Management Accounting Report: Alpha Ltd. UK Pizza Production Analysis

VerifiedAdded on 2023/01/18

|21

|5617

|25

Report

AI Summary

This report provides a comprehensive analysis of Management Accounting (MA) practices within Alpha Limited, a UK-based pizza production company. It delves into various aspects of MA, including cost accounting systems, inventory management, and price optimization systems, highlighting their importance in internal decision-making. The report examines different types of MA reports, such as inventory, performance, and budget reports, and their role in monitoring financial and operational performance. Furthermore, it presents the preparation of income statements using both absorption and marginal costing methods, accompanied by financial statements and interpretation. The report also discusses the advantages and disadvantages of planning tools like budgetary control and their application in forecasting and budget preparation. Finally, it explores the role of Management Accounting Systems (MAS) in addressing financial issues within different enterprises, emphasizing their significance in financial problem-solving and overcoming monetary challenges.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1 ...........................................................................................................................................3

P1. MA and its types...................................................................................................................3

P2. Different methods of MA reports.........................................................................................4

M1. Benefits of MAS..................................................................................................................5

D1. Integration of MAS and MA reports with business process................................................6

TASK 2 ...........................................................................................................................................6

P3. Preparation of income statement by help of absorption and marginal costing.....................6

M2 Accounting techniques to produce financial statements.....................................................12

D2. Interpretation of produced financial statements.................................................................12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of different planning tools of budgetary control...............12

M3. Role of planning tools in order to make accurate forecasting and preparing the budgets.14

TASK 4..........................................................................................................................................14

P5. Difference between enterprises in order to sort financial issues by help of different MAS.

...................................................................................................................................................14

M4. Importance of MAS in the context of solving financial problems....................................16

D3. Role of planning tools in overcoming from monetary issues.............................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1 ...........................................................................................................................................3

P1. MA and its types...................................................................................................................3

P2. Different methods of MA reports.........................................................................................4

M1. Benefits of MAS..................................................................................................................5

D1. Integration of MAS and MA reports with business process................................................6

TASK 2 ...........................................................................................................................................6

P3. Preparation of income statement by help of absorption and marginal costing.....................6

M2 Accounting techniques to produce financial statements.....................................................12

D2. Interpretation of produced financial statements.................................................................12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of different planning tools of budgetary control...............12

M3. Role of planning tools in order to make accurate forecasting and preparing the budgets.14

TASK 4..........................................................................................................................................14

P5. Difference between enterprises in order to sort financial issues by help of different MAS.

...................................................................................................................................................14

M4. Importance of MAS in the context of solving financial problems....................................16

D3. Role of planning tools in overcoming from monetary issues.............................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Accounting is a major aspect of corporations in order to help monitor financial

transactions. The MA is one of the major components of accounting. It is connected to the

process of acquiring financial and non-financial information in order to prepare internal

statements when administrators need it (Siverbo, 2014). Only the internal investors are provided

with these reports. The goal of the project report is to examine the position of this company

accounting. Alpha limited company, which is headquartered in the United Kingdom and

specializes in the production of pizzas, has been selected in the report. The report contains

comprehensive information on various MAS, MA reports and instruments for planning, etc.

Furthermore, the report also mentions the role of different MAS in the monetary problem

filtering aspect.

MAIN BODY

TASK 1

P1. MA and its types.

MA- It is characterized as a form of accounting that functions in the process of gathering

qualitative and quantitative data so that inner reports can be prepared by the accountant. These

documents provide the supervisors with a comprehensive structure for making important internal

decisions. Several forms of MA are shown below, such as:

Cost accounting system - It is an accounting system that is applied with finance

department with the goal of making revolutionary budget estimates. Through having

estimates of additional costs, it then becomes easier for administrators to take appropriate

action to allocate funds as an arrangement of need in order to minimize costs (Granlund

and Lukka, 2017). This accounting system is important for companies to monitor the use

of funds and the total cost of running various functions performed. They use this

accounting system in the sense of the above-mentioned Alpha limited company to keep

costs lower than projections.

Essential requirement- This accounting system is essential for companies to track the

volume of cost of various kinds of operations and activities. On the basis of it, companies

take accurate decisions regards to allocation of funds into various tasks.

Accounting is a major aspect of corporations in order to help monitor financial

transactions. The MA is one of the major components of accounting. It is connected to the

process of acquiring financial and non-financial information in order to prepare internal

statements when administrators need it (Siverbo, 2014). Only the internal investors are provided

with these reports. The goal of the project report is to examine the position of this company

accounting. Alpha limited company, which is headquartered in the United Kingdom and

specializes in the production of pizzas, has been selected in the report. The report contains

comprehensive information on various MAS, MA reports and instruments for planning, etc.

Furthermore, the report also mentions the role of different MAS in the monetary problem

filtering aspect.

MAIN BODY

TASK 1

P1. MA and its types.

MA- It is characterized as a form of accounting that functions in the process of gathering

qualitative and quantitative data so that inner reports can be prepared by the accountant. These

documents provide the supervisors with a comprehensive structure for making important internal

decisions. Several forms of MA are shown below, such as:

Cost accounting system - It is an accounting system that is applied with finance

department with the goal of making revolutionary budget estimates. Through having

estimates of additional costs, it then becomes easier for administrators to take appropriate

action to allocate funds as an arrangement of need in order to minimize costs (Granlund

and Lukka, 2017). This accounting system is important for companies to monitor the use

of funds and the total cost of running various functions performed. They use this

accounting system in the sense of the above-mentioned Alpha limited company to keep

costs lower than projections.

Essential requirement- This accounting system is essential for companies to track the

volume of cost of various kinds of operations and activities. On the basis of it, companies

take accurate decisions regards to allocation of funds into various tasks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system- This is a form of accounting system correlated with the

process of monitoring regular stock value usage for the production of new goods. It is

entirely based on techniques of valuation such as last and first step, first method in first

method out and much more. It is important for companies to cut the storage costs as well

as to obtain information about the use of stock in undertaking manufacturing operations.

It is used in the dimension of the above-mentioned Alpha limited company, which allows

them to determine material use, finished products and many more.

Essential requirement- It is essential for manufacturing companies to compute cost and

quantity of stored stock. It determines about how much stock is remained in the

warehouses at the end of month or quarter that leads to better decision for managers.

Price optimisation system- It can be described as a form of management system that is

effectively related to the process of pricing goods and services. It becomes feasible

because key information about consumer understanding, reviews as well as potential

market is used by sales team. Based on this, they set prices of different products for

different parts of the market and clients. It is important for corporations to adjust prices of

products in line with market research. Their sales team, like in the Alpha limited

company, set Pizzas rates according to market dominance and customer needs.

Essential requirement- It is essential for keeping prices of products and services at a level

from which companies cannot get any lose. This becomes possible because under it

prices are set in accordance of market research.

Job order costing system- This is a form of cost system that uses the allocated number of

jobs to calculate the cost of each event (Kastberg and Siverbo, 2016). It is implemented

in those business entities in which portfolio of products is too larger because by help of

this they can assess cost of each performed functions individually. For instance in the

Alpha limited company, their managers implement this accounting system with an aim of

keeping control over the cost of job aligned to different number of activities and

operations.

Essential requirement- This is essential for determining cost of each output or product

produced by a company. Under it, cost is calculated in accordance of job cost aligned

with completing different activities.

process of monitoring regular stock value usage for the production of new goods. It is

entirely based on techniques of valuation such as last and first step, first method in first

method out and much more. It is important for companies to cut the storage costs as well

as to obtain information about the use of stock in undertaking manufacturing operations.

It is used in the dimension of the above-mentioned Alpha limited company, which allows

them to determine material use, finished products and many more.

Essential requirement- It is essential for manufacturing companies to compute cost and

quantity of stored stock. It determines about how much stock is remained in the

warehouses at the end of month or quarter that leads to better decision for managers.

Price optimisation system- It can be described as a form of management system that is

effectively related to the process of pricing goods and services. It becomes feasible

because key information about consumer understanding, reviews as well as potential

market is used by sales team. Based on this, they set prices of different products for

different parts of the market and clients. It is important for corporations to adjust prices of

products in line with market research. Their sales team, like in the Alpha limited

company, set Pizzas rates according to market dominance and customer needs.

Essential requirement- It is essential for keeping prices of products and services at a level

from which companies cannot get any lose. This becomes possible because under it

prices are set in accordance of market research.

Job order costing system- This is a form of cost system that uses the allocated number of

jobs to calculate the cost of each event (Kastberg and Siverbo, 2016). It is implemented

in those business entities in which portfolio of products is too larger because by help of

this they can assess cost of each performed functions individually. For instance in the

Alpha limited company, their managers implement this accounting system with an aim of

keeping control over the cost of job aligned to different number of activities and

operations.

Essential requirement- This is essential for determining cost of each output or product

produced by a company. Under it, cost is calculated in accordance of job cost aligned

with completing different activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Characteristics of financial information:

Reliability- This is essential for companies that their financial information should be

reliable as per the nature and activities of business.

Accuracy- As well as financial information needs to be accurate so that accountant can

produce correct financial statements at the end of financial year.

Timeliness- In addition, financial information needs to be presented to external and

internal stakeholders at the end of financial year. Any kinds of delay may lead to lose of

company.

P2. Different methods of MA reports.

MA reports – The term MA reports can be described as records that encompass important

information pertaining to all financial and anti-financial aspects. They prepare different kinds of

reports in the sense of the above-mentioned Alpha limited company, such as:

Inventory report- It can be described as a type of report that includes key information

related to the opened and closed of the balance of various forms of inventory, including

raw resources, completed goods etc. This report includes all types of data in order to

assess stock quantities under LIFO, FIFO and the weighted average method. Managers

use this report in the above-mentioned Alpha limited company with the aim of staying in

touch to how much material they have at the end of a specific day.

Performance report - This is a form of document that contains in depth key performance-

related information about each and every element. It's used by organization executives to

make logical decisions on employee growth. The overall performance of workers can be

hidden in the lack of this report. In addition to employee performance data, it offers key

details such as performance of various functions and tasks conducted, etc. The

accountants are conducting this document in the sense of the above-mentioned Alpha

limited company in order to ensure sustainable economic growth in different aspects.

Budget report- It is a document that provides specific information about the performance

of the plan and the actual output (Hirsch, Seubert and Sohn, 2015). Using this document,

the division of finance becomes able to evaluate the difference between actual and

projected performance. The accountants generate this report in the scope of the above-

mentioned Alpha limited company to monitor variances and to maintain an extra finger

on actual performance.

Reliability- This is essential for companies that their financial information should be

reliable as per the nature and activities of business.

Accuracy- As well as financial information needs to be accurate so that accountant can

produce correct financial statements at the end of financial year.

Timeliness- In addition, financial information needs to be presented to external and

internal stakeholders at the end of financial year. Any kinds of delay may lead to lose of

company.

P2. Different methods of MA reports.

MA reports – The term MA reports can be described as records that encompass important

information pertaining to all financial and anti-financial aspects. They prepare different kinds of

reports in the sense of the above-mentioned Alpha limited company, such as:

Inventory report- It can be described as a type of report that includes key information

related to the opened and closed of the balance of various forms of inventory, including

raw resources, completed goods etc. This report includes all types of data in order to

assess stock quantities under LIFO, FIFO and the weighted average method. Managers

use this report in the above-mentioned Alpha limited company with the aim of staying in

touch to how much material they have at the end of a specific day.

Performance report - This is a form of document that contains in depth key performance-

related information about each and every element. It's used by organization executives to

make logical decisions on employee growth. The overall performance of workers can be

hidden in the lack of this report. In addition to employee performance data, it offers key

details such as performance of various functions and tasks conducted, etc. The

accountants are conducting this document in the sense of the above-mentioned Alpha

limited company in order to ensure sustainable economic growth in different aspects.

Budget report- It is a document that provides specific information about the performance

of the plan and the actual output (Hirsch, Seubert and Sohn, 2015). Using this document,

the division of finance becomes able to evaluate the difference between actual and

projected performance. The accountants generate this report in the scope of the above-

mentioned Alpha limited company to monitor variances and to maintain an extra finger

on actual performance.

Accounts receivable ageing report - This can be described as a document which provides

comprehensive information on the maximum value of debt that will need to be

accumulated in the forthcoming period. Finance managers make further preparations as to

the need for funds to complete operations and events in conjunction with this report. One

of it's key features is that info is systematically reported under it so that executives can

easily check the debt level. In the Alpha limited company, they prepare this report and

their finance department collects funds according to information provided by report.

M1. Benefits of MAS.

MAS Benefits

Cost accounting system This accounting system is concerned, in accordance with the above

explanation, with the process of monitoring and reducing the costs of

various operations. They gain from this accounting in the above-

mentioned Alpha limited company by handling aggregate

expenditures and charges.

Inventory management

system

This helps companies' sales and manufacturing departments to

monitor goods usage and to calculate the opening & closing balance.

They benefit from this accounting, such as in the above-mentioned

Alpha limited company, by maintaining cost of storage low.

Price optimisation

system

It is attached to the organization sales department and to effectively

set prices of products. They update their pricing strategies in keeping

with the market environment in the Alpha limited company.

Job order costing system This is based on individually calculating the cost of various activities.

They are benefiting from this accounting system in the Alpha limited

company by tracking job costs effectively.

D1. Integration of MAS and MA reports with business process.

If companies struggle to align their divisions with accounting systems, it can become

impossible to operate lookup tables and activities efficiently (Chandar, Collier and Miranti,

2012). Their sales department is combined with price optimization system and inventory

comprehensive information on the maximum value of debt that will need to be

accumulated in the forthcoming period. Finance managers make further preparations as to

the need for funds to complete operations and events in conjunction with this report. One

of it's key features is that info is systematically reported under it so that executives can

easily check the debt level. In the Alpha limited company, they prepare this report and

their finance department collects funds according to information provided by report.

M1. Benefits of MAS.

MAS Benefits

Cost accounting system This accounting system is concerned, in accordance with the above

explanation, with the process of monitoring and reducing the costs of

various operations. They gain from this accounting in the above-

mentioned Alpha limited company by handling aggregate

expenditures and charges.

Inventory management

system

This helps companies' sales and manufacturing departments to

monitor goods usage and to calculate the opening & closing balance.

They benefit from this accounting, such as in the above-mentioned

Alpha limited company, by maintaining cost of storage low.

Price optimisation

system

It is attached to the organization sales department and to effectively

set prices of products. They update their pricing strategies in keeping

with the market environment in the Alpha limited company.

Job order costing system This is based on individually calculating the cost of various activities.

They are benefiting from this accounting system in the Alpha limited

company by tracking job costs effectively.

D1. Integration of MAS and MA reports with business process.

If companies struggle to align their divisions with accounting systems, it can become

impossible to operate lookup tables and activities efficiently (Chandar, Collier and Miranti,

2012). Their sales department is combined with price optimization system and inventory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management system, as in the Alpha limited company. Furthermore, their manufacturing

department uses important stock management report information and the accounting department

also evaluates important information from the account receivable ageing report.

Difference between financial and management accounting:

Financial accounting Management accounting

In this accounting only monetary information

is included.

While in this accounting monetary and anti

monetary information is included.

This is applied for assessing financial

condition of companies.

On the other hand, this accounting is

implemented for internal management.

Under it, financial statements are prepared as

per the accounting standards.

There is no any accounting standards to

prepare internal reports.

TASK 2

P3. Preparation of income statement by help of absorption and marginal costing.

It is necessary for companies to produce financial statements at the end of an accounting

period. For this purpose accountants become responsible to follow all standards and techniques

to prepare statements in an effective manner. Herein, below some techniques are mentioned that

are used to prepare income statements such as:

Absorption costing system- It is also known as full absorption costing method for

assessing all types of cost that is aligned to manufacturing process. Different types of cost

like direct material, labour etc. are absorbed in this method. This technique needed by

generally accepted accounting principle for purpose of external reporting.

department uses important stock management report information and the accounting department

also evaluates important information from the account receivable ageing report.

Difference between financial and management accounting:

Financial accounting Management accounting

In this accounting only monetary information

is included.

While in this accounting monetary and anti

monetary information is included.

This is applied for assessing financial

condition of companies.

On the other hand, this accounting is

implemented for internal management.

Under it, financial statements are prepared as

per the accounting standards.

There is no any accounting standards to

prepare internal reports.

TASK 2

P3. Preparation of income statement by help of absorption and marginal costing.

It is necessary for companies to produce financial statements at the end of an accounting

period. For this purpose accountants become responsible to follow all standards and techniques

to prepare statements in an effective manner. Herein, below some techniques are mentioned that

are used to prepare income statements such as:

Absorption costing system- It is also known as full absorption costing method for

assessing all types of cost that is aligned to manufacturing process. Different types of cost

like direct material, labour etc. are absorbed in this method. This technique needed by

generally accepted accounting principle for purpose of external reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing system- This is a type of technique in that variable costs are allocated to

cost of unit and fixed costs are as period cost. It is opposite from above costing technique

because under this total incurred cost is not absorbed (Horton and de Araujo Wanderley,

2018).

Problem 1.

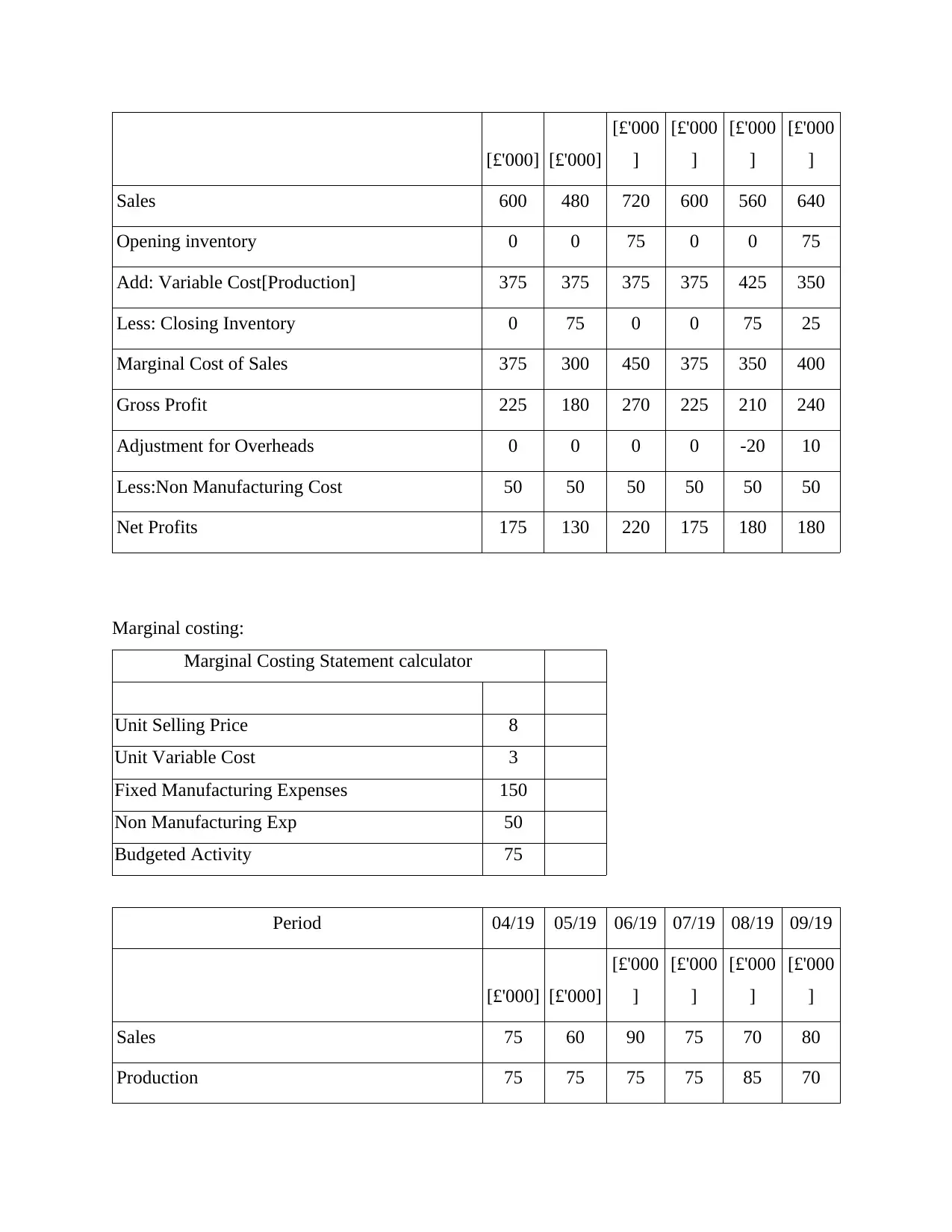

Income statement under absorption and marginal costing:

Absorption costing:

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19

01/09/

19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

cost of unit and fixed costs are as period cost. It is opposite from above costing technique

because under this total incurred cost is not absorbed (Horton and de Araujo Wanderley,

2018).

Problem 1.

Income statement under absorption and marginal costing:

Absorption costing:

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19

01/09/

19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost[Production] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

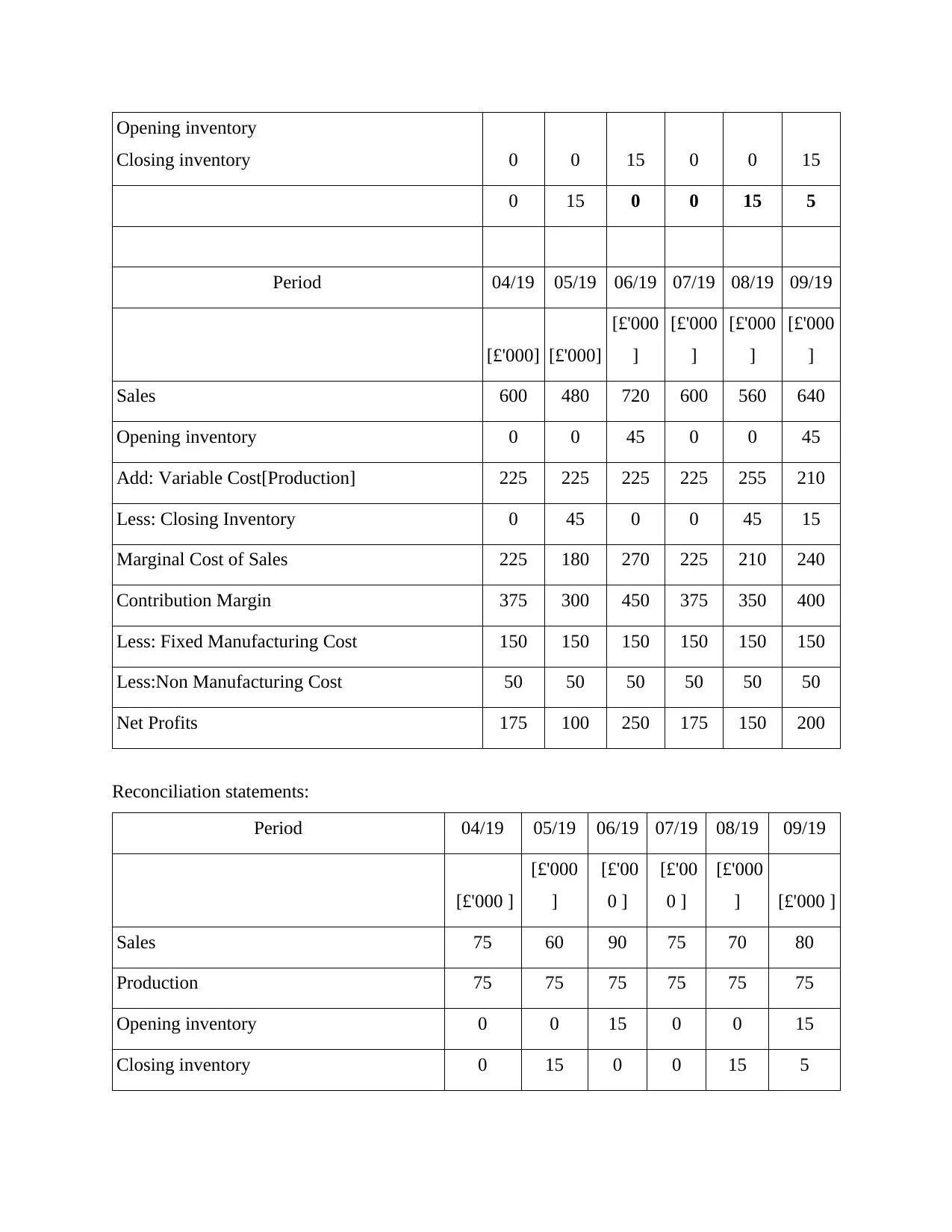

Marginal costing:

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost[Production] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Marginal costing:

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Production] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufacturing Cost 150 150 150 150 150 150

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Sales 75 60 90 75 70 80

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Production] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufacturing Cost 150 150 150 150 150 150

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Sales 75 60 90 75 70 80

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units)= Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues)= Fixed cost/ PV ratio

= 180000/ 30*100

= £600000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units)= Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues)= Fixed cost/ PV ratio

= 180000/ 30*100

= £600000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

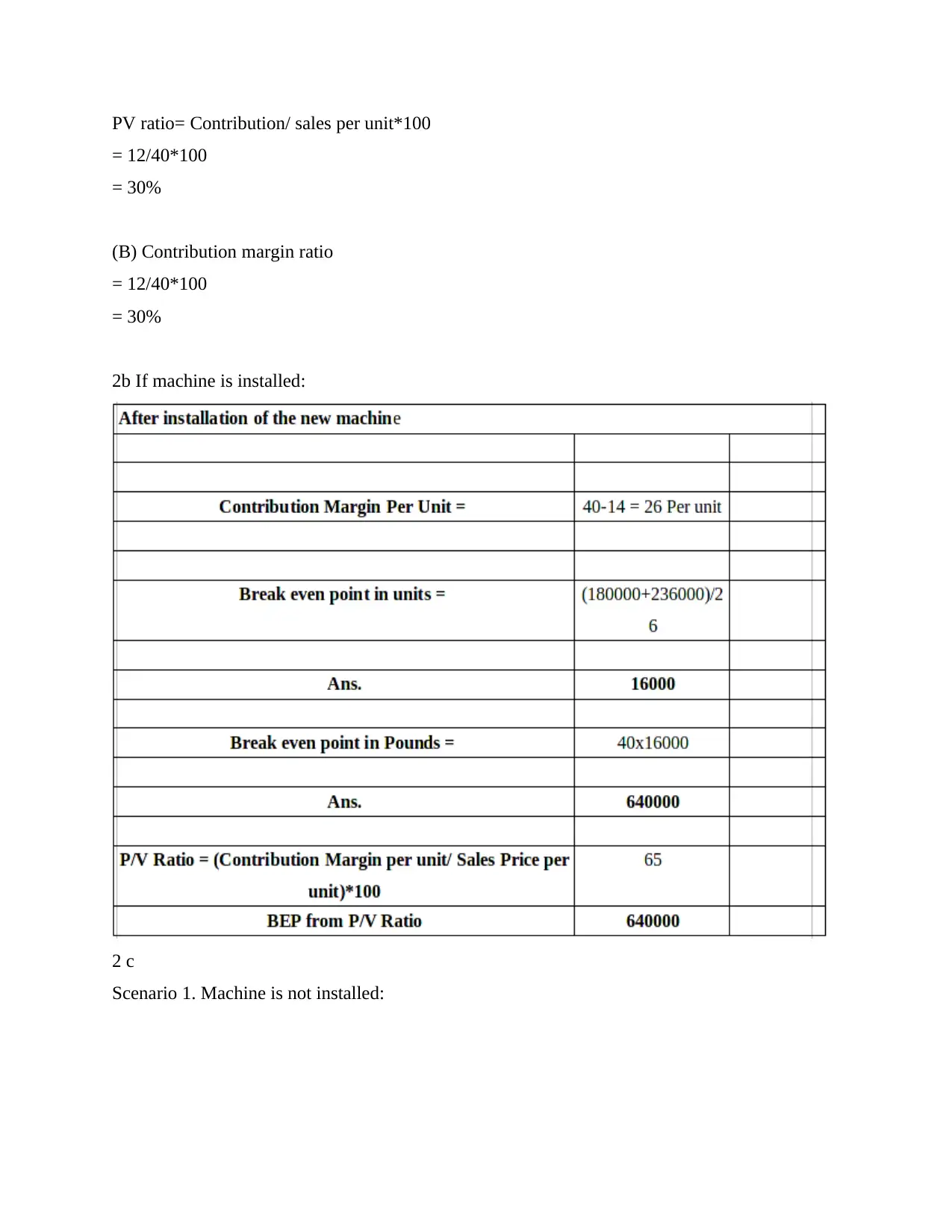

PV ratio= Contribution/ sales per unit*100

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

2b If machine is installed:

2 c

Scenario 1. Machine is not installed:

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

2b If machine is installed:

2 c

Scenario 1. Machine is not installed:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.