Alpaka.io: Discounted Cash Flow and Earnings Valuation Report

VerifiedAdded on 2022/09/01

|16

|2966

|18

Report

AI Summary

This report provides a comprehensive financial analysis of Alpaka.io, a five-year-old software startup. The analysis employs the Discounted Cash Flow (DCF) and Earnings Multiple methods to determine the company's valuation under various scenarios. The report includes detailed calculations and assumptions for each case, considering factors such as Weighted Average Cost of Capital (WACC), growth rates, and industry averages. The analysis explores potential exit strategies, including IPOs and strategic sales, based on the different valuation results. Furthermore, it discusses alternative investment avenues, such as angel investors, venture capitalists, and loans, to assess the company's expansion possibilities. The report concludes with a discussion of caveats and limitations, offering a well-rounded view of Alpaka.io's financial position and future prospects.

Running head: ALPAKA ANALYSIS

Alpaka Analysis

Name of the Student:

Name of the University:

Author Note:

Alpaka Analysis

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ALPAKA ANALYSIS

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Discounted Cash Flow and Earnings Method:.......................................................................2

Discounted Cash Flow Case 1:..........................................................................................2

Earnings Multiple Method Case 1:....................................................................................4

Discounted Cash Flow Case 2:..........................................................................................5

Earnings Multiple Method Case 2:....................................................................................7

Discounted Cash Flow Case 3:..........................................................................................8

Earnings Multiple Method Case 3:....................................................................................9

Exit strategy:........................................................................................................................10

Case 1:..............................................................................................................................10

Case 2:..............................................................................................................................11

Case 3:..............................................................................................................................11

Caveats:............................................................................................................................11

Other Investment Avenues:..................................................................................................12

Conclusion:..............................................................................................................................12

References:...............................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Discounted Cash Flow and Earnings Method:.......................................................................2

Discounted Cash Flow Case 1:..........................................................................................2

Earnings Multiple Method Case 1:....................................................................................4

Discounted Cash Flow Case 2:..........................................................................................5

Earnings Multiple Method Case 2:....................................................................................7

Discounted Cash Flow Case 3:..........................................................................................8

Earnings Multiple Method Case 3:....................................................................................9

Exit strategy:........................................................................................................................10

Case 1:..............................................................................................................................10

Case 2:..............................................................................................................................11

Case 3:..............................................................................................................................11

Caveats:............................................................................................................................11

Other Investment Avenues:..................................................................................................12

Conclusion:..............................................................................................................................12

References:...............................................................................................................................14

2ALPAKA ANALYSIS

Introduction:

The Company Alpaka.io is a start-up company which had been in operation from the

past 5 years. The company is based in New South Wales and England and has been providing

Software services to various Companies. The Calender management service which the

company provides is the sole generator of revenue for the company. It enhances the

production and management of the companies which are taking the service from this

company. Since the software which is provided by the company enables the company to be

flexible in its services such that the companies which it caters to are never dissatisfied with its

services (alpaka.io).

In the following report the valuation of the company after 3 years is analysed using

the discounted cash flow method and the earnings multiple method. The valuation is

conducted to analyse the relevant exit strategies for the company which it can undertake after

3 years. Different scenarios and valuations are incorporated with the different stock price

which is expected after 3 years.

Discussion:

Discounted Cash Flow and Earnings Method:

Discounted Cash Flow Case 1:

The discounted cash flow is the discounting of the expected cash flows at a relevant

discount rate to analyse the present value of the company. Thus the free cash flow for the

firm is calculated using the formula,

FCFF= Net Income+Depreciation+int *(1-tax rate)- Capex -Changes in working capital

Introduction:

The Company Alpaka.io is a start-up company which had been in operation from the

past 5 years. The company is based in New South Wales and England and has been providing

Software services to various Companies. The Calender management service which the

company provides is the sole generator of revenue for the company. It enhances the

production and management of the companies which are taking the service from this

company. Since the software which is provided by the company enables the company to be

flexible in its services such that the companies which it caters to are never dissatisfied with its

services (alpaka.io).

In the following report the valuation of the company after 3 years is analysed using

the discounted cash flow method and the earnings multiple method. The valuation is

conducted to analyse the relevant exit strategies for the company which it can undertake after

3 years. Different scenarios and valuations are incorporated with the different stock price

which is expected after 3 years.

Discussion:

Discounted Cash Flow and Earnings Method:

Discounted Cash Flow Case 1:

The discounted cash flow is the discounting of the expected cash flows at a relevant

discount rate to analyse the present value of the company. Thus the free cash flow for the

firm is calculated using the formula,

FCFF= Net Income+Depreciation+int *(1-tax rate)- Capex -Changes in working capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ALPAKA ANALYSIS

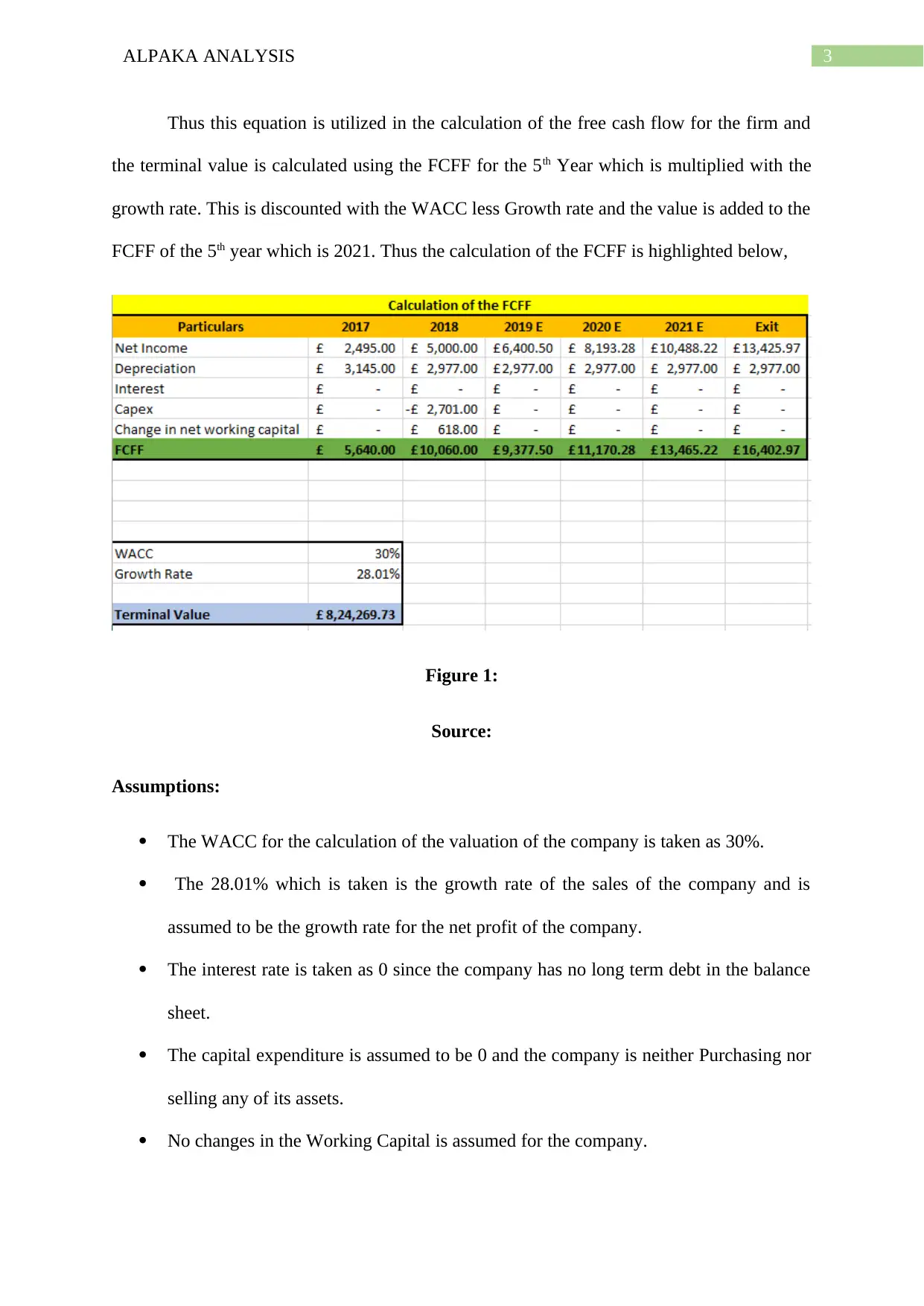

Thus this equation is utilized in the calculation of the free cash flow for the firm and

the terminal value is calculated using the FCFF for the 5th Year which is multiplied with the

growth rate. This is discounted with the WACC less Growth rate and the value is added to the

FCFF of the 5th year which is 2021. Thus the calculation of the FCFF is highlighted below,

Figure 1:

Source:

Assumptions:

The WACC for the calculation of the valuation of the company is taken as 30%.

The 28.01% which is taken is the growth rate of the sales of the company and is

assumed to be the growth rate for the net profit of the company.

The interest rate is taken as 0 since the company has no long term debt in the balance

sheet.

The capital expenditure is assumed to be 0 and the company is neither Purchasing nor

selling any of its assets.

No changes in the Working Capital is assumed for the company.

Thus this equation is utilized in the calculation of the free cash flow for the firm and

the terminal value is calculated using the FCFF for the 5th Year which is multiplied with the

growth rate. This is discounted with the WACC less Growth rate and the value is added to the

FCFF of the 5th year which is 2021. Thus the calculation of the FCFF is highlighted below,

Figure 1:

Source:

Assumptions:

The WACC for the calculation of the valuation of the company is taken as 30%.

The 28.01% which is taken is the growth rate of the sales of the company and is

assumed to be the growth rate for the net profit of the company.

The interest rate is taken as 0 since the company has no long term debt in the balance

sheet.

The capital expenditure is assumed to be 0 and the company is neither Purchasing nor

selling any of its assets.

No changes in the Working Capital is assumed for the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ALPAKA ANALYSIS

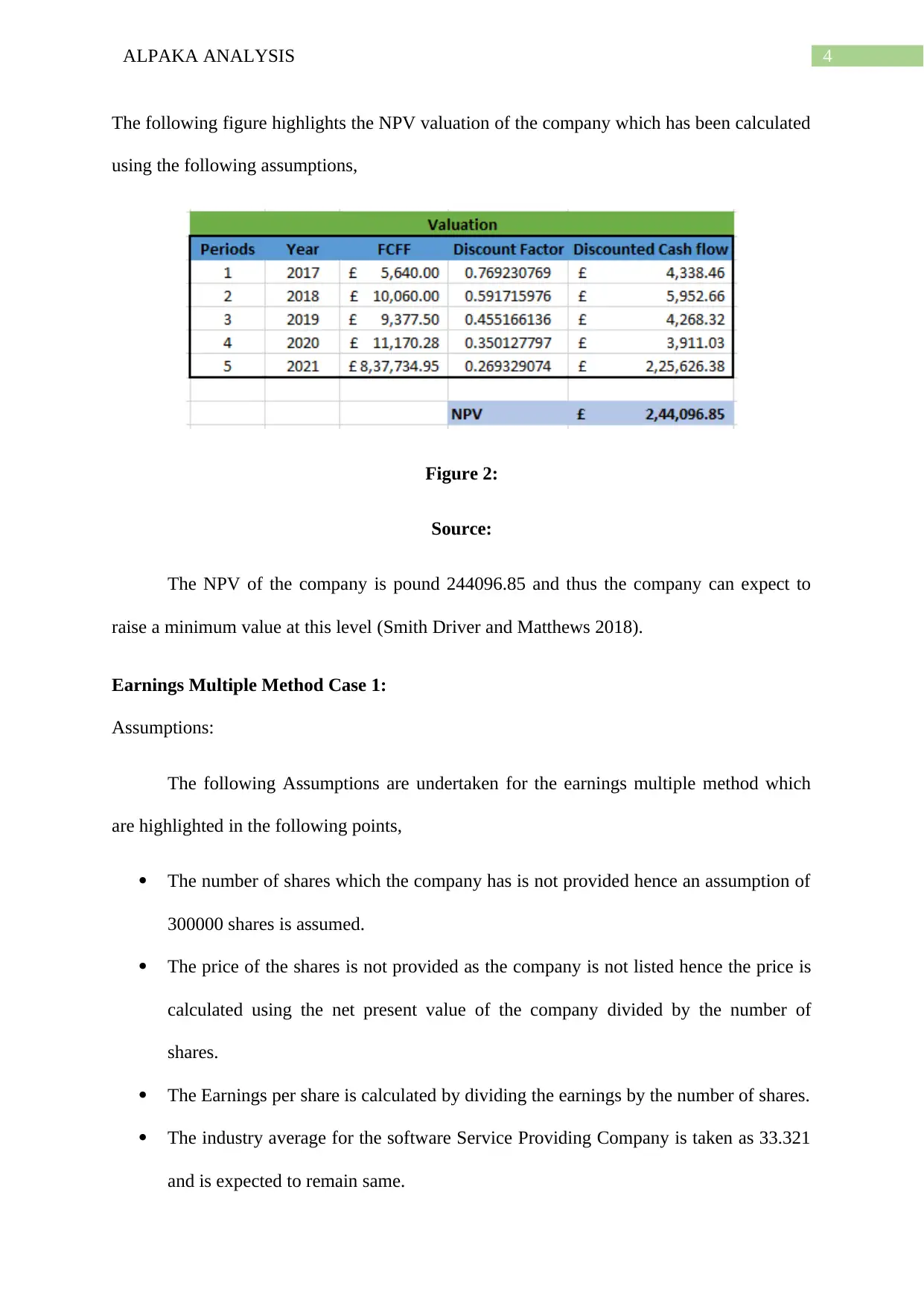

The following figure highlights the NPV valuation of the company which has been calculated

using the following assumptions,

Figure 2:

Source:

The NPV of the company is pound 244096.85 and thus the company can expect to

raise a minimum value at this level (Smith Driver and Matthews 2018).

Earnings Multiple Method Case 1:

Assumptions:

The following Assumptions are undertaken for the earnings multiple method which

are highlighted in the following points,

The number of shares which the company has is not provided hence an assumption of

300000 shares is assumed.

The price of the shares is not provided as the company is not listed hence the price is

calculated using the net present value of the company divided by the number of

shares.

The Earnings per share is calculated by dividing the earnings by the number of shares.

The industry average for the software Service Providing Company is taken as 33.321

and is expected to remain same.

The following figure highlights the NPV valuation of the company which has been calculated

using the following assumptions,

Figure 2:

Source:

The NPV of the company is pound 244096.85 and thus the company can expect to

raise a minimum value at this level (Smith Driver and Matthews 2018).

Earnings Multiple Method Case 1:

Assumptions:

The following Assumptions are undertaken for the earnings multiple method which

are highlighted in the following points,

The number of shares which the company has is not provided hence an assumption of

300000 shares is assumed.

The price of the shares is not provided as the company is not listed hence the price is

calculated using the net present value of the company divided by the number of

shares.

The Earnings per share is calculated by dividing the earnings by the number of shares.

The industry average for the software Service Providing Company is taken as 33.321

and is expected to remain same.

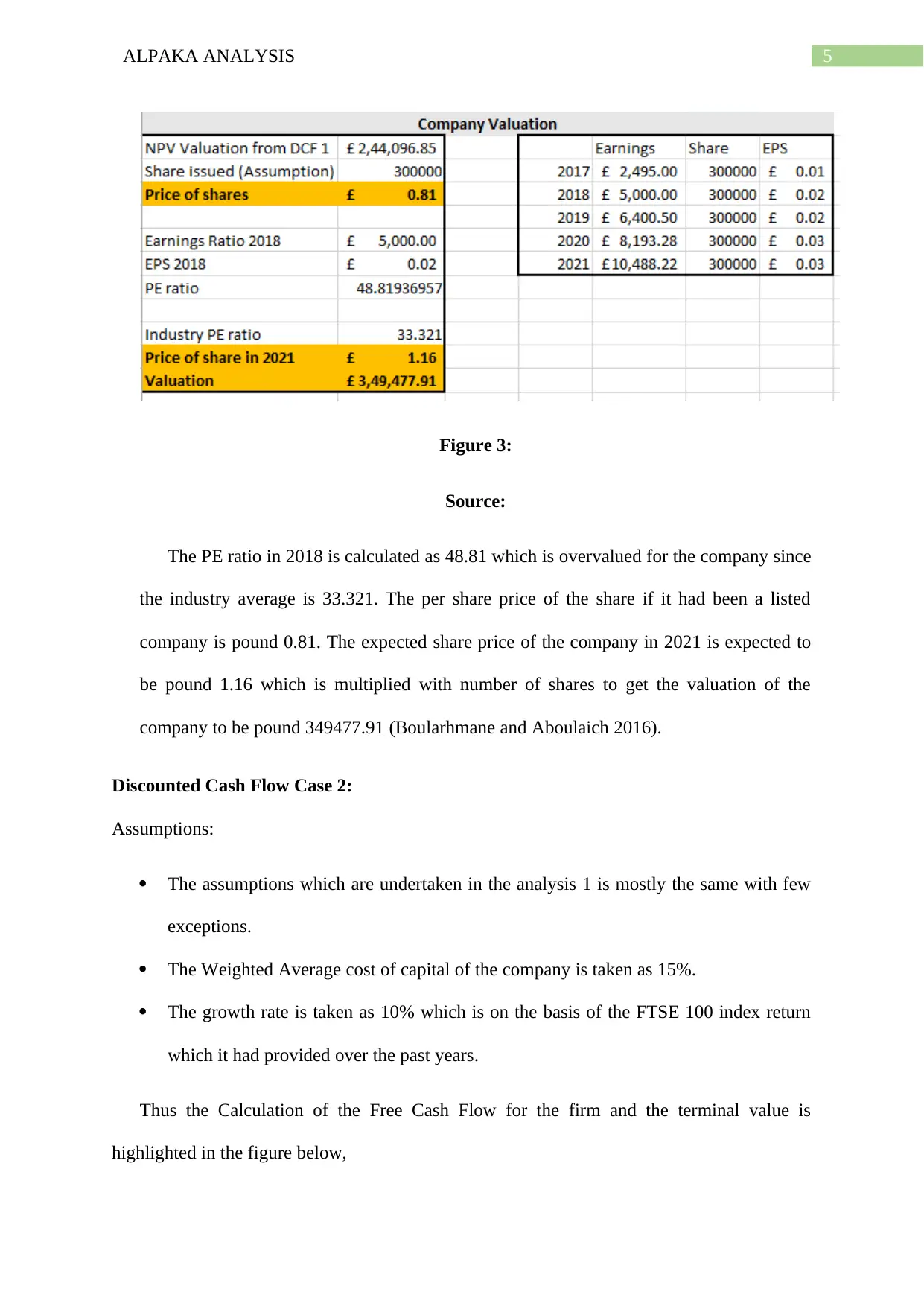

5ALPAKA ANALYSIS

Figure 3:

Source:

The PE ratio in 2018 is calculated as 48.81 which is overvalued for the company since

the industry average is 33.321. The per share price of the share if it had been a listed

company is pound 0.81. The expected share price of the company in 2021 is expected to

be pound 1.16 which is multiplied with number of shares to get the valuation of the

company to be pound 349477.91 (Boularhmane and Aboulaich 2016).

Discounted Cash Flow Case 2:

Assumptions:

The assumptions which are undertaken in the analysis 1 is mostly the same with few

exceptions.

The Weighted Average cost of capital of the company is taken as 15%.

The growth rate is taken as 10% which is on the basis of the FTSE 100 index return

which it had provided over the past years.

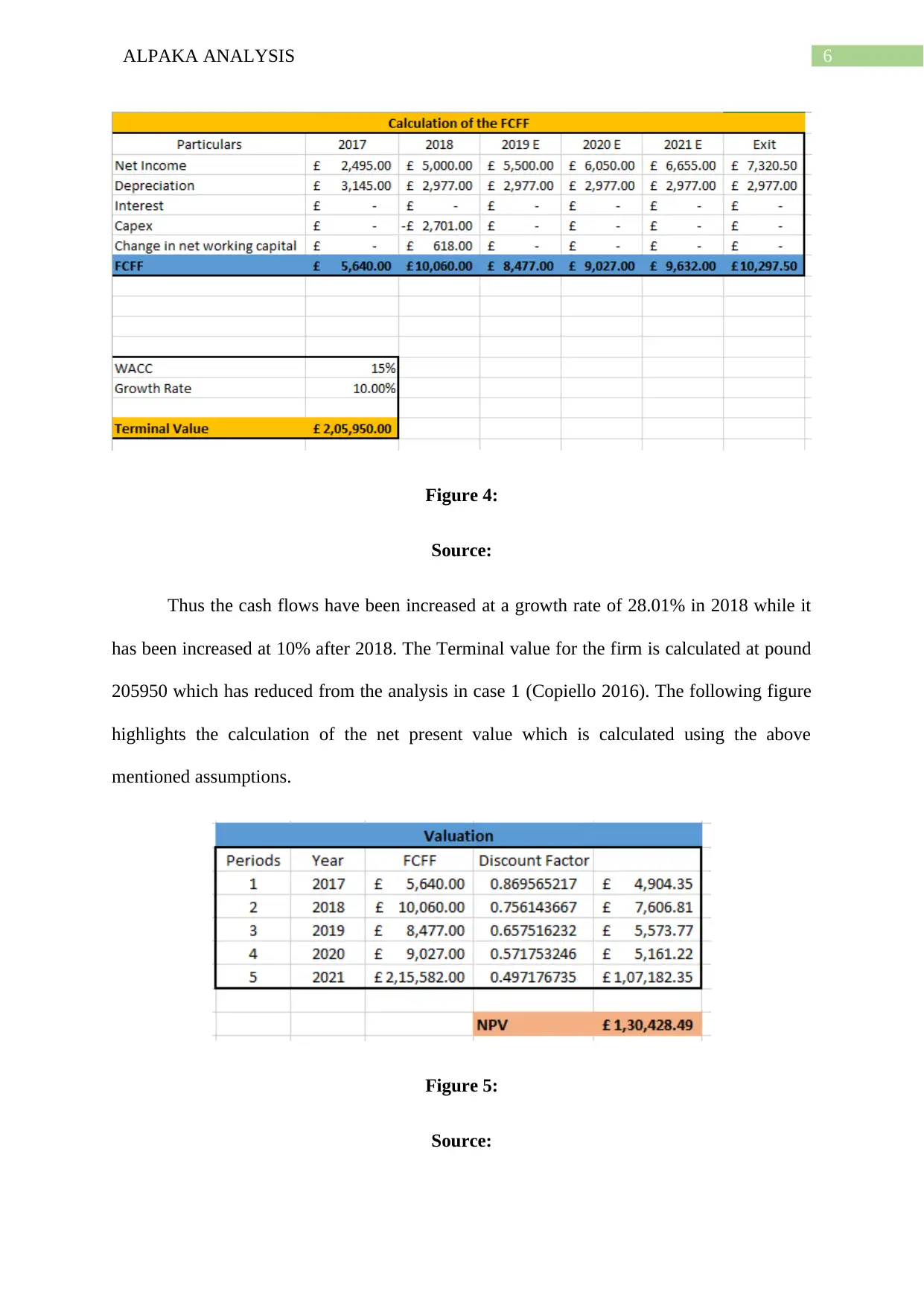

Thus the Calculation of the Free Cash Flow for the firm and the terminal value is

highlighted in the figure below,

Figure 3:

Source:

The PE ratio in 2018 is calculated as 48.81 which is overvalued for the company since

the industry average is 33.321. The per share price of the share if it had been a listed

company is pound 0.81. The expected share price of the company in 2021 is expected to

be pound 1.16 which is multiplied with number of shares to get the valuation of the

company to be pound 349477.91 (Boularhmane and Aboulaich 2016).

Discounted Cash Flow Case 2:

Assumptions:

The assumptions which are undertaken in the analysis 1 is mostly the same with few

exceptions.

The Weighted Average cost of capital of the company is taken as 15%.

The growth rate is taken as 10% which is on the basis of the FTSE 100 index return

which it had provided over the past years.

Thus the Calculation of the Free Cash Flow for the firm and the terminal value is

highlighted in the figure below,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ALPAKA ANALYSIS

Figure 4:

Source:

Thus the cash flows have been increased at a growth rate of 28.01% in 2018 while it

has been increased at 10% after 2018. The Terminal value for the firm is calculated at pound

205950 which has reduced from the analysis in case 1 (Copiello 2016). The following figure

highlights the calculation of the net present value which is calculated using the above

mentioned assumptions.

Figure 5:

Source:

Figure 4:

Source:

Thus the cash flows have been increased at a growth rate of 28.01% in 2018 while it

has been increased at 10% after 2018. The Terminal value for the firm is calculated at pound

205950 which has reduced from the analysis in case 1 (Copiello 2016). The following figure

highlights the calculation of the net present value which is calculated using the above

mentioned assumptions.

Figure 5:

Source:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ALPAKA ANALYSIS

The net present value calculated using the 15% discount rate provides the net present

value of pound 130428.49. Thus the valuation of the company has fallen by taking a lower

growth rate and lower weighted average cost of capital (Le 2017).

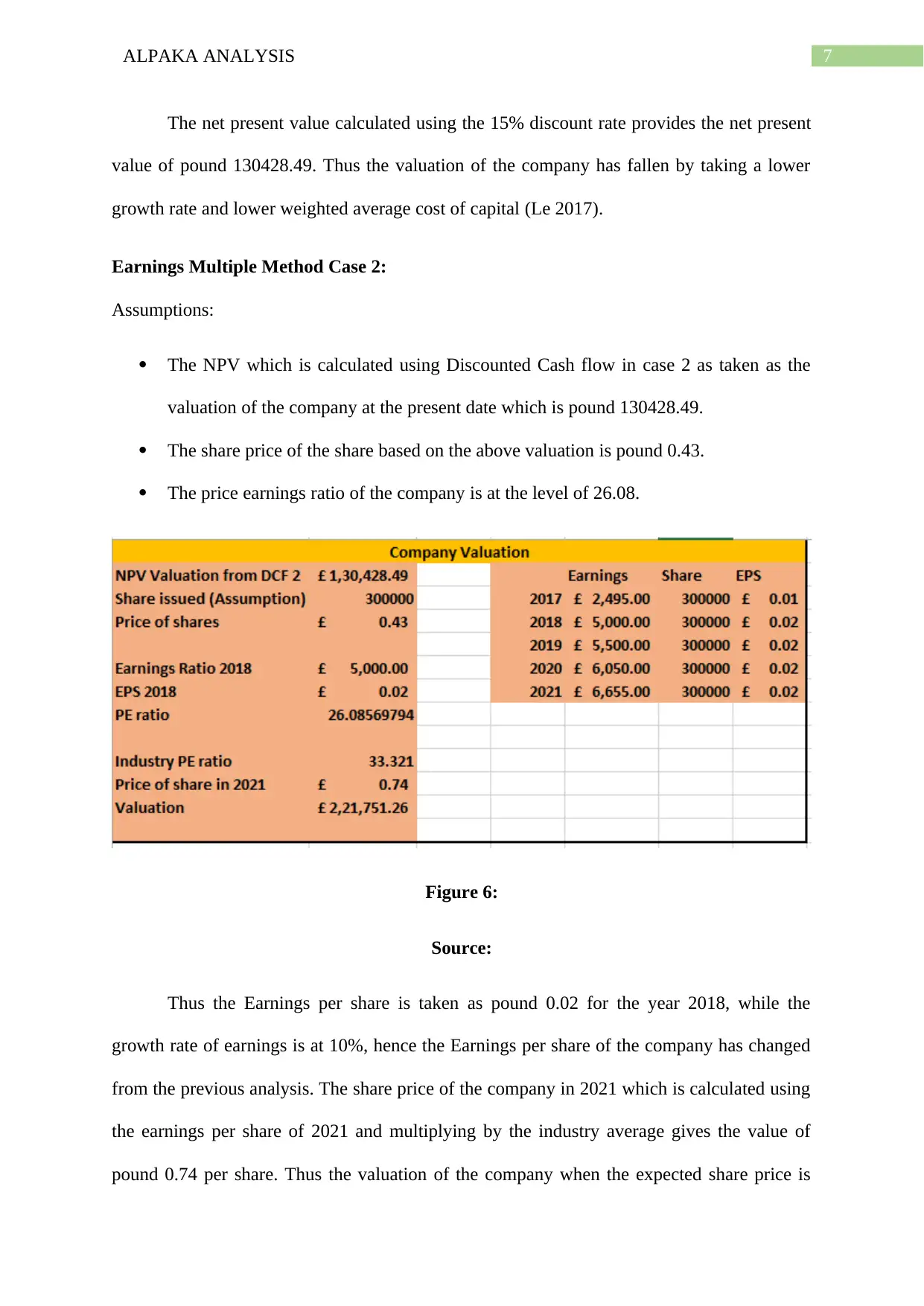

Earnings Multiple Method Case 2:

Assumptions:

The NPV which is calculated using Discounted Cash flow in case 2 as taken as the

valuation of the company at the present date which is pound 130428.49.

The share price of the share based on the above valuation is pound 0.43.

The price earnings ratio of the company is at the level of 26.08.

Figure 6:

Source:

Thus the Earnings per share is taken as pound 0.02 for the year 2018, while the

growth rate of earnings is at 10%, hence the Earnings per share of the company has changed

from the previous analysis. The share price of the company in 2021 which is calculated using

the earnings per share of 2021 and multiplying by the industry average gives the value of

pound 0.74 per share. Thus the valuation of the company when the expected share price is

The net present value calculated using the 15% discount rate provides the net present

value of pound 130428.49. Thus the valuation of the company has fallen by taking a lower

growth rate and lower weighted average cost of capital (Le 2017).

Earnings Multiple Method Case 2:

Assumptions:

The NPV which is calculated using Discounted Cash flow in case 2 as taken as the

valuation of the company at the present date which is pound 130428.49.

The share price of the share based on the above valuation is pound 0.43.

The price earnings ratio of the company is at the level of 26.08.

Figure 6:

Source:

Thus the Earnings per share is taken as pound 0.02 for the year 2018, while the

growth rate of earnings is at 10%, hence the Earnings per share of the company has changed

from the previous analysis. The share price of the company in 2021 which is calculated using

the earnings per share of 2021 and multiplying by the industry average gives the value of

pound 0.74 per share. Thus the valuation of the company when the expected share price is

8ALPAKA ANALYSIS

multiplied with the number of shares gives the value of pound 221751.26. At the current

price earnings ratio of 26.08 the company seems to be under-priced when compared with the

industry average (Shittu Ahmad and Ishak 2018).

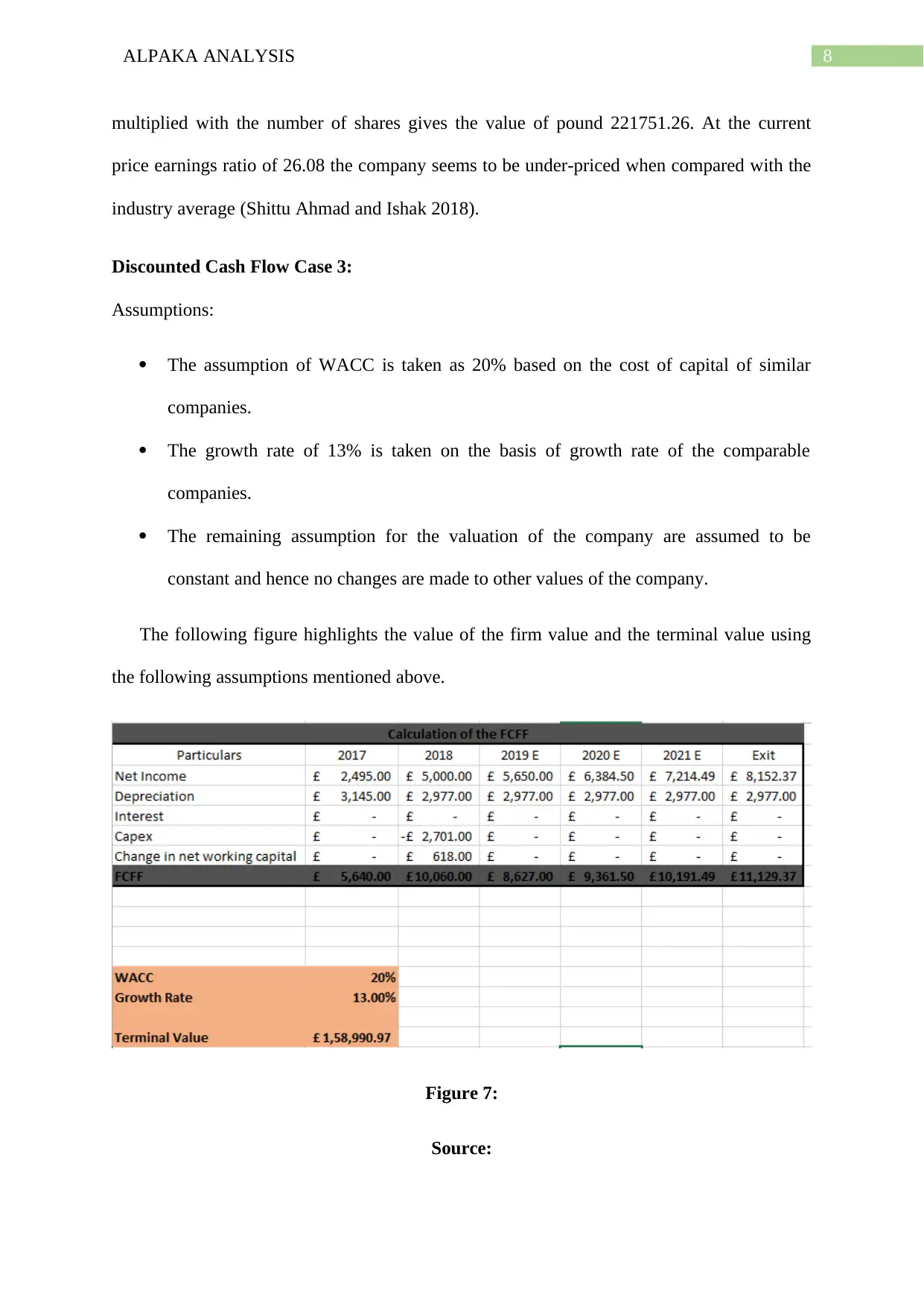

Discounted Cash Flow Case 3:

Assumptions:

The assumption of WACC is taken as 20% based on the cost of capital of similar

companies.

The growth rate of 13% is taken on the basis of growth rate of the comparable

companies.

The remaining assumption for the valuation of the company are assumed to be

constant and hence no changes are made to other values of the company.

The following figure highlights the value of the firm value and the terminal value using

the following assumptions mentioned above.

Figure 7:

Source:

multiplied with the number of shares gives the value of pound 221751.26. At the current

price earnings ratio of 26.08 the company seems to be under-priced when compared with the

industry average (Shittu Ahmad and Ishak 2018).

Discounted Cash Flow Case 3:

Assumptions:

The assumption of WACC is taken as 20% based on the cost of capital of similar

companies.

The growth rate of 13% is taken on the basis of growth rate of the comparable

companies.

The remaining assumption for the valuation of the company are assumed to be

constant and hence no changes are made to other values of the company.

The following figure highlights the value of the firm value and the terminal value using

the following assumptions mentioned above.

Figure 7:

Source:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ALPAKA ANALYSIS

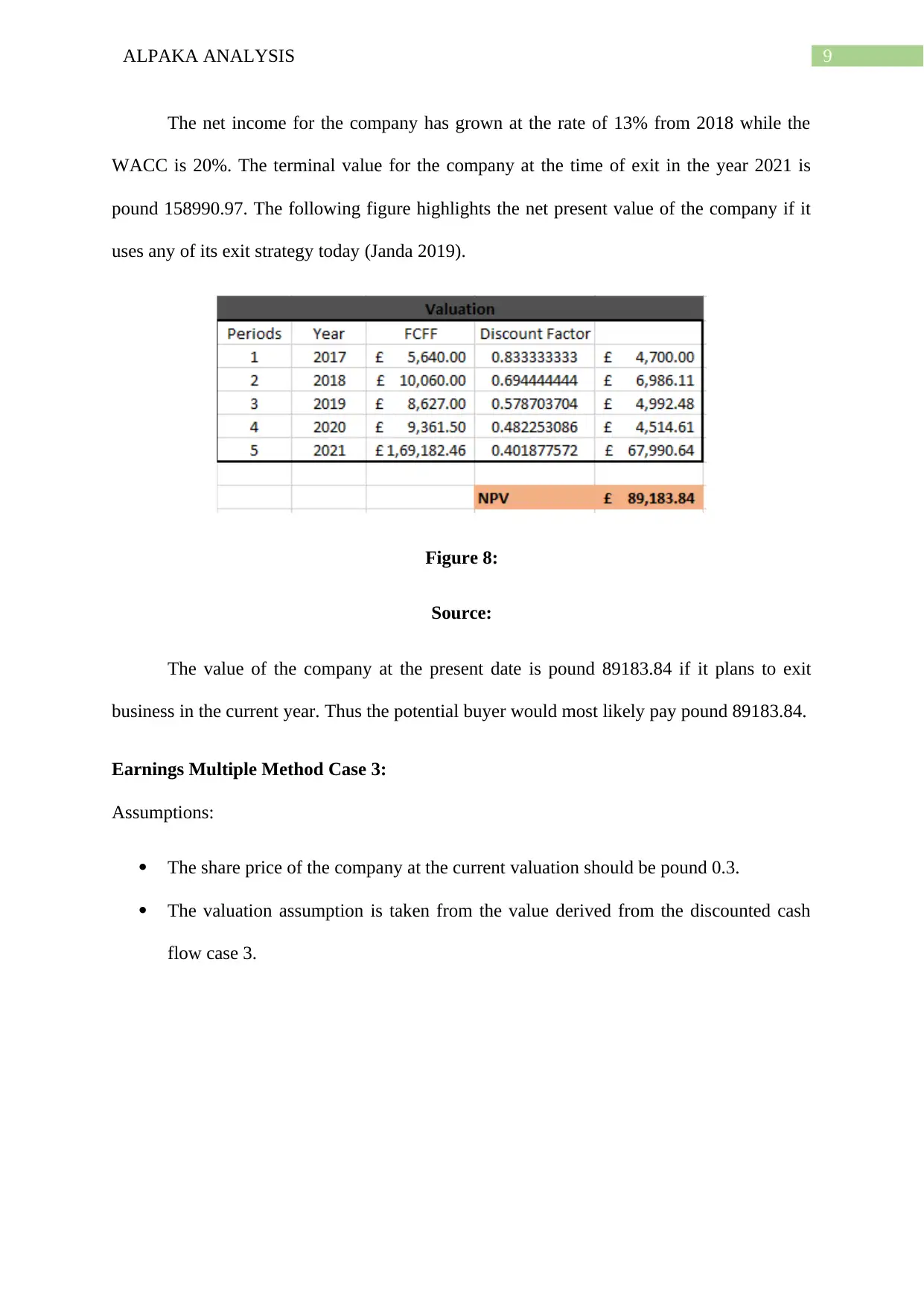

The net income for the company has grown at the rate of 13% from 2018 while the

WACC is 20%. The terminal value for the company at the time of exit in the year 2021 is

pound 158990.97. The following figure highlights the net present value of the company if it

uses any of its exit strategy today (Janda 2019).

Figure 8:

Source:

The value of the company at the present date is pound 89183.84 if it plans to exit

business in the current year. Thus the potential buyer would most likely pay pound 89183.84.

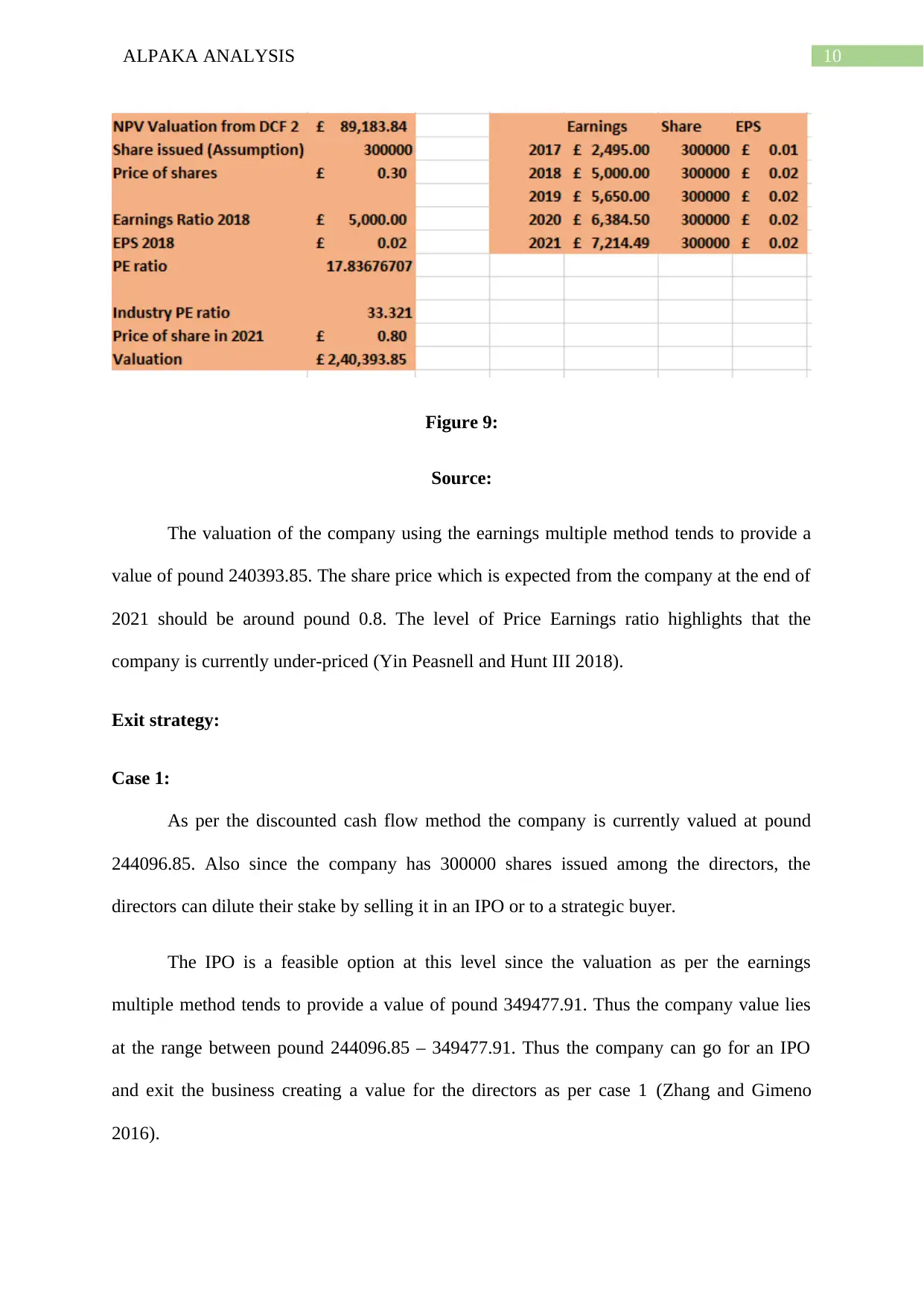

Earnings Multiple Method Case 3:

Assumptions:

The share price of the company at the current valuation should be pound 0.3.

The valuation assumption is taken from the value derived from the discounted cash

flow case 3.

The net income for the company has grown at the rate of 13% from 2018 while the

WACC is 20%. The terminal value for the company at the time of exit in the year 2021 is

pound 158990.97. The following figure highlights the net present value of the company if it

uses any of its exit strategy today (Janda 2019).

Figure 8:

Source:

The value of the company at the present date is pound 89183.84 if it plans to exit

business in the current year. Thus the potential buyer would most likely pay pound 89183.84.

Earnings Multiple Method Case 3:

Assumptions:

The share price of the company at the current valuation should be pound 0.3.

The valuation assumption is taken from the value derived from the discounted cash

flow case 3.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ALPAKA ANALYSIS

Figure 9:

Source:

The valuation of the company using the earnings multiple method tends to provide a

value of pound 240393.85. The share price which is expected from the company at the end of

2021 should be around pound 0.8. The level of Price Earnings ratio highlights that the

company is currently under-priced (Yin Peasnell and Hunt III 2018).

Exit strategy:

Case 1:

As per the discounted cash flow method the company is currently valued at pound

244096.85. Also since the company has 300000 shares issued among the directors, the

directors can dilute their stake by selling it in an IPO or to a strategic buyer.

The IPO is a feasible option at this level since the valuation as per the earnings

multiple method tends to provide a value of pound 349477.91. Thus the company value lies

at the range between pound 244096.85 – 349477.91. Thus the company can go for an IPO

and exit the business creating a value for the directors as per case 1 (Zhang and Gimeno

2016).

Figure 9:

Source:

The valuation of the company using the earnings multiple method tends to provide a

value of pound 240393.85. The share price which is expected from the company at the end of

2021 should be around pound 0.8. The level of Price Earnings ratio highlights that the

company is currently under-priced (Yin Peasnell and Hunt III 2018).

Exit strategy:

Case 1:

As per the discounted cash flow method the company is currently valued at pound

244096.85. Also since the company has 300000 shares issued among the directors, the

directors can dilute their stake by selling it in an IPO or to a strategic buyer.

The IPO is a feasible option at this level since the valuation as per the earnings

multiple method tends to provide a value of pound 349477.91. Thus the company value lies

at the range between pound 244096.85 – 349477.91. Thus the company can go for an IPO

and exit the business creating a value for the directors as per case 1 (Zhang and Gimeno

2016).

11ALPAKA ANALYSIS

Case 2:

As per Case 2 the valuation of the company lies between pound 130428.49 –

221751.26. Thus the company can consider the strategic buying option since the IPO at such

low valuation tend to be not feasible for the company. Also since the valuation is so low as

per the case 2, a strategic buyer will tend to pay a higher amount to the directors as it would

provide a benefit to the strategic buyer (Kunal Katti and Phani 2018).

The benefit which will be present with the strategic buyer who is in the same line of

business will get the necessary infrastructure which would be required to its business. Thus

this will provide additional support to the already existing infrastructure. Thus a strategic

buyer will tend to pay more to the directors. However, financial buyer can also be considered

but the extra money would not be available to the directors (Jiao Wang and Chen 2018).

Case 3:

As per case 3 the valuation of the company is present in a long range between pound

89183.84 to 240393.85. Thus the company can exit the business by IPO, Strategic sale or

liquidation of the assets. The liquidation of the company is being considered although the

value is positive because of the higher range, since this might lead to the generation of a

value which is greater than pound 89183.84 (Kim 2017).

The IPO is considered as the company has a very high valuation at pound 240393.85,

which is feasible for an IPO. However, further analysis needs to be considered for

undertaking the IPO strategy and the strategic sale of business as per this case (Aktas Andres

and Ozdakak 2018).

Caveats:

Management buyout as an option is not considered as it is assumed that the funding

in the start-up is undertaken by the management itself.

Case 2:

As per Case 2 the valuation of the company lies between pound 130428.49 –

221751.26. Thus the company can consider the strategic buying option since the IPO at such

low valuation tend to be not feasible for the company. Also since the valuation is so low as

per the case 2, a strategic buyer will tend to pay a higher amount to the directors as it would

provide a benefit to the strategic buyer (Kunal Katti and Phani 2018).

The benefit which will be present with the strategic buyer who is in the same line of

business will get the necessary infrastructure which would be required to its business. Thus

this will provide additional support to the already existing infrastructure. Thus a strategic

buyer will tend to pay more to the directors. However, financial buyer can also be considered

but the extra money would not be available to the directors (Jiao Wang and Chen 2018).

Case 3:

As per case 3 the valuation of the company is present in a long range between pound

89183.84 to 240393.85. Thus the company can exit the business by IPO, Strategic sale or

liquidation of the assets. The liquidation of the company is being considered although the

value is positive because of the higher range, since this might lead to the generation of a

value which is greater than pound 89183.84 (Kim 2017).

The IPO is considered as the company has a very high valuation at pound 240393.85,

which is feasible for an IPO. However, further analysis needs to be considered for

undertaking the IPO strategy and the strategic sale of business as per this case (Aktas Andres

and Ozdakak 2018).

Caveats:

Management buyout as an option is not considered as it is assumed that the funding

in the start-up is undertaken by the management itself.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.