Accounting Information System and Decision Making in Australia

VerifiedAdded on 2020/05/08

|13

|2450

|74

Report

AI Summary

This report examines the impact of Accounting Information Systems (AIS) on decision-making within the food and beverage industry in Australia. It explores the role of AIS in enhancing organizational performance, improving financial reporting, and facilitating effective internal controls. The research methodology includes a literature review, outlining the conceptual and empirical frameworks, and a survey of employees from food product companies. The study investigates the relationship between AIS implementation and decision-making effectiveness, testing the hypothesis that there is a significant association between the two. Data analysis techniques, including correlation and regression, are employed to analyze the survey responses and draw conclusions. The report also discusses the ethical considerations, contributions, and limitations of the research, providing insights into how AIS can be leveraged to improve decision-making processes, manage uncertainty, and enhance competitive advantages in the food and beverage sector. The research highlights the importance of AIS in supporting managers and improving the quality of financial information.

Running head: ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

Accounting Information System as an Aid to Decision Making In Food and

Beverages Companies in Australia

Name of the University:

Name of the Student:

Authors Note:

Accounting Information System as an Aid to Decision Making In Food and

Beverages Companies in Australia

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

Abstract

The research tends to explain that in managing a company along with implementing internal

control system, effect of accounting information system is important. The findings are also

deemed to reveal that with the growing years, increasing number of companies must consider

using effective information technology for improving and increasing their competitive

advantages in highly competitive industry. It will be gathered from completion of the research

that accounting information can facilitate the managers in understanding their work in a better

manner along with decreasing uncertainty in order to make effective decisions.

Abstract

The research tends to explain that in managing a company along with implementing internal

control system, effect of accounting information system is important. The findings are also

deemed to reveal that with the growing years, increasing number of companies must consider

using effective information technology for improving and increasing their competitive

advantages in highly competitive industry. It will be gathered from completion of the research

that accounting information can facilitate the managers in understanding their work in a better

manner along with decreasing uncertainty in order to make effective decisions.

2ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

Table of Contents

1. Introduction......................................................................................................................3

2. Literature Review............................................................................................................3

2.1. Impact of AIS on Organizational Decision Making.................................................3

2.2. Conceptual Framework.............................................................................................3

2.3. Value Relevance.......................................................................................................4

2.4. Empirical Framework...............................................................................................4

3. Research Objectives and Hypothesis...............................................................................5

4. Research Method.............................................................................................................5

4.1. Scope of Research.....................................................................................................5

4.2. Sampling Frame........................................................................................................6

4.3. Research Technique..................................................................................................6

4.4. Data Analysis Technique..........................................................................................7

4.5. Ethical Consideration................................................................................................7

5. Contributions and Limitations.........................................................................................8

References............................................................................................................................9

Appendix............................................................................................................................11

Table of Contents

1. Introduction......................................................................................................................3

2. Literature Review............................................................................................................3

2.1. Impact of AIS on Organizational Decision Making.................................................3

2.2. Conceptual Framework.............................................................................................3

2.3. Value Relevance.......................................................................................................4

2.4. Empirical Framework...............................................................................................4

3. Research Objectives and Hypothesis...............................................................................5

4. Research Method.............................................................................................................5

4.1. Scope of Research.....................................................................................................5

4.2. Sampling Frame........................................................................................................6

4.3. Research Technique..................................................................................................6

4.4. Data Analysis Technique..........................................................................................7

4.5. Ethical Consideration................................................................................................7

5. Contributions and Limitations.........................................................................................8

References............................................................................................................................9

Appendix............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

1. Introduction

In the current era, certain developments in the information systems all through the world

have necessitated the companies to invest resources in this part if they decide to compete

successfully in the local and international market. In the recent years, accounting systems are

likely to act as an information system that does not get affected by data or financial information

limits (Alamin, Matthew and Scott 2015). Moreover, the modified accounting informant system

encompasses quantitative and descriptive information that supports decision making of the users.

Users of data gathered from accounting information system are consumers, suppliers, investors

and government in order to develop a goal based in the gathered accounting information.

2. Literature Review

2.1. Impact of AIS on Organizational Decision Making

Caria and Lídia (2016) Indicated that AIS serves as an effective decision making tool in

order to control and coordinate all the activities of a company. It is also gathered that AIS is

highly important to production of quality accounting information on a timely manner along with

communication of the same information to the decision makers. AIS is most vital system for a

company as accounting information has an important role in realizing the financial position of

the company. Collier (2015) argued that integrating accounting information systems results in

organizational coordination that further enhances the quality of information.

2.2. Conceptual Framework

Dutta, Raef and David (2015) explained that the conceptual framework is segmented in

two parts. The first part analyses the usefulness and concept of accounting information systems

1. Introduction

In the current era, certain developments in the information systems all through the world

have necessitated the companies to invest resources in this part if they decide to compete

successfully in the local and international market. In the recent years, accounting systems are

likely to act as an information system that does not get affected by data or financial information

limits (Alamin, Matthew and Scott 2015). Moreover, the modified accounting informant system

encompasses quantitative and descriptive information that supports decision making of the users.

Users of data gathered from accounting information system are consumers, suppliers, investors

and government in order to develop a goal based in the gathered accounting information.

2. Literature Review

2.1. Impact of AIS on Organizational Decision Making

Caria and Lídia (2016) Indicated that AIS serves as an effective decision making tool in

order to control and coordinate all the activities of a company. It is also gathered that AIS is

highly important to production of quality accounting information on a timely manner along with

communication of the same information to the decision makers. AIS is most vital system for a

company as accounting information has an important role in realizing the financial position of

the company. Collier (2015) argued that integrating accounting information systems results in

organizational coordination that further enhances the quality of information.

2.2. Conceptual Framework

Dutta, Raef and David (2015) explained that the conceptual framework is segmented in

two parts. The first part analyses the usefulness and concept of accounting information systems

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

within companies and the second part analyses the relevance value of accounting information in

supporting investors to take investment decisions. Galliers, Robert and Dorothy (2014) revealed

that efficiency of accounting information systems are relied on the perception of decision makers

regarding information usefulness that is generated from system for satisfying operations

processes information needs. Consequently, it can be said that accounting information system’s

effectiveness not only relies on the systems purpose but also relies on contingency factors of

every organization. Accounting systems are vital aspects of the organizational life and these are

required to be analyzed in broader organizational, managerial and environmental context.

2.3. Value Relevance

Ijiri (2014) explained that value relevance is the capability of financial statement

information for gathering and summering organizational value. This is also observed to

investigate the link between a security price dependent variable and independent accounting

variables set. The definitions presented by several researchers on value relevance explain a

common thing that an accounting amount is observed to be value relevant if it has considerable

link with security market value. Laudon, Kenneth and Jane (2014) stated that the information

aspect of value relevance is employed in this research to evaluate the accounting data value

relevance of selected organizations. Informational aspect measures the usefulness of accounting

for the individual users devoid of excessive focus on detailed structure of relation between firm

value and accounting data.

2.4. Empirical Framework

Previous literature provides detailed evidence of relationship among accounting

information system and its impact on financial performance of companies. Prasad and Peter

(2015) discovered positive association between accounting information system (AIS) design and

within companies and the second part analyses the relevance value of accounting information in

supporting investors to take investment decisions. Galliers, Robert and Dorothy (2014) revealed

that efficiency of accounting information systems are relied on the perception of decision makers

regarding information usefulness that is generated from system for satisfying operations

processes information needs. Consequently, it can be said that accounting information system’s

effectiveness not only relies on the systems purpose but also relies on contingency factors of

every organization. Accounting systems are vital aspects of the organizational life and these are

required to be analyzed in broader organizational, managerial and environmental context.

2.3. Value Relevance

Ijiri (2014) explained that value relevance is the capability of financial statement

information for gathering and summering organizational value. This is also observed to

investigate the link between a security price dependent variable and independent accounting

variables set. The definitions presented by several researchers on value relevance explain a

common thing that an accounting amount is observed to be value relevant if it has considerable

link with security market value. Laudon, Kenneth and Jane (2014) stated that the information

aspect of value relevance is employed in this research to evaluate the accounting data value

relevance of selected organizations. Informational aspect measures the usefulness of accounting

for the individual users devoid of excessive focus on detailed structure of relation between firm

value and accounting data.

2.4. Empirical Framework

Previous literature provides detailed evidence of relationship among accounting

information system and its impact on financial performance of companies. Prasad and Peter

(2015) discovered positive association between accounting information system (AIS) design and

5ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

organizational strategy with performance. For such treasons, successful implementation of AIS

can save money and time of shareholders. Information usefulness can be understood as the extent

to which information supports decision making. This includes the following:

Subject’s demand for product

The extent to which the product impacts the subject’s forecast

The extent to which the product results in effective forecasting

The extent to which a product impacts the subject’s decisions, and

The extent to which the product leads in effective decision making

3. Research Objectives and Hypothesis

The objective of the paper will be to analyze the ways in which accounting information

systems serves as an aid in decision making of food and beverages companies in Australia. The

hypotheses those are set and are to be tested through the current research are mentioned below:

H0: There is no significant association between effective decision making and use of

accounting information system

H1: There is a significant association between effective decision making and use of

accounting information system

4. Research Method

4.1. Scope of Research

The research tends to explain that in managing a company along with implementing

internal control system, effect of accounting information system is important (Schaltegger, Roger

and Joanne 2015). Advantages of accounting information system might be accessed through its

organizational strategy with performance. For such treasons, successful implementation of AIS

can save money and time of shareholders. Information usefulness can be understood as the extent

to which information supports decision making. This includes the following:

Subject’s demand for product

The extent to which the product impacts the subject’s forecast

The extent to which the product results in effective forecasting

The extent to which a product impacts the subject’s decisions, and

The extent to which the product leads in effective decision making

3. Research Objectives and Hypothesis

The objective of the paper will be to analyze the ways in which accounting information

systems serves as an aid in decision making of food and beverages companies in Australia. The

hypotheses those are set and are to be tested through the current research are mentioned below:

H0: There is no significant association between effective decision making and use of

accounting information system

H1: There is a significant association between effective decision making and use of

accounting information system

4. Research Method

4.1. Scope of Research

The research tends to explain that in managing a company along with implementing

internal control system, effect of accounting information system is important (Schaltegger, Roger

and Joanne 2015). Advantages of accounting information system might be accessed through its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

effects on enhancing the decision making process, accounting information quality, performance

analysis along with facilitating organizational transactions. Moreover, the research intends to

explain the ways in which appropriate implementation of accounting information can facilitate

managers to understand tasks properly and decrease uncertainty before making certain decisions

(Simkin and Jacob 2014).

4.2. Sampling Frame

The sampling technique that is used in the current research is simple random sampling.

This sampling technique is used for the reason that this serves as most effective way in gathering

a representative sample from the population. It is also gathered that random sampling is a

technique through which all the members from the population can have an equal opportunity to

get selected from the sample (Simkin and Jacob 2014). This sampling method is also deemed to

be highly relevant for the reason that in this process selection of a person for the sample does not

impact the chances of any individual being selected. Additionally, opinion of several investors,

portfolio managers, and stock brokers along with investment advisors within a stock exchange

might be sought.

The sample of the study includes several employees within the food products companies

in Australia. 100 major employees from selected seven food product companies are selected.

These employees are particularly peopling that use accounting information system in

accomplishing their job responsibilities.

4.3. Research Technique

In the current research, relevant data will be gathered from important primary sources.

The primary sources of important data are the questionnaires those are developed efficiently and

effects on enhancing the decision making process, accounting information quality, performance

analysis along with facilitating organizational transactions. Moreover, the research intends to

explain the ways in which appropriate implementation of accounting information can facilitate

managers to understand tasks properly and decrease uncertainty before making certain decisions

(Simkin and Jacob 2014).

4.2. Sampling Frame

The sampling technique that is used in the current research is simple random sampling.

This sampling technique is used for the reason that this serves as most effective way in gathering

a representative sample from the population. It is also gathered that random sampling is a

technique through which all the members from the population can have an equal opportunity to

get selected from the sample (Simkin and Jacob 2014). This sampling method is also deemed to

be highly relevant for the reason that in this process selection of a person for the sample does not

impact the chances of any individual being selected. Additionally, opinion of several investors,

portfolio managers, and stock brokers along with investment advisors within a stock exchange

might be sought.

The sample of the study includes several employees within the food products companies

in Australia. 100 major employees from selected seven food product companies are selected.

These employees are particularly peopling that use accounting information system in

accomplishing their job responsibilities.

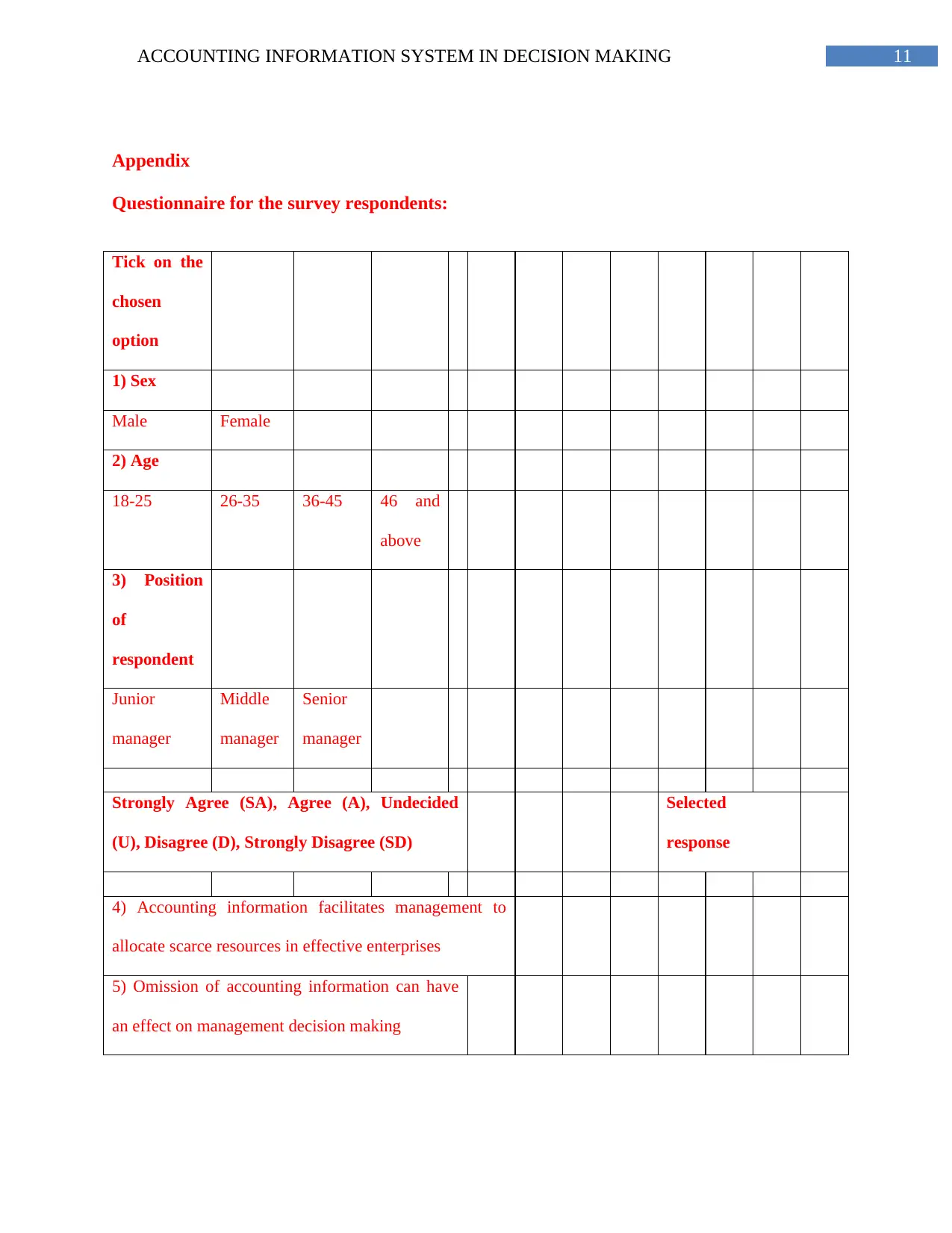

4.3. Research Technique

In the current research, relevant data will be gathered from important primary sources.

The primary sources of important data are the questionnaires those are developed efficiently and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

provided to the target respondents of 100 employees from selected organizations. The questions

within the questionnaire will be both open and close ended that makes sure responses from the

survey is gathered from using five point likert scale questions. The developed questionnaire

includes twenty questions that are designed carefully in gathering important data. The research

instrument was put under pilot study by expert planner that encompasses important members of

the company (Xu 2015). From the survey, 45 questionnaires returned successfully with complete

answers and the rest 5 questionnaires arrived with inadequate information. Therefore, total 45

questionnaires were available for analysis of data.

4.4. Data Analysis Technique

For the reason that the sampling technique that was considered suitable for this research

is probability sampling method, correlation and regression data analysis technique is adopted.

These analyses were carried out in consideration to value of 0.05% significance along with 95%

level of confidence (Schaltegger, Roger and Joanne 2015). Hypothesis testing is conducted based

on the results of correlation and regression analysis of the gathered questionnaire responses.

Analysis of data was carried out through Karl Pearson’s product moment correlation.

4.5. Ethical Consideration

While accomplishing the current research, several ethical considerations was taken into

account by the researcher in order to ensure reliability of the study. At the time of completing the

research, the researcher has made sure that confidentiality of information related to survey

participants was mentioned (Dutta, Raef and David 2015). Moreover, willful consent of the

participants was gathered at the time of developing survey questionnaire. Additionally, the

researcher has also focused on the fact that the entire research is a sole work of the researcher.

provided to the target respondents of 100 employees from selected organizations. The questions

within the questionnaire will be both open and close ended that makes sure responses from the

survey is gathered from using five point likert scale questions. The developed questionnaire

includes twenty questions that are designed carefully in gathering important data. The research

instrument was put under pilot study by expert planner that encompasses important members of

the company (Xu 2015). From the survey, 45 questionnaires returned successfully with complete

answers and the rest 5 questionnaires arrived with inadequate information. Therefore, total 45

questionnaires were available for analysis of data.

4.4. Data Analysis Technique

For the reason that the sampling technique that was considered suitable for this research

is probability sampling method, correlation and regression data analysis technique is adopted.

These analyses were carried out in consideration to value of 0.05% significance along with 95%

level of confidence (Schaltegger, Roger and Joanne 2015). Hypothesis testing is conducted based

on the results of correlation and regression analysis of the gathered questionnaire responses.

Analysis of data was carried out through Karl Pearson’s product moment correlation.

4.5. Ethical Consideration

While accomplishing the current research, several ethical considerations was taken into

account by the researcher in order to ensure reliability of the study. At the time of completing the

research, the researcher has made sure that confidentiality of information related to survey

participants was mentioned (Dutta, Raef and David 2015). Moreover, willful consent of the

participants was gathered at the time of developing survey questionnaire. Additionally, the

researcher has also focused on the fact that the entire research is a sole work of the researcher.

8ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

5. Contributions and Limitations

Completion of the current research tends to offer researchers with certain supportive

evidences for successful implementation of accounting information system. The findings of this

current research well explain the efficiency of accounting information systems in better decision

making in distinct angle such as effective decision making by managers and efficient internal

control systems. Moreover, it will also reveal the ways in which quality of financial report can be

maintained along with maintaining highly effective financial transaction prices (Simkin and

Jacob 2014). The findings are also deemed to reveal that with the growing years, increasing

number of companies must consider using effective information technology for improving and

increasing their competitive advantages in highly competitive industry. It will be gathered from

completion of the research that accounting information can facilitate the managers in

understanding their work in a better manner along with decreasing uncertainty in order to make

effective decisions.

However, despite of having several useful implications, there might be certain limitations

of the current research. Due to time constraints this research failed to conduct detailed evaluation

of accounting information system with corporation of AIS designed organizations. It also did not

focus on evaluating effectiveness of AIS as an aspect of MIS and could not explain impacts of

user participation while designing AIS (Simkin and Jacob 2014). All these limitations will be

addressed in the future research along with analyzing the extent to which aspects like inflation

and human resource accounting can be taken into consideration while developing an accounting

information system.

5. Contributions and Limitations

Completion of the current research tends to offer researchers with certain supportive

evidences for successful implementation of accounting information system. The findings of this

current research well explain the efficiency of accounting information systems in better decision

making in distinct angle such as effective decision making by managers and efficient internal

control systems. Moreover, it will also reveal the ways in which quality of financial report can be

maintained along with maintaining highly effective financial transaction prices (Simkin and

Jacob 2014). The findings are also deemed to reveal that with the growing years, increasing

number of companies must consider using effective information technology for improving and

increasing their competitive advantages in highly competitive industry. It will be gathered from

completion of the research that accounting information can facilitate the managers in

understanding their work in a better manner along with decreasing uncertainty in order to make

effective decisions.

However, despite of having several useful implications, there might be certain limitations

of the current research. Due to time constraints this research failed to conduct detailed evaluation

of accounting information system with corporation of AIS designed organizations. It also did not

focus on evaluating effectiveness of AIS as an aspect of MIS and could not explain impacts of

user participation while designing AIS (Simkin and Jacob 2014). All these limitations will be

addressed in the future research along with analyzing the extent to which aspects like inflation

and human resource accounting can be taken into consideration while developing an accounting

information system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

References

Alamin, Adel, William Yeoh, Matthew Warren, and Scott Salzman. "An empirical study of

factors influencing accounting information systems adoption." In Proceedings of the

Twenty-Third European Conference on Information Systems, pp. 1-11. ECIS, 2015.

Caria, Ana Alexandra, Anabela Martins Silva, Delfina Rosa Rocha Gomes, and Lídia Cristina

Alves Morais Oliveira. "Accounting as an Information System." In MBA, pp. 125-156.

Springer International Publishing, 2016.

Collier, Paul M. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons, 2015.

Dutta, Saurav K., Raef A. Lawson, and David Marcinko. "A Conceptual Foundation for

Management Accounting Information to Support Sustainability Strategies." 2015.

Galliers, Robert D., and Dorothy E. Leidner, eds. Strategic information management: challenges

and strategies in managing information systems. Routledge, 2014.

Ijiri, Yuji. "The beauty of double-entry bookkeeping and its impact on the nature of accounting

information." Economie Notes by Monte dei Paschi di Siena 22, no. 2-1993 (2014): 265-

285.

Laudon, Kenneth C., and Jane P. Laudon. Management information system. Pearson Education

India, 2016.

References

Alamin, Adel, William Yeoh, Matthew Warren, and Scott Salzman. "An empirical study of

factors influencing accounting information systems adoption." In Proceedings of the

Twenty-Third European Conference on Information Systems, pp. 1-11. ECIS, 2015.

Caria, Ana Alexandra, Anabela Martins Silva, Delfina Rosa Rocha Gomes, and Lídia Cristina

Alves Morais Oliveira. "Accounting as an Information System." In MBA, pp. 125-156.

Springer International Publishing, 2016.

Collier, Paul M. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons, 2015.

Dutta, Saurav K., Raef A. Lawson, and David Marcinko. "A Conceptual Foundation for

Management Accounting Information to Support Sustainability Strategies." 2015.

Galliers, Robert D., and Dorothy E. Leidner, eds. Strategic information management: challenges

and strategies in managing information systems. Routledge, 2014.

Ijiri, Yuji. "The beauty of double-entry bookkeeping and its impact on the nature of accounting

information." Economie Notes by Monte dei Paschi di Siena 22, no. 2-1993 (2014): 265-

285.

Laudon, Kenneth C., and Jane P. Laudon. Management information system. Pearson Education

India, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

Prasad, Acklesh, and Peter Green. "Organizational competencies and dynamic accounting

information system capability: impact on AIS processes and firm performance." Journal

of Information Systems 29, no. 3 (2015): 123-149.

Schaltegger, Stefan, Roger Burritt, Dimitar Zvezdov, Jacob Hörisch, and Joanne Tingey‐

Holyoak. "Management roles and sustainability information. Exploring corporate

practice." Australian Accounting Review 25, no. 4 (2015): 328-345.

Simkin, Mark G., Carolyn S. Norman, and Jacob M. Rose. Core concepts of accounting

information systems. John Wiley & Sons, 2014.

Sousa, Ken, and Effy Oz. Management information systems. Nelson Education, 2014.

Xu, Hongjiang. "What Are the Most Important Factors for Accounting Information Quality and

Their Impact on AIS Data Quality Outcomes?." Journal of Data and Information Quality

(JDIQ) 5, no. 4 (2015): 14.

Prasad, Acklesh, and Peter Green. "Organizational competencies and dynamic accounting

information system capability: impact on AIS processes and firm performance." Journal

of Information Systems 29, no. 3 (2015): 123-149.

Schaltegger, Stefan, Roger Burritt, Dimitar Zvezdov, Jacob Hörisch, and Joanne Tingey‐

Holyoak. "Management roles and sustainability information. Exploring corporate

practice." Australian Accounting Review 25, no. 4 (2015): 328-345.

Simkin, Mark G., Carolyn S. Norman, and Jacob M. Rose. Core concepts of accounting

information systems. John Wiley & Sons, 2014.

Sousa, Ken, and Effy Oz. Management information systems. Nelson Education, 2014.

Xu, Hongjiang. "What Are the Most Important Factors for Accounting Information Quality and

Their Impact on AIS Data Quality Outcomes?." Journal of Data and Information Quality

(JDIQ) 5, no. 4 (2015): 14.

11ACCOUNTING INFORMATION SYSTEM IN DECISION MAKING

Appendix

Questionnaire for the survey respondents:

Tick on the

chosen

option

1) Sex

Male Female

2) Age

18-25 26-35 36-45 46 and

above

3) Position

of

respondent

Junior

manager

Middle

manager

Senior

manager

Strongly Agree (SA), Agree (A), Undecided

(U), Disagree (D), Strongly Disagree (SD)

Selected

response

4) Accounting information facilitates management to

allocate scarce resources in effective enterprises

5) Omission of accounting information can have

an effect on management decision making

Appendix

Questionnaire for the survey respondents:

Tick on the

chosen

option

1) Sex

Male Female

2) Age

18-25 26-35 36-45 46 and

above

3) Position

of

respondent

Junior

manager

Middle

manager

Senior

manager

Strongly Agree (SA), Agree (A), Undecided

(U), Disagree (D), Strongly Disagree (SD)

Selected

response

4) Accounting information facilitates management to

allocate scarce resources in effective enterprises

5) Omission of accounting information can have

an effect on management decision making

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.