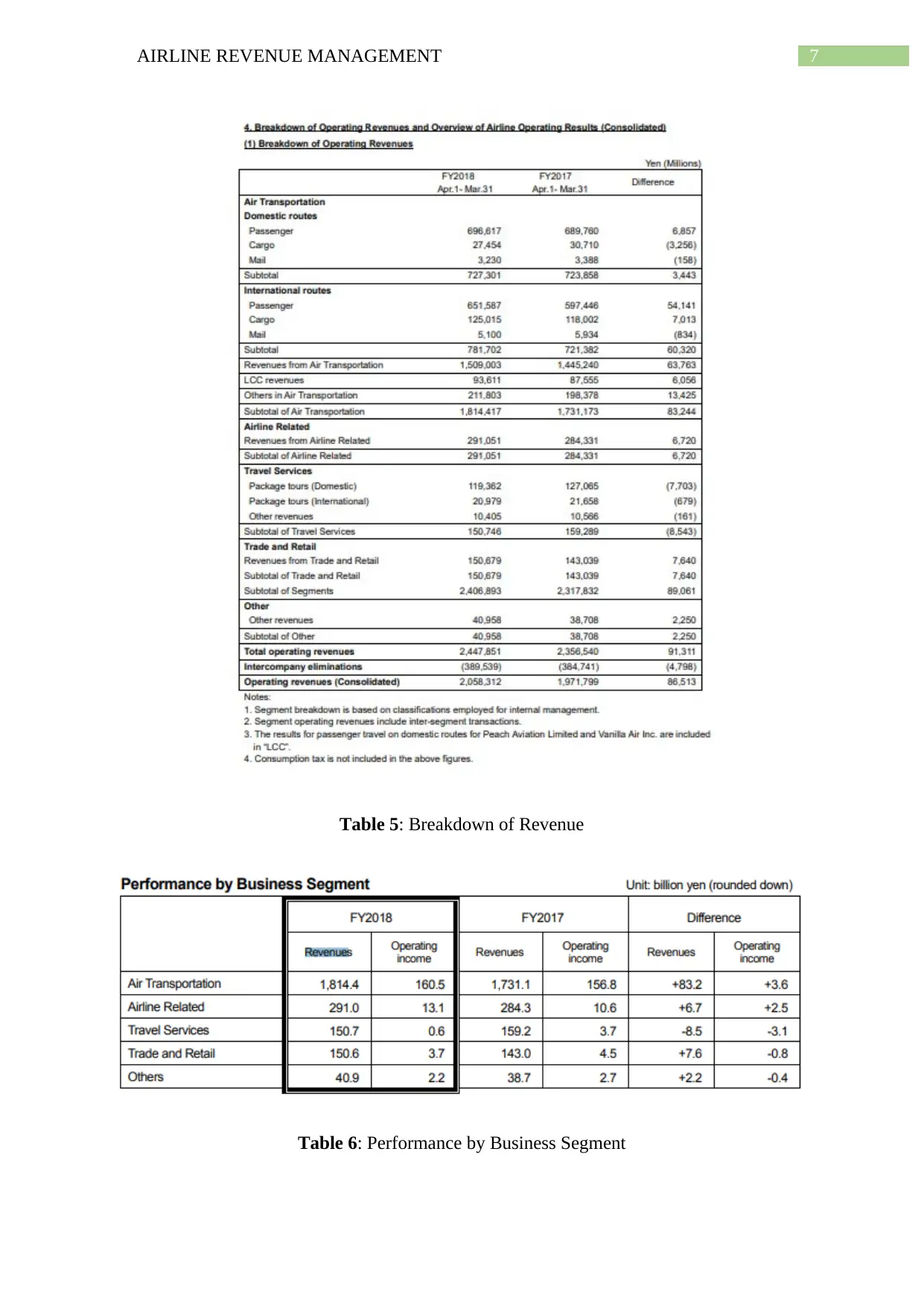

Analysis of Revenues and Costs of Company

The consolidates results for fiscal years shows the operating revenue of 2,058.3b yen

and the operating income of 165.0 billion yen because of increase in the revenue mainly in

the transportation of air. This has reached the record level for fourth consecutive year. As it

can be viewed in the below consolidated income statement that revenues of the airline have

increased by 4% (Stalnaker, Usman and Taylor 2016). The revenue of ANA airline comes

from air transportation (domestic passenger service, international passenger service, cargo

service LCC and others in air transportation), travel services, airline related, travel and retail

and others. The highest revenue of airline comes from air travel, which has increased by 4%

in comparison to 2017. Moreover, it is because of strong and robust performance in the

international passenger services, the revenues have been increased mainly in the business of

airline (Bitzan and Peoples 2016). However, the cost of company has also increased by 5%.

This hike in the cost is mainly because of the factors such as increase in the crude oil prices

that results in passing on to the fares and other charges, fluctuations in the rates of foreign

exchange that is again passed on to the fare and the charges, increased compliance with

environmental regulation, increased competitive risks. Moreover, the cost also increases by

the factor such as increase in cost of raising funds, which significantly affects the

performance of ANA (Laurino and Beria 2014). These determinants affect the company that

ultimately results in increasing cost and decreasing profitability. However, in order to manage

these costs, ANA takes various steps such as hedging, currency options, foreign exchange

agreements, reducing indirect fixed costs (Ssl4.eir-parts.net. 2020).

Analysis of Revenues and Costs of Company

The consolidates results for fiscal years shows the operating revenue of 2,058.3b yen

and the operating income of 165.0 billion yen because of increase in the revenue mainly in

the transportation of air. This has reached the record level for fourth consecutive year. As it

can be viewed in the below consolidated income statement that revenues of the airline have

increased by 4% (Stalnaker, Usman and Taylor 2016). The revenue of ANA airline comes

from air transportation (domestic passenger service, international passenger service, cargo

service LCC and others in air transportation), travel services, airline related, travel and retail

and others. The highest revenue of airline comes from air travel, which has increased by 4%

in comparison to 2017. Moreover, it is because of strong and robust performance in the

international passenger services, the revenues have been increased mainly in the business of

airline (Bitzan and Peoples 2016). However, the cost of company has also increased by 5%.

This hike in the cost is mainly because of the factors such as increase in the crude oil prices

that results in passing on to the fares and other charges, fluctuations in the rates of foreign

exchange that is again passed on to the fare and the charges, increased compliance with

environmental regulation, increased competitive risks. Moreover, the cost also increases by

the factor such as increase in cost of raising funds, which significantly affects the

performance of ANA (Laurino and Beria 2014). These determinants affect the company that

ultimately results in increasing cost and decreasing profitability. However, in order to manage

these costs, ANA takes various steps such as hedging, currency options, foreign exchange

agreements, reducing indirect fixed costs (Ssl4.eir-parts.net. 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AIRLINE REVENUE MANAGEMENT

Table 5: Breakdown of Revenue

Table 6: Performance by Business Segment

Table 5: Breakdown of Revenue

Table 6: Performance by Business Segment

8AIRLINE REVENUE MANAGEMENT

Conclusion

Therefore, this report concludes that ANA Group is one of the largest airline company

of Japan in terms of revenue and market capitalization. It has been analyzed that the

profitability of ANA has been reduced over the years. This reduction of profitability is

because of increase in cost of goods sold, increased expenses, assets not able to generate

higher income and more uses of debt. Further, the liquidity position of ANA has been

reduced but still ANA is able to pay-off its short-term liabilities. Moreover, ANA efficiency

in extending of credit and collecting the debt from the debtors has been reduced. The

solvency position of ANA indicates that company is able to cover its interest from its income,

however, the uses of debt by the airline is higher in comparison to the equity. As debt is

considered to be less costly, but it is riskier. Lastly, it has been analyzed from the revenue

cost management of ANA that the revenue of airline has been increased, especially in air

transportation, however, its cost has been drastically increased that have affected its

profitability. Hence, it is suggested to the ANA Group to reduce the cost of operations. It will

increase the profitability and justify the highest revenue of the company. Further, ANA

should reduce the uses of debt, as it is riskier than equity.

Conclusion

Therefore, this report concludes that ANA Group is one of the largest airline company

of Japan in terms of revenue and market capitalization. It has been analyzed that the

profitability of ANA has been reduced over the years. This reduction of profitability is

because of increase in cost of goods sold, increased expenses, assets not able to generate

higher income and more uses of debt. Further, the liquidity position of ANA has been

reduced but still ANA is able to pay-off its short-term liabilities. Moreover, ANA efficiency

in extending of credit and collecting the debt from the debtors has been reduced. The

solvency position of ANA indicates that company is able to cover its interest from its income,

however, the uses of debt by the airline is higher in comparison to the equity. As debt is

considered to be less costly, but it is riskier. Lastly, it has been analyzed from the revenue

cost management of ANA that the revenue of airline has been increased, especially in air

transportation, however, its cost has been drastically increased that have affected its

profitability. Hence, it is suggested to the ANA Group to reduce the cost of operations. It will

increase the profitability and justify the highest revenue of the company. Further, ANA

should reduce the uses of debt, as it is riskier than equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AIRLINE REVENUE MANAGEMENT

Reference

Bitzan, J. and Peoples, J., 2016. A comparative analysis of cost change for low-cost, full-

service, and other carriers in the US airline industry. Research in Transportation

Economics, 56, pp.25-41.

Laurino, A. and Beria, P., 2014. Low-cost carriers and secondary airports: Three experiences

from Italy. Journal of Destination Marketing & Management, 3(3), pp.180-191.

Min, H. and Joo, S.J., 2016. A comparative performance analysis of airline strategic alliances

using data envelopment analysis. Journal of Air Transport Management, 52, pp.99-110.

Morrell, P.S., 2018. Airline finance. Routledge.

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on

Statement of Financial Position and Key Ratios: A Case Study on an Airline Company in

Turkey. Business and Economics Research Journal, 7(4), p.143.

Pineda, P.J.G., Liou, J.J., Hsu, C.C. and Chuang, Y.C., 2018. An integrated MCDM model

for improving airline operational and financial performance. Journal of Air Transport

Management, 68, pp.103-117.

Schosser, M. and Wittmer, A., 2015. Cost and revenue synergies in airline mergers–

Examining geographical differences. Journal of Air Transport Management, 47, pp.142-153.

Ssl4.eir-parts.net. 2020. [online] Available at:

https://ssl4.eir-parts.net/doc/9202/tdnet/1696202/00.pdf [Accessed 29 Feb. 2020].

Stalnaker, T., Usman, K. and Taylor, A., 2016. Airline economic analysis. Oliver Wyman,

pp.1-68.

Reference

Bitzan, J. and Peoples, J., 2016. A comparative analysis of cost change for low-cost, full-

service, and other carriers in the US airline industry. Research in Transportation

Economics, 56, pp.25-41.

Laurino, A. and Beria, P., 2014. Low-cost carriers and secondary airports: Three experiences

from Italy. Journal of Destination Marketing & Management, 3(3), pp.180-191.

Min, H. and Joo, S.J., 2016. A comparative performance analysis of airline strategic alliances

using data envelopment analysis. Journal of Air Transport Management, 52, pp.99-110.

Morrell, P.S., 2018. Airline finance. Routledge.

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on

Statement of Financial Position and Key Ratios: A Case Study on an Airline Company in

Turkey. Business and Economics Research Journal, 7(4), p.143.

Pineda, P.J.G., Liou, J.J., Hsu, C.C. and Chuang, Y.C., 2018. An integrated MCDM model

for improving airline operational and financial performance. Journal of Air Transport

Management, 68, pp.103-117.

Schosser, M. and Wittmer, A., 2015. Cost and revenue synergies in airline mergers–

Examining geographical differences. Journal of Air Transport Management, 47, pp.142-153.

Ssl4.eir-parts.net. 2020. [online] Available at:

https://ssl4.eir-parts.net/doc/9202/tdnet/1696202/00.pdf [Accessed 29 Feb. 2020].

Stalnaker, T., Usman, K. and Taylor, A., 2016. Airline economic analysis. Oliver Wyman,

pp.1-68.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AIRLINE REVENUE MANAGEMENT

Stepanyan, A., 2014. Traditional ratio analysis in the airline business: a case study of leading

US Carriers. AMIS 2014, p.841.

Treanor, S.D., Rogers, D.A., Carter, D.A. and Simkins, B.J., 2014. Exposure, hedging, and

value: New evidence from the US airline industry. International Review of Financial

Analysis, 34, pp.200-211.

Vogel, H.L., 2016. Travel industry economics: A guide for financial analysis. Springer.

Stepanyan, A., 2014. Traditional ratio analysis in the airline business: a case study of leading

US Carriers. AMIS 2014, p.841.

Treanor, S.D., Rogers, D.A., Carter, D.A. and Simkins, B.J., 2014. Exposure, hedging, and

value: New evidence from the US airline industry. International Review of Financial

Analysis, 34, pp.200-211.

Vogel, H.L., 2016. Travel industry economics: A guide for financial analysis. Springer.

11AIRLINE REVENUE MANAGEMENT

Appendix

Ratio Calculation

Net Profit Margin 2018 2017

Net Profit 111,837.00 145,638.00

Sales 2,058,312.00 1,971,799.00

Result 5% 7%

Return on Assets 2018 2017

Net Income 111,837.00 145,638.00

Total Assets 2,687,122.00 2,562,462.00

Result 4% 6%

Return on Capital Employed 2018 2017

Operating Profit 165,019.00 164,516.00

Capital Employed 1,958,520.00 1,899,558.00

Result 8% 9%

Current Ratio 2018 2017

Current Assets 700,230.00 723,493.00

Current Liabilities 685,933.00 648,080.00

Result 1.02 1.12

Quick Ratio 2018 2017

Quick Assets 638,100.00 661,023.00

Current Liabilities 685,933.00 648,080.00

Result 0.93 1.02

Inventory Turnover Ratio 2018 2017

Cost of Goods Sold 1,559,876.00 1,481,881.00

Average Inventory 62,300.00 63,691.00

Result 25.04 23.27

Accounts Receivables Turnover Ratio 2018 2017

Sales 2,058,312.00 1,971,799.00

Average Accounts Receivable 177,069.50 164,679.50

Result 11.62 11.97

Debt to Equity Ratio 2018 2017

Total Debt 1,577,809.00 1,561,910.00

Total Equity 1,066,644.00 985,728.00

Result 1.48 1.58

Interest Coverage Ratio 2018 2017

EBIT 165,019.00 164,516.00

Total Interest Expenses 6,995.00 8,676.00

Result 23.59 18.96

Efficiency Ratio

Liquidity Ratio

Profitability Ratio

Solvency Ratio

ANA Airline

Appendix

Ratio Calculation

Net Profit Margin 2018 2017

Net Profit 111,837.00 145,638.00

Sales 2,058,312.00 1,971,799.00

Result 5% 7%

Return on Assets 2018 2017

Net Income 111,837.00 145,638.00

Total Assets 2,687,122.00 2,562,462.00

Result 4% 6%

Return on Capital Employed 2018 2017

Operating Profit 165,019.00 164,516.00

Capital Employed 1,958,520.00 1,899,558.00

Result 8% 9%

Current Ratio 2018 2017

Current Assets 700,230.00 723,493.00

Current Liabilities 685,933.00 648,080.00

Result 1.02 1.12

Quick Ratio 2018 2017

Quick Assets 638,100.00 661,023.00

Current Liabilities 685,933.00 648,080.00

Result 0.93 1.02

Inventory Turnover Ratio 2018 2017

Cost of Goods Sold 1,559,876.00 1,481,881.00

Average Inventory 62,300.00 63,691.00

Result 25.04 23.27

Accounts Receivables Turnover Ratio 2018 2017

Sales 2,058,312.00 1,971,799.00

Average Accounts Receivable 177,069.50 164,679.50

Result 11.62 11.97

Debt to Equity Ratio 2018 2017

Total Debt 1,577,809.00 1,561,910.00

Total Equity 1,066,644.00 985,728.00

Result 1.48 1.58

Interest Coverage Ratio 2018 2017

EBIT 165,019.00 164,516.00

Total Interest Expenses 6,995.00 8,676.00

Result 23.59 18.96

Efficiency Ratio

Liquidity Ratio

Profitability Ratio

Solvency Ratio

ANA Airline

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.