Al Anwar Ceramic Company: Financial Analysis and Investment Rationale

VerifiedAdded on 2021/02/21

|12

|1942

|52

Report

AI Summary

This report presents a comprehensive financial analysis of Al Anwar Ceramic, a ceramic tile manufacturer based in Oman. It begins with an overview of the company, including its establishment in 1998 and current production capacity. The report then provides an investment summary, highlighting the company's position in the Omani market and its cost management strategies. Key catalysts, such as production capacity expansion, are discussed, followed by an investment rationale based on the growing demand in the construction sector. The core of the report is a detailed ratio analysis, covering profitability, liquidity, efficiency, and valuation ratios. The analysis includes tables for financial projections and discounted cash flow valuation, concluding that the company's shares are undervalued. A price comparison with competitors is also provided. The report concludes that Al Anwar Ceramic is performing well and has expansion plans, supported by the analysis of its financial statements.

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Overview of company..................................................................................................................3

Investment summary....................................................................................................................3

Key catalysts................................................................................................................................3

Investment rationale.....................................................................................................................4

Ratio analysis...............................................................................................................................4

CONCLUSION .............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION...........................................................................................................................3

Overview of company..................................................................................................................3

Investment summary....................................................................................................................3

Key catalysts................................................................................................................................3

Investment rationale.....................................................................................................................4

Ratio analysis...............................................................................................................................4

CONCLUSION .............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION

Finance is term that refers to a process of implementing proper management of monitory

resources of the company. The major motive of implementing finance is to maintain sufficient

amount of financial resources within the company and formulate effective strategies in such a

way so that company's financial position could be improved. Al Anwar ceramic is a company

that manufactures ceramic tiles in the Oman. The present stud includes a brief description of

overall business of Al Anwar ceramic company. Further it also includes a detailed analysis of

financial performance of the company.

Overview of company

Al Anwar ceramic is company which is specialised in manufacturing and distribution of

finest ceramic tiles. It was establish in the year 1998. The company uses different raw materials,

galzes, pigments, frits, etc. available in the local market. Currently its production capacity is 3.5

million square meter per annum. It is formulating its new plans and procedures in order to

increase its capacity to 17 million square meter per annum.

Investment summary

Al Anwar ceramic is an Oman based company. Thus, majority of its business depends

upon the demand of ceramic tiles and other products produced by it in the market of Oman

(Alian, Shinen and Ali, 2018). With the help of growing demand of ceramic tiles in Oman, the

company has become able to become one among the top three companies of the ceramic tiles

industry.Further, with the help of effective cost management, the company's profitability has also

been improved.

In addition, with the help of strong balance sheet and lower value of leverage, the

company is maintaining consistency in payment of dividend and develop more effective future

investment plans as well. By analysing financial statements of last few years, it can be states that

Al Anwar ceramic’s capability of paying dividend.

Key catalysts

Recently the company has become able to increase its capacity of production upto 3.5

million square meter per annum .Al Anwar ceramic is one the most leading tiles manufacturer

company of Oman.The latest objective of the company is to expand its business in Nizwa and

Finance is term that refers to a process of implementing proper management of monitory

resources of the company. The major motive of implementing finance is to maintain sufficient

amount of financial resources within the company and formulate effective strategies in such a

way so that company's financial position could be improved. Al Anwar ceramic is a company

that manufactures ceramic tiles in the Oman. The present stud includes a brief description of

overall business of Al Anwar ceramic company. Further it also includes a detailed analysis of

financial performance of the company.

Overview of company

Al Anwar ceramic is company which is specialised in manufacturing and distribution of

finest ceramic tiles. It was establish in the year 1998. The company uses different raw materials,

galzes, pigments, frits, etc. available in the local market. Currently its production capacity is 3.5

million square meter per annum. It is formulating its new plans and procedures in order to

increase its capacity to 17 million square meter per annum.

Investment summary

Al Anwar ceramic is an Oman based company. Thus, majority of its business depends

upon the demand of ceramic tiles and other products produced by it in the market of Oman

(Alian, Shinen and Ali, 2018). With the help of growing demand of ceramic tiles in Oman, the

company has become able to become one among the top three companies of the ceramic tiles

industry.Further, with the help of effective cost management, the company's profitability has also

been improved.

In addition, with the help of strong balance sheet and lower value of leverage, the

company is maintaining consistency in payment of dividend and develop more effective future

investment plans as well. By analysing financial statements of last few years, it can be states that

Al Anwar ceramic’s capability of paying dividend.

Key catalysts

Recently the company has become able to increase its capacity of production upto 3.5

million square meter per annum .Al Anwar ceramic is one the most leading tiles manufacturer

company of Oman.The latest objective of the company is to expand its business in Nizwa and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expand its capacity to 17 million square meter per annum. The managers of company also have

formulated their plans and policies through which it would be able to minimise its cost and

improve the profitability as well.

Investment rationale

Increase in demand of Oman's building and construction sector results in driving the

demand of ceramic tiles of Al Anwar ceramic (Millan Cárdenas and et.al., 2017). As per annual

reports of Al Anwar ceramic, net income of the company rose to 69%. to OMR623K. Growth in

the ceramic tiles industry is more faster than the growth of GDP. Cement.

Further, the study also shows that the overall operating cash flow of the company

increased by 22.04 % recently. Thus, it can be analysed that Al Anwar ceramic is currently

performing efficiently in context to its financial performance.

Ratio analysis

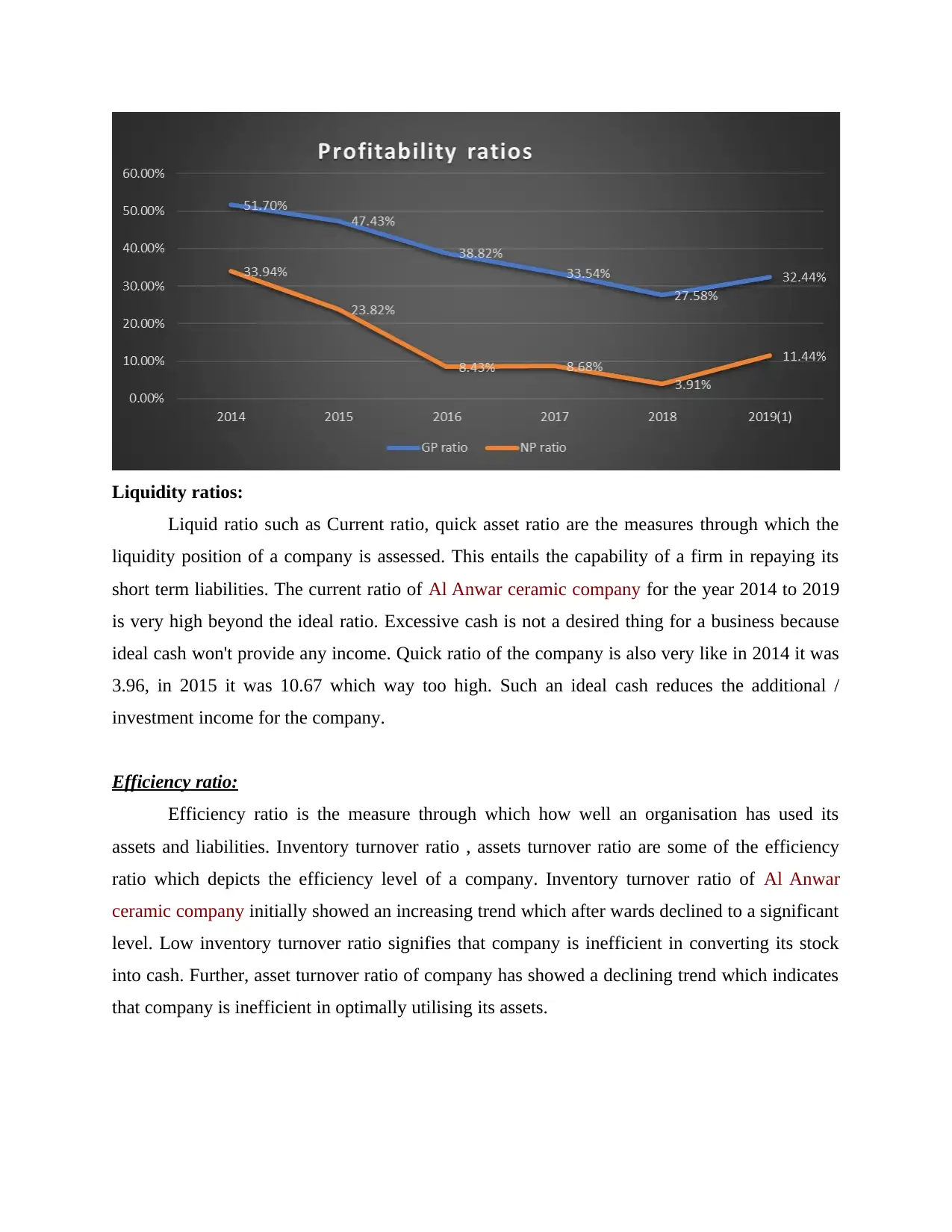

Profitability ratios

Profitability ratio is one of the category of financial metrics which are applied for the

purpose of assessing the ability of company of generating earnings in relation to operating costs,

revenue, assets and equity by using a particular time period. In other words, it displays how

effectively the company has used its resources for generating its profits. It includes gross profit,

net profit ratios. The gross profit ratio entails the relationship between sales and gross profit of a

business. The GP ratio of Al Anwar ceramic company for the la32st few years have declined as it

was 51.70% in 2014 which has declined to 32.44% in the year 2019(1). While net profit ratio is

also depicting a declining trend over the last years. This means that company's effciciny has

decreased significantly.

formulated their plans and policies through which it would be able to minimise its cost and

improve the profitability as well.

Investment rationale

Increase in demand of Oman's building and construction sector results in driving the

demand of ceramic tiles of Al Anwar ceramic (Millan Cárdenas and et.al., 2017). As per annual

reports of Al Anwar ceramic, net income of the company rose to 69%. to OMR623K. Growth in

the ceramic tiles industry is more faster than the growth of GDP. Cement.

Further, the study also shows that the overall operating cash flow of the company

increased by 22.04 % recently. Thus, it can be analysed that Al Anwar ceramic is currently

performing efficiently in context to its financial performance.

Ratio analysis

Profitability ratios

Profitability ratio is one of the category of financial metrics which are applied for the

purpose of assessing the ability of company of generating earnings in relation to operating costs,

revenue, assets and equity by using a particular time period. In other words, it displays how

effectively the company has used its resources for generating its profits. It includes gross profit,

net profit ratios. The gross profit ratio entails the relationship between sales and gross profit of a

business. The GP ratio of Al Anwar ceramic company for the la32st few years have declined as it

was 51.70% in 2014 which has declined to 32.44% in the year 2019(1). While net profit ratio is

also depicting a declining trend over the last years. This means that company's effciciny has

decreased significantly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liquidity ratios:

Liquid ratio such as Current ratio, quick asset ratio are the measures through which the

liquidity position of a company is assessed. This entails the capability of a firm in repaying its

short term liabilities. The current ratio of Al Anwar ceramic company for the year 2014 to 2019

is very high beyond the ideal ratio. Excessive cash is not a desired thing for a business because

ideal cash won't provide any income. Quick ratio of the company is also very like in 2014 it was

3.96, in 2015 it was 10.67 which way too high. Such an ideal cash reduces the additional /

investment income for the company.

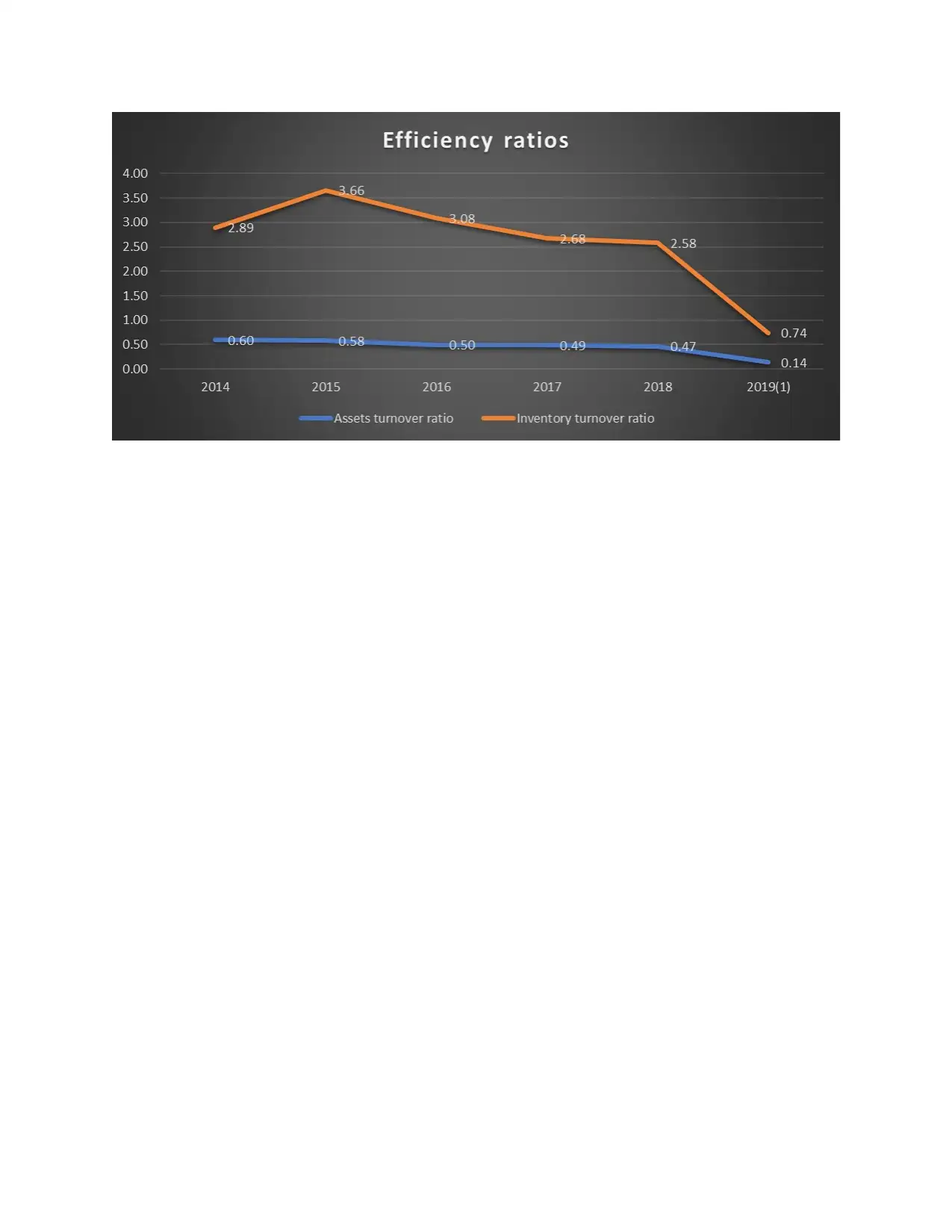

Efficiency ratio:

Efficiency ratio is the measure through which how well an organisation has used its

assets and liabilities. Inventory turnover ratio , assets turnover ratio are some of the efficiency

ratio which depicts the efficiency level of a company. Inventory turnover ratio of Al Anwar

ceramic company initially showed an increasing trend which after wards declined to a significant

level. Low inventory turnover ratio signifies that company is inefficient in converting its stock

into cash. Further, asset turnover ratio of company has showed a declining trend which indicates

that company is inefficient in optimally utilising its assets.

Liquid ratio such as Current ratio, quick asset ratio are the measures through which the

liquidity position of a company is assessed. This entails the capability of a firm in repaying its

short term liabilities. The current ratio of Al Anwar ceramic company for the year 2014 to 2019

is very high beyond the ideal ratio. Excessive cash is not a desired thing for a business because

ideal cash won't provide any income. Quick ratio of the company is also very like in 2014 it was

3.96, in 2015 it was 10.67 which way too high. Such an ideal cash reduces the additional /

investment income for the company.

Efficiency ratio:

Efficiency ratio is the measure through which how well an organisation has used its

assets and liabilities. Inventory turnover ratio , assets turnover ratio are some of the efficiency

ratio which depicts the efficiency level of a company. Inventory turnover ratio of Al Anwar

ceramic company initially showed an increasing trend which after wards declined to a significant

level. Low inventory turnover ratio signifies that company is inefficient in converting its stock

into cash. Further, asset turnover ratio of company has showed a declining trend which indicates

that company is inefficient in optimally utilising its assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

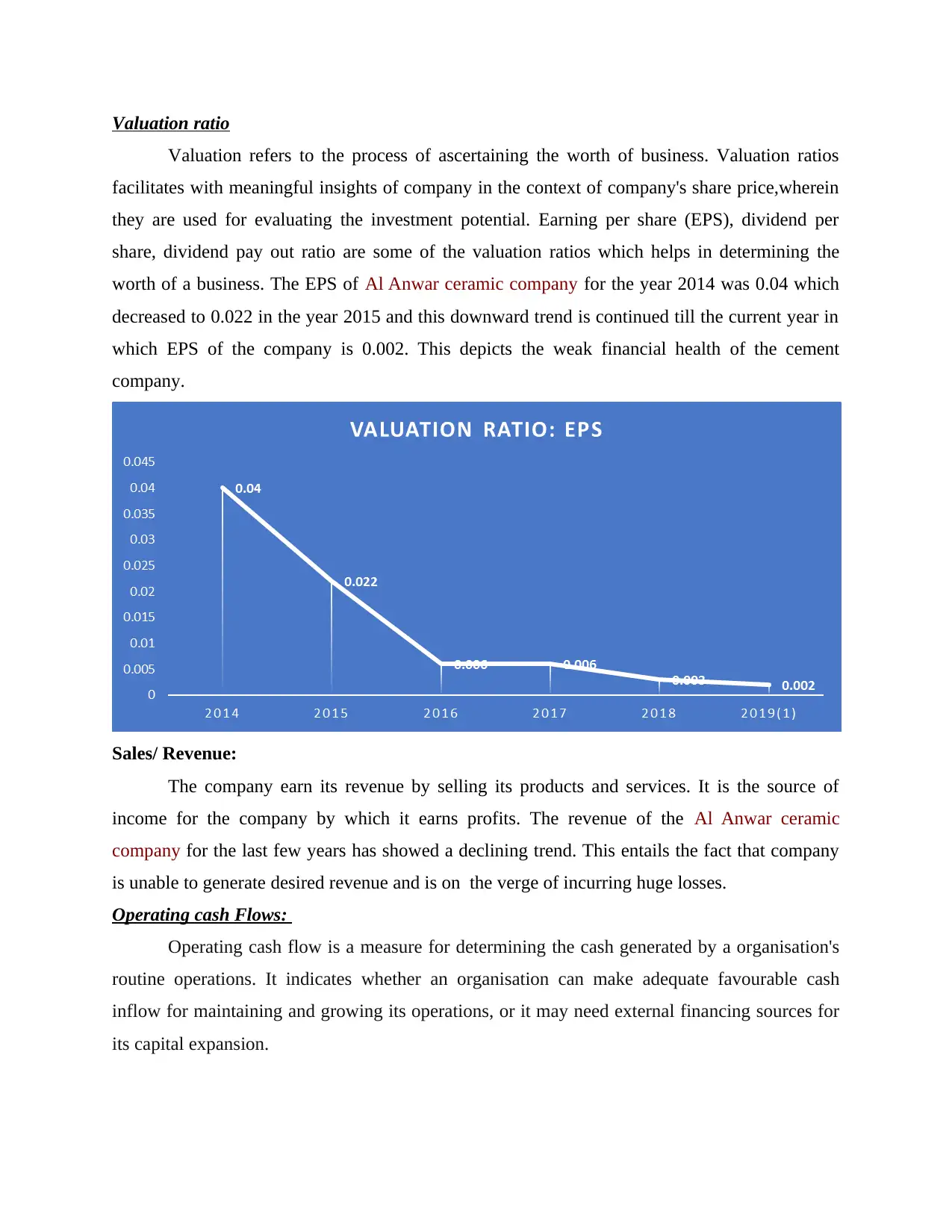

Valuation ratio

Valuation refers to the process of ascertaining the worth of business. Valuation ratios

facilitates with meaningful insights of company in the context of company's share price,wherein

they are used for evaluating the investment potential. Earning per share (EPS), dividend per

share, dividend pay out ratio are some of the valuation ratios which helps in determining the

worth of a business. The EPS of Al Anwar ceramic company for the year 2014 was 0.04 which

decreased to 0.022 in the year 2015 and this downward trend is continued till the current year in

which EPS of the company is 0.002. This depicts the weak financial health of the cement

company.

Sales/ Revenue:

The company earn its revenue by selling its products and services. It is the source of

income for the company by which it earns profits. The revenue of the Al Anwar ceramic

company for the last few years has showed a declining trend. This entails the fact that company

is unable to generate desired revenue and is on the verge of incurring huge losses.

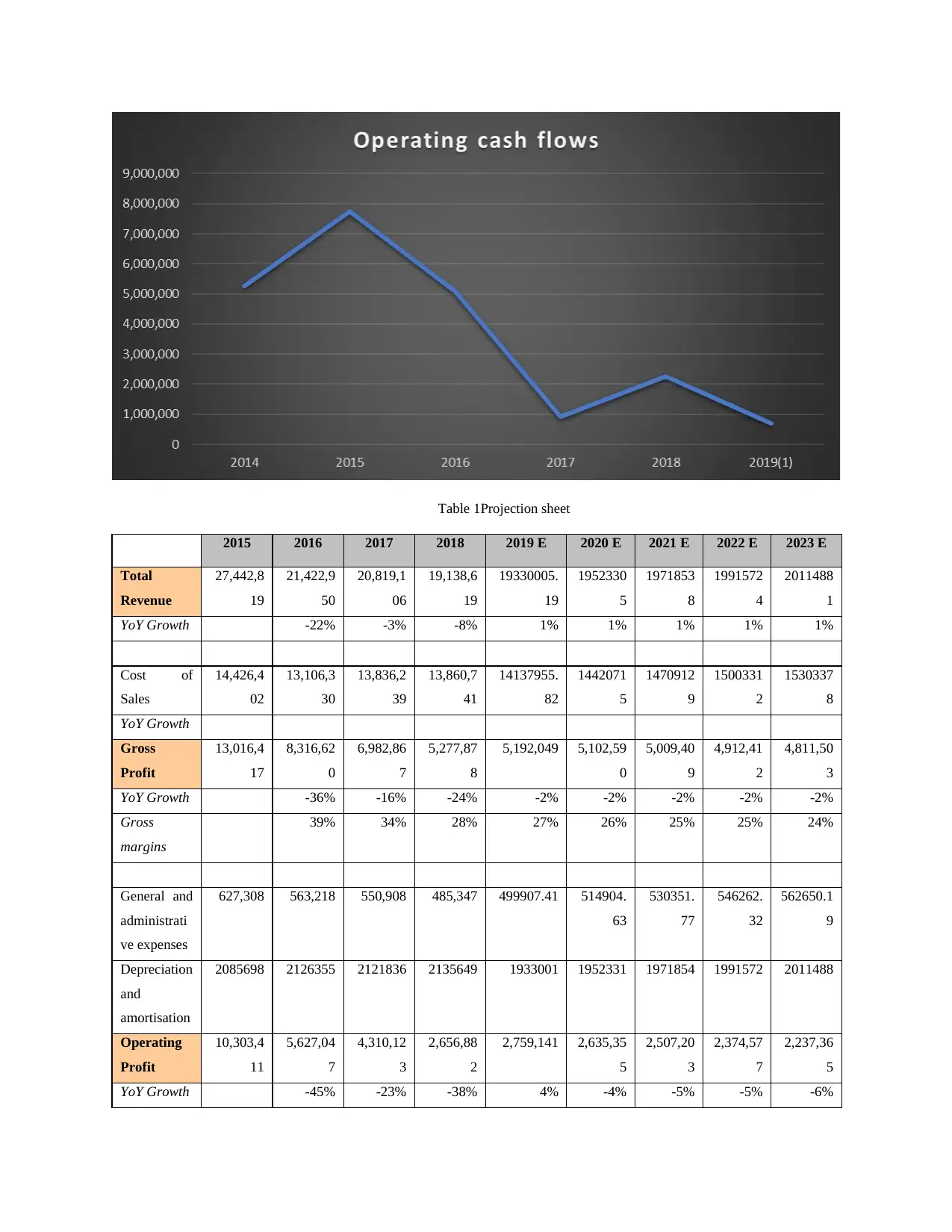

Operating cash Flows:

Operating cash flow is a measure for determining the cash generated by a organisation's

routine operations. It indicates whether an organisation can make adequate favourable cash

inflow for maintaining and growing its operations, or it may need external financing sources for

its capital expansion.

Valuation refers to the process of ascertaining the worth of business. Valuation ratios

facilitates with meaningful insights of company in the context of company's share price,wherein

they are used for evaluating the investment potential. Earning per share (EPS), dividend per

share, dividend pay out ratio are some of the valuation ratios which helps in determining the

worth of a business. The EPS of Al Anwar ceramic company for the year 2014 was 0.04 which

decreased to 0.022 in the year 2015 and this downward trend is continued till the current year in

which EPS of the company is 0.002. This depicts the weak financial health of the cement

company.

Sales/ Revenue:

The company earn its revenue by selling its products and services. It is the source of

income for the company by which it earns profits. The revenue of the Al Anwar ceramic

company for the last few years has showed a declining trend. This entails the fact that company

is unable to generate desired revenue and is on the verge of incurring huge losses.

Operating cash Flows:

Operating cash flow is a measure for determining the cash generated by a organisation's

routine operations. It indicates whether an organisation can make adequate favourable cash

inflow for maintaining and growing its operations, or it may need external financing sources for

its capital expansion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

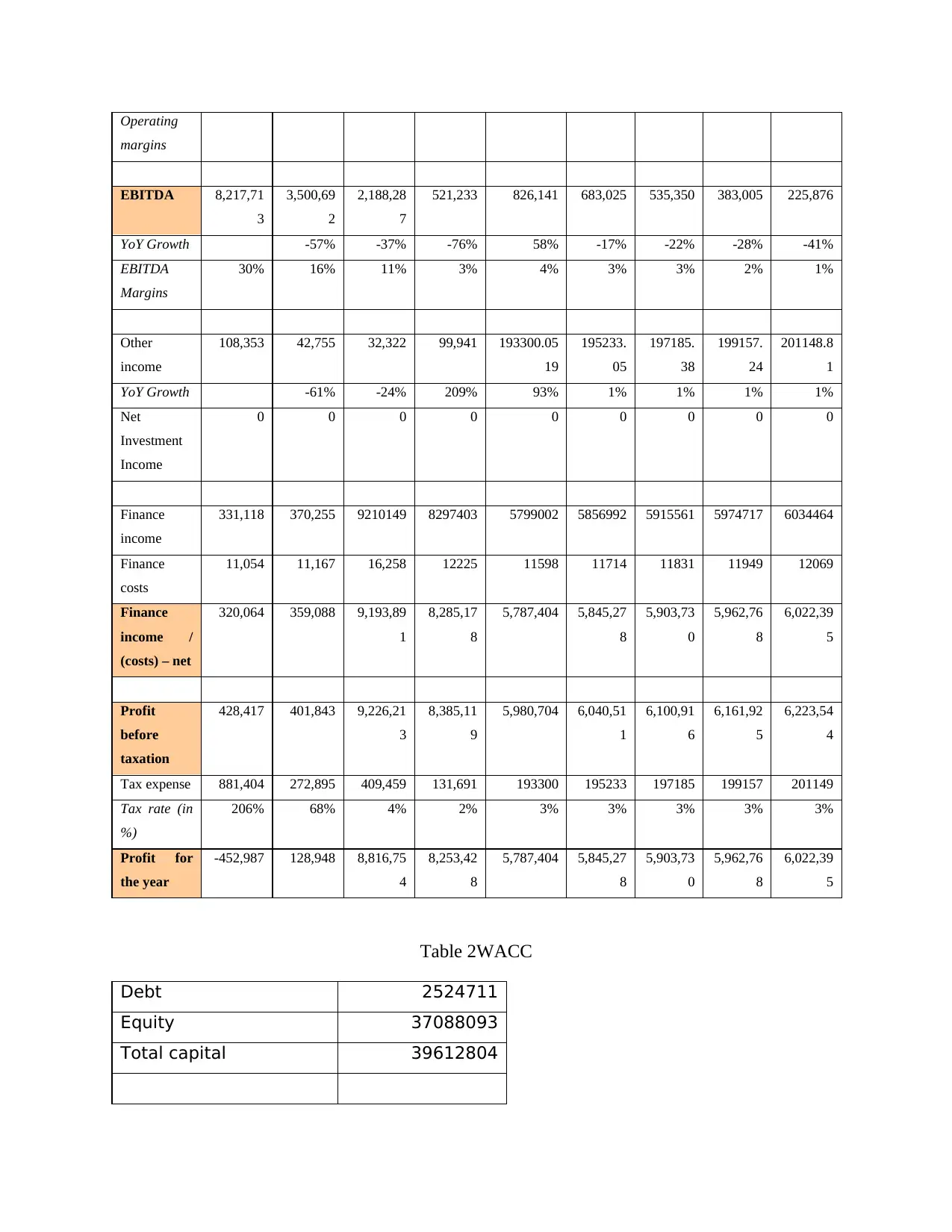

Table 1Projection sheet

2015 2016 2017 2018 2019 E 2020 E 2021 E 2022 E 2023 E

Total

Revenue

27,442,8

19

21,422,9

50

20,819,1

06

19,138,6

19

19330005.

19

1952330

5

1971853

8

1991572

4

2011488

1

YoY Growth -22% -3% -8% 1% 1% 1% 1% 1%

Cost of

Sales

14,426,4

02

13,106,3

30

13,836,2

39

13,860,7

41

14137955.

82

1442071

5

1470912

9

1500331

2

1530337

8

YoY Growth

Gross

Profit

13,016,4

17

8,316,62

0

6,982,86

7

5,277,87

8

5,192,049 5,102,59

0

5,009,40

9

4,912,41

2

4,811,50

3

YoY Growth -36% -16% -24% -2% -2% -2% -2% -2%

Gross

margins

39% 34% 28% 27% 26% 25% 25% 24%

General and

administrati

ve expenses

627,308 563,218 550,908 485,347 499907.41 514904.

63

530351.

77

546262.

32

562650.1

9

Depreciation

and

amortisation

2085698 2126355 2121836 2135649 1933001 1952331 1971854 1991572 2011488

Operating

Profit

10,303,4

11

5,627,04

7

4,310,12

3

2,656,88

2

2,759,141 2,635,35

5

2,507,20

3

2,374,57

7

2,237,36

5

YoY Growth -45% -23% -38% 4% -4% -5% -5% -6%

2015 2016 2017 2018 2019 E 2020 E 2021 E 2022 E 2023 E

Total

Revenue

27,442,8

19

21,422,9

50

20,819,1

06

19,138,6

19

19330005.

19

1952330

5

1971853

8

1991572

4

2011488

1

YoY Growth -22% -3% -8% 1% 1% 1% 1% 1%

Cost of

Sales

14,426,4

02

13,106,3

30

13,836,2

39

13,860,7

41

14137955.

82

1442071

5

1470912

9

1500331

2

1530337

8

YoY Growth

Gross

Profit

13,016,4

17

8,316,62

0

6,982,86

7

5,277,87

8

5,192,049 5,102,59

0

5,009,40

9

4,912,41

2

4,811,50

3

YoY Growth -36% -16% -24% -2% -2% -2% -2% -2%

Gross

margins

39% 34% 28% 27% 26% 25% 25% 24%

General and

administrati

ve expenses

627,308 563,218 550,908 485,347 499907.41 514904.

63

530351.

77

546262.

32

562650.1

9

Depreciation

and

amortisation

2085698 2126355 2121836 2135649 1933001 1952331 1971854 1991572 2011488

Operating

Profit

10,303,4

11

5,627,04

7

4,310,12

3

2,656,88

2

2,759,141 2,635,35

5

2,507,20

3

2,374,57

7

2,237,36

5

YoY Growth -45% -23% -38% 4% -4% -5% -5% -6%

Operating

margins

EBITDA 8,217,71

3

3,500,69

2

2,188,28

7

521,233 826,141 683,025 535,350 383,005 225,876

YoY Growth -57% -37% -76% 58% -17% -22% -28% -41%

EBITDA

Margins

30% 16% 11% 3% 4% 3% 3% 2% 1%

Other

income

108,353 42,755 32,322 99,941 193300.05

19

195233.

05

197185.

38

199157.

24

201148.8

1

YoY Growth -61% -24% 209% 93% 1% 1% 1% 1%

Net

Investment

Income

0 0 0 0 0 0 0 0 0

Finance

income

331,118 370,255 9210149 8297403 5799002 5856992 5915561 5974717 6034464

Finance

costs

11,054 11,167 16,258 12225 11598 11714 11831 11949 12069

Finance

income /

(costs) – net

320,064 359,088 9,193,89

1

8,285,17

8

5,787,404 5,845,27

8

5,903,73

0

5,962,76

8

6,022,39

5

Profit

before

taxation

428,417 401,843 9,226,21

3

8,385,11

9

5,980,704 6,040,51

1

6,100,91

6

6,161,92

5

6,223,54

4

Tax expense 881,404 272,895 409,459 131,691 193300 195233 197185 199157 201149

Tax rate (in

%)

206% 68% 4% 2% 3% 3% 3% 3% 3%

Profit for

the year

-452,987 128,948 8,816,75

4

8,253,42

8

5,787,404 5,845,27

8

5,903,73

0

5,962,76

8

6,022,39

5

Table 2WACC

Debt 2524711

Equity 37088093

Total capital 39612804

margins

EBITDA 8,217,71

3

3,500,69

2

2,188,28

7

521,233 826,141 683,025 535,350 383,005 225,876

YoY Growth -57% -37% -76% 58% -17% -22% -28% -41%

EBITDA

Margins

30% 16% 11% 3% 4% 3% 3% 2% 1%

Other

income

108,353 42,755 32,322 99,941 193300.05

19

195233.

05

197185.

38

199157.

24

201148.8

1

YoY Growth -61% -24% 209% 93% 1% 1% 1% 1%

Net

Investment

Income

0 0 0 0 0 0 0 0 0

Finance

income

331,118 370,255 9210149 8297403 5799002 5856992 5915561 5974717 6034464

Finance

costs

11,054 11,167 16,258 12225 11598 11714 11831 11949 12069

Finance

income /

(costs) – net

320,064 359,088 9,193,89

1

8,285,17

8

5,787,404 5,845,27

8

5,903,73

0

5,962,76

8

6,022,39

5

Profit

before

taxation

428,417 401,843 9,226,21

3

8,385,11

9

5,980,704 6,040,51

1

6,100,91

6

6,161,92

5

6,223,54

4

Tax expense 881,404 272,895 409,459 131,691 193300 195233 197185 199157 201149

Tax rate (in

%)

206% 68% 4% 2% 3% 3% 3% 3% 3%

Profit for

the year

-452,987 128,948 8,816,75

4

8,253,42

8

5,787,404 5,845,27

8

5,903,73

0

5,962,76

8

6,022,39

5

Table 2WACC

Debt 2524711

Equity 37088093

Total capital 39612804

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debt/Total capital 6%

Equity/Total capital 94%

% Interest rate 7%

% Cost of equity 6.32%

WACC or cost of capital 6.36%

Table 3Discounted cash flow

DCF Method FY19E FY20E FY21E FY22E FY23E

27-07-19 31-12-19 31-12-20 31-12-21 31-12-22 31-12-23

No of Days 157 523 888 1,253 1,618

Time Remaining (Years) 0.43 1.43 2.43 3.43 4.43

Operating profit Before Interest and Tax 2,759,141 2,635,355 2,507,203 2,374,577 2,237,365

growth(%) -4.5% -4.9% -5.3% -5.8%

Tax rate 15.0% 15.0% 15.0% 15.0% 15.0%

Post-tax operating profit (NOPAT) 2,345,270 2,240,052 2,131,123 2,018,391 1,901,760

Add: Depreciation & amortization 1,933,001 1,952,331 1,971,854 1,991,572 2,011,488

Less: Change in working capital 350,633 350,633 350,633 350,633 350,633

Less: Capex 155,229 97,795 61,611 38,815 24,453

Free Cash Flow to Firm 4,784,133 4,640,810 4,515,220 4,399,411 4,288,334

FCF growth -3.0% -2.7% -2.6% -2.5%

Discount factor 0.97 1.00 1.00 1.00 1.00

PV of Free Cash Flows 4,658,853 4,640,810 4,515,220 4,399,411 4,288,334

Sum of present values of FCFs 22,502,629

Free cash flow (t+1) 4,288,334

Terminal value 9,894,722,737

Present value of terminal value 9,894,722,737

EV 9,917,225,366

Less: Net debt 2,390,072

Equity value 9,919,615,437

Fair value per share (RO) 0.335

Shares O/s 29,621,000,000

Upside/Downside 256.3%

Current Price 0.094

Interpretation

Equity/Total capital 94%

% Interest rate 7%

% Cost of equity 6.32%

WACC or cost of capital 6.36%

Table 3Discounted cash flow

DCF Method FY19E FY20E FY21E FY22E FY23E

27-07-19 31-12-19 31-12-20 31-12-21 31-12-22 31-12-23

No of Days 157 523 888 1,253 1,618

Time Remaining (Years) 0.43 1.43 2.43 3.43 4.43

Operating profit Before Interest and Tax 2,759,141 2,635,355 2,507,203 2,374,577 2,237,365

growth(%) -4.5% -4.9% -5.3% -5.8%

Tax rate 15.0% 15.0% 15.0% 15.0% 15.0%

Post-tax operating profit (NOPAT) 2,345,270 2,240,052 2,131,123 2,018,391 1,901,760

Add: Depreciation & amortization 1,933,001 1,952,331 1,971,854 1,991,572 2,011,488

Less: Change in working capital 350,633 350,633 350,633 350,633 350,633

Less: Capex 155,229 97,795 61,611 38,815 24,453

Free Cash Flow to Firm 4,784,133 4,640,810 4,515,220 4,399,411 4,288,334

FCF growth -3.0% -2.7% -2.6% -2.5%

Discount factor 0.97 1.00 1.00 1.00 1.00

PV of Free Cash Flows 4,658,853 4,640,810 4,515,220 4,399,411 4,288,334

Sum of present values of FCFs 22,502,629

Free cash flow (t+1) 4,288,334

Terminal value 9,894,722,737

Present value of terminal value 9,894,722,737

EV 9,917,225,366

Less: Net debt 2,390,072

Equity value 9,919,615,437

Fair value per share (RO) 0.335

Shares O/s 29,621,000,000

Upside/Downside 256.3%

Current Price 0.094

Interpretation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

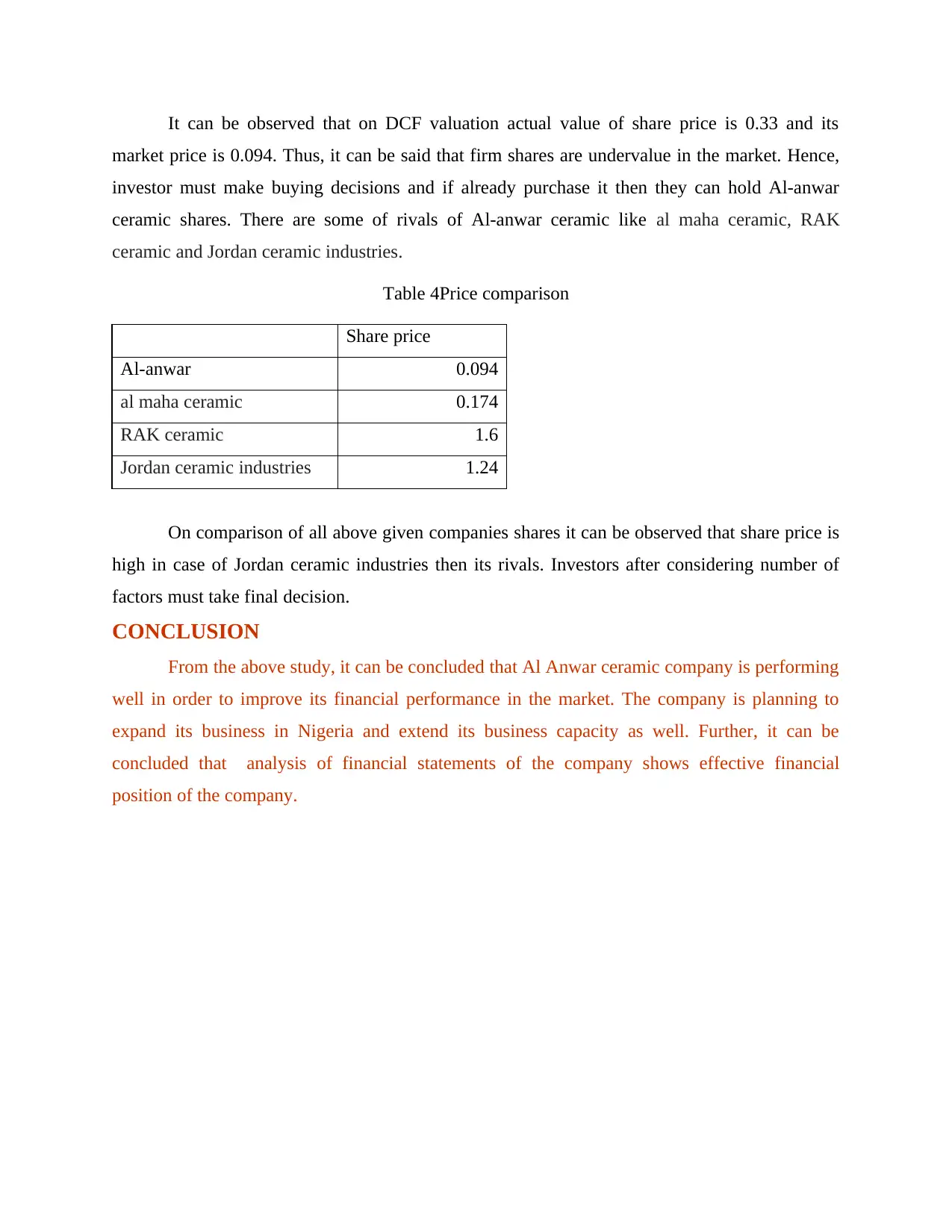

It can be observed that on DCF valuation actual value of share price is 0.33 and its

market price is 0.094. Thus, it can be said that firm shares are undervalue in the market. Hence,

investor must make buying decisions and if already purchase it then they can hold Al-anwar

ceramic shares. There are some of rivals of Al-anwar ceramic like al maha ceramic, RAK

ceramic and Jordan ceramic industries.

Table 4Price comparison

Share price

Al-anwar 0.094

al maha ceramic 0.174

RAK ceramic 1.6

Jordan ceramic industries 1.24

On comparison of all above given companies shares it can be observed that share price is

high in case of Jordan ceramic industries then its rivals. Investors after considering number of

factors must take final decision.

CONCLUSION

From the above study, it can be concluded that Al Anwar ceramic company is performing

well in order to improve its financial performance in the market. The company is planning to

expand its business in Nigeria and extend its business capacity as well. Further, it can be

concluded that analysis of financial statements of the company shows effective financial

position of the company.

market price is 0.094. Thus, it can be said that firm shares are undervalue in the market. Hence,

investor must make buying decisions and if already purchase it then they can hold Al-anwar

ceramic shares. There are some of rivals of Al-anwar ceramic like al maha ceramic, RAK

ceramic and Jordan ceramic industries.

Table 4Price comparison

Share price

Al-anwar 0.094

al maha ceramic 0.174

RAK ceramic 1.6

Jordan ceramic industries 1.24

On comparison of all above given companies shares it can be observed that share price is

high in case of Jordan ceramic industries then its rivals. Investors after considering number of

factors must take final decision.

CONCLUSION

From the above study, it can be concluded that Al Anwar ceramic company is performing

well in order to improve its financial performance in the market. The company is planning to

expand its business in Nigeria and extend its business capacity as well. Further, it can be

concluded that analysis of financial statements of the company shows effective financial

position of the company.

REFERENCES

Books and Journals

Alian, N. K., Shinen, M. H. and Ali, A. H., 2018. Modification of Dielectric Strength of Iraqi

Kaolin by the Addition of Micro and Nano Zirconia. Journal of University of Babylon for

Pure and Applied Sciences, 26(7), pp.284-268.

Millan Cárdenas, A. and et.al., 2017. Effect of MDP-containing silane and adhesive used alone

or in combination on the long-term bond strength and chemical interaction with Lithium

Disilicate Ceramics.

Books and Journals

Alian, N. K., Shinen, M. H. and Ali, A. H., 2018. Modification of Dielectric Strength of Iraqi

Kaolin by the Addition of Micro and Nano Zirconia. Journal of University of Babylon for

Pure and Applied Sciences, 26(7), pp.284-268.

Millan Cárdenas, A. and et.al., 2017. Effect of MDP-containing silane and adhesive used alone

or in combination on the long-term bond strength and chemical interaction with Lithium

Disilicate Ceramics.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.