Analyzing Alchimist Ltd's Financial Statements and Performance

VerifiedAdded on 2020/01/23

|12

|2622

|220

Report

AI Summary

This report presents a comprehensive financial analysis of Alchimist Ltd, a small private limited company specializing in perfumes, lotions, and candles. The analysis examines the company's Statements of Comprehensive Income (SOCI), Statements of Financial Position (SOFP), and Statements of Cash Flow (SOCF) for the year 2015, focusing on revenue trends, profitability, and cash flow management. The report delves into the impact of new online stores and hotel chain contracts on revenue, the interpretation of key financial ratios like gross profit and net profit, and the implications of non-current assets and Redstone's proposed investment. Furthermore, it discusses the impact of out-of-fashion products on financial statements, the reasons behind negative cash flow from operating activities, and the calculation of relevant ratios. The report concludes with a professional assessment for Redstone's board of directors, recommending an investment based on Alchimist's sound financial performance.

UNDERSTANDING

FINANCIAL

STATEMENTS

FINANCIAL

STATEMENTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

QUESTION 1 Features of Alchmists's financial statements......................................................1

a) Secure long term debt and hired administrator to oversee and co-ordinate the contract...1

b) Linkage between three primary financial statements........................................................1

c) Fashionable and out of fashion products...........................................................................2

QUESTION 2 Interpretation of SOCI........................................................................................2

a) Revenue.............................................................................................................................2

b) Gross profit (GP)...............................................................................................................5

c) Other SOCI's costs.............................................................................................................5

d) Net profit (NP)..................................................................................................................6

QUESTION 3 Interpretation of Alchimist's SOFP....................................................................7

a) Non-current assets.............................................................................................................7

b) Redstone proposed investment..........................................................................................8

QUESTION 4 Interpretation of SOCF.......................................................................................8

a) Three reasons for negative cash flow from operating activities........................................8

b) Two ratios from SOCF......................................................................................................8

QUESTION 5 Professional report..............................................................................................9

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................10

Illustration Index

Illustration 1: Movement in total revenues.................................................................................3

Illustration 2: Revenue movement of retail operations .............................................................4

Illustration 3: Segmental revenues in the year 2015..................................................................4

Illustration 4: Trend line for distribution and transportation costs.............................................6

Illustration 5: Trend line for Royalties.......................................................................................6

INTRODUCTION......................................................................................................................1

QUESTION 1 Features of Alchmists's financial statements......................................................1

a) Secure long term debt and hired administrator to oversee and co-ordinate the contract...1

b) Linkage between three primary financial statements........................................................1

c) Fashionable and out of fashion products...........................................................................2

QUESTION 2 Interpretation of SOCI........................................................................................2

a) Revenue.............................................................................................................................2

b) Gross profit (GP)...............................................................................................................5

c) Other SOCI's costs.............................................................................................................5

d) Net profit (NP)..................................................................................................................6

QUESTION 3 Interpretation of Alchimist's SOFP....................................................................7

a) Non-current assets.............................................................................................................7

b) Redstone proposed investment..........................................................................................8

QUESTION 4 Interpretation of SOCF.......................................................................................8

a) Three reasons for negative cash flow from operating activities........................................8

b) Two ratios from SOCF......................................................................................................8

QUESTION 5 Professional report..............................................................................................9

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................10

Illustration Index

Illustration 1: Movement in total revenues.................................................................................3

Illustration 2: Revenue movement of retail operations .............................................................4

Illustration 3: Segmental revenues in the year 2015..................................................................4

Illustration 4: Trend line for distribution and transportation costs.............................................6

Illustration 5: Trend line for Royalties.......................................................................................6

INTRODUCTION

Alchimist Ltd, is a small sized private limited company that manufactures and sell its

own branded perfumes, lotions and candles to the public and to other large retail companies.

In the year 2015, it developed on-line stores and hotel chain contracts to enlarge its revenues

and profitability as well. The present report will helps us to determine the financial

performance of the firm through evaluation and examination of its financial statements.

QUESTION 1 FEATURES OF ALCHMISTS'S FINANCIAL

STATEMENTS

a) Secure long term debt and hired administrator to oversee and co-ordinate the contract

(1). Relationship of the description with SOCI and SOFP

1st description is related to SOFP because in this, it has been said that Alchimist is

able to secure long term bank funding. While, other description is linked with SOCI because

administrator has been hired to oversee and co-ordinate the contract with the company's

management.

(2). Allocation of both the transactions

1st Statement can be related to the long term borrowings of £412 which tells that firm

is able to take additional borrowings through bank. While, 2nd description is related to the

administration expenses in SOCI. It comprises employee expenses that are providing services

within and outside UK.

b) Linkage between three primary financial statements

Alchimist's SOCI feeds into the SOFP

From the SOCI, Alchimist's net profit of £405 and £227 has been transferred into

SOFP as retained earnings. With this, total invested share capital has been affected.

Alchimist's SOFP feeds into the SOCF

From the SOFP, difference between current assets such as receivables, inventories

and difference in current liabilities such as payables has been recorded in Alchimist's SOCF

under operating activities (Khan and Bradbury, 2014). Moreover, purchase and sales of fixed

assets such as PPE and investment in new product development has been reported a investing

activities. However, purchase and sales of debt and equity has been recorded into financing

activities.

Alchimist's SOCI feeds into the SOCF

Alchimist Ltd, is a small sized private limited company that manufactures and sell its

own branded perfumes, lotions and candles to the public and to other large retail companies.

In the year 2015, it developed on-line stores and hotel chain contracts to enlarge its revenues

and profitability as well. The present report will helps us to determine the financial

performance of the firm through evaluation and examination of its financial statements.

QUESTION 1 FEATURES OF ALCHMISTS'S FINANCIAL

STATEMENTS

a) Secure long term debt and hired administrator to oversee and co-ordinate the contract

(1). Relationship of the description with SOCI and SOFP

1st description is related to SOFP because in this, it has been said that Alchimist is

able to secure long term bank funding. While, other description is linked with SOCI because

administrator has been hired to oversee and co-ordinate the contract with the company's

management.

(2). Allocation of both the transactions

1st Statement can be related to the long term borrowings of £412 which tells that firm

is able to take additional borrowings through bank. While, 2nd description is related to the

administration expenses in SOCI. It comprises employee expenses that are providing services

within and outside UK.

b) Linkage between three primary financial statements

Alchimist's SOCI feeds into the SOFP

From the SOCI, Alchimist's net profit of £405 and £227 has been transferred into

SOFP as retained earnings. With this, total invested share capital has been affected.

Alchimist's SOFP feeds into the SOCF

From the SOFP, difference between current assets such as receivables, inventories

and difference in current liabilities such as payables has been recorded in Alchimist's SOCF

under operating activities (Khan and Bradbury, 2014). Moreover, purchase and sales of fixed

assets such as PPE and investment in new product development has been reported a investing

activities. However, purchase and sales of debt and equity has been recorded into financing

activities.

Alchimist's SOCI feeds into the SOCF

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the SOCI, payment in terms of income tax, interest and dividend has been

recorded into SOCF under operating activities. Moreover, non cash affecting transactions

also have been adjusted in operating activities of SOCF such as depreciation worth £52 and

£40 in 2014 and 2015.

c) Fashionable and out of fashion products

IAS 2 for inventory valuation

According to IAS 2, inventory should be recognized at costs or net realisable value,

which ever is lower (Brochet, Jagolinzer and Riedl, 2013.).

Recognition criteria in the regulatory framework

As per this, inventory costs accumulates purchasing cost, conversion cost and other

expenses incurred in bringing goods to their selling conditions. However, net realisable value

refers to expected revenues that can be earned through selling the inventory.

Impact of out of fashion products on SOCI and SOFP

Products that had gone out of fashion will be recognised at net realisable value.

Hence, it will reduce Alchimist's profit in SOCI and closing inventory in SOFP results in

lowering current assets.

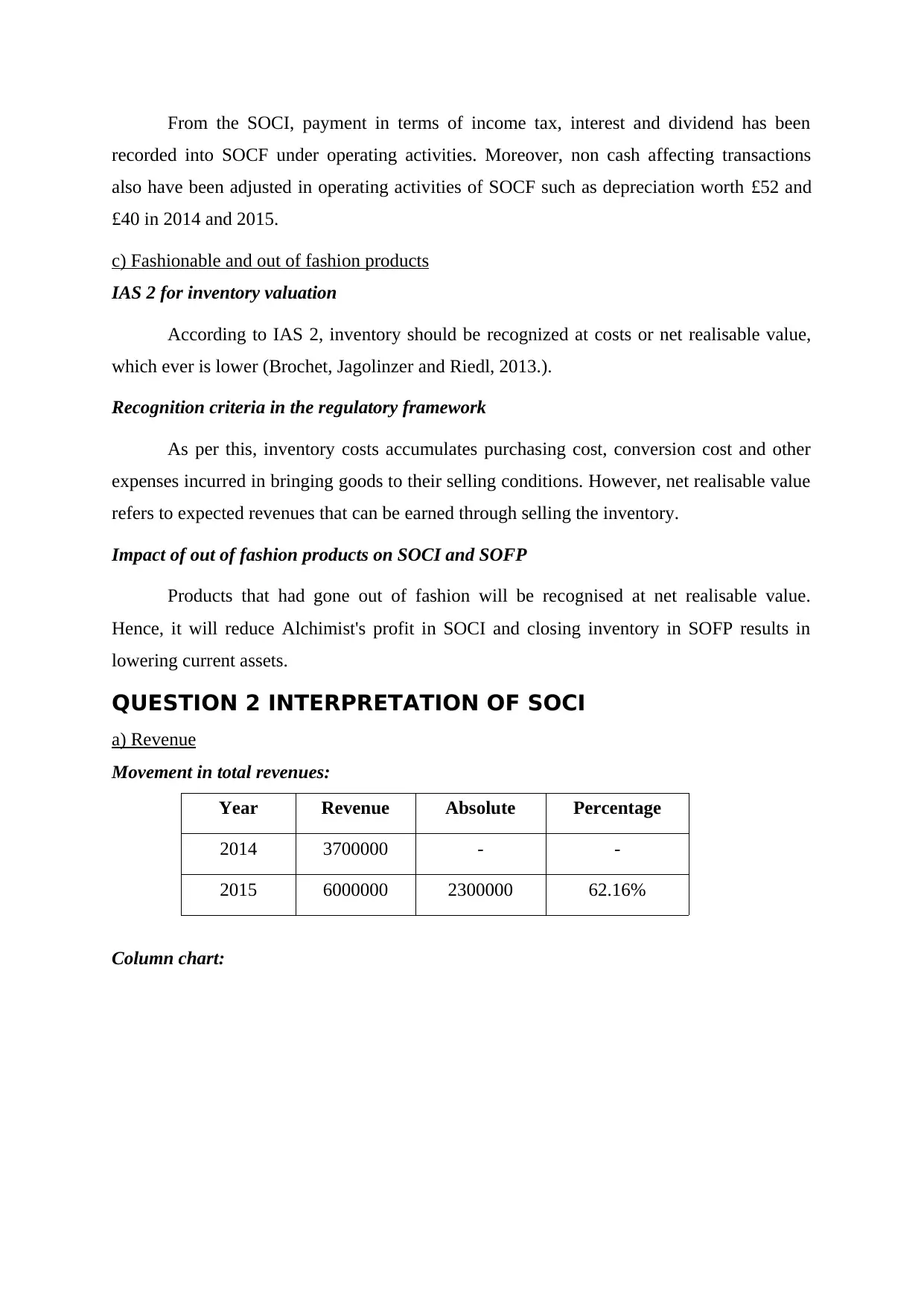

QUESTION 2 INTERPRETATION OF SOCI

a) Revenue

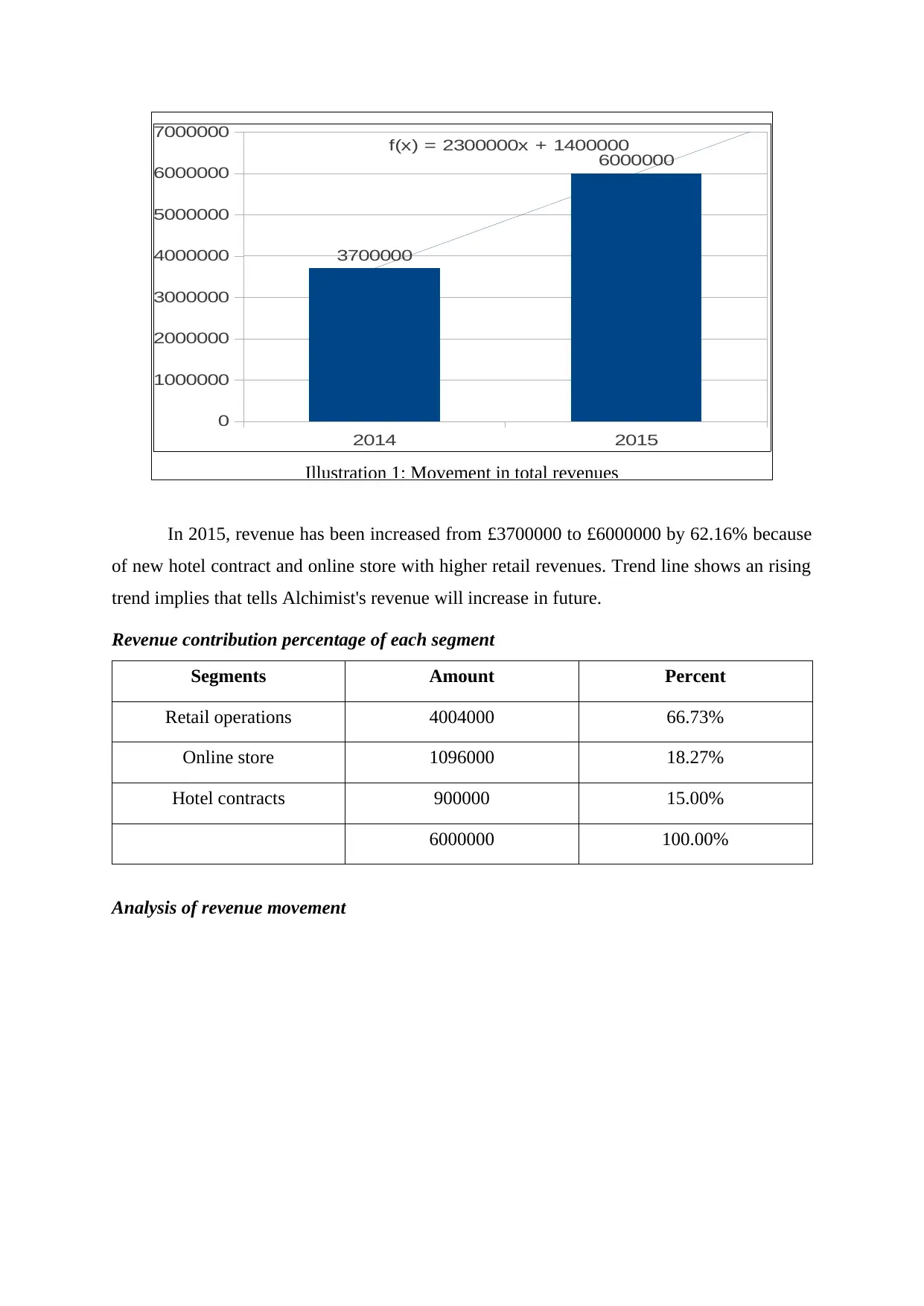

Movement in total revenues:

Year Revenue Absolute Percentage

2014 3700000 - -

2015 6000000 2300000 62.16%

Column chart:

recorded into SOCF under operating activities. Moreover, non cash affecting transactions

also have been adjusted in operating activities of SOCF such as depreciation worth £52 and

£40 in 2014 and 2015.

c) Fashionable and out of fashion products

IAS 2 for inventory valuation

According to IAS 2, inventory should be recognized at costs or net realisable value,

which ever is lower (Brochet, Jagolinzer and Riedl, 2013.).

Recognition criteria in the regulatory framework

As per this, inventory costs accumulates purchasing cost, conversion cost and other

expenses incurred in bringing goods to their selling conditions. However, net realisable value

refers to expected revenues that can be earned through selling the inventory.

Impact of out of fashion products on SOCI and SOFP

Products that had gone out of fashion will be recognised at net realisable value.

Hence, it will reduce Alchimist's profit in SOCI and closing inventory in SOFP results in

lowering current assets.

QUESTION 2 INTERPRETATION OF SOCI

a) Revenue

Movement in total revenues:

Year Revenue Absolute Percentage

2014 3700000 - -

2015 6000000 2300000 62.16%

Column chart:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In 2015, revenue has been increased from £3700000 to £6000000 by 62.16% because

of new hotel contract and online store with higher retail revenues. Trend line shows an rising

trend implies that tells Alchimist's revenue will increase in future.

Revenue contribution percentage of each segment

Segments Amount Percent

Retail operations 4004000 66.73%

Online store 1096000 18.27%

Hotel contracts 900000 15.00%

6000000 100.00%

Analysis of revenue movement

2014 2015

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

3700000

6000000

f(x) = 2300000x + 1400000

Illustration 1: Movement in total revenues

of new hotel contract and online store with higher retail revenues. Trend line shows an rising

trend implies that tells Alchimist's revenue will increase in future.

Revenue contribution percentage of each segment

Segments Amount Percent

Retail operations 4004000 66.73%

Online store 1096000 18.27%

Hotel contracts 900000 15.00%

6000000 100.00%

Analysis of revenue movement

2014 2015

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

3700000

6000000

f(x) = 2300000x + 1400000

Illustration 1: Movement in total revenues

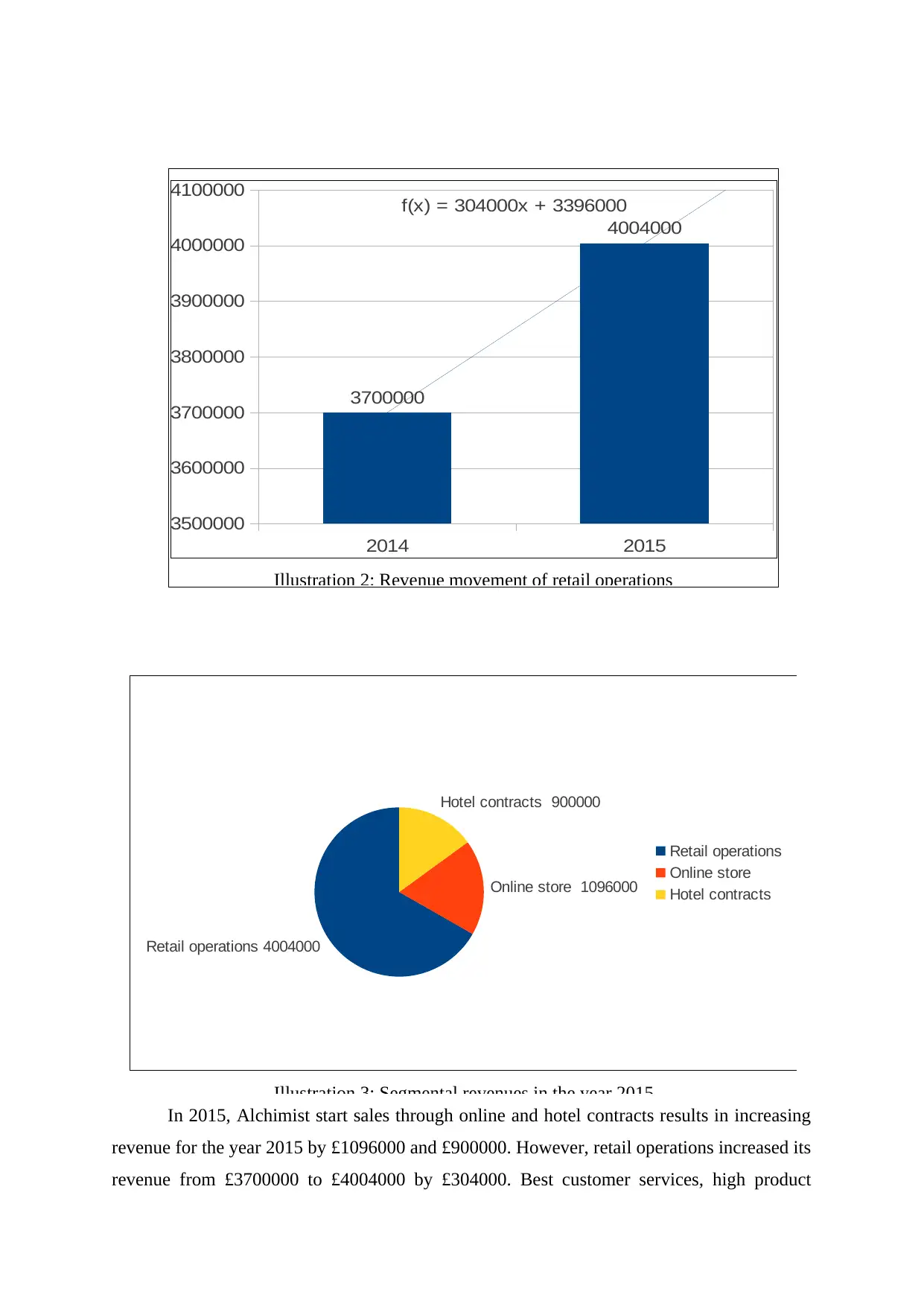

In 2015, Alchimist start sales through online and hotel contracts results in increasing

revenue for the year 2015 by £1096000 and £900000. However, retail operations increased its

revenue from £3700000 to £4004000 by £304000. Best customer services, high product

2014 2015

3500000

3600000

3700000

3800000

3900000

4000000

4100000

3700000

4004000

f(x) = 304000x + 3396000

Illustration 2: Revenue movement of retail operations

Retail operations 4004000

Online store 1096000

Hotel contracts 900000

Retail operations

Online store

Hotel contracts

Illustration 3: Segmental revenues in the year 2015

revenue for the year 2015 by £1096000 and £900000. However, retail operations increased its

revenue from £3700000 to £4004000 by £304000. Best customer services, high product

2014 2015

3500000

3600000

3700000

3800000

3900000

4000000

4100000

3700000

4004000

f(x) = 304000x + 3396000

Illustration 2: Revenue movement of retail operations

Retail operations 4004000

Online store 1096000

Hotel contracts 900000

Retail operations

Online store

Hotel contracts

Illustration 3: Segmental revenues in the year 2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

price, high customer demand and higher units sales may be the reason behind inclined

revenues (Petersen and Plenborg, 2010).

Additional information

Additional information such as gearing ratio and interest coverage ratio will also be

useful to determine the level of risk associated with Redstone's potential investment.

Moreover, ROCE and dividend rate also helps to determine Alchimist's ability to earn return

on invested capital. It helps to determine the expected earnings on Redstone's investment.

b) Gross profit (GP)

Meaning

It tells that how much amount Alchimist has earned on its total revenue through its

mark-up (Delen, Kuzey and Uyar, 2013). Further, it tells the percentage difference between

cost of sales and sales on Alchimist's total revenue.

Segmental GP ratio

Gross profit ratio = Gross profit/Total revenues*100

Hotel contract's GP

It is too much higher than other segments because of product branding which enable

sales directors to sell the product at premium prices. One example is Tincture product that

cost is £35 and normally sold at £50 but due to Badngolo logo, it has been sold at £62.

c) Other SOCI's costs

Cost of sales and overheads

Cost of sales combines all the expenses that directly can be allocated to product such

as purchase, carriage inward, octroi, import duty etc (Schoenebeck and Holtzman, 2013).

While, overhead comprises all the indirect expenses that are not directly related to the

products such as office expense and distribution costs.

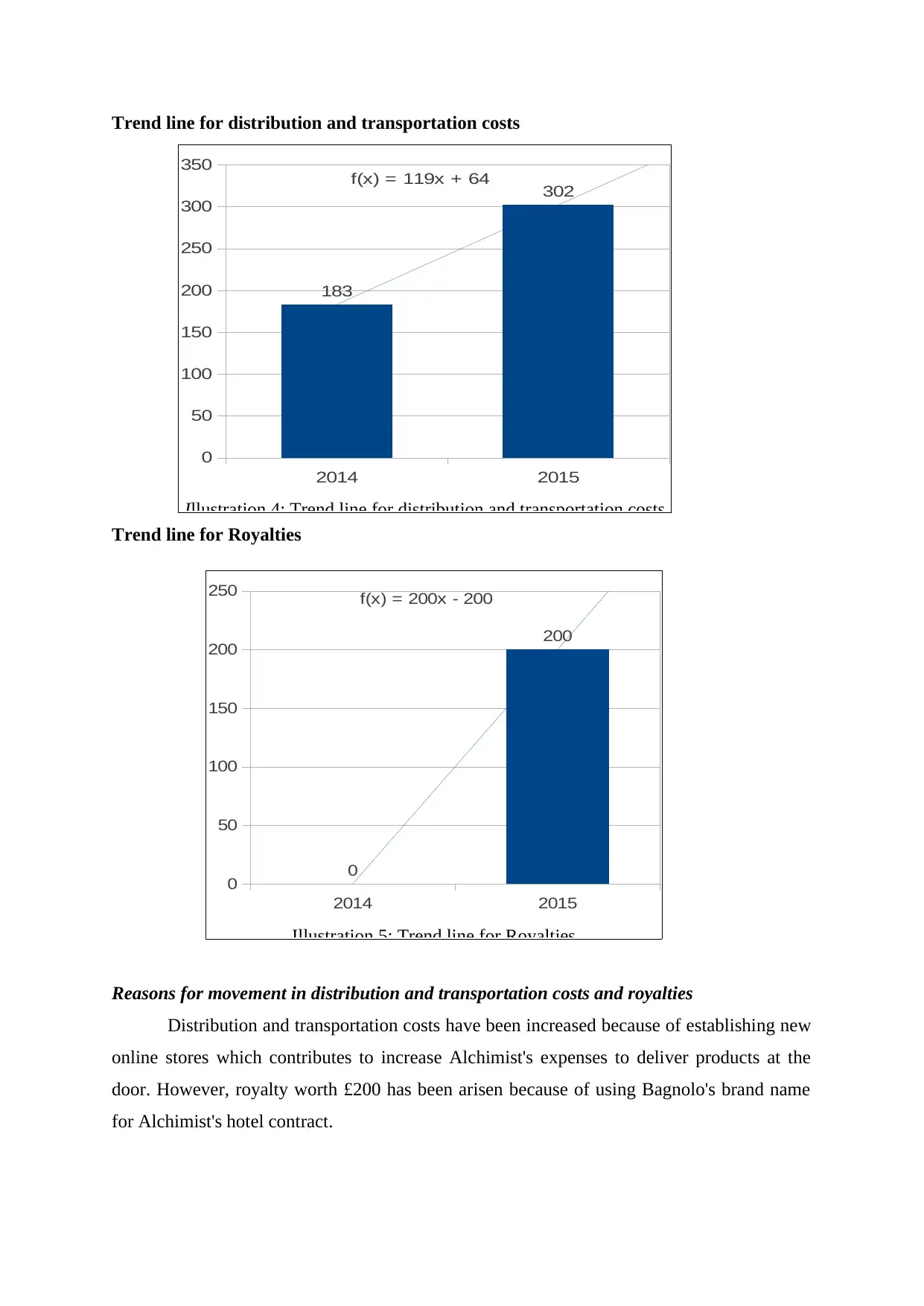

Distribution and transportation costs and royalty costs

revenues (Petersen and Plenborg, 2010).

Additional information

Additional information such as gearing ratio and interest coverage ratio will also be

useful to determine the level of risk associated with Redstone's potential investment.

Moreover, ROCE and dividend rate also helps to determine Alchimist's ability to earn return

on invested capital. It helps to determine the expected earnings on Redstone's investment.

b) Gross profit (GP)

Meaning

It tells that how much amount Alchimist has earned on its total revenue through its

mark-up (Delen, Kuzey and Uyar, 2013). Further, it tells the percentage difference between

cost of sales and sales on Alchimist's total revenue.

Segmental GP ratio

Gross profit ratio = Gross profit/Total revenues*100

Hotel contract's GP

It is too much higher than other segments because of product branding which enable

sales directors to sell the product at premium prices. One example is Tincture product that

cost is £35 and normally sold at £50 but due to Badngolo logo, it has been sold at £62.

c) Other SOCI's costs

Cost of sales and overheads

Cost of sales combines all the expenses that directly can be allocated to product such

as purchase, carriage inward, octroi, import duty etc (Schoenebeck and Holtzman, 2013).

While, overhead comprises all the indirect expenses that are not directly related to the

products such as office expense and distribution costs.

Distribution and transportation costs and royalty costs

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trend line for distribution and transportation costs

Trend line for Royalties

Reasons for movement in distribution and transportation costs and royalties

Distribution and transportation costs have been increased because of establishing new

online stores which contributes to increase Alchimist's expenses to deliver products at the

door. However, royalty worth £200 has been arisen because of using Bagnolo's brand name

for Alchimist's hotel contract.

2014 2015

0

50

100

150

200

250

300

350

183

302

f(x) = 119x + 64

Illustration 4: Trend line for distribution and transportation costs

2014 2015

0

50

100

150

200

250

0

200

f(x) = 200x - 200

Illustration 5: Trend line for Royalties

Trend line for Royalties

Reasons for movement in distribution and transportation costs and royalties

Distribution and transportation costs have been increased because of establishing new

online stores which contributes to increase Alchimist's expenses to deliver products at the

door. However, royalty worth £200 has been arisen because of using Bagnolo's brand name

for Alchimist's hotel contract.

2014 2015

0

50

100

150

200

250

300

350

183

302

f(x) = 119x + 64

Illustration 4: Trend line for distribution and transportation costs

2014 2015

0

50

100

150

200

250

0

200

f(x) = 200x - 200

Illustration 5: Trend line for Royalties

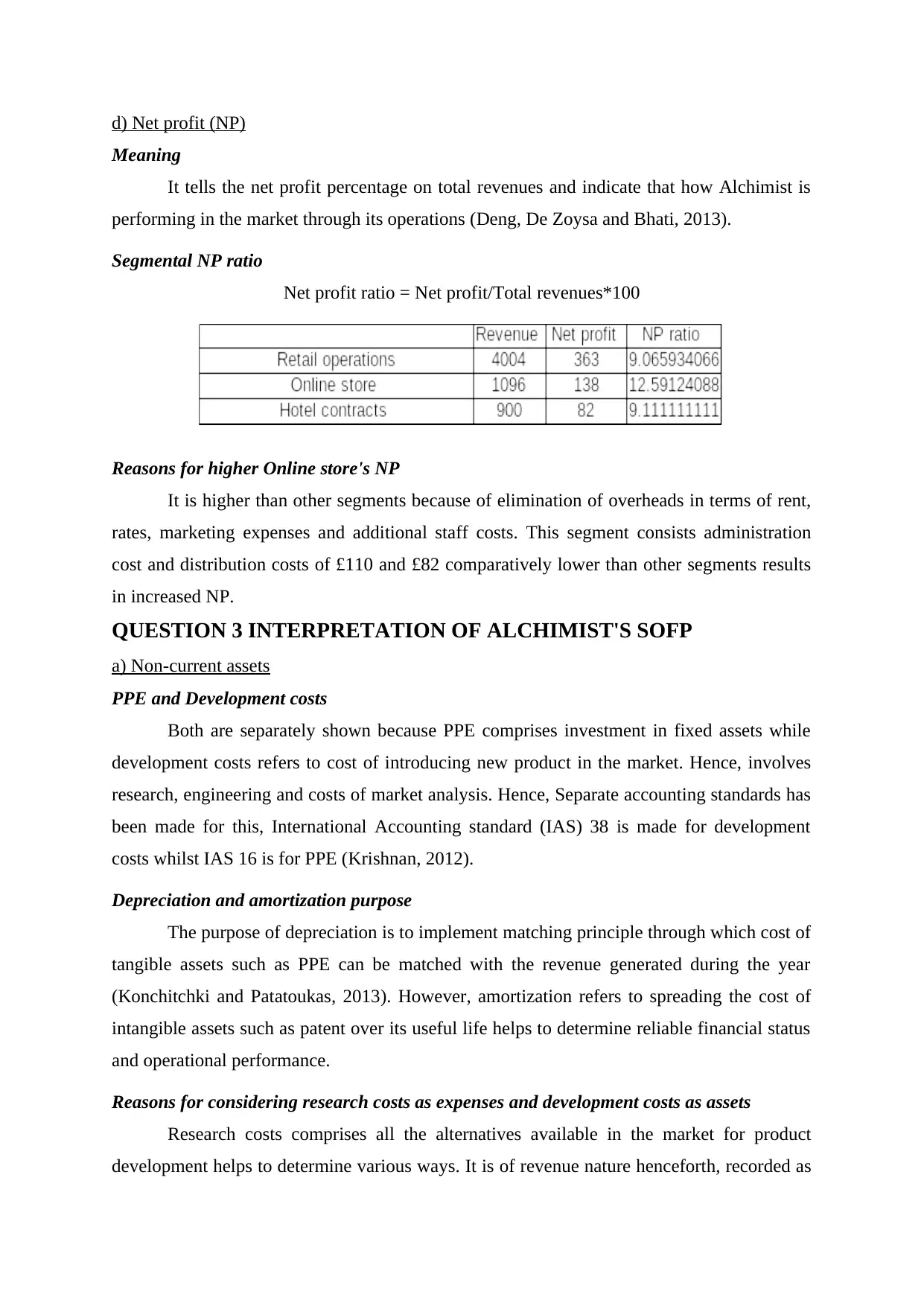

d) Net profit (NP)

Meaning

It tells the net profit percentage on total revenues and indicate that how Alchimist is

performing in the market through its operations (Deng, De Zoysa and Bhati, 2013).

Segmental NP ratio

Net profit ratio = Net profit/Total revenues*100

Reasons for higher Online store's NP

It is higher than other segments because of elimination of overheads in terms of rent,

rates, marketing expenses and additional staff costs. This segment consists administration

cost and distribution costs of £110 and £82 comparatively lower than other segments results

in increased NP.

QUESTION 3 INTERPRETATION OF ALCHIMIST'S SOFP

a) Non-current assets

PPE and Development costs

Both are separately shown because PPE comprises investment in fixed assets while

development costs refers to cost of introducing new product in the market. Hence, involves

research, engineering and costs of market analysis. Hence, Separate accounting standards has

been made for this, International Accounting standard (IAS) 38 is made for development

costs whilst IAS 16 is for PPE (Krishnan, 2012).

Depreciation and amortization purpose

The purpose of depreciation is to implement matching principle through which cost of

tangible assets such as PPE can be matched with the revenue generated during the year

(Konchitchki and Patatoukas, 2013). However, amortization refers to spreading the cost of

intangible assets such as patent over its useful life helps to determine reliable financial status

and operational performance.

Reasons for considering research costs as expenses and development costs as assets

Research costs comprises all the alternatives available in the market for product

development helps to determine various ways. It is of revenue nature henceforth, recorded as

Meaning

It tells the net profit percentage on total revenues and indicate that how Alchimist is

performing in the market through its operations (Deng, De Zoysa and Bhati, 2013).

Segmental NP ratio

Net profit ratio = Net profit/Total revenues*100

Reasons for higher Online store's NP

It is higher than other segments because of elimination of overheads in terms of rent,

rates, marketing expenses and additional staff costs. This segment consists administration

cost and distribution costs of £110 and £82 comparatively lower than other segments results

in increased NP.

QUESTION 3 INTERPRETATION OF ALCHIMIST'S SOFP

a) Non-current assets

PPE and Development costs

Both are separately shown because PPE comprises investment in fixed assets while

development costs refers to cost of introducing new product in the market. Hence, involves

research, engineering and costs of market analysis. Hence, Separate accounting standards has

been made for this, International Accounting standard (IAS) 38 is made for development

costs whilst IAS 16 is for PPE (Krishnan, 2012).

Depreciation and amortization purpose

The purpose of depreciation is to implement matching principle through which cost of

tangible assets such as PPE can be matched with the revenue generated during the year

(Konchitchki and Patatoukas, 2013). However, amortization refers to spreading the cost of

intangible assets such as patent over its useful life helps to determine reliable financial status

and operational performance.

Reasons for considering research costs as expenses and development costs as assets

Research costs comprises all the alternatives available in the market for product

development helps to determine various ways. It is of revenue nature henceforth, recorded as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses in SOCI (Hodder, Hopkins and Wood, 2008). However, development costs includes

expenditure for developing new product henceforth, it is of capital nature and recorded as

assets.

b) Redstone proposed investment

Impact on SOFP due to wholly cash investment and used to pay overdraft

It will increase share capital by £500000 and will reach to £1050000.

It will increase cash balance by net amount of £432 (£500-£68) and will reach at

£432. It will reduce bank overdraft by £68 and will reach at Zero.

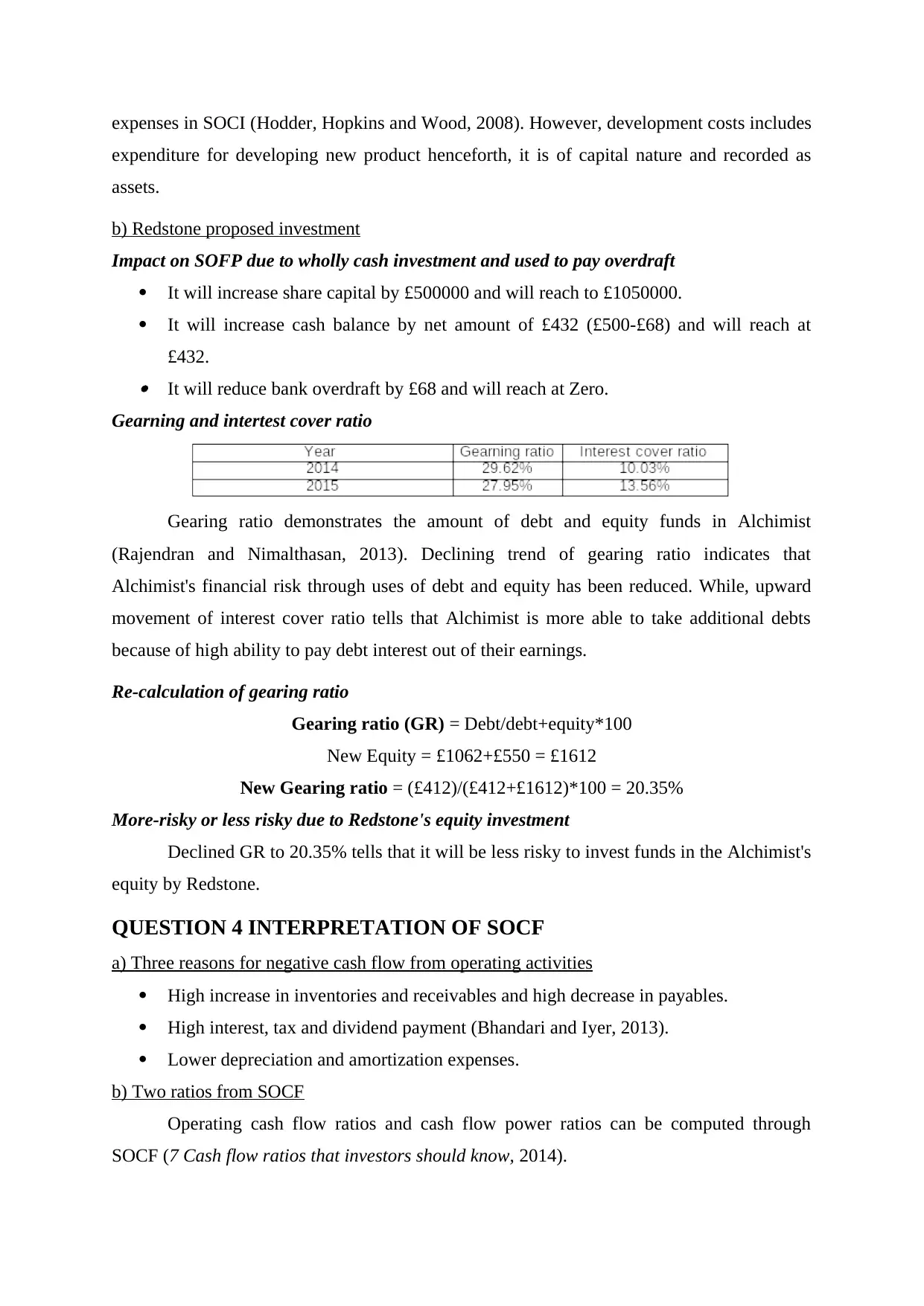

Gearning and intertest cover ratio

Gearing ratio demonstrates the amount of debt and equity funds in Alchimist

(Rajendran and Nimalthasan, 2013). Declining trend of gearing ratio indicates that

Alchimist's financial risk through uses of debt and equity has been reduced. While, upward

movement of interest cover ratio tells that Alchimist is more able to take additional debts

because of high ability to pay debt interest out of their earnings.

Re-calculation of gearing ratio

Gearing ratio (GR) = Debt/debt+equity*100

New Equity = £1062+£550 = £1612

New Gearing ratio = (£412)/(£412+£1612)*100 = 20.35%

More-risky or less risky due to Redstone's equity investment

Declined GR to 20.35% tells that it will be less risky to invest funds in the Alchimist's

equity by Redstone.

QUESTION 4 INTERPRETATION OF SOCF

a) Three reasons for negative cash flow from operating activities

High increase in inventories and receivables and high decrease in payables.

High interest, tax and dividend payment (Bhandari and Iyer, 2013).

Lower depreciation and amortization expenses.

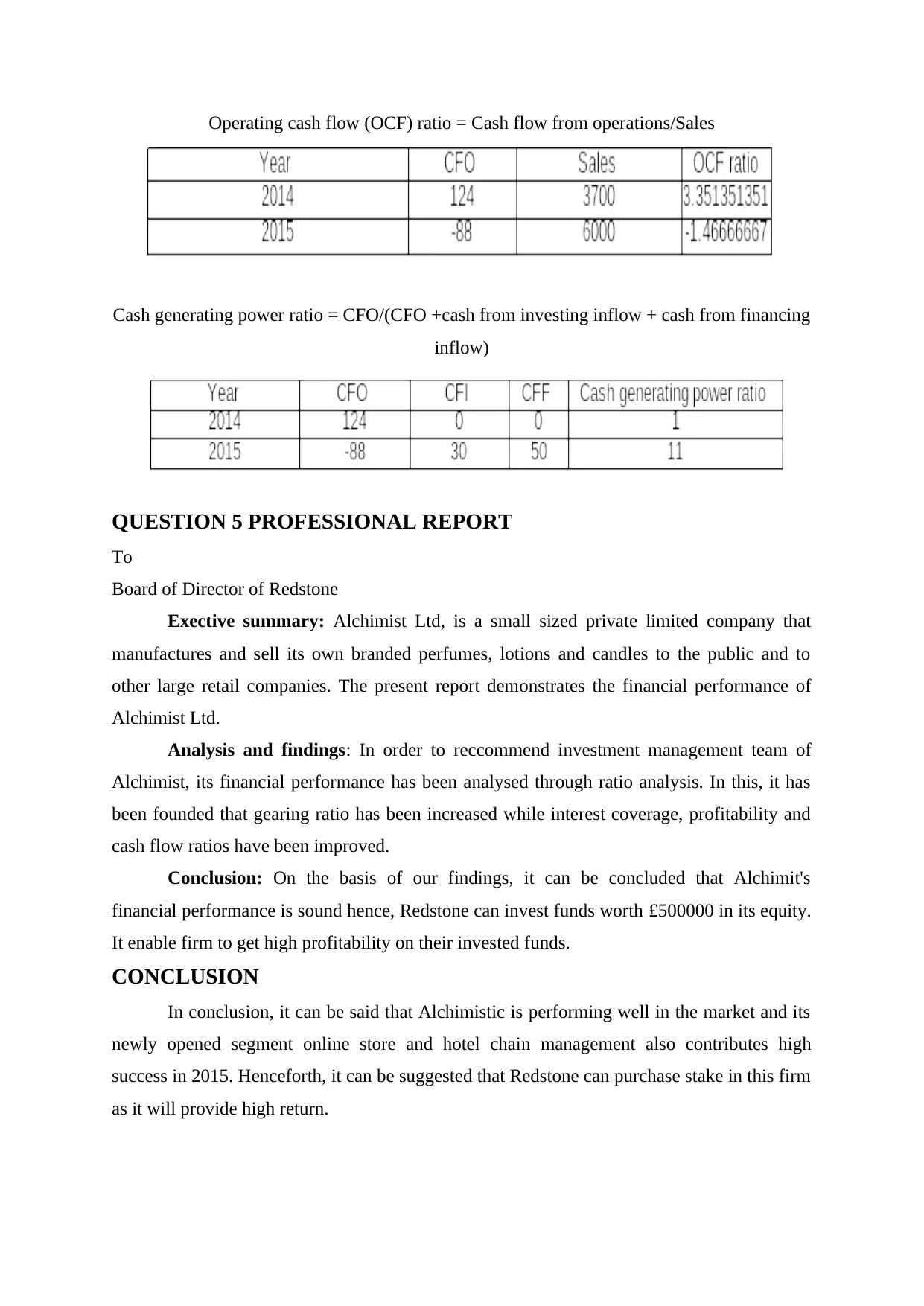

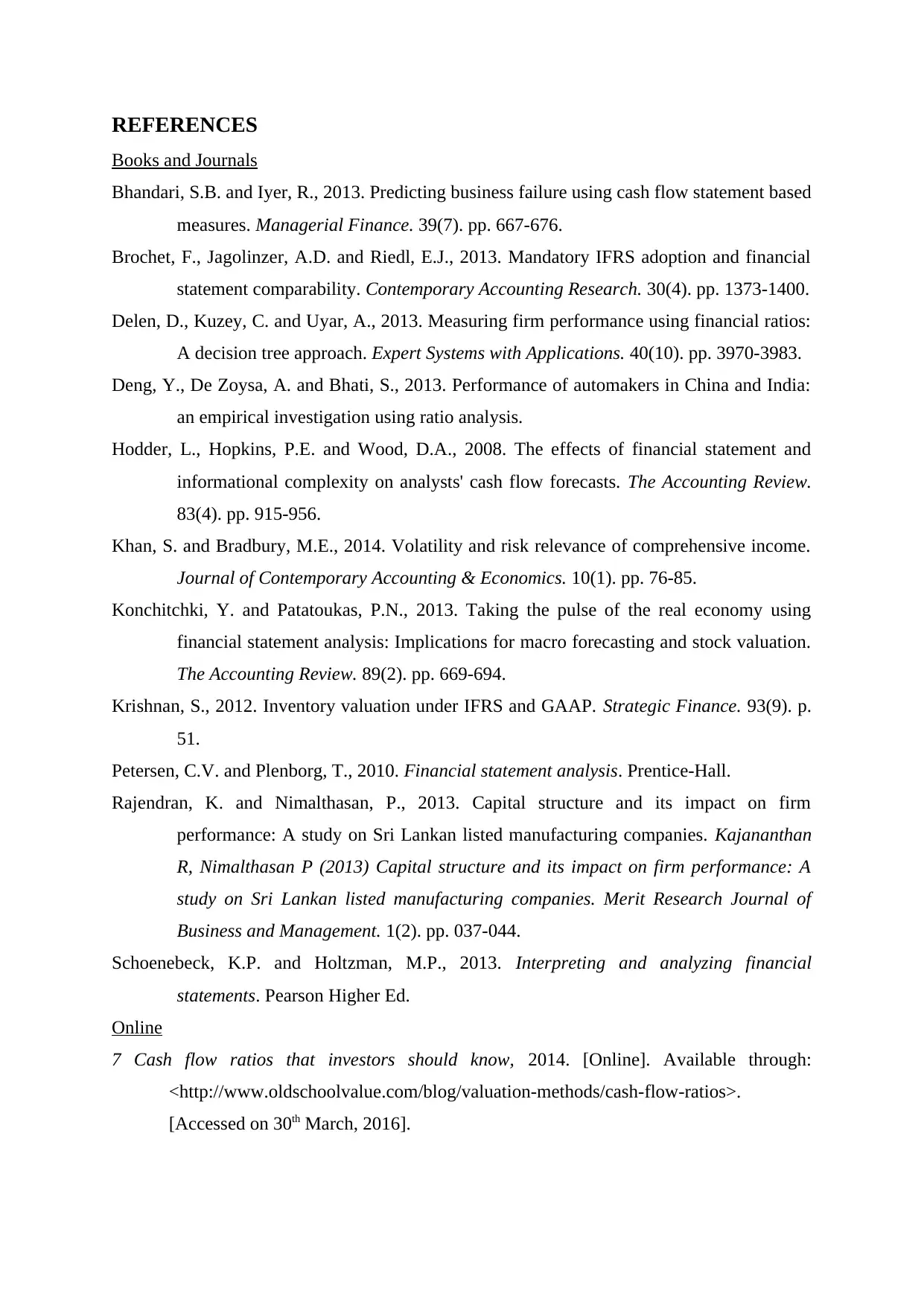

b) Two ratios from SOCF

Operating cash flow ratios and cash flow power ratios can be computed through

SOCF (7 Cash flow ratios that investors should know, 2014).

expenditure for developing new product henceforth, it is of capital nature and recorded as

assets.

b) Redstone proposed investment

Impact on SOFP due to wholly cash investment and used to pay overdraft

It will increase share capital by £500000 and will reach to £1050000.

It will increase cash balance by net amount of £432 (£500-£68) and will reach at

£432. It will reduce bank overdraft by £68 and will reach at Zero.

Gearning and intertest cover ratio

Gearing ratio demonstrates the amount of debt and equity funds in Alchimist

(Rajendran and Nimalthasan, 2013). Declining trend of gearing ratio indicates that

Alchimist's financial risk through uses of debt and equity has been reduced. While, upward

movement of interest cover ratio tells that Alchimist is more able to take additional debts

because of high ability to pay debt interest out of their earnings.

Re-calculation of gearing ratio

Gearing ratio (GR) = Debt/debt+equity*100

New Equity = £1062+£550 = £1612

New Gearing ratio = (£412)/(£412+£1612)*100 = 20.35%

More-risky or less risky due to Redstone's equity investment

Declined GR to 20.35% tells that it will be less risky to invest funds in the Alchimist's

equity by Redstone.

QUESTION 4 INTERPRETATION OF SOCF

a) Three reasons for negative cash flow from operating activities

High increase in inventories and receivables and high decrease in payables.

High interest, tax and dividend payment (Bhandari and Iyer, 2013).

Lower depreciation and amortization expenses.

b) Two ratios from SOCF

Operating cash flow ratios and cash flow power ratios can be computed through

SOCF (7 Cash flow ratios that investors should know, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating cash flow (OCF) ratio = Cash flow from operations/Sales

Cash generating power ratio = CFO/(CFO +cash from investing inflow + cash from financing

inflow)

QUESTION 5 PROFESSIONAL REPORT

To

Board of Director of Redstone

Exective summary: Alchimist Ltd, is a small sized private limited company that

manufactures and sell its own branded perfumes, lotions and candles to the public and to

other large retail companies. The present report demonstrates the financial performance of

Alchimist Ltd.

Analysis and findings: In order to reccommend investment management team of

Alchimist, its financial performance has been analysed through ratio analysis. In this, it has

been founded that gearing ratio has been increased while interest coverage, profitability and

cash flow ratios have been improved.

Conclusion: On the basis of our findings, it can be concluded that Alchimit's

financial performance is sound hence, Redstone can invest funds worth £500000 in its equity.

It enable firm to get high profitability on their invested funds.

CONCLUSION

In conclusion, it can be said that Alchimistic is performing well in the market and its

newly opened segment online store and hotel chain management also contributes high

success in 2015. Henceforth, it can be suggested that Redstone can purchase stake in this firm

as it will provide high return.

Cash generating power ratio = CFO/(CFO +cash from investing inflow + cash from financing

inflow)

QUESTION 5 PROFESSIONAL REPORT

To

Board of Director of Redstone

Exective summary: Alchimist Ltd, is a small sized private limited company that

manufactures and sell its own branded perfumes, lotions and candles to the public and to

other large retail companies. The present report demonstrates the financial performance of

Alchimist Ltd.

Analysis and findings: In order to reccommend investment management team of

Alchimist, its financial performance has been analysed through ratio analysis. In this, it has

been founded that gearing ratio has been increased while interest coverage, profitability and

cash flow ratios have been improved.

Conclusion: On the basis of our findings, it can be concluded that Alchimit's

financial performance is sound hence, Redstone can invest funds worth £500000 in its equity.

It enable firm to get high profitability on their invested funds.

CONCLUSION

In conclusion, it can be said that Alchimistic is performing well in the market and its

newly opened segment online store and hotel chain management also contributes high

success in 2015. Henceforth, it can be suggested that Redstone can purchase stake in this firm

as it will provide high return.

REFERENCES

Books and Journals

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance. 39(7). pp. 667-676.

Brochet, F., Jagolinzer, A.D. and Riedl, E.J., 2013. Mandatory IFRS adoption and financial

statement comparability. Contemporary Accounting Research. 30(4). pp. 1373-1400.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications. 40(10). pp. 3970-3983.

Deng, Y., De Zoysa, A. and Bhati, S., 2013. Performance of automakers in China and India:

an empirical investigation using ratio analysis.

Hodder, L., Hopkins, P.E. and Wood, D.A., 2008. The effects of financial statement and

informational complexity on analysts' cash flow forecasts. The Accounting Review.

83(4). pp. 915-956.

Khan, S. and Bradbury, M.E., 2014. Volatility and risk relevance of comprehensive income.

Journal of Contemporary Accounting & Economics. 10(1). pp. 76-85.

Konchitchki, Y. and Patatoukas, P.N., 2013. Taking the pulse of the real economy using

financial statement analysis: Implications for macro forecasting and stock valuation.

The Accounting Review. 89(2). pp. 669-694.

Krishnan, S., 2012. Inventory valuation under IFRS and GAAP. Strategic Finance. 93(9). p.

51.

Petersen, C.V. and Plenborg, T., 2010. Financial statement analysis. Prentice-Hall.

Rajendran, K. and Nimalthasan, P., 2013. Capital structure and its impact on firm

performance: A study on Sri Lankan listed manufacturing companies. Kajananthan

R, Nimalthasan P (2013) Capital structure and its impact on firm performance: A

study on Sri Lankan listed manufacturing companies. Merit Research Journal of

Business and Management. 1(2). pp. 037-044.

Schoenebeck, K.P. and Holtzman, M.P., 2013. Interpreting and analyzing financial

statements. Pearson Higher Ed.

Online

7 Cash flow ratios that investors should know, 2014. [Online]. Available through:

<http://www.oldschoolvalue.com/blog/valuation-methods/cash-flow-ratios>.

[Accessed on 30th March, 2016].

Books and Journals

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance. 39(7). pp. 667-676.

Brochet, F., Jagolinzer, A.D. and Riedl, E.J., 2013. Mandatory IFRS adoption and financial

statement comparability. Contemporary Accounting Research. 30(4). pp. 1373-1400.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications. 40(10). pp. 3970-3983.

Deng, Y., De Zoysa, A. and Bhati, S., 2013. Performance of automakers in China and India:

an empirical investigation using ratio analysis.

Hodder, L., Hopkins, P.E. and Wood, D.A., 2008. The effects of financial statement and

informational complexity on analysts' cash flow forecasts. The Accounting Review.

83(4). pp. 915-956.

Khan, S. and Bradbury, M.E., 2014. Volatility and risk relevance of comprehensive income.

Journal of Contemporary Accounting & Economics. 10(1). pp. 76-85.

Konchitchki, Y. and Patatoukas, P.N., 2013. Taking the pulse of the real economy using

financial statement analysis: Implications for macro forecasting and stock valuation.

The Accounting Review. 89(2). pp. 669-694.

Krishnan, S., 2012. Inventory valuation under IFRS and GAAP. Strategic Finance. 93(9). p.

51.

Petersen, C.V. and Plenborg, T., 2010. Financial statement analysis. Prentice-Hall.

Rajendran, K. and Nimalthasan, P., 2013. Capital structure and its impact on firm

performance: A study on Sri Lankan listed manufacturing companies. Kajananthan

R, Nimalthasan P (2013) Capital structure and its impact on firm performance: A

study on Sri Lankan listed manufacturing companies. Merit Research Journal of

Business and Management. 1(2). pp. 037-044.

Schoenebeck, K.P. and Holtzman, M.P., 2013. Interpreting and analyzing financial

statements. Pearson Higher Ed.

Online

7 Cash flow ratios that investors should know, 2014. [Online]. Available through:

<http://www.oldschoolvalue.com/blog/valuation-methods/cash-flow-ratios>.

[Accessed on 30th March, 2016].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.