Financial Crime and Risk Management: A Strategic Plan for Aldi

VerifiedAdded on 2020/05/28

|18

|5885

|52

Report

AI Summary

This report presents a comprehensive strategic plan for Aldi to address financial crime and risk management. It begins by outlining the current state of financial crime in Australia, highlighting the rising incidents and costs associated with fraud, emphasizing the need for robust strategies. The report then details Aldi's approach, aligning with the AS 8001-2008 standard, and focuses on prevention, detection, and response strategies. The prevention plan includes risk assessment, integrity structure maintenance, governance arrangements, management commitment, ethical structure, accountability, internal controls, employee awareness, and community awareness. The detection plan emphasizes the use of varied data sources, data cleaning, ontology systems, real-time transaction monitoring, customer profiling, and link analysis. The response strategy focuses on risk exposure, operating models, and infrastructure. The report provides detailed steps for each strategy, incorporating automated approaches and proactive measures to mitigate financial crime risks and ensure compliance.

Running head: FINANCIAL CRIME AND RISK MANAGEMENT

FINANCIAL CRIME AND RISK MANGEMENT

Name of the Student:

Name of the University:

Author’s Note:

FINANCIAL CRIME AND RISK MANGEMENT

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL CRIME AND RISK MANAGEMENT

Strategic Plan for the organization Aldi to deal with financial crime

The problems of financial crime can be considered to be a popular and at the same time

widespread issue that influences brand vaue as well as reputation, company’s goodwill

together with revenue of corporations. Several studies as well as surveys of financial crime

within the Australian nation reveals the fact that costs of fraud is no less than $3 billion every

year.,

Current State of Affairs of financial crime in Australia

Essentially, as mentioned in AS 8001-2008, the fraud incidents particularly within the

Australian economy is rising year after year with approximately 63% of the Australian

nations experiencing financial crime (Gottschalk, 2016). Reports also suggest that the larger

the size of the corporation, the higher is the probability to suffer from financial crime at

certain point in the business cycle (Deloitte.com, 2018). Results of survey also indicate that

Australian corporations might suffer a greater rate of reported fraud than the worldwide

average. Research in this area suggest that primary source of fraudulent actions stem from

within the business concern in which internal factors stand for 75% of the events as well as

value of loss suffered. Several Australian corporations are therefore not properly prepared to

identify and avert financial crime (Leong, 2016).

Key observations:

There is need to appropriately handle financial crime holistically and recognized certain

issues that are vital to the process of formulation of financial crime strategy:

Increase in the regulatory necessities from regional, transnational as well as local

stakeholders. Increase in need for an analytical comprehension of financial crime can be

observed(Masciandaro, 2017). Intricacy is present in the process of implementation as well as

on-going administration of financial crime evaluation and reporting is all the time becoming

major concern for corporations. Again, technology is an important key in the process of

focussing probable areas of risk and permits them to be more concentrated or else targeted in

their endeavours to avert financial crime (Wilson, 2017). Approaches of corporations in

Australia to handle financial crime is constantly altering and transforming to handle newly

identified issues (Pratt & Peters, 2017).

Fraud and financial crime management strategy

Strategic Plan for the organization Aldi to deal with financial crime

The problems of financial crime can be considered to be a popular and at the same time

widespread issue that influences brand vaue as well as reputation, company’s goodwill

together with revenue of corporations. Several studies as well as surveys of financial crime

within the Australian nation reveals the fact that costs of fraud is no less than $3 billion every

year.,

Current State of Affairs of financial crime in Australia

Essentially, as mentioned in AS 8001-2008, the fraud incidents particularly within the

Australian economy is rising year after year with approximately 63% of the Australian

nations experiencing financial crime (Gottschalk, 2016). Reports also suggest that the larger

the size of the corporation, the higher is the probability to suffer from financial crime at

certain point in the business cycle (Deloitte.com, 2018). Results of survey also indicate that

Australian corporations might suffer a greater rate of reported fraud than the worldwide

average. Research in this area suggest that primary source of fraudulent actions stem from

within the business concern in which internal factors stand for 75% of the events as well as

value of loss suffered. Several Australian corporations are therefore not properly prepared to

identify and avert financial crime (Leong, 2016).

Key observations:

There is need to appropriately handle financial crime holistically and recognized certain

issues that are vital to the process of formulation of financial crime strategy:

Increase in the regulatory necessities from regional, transnational as well as local

stakeholders. Increase in need for an analytical comprehension of financial crime can be

observed(Masciandaro, 2017). Intricacy is present in the process of implementation as well as

on-going administration of financial crime evaluation and reporting is all the time becoming

major concern for corporations. Again, technology is an important key in the process of

focussing probable areas of risk and permits them to be more concentrated or else targeted in

their endeavours to avert financial crime (Wilson, 2017). Approaches of corporations in

Australia to handle financial crime is constantly altering and transforming to handle newly

identified issues (Pratt & Peters, 2017).

Fraud and financial crime management strategy

2FINANCIAL CRIME AND RISK MANAGEMENT

Aldi, a leading worldwide supermarket chain is necessarily subject to mandatory regulations

of both financial as well as risk management (Gregson & Crang, 2017). In essence, the

Standards Australia AS 8001-2008 (Fraud and Corruption Control Standard) can be

considered to be practice resource that the corporation can adopt for development of robust

tactic to avert financial crime (Wilson, 2014).

Strategies for fraud development of financial crime combating plan comprises of :

Prevention

The strategy is to develop proactive emasures for lessening the fraud risk and corruption

occurring in the first place (Brody et al., 2016).

Detection

The strategy involves formulation of measures categorically designed to unearth incidents of

financial crime at the time when they take place

Aldi, a leading worldwide supermarket chain is necessarily subject to mandatory regulations

of both financial as well as risk management (Gregson & Crang, 2017). In essence, the

Standards Australia AS 8001-2008 (Fraud and Corruption Control Standard) can be

considered to be practice resource that the corporation can adopt for development of robust

tactic to avert financial crime (Wilson, 2014).

Strategies for fraud development of financial crime combating plan comprises of :

Prevention

The strategy is to develop proactive emasures for lessening the fraud risk and corruption

occurring in the first place (Brody et al., 2016).

Detection

The strategy involves formulation of measures categorically designed to unearth incidents of

financial crime at the time when they take place

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL CRIME AND RISK MANAGEMENT

Response

The specific stratagem includes development of measures that can be designed for the

purpose of divising corrective actions as well as remedies for the caused harm occurring

owing to financial crime or fraud (Kuhlmann et al., 2016).

Detailed presentation of prevention plan:

Approach of the corporation Aldi to handle the risks of financial crime have the need to be

underpinned by a complete organuzational policy structure, with suitable benchmarks that are

instituted against best practice programs as well as standards (Gottschalk, 2014). The

strategic plan for combating financial crime that can be adopted by Aldi can be described as

follows:

Stage 1: Assessment of risk of financial crime:

Consideration need to be given to the overall size as well as functionalities of the corporation

Aldi, any alteration in the overall framework otherwise function, both internal as well as

external risks of fraud, new as well we emerging fraud risks (Holtfreter, 2015). In addition to

this, it is also important to take into account wider organizational operating environment risks

for the purpose of development of profile of financial crime risk. As per regulations of AS

8001-2008, the approach to controlling fraud is in line with the objective of the regulation

(Merkel et al., 2016).

Stage 2: Execution and maintenance of integrity structure

The company have the need to adopt corruption prevention principles for the the purpose of

forming an important part of corporate, functional planning procedures as well as strategic

procedures, both yearly and long term basis (Deloitte.com, 2018). Corruption prevention

principles can be adopted for project planning, business procedures and processes of review

of services. In addition to this, management of the firm Aldi can carry out independent

reviews of different operations and efficacy of systems of internal control for making certain

adequate prevention, deterrence as well as detection of major financial crime (Stowell et al.,

2017).

Stage 3: Development of governance arrangements for controlling financial crime

Response

The specific stratagem includes development of measures that can be designed for the

purpose of divising corrective actions as well as remedies for the caused harm occurring

owing to financial crime or fraud (Kuhlmann et al., 2016).

Detailed presentation of prevention plan:

Approach of the corporation Aldi to handle the risks of financial crime have the need to be

underpinned by a complete organuzational policy structure, with suitable benchmarks that are

instituted against best practice programs as well as standards (Gottschalk, 2014). The

strategic plan for combating financial crime that can be adopted by Aldi can be described as

follows:

Stage 1: Assessment of risk of financial crime:

Consideration need to be given to the overall size as well as functionalities of the corporation

Aldi, any alteration in the overall framework otherwise function, both internal as well as

external risks of fraud, new as well we emerging fraud risks (Holtfreter, 2015). In addition to

this, it is also important to take into account wider organizational operating environment risks

for the purpose of development of profile of financial crime risk. As per regulations of AS

8001-2008, the approach to controlling fraud is in line with the objective of the regulation

(Merkel et al., 2016).

Stage 2: Execution and maintenance of integrity structure

The company have the need to adopt corruption prevention principles for the the purpose of

forming an important part of corporate, functional planning procedures as well as strategic

procedures, both yearly and long term basis (Deloitte.com, 2018). Corruption prevention

principles can be adopted for project planning, business procedures and processes of review

of services. In addition to this, management of the firm Aldi can carry out independent

reviews of different operations and efficacy of systems of internal control for making certain

adequate prevention, deterrence as well as detection of major financial crime (Stowell et al.,

2017).

Stage 3: Development of governance arrangements for controlling financial crime

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL CRIME AND RISK MANAGEMENT

A particular member of the manmagement can be considered to be the important point of

contact for financial crime control policies within the firm. This policy can help in

communicating the commitment of the corporation to specifically fraud as well as control of

corruption.

Stage 4: Commitment of management to control the risk of financial crime

Fundamentally, ethics, financial crime prevention objectives need to be included in the

measures of performamce against which cokmpany’s managers can be appraised (Kim et al.,

2014).

Stage 5: Development of ethical structure

An ethical code of conduct can be designed that can act as a standard that employees need to

be meet.

Stage 6: Development of accountability of line management

Individuals in high risk positions, namely procurement of raw materials, receipt of revenue,

delivering exemptions or else having discretionary decision making authority need to be

properly trained, monitored and supported (Chambers-Jones & Hillman, 2014).

Stage 7: Establishment of internal controls

The prevention plan can also include uses of internal audit for the purpose of actively

assessing system of risk management as well as control, and arranging the same in a line that

matches with the risk profile of the firm. The organization can prevent the financial crime by

way of systematically monitoring and reporting different efficacies of fraud control

stratagems and present clearly documented processes for carrying out high risk actions.

Stage 8: Creation of awareness among employees

In order to prevent financial crime in the future period, the management of Aldi can provide

awareness training to employees regarding financial crime in order to ensure that they are

capable to undertake proper actions (Ryder, 2014).

Stage 9: Generation of awareness among client as well as community

The customers of the firm Aldi as well as the community need to be made aware regarding

the fact that business concerns shall not tolerate fraudulent actions and financial crimes

A particular member of the manmagement can be considered to be the important point of

contact for financial crime control policies within the firm. This policy can help in

communicating the commitment of the corporation to specifically fraud as well as control of

corruption.

Stage 4: Commitment of management to control the risk of financial crime

Fundamentally, ethics, financial crime prevention objectives need to be included in the

measures of performamce against which cokmpany’s managers can be appraised (Kim et al.,

2014).

Stage 5: Development of ethical structure

An ethical code of conduct can be designed that can act as a standard that employees need to

be meet.

Stage 6: Development of accountability of line management

Individuals in high risk positions, namely procurement of raw materials, receipt of revenue,

delivering exemptions or else having discretionary decision making authority need to be

properly trained, monitored and supported (Chambers-Jones & Hillman, 2014).

Stage 7: Establishment of internal controls

The prevention plan can also include uses of internal audit for the purpose of actively

assessing system of risk management as well as control, and arranging the same in a line that

matches with the risk profile of the firm. The organization can prevent the financial crime by

way of systematically monitoring and reporting different efficacies of fraud control

stratagems and present clearly documented processes for carrying out high risk actions.

Stage 8: Creation of awareness among employees

In order to prevent financial crime in the future period, the management of Aldi can provide

awareness training to employees regarding financial crime in order to ensure that they are

capable to undertake proper actions (Ryder, 2014).

Stage 9: Generation of awareness among client as well as community

The customers of the firm Aldi as well as the community need to be made aware regarding

the fact that business concerns shall not tolerate fraudulent actions and financial crimes

5FINANCIAL CRIME AND RISK MANAGEMENT

Stage 10: Development of avenues for the purpose of reporting diverse suspected events

A wide range of internal as well as external mechanisms of reporting can be instituted for the

purpose of reporting financial crime (Rahman & Rahman, 2016).

Stage 11: Providing protection for specific disclosures

Specific mechanisms, strategies as well as procedures for the purpose of supporting and at the

same time shielding disclosures can be instituted as per the obligations of the Protected

Disclosures Act of the year 2012. As such, stringent system of maintaining confidentiality is

important for receiving and at the same time processing of declarations of financial crime.

Stage 10: Development of avenues for the purpose of reporting diverse suspected events

A wide range of internal as well as external mechanisms of reporting can be instituted for the

purpose of reporting financial crime (Rahman & Rahman, 2016).

Stage 11: Providing protection for specific disclosures

Specific mechanisms, strategies as well as procedures for the purpose of supporting and at the

same time shielding disclosures can be instituted as per the obligations of the Protected

Disclosures Act of the year 2012. As such, stringent system of maintaining confidentiality is

important for receiving and at the same time processing of declarations of financial crime.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL CRIME AND RISK MANAGEMENT

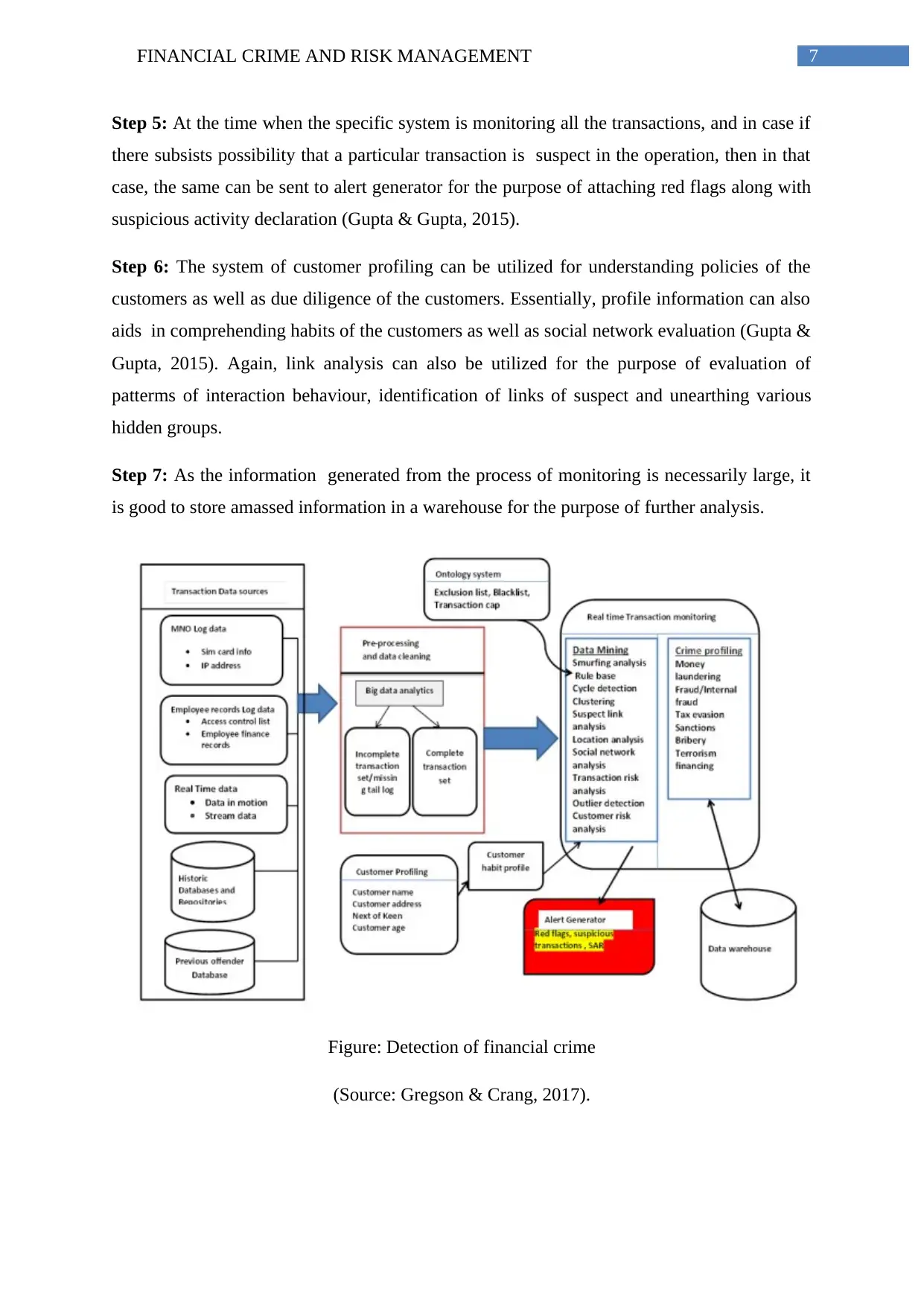

Detailed presentation of detection plan

This essentially includes establishment of monitoring activities that refers to fraud and social

network analysis. As such, automated approaches can be used for detection of financial

crime.

Steps in strategic plan for detection of financial crime

Step 1: Varied sources of information can be used for processing of data. The management of

the company can analyse the transaction data sources namely MNO log data, employee

records log data, real time data, historic databases and prior offender databases (Holtfreter,

2015).

Step 2: Transaction data that are in action need to be subjected to data cleaning in which

successful and failed transactions need to be cleaned for the purpose of processing. Data

amassed have the need to be cleaned for reviewing incomplete transactions. As such,

management of the Aldi can implement big data tools of analytics as the data might perhaps

be in motion and data might be huge. However, complete transactions can be forwarded for

the purpose of monitoring.

Step 3: Ontologies can be considered to be domain associated to intensional models

developed for the purpose of capturing information and knowledge. Ontology can be

considered as necessarily a knowledge based scheme that utilizes a declarative knowledge

foundation containing diverse themes and associations that subsist in a specific domain

(Baker, 2018). Thus, it can be hereby stated that the system of ontology can help in producing

the exclusion list, black list as well as transaction cap for the firm Aldi.

Step 4: Thereafter, management of the firm Aldi can adopt the real time transaction

monitoring. In this connection it can be stated that majority of the tools of detection and

mechanisms are necessarily passive in character. However, in the current proposed structure,

the specified module can examine suspicious transactions and that too at a real time basis.

Further, specific techniques of data mining can be utilized for examining diverse offenses by

means of clustering, deduced analysis of link, analysis of location in which system can

review both geographical location as well as habits of customers. In case if a specific

transaction is considered to be suspect, it can be profiled relying upon possibilities of the

variable as well as rank (Reurink, 2016).

Detailed presentation of detection plan

This essentially includes establishment of monitoring activities that refers to fraud and social

network analysis. As such, automated approaches can be used for detection of financial

crime.

Steps in strategic plan for detection of financial crime

Step 1: Varied sources of information can be used for processing of data. The management of

the company can analyse the transaction data sources namely MNO log data, employee

records log data, real time data, historic databases and prior offender databases (Holtfreter,

2015).

Step 2: Transaction data that are in action need to be subjected to data cleaning in which

successful and failed transactions need to be cleaned for the purpose of processing. Data

amassed have the need to be cleaned for reviewing incomplete transactions. As such,

management of the Aldi can implement big data tools of analytics as the data might perhaps

be in motion and data might be huge. However, complete transactions can be forwarded for

the purpose of monitoring.

Step 3: Ontologies can be considered to be domain associated to intensional models

developed for the purpose of capturing information and knowledge. Ontology can be

considered as necessarily a knowledge based scheme that utilizes a declarative knowledge

foundation containing diverse themes and associations that subsist in a specific domain

(Baker, 2018). Thus, it can be hereby stated that the system of ontology can help in producing

the exclusion list, black list as well as transaction cap for the firm Aldi.

Step 4: Thereafter, management of the firm Aldi can adopt the real time transaction

monitoring. In this connection it can be stated that majority of the tools of detection and

mechanisms are necessarily passive in character. However, in the current proposed structure,

the specified module can examine suspicious transactions and that too at a real time basis.

Further, specific techniques of data mining can be utilized for examining diverse offenses by

means of clustering, deduced analysis of link, analysis of location in which system can

review both geographical location as well as habits of customers. In case if a specific

transaction is considered to be suspect, it can be profiled relying upon possibilities of the

variable as well as rank (Reurink, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL CRIME AND RISK MANAGEMENT

Step 5: At the time when the specific system is monitoring all the transactions, and in case if

there subsists possibility that a particular transaction is suspect in the operation, then in that

case, the same can be sent to alert generator for the purpose of attaching red flags along with

suspicious activity declaration (Gupta & Gupta, 2015).

Step 6: The system of customer profiling can be utilized for understanding policies of the

customers as well as due diligence of the customers. Essentially, profile information can also

aids in comprehending habits of the customers as well as social network evaluation (Gupta &

Gupta, 2015). Again, link analysis can also be utilized for the purpose of evaluation of

patterms of interaction behaviour, identification of links of suspect and unearthing various

hidden groups.

Step 7: As the information generated from the process of monitoring is necessarily large, it

is good to store amassed information in a warehouse for the purpose of further analysis.

Figure: Detection of financial crime

(Source: Gregson & Crang, 2017).

Step 5: At the time when the specific system is monitoring all the transactions, and in case if

there subsists possibility that a particular transaction is suspect in the operation, then in that

case, the same can be sent to alert generator for the purpose of attaching red flags along with

suspicious activity declaration (Gupta & Gupta, 2015).

Step 6: The system of customer profiling can be utilized for understanding policies of the

customers as well as due diligence of the customers. Essentially, profile information can also

aids in comprehending habits of the customers as well as social network evaluation (Gupta &

Gupta, 2015). Again, link analysis can also be utilized for the purpose of evaluation of

patterms of interaction behaviour, identification of links of suspect and unearthing various

hidden groups.

Step 7: As the information generated from the process of monitoring is necessarily large, it

is good to store amassed information in a warehouse for the purpose of further analysis.

Figure: Detection of financial crime

(Source: Gregson & Crang, 2017).

8FINANCIAL CRIME AND RISK MANAGEMENT

Response Strategy with special orientation to the operations of Aldi

Risk exposure

As per reports presented by Deloitte Consulting, majority of respondents operating in three

different cities of Australia can classify financial crime risk exposure. According to them,

regulatory framework in which business operates, geographies in which the firm operates,

customer type and business type characterise risk exposure of firm to financial crime.

Strikingly, delegtes in Sydney classified risk as per business type at particularly higher rate

than that of the respondents in Melbourne. Therefore, based on amassed data (both internal

and external data) management of the firm Aldi can aptly respond appropriately after gauging

risk exposure of the firm based on type of businesses (Gregson & Crang, 2017).

Operating model and infrastructure

Business concerns still do not have functional convergence program for the purpose of

integrating fraud as well as financial crime groups even after recognizing the fact that

operating framework was a potential barrier in the way of attaining holistic financial crime

approach. There exists a gap in the operational groups of the corporation’s fraud as well as

financial crime. For example, the lack of an appropriate IT system might increase the risks of

becoming a victim of financial crime. Particularly, in Melbourne, reports presented by

Fianncial Solutions Lead recommended that diverse technology tools can provide

corporations a more appropriate view of the data, focussing probable quarters of risk and

permit them to become more focussed in the process of fighting the financial crime

encountered by the corporation (Saiglobal.com, 2018). Thus, it can be hereby identified that

technology is a chief aspect in the process of handling the management and examination of

the origin as well as cause of cyber incidents. In addition to this, business concern also do not

have appropriate infrastructure for future as well as constantly altering legislations, for

instance, FATCA. Therefore, the management of Aldi can consider proper response of

combating financial crime by developing apposite infrastructure that can support the process.

Incidence of cyber incidence and data violation

In addition to this, another state of affairs that affects conditions financial crime of the

supermarket chains in the Australia include data breaches as a specific issue. Panel

conversation identified the fact that data violation lead to financial crime. In essence,

criminals as well as organized groups have got to know the way of using technology in their

Response Strategy with special orientation to the operations of Aldi

Risk exposure

As per reports presented by Deloitte Consulting, majority of respondents operating in three

different cities of Australia can classify financial crime risk exposure. According to them,

regulatory framework in which business operates, geographies in which the firm operates,

customer type and business type characterise risk exposure of firm to financial crime.

Strikingly, delegtes in Sydney classified risk as per business type at particularly higher rate

than that of the respondents in Melbourne. Therefore, based on amassed data (both internal

and external data) management of the firm Aldi can aptly respond appropriately after gauging

risk exposure of the firm based on type of businesses (Gregson & Crang, 2017).

Operating model and infrastructure

Business concerns still do not have functional convergence program for the purpose of

integrating fraud as well as financial crime groups even after recognizing the fact that

operating framework was a potential barrier in the way of attaining holistic financial crime

approach. There exists a gap in the operational groups of the corporation’s fraud as well as

financial crime. For example, the lack of an appropriate IT system might increase the risks of

becoming a victim of financial crime. Particularly, in Melbourne, reports presented by

Fianncial Solutions Lead recommended that diverse technology tools can provide

corporations a more appropriate view of the data, focussing probable quarters of risk and

permit them to become more focussed in the process of fighting the financial crime

encountered by the corporation (Saiglobal.com, 2018). Thus, it can be hereby identified that

technology is a chief aspect in the process of handling the management and examination of

the origin as well as cause of cyber incidents. In addition to this, business concern also do not

have appropriate infrastructure for future as well as constantly altering legislations, for

instance, FATCA. Therefore, the management of Aldi can consider proper response of

combating financial crime by developing apposite infrastructure that can support the process.

Incidence of cyber incidence and data violation

In addition to this, another state of affairs that affects conditions financial crime of the

supermarket chains in the Australia include data breaches as a specific issue. Panel

conversation identified the fact that data violation lead to financial crime. In essence,

criminals as well as organized groups have got to know the way of using technology in their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL CRIME AND RISK MANAGEMENT

favour for making their own products even more sophisticated. Credit card fraud has become

also common in the retaining industry in which Aldi operates. For this reason, upgrading the

existing company infrastructure particularly technology as well as intelligence can be

considered to be important for the purpose of combating novel fraud (Deloitte.com, 2018).

Responding to fake invoices

Financial crime in the online payment system and use of fake invoices is reported in case of

the retail business. Thus, this issue of financial crime that involves false invoicing has been

seen in Aldi that led to claim for payments of goods as well as services that is actually not

delivered by the company. The company can address the problem by proper internal control.

The e-platforms, digital money as well as other electronic platforms is a playing field for

financial crime owing to the speed at which money gets transferred, inadequate physical

contact, potential of layering multiple stages of transactions. As per AS 8001-2008, this is an

issue and challenge associated to use of technology and admittance to banking services that

lead to financial crime and need to be addressed (Deloitte.com, 2018). In this case, the

management of the firm encounters threat to security of data and financial crime. In this

regard, management of the firm Aldi can consider implementation of fraud detection tools for

the purpose of countering this specific financial crime. As per requirement of Corruption

Perception Index mentioned in AS 8001-2008, it is important to maintain transparency

(Saiglobal.com, 2018). In line with the scope of the corruption control program as considered

by the Standard AS 8001-2008, the management of the firm can also respond to the detected

issues by maintenance of transparency, release of required information for non-financial

purpose. As stated in the section “managing the risks” under AS 8001-2008, the business

entity Aldi too can adopt approach to manage the fraud risks by underpinning the corporation

wide policy designed with both internal as well as external consultation with apposite

benchmarking (Deloitte.com, 2018). This benchmark or yardstick is necessarily against

instituted best practice prevention as well as detection programs along with standards and

needs to apply sound ways of risk management.

favour for making their own products even more sophisticated. Credit card fraud has become

also common in the retaining industry in which Aldi operates. For this reason, upgrading the

existing company infrastructure particularly technology as well as intelligence can be

considered to be important for the purpose of combating novel fraud (Deloitte.com, 2018).

Responding to fake invoices

Financial crime in the online payment system and use of fake invoices is reported in case of

the retail business. Thus, this issue of financial crime that involves false invoicing has been

seen in Aldi that led to claim for payments of goods as well as services that is actually not

delivered by the company. The company can address the problem by proper internal control.

The e-platforms, digital money as well as other electronic platforms is a playing field for

financial crime owing to the speed at which money gets transferred, inadequate physical

contact, potential of layering multiple stages of transactions. As per AS 8001-2008, this is an

issue and challenge associated to use of technology and admittance to banking services that

lead to financial crime and need to be addressed (Deloitte.com, 2018). In this case, the

management of the firm encounters threat to security of data and financial crime. In this

regard, management of the firm Aldi can consider implementation of fraud detection tools for

the purpose of countering this specific financial crime. As per requirement of Corruption

Perception Index mentioned in AS 8001-2008, it is important to maintain transparency

(Saiglobal.com, 2018). In line with the scope of the corruption control program as considered

by the Standard AS 8001-2008, the management of the firm can also respond to the detected

issues by maintenance of transparency, release of required information for non-financial

purpose. As stated in the section “managing the risks” under AS 8001-2008, the business

entity Aldi too can adopt approach to manage the fraud risks by underpinning the corporation

wide policy designed with both internal as well as external consultation with apposite

benchmarking (Deloitte.com, 2018). This benchmark or yardstick is necessarily against

instituted best practice prevention as well as detection programs along with standards and

needs to apply sound ways of risk management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL CRIME AND RISK MANAGEMENT

The company selected for the purpose of the analysis of financial crime is Aldi. Aldi

is a global brand which is a leading global discount supermarket chain which has more than

10000 stores in around 18 countries in the world. The estimated turnover of the company is

around €50 billion. The brand has two leading brands of supermarket chains which owns

more than 10000 stores over 18 countries. The original brand was established and founded in

1913 and then the brand was split in two parts in 1960 which were given the names Aldi

Nord and Aldi Sud. The chain was founded by karl and Theo Albrecht in 1946. The grocery

chain has its headquarters situated in Germany. The company’s earliest traces can be found

when the owners of the company opened a small store in Essen. The Aldi Nord group

independently controls 35 regional branches which has approximately around 2500 stores.

Aldi Sud group has around 31 companies under its control which has approximately 1600

stores. Aldi Sud operates in Australia, United States, Austria and Ireland.

Some of the common practices of the Aldi group are metal gates, turnstiles which

forces customers to exit through checkouts and charging customers for the shopping bags

which is provided by the company. The company followed the policy of accepting payments

only in cash but in some countries like Australia, UK the use of credit cards for making

payments is also allowed. The grocery chain specialises in items such as food, beverages,

sanitary articles and other widely used household items. The most of the items which the

company keeps in the stores are own brands of Aldi. The discount grocery chain supermarket

Aldi is performing well in Australian market as the company has no or little competition in

this industry in Australia. The company has been maintained around 12.6% market shares as

per the estimates of the 2016 and the discount chain grocery market is growing rapidly. Aldi

also has the policy of offering special offers to its customers on weekends on some of the

expensive items such as appliances, electronic products. The company also provides

discounts on items like clothes, toys, gifts provided a strict quantity of the product has been

purchased from the store. Besides this Aldi is the largest wine retailer in Germany and also

has options of alcohol for its customers in Australian markets. Another policy of the company

which is easily identifiable is that the company generally sells products which are exclusively

or custom branded. Therefore it can be established that the company maintains certain

standards when it comes selling products in the market. Another characteristic which can be

identified with the Aldi group is that the company establishes relationship with the local

The company selected for the purpose of the analysis of financial crime is Aldi. Aldi

is a global brand which is a leading global discount supermarket chain which has more than

10000 stores in around 18 countries in the world. The estimated turnover of the company is

around €50 billion. The brand has two leading brands of supermarket chains which owns

more than 10000 stores over 18 countries. The original brand was established and founded in

1913 and then the brand was split in two parts in 1960 which were given the names Aldi

Nord and Aldi Sud. The chain was founded by karl and Theo Albrecht in 1946. The grocery

chain has its headquarters situated in Germany. The company’s earliest traces can be found

when the owners of the company opened a small store in Essen. The Aldi Nord group

independently controls 35 regional branches which has approximately around 2500 stores.

Aldi Sud group has around 31 companies under its control which has approximately 1600

stores. Aldi Sud operates in Australia, United States, Austria and Ireland.

Some of the common practices of the Aldi group are metal gates, turnstiles which

forces customers to exit through checkouts and charging customers for the shopping bags

which is provided by the company. The company followed the policy of accepting payments

only in cash but in some countries like Australia, UK the use of credit cards for making

payments is also allowed. The grocery chain specialises in items such as food, beverages,

sanitary articles and other widely used household items. The most of the items which the

company keeps in the stores are own brands of Aldi. The discount grocery chain supermarket

Aldi is performing well in Australian market as the company has no or little competition in

this industry in Australia. The company has been maintained around 12.6% market shares as

per the estimates of the 2016 and the discount chain grocery market is growing rapidly. Aldi

also has the policy of offering special offers to its customers on weekends on some of the

expensive items such as appliances, electronic products. The company also provides

discounts on items like clothes, toys, gifts provided a strict quantity of the product has been

purchased from the store. Besides this Aldi is the largest wine retailer in Germany and also

has options of alcohol for its customers in Australian markets. Another policy of the company

which is easily identifiable is that the company generally sells products which are exclusively

or custom branded. Therefore it can be established that the company maintains certain

standards when it comes selling products in the market. Another characteristic which can be

identified with the Aldi group is that the company establishes relationship with the local

11FINANCIAL CRIME AND RISK MANAGEMENT

farmers of the country in which the grocery chain is established in order to acquire fresh

vegetables and food products from the local farmers.

The discount chain grocery firm Aldi is operating well in Australia. The first store of

Aldi was established in the year 2001 in Australia and since the brand is growing rapidly and

maintained a 12.6% market shares in the Industry. However the company faces certain risks

and problems which need to be overcome in order for smooth running of the business. In the

wake of financial frauds which have been occurring in various companies the management of

Aldi wants to ensure that the company is prepared to face such risks. The company wants to

incorporate a strategy which could tackle the financial risks which the business is exposed

around (Vona, 2012). The company wants to formulate a strategy which will be according to

the Australian Standard on Corporate Governance which is AS 8001 which deals with Fraud

and Corruption Control which was introduced in 2008. The problem which the grocery chain

faces is that fake invoices are used by employee which causes loss to the company. As seen

in most of the company employees are present in the store for a larger time period and they

get accesses to the various areas of the store. These employees are expected to perform their

duties smoothly and therefore have access to entire store. In some of the cases such

employees engages themselves in fraudulent activities in order for personal gains. In such

cases the employee who has the access to the revenue department can issue a fake invoice

and take cash or goods on the basis of such fake invoices. The management of the company

cannot identify such losses as these are generally of small amounts and are generally

continued for a longer period unless such unethical behaviours are noticed by the

management of the business. The management of Aldi has faced such an issue where the

employee is accused of internal thief. Some of the other unethical shrink which can be caused

by internal means are theft, vandalism, wastage of grocery items of business, abuse of

position in a business (Lotta, & Bogue, 2015). Nowadays this has become common as the

employees have access to the entire building and for a longer period of time, therefore they

can cause significant losses to the company during non business hours. Even though cash

misappropriations are a bit easy to identify, the same is not the case when the grocery

products of the company are stolen. These kinds of losses are not easy to identify. Therefore

the Aldi chain wants to revise their strategic plans and security and incorporate a new

mechanism which will prevent or discourage such a loss. The mechanism that will be

introduced will also mitigate the financial risks which the business is prone to face. Another

farmers of the country in which the grocery chain is established in order to acquire fresh

vegetables and food products from the local farmers.

The discount chain grocery firm Aldi is operating well in Australia. The first store of

Aldi was established in the year 2001 in Australia and since the brand is growing rapidly and

maintained a 12.6% market shares in the Industry. However the company faces certain risks

and problems which need to be overcome in order for smooth running of the business. In the

wake of financial frauds which have been occurring in various companies the management of

Aldi wants to ensure that the company is prepared to face such risks. The company wants to

incorporate a strategy which could tackle the financial risks which the business is exposed

around (Vona, 2012). The company wants to formulate a strategy which will be according to

the Australian Standard on Corporate Governance which is AS 8001 which deals with Fraud

and Corruption Control which was introduced in 2008. The problem which the grocery chain

faces is that fake invoices are used by employee which causes loss to the company. As seen

in most of the company employees are present in the store for a larger time period and they

get accesses to the various areas of the store. These employees are expected to perform their

duties smoothly and therefore have access to entire store. In some of the cases such

employees engages themselves in fraudulent activities in order for personal gains. In such

cases the employee who has the access to the revenue department can issue a fake invoice

and take cash or goods on the basis of such fake invoices. The management of the company

cannot identify such losses as these are generally of small amounts and are generally

continued for a longer period unless such unethical behaviours are noticed by the

management of the business. The management of Aldi has faced such an issue where the

employee is accused of internal thief. Some of the other unethical shrink which can be caused

by internal means are theft, vandalism, wastage of grocery items of business, abuse of

position in a business (Lotta, & Bogue, 2015). Nowadays this has become common as the

employees have access to the entire building and for a longer period of time, therefore they

can cause significant losses to the company during non business hours. Even though cash

misappropriations are a bit easy to identify, the same is not the case when the grocery

products of the company are stolen. These kinds of losses are not easy to identify. Therefore

the Aldi chain wants to revise their strategic plans and security and incorporate a new

mechanism which will prevent or discourage such a loss. The mechanism that will be

introduced will also mitigate the financial risks which the business is prone to face. Another

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.