Alliance Pension Fund: Investment Strategies and Report

VerifiedAdded on 2022/09/29

|16

|3139

|24

Report

AI Summary

This report examines the Alliance Pension Fund's investment strategies, focusing on how pension funds are invested in stocks, mutual funds, and other financial instruments to generate returns for retirees. The report provides an overview of different investment options, including risky stocks, risk-free returns, and index funds. It discusses the roles of various investment managers, such as Mutual Assurance Company, Global Investment Managers, and City Gilt Managers, and analyzes their approaches to managing pension funds. The report also addresses problems and challenges faced by the pension fund, including union concerns and market risks. It includes financial data, regression analysis, and comparisons to other pension providers. The analysis covers international diversification, investment in gilts, hedge funds, and exchange-traded funds, highlighting the importance of diversification and risk management in securing the financial future of pensioners. The report emphasizes the necessity of understanding market dynamics and making informed investment decisions to ensure the sustainability and growth of pension funds.

ALLIANCE PENSION FUND

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

This report tells us about the investment schemes that can happen with the fund of the

pensions of the individual. The amount that is taken as a pension fund to provide the

individual at the time of retirement is an investment in the stocks and mutual funds. This will

help to increase the amount of the pension fund and the economy of the country. There are

different types of funds in the stock market. The risky stocks give a higher return, but the risk

involved in these shares is high. Risk-free returns are something in which return is less, but

the risk is not there. This report gives a brief discussion about the stocks, funds and

investment with the pension plan funds.

2

This report tells us about the investment schemes that can happen with the fund of the

pensions of the individual. The amount that is taken as a pension fund to provide the

individual at the time of retirement is an investment in the stocks and mutual funds. This will

help to increase the amount of the pension fund and the economy of the country. There are

different types of funds in the stock market. The risky stocks give a higher return, but the risk

involved in these shares is high. Risk-free returns are something in which return is less, but

the risk is not there. This report gives a brief discussion about the stocks, funds and

investment with the pension plan funds.

2

Table of Contents

Introduction................................................................................................................................4

Background of study..................................................................................................................4

Problems and statement..............................................................................................................6

Findings and analysis.................................................................................................................7

Conclusion................................................................................................................................10

Reference list............................................................................................................................11

Appendices...............................................................................................................................13

3

Introduction................................................................................................................................4

Background of study..................................................................................................................4

Problems and statement..............................................................................................................6

Findings and analysis.................................................................................................................7

Conclusion................................................................................................................................10

Reference list............................................................................................................................11

Appendices...............................................................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The pension plans help the employees to get an income after their retirement. This helps to

earn their living. The company with whom the person is working gives this benefit to their

employees. It has assets of 200 million pound. The pensioner has absorbed 10 million pound

income in the current year and rise will happen of 8%, which will make the amount to 20

million pounds. The trustees of the fund consult the actuary who looks after the day to day

facilities of the fund. The pension plan is the hope for the people as they will get an amount

after their retirement, and that will help them to live a better life. This is the responsibility

that is shared by both employer and the employee for many any decision like investment

decisions. The amount of the pension is deducted from the employee’s salary. They are ready

to take less amount of salary so that they get benefit at the time of requirement. In a study, it

is seen that in the US the 50% of employees are saving money for their retirement between

the age group of 20 to 29 years. It is essential to train employees about the benefits of the

pension plan to give knowledge about its benefits that are provided to the employees and the

company to restore its financial resources.

Background of study

● Mutual assurance company

The fund is managed by this company to pursue a “contra-cyclical policy” which

includes a large part of the pension fund. It helps the company at the time of market

fall and is allowed to deposit in the “variable rate deposit account”. They take the

help of the actuary to understand the investment policy that they want to hold. They

are invited to the parade, which helps them to increase their moderate turnover.

● Global investment managers

This is a conservative policy which concentrates on value. The decisions are taken by

the company’s group of members who have high proposed degrees. This can offer

"low management charges," i.e. 0.1% and

"low turnover," i.e. 10% per year.

Investment is made in the areas the managers are aware of, i.e. the US, UK and Japan

(Enoch et al. 2017). These managers have full knowledge of the market and its

approach. They help in development and growth by investing in the right hands.

● Index funds the UK

4

The pension plans help the employees to get an income after their retirement. This helps to

earn their living. The company with whom the person is working gives this benefit to their

employees. It has assets of 200 million pound. The pensioner has absorbed 10 million pound

income in the current year and rise will happen of 8%, which will make the amount to 20

million pounds. The trustees of the fund consult the actuary who looks after the day to day

facilities of the fund. The pension plan is the hope for the people as they will get an amount

after their retirement, and that will help them to live a better life. This is the responsibility

that is shared by both employer and the employee for many any decision like investment

decisions. The amount of the pension is deducted from the employee’s salary. They are ready

to take less amount of salary so that they get benefit at the time of requirement. In a study, it

is seen that in the US the 50% of employees are saving money for their retirement between

the age group of 20 to 29 years. It is essential to train employees about the benefits of the

pension plan to give knowledge about its benefits that are provided to the employees and the

company to restore its financial resources.

Background of study

● Mutual assurance company

The fund is managed by this company to pursue a “contra-cyclical policy” which

includes a large part of the pension fund. It helps the company at the time of market

fall and is allowed to deposit in the “variable rate deposit account”. They take the

help of the actuary to understand the investment policy that they want to hold. They

are invited to the parade, which helps them to increase their moderate turnover.

● Global investment managers

This is a conservative policy which concentrates on value. The decisions are taken by

the company’s group of members who have high proposed degrees. This can offer

"low management charges," i.e. 0.1% and

"low turnover," i.e. 10% per year.

Investment is made in the areas the managers are aware of, i.e. the US, UK and Japan

(Enoch et al. 2017). These managers have full knowledge of the market and its

approach. They help in development and growth by investing in the right hands.

● Index funds the UK

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The performance is the same as the

“FTSE 100 index” they promise to give such

returns in capital gains and as well in monthly dividends. They invest in

“Exchange

Traded Funds where there are no charges with the services, but the returns are good.

They even get a monthly dividend. There is no charge applied to have such funds

(Andonov et al. 2018). Many index managers claim charge of their service and the

service is not appropriate as they show no guarantees.

● City glit managers

They offer:

❏ "Guarantee return of 6% in the next five years."

❏ "Return of inflation rate."

❏ “3% foreseeable future”

The charges of these assets are 0.25% pa. They use

“advanced portfolio

immunization technique” and other bond techniques as well. Capital bonds

are such assets in which they invest their money. They have a debate about

wealth has been destroyed by inflation (Bridgen and Naczyk, 2019). The

company should give information to the investors about the shares in which

they are investing in. The investors should know the share market risk and

return.● “Enhanced Performance Managers”: They know the market and its risk and

returns. They have trading strategies that they have learnt from the past trading

performance. They take fees of “0.1% of NAV and performance charge of 1% of

returns over 12%”. This fund has a high turnover. This should continue in the

future. They have inside information on the market that helps them decide about their

future investments.

5

Mutual assurance

company

Global investment

managers Index funds UK

City glit managers

“Enhanced

Performance

Managers”

“FTSE 100 index” they promise to give such

returns in capital gains and as well in monthly dividends. They invest in

“Exchange

Traded Funds where there are no charges with the services, but the returns are good.

They even get a monthly dividend. There is no charge applied to have such funds

(Andonov et al. 2018). Many index managers claim charge of their service and the

service is not appropriate as they show no guarantees.

● City glit managers

They offer:

❏ "Guarantee return of 6% in the next five years."

❏ "Return of inflation rate."

❏ “3% foreseeable future”

The charges of these assets are 0.25% pa. They use

“advanced portfolio

immunization technique” and other bond techniques as well. Capital bonds

are such assets in which they invest their money. They have a debate about

wealth has been destroyed by inflation (Bridgen and Naczyk, 2019). The

company should give information to the investors about the shares in which

they are investing in. The investors should know the share market risk and

return.● “Enhanced Performance Managers”: They know the market and its risk and

returns. They have trading strategies that they have learnt from the past trading

performance. They take fees of “0.1% of NAV and performance charge of 1% of

returns over 12%”. This fund has a high turnover. This should continue in the

future. They have inside information on the market that helps them decide about their

future investments.

5

Mutual assurance

company

Global investment

managers Index funds UK

City glit managers

“Enhanced

Performance

Managers”

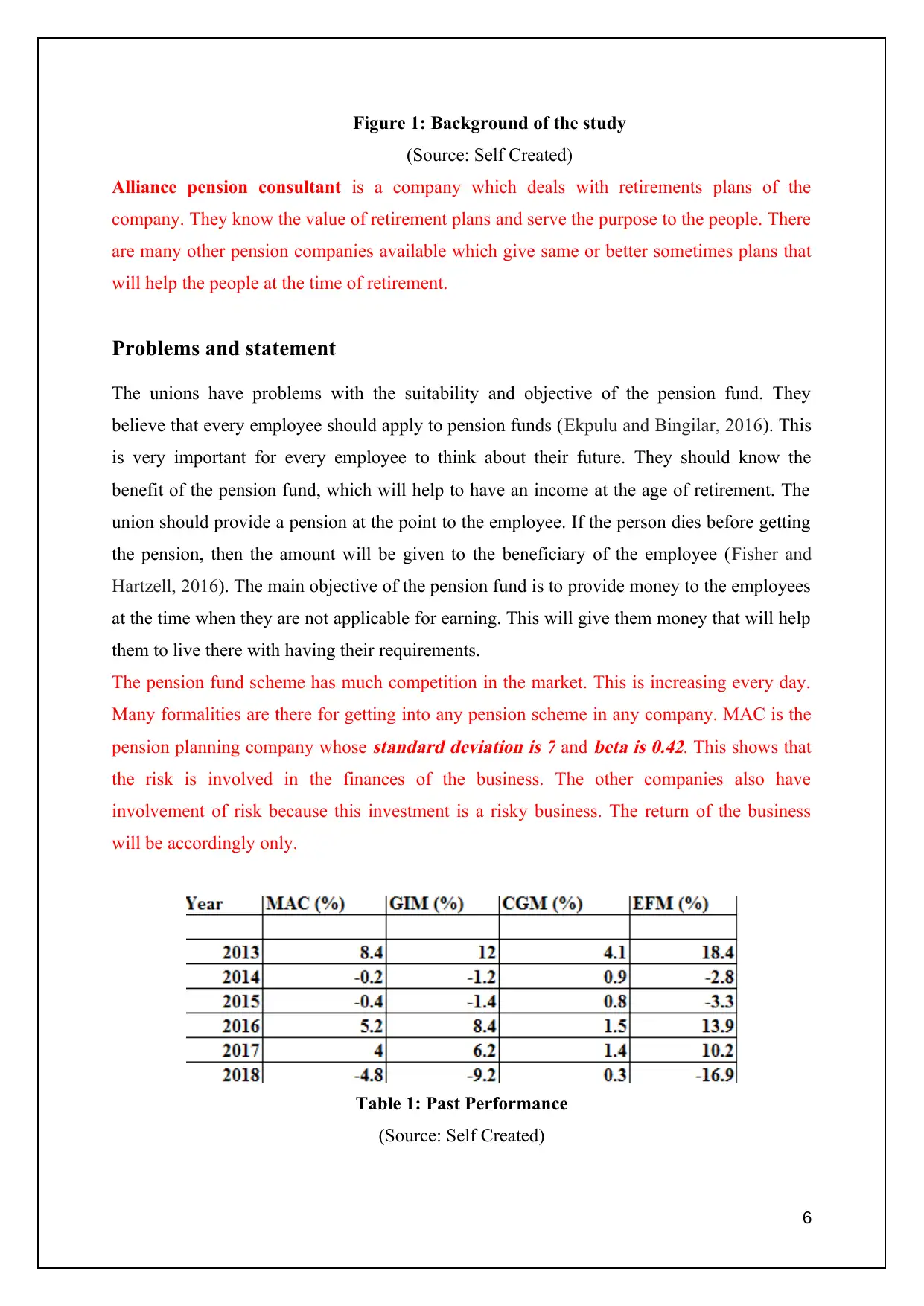

Figure 1: Background of the study

(Source: Self Created)

Alliance pension consultant is a company which deals with retirements plans of the

company. They know the value of retirement plans and serve the purpose to the people. There

are many other pension companies available which give same or better sometimes plans that

will help the people at the time of retirement.

Problems and statement

The unions have problems with the suitability and objective of the pension fund. They

believe that every employee should apply to pension funds (Ekpulu and Bingilar, 2016). This

is very important for every employee to think about their future. They should know the

benefit of the pension fund, which will help to have an income at the age of retirement. The

union should provide a pension at the point to the employee. If the person dies before getting

the pension, then the amount will be given to the beneficiary of the employee (Fisher and

Hartzell, 2016). The main objective of the pension fund is to provide money to the employees

at the time when they are not applicable for earning. This will give them money that will help

them to live there with having their requirements.

The pension fund scheme has much competition in the market. This is increasing every day.

Many formalities are there for getting into any pension scheme in any company. MAC is the

pension planning company whose

standard deviation is 7 and

beta is 0.42. This shows that

the risk is involved in the finances of the business. The other companies also have

involvement of risk because this investment is a risky business. The return of the business

will be accordingly only.

Table 1: Past Performance

(Source: Self Created)

6

(Source: Self Created)

Alliance pension consultant is a company which deals with retirements plans of the

company. They know the value of retirement plans and serve the purpose to the people. There

are many other pension companies available which give same or better sometimes plans that

will help the people at the time of retirement.

Problems and statement

The unions have problems with the suitability and objective of the pension fund. They

believe that every employee should apply to pension funds (Ekpulu and Bingilar, 2016). This

is very important for every employee to think about their future. They should know the

benefit of the pension fund, which will help to have an income at the age of retirement. The

union should provide a pension at the point to the employee. If the person dies before getting

the pension, then the amount will be given to the beneficiary of the employee (Fisher and

Hartzell, 2016). The main objective of the pension fund is to provide money to the employees

at the time when they are not applicable for earning. This will give them money that will help

them to live there with having their requirements.

The pension fund scheme has much competition in the market. This is increasing every day.

Many formalities are there for getting into any pension scheme in any company. MAC is the

pension planning company whose

standard deviation is 7 and

beta is 0.42. This shows that

the risk is involved in the finances of the business. The other companies also have

involvement of risk because this investment is a risky business. The return of the business

will be accordingly only.

Table 1: Past Performance

(Source: Self Created)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

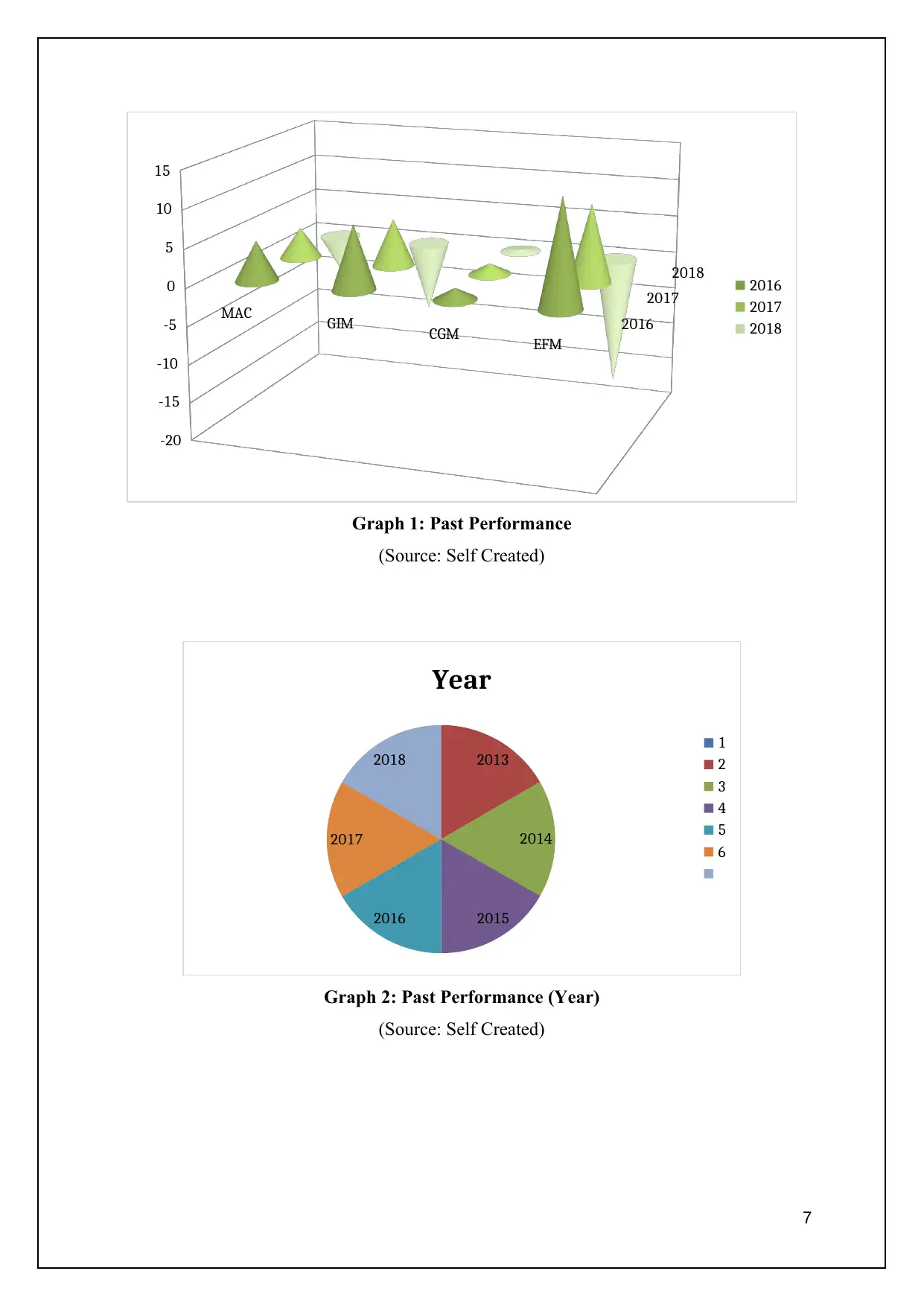

MAC GIM CGM EFM

-20

-15

-10

-5

0

5

10

15

2016

2017

2018 2016

2017

2018

Graph 1: Past Performance

(Source: Self Created)

2013

2014

20152016

2017

2018

Year

1

2

3

4

5

6

Graph 2: Past Performance (Year)

(Source: Self Created)

7

-20

-15

-10

-5

0

5

10

15

2016

2017

2018 2016

2017

2018

Graph 1: Past Performance

(Source: Self Created)

2013

2014

20152016

2017

2018

Year

1

2

3

4

5

6

Graph 2: Past Performance (Year)

(Source: Self Created)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Findings and analysis

● Claims of managers

The manager helps the company to manage their department of pension funds. These

departments take care of the pension fund collection and pass the bill. They need to

look after all the aspects of the company and its employees. They managed the

accounts of the individual employees so that the employees get their benefit at the

time of retirement. Alliance Pension Company has employees and managers who help

them to get knowledge about the plans that customers would want. This helps them to

know about their clients and their requirements.

● Risk-adjusted measures

The money collected from the employees is investments in funds or securities.

However, the return of such a market is not consistent. It depends upon the market

factor that the rate is fluctuating (Mutula and Kagiri, 2018). So the investment of the

money should be made by the officials who know the market. There is always the risk

that is involved in the share market. The risk involved in the alliance pension

company or any other company will be high because the Investment Company works

based on data. However, sometimes, the data analysis might affect the economic

condition. The measures should be strong enough to analyze the losses.

● Stock market index

This affects the pension received to the employees. If the money is invested in

inadequate plans and fund, then the return will be low. The stock market is the

fluctuating market and does not depend upon anything. The prices change every day

with any decision taken by the government or the company. So investing the money

of the pension fund to the stock is quite risking. However, taking a risk will give more

profits. Index marketing is used to duplicate the effect of a specific index. The

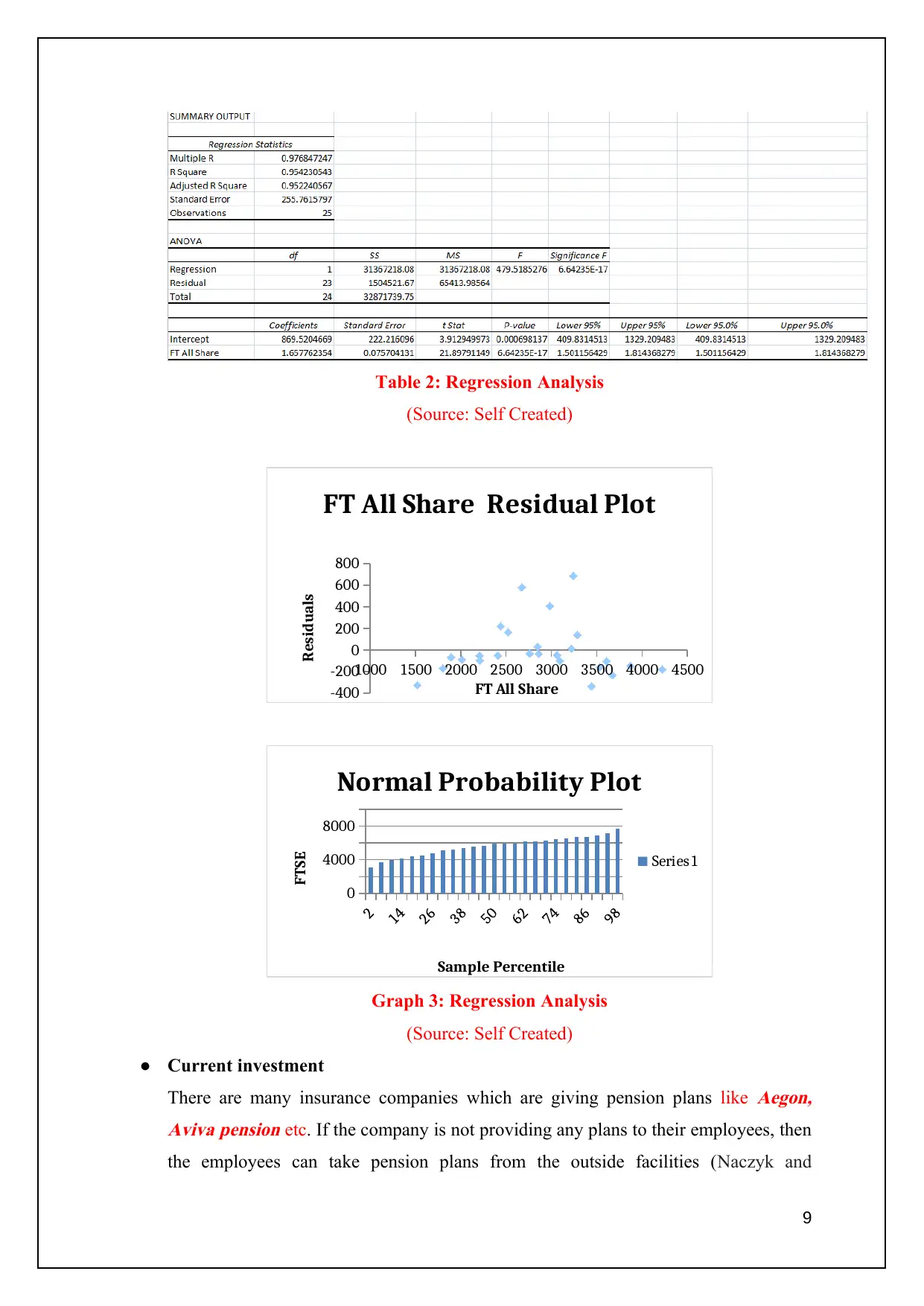

specific index includes “equity or fixed income index”. The regression (R Square)

of the alliance pension is 0.954230543 that is according to data that was provided.

The company needs to work more on their plans and strategies in order to sustain the

business.

8

● Claims of managers

The manager helps the company to manage their department of pension funds. These

departments take care of the pension fund collection and pass the bill. They need to

look after all the aspects of the company and its employees. They managed the

accounts of the individual employees so that the employees get their benefit at the

time of retirement. Alliance Pension Company has employees and managers who help

them to get knowledge about the plans that customers would want. This helps them to

know about their clients and their requirements.

● Risk-adjusted measures

The money collected from the employees is investments in funds or securities.

However, the return of such a market is not consistent. It depends upon the market

factor that the rate is fluctuating (Mutula and Kagiri, 2018). So the investment of the

money should be made by the officials who know the market. There is always the risk

that is involved in the share market. The risk involved in the alliance pension

company or any other company will be high because the Investment Company works

based on data. However, sometimes, the data analysis might affect the economic

condition. The measures should be strong enough to analyze the losses.

● Stock market index

This affects the pension received to the employees. If the money is invested in

inadequate plans and fund, then the return will be low. The stock market is the

fluctuating market and does not depend upon anything. The prices change every day

with any decision taken by the government or the company. So investing the money

of the pension fund to the stock is quite risking. However, taking a risk will give more

profits. Index marketing is used to duplicate the effect of a specific index. The

specific index includes “equity or fixed income index”. The regression (R Square)

of the alliance pension is 0.954230543 that is according to data that was provided.

The company needs to work more on their plans and strategies in order to sustain the

business.

8

Table 2: Regression Analysis

(Source: Self Created)

1000 1500 2000 2500 3000 3500 4000 4500

-400

-200

0

200

400

600

800

FT All Share Residual Plot

FT All Share

Residuals

0

4000

8000

Normal Probability Plot

Series1

Sample Percentile

FTSE

Graph 3: Regression Analysis

(Source: Self Created)

● Current investment

There are many insurance companies which are giving pension plans like

Aegon,

Aviva pension etc. If the company is not providing any plans to their employees, then

the employees can take pension plans from the outside facilities (Naczyk and

9

(Source: Self Created)

1000 1500 2000 2500 3000 3500 4000 4500

-400

-200

0

200

400

600

800

FT All Share Residual Plot

FT All Share

Residuals

0

4000

8000

Normal Probability Plot

Series1

Sample Percentile

FTSE

Graph 3: Regression Analysis

(Source: Self Created)

● Current investment

There are many insurance companies which are giving pension plans like

Aegon,

Aviva pension etc. If the company is not providing any plans to their employees, then

the employees can take pension plans from the outside facilities (Naczyk and

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Domonkos, 2016). This will take a certain amount of their every month and will be

given to them at the time of retirement. The plans and strategies of such company are

essential for the other competitive company. This will help the alliance pension

company to know about the investment structure and facilities that are attracting

customers. (sdg.iisd.org, 2019)

● International diversification

Many countries are working on their pension plans, which will help the ageing

people. The international market has so many competitive companies that are giving

pension plans to benefit the customers. The alliance pension fund should know all the

companies to enhance their business. International diversification plays an important

role in fundamentally justifying the portfolio as:

❏ Enhancing the pool of potential assets

❏ The returns can be increased by the investors that will help to reduce the risk

with the

selection of “complementary assets” with “low correlation”.

Figure 2: International diversification

(Source: Self Created)

● Investment in gilts

Gilts are issued by the government known as

“gilt-edged securities”. These securities

give money to the government, i.e. the money investing is going to the government.

10

Enhancing the pool of

potential assets

Selection of

“complementary assets”

with “low correlation

given to them at the time of retirement. The plans and strategies of such company are

essential for the other competitive company. This will help the alliance pension

company to know about the investment structure and facilities that are attracting

customers. (sdg.iisd.org, 2019)

● International diversification

Many countries are working on their pension plans, which will help the ageing

people. The international market has so many competitive companies that are giving

pension plans to benefit the customers. The alliance pension fund should know all the

companies to enhance their business. International diversification plays an important

role in fundamentally justifying the portfolio as:

❏ Enhancing the pool of potential assets

❏ The returns can be increased by the investors that will help to reduce the risk

with the

selection of “complementary assets” with “low correlation”.

Figure 2: International diversification

(Source: Self Created)

● Investment in gilts

Gilts are issued by the government known as

“gilt-edged securities”. These securities

give money to the government, i.e. the money investing is going to the government.

10

Enhancing the pool of

potential assets

Selection of

“complementary assets”

with “low correlation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These are issues as 100 million pounds units. The income of the investment is fixed,

and the term is also fixed. Nominal capital value is paid to the investors when the gilt

is matured. When the interest rate is low, then it is said to be the ideal time for

investing in gilt. These are government securities, so they are benefited with

“20%

indexation benefit” (Norris, 2017). The company GIM have a standard deviation of

11.8 and a beta of 0.74. It is seen that the risks involved are negligible, but this risk

can be anytime increased. The alliance company should look at the plans of the other

companies like Aviva pension, Aegon pension. These are one of the leading pension

companies in the US. Plans and strategies are essential for other companies. Every

company should know about its competitive firm.

● Hedge funds

It is another option for investing pension money. This fund gives good returns. They

attract investors by pooling the capital and investing in different assets. They have

“complex portfolio management” and

“risk management techniques. In fund

equity, the interest exchange is contributed to the capital by investors or individually

to raise money. These funds do not use an advertisement, which makes it unavailable

for many potential investors. These work mainly within closed markets. Hedge funds

get many exceptions in the securities act. Minimum of $1 million is required to

participate in the hedge fund. The managers and partners make this regulation of the

fund. This fund includes high risk (Ząbkowicz, 2019). The risk is so high that it can

destroy the entire investment. As high risk is involved, so the growth rate is also high

in this fund. This fund can be in any “land”, “real estate” and any “other alternative

assets”. (pensionseurope.eu, 2019)

● Exchange-traded funds

These are “collection of securities”, for example

, stocks, "mixture of investment",

bonds or

commodities. There are "traded" into open markets which make readily

available for the investors. The change in marketing habits will be known as the

investor. IPO launch these funds in the market to gain more money in the "open

market" which is like stock. These stocks can be purchased through:

❏ They are open stock traded in the market precisely like stocks

❏ The taxes levied in this stock are less.

❏ As it is precisely like stocks, so the individual has to pay a "brokerage

commission" whenever they buy or sell the shares.

11

and the term is also fixed. Nominal capital value is paid to the investors when the gilt

is matured. When the interest rate is low, then it is said to be the ideal time for

investing in gilt. These are government securities, so they are benefited with

“20%

indexation benefit” (Norris, 2017). The company GIM have a standard deviation of

11.8 and a beta of 0.74. It is seen that the risks involved are negligible, but this risk

can be anytime increased. The alliance company should look at the plans of the other

companies like Aviva pension, Aegon pension. These are one of the leading pension

companies in the US. Plans and strategies are essential for other companies. Every

company should know about its competitive firm.

● Hedge funds

It is another option for investing pension money. This fund gives good returns. They

attract investors by pooling the capital and investing in different assets. They have

“complex portfolio management” and

“risk management techniques. In fund

equity, the interest exchange is contributed to the capital by investors or individually

to raise money. These funds do not use an advertisement, which makes it unavailable

for many potential investors. These work mainly within closed markets. Hedge funds

get many exceptions in the securities act. Minimum of $1 million is required to

participate in the hedge fund. The managers and partners make this regulation of the

fund. This fund includes high risk (Ząbkowicz, 2019). The risk is so high that it can

destroy the entire investment. As high risk is involved, so the growth rate is also high

in this fund. This fund can be in any “land”, “real estate” and any “other alternative

assets”. (pensionseurope.eu, 2019)

● Exchange-traded funds

These are “collection of securities”, for example

, stocks, "mixture of investment",

bonds or

commodities. There are "traded" into open markets which make readily

available for the investors. The change in marketing habits will be known as the

investor. IPO launch these funds in the market to gain more money in the "open

market" which is like stock. These stocks can be purchased through:

❏ They are open stock traded in the market precisely like stocks

❏ The taxes levied in this stock are less.

❏ As it is precisely like stocks, so the individual has to pay a "brokerage

commission" whenever they buy or sell the shares.

11

These are a few of the options in which the amount of the pension plan can be invested. This

will help the insurance company or the company who has its pension plan for employees to

invest in getting huge returns. (News media alliance.org, 2019)

Conclusion

There are different funds in the stock market. Some are risk-oriented, and others are risk-free.

It depends upon the company in which shares they want to invest the money. They need a

person who understands the market fluctuation and managing these funds. The other option is

the insurance companies which are providing pension plans for the employees. Alliance

Pension Company is one of the leading companies in retirement plans. However, many other

companies are also earning huge profits. Companies like Aegon, which is doing good

business. So it is essential to have good policies, as it attracts customers. This will help to

make better policies than other competitive companies. In addition to this, The company GIM

have a standard deviation of 11.8 and a beta of 0.74 which reveals that in order to have 1 %

of return company will have .74 beta which is showing the low level of risk with high return

it will help in strengthen the return on capital employed invested in the selected pension fund.

However, investing capital in this pension fund will be beneficial and will stable earning to

the investors. Although, this company needs to work more on their plans and strategies in

order to sustain the business. Furthermore, MAC is the pension planning company whosestandard deviation is 7 and

beta is 0.42. This shows that the risk is involved in the finances

of the business but as compared to investment return, this company will give much better

return. The strategy would be to take low risk and high return. This will give higher return to

create value on this investment with low risk.

12

will help the insurance company or the company who has its pension plan for employees to

invest in getting huge returns. (News media alliance.org, 2019)

Conclusion

There are different funds in the stock market. Some are risk-oriented, and others are risk-free.

It depends upon the company in which shares they want to invest the money. They need a

person who understands the market fluctuation and managing these funds. The other option is

the insurance companies which are providing pension plans for the employees. Alliance

Pension Company is one of the leading companies in retirement plans. However, many other

companies are also earning huge profits. Companies like Aegon, which is doing good

business. So it is essential to have good policies, as it attracts customers. This will help to

make better policies than other competitive companies. In addition to this, The company GIM

have a standard deviation of 11.8 and a beta of 0.74 which reveals that in order to have 1 %

of return company will have .74 beta which is showing the low level of risk with high return

it will help in strengthen the return on capital employed invested in the selected pension fund.

However, investing capital in this pension fund will be beneficial and will stable earning to

the investors. Although, this company needs to work more on their plans and strategies in

order to sustain the business. Furthermore, MAC is the pension planning company whosestandard deviation is 7 and

beta is 0.42. This shows that the risk is involved in the finances

of the business but as compared to investment return, this company will give much better

return. The strategy would be to take low risk and high return. This will give higher return to

create value on this investment with low risk.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.