Management Accounting Report: Alpha Ltd Case Study Analysis

VerifiedAdded on 2023/01/18

|20

|5224

|52

Report

AI Summary

This report delves into the realm of management accounting, exploring various systems, costing techniques, and planning tools within the context of Alpha Ltd, a medium-sized manufacturing company. The report begins by defining management accounting and its significance in decision-making, then proceeds to examine different types of management accounting systems such as job costing, price optimizing, cost accounting, and inventory management. It further outlines various management accounting reports, including performance reports, cost accounting reports, accounts receivable reports, and manufacturing and inventory reports, emphasizing their importance and applications. The report then proceeds to compute costs using absorption and marginal costing methods, providing detailed calculations and analyses. Finally, it discusses the advantages and disadvantages of different planning tools, their application in solving financial problems, and the role of management accounting systems in addressing financial challenges. The report concludes with a critical evaluation of the management accounting systems and reports, offering a comprehensive overview of the subject matter.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

SCENARIO 1 ..................................................................................................................................1

PART – I......................................................................................................................................1

Management Accounting different types of Management Accounting Systems.........................1

Different methods used for management accounting reporting...................................................3

Important of various MA system and its applications.................................................................4

Critically evaluation of MAS and reports integrated within organization...................................5

SCENARIO 2 ..................................................................................................................................5

TASK 2........................................................................................................................................5

Computation of cost with the help of absorption and marginal costing methods........................5

TASK 3..........................................................................................................................................12

Advantages and disadvantages of different types of planning tools..........................................12

Use of planning tools and their application...............................................................................13

Comparison of organization on the basis of Adoption of MAS................................................13

Role of MAS in responding to financial problems....................................................................15

Planning tools used in solving financial problems....................................................................15

CONCLUSION .............................................................................................................................15

REFERENCERS ...........................................................................................................................16

INTRODUCTION...........................................................................................................................1

SCENARIO 1 ..................................................................................................................................1

PART – I......................................................................................................................................1

Management Accounting different types of Management Accounting Systems.........................1

Different methods used for management accounting reporting...................................................3

Important of various MA system and its applications.................................................................4

Critically evaluation of MAS and reports integrated within organization...................................5

SCENARIO 2 ..................................................................................................................................5

TASK 2........................................................................................................................................5

Computation of cost with the help of absorption and marginal costing methods........................5

TASK 3..........................................................................................................................................12

Advantages and disadvantages of different types of planning tools..........................................12

Use of planning tools and their application...............................................................................13

Comparison of organization on the basis of Adoption of MAS................................................13

Role of MAS in responding to financial problems....................................................................15

Planning tools used in solving financial problems....................................................................15

CONCLUSION .............................................................................................................................15

REFERENCERS ...........................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In its basic form, accounting is a means of communicating to all stakeholders the

financial condition of a company or association. This is a way which help shareholders to

determine assets, liabilities and cash flow within company (Jansen, 2018). Management

accounting is defined as the process of grouping, posting, summarising, evaluating the crucial

accounting information into legal internal accounts to make effective decision. Accounts that are

prepared by the inner manager of company help them to make more authentic judgement in

respect to increase the entire profit making and market image. In the modern business time,

every company wants to have the better management system so that they can efficiently make

use of entire available resources and employees. In order to gain the in depth understanding of

MA Alpha Ltd have been selected that is a medium-sized manufacture company. The firm

produces different types of Pizza and was established in 2001.

in this respective report, several kind of MA system and their importance are shows,

number of useful MA report and their integration to company process are also discussed.

Furthermore, using different kind of costing technique's to prepare income statements and

evaluation of net profit, use of planning tool to strengthen budgetary process is defined in this

report. Various types of MA tool and methods plays a crucial role in company that is to detect

and resolve various financial problems are shown in this report.

SCENARIO 1

PART – I

Management Accounting different types of Management Accounting Systems

The concept of collecting, reporting, summarizing, and assessing the financial and non-

accounting information into authentic account which support manager to make valuable decision.

By qualified professionals is being used within businesses so that senior management can better

develop specific strategies for the smooth running of the company (Rickards and Ritsert, 2018).

Management accounting systems assist to analyze costs involved in various processes, determine

the paths in which prices are cut and the customer is provided with superior products, means of

measuring performance that enhances business productivity and therefore maximizes

profitability. There are number of useful system which can be applied by the Alpha Ltd in order

to make more better functional of different operations. These are discussed below:

1

In its basic form, accounting is a means of communicating to all stakeholders the

financial condition of a company or association. This is a way which help shareholders to

determine assets, liabilities and cash flow within company (Jansen, 2018). Management

accounting is defined as the process of grouping, posting, summarising, evaluating the crucial

accounting information into legal internal accounts to make effective decision. Accounts that are

prepared by the inner manager of company help them to make more authentic judgement in

respect to increase the entire profit making and market image. In the modern business time,

every company wants to have the better management system so that they can efficiently make

use of entire available resources and employees. In order to gain the in depth understanding of

MA Alpha Ltd have been selected that is a medium-sized manufacture company. The firm

produces different types of Pizza and was established in 2001.

in this respective report, several kind of MA system and their importance are shows,

number of useful MA report and their integration to company process are also discussed.

Furthermore, using different kind of costing technique's to prepare income statements and

evaluation of net profit, use of planning tool to strengthen budgetary process is defined in this

report. Various types of MA tool and methods plays a crucial role in company that is to detect

and resolve various financial problems are shown in this report.

SCENARIO 1

PART – I

Management Accounting different types of Management Accounting Systems

The concept of collecting, reporting, summarizing, and assessing the financial and non-

accounting information into authentic account which support manager to make valuable decision.

By qualified professionals is being used within businesses so that senior management can better

develop specific strategies for the smooth running of the company (Rickards and Ritsert, 2018).

Management accounting systems assist to analyze costs involved in various processes, determine

the paths in which prices are cut and the customer is provided with superior products, means of

measuring performance that enhances business productivity and therefore maximizes

profitability. There are number of useful system which can be applied by the Alpha Ltd in order

to make more better functional of different operations. These are discussed below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

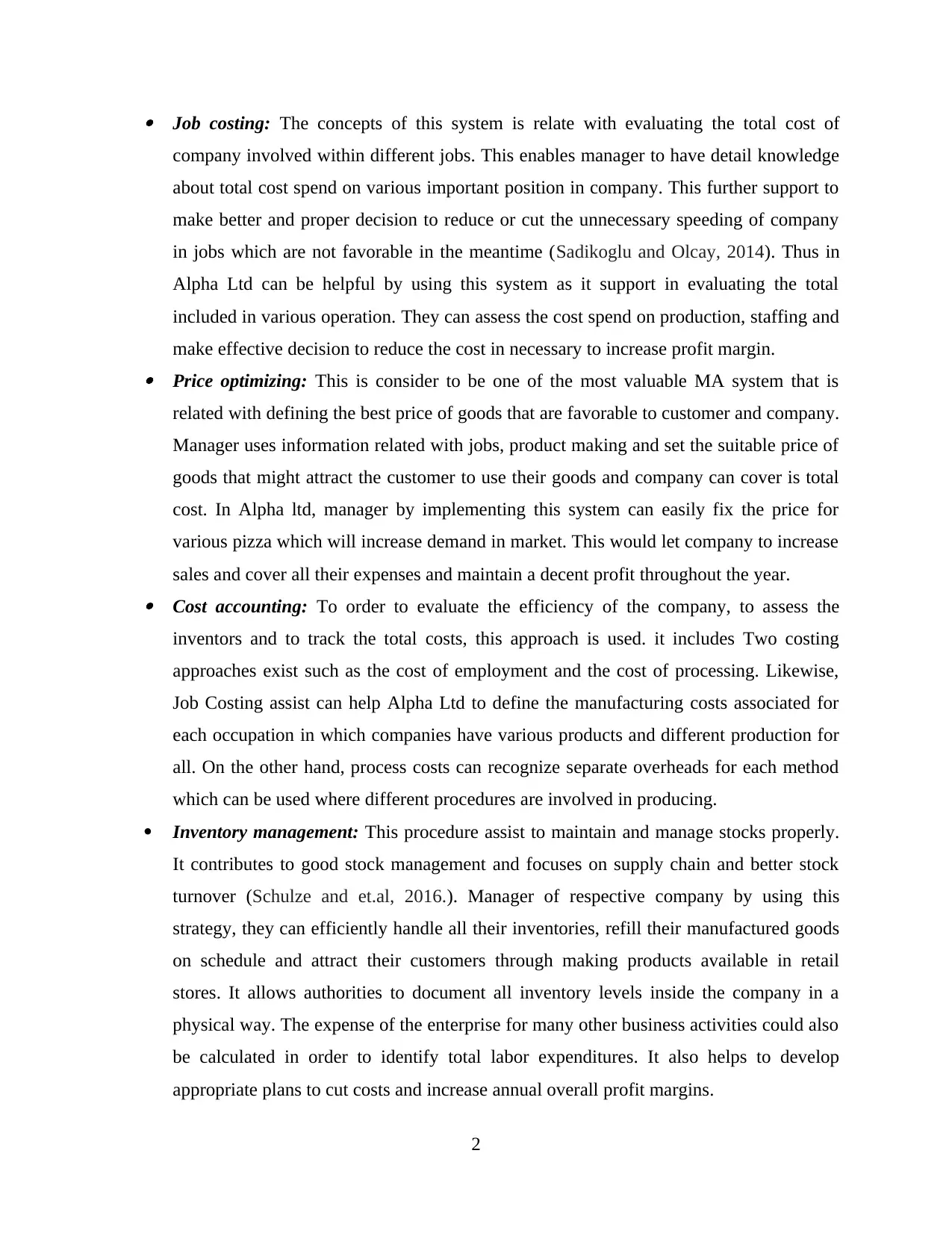

Job costing: The concepts of this system is relate with evaluating the total cost of

company involved within different jobs. This enables manager to have detail knowledge

about total cost spend on various important position in company. This further support to

make better and proper decision to reduce or cut the unnecessary speeding of company

in jobs which are not favorable in the meantime (Sadikoglu and Olcay, 2014). Thus in

Alpha Ltd can be helpful by using this system as it support in evaluating the total

included in various operation. They can assess the cost spend on production, staffing and

make effective decision to reduce the cost in necessary to increase profit margin. Price optimizing: This is consider to be one of the most valuable MA system that is

related with defining the best price of goods that are favorable to customer and company.

Manager uses information related with jobs, product making and set the suitable price of

goods that might attract the customer to use their goods and company can cover is total

cost. In Alpha ltd, manager by implementing this system can easily fix the price for

various pizza which will increase demand in market. This would let company to increase

sales and cover all their expenses and maintain a decent profit throughout the year. Cost accounting: To order to evaluate the efficiency of the company, to assess the

inventors and to track the total costs, this approach is used. it includes Two costing

approaches exist such as the cost of employment and the cost of processing. Likewise,

Job Costing assist can help Alpha Ltd to define the manufacturing costs associated for

each occupation in which companies have various products and different production for

all. On the other hand, process costs can recognize separate overheads for each method

which can be used where different procedures are involved in producing.

Inventory management: This procedure assist to maintain and manage stocks properly.

It contributes to good stock management and focuses on supply chain and better stock

turnover (Schulze and et.al, 2016.). Manager of respective company by using this

strategy, they can efficiently handle all their inventories, refill their manufactured goods

on schedule and attract their customers through making products available in retail

stores. It allows authorities to document all inventory levels inside the company in a

physical way. The expense of the enterprise for many other business activities could also

be calculated in order to identify total labor expenditures. It also helps to develop

appropriate plans to cut costs and increase annual overall profit margins.

2

company involved within different jobs. This enables manager to have detail knowledge

about total cost spend on various important position in company. This further support to

make better and proper decision to reduce or cut the unnecessary speeding of company

in jobs which are not favorable in the meantime (Sadikoglu and Olcay, 2014). Thus in

Alpha Ltd can be helpful by using this system as it support in evaluating the total

included in various operation. They can assess the cost spend on production, staffing and

make effective decision to reduce the cost in necessary to increase profit margin. Price optimizing: This is consider to be one of the most valuable MA system that is

related with defining the best price of goods that are favorable to customer and company.

Manager uses information related with jobs, product making and set the suitable price of

goods that might attract the customer to use their goods and company can cover is total

cost. In Alpha ltd, manager by implementing this system can easily fix the price for

various pizza which will increase demand in market. This would let company to increase

sales and cover all their expenses and maintain a decent profit throughout the year. Cost accounting: To order to evaluate the efficiency of the company, to assess the

inventors and to track the total costs, this approach is used. it includes Two costing

approaches exist such as the cost of employment and the cost of processing. Likewise,

Job Costing assist can help Alpha Ltd to define the manufacturing costs associated for

each occupation in which companies have various products and different production for

all. On the other hand, process costs can recognize separate overheads for each method

which can be used where different procedures are involved in producing.

Inventory management: This procedure assist to maintain and manage stocks properly.

It contributes to good stock management and focuses on supply chain and better stock

turnover (Schulze and et.al, 2016.). Manager of respective company by using this

strategy, they can efficiently handle all their inventories, refill their manufactured goods

on schedule and attract their customers through making products available in retail

stores. It allows authorities to document all inventory levels inside the company in a

physical way. The expense of the enterprise for many other business activities could also

be calculated in order to identify total labor expenditures. It also helps to develop

appropriate plans to cut costs and increase annual overall profit margins.

2

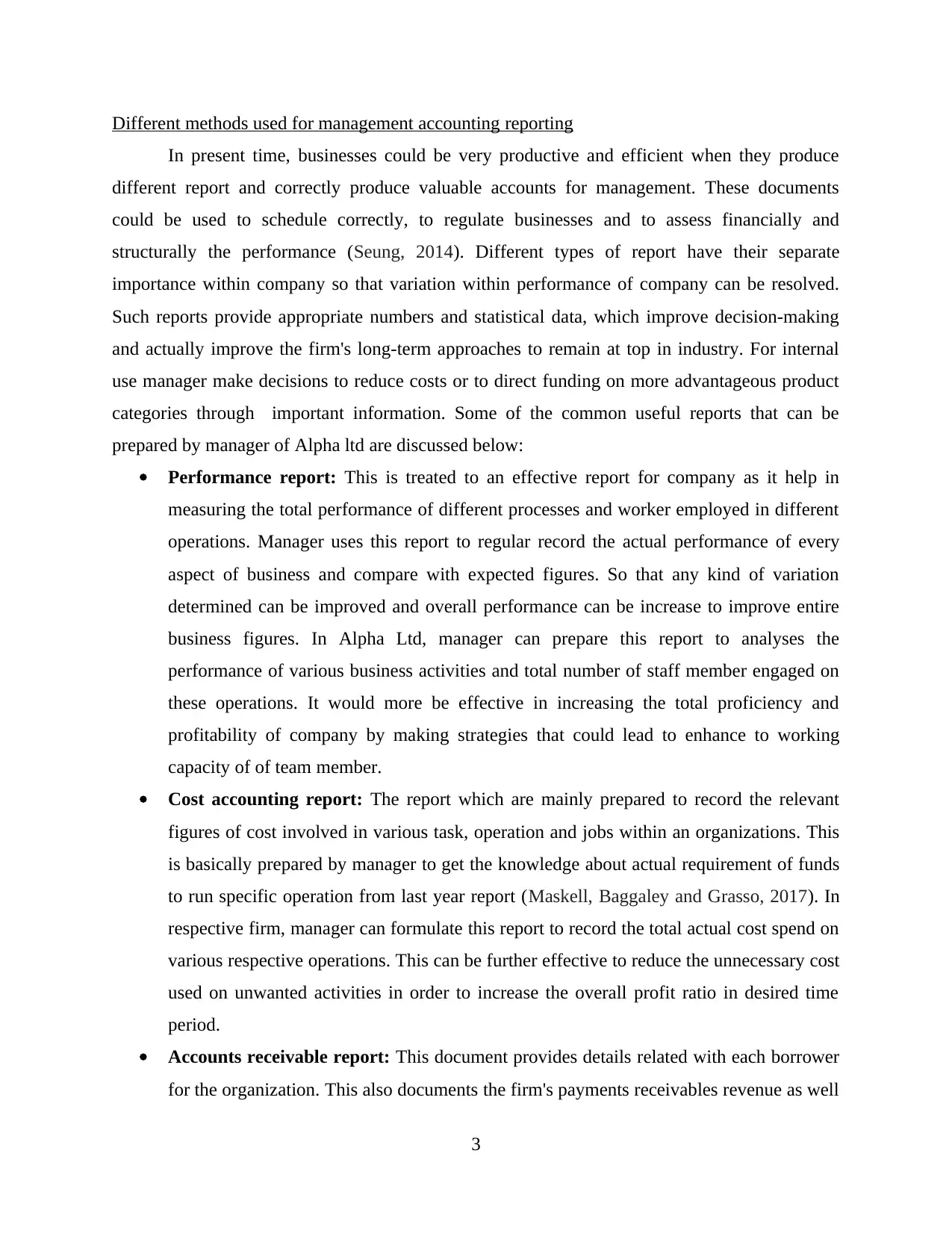

Different methods used for management accounting reporting

In present time, businesses could be very productive and efficient when they produce

different report and correctly produce valuable accounts for management. These documents

could be used to schedule correctly, to regulate businesses and to assess financially and

structurally the performance (Seung, 2014). Different types of report have their separate

importance within company so that variation within performance of company can be resolved.

Such reports provide appropriate numbers and statistical data, which improve decision-making

and actually improve the firm's long-term approaches to remain at top in industry. For internal

use manager make decisions to reduce costs or to direct funding on more advantageous product

categories through important information. Some of the common useful reports that can be

prepared by manager of Alpha ltd are discussed below:

Performance report: This is treated to an effective report for company as it help in

measuring the total performance of different processes and worker employed in different

operations. Manager uses this report to regular record the actual performance of every

aspect of business and compare with expected figures. So that any kind of variation

determined can be improved and overall performance can be increase to improve entire

business figures. In Alpha Ltd, manager can prepare this report to analyses the

performance of various business activities and total number of staff member engaged on

these operations. It would more be effective in increasing the total proficiency and

profitability of company by making strategies that could lead to enhance to working

capacity of of team member.

Cost accounting report: The report which are mainly prepared to record the relevant

figures of cost involved in various task, operation and jobs within an organizations. This

is basically prepared by manager to get the knowledge about actual requirement of funds

to run specific operation from last year report (Maskell, Baggaley and Grasso, 2017). In

respective firm, manager can formulate this report to record the total actual cost spend on

various respective operations. This can be further effective to reduce the unnecessary cost

used on unwanted activities in order to increase the overall profit ratio in desired time

period.

Accounts receivable report: This document provides details related with each borrower

for the organization. This also documents the firm's payments receivables revenue as well

3

In present time, businesses could be very productive and efficient when they produce

different report and correctly produce valuable accounts for management. These documents

could be used to schedule correctly, to regulate businesses and to assess financially and

structurally the performance (Seung, 2014). Different types of report have their separate

importance within company so that variation within performance of company can be resolved.

Such reports provide appropriate numbers and statistical data, which improve decision-making

and actually improve the firm's long-term approaches to remain at top in industry. For internal

use manager make decisions to reduce costs or to direct funding on more advantageous product

categories through important information. Some of the common useful reports that can be

prepared by manager of Alpha ltd are discussed below:

Performance report: This is treated to an effective report for company as it help in

measuring the total performance of different processes and worker employed in different

operations. Manager uses this report to regular record the actual performance of every

aspect of business and compare with expected figures. So that any kind of variation

determined can be improved and overall performance can be increase to improve entire

business figures. In Alpha Ltd, manager can prepare this report to analyses the

performance of various business activities and total number of staff member engaged on

these operations. It would more be effective in increasing the total proficiency and

profitability of company by making strategies that could lead to enhance to working

capacity of of team member.

Cost accounting report: The report which are mainly prepared to record the relevant

figures of cost involved in various task, operation and jobs within an organizations. This

is basically prepared by manager to get the knowledge about actual requirement of funds

to run specific operation from last year report (Maskell, Baggaley and Grasso, 2017). In

respective firm, manager can formulate this report to record the total actual cost spend on

various respective operations. This can be further effective to reduce the unnecessary cost

used on unwanted activities in order to increase the overall profit ratio in desired time

period.

Accounts receivable report: This document provides details related with each borrower

for the organization. This also documents the firm's payments receivables revenue as well

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as the length of time they took to pay back the outstanding amount to company. In this

respect, the firm is also aware that the collection policy has to be tightened and is

beneficial to track the debtors who are doubtful those can demand to extend transaction

dates.

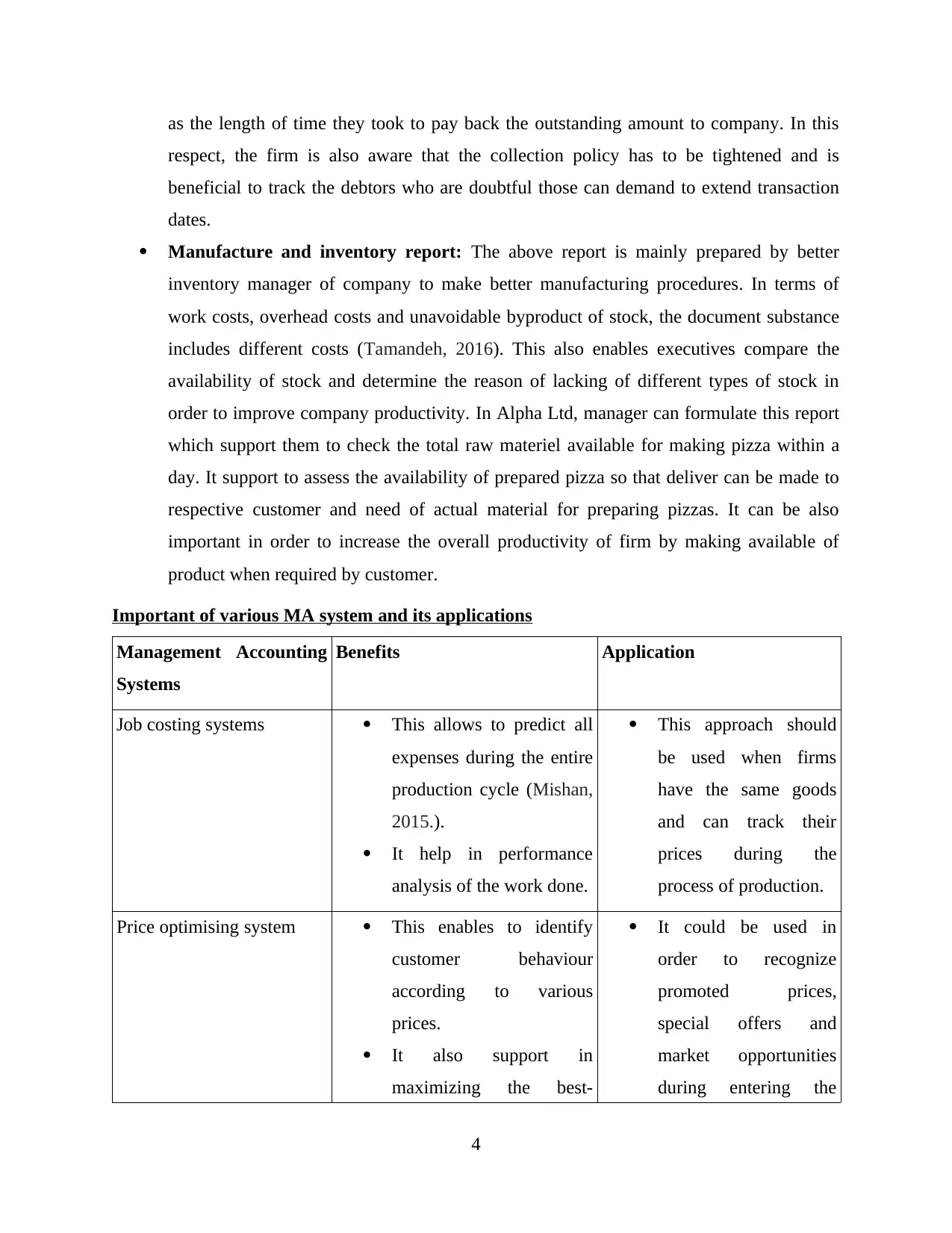

Manufacture and inventory report: The above report is mainly prepared by better

inventory manager of company to make better manufacturing procedures. In terms of

work costs, overhead costs and unavoidable byproduct of stock, the document substance

includes different costs (Tamandeh, 2016). This also enables executives compare the

availability of stock and determine the reason of lacking of different types of stock in

order to improve company productivity. In Alpha Ltd, manager can formulate this report

which support them to check the total raw materiel available for making pizza within a

day. It support to assess the availability of prepared pizza so that deliver can be made to

respective customer and need of actual material for preparing pizzas. It can be also

important in order to increase the overall productivity of firm by making available of

product when required by customer.

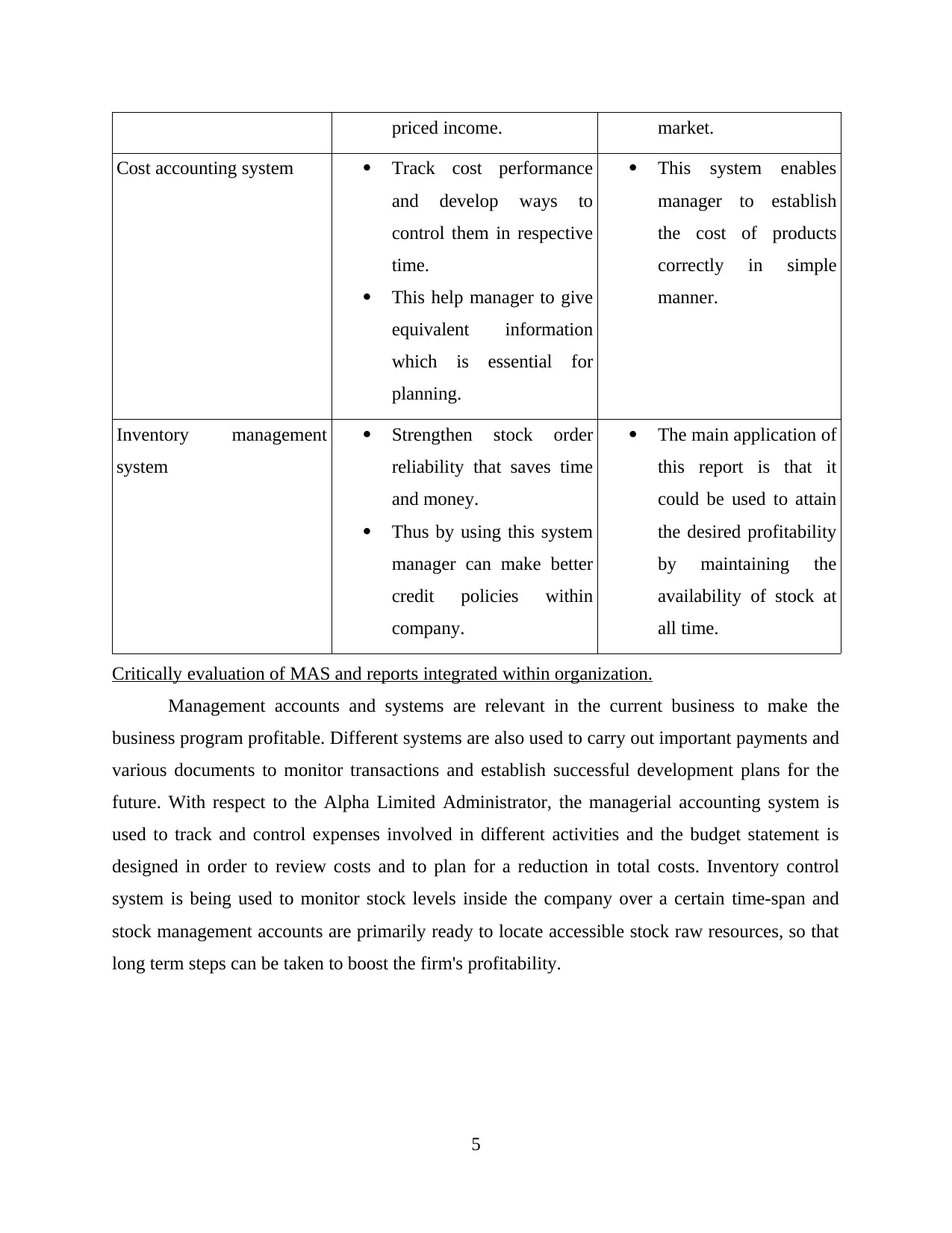

Important of various MA system and its applications

Management Accounting

Systems

Benefits Application

Job costing systems This allows to predict all

expenses during the entire

production cycle (Mishan,

2015.).

It help in performance

analysis of the work done.

This approach should

be used when firms

have the same goods

and can track their

prices during the

process of production.

Price optimising system This enables to identify

customer behaviour

according to various

prices.

It also support in

maximizing the best-

It could be used in

order to recognize

promoted prices,

special offers and

market opportunities

during entering the

4

respect, the firm is also aware that the collection policy has to be tightened and is

beneficial to track the debtors who are doubtful those can demand to extend transaction

dates.

Manufacture and inventory report: The above report is mainly prepared by better

inventory manager of company to make better manufacturing procedures. In terms of

work costs, overhead costs and unavoidable byproduct of stock, the document substance

includes different costs (Tamandeh, 2016). This also enables executives compare the

availability of stock and determine the reason of lacking of different types of stock in

order to improve company productivity. In Alpha Ltd, manager can formulate this report

which support them to check the total raw materiel available for making pizza within a

day. It support to assess the availability of prepared pizza so that deliver can be made to

respective customer and need of actual material for preparing pizzas. It can be also

important in order to increase the overall productivity of firm by making available of

product when required by customer.

Important of various MA system and its applications

Management Accounting

Systems

Benefits Application

Job costing systems This allows to predict all

expenses during the entire

production cycle (Mishan,

2015.).

It help in performance

analysis of the work done.

This approach should

be used when firms

have the same goods

and can track their

prices during the

process of production.

Price optimising system This enables to identify

customer behaviour

according to various

prices.

It also support in

maximizing the best-

It could be used in

order to recognize

promoted prices,

special offers and

market opportunities

during entering the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

priced income. market.

Cost accounting system Track cost performance

and develop ways to

control them in respective

time.

This help manager to give

equivalent information

which is essential for

planning.

This system enables

manager to establish

the cost of products

correctly in simple

manner.

Inventory management

system

Strengthen stock order

reliability that saves time

and money.

Thus by using this system

manager can make better

credit policies within

company.

The main application of

this report is that it

could be used to attain

the desired profitability

by maintaining the

availability of stock at

all time.

Critically evaluation of MAS and reports integrated within organization.

Management accounts and systems are relevant in the current business to make the

business program profitable. Different systems are also used to carry out important payments and

various documents to monitor transactions and establish successful development plans for the

future. With respect to the Alpha Limited Administrator, the managerial accounting system is

used to track and control expenses involved in different activities and the budget statement is

designed in order to review costs and to plan for a reduction in total costs. Inventory control

system is being used to monitor stock levels inside the company over a certain time-span and

stock management accounts are primarily ready to locate accessible stock raw resources, so that

long term steps can be taken to boost the firm's profitability.

5

Cost accounting system Track cost performance

and develop ways to

control them in respective

time.

This help manager to give

equivalent information

which is essential for

planning.

This system enables

manager to establish

the cost of products

correctly in simple

manner.

Inventory management

system

Strengthen stock order

reliability that saves time

and money.

Thus by using this system

manager can make better

credit policies within

company.

The main application of

this report is that it

could be used to attain

the desired profitability

by maintaining the

availability of stock at

all time.

Critically evaluation of MAS and reports integrated within organization.

Management accounts and systems are relevant in the current business to make the

business program profitable. Different systems are also used to carry out important payments and

various documents to monitor transactions and establish successful development plans for the

future. With respect to the Alpha Limited Administrator, the managerial accounting system is

used to track and control expenses involved in different activities and the budget statement is

designed in order to review costs and to plan for a reduction in total costs. Inventory control

system is being used to monitor stock levels inside the company over a certain time-span and

stock management accounts are primarily ready to locate accessible stock raw resources, so that

long term steps can be taken to boost the firm's profitability.

5

SCENARIO 2

TASK 2

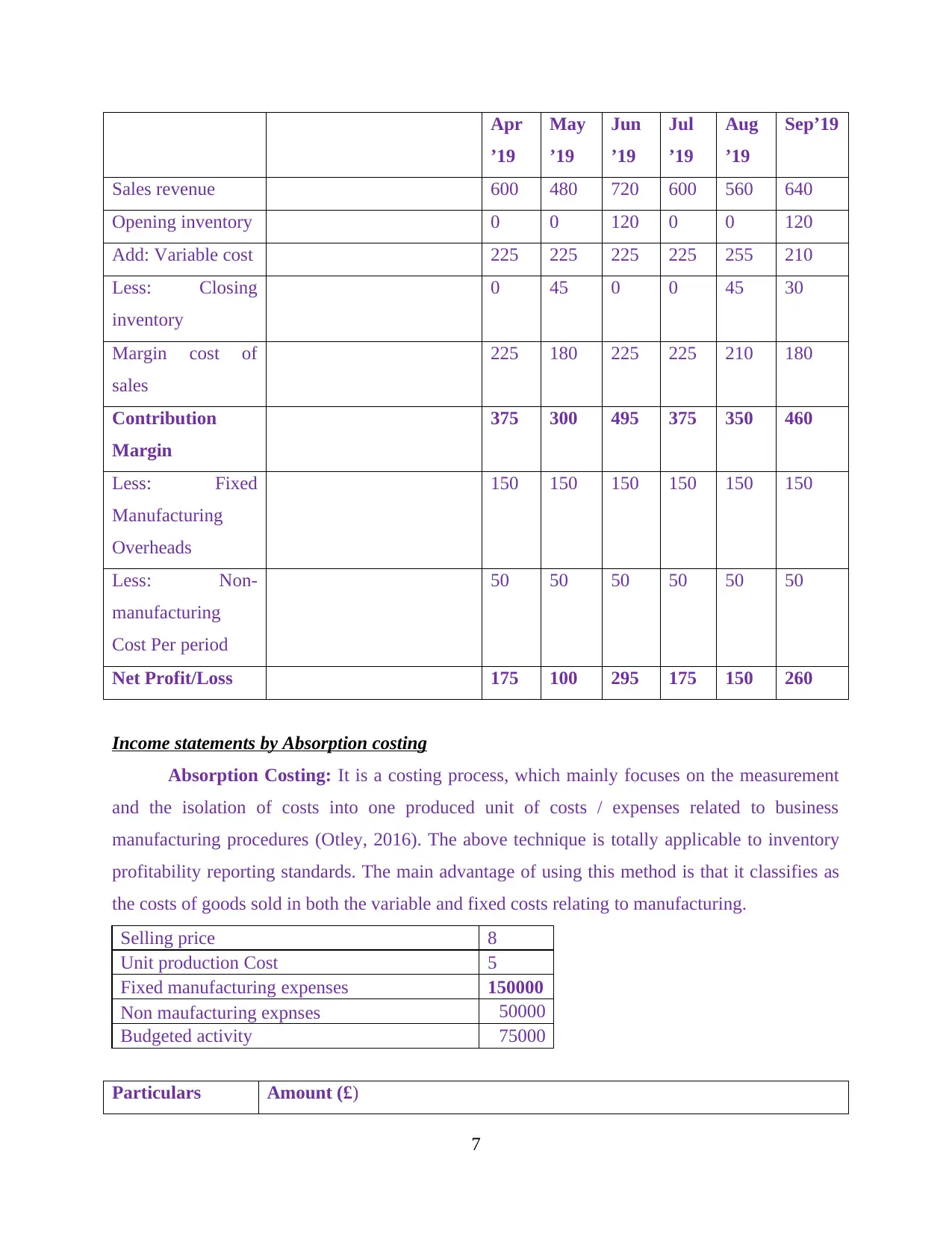

Computation of cost with the help of absorption and marginal costing methods.

Cost is something that is use by companies on different operation and activities in order

to reach the desired results and favorable outcome (Mohamed, Kerosi, and Tirimba, 2016).

These are the expense made to produce something useful for company that will generate future

profit in particular time period. Some of the common methods used calculate cost and determine

profit margin is discussed underneath:

Marginal Costing: The concept of costing techniques is related with evaluate the cost

related with every additional unit of manufacture good. It is a basic technique where the total

cost are categorised into variable and fixed cost for the product and treated separately while

preparing income statements.

Selling price 8

Unit Variable Cost 3

Fixed manufacturing expenses 150000

Non maufacturing expnses 50000

Budgeted activity 75000

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening

inventory

0 0 15 0 0 15

Closing

inventory

0 15 0 0 15 10

Profit and loss

account:

Particulars Amount (£)

6

TASK 2

Computation of cost with the help of absorption and marginal costing methods.

Cost is something that is use by companies on different operation and activities in order

to reach the desired results and favorable outcome (Mohamed, Kerosi, and Tirimba, 2016).

These are the expense made to produce something useful for company that will generate future

profit in particular time period. Some of the common methods used calculate cost and determine

profit margin is discussed underneath:

Marginal Costing: The concept of costing techniques is related with evaluate the cost

related with every additional unit of manufacture good. It is a basic technique where the total

cost are categorised into variable and fixed cost for the product and treated separately while

preparing income statements.

Selling price 8

Unit Variable Cost 3

Fixed manufacturing expenses 150000

Non maufacturing expnses 50000

Budgeted activity 75000

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening

inventory

0 0 15 0 0 15

Closing

inventory

0 15 0 0 15 10

Profit and loss

account:

Particulars Amount (£)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Apr

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales revenue 600 480 720 600 560 640

Opening inventory 0 0 120 0 0 120

Add: Variable cost 225 225 225 225 255 210

Less: Closing

inventory

0 45 0 0 45 30

Margin cost of

sales

225 180 225 225 210 180

Contribution

Margin

375 300 495 375 350 460

Less: Fixed

Manufacturing

Overheads

150 150 150 150 150 150

Less: Non-

manufacturing

Cost Per period

50 50 50 50 50 50

Net Profit/Loss 175 100 295 175 150 260

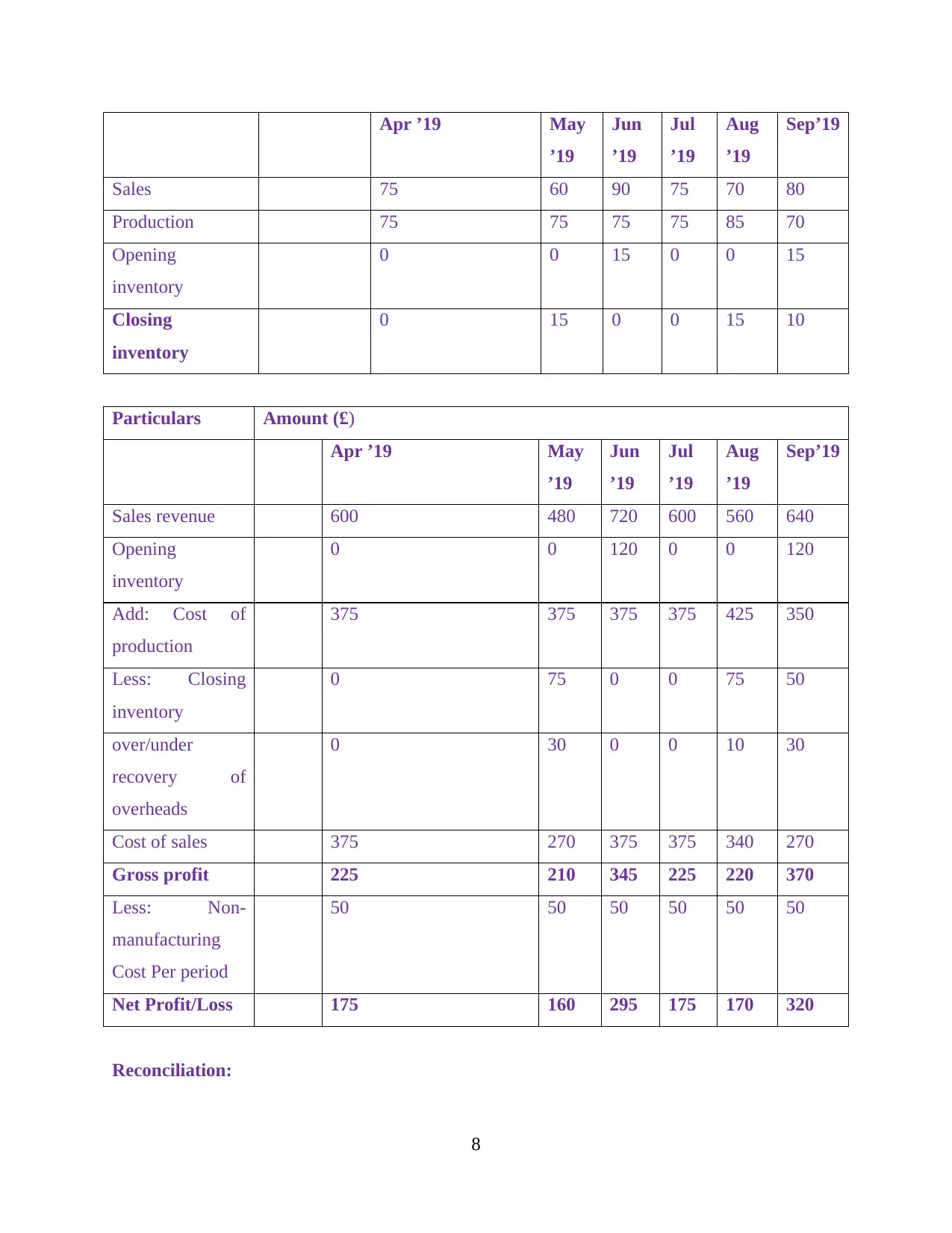

Income statements by Absorption costing

Absorption Costing: It is a costing process, which mainly focuses on the measurement

and the isolation of costs into one produced unit of costs / expenses related to business

manufacturing procedures (Otley, 2016). The above technique is totally applicable to inventory

profitability reporting standards. The main advantage of using this method is that it classifies as

the costs of goods sold in both the variable and fixed costs relating to manufacturing.

Selling price 8

Unit production Cost 5

Fixed manufacturing expenses 150000

Non maufacturing expnses 50000

Budgeted activity 75000

Particulars Amount (£)

7

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales revenue 600 480 720 600 560 640

Opening inventory 0 0 120 0 0 120

Add: Variable cost 225 225 225 225 255 210

Less: Closing

inventory

0 45 0 0 45 30

Margin cost of

sales

225 180 225 225 210 180

Contribution

Margin

375 300 495 375 350 460

Less: Fixed

Manufacturing

Overheads

150 150 150 150 150 150

Less: Non-

manufacturing

Cost Per period

50 50 50 50 50 50

Net Profit/Loss 175 100 295 175 150 260

Income statements by Absorption costing

Absorption Costing: It is a costing process, which mainly focuses on the measurement

and the isolation of costs into one produced unit of costs / expenses related to business

manufacturing procedures (Otley, 2016). The above technique is totally applicable to inventory

profitability reporting standards. The main advantage of using this method is that it classifies as

the costs of goods sold in both the variable and fixed costs relating to manufacturing.

Selling price 8

Unit production Cost 5

Fixed manufacturing expenses 150000

Non maufacturing expnses 50000

Budgeted activity 75000

Particulars Amount (£)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Apr ’19 May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening

inventory

0 0 15 0 0 15

Closing

inventory

0 15 0 0 15 10

Particulars Amount (£)

Apr ’19 May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales revenue 600 480 720 600 560 640

Opening

inventory

0 0 120 0 0 120

Add: Cost of

production

375 375 375 375 425 350

Less: Closing

inventory

0 75 0 0 75 50

over/under

recovery of

overheads

0 30 0 0 10 30

Cost of sales 375 270 375 375 340 270

Gross profit 225 210 345 225 220 370

Less: Non-

manufacturing

Cost Per period

50 50 50 50 50 50

Net Profit/Loss 175 160 295 175 170 320

Reconciliation:

8

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening

inventory

0 0 15 0 0 15

Closing

inventory

0 15 0 0 15 10

Particulars Amount (£)

Apr ’19 May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales revenue 600 480 720 600 560 640

Opening

inventory

0 0 120 0 0 120

Add: Cost of

production

375 375 375 375 425 350

Less: Closing

inventory

0 75 0 0 75 50

over/under

recovery of

overheads

0 30 0 0 10 30

Cost of sales 375 270 375 375 340 270

Gross profit 225 210 345 225 220 370

Less: Non-

manufacturing

Cost Per period

50 50 50 50 50 50

Net Profit/Loss 175 160 295 175 170 320

Reconciliation:

8

Particulars

Apr ’19 May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening

inventory

0 0 15 0 0 15

Closing

inventory

0 15 0 0 15 10

Apr

’19

May

’19

Jun

’19

Jul ’19 Aug

’19

Sep’19

Net profits under

absorption costing

175 130 295 175 160 290

ADD: Fixed overheads in

opening

0 30 0 0 10 30

175 100 295 175 150 260

From the above calculation it has been determined that the net profit from marginal

costing method for the different month is lower than the absorption costing techniques. The main

reason for difference in the balance is because treatment of fixed cost that gates absorbed in the

absorption costing technique. Thus, it is suggested to company to implement the absorption

costing techniques in order to get more reliable results.

a) Before installation of the new machine

Contribution Margin Per Unit =

Sales Price per unit – Variable cost per

unit

40-28 = 12 p.u.

Break even point in units = Fixed Costs/ Contribution Margin per

9

Apr ’19 May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’19

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening

inventory

0 0 15 0 0 15

Closing

inventory

0 15 0 0 15 10

Apr

’19

May

’19

Jun

’19

Jul ’19 Aug

’19

Sep’19

Net profits under

absorption costing

175 130 295 175 160 290

ADD: Fixed overheads in

opening

0 30 0 0 10 30

175 100 295 175 150 260

From the above calculation it has been determined that the net profit from marginal

costing method for the different month is lower than the absorption costing techniques. The main

reason for difference in the balance is because treatment of fixed cost that gates absorbed in the

absorption costing technique. Thus, it is suggested to company to implement the absorption

costing techniques in order to get more reliable results.

a) Before installation of the new machine

Contribution Margin Per Unit =

Sales Price per unit – Variable cost per

unit

40-28 = 12 p.u.

Break even point in units = Fixed Costs/ Contribution Margin per

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.