Comprehensive Financial Analysis of Almarai Company (2016-2017)

VerifiedAdded on 2022/11/18

|16

|2960

|474

Report

AI Summary

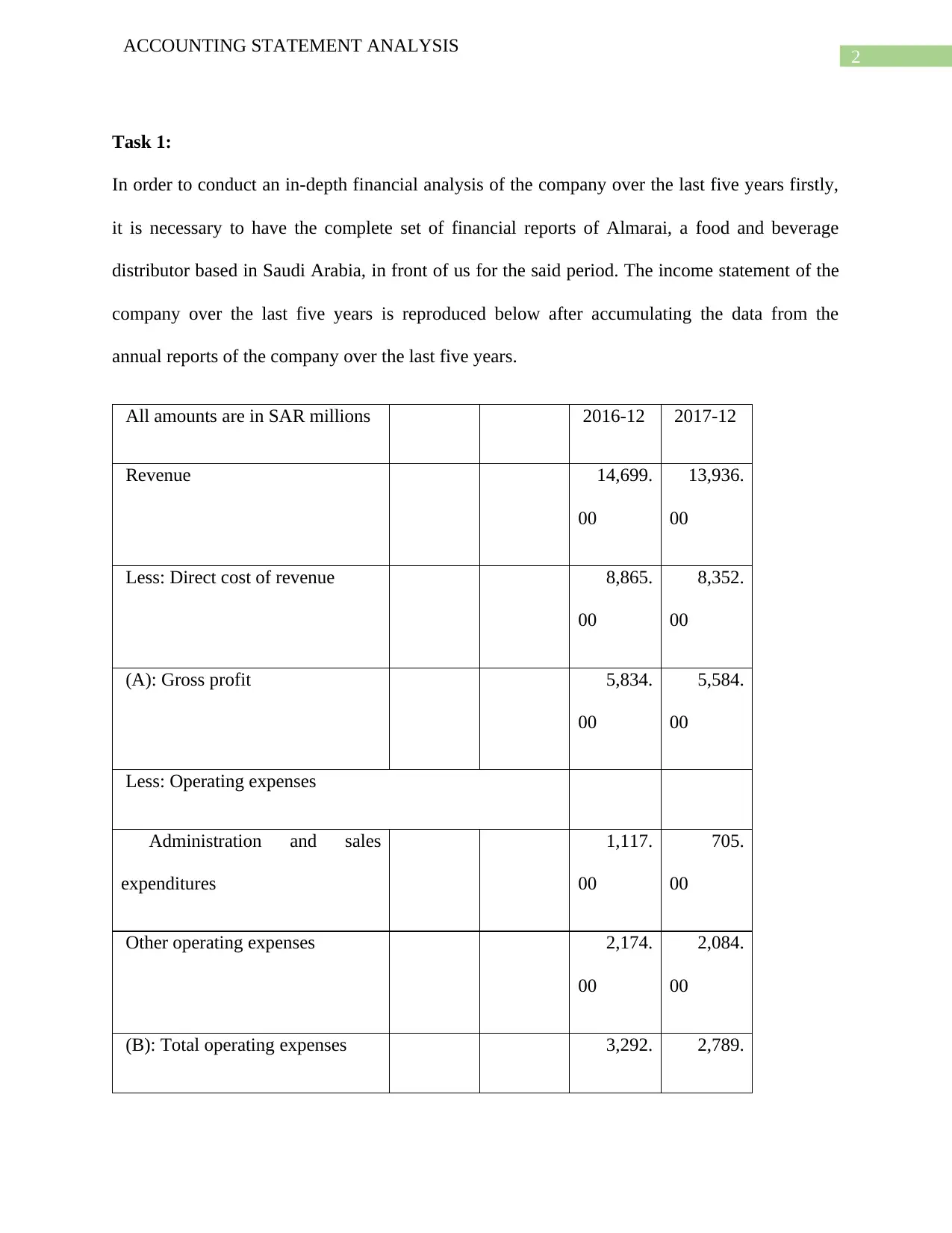

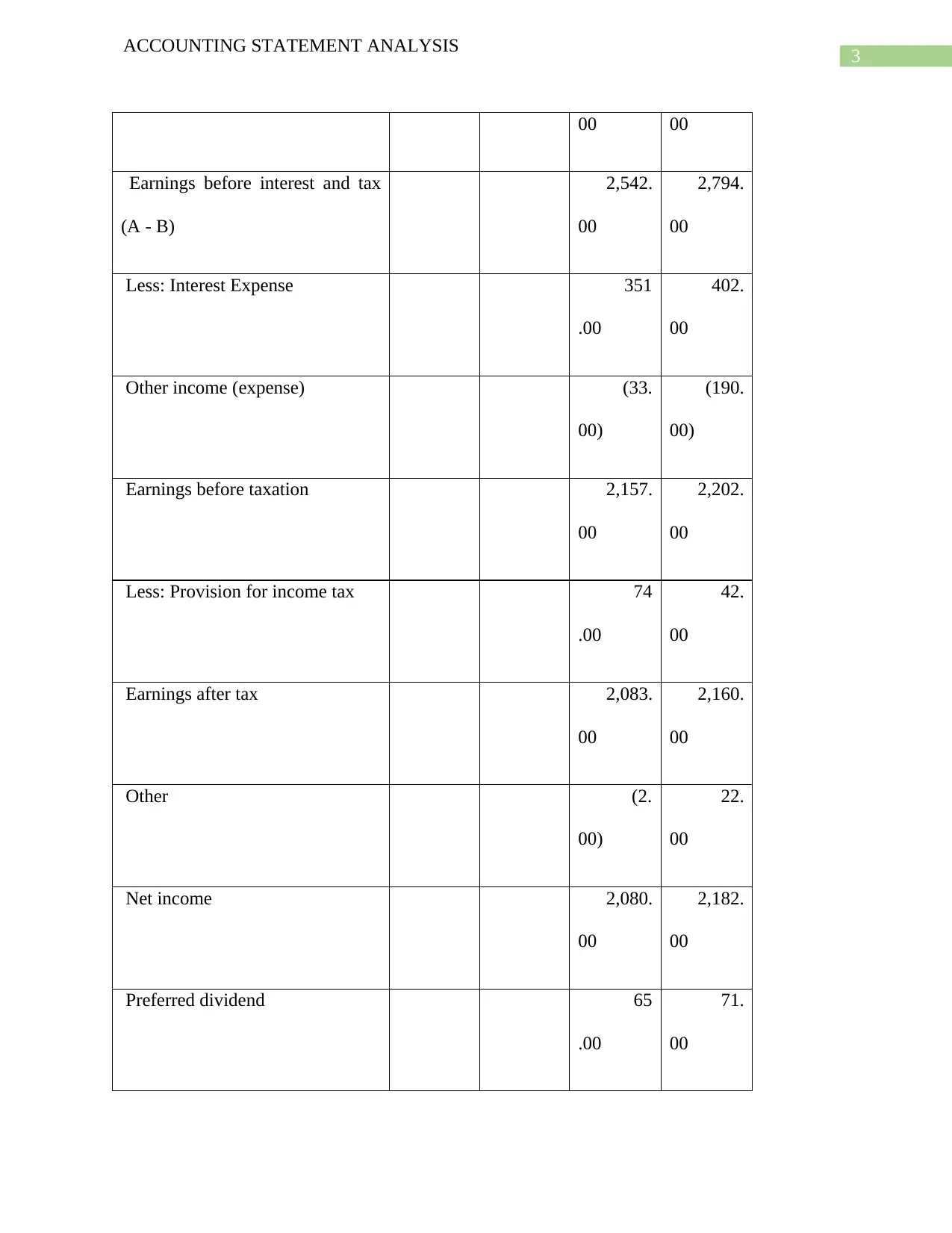

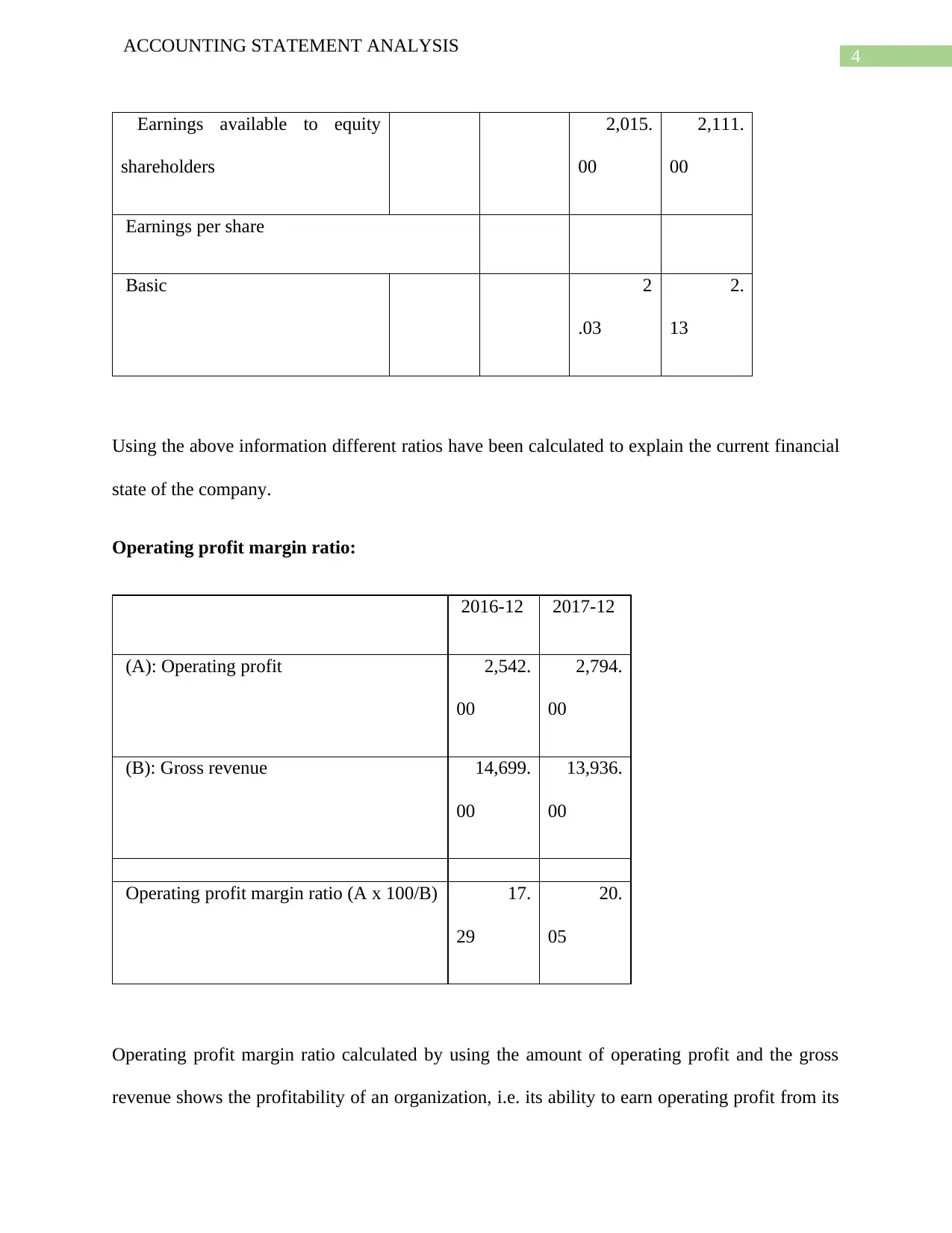

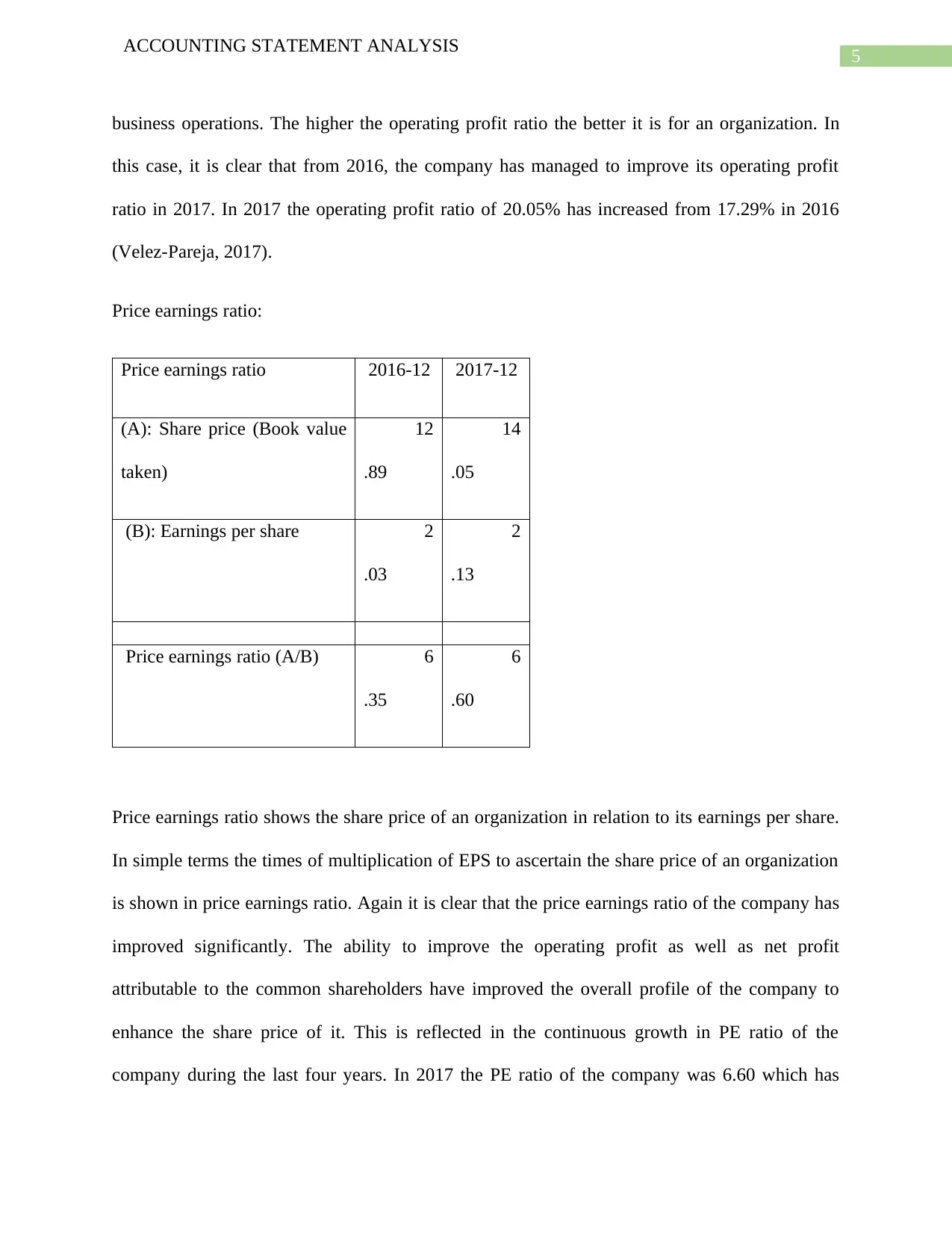

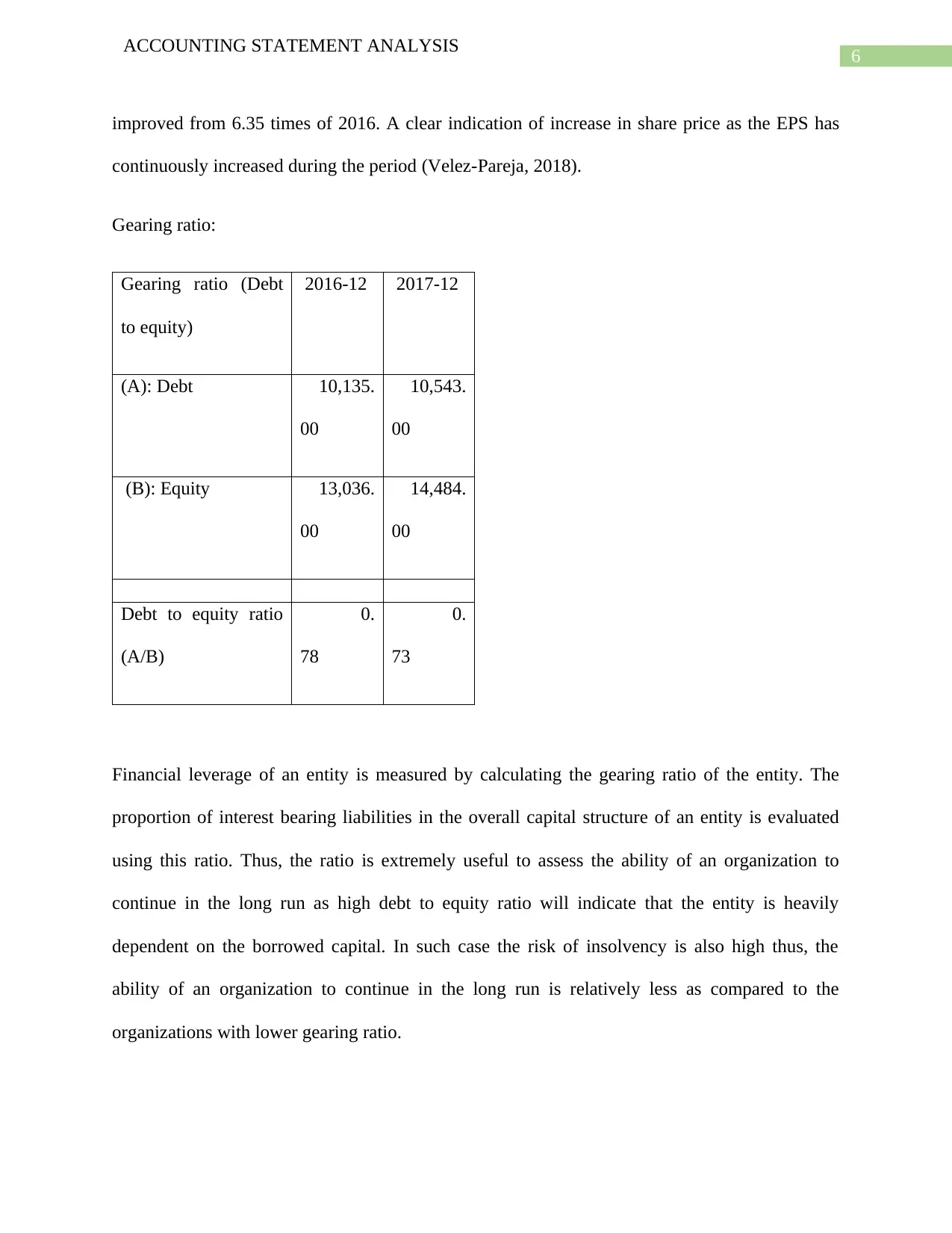

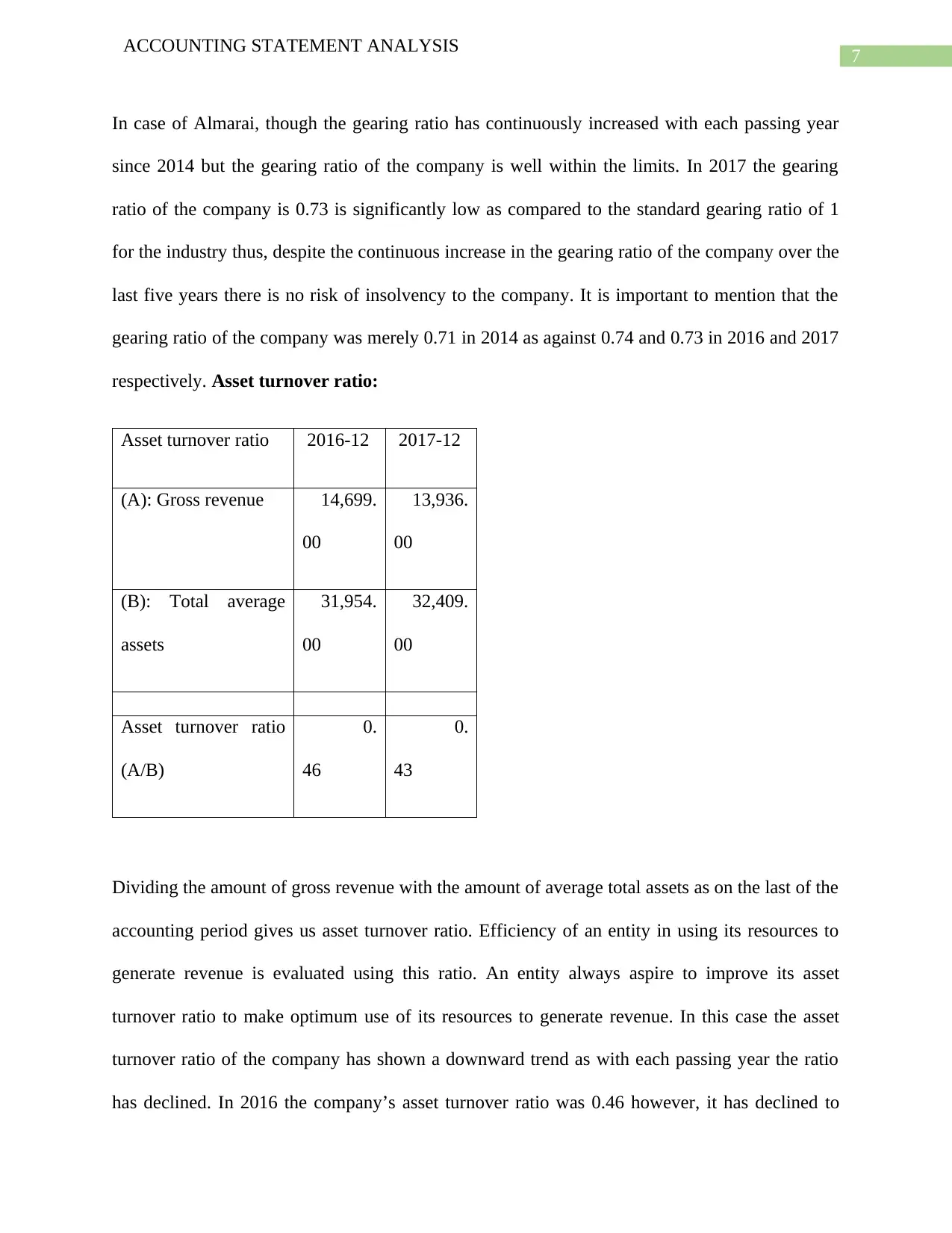

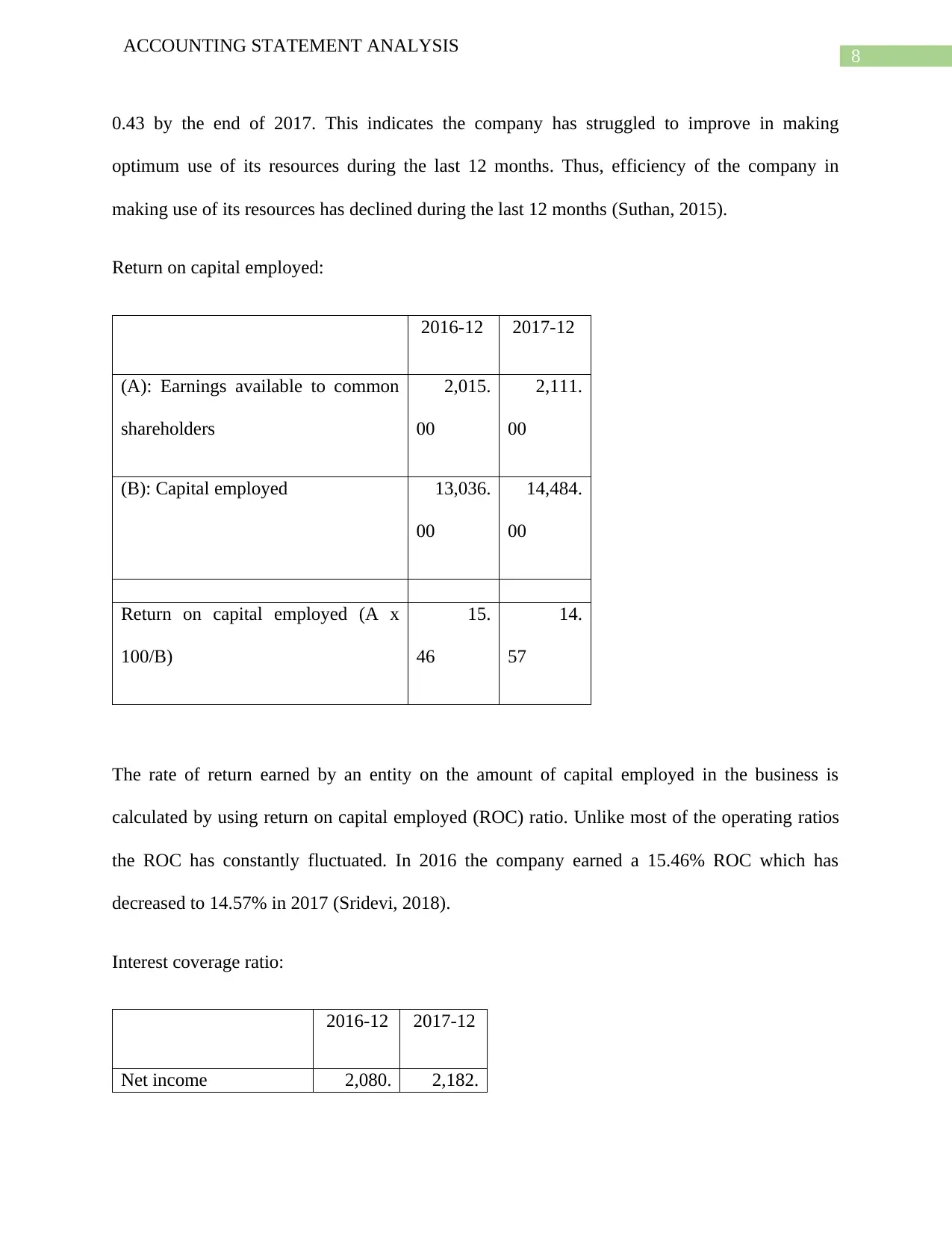

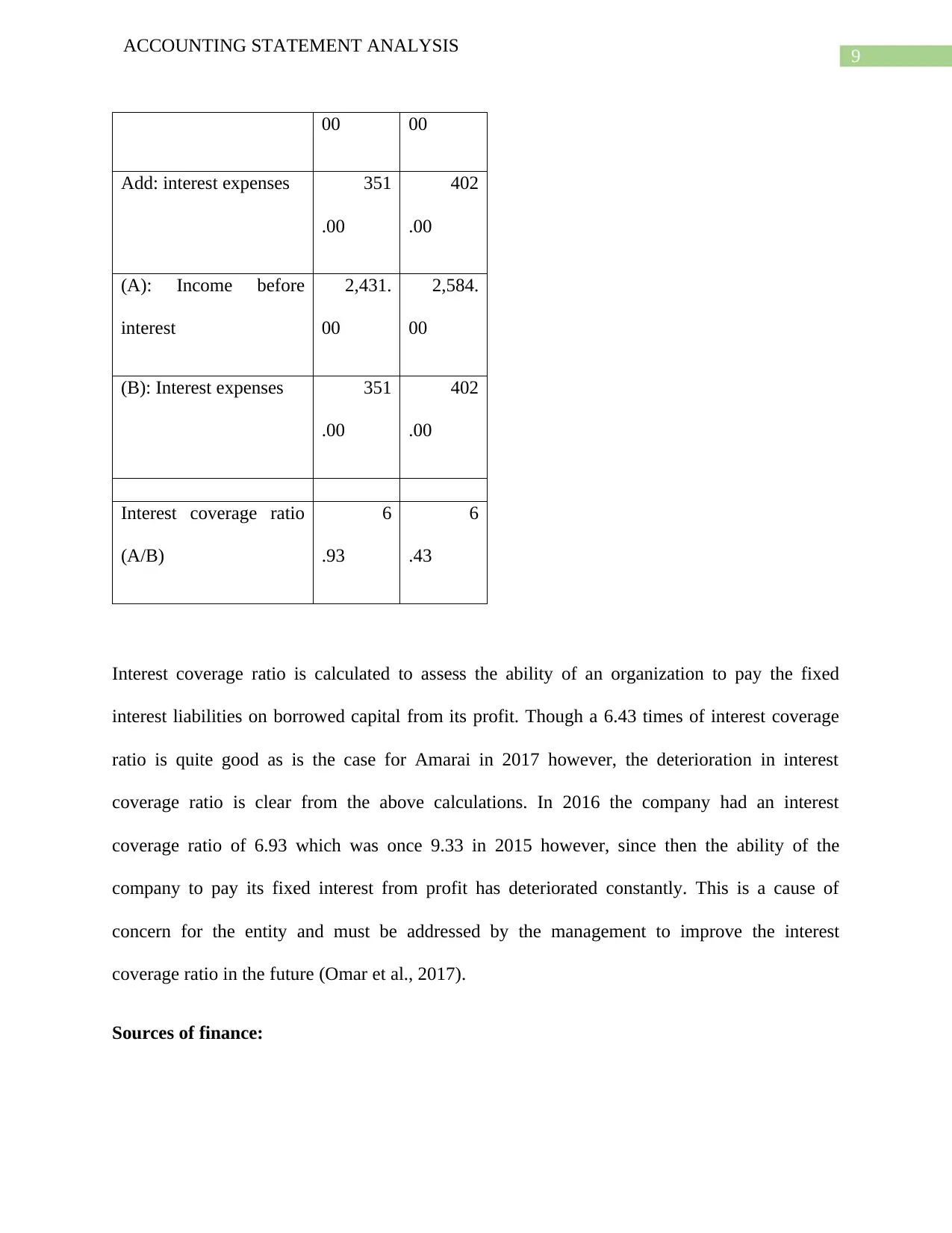

This report presents a detailed financial analysis of Almarai, a Saudi Arabian food and beverage company, examining its performance from 2016 to 2017. The analysis includes the calculation and interpretation of key financial ratios such as operating profit margin, price earnings ratio, gearing ratio, asset turnover ratio, return on capital employed, and interest coverage ratio, providing insights into the company's profitability, efficiency, and solvency. The report also explores the sources of finance for Almarai and the importance of budgeting for business operations, discussing the pros and cons of budgeting and the impact of technological advancements on financial management practices. The analysis highlights trends in Almarai's financial performance, including improvements in operating profit and price earnings ratios, while also noting areas of concern such as declining asset turnover and interest coverage ratios, and the impact of debt on financial leverage.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.