FIN4006 Business Maths Assignment: Algebra, Forecasting Techniques

VerifiedAdded on 2023/06/04

|15

|2615

|90

Homework Assignment

AI Summary

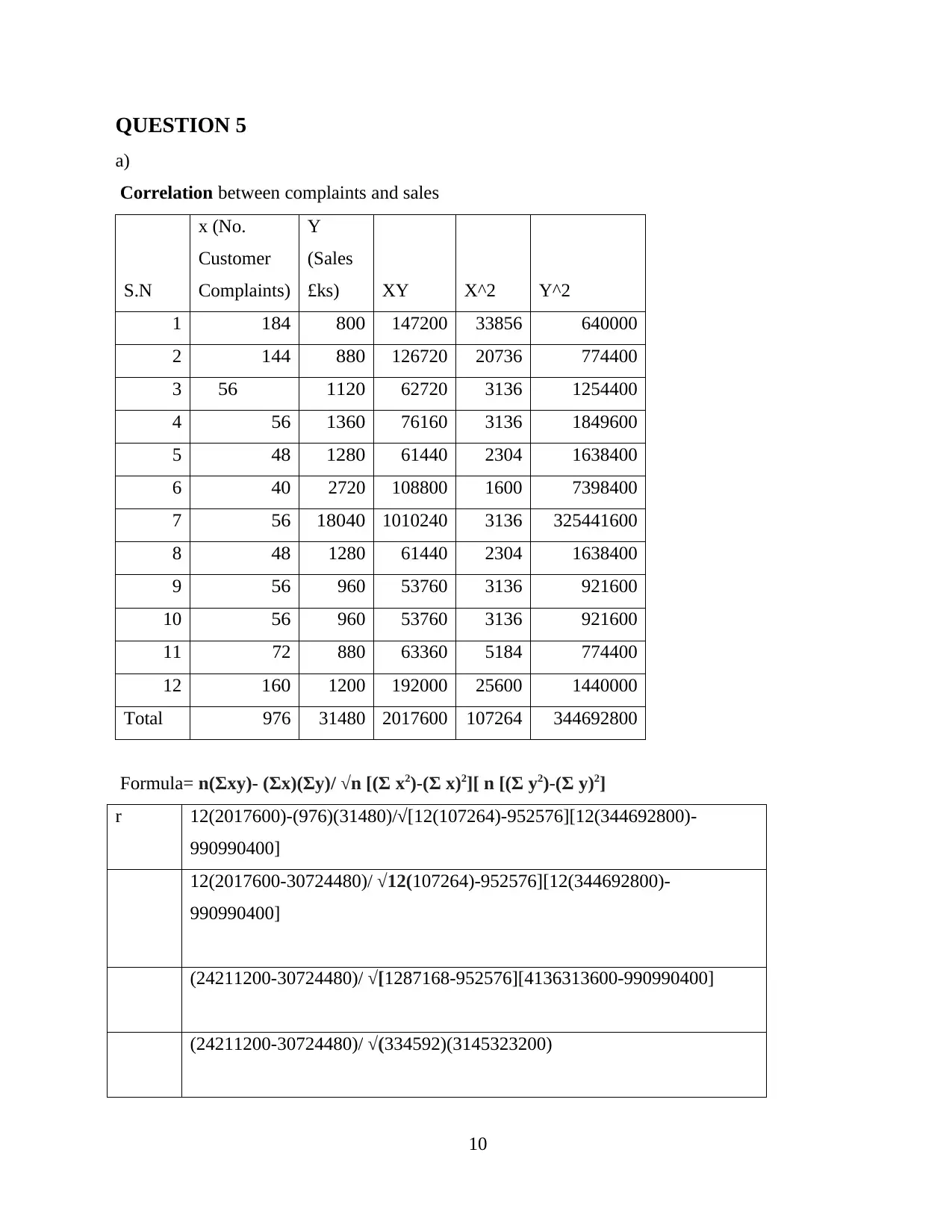

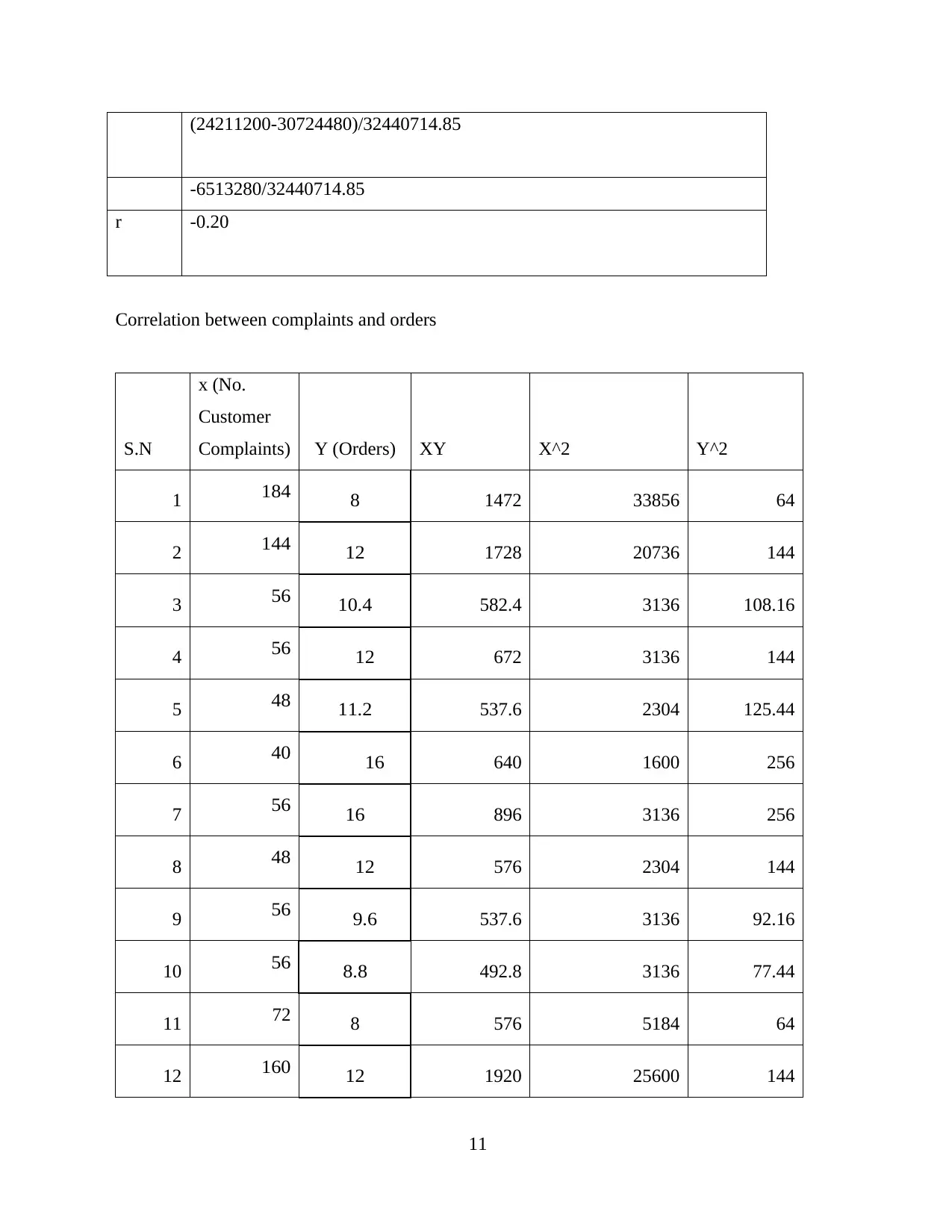

This document presents a detailed solution to a Business Maths assignment, addressing various aspects of algebra and its application in financial decision-making. The assignment covers topics such as solving algebraic equations, calculating markup and margin, understanding simple and compound interest, and applying forecasting techniques like moving averages. It also includes probability calculations, expected value analysis, payback period, net present value (NPV), and internal rate of return (IRR) for investment decisions. Furthermore, the solution provides correlation analysis between complaints and sales/orders, along with a discussion on the weaknesses of correlation analysis. Desklib provides a platform to explore similar solved assignments and access AI-powered study tools for students.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.