Comprehensive Management Accounting Report for Al Sham Automotive

VerifiedAdded on 2020/07/22

|14

|4128

|35

Report

AI Summary

This report examines management accounting principles and practices within the context of Al Sham Automotive Co. It begins by identifying core principles such as influence, relevance, value, trust, and integration, and then differentiates between financial and managerial accounting. The report explores the roles and responsibilities of accounting and financial managers, highlighting their contributions to decision-making and financial reporting. It also presents common accounting systems like cost, inventory, and lean accounting, and assesses their roles in planning, controlling, and managing business operations. Furthermore, the report discusses the significance of management accounting in preparing plans, making make-or-buy decisions, and forecasting cash flow, emphasizing its crucial role in enhancing business performance and achieving organizational goals. The report is a valuable resource for students seeking to understand the practical application of management accounting concepts.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

1. Identifying the principles of management accounting.......................................................1

2. Presenting the most common accounting systems used by organizations.........................5

3. Assessing the role of management accounting and methods that can be used for the

purpose of reporting...............................................................................................................6

4. Explaining the manner in which management accounting is integrated within an

organization............................................................................................................................8

CONCLUSION..........................................................................................................................8

REFERENCES.........................................................................................................................10

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

1. Identifying the principles of management accounting.......................................................1

2. Presenting the most common accounting systems used by organizations.........................5

3. Assessing the role of management accounting and methods that can be used for the

purpose of reporting...............................................................................................................6

4. Explaining the manner in which management accounting is integrated within an

organization............................................................................................................................8

CONCLUSION..........................................................................................................................8

REFERENCES.........................................................................................................................10

INTRODUCTION

In the present era, business unit places high level of emphasis on undertaking

managerial accounting tools and techniques. The rationale behind this, management

accounting tools provides input for the cost control and thereby helps in enhancing business

performance in monetary terms. Such accounting field also provides high level of assistance

in monitoring business activities and overall performance to a great extent. In this way,

managerial accounting aid in decision making and contributes in the attainment of

organizational goals and objectives. The present report is based on Al Sham Automotive Co,

which is operating in the small business segment of car industry. In this, report will highlight

the extent to which financial accounting varies from managerial. Besides this, it will provide

deeper insight about the aspects of management accounting and reporting. Further, report also

depicts the roles and responsibilities shared by accounting as well as financial manager

within the firm.

TASK 1

1. Identifying the principles of management accounting

Management accounting and reports provide managers with appropriate and timely

financial as well as statistical information. Hence, managerial reports assist in making day to

day and short-term decision that contributes in the growth of firm. Thus, managerial

accounting may be served as a process of analysing, interpreting and presenting information

in front of higher management team for decision making. By considering all such aspects Al

Sham Automotive Co lays emphasis on undertaking the tools and techniques of management

accounting.

Principles of management accounting: The main principles of management accounting

which are accepted at global level as follows:

Influence:In management accounting, decision making aspect is based on effective

communication so it must be influential. Hence, managerial accounting improves

In the present era, business unit places high level of emphasis on undertaking

managerial accounting tools and techniques. The rationale behind this, management

accounting tools provides input for the cost control and thereby helps in enhancing business

performance in monetary terms. Such accounting field also provides high level of assistance

in monitoring business activities and overall performance to a great extent. In this way,

managerial accounting aid in decision making and contributes in the attainment of

organizational goals and objectives. The present report is based on Al Sham Automotive Co,

which is operating in the small business segment of car industry. In this, report will highlight

the extent to which financial accounting varies from managerial. Besides this, it will provide

deeper insight about the aspects of management accounting and reporting. Further, report also

depicts the roles and responsibilities shared by accounting as well as financial manager

within the firm.

TASK 1

1. Identifying the principles of management accounting

Management accounting and reports provide managers with appropriate and timely

financial as well as statistical information. Hence, managerial reports assist in making day to

day and short-term decision that contributes in the growth of firm. Thus, managerial

accounting may be served as a process of analysing, interpreting and presenting information

in front of higher management team for decision making. By considering all such aspects Al

Sham Automotive Co lays emphasis on undertaking the tools and techniques of management

accounting.

Principles of management accounting: The main principles of management accounting

which are accepted at global level as follows:

Influence:In management accounting, decision making aspect is based on effective

communication so it must be influential. Hence, managerial accounting improves

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision making to a great extent by serving useful information at all level. Such

principle lays high level of emphasis on integrated thinking and assists in

understanding the business areas in a prominent way. On the basis of decision makers

need relevant information is sourced and analysed under such field (Otley, 2016).

Hence, by taking into account all such aspects it can be said that recommendations are

highly useful for decision makers and helps in the formulation of competent strategic

framework. Relevance:The main focus of management accounting is on the relevancy aspect and

appropriateness of information. Thus, as per the needs of stakeholders such as

management, managerial accounting team gathers relevant information and prepared

the same for analysis. Hence, such principle facilitates balance between past, present

and future related information (The 4 Global Management Accounting Principles

Your Company Can Adopt, 2017). Along with this, it also tends to make focus on

getting information about financial, non-financial, environmental and social aspects.

This in turn helps in making appropriate decision for the business organization’s

success. Value:As per such principle, managers make focus on risk, cost, value generationand

potential of opportunities. Hence, scenario analysis is the most effectual techniques

that can be undertaken by the firm to evaluate the impact of opportunities and risks. In

this way, value principle of management accounting helps in assessing the ways

through which firm can grab the opportunity and mitigate risk level.

Trust:It entails and place emphasis on improving the trust of stakeholder group. On

the basis of trust factor, it is highly required for firm to get feedback and give quick

response to the questions and complaints (Weetman, 2016). By doing this, business

unit can indulge trust, creditability and thereby would become able to improve

process as well as brand image. Integration: In accordance with such principle,information must be integrated with

all the departments. Moreover, without having integration informationfirm is not in

position to develop competent framework for the near future.

Difference between managerial and financial accounting are enumerated below:

Basis of difference Managerial accounting Financial accounting

Meaning It offers input to the managers This accounting system lays

principle lays high level of emphasis on integrated thinking and assists in

understanding the business areas in a prominent way. On the basis of decision makers

need relevant information is sourced and analysed under such field (Otley, 2016).

Hence, by taking into account all such aspects it can be said that recommendations are

highly useful for decision makers and helps in the formulation of competent strategic

framework. Relevance:The main focus of management accounting is on the relevancy aspect and

appropriateness of information. Thus, as per the needs of stakeholders such as

management, managerial accounting team gathers relevant information and prepared

the same for analysis. Hence, such principle facilitates balance between past, present

and future related information (The 4 Global Management Accounting Principles

Your Company Can Adopt, 2017). Along with this, it also tends to make focus on

getting information about financial, non-financial, environmental and social aspects.

This in turn helps in making appropriate decision for the business organization’s

success. Value:As per such principle, managers make focus on risk, cost, value generationand

potential of opportunities. Hence, scenario analysis is the most effectual techniques

that can be undertaken by the firm to evaluate the impact of opportunities and risks. In

this way, value principle of management accounting helps in assessing the ways

through which firm can grab the opportunity and mitigate risk level.

Trust:It entails and place emphasis on improving the trust of stakeholder group. On

the basis of trust factor, it is highly required for firm to get feedback and give quick

response to the questions and complaints (Weetman, 2016). By doing this, business

unit can indulge trust, creditability and thereby would become able to improve

process as well as brand image. Integration: In accordance with such principle,information must be integrated with

all the departments. Moreover, without having integration informationfirm is not in

position to develop competent framework for the near future.

Difference between managerial and financial accounting are enumerated below:

Basis of difference Managerial accounting Financial accounting

Meaning It offers input to the managers This accounting system lays

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for the formulation of policies,

plan and strategies. Hence, such

system is highly significant

which in turn ensures the

smooth functioning of business

operations.

emphasis on the preparation of

financial statements. The main

motive behind such accounting

is to provide all the related

parties with appropriate

financial information.

Compulsion In the case of managerial

accounting, it is not compulsory

for the managers to prepare

reports(Messner, 2016).

Unlike managerial, private and

public firms require to employ

the system of financial

accounting.

Information Such accounting system serves

both financial and non-financial

information for decision

making.

Field of financial accounting

only offers financial

information to the stakeholders

for decision making.

Motive The main objective of firm

behind undertaking managerial

accounting practices is to assist

managers on various matters

(Difference between financial

and managerial accounting,

2017).

Objective of financial

accounting lays high level of

emphasis on meeting the needs

of outsiders such as suppliers,

investors, government etc.

Format Under managerial accounting,

no specific format is followed

by the managers.

In financial accounting, reports

or statements are prepared and

presented in a highly structured

way with appropriate format.

Reporting Managerial reports furnish

complete and detailed

information about various

fields.

It gives summarized

information regarding the

financial position and

performance of firm.

Publishing and auditing

requirements

There is no need of publishing

and auditing under managerial

accounting.

Financial reports must be

published after auditing by a

statutory auditor.

Hence, by taking into account all the above depicted aspects it can be stated that

financial and managerial accounting differs on the basis of various aspects.

Roles and responsibilities of managers at different levels are as follows:

plan and strategies. Hence, such

system is highly significant

which in turn ensures the

smooth functioning of business

operations.

emphasis on the preparation of

financial statements. The main

motive behind such accounting

is to provide all the related

parties with appropriate

financial information.

Compulsion In the case of managerial

accounting, it is not compulsory

for the managers to prepare

reports(Messner, 2016).

Unlike managerial, private and

public firms require to employ

the system of financial

accounting.

Information Such accounting system serves

both financial and non-financial

information for decision

making.

Field of financial accounting

only offers financial

information to the stakeholders

for decision making.

Motive The main objective of firm

behind undertaking managerial

accounting practices is to assist

managers on various matters

(Difference between financial

and managerial accounting,

2017).

Objective of financial

accounting lays high level of

emphasis on meeting the needs

of outsiders such as suppliers,

investors, government etc.

Format Under managerial accounting,

no specific format is followed

by the managers.

In financial accounting, reports

or statements are prepared and

presented in a highly structured

way with appropriate format.

Reporting Managerial reports furnish

complete and detailed

information about various

fields.

It gives summarized

information regarding the

financial position and

performance of firm.

Publishing and auditing

requirements

There is no need of publishing

and auditing under managerial

accounting.

Financial reports must be

published after auditing by a

statutory auditor.

Hence, by taking into account all the above depicted aspects it can be stated that

financial and managerial accounting differs on the basis of various aspects.

Roles and responsibilities of managers at different levels are as follows:

Accounting manager:

In the business unit, manager plays a vital role in assessing and ensuring that

transactions are in line with policy, regulatory as well as other requirements.

Along with this, manager also makes efforts in relation to assessing, maintaining as

well as exceeding the minimum amount of sales (Duties & Responsibilities of an

Account Manager, 2017). For this purpose, manager continuously makes assessment

of actual performance in against to set standards. Hence, after assessing the causesof

deviations, manager tries to take strategic measure that helps in getting the desired

level of outcome or success.

Reporting: It is the accountability of manager to prepare various reports regarding

quarterly sales, annual forecast etc and present the same to higher management.

Financial manager: In the business unit, financial manager performs several roles and carry

out responsibilities such as:

Finance managers role is highly significantwithin the firm as they prepare financial

statements and business activity report.

In addition to this, managers makesassessment and monitoring of the financial details

to identify the extent to which legal requirements are met.

Financial managerperforms most important function within the business unit in

relation to allocation of funds. At the time offund allocation, financial manager

considers several aspects such as size of firm, growth capability, status of asset and

mode of raising funds etc (Role of a Financial Manager,2017). All such aspects help

manager in making allocation of fund in such a manner as it is used optimally.

Profit earning and maximization is the prime function of an organization.In this, it is

the accountability of manager to assess the factors which have greater impact on

firm’s profitability. Such factors include pricing, competition, state of economy,

demand & supply mechanism, cost and output. Thus, it is the duty of manager to

assess the factors that closely influence profit margin or level and find out the

alternative.

Accountabilities of financial manager include evaluation of financial reports which in

turn helps in assessing the ways through which cost can be reduced (Weygandt,

Kimmel and Kieso, 2015).

In the business unit, manager plays a vital role in assessing and ensuring that

transactions are in line with policy, regulatory as well as other requirements.

Along with this, manager also makes efforts in relation to assessing, maintaining as

well as exceeding the minimum amount of sales (Duties & Responsibilities of an

Account Manager, 2017). For this purpose, manager continuously makes assessment

of actual performance in against to set standards. Hence, after assessing the causesof

deviations, manager tries to take strategic measure that helps in getting the desired

level of outcome or success.

Reporting: It is the accountability of manager to prepare various reports regarding

quarterly sales, annual forecast etc and present the same to higher management.

Financial manager: In the business unit, financial manager performs several roles and carry

out responsibilities such as:

Finance managers role is highly significantwithin the firm as they prepare financial

statements and business activity report.

In addition to this, managers makesassessment and monitoring of the financial details

to identify the extent to which legal requirements are met.

Financial managerperforms most important function within the business unit in

relation to allocation of funds. At the time offund allocation, financial manager

considers several aspects such as size of firm, growth capability, status of asset and

mode of raising funds etc (Role of a Financial Manager,2017). All such aspects help

manager in making allocation of fund in such a manner as it is used optimally.

Profit earning and maximization is the prime function of an organization.In this, it is

the accountability of manager to assess the factors which have greater impact on

firm’s profitability. Such factors include pricing, competition, state of economy,

demand & supply mechanism, cost and output. Thus, it is the duty of manager to

assess the factors that closely influence profit margin or level and find out the

alternative.

Accountabilities of financial manager include evaluation of financial reports which in

turn helps in assessing the ways through which cost can be reduced (Weygandt,

Kimmel and Kieso, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, it is the duty of financial manager to analysethe market trend and identify the

opportunities for expansion. Thus, referring the all such aspects it can be presented

that financial manager role is highly effectual in making monetary decisions.

2. Presenting the most common accounting systems used by organizations

With the motive to attain success over competitors Al Sham Automotive is planning

to undertake MA tools and techniques.The main reason behind this, system of MA furnishes

appropriate information to the managers for planning, controlling and managing the

operations of business. Thus, MA facilitates optimum utilization of resources by eliminating

the waste to a great extent. Hence, MA system that can be undertaken by Al Sham

Automotives are depicted below:

Cost accounting:It implies for the process of recording, classification, recording,

analysis, summarization, allocation as well as evaluation of various alternatives. Cost

accounting is the most effectual system which assists in identifying and advising the

most appropriate action through which financial efficiency as well as capability can

be raised. By employing such system manager can determine cost of product, process

and objects to a great extent (Chenhall and Moers, 2015). Moreover, such system

helps in assessing the cost incurred by Al Sham Automotive for manufacturing one

car. By dividing the total expenses from number of cars manufactured business

organization can determine per unit cost. Thus, by adding the profit margin in per unit

cost Al Sham Automotive can determine price level and becomes able to attain

profitability. Further, such system also helps firm in assessing as well as reporting

cost of inventory and COGS.

Inventory accounting: By using such system business unit can plan or track the

inventory level or associated activities. Thus, by making focus on bar code tracking

system firm can track the level of stock in a prominent way. Moreover, in this, each

inventory item is tagged with a bar code which provides information about when

stock is brought into or moved out from warehouse (Otley and Emmanuel, 2013).

Along with this,there is several othersystems that can be undertaken by Al Sham

Automotive for identifying the level of inventory such as raw partsneedto be

maintained within the firm for ensuring the smooth functioning of operations such as

EOQ, JIT etc. By applying such tools and techniques firm can assess the level or

holding and ordering cost. In this way, by using inventory related tools car

manufacturing company can exert control on cost level to the significant level.

opportunities for expansion. Thus, referring the all such aspects it can be presented

that financial manager role is highly effectual in making monetary decisions.

2. Presenting the most common accounting systems used by organizations

With the motive to attain success over competitors Al Sham Automotive is planning

to undertake MA tools and techniques.The main reason behind this, system of MA furnishes

appropriate information to the managers for planning, controlling and managing the

operations of business. Thus, MA facilitates optimum utilization of resources by eliminating

the waste to a great extent. Hence, MA system that can be undertaken by Al Sham

Automotives are depicted below:

Cost accounting:It implies for the process of recording, classification, recording,

analysis, summarization, allocation as well as evaluation of various alternatives. Cost

accounting is the most effectual system which assists in identifying and advising the

most appropriate action through which financial efficiency as well as capability can

be raised. By employing such system manager can determine cost of product, process

and objects to a great extent (Chenhall and Moers, 2015). Moreover, such system

helps in assessing the cost incurred by Al Sham Automotive for manufacturing one

car. By dividing the total expenses from number of cars manufactured business

organization can determine per unit cost. Thus, by adding the profit margin in per unit

cost Al Sham Automotive can determine price level and becomes able to attain

profitability. Further, such system also helps firm in assessing as well as reporting

cost of inventory and COGS.

Inventory accounting: By using such system business unit can plan or track the

inventory level or associated activities. Thus, by making focus on bar code tracking

system firm can track the level of stock in a prominent way. Moreover, in this, each

inventory item is tagged with a bar code which provides information about when

stock is brought into or moved out from warehouse (Otley and Emmanuel, 2013).

Along with this,there is several othersystems that can be undertaken by Al Sham

Automotive for identifying the level of inventory such as raw partsneedto be

maintained within the firm for ensuring the smooth functioning of operations such as

EOQ, JIT etc. By applying such tools and techniques firm can assess the level or

holding and ordering cost. In this way, by using inventory related tools car

manufacturing company can exert control on cost level to the significant level.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lean accounting: Al Sham Automotive can measure as well as motivate excellent

business practices by employing the system of lean accounting. This system focuses

on the elimination of wastage from the accounting system and makes reporting aspect

faster (Fullerton, Kennedy and Widener, 2014). Moreover, it offers appropriate, timey

and understandable information that manager can use for decision-making purpose.

Lean accounting system renders information about both operational as well as

financial aspects and gives input for strategy development.

3. Assessing the role of management accounting and methods that can be used for the

purpose of reporting

(Source: Management accounting and its importance, 2016)

Now, role of management accounting is increased significantly as compared to the

prior years. The rationale behind this, in the competitive environment firm can get success

only when it reduces the cost and provides customers with quality products or services at

affordable prices. Thus, AL sham Automotivealso needs to employ management accounting

techniques as it has high level of significance in the following way:

Helps in the preparation of plan:Managerial accounting focuses on analysing present

as well as future aspects of business. Thus, it can be presented that management

accounting tools helps in making proper forecast of future (Suomala, Lyly-Yrjänäinen

and Lukka, 2014). This inturn helps in developing highly suitable plan and thereby

assists in gaining competitive edge over others.

Assists in make or buy decision: Field of MA includes discussion regarding the make

or buy decision. For instance: Al Sham Automotive can use MA tools and thereby

identifywhether they should manufacture parts of car in-house or buy from

others.Thus, it can be said that by doing make or buy analysis firm can identify the

activity which in turn helps it in attaining more profit.

business practices by employing the system of lean accounting. This system focuses

on the elimination of wastage from the accounting system and makes reporting aspect

faster (Fullerton, Kennedy and Widener, 2014). Moreover, it offers appropriate, timey

and understandable information that manager can use for decision-making purpose.

Lean accounting system renders information about both operational as well as

financial aspects and gives input for strategy development.

3. Assessing the role of management accounting and methods that can be used for the

purpose of reporting

(Source: Management accounting and its importance, 2016)

Now, role of management accounting is increased significantly as compared to the

prior years. The rationale behind this, in the competitive environment firm can get success

only when it reduces the cost and provides customers with quality products or services at

affordable prices. Thus, AL sham Automotivealso needs to employ management accounting

techniques as it has high level of significance in the following way:

Helps in the preparation of plan:Managerial accounting focuses on analysing present

as well as future aspects of business. Thus, it can be presented that management

accounting tools helps in making proper forecast of future (Suomala, Lyly-Yrjänäinen

and Lukka, 2014). This inturn helps in developing highly suitable plan and thereby

assists in gaining competitive edge over others.

Assists in make or buy decision: Field of MA includes discussion regarding the make

or buy decision. For instance: Al Sham Automotive can use MA tools and thereby

identifywhether they should manufacture parts of car in-house or buy from

others.Thus, it can be said that by doing make or buy analysis firm can identify the

activity which in turn helps it in attaining more profit.

Provides assistance in forecasting cash flow:By applying MA tools Al sham

Automotive can assess the sources from which revenue will be generated by it in the

near future. Along with this, it also helps manager in assessing whether revenue will

increase or decrease in the near future (Management accounting and its importance,

2016). Further, techniques of MA also help in assessing the expenditure which will be

incurred by Al Sham Automotive manufacturing company in the near future. All such

aspects show that system of MA helps in making proper forecast of both inflows as

well as outflows and thereby assists in developing suitable financial plan.

Understanding performance variances:System or techniques of MA provides high

level of assistance in analysing the areas of business unit that demand for

improvement. Thus, analytical techniques of MA help management in relation to

build on positive variance and managing the negative one.

Analysing rate of return: By using the tools of MA, business unit can analyse the

expected return on investment (Fullerton, Kennedy and Widener, 2013). For instance:

Al Sham Automotive can determine BEP point, years needs to cover initial

investment, cash flows etc which are the main aspects for the purpose of decision

making.

Thus, it can be depicted that management accounting system covers wide range of tools

and assists in making decision regarding cost reduction as well as profit planning.

Managerial reports: By preparing the below mentioned reports manager of Al Sham

Automotive can develop competent plan for the upcoming time period such as:

Job costing report:This report is highly prominent because it provides deeper insight

about the company’s profitability on the basis of job.Hence, by using the technique of

job costing Al sham Automotive company can assess the revenue generated through

the performance of each job. In this way, by making comparison of revenue generated

business unit can assess the profitability which is associated with specific job. Thus,

by undertake job costing report manager of concerned manufacturing company can

assess the segment which is highly profitable (Types of Managerial Accounting

Reports, 2017). Further, it also entails the segment which is facing issues and that

needs to be addressed for the attainment of high profit margin. Thus, by using such

report manager of the car company can take strategic decisions and would become

able to run business operations successfully.

Automotive can assess the sources from which revenue will be generated by it in the

near future. Along with this, it also helps manager in assessing whether revenue will

increase or decrease in the near future (Management accounting and its importance,

2016). Further, techniques of MA also help in assessing the expenditure which will be

incurred by Al Sham Automotive manufacturing company in the near future. All such

aspects show that system of MA helps in making proper forecast of both inflows as

well as outflows and thereby assists in developing suitable financial plan.

Understanding performance variances:System or techniques of MA provides high

level of assistance in analysing the areas of business unit that demand for

improvement. Thus, analytical techniques of MA help management in relation to

build on positive variance and managing the negative one.

Analysing rate of return: By using the tools of MA, business unit can analyse the

expected return on investment (Fullerton, Kennedy and Widener, 2013). For instance:

Al Sham Automotive can determine BEP point, years needs to cover initial

investment, cash flows etc which are the main aspects for the purpose of decision

making.

Thus, it can be depicted that management accounting system covers wide range of tools

and assists in making decision regarding cost reduction as well as profit planning.

Managerial reports: By preparing the below mentioned reports manager of Al Sham

Automotive can develop competent plan for the upcoming time period such as:

Job costing report:This report is highly prominent because it provides deeper insight

about the company’s profitability on the basis of job.Hence, by using the technique of

job costing Al sham Automotive company can assess the revenue generated through

the performance of each job. In this way, by making comparison of revenue generated

business unit can assess the profitability which is associated with specific job. Thus,

by undertake job costing report manager of concerned manufacturing company can

assess the segment which is highly profitable (Types of Managerial Accounting

Reports, 2017). Further, it also entails the segment which is facing issues and that

needs to be addressed for the attainment of high profit margin. Thus, by using such

report manager of the car company can take strategic decisions and would become

able to run business operations successfully.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report:In the context of Al Sham Automotive, by undertaking budget report

manager can do analysis of departmental performance and control cost. In addition to

this, by undertaking budget report owners as well as managers can provide personnel

with suitable incentives and enhance their motivational aspect. Hence, for achieving

specific financial goals some of the budgeted amount is given to the employees such

as bonuses.

Operating budget report: It covers information regarding the expected revenue and

expenses pertaining to the specific time period. Operating budget report allows

manager and production supervisors to examine variances by making comparison of

actual performance with standards. This in turn helps manager in making estimation

of monthly profitthrough the comparison of expected sales revenue as well as

expenditure (Williams, 2014). Thus, it can be presented that operating budget is the

most effectual tools which provide assistance in making effectual planning of

expenditure over the time frame.

Accounts receivable aging: This report is critical tool which in turn provides

assistance in managing the cash flow for companies. Moreover, such report entails the

time -period within which firm will recover amount from debtors. It clearly indicates

that customers are able to pay their balances or not. Hence, by making evaluation of

suchaspect Al Sham Automotive can assess that there is a requirement to tighten the

creditpolicies or not.

Hence, it can be stated that management accounting reporting offers highly valuable

information toAl Sham Automotive. By considering such reportsfirm can get necessary

information and take strategic move for running the successful business operations as well as

functions.

4. Explaining the manner in which management accounting is integrated within an

organization

From assessment, it has been identified that management accounting system is highly

integrated within the organization. Moreover, it focuses on each & every department and

thereby helps in developing plan which in turn may result into organizational success.

Standard costing system is one of the main examples of MA that facilitates effectual

judgement (Chenhall and Moers, 2015). Under standard costing system, manager makes

comparison of actual results with the budgeted figures and thereby helps in assessing

deviation. For instance: If selling & distribution expenses of Al sham Automotive is higher

manager can do analysis of departmental performance and control cost. In addition to

this, by undertaking budget report owners as well as managers can provide personnel

with suitable incentives and enhance their motivational aspect. Hence, for achieving

specific financial goals some of the budgeted amount is given to the employees such

as bonuses.

Operating budget report: It covers information regarding the expected revenue and

expenses pertaining to the specific time period. Operating budget report allows

manager and production supervisors to examine variances by making comparison of

actual performance with standards. This in turn helps manager in making estimation

of monthly profitthrough the comparison of expected sales revenue as well as

expenditure (Williams, 2014). Thus, it can be presented that operating budget is the

most effectual tools which provide assistance in making effectual planning of

expenditure over the time frame.

Accounts receivable aging: This report is critical tool which in turn provides

assistance in managing the cash flow for companies. Moreover, such report entails the

time -period within which firm will recover amount from debtors. It clearly indicates

that customers are able to pay their balances or not. Hence, by making evaluation of

suchaspect Al Sham Automotive can assess that there is a requirement to tighten the

creditpolicies or not.

Hence, it can be stated that management accounting reporting offers highly valuable

information toAl Sham Automotive. By considering such reportsfirm can get necessary

information and take strategic move for running the successful business operations as well as

functions.

4. Explaining the manner in which management accounting is integrated within an

organization

From assessment, it has been identified that management accounting system is highly

integrated within the organization. Moreover, it focuses on each & every department and

thereby helps in developing plan which in turn may result into organizational success.

Standard costing system is one of the main examples of MA that facilitates effectual

judgement (Chenhall and Moers, 2015). Under standard costing system, manager makes

comparison of actual results with the budgeted figures and thereby helps in assessing

deviation. For instance: If selling & distribution expenses of Al sham Automotive is higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

than the budgeted amount then manager needs to make efforts in relation to identifying

causes behind the deviations occurred. In this way, strategic move which will be taken by the

firm helps in improving the performance of both sales department and overall organization

(Fullerton, Kennedy and Widener, 2013). Moreover, cost reduction and control is one of the

main motives of business unit. This aspect shows that, standing costing of management

accounting assists in integrating performance within the business unit.

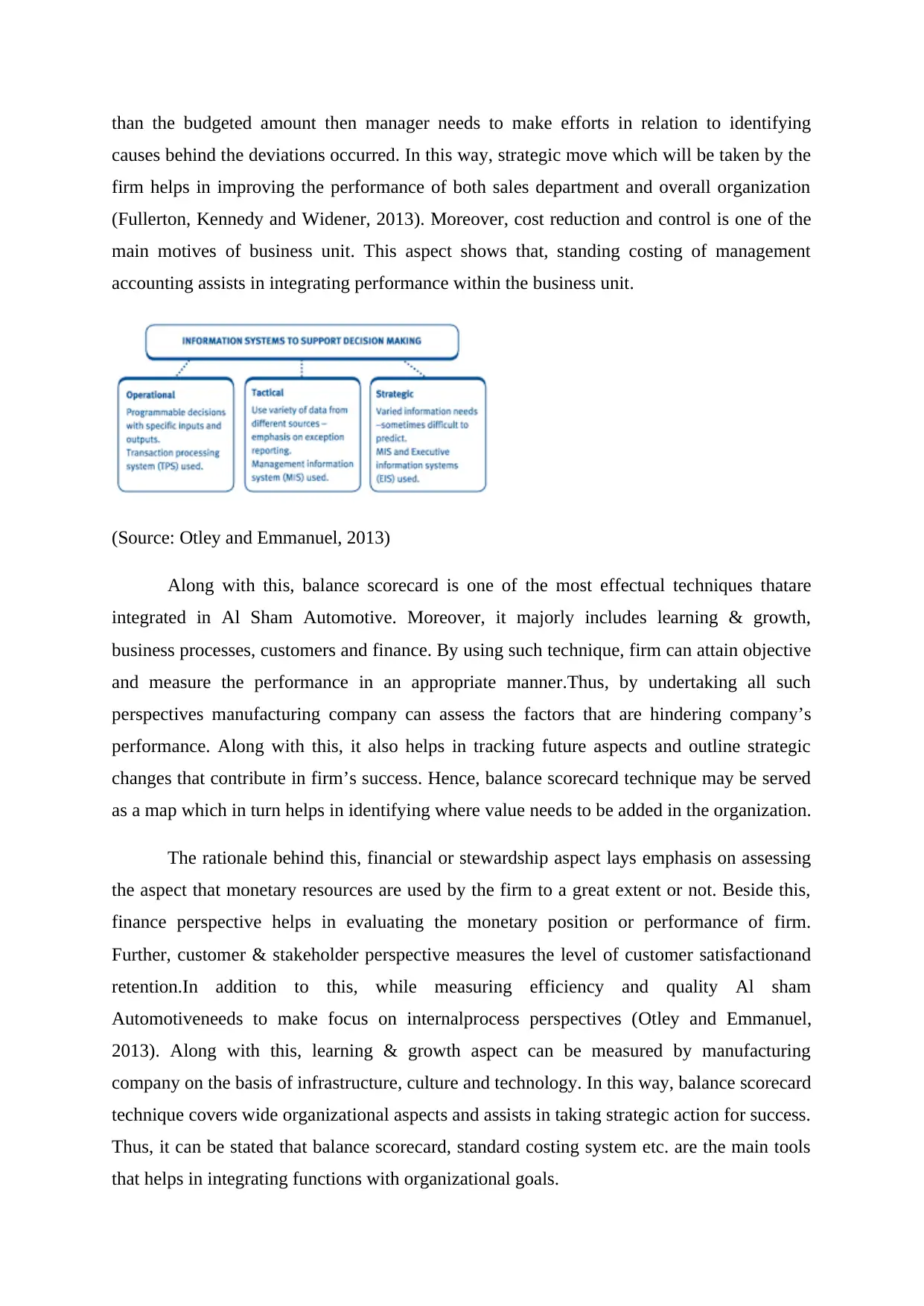

(Source: Otley and Emmanuel, 2013)

Along with this, balance scorecard is one of the most effectual techniques thatare

integrated in Al Sham Automotive. Moreover, it majorly includes learning & growth,

business processes, customers and finance. By using such technique, firm can attain objective

and measure the performance in an appropriate manner.Thus, by undertaking all such

perspectives manufacturing company can assess the factors that are hindering company’s

performance. Along with this, it also helps in tracking future aspects and outline strategic

changes that contribute in firm’s success. Hence, balance scorecard technique may be served

as a map which in turn helps in identifying where value needs to be added in the organization.

The rationale behind this, financial or stewardship aspect lays emphasis on assessing

the aspect that monetary resources are used by the firm to a great extent or not. Beside this,

finance perspective helps in evaluating the monetary position or performance of firm.

Further, customer & stakeholder perspective measures the level of customer satisfactionand

retention.In addition to this, while measuring efficiency and quality Al sham

Automotiveneeds to make focus on internalprocess perspectives (Otley and Emmanuel,

2013). Along with this, learning & growth aspect can be measured by manufacturing

company on the basis of infrastructure, culture and technology. In this way, balance scorecard

technique covers wide organizational aspects and assists in taking strategic action for success.

Thus, it can be stated that balance scorecard, standard costing system etc. are the main tools

that helps in integrating functions with organizational goals.

causes behind the deviations occurred. In this way, strategic move which will be taken by the

firm helps in improving the performance of both sales department and overall organization

(Fullerton, Kennedy and Widener, 2013). Moreover, cost reduction and control is one of the

main motives of business unit. This aspect shows that, standing costing of management

accounting assists in integrating performance within the business unit.

(Source: Otley and Emmanuel, 2013)

Along with this, balance scorecard is one of the most effectual techniques thatare

integrated in Al Sham Automotive. Moreover, it majorly includes learning & growth,

business processes, customers and finance. By using such technique, firm can attain objective

and measure the performance in an appropriate manner.Thus, by undertaking all such

perspectives manufacturing company can assess the factors that are hindering company’s

performance. Along with this, it also helps in tracking future aspects and outline strategic

changes that contribute in firm’s success. Hence, balance scorecard technique may be served

as a map which in turn helps in identifying where value needs to be added in the organization.

The rationale behind this, financial or stewardship aspect lays emphasis on assessing

the aspect that monetary resources are used by the firm to a great extent or not. Beside this,

finance perspective helps in evaluating the monetary position or performance of firm.

Further, customer & stakeholder perspective measures the level of customer satisfactionand

retention.In addition to this, while measuring efficiency and quality Al sham

Automotiveneeds to make focus on internalprocess perspectives (Otley and Emmanuel,

2013). Along with this, learning & growth aspect can be measured by manufacturing

company on the basis of infrastructure, culture and technology. In this way, balance scorecard

technique covers wide organizational aspects and assists in taking strategic action for success.

Thus, it can be stated that balance scorecard, standard costing system etc. are the main tools

that helps in integrating functions with organizational goals.

CONCLUSION

By summing up this report, it has been articulated that principle of management

accounting are highly prominent which in turn helps in preparing suitable reports. Besides

this, it can be inferred that by employing MA tools and techniques Al Sham Automotive can

make forecast of cash flows, cost, profit etc. It can be seen in the report that effectual long

term strategic plan is highly based on budget, job costing and operating budget reports.

Hence, by making assessment of all such reports Al Sham Automotive can take decision for

the near future. Further, it can be summarized that accounting manager carriesout several

responsibilities and assist higher manager in decision making. It can be stated from overall

evaluation that MA methods are highly integrated within the firm and facilitates the

formulation of competent plan. Hence, MA system is highly significant for Al Sham

Automotive which helps in enhancingefficiency, performance and process to a great extent.

REFERENCES

Books and Journals

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47.pp.1-13.

Demski, J., 2013. Managerial uses of accounting information. Springer Science & Business

Media.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and

control practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7). pp.414-428.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research. 31. pp.103-111.

By summing up this report, it has been articulated that principle of management

accounting are highly prominent which in turn helps in preparing suitable reports. Besides

this, it can be inferred that by employing MA tools and techniques Al Sham Automotive can

make forecast of cash flows, cost, profit etc. It can be seen in the report that effectual long

term strategic plan is highly based on budget, job costing and operating budget reports.

Hence, by making assessment of all such reports Al Sham Automotive can take decision for

the near future. Further, it can be summarized that accounting manager carriesout several

responsibilities and assist higher manager in decision making. It can be stated from overall

evaluation that MA methods are highly integrated within the firm and facilitates the

formulation of competent plan. Hence, MA system is highly significant for Al Sham

Automotive which helps in enhancingefficiency, performance and process to a great extent.

REFERENCES

Books and Journals

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47.pp.1-13.

Demski, J., 2013. Managerial uses of accounting information. Springer Science & Business

Media.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and

control practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7). pp.414-428.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research. 31. pp.103-111.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.