Corporate Accounting Report: Financial Analysis of ALS Global Limited

VerifiedAdded on 2024/05/31

|12

|2721

|441

Report

AI Summary

This report provides an in-depth examination of ALS Global Limited's financial statements, focusing on the cash flow statement, other comprehensive income statement, and accounting for corporate income tax. The analysis includes a comparative assessment of operating, investing, and financing activities to determine cash inflows and outflows. It identifies key items within each section of the cash flow statement, such as cash receipts from customers, payments to suppliers and employees, and proceeds from borrowings. The report also explains items recorded in the other comprehensive income statement, including foreign exchange translation and gains on hedges. Furthermore, it delves into the company's tax expenses, deferred tax assets and liabilities, and the relationship between income tax expense and income tax paid. The report concludes with a reflection on the complexities and insights gained from analyzing ALS Global Limited's financial reporting, highlighting the transparency in its taxation practices.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................3

Cash Flow Statement...................................................................................................................................4

Other Comprehensive Income Statement....................................................................................................8

Accounting for Corporate Income Tax........................................................................................................9

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

2

Introduction.................................................................................................................................................3

Cash Flow Statement...................................................................................................................................4

Other Comprehensive Income Statement....................................................................................................8

Accounting for Corporate Income Tax........................................................................................................9

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

2

Introduction

This report deals with the examination of the financial statements of the ALS Global Limited so

that it financial position can be examined and the changes in the statement can be done

accordingly. The cash flow statement is analyzed and the items which are reported in the cash

flow are predicted. With this the comparative statement analysis is of the investing, operating

and the financial activities are done so that the inflow and the outflow of the cash and cash

equivalents can be determined. ALS Global Limited is the organization which basically provides

the testing services. It was founded in 1863 under the name Campbell Brothers. It is basically

inspection, testing and Certification Company which have its headquarters in Brisbane,

Australia. It has more than 11,500 staff which operates in over 370 locations in approximately 65

countries. The examination of the company’s taxes is also done so that the better understanding

of the taxes can be gained.

3

This report deals with the examination of the financial statements of the ALS Global Limited so

that it financial position can be examined and the changes in the statement can be done

accordingly. The cash flow statement is analyzed and the items which are reported in the cash

flow are predicted. With this the comparative statement analysis is of the investing, operating

and the financial activities are done so that the inflow and the outflow of the cash and cash

equivalents can be determined. ALS Global Limited is the organization which basically provides

the testing services. It was founded in 1863 under the name Campbell Brothers. It is basically

inspection, testing and Certification Company which have its headquarters in Brisbane,

Australia. It has more than 11,500 staff which operates in over 370 locations in approximately 65

countries. The examination of the company’s taxes is also done so that the better understanding

of the taxes can be gained.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash Flow Statement

(I) The cash flow statement of the ALS Global Limited shows the inflow and the outflow

of cash (Sözbilir, et. al., 2015). The items which are listed in the cash flow statement

of the organization are:

Operating Activities: The cash from the operating activities basically focuses on the inflow and

outflow of company’s business activities which are related with buying and selling of services

and merchandise (ALS Global Limited, 2018). The items which are listed of the operating

activities are:

Cash receipt from customers: It show the proceeds of all the cash which are received

from the customers to the organization (De Cristofaro and Falzago, 2014).

Cash paid to suppliers and employees: It includes the payments which are done to the

employees for their contribution as well as the suppliers (ALS Global Limited, 2018).

Interest Paid: It is the amount of interest which is paid by the organization on fixed or the

variable rate for securities.

Interest Received: It determines the interest which is received as the income for the

purchase of securities (ALS Global Limited, 2018).

Income Taxes Paid: It is the obligation which has to be paid by the organizations on the

assessable income.

Investing Activities: It determines the amount of cash which is received by the organizations for

doing investment in the financial markets. The items of the investing activities are:

Payments for property, plant and equipments: It shows all the payments which are

made by the organization for purchasing the property, equipments and the plant (ALS

Global Limited, 2018).

Repayments / Loans joint venture entity: It shows the repayment of all the loans which

are taken by the organization for the business purpose (ALS Global Limited, 2018).

Payment for net assets on acquisition of business and subsidies: It is the payment which

is made for the acquisition of the net assets for the business purpose (Safonova, et. al.,

2016).

Acquisition of minority interest equity: The acquisition for the fraction share of

company which is amounting to be less than 50% of the voting shares (ALS Global

Limited, 2018).

4

(I) The cash flow statement of the ALS Global Limited shows the inflow and the outflow

of cash (Sözbilir, et. al., 2015). The items which are listed in the cash flow statement

of the organization are:

Operating Activities: The cash from the operating activities basically focuses on the inflow and

outflow of company’s business activities which are related with buying and selling of services

and merchandise (ALS Global Limited, 2018). The items which are listed of the operating

activities are:

Cash receipt from customers: It show the proceeds of all the cash which are received

from the customers to the organization (De Cristofaro and Falzago, 2014).

Cash paid to suppliers and employees: It includes the payments which are done to the

employees for their contribution as well as the suppliers (ALS Global Limited, 2018).

Interest Paid: It is the amount of interest which is paid by the organization on fixed or the

variable rate for securities.

Interest Received: It determines the interest which is received as the income for the

purchase of securities (ALS Global Limited, 2018).

Income Taxes Paid: It is the obligation which has to be paid by the organizations on the

assessable income.

Investing Activities: It determines the amount of cash which is received by the organizations for

doing investment in the financial markets. The items of the investing activities are:

Payments for property, plant and equipments: It shows all the payments which are

made by the organization for purchasing the property, equipments and the plant (ALS

Global Limited, 2018).

Repayments / Loans joint venture entity: It shows the repayment of all the loans which

are taken by the organization for the business purpose (ALS Global Limited, 2018).

Payment for net assets on acquisition of business and subsidies: It is the payment which

is made for the acquisition of the net assets for the business purpose (Safonova, et. al.,

2016).

Acquisition of minority interest equity: The acquisition for the fraction share of

company which is amounting to be less than 50% of the voting shares (ALS Global

Limited, 2018).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acquisition of associate entity equity: It is the amount which is received for the

investments in the associations.

Dividend from associate: The amount which is received as dividends from the

associates (ALS Global Limited, 2018).

Proceeds from sale of other non-current assets: It is the earnings from the sale of assets

which are non-current (Devalle and Magarini, 2012).

Financing Activities: These are those transactions which are with the creditors or investors used

to fund the operations of the company and its expansion (Sözbilir, et. al., 2015). The items of the

financing activities are:

Proceeds from borrowings: It is the amount which is received from the sale of

borrowings (ALS Global Limited, 2018).

Repayment of borrowings: It is the act to pay back the money which is received from the

lender for borrowings.

Proceeds from issue of new issued capital: This shows the amount which is received by

the organizations for issue of new share capital.

Lease Payments: It is the payment done for any of the property which is taken as the

lease by organization.

Dividends paid: It is the payment to shareholders which is done as the distribution of

profits (Sözbilir, et. al., 2015).

There were the changes in the cash flow statement as there were no repayments in the year 2017

for the organization and with that the amount of acquisition of minority interest equity was also

missing (Sözbilir, et. al., 2015). This was there as the acquisitions were not made during the year

and the amount was not adjusted to equity.

5

investments in the associations.

Dividend from associate: The amount which is received as dividends from the

associates (ALS Global Limited, 2018).

Proceeds from sale of other non-current assets: It is the earnings from the sale of assets

which are non-current (Devalle and Magarini, 2012).

Financing Activities: These are those transactions which are with the creditors or investors used

to fund the operations of the company and its expansion (Sözbilir, et. al., 2015). The items of the

financing activities are:

Proceeds from borrowings: It is the amount which is received from the sale of

borrowings (ALS Global Limited, 2018).

Repayment of borrowings: It is the act to pay back the money which is received from the

lender for borrowings.

Proceeds from issue of new issued capital: This shows the amount which is received by

the organizations for issue of new share capital.

Lease Payments: It is the payment done for any of the property which is taken as the

lease by organization.

Dividends paid: It is the payment to shareholders which is done as the distribution of

profits (Sözbilir, et. al., 2015).

There were the changes in the cash flow statement as there were no repayments in the year 2017

for the organization and with that the amount of acquisition of minority interest equity was also

missing (Sözbilir, et. al., 2015). This was there as the acquisitions were not made during the year

and the amount was not adjusted to equity.

5

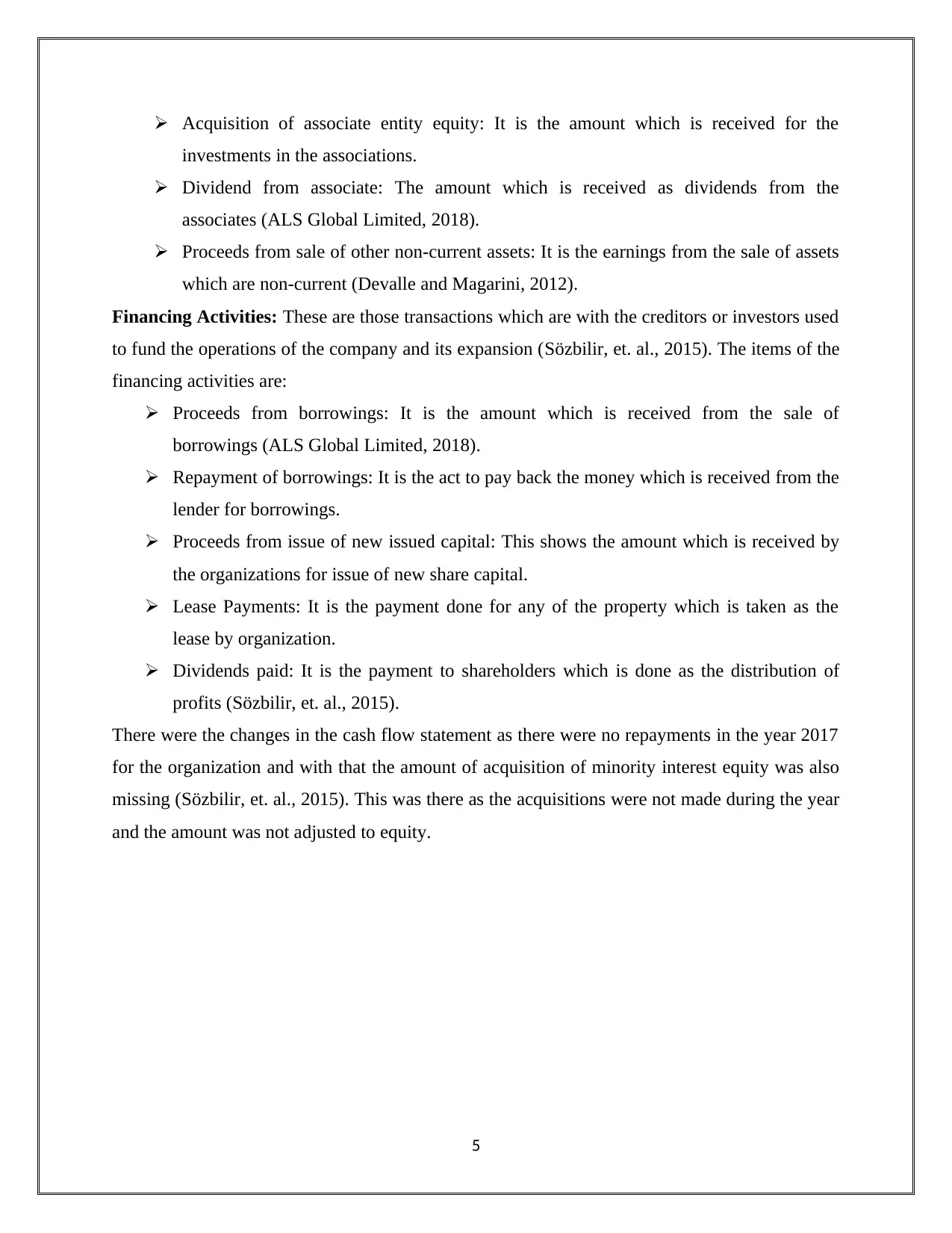

(II)

2015-2016

6

2015-2016

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

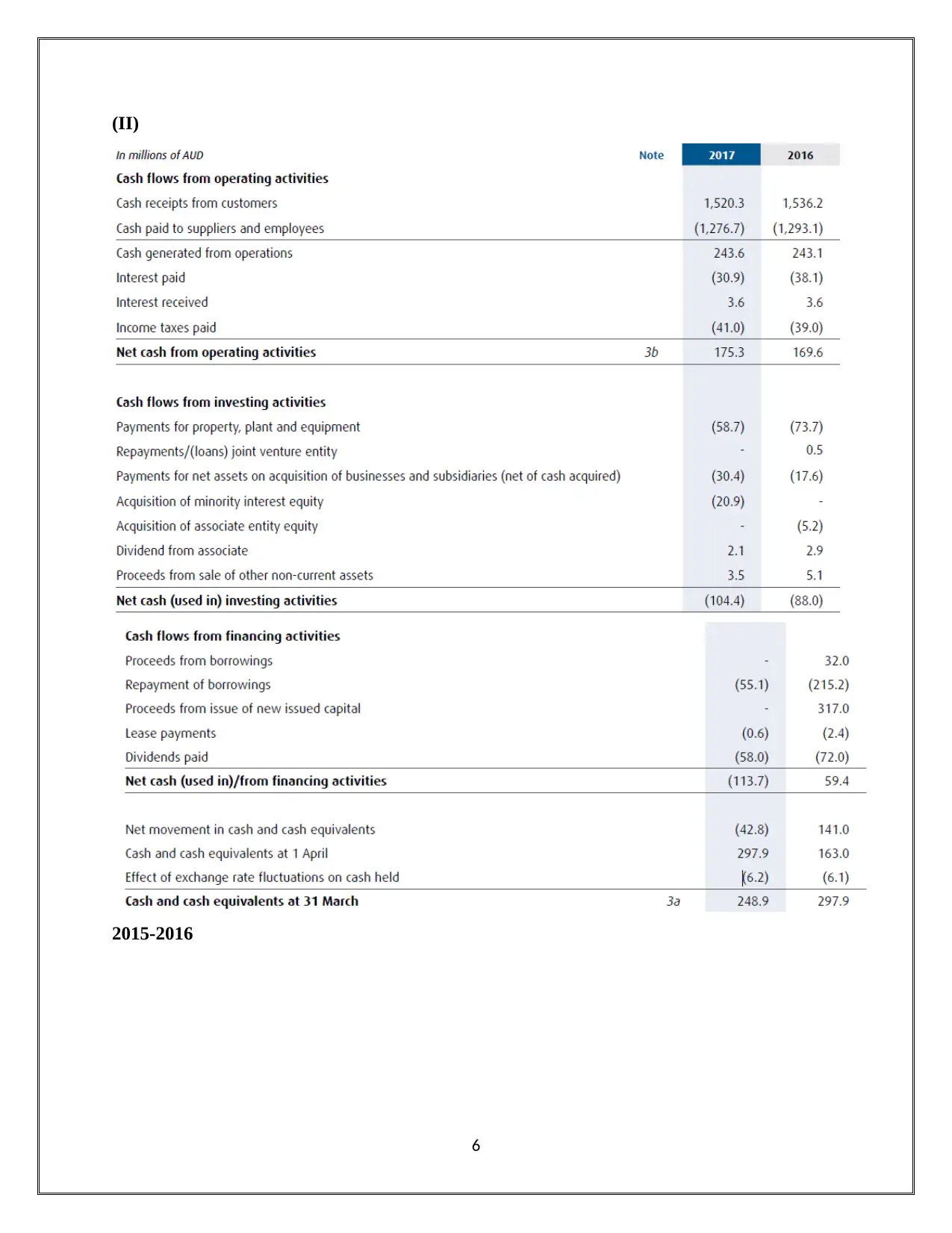

These are the cash flow statement of all the 3 years of ALS Global Limited. It can be evaluated

that in 2015 the operating activities was 215.2 while in the year 2016 it was 169.6 and in 2017 it

was 175.3 which shows that the cash received from the operations was more in 2015 but it got

decreased and again increased in 2017 (ALS Global Limited, 2018). The cash flows from the

investing activities was for 2015-16 and 2016-17 was 83, 88 and 104 so it showed that the

company in investing in the activities which are producing the positive returns in investment

activities. The flows from financing activities in 2015 were 110 and in 2016 were 59.4 and in

2017 it was 113.7. This shows that the operations of the business are running properly from the

preceding year (ALS Global Limited, 2018).

7

that in 2015 the operating activities was 215.2 while in the year 2016 it was 169.6 and in 2017 it

was 175.3 which shows that the cash received from the operations was more in 2015 but it got

decreased and again increased in 2017 (ALS Global Limited, 2018). The cash flows from the

investing activities was for 2015-16 and 2016-17 was 83, 88 and 104 so it showed that the

company in investing in the activities which are producing the positive returns in investment

activities. The flows from financing activities in 2015 were 110 and in 2016 were 59.4 and in

2017 it was 113.7. This shows that the operations of the business are running properly from the

preceding year (ALS Global Limited, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other Comprehensive Income Statement

(III) The items which are recorded in the other comprehensive income statement are:

o Foreign exchange translation

o Gain/ Loss on hedge of net investments in foreign subsidies

o Gain on cash flow hedges taken to equity, net of tax (ALS Global Limited, 2018)

(IV) The items which are listed in the other comprehensive income statements are explained

as:

Foreign Exchange translation: In the foreign exchange translation the foreign currency

transactions are translated into one rate and then the losses and gains are recorded in the other

comprehensive income statement as the foreign exchange translation (ALS Global Limited,

2018).

Gains on hedge of net investments in foreign subsidies: These are the gains which are

received to the organization from doing the investment in the foreign subsidies (Muthuvelan,

2015).

Gain on cash flow hedges taken to equity, net of tax: These are the gains which are received

by the organization and from that the investment is done to equity (Sözbilir, et. al., 2015).

(V) These items are not been reported in the income statement as these items are not been

realized till the closing date of the income statement. These will be recorded in income

statement once they will be realized (Muthuvelan, 2015). The other comprehensive

income statement includes all the other revenues, gains and expenses that have affected

the equity of shareholder during the accounting period.

8

(III) The items which are recorded in the other comprehensive income statement are:

o Foreign exchange translation

o Gain/ Loss on hedge of net investments in foreign subsidies

o Gain on cash flow hedges taken to equity, net of tax (ALS Global Limited, 2018)

(IV) The items which are listed in the other comprehensive income statements are explained

as:

Foreign Exchange translation: In the foreign exchange translation the foreign currency

transactions are translated into one rate and then the losses and gains are recorded in the other

comprehensive income statement as the foreign exchange translation (ALS Global Limited,

2018).

Gains on hedge of net investments in foreign subsidies: These are the gains which are

received to the organization from doing the investment in the foreign subsidies (Muthuvelan,

2015).

Gain on cash flow hedges taken to equity, net of tax: These are the gains which are received

by the organization and from that the investment is done to equity (Sözbilir, et. al., 2015).

(V) These items are not been reported in the income statement as these items are not been

realized till the closing date of the income statement. These will be recorded in income

statement once they will be realized (Muthuvelan, 2015). The other comprehensive

income statement includes all the other revenues, gains and expenses that have affected

the equity of shareholder during the accounting period.

8

Accounting for Corporate Income Tax

(VI) The tax expenses are the expenses amount that is recognized by the business in the

accounting period for the payment of the taxes to the government. It is related to the

taxable profits. The amount of tax expenses of ALS Global Limited is $41.1 in 2017

(ALS Global Limited, 2018). This is the liability which is owed by the organization to

the government (Frank and James, 2014).

(VII) Yes, it is same as the effective tax rate determines that rate at which the taxes are

charged by the company. The tax rate is different for the individual tax rates as for them

the tax is charged from that of the income which is earned by the individuals. But there

is slight difference between the tax rates of the corporate and individuals that the tax of

the tax of the corporate are charged at the pre-tax profits (Frank and James, 2014).

Therefore, it can be seen that the tax rate is same as that of the company’s tax rate times.

(VIII) The deferred tax asset and liabilities which are recorded in the balance sheet of ALS

Global Limited are as deferred tax assets are 20.5 and the liabilities are 9 (ALS Global

Limited, 2018). They are been recorded in the balance sheet as these are the liabilities of

the organization which has to be paid (Safonova, et. al., 2016). The deferred tax is

provided for the temporary purposes between the carrying amount of assets as well as

the liabilities. These deferred taxes are provided on the basis of its realization value.

These differences occur due to investment in subsidiaries that they will not reverse in

future (Frank and James, 2014).

(IX) Yes, there are the income tax payables recorded by the organization in the consolidated

statement of the cash flow. The amount of income tax paid is $41 (ALS Global Limited,

2018). The amount of income tax expense and the income tax paid is not same as the tax

paid is treated as the liability of the organization while the income tax expense is treated

as the revenue for the business. Since both the taxes are the obligations for the

government but the tax expense is the amount that is owned in accordance with the

accounting standards while the tax payable are the actual amount that is owed by the

organization and has to be paid to the government (Frank and James, 2014).

(X) The income tax expense shown in the income statement is not same as that of the income

tax paid in the cash flow statement (Frank and James, 2014). As the tax expense is the

income for the organization so it is shown in the income statement and the tax payable is

9

(VI) The tax expenses are the expenses amount that is recognized by the business in the

accounting period for the payment of the taxes to the government. It is related to the

taxable profits. The amount of tax expenses of ALS Global Limited is $41.1 in 2017

(ALS Global Limited, 2018). This is the liability which is owed by the organization to

the government (Frank and James, 2014).

(VII) Yes, it is same as the effective tax rate determines that rate at which the taxes are

charged by the company. The tax rate is different for the individual tax rates as for them

the tax is charged from that of the income which is earned by the individuals. But there

is slight difference between the tax rates of the corporate and individuals that the tax of

the tax of the corporate are charged at the pre-tax profits (Frank and James, 2014).

Therefore, it can be seen that the tax rate is same as that of the company’s tax rate times.

(VIII) The deferred tax asset and liabilities which are recorded in the balance sheet of ALS

Global Limited are as deferred tax assets are 20.5 and the liabilities are 9 (ALS Global

Limited, 2018). They are been recorded in the balance sheet as these are the liabilities of

the organization which has to be paid (Safonova, et. al., 2016). The deferred tax is

provided for the temporary purposes between the carrying amount of assets as well as

the liabilities. These deferred taxes are provided on the basis of its realization value.

These differences occur due to investment in subsidiaries that they will not reverse in

future (Frank and James, 2014).

(IX) Yes, there are the income tax payables recorded by the organization in the consolidated

statement of the cash flow. The amount of income tax paid is $41 (ALS Global Limited,

2018). The amount of income tax expense and the income tax paid is not same as the tax

paid is treated as the liability of the organization while the income tax expense is treated

as the revenue for the business. Since both the taxes are the obligations for the

government but the tax expense is the amount that is owned in accordance with the

accounting standards while the tax payable are the actual amount that is owed by the

organization and has to be paid to the government (Frank and James, 2014).

(X) The income tax expense shown in the income statement is not same as that of the income

tax paid in the cash flow statement (Frank and James, 2014). As the tax expense is the

income for the organization so it is shown in the income statement and the tax payable is

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the outflow of the cash from the organization so it is shown in the cash flow statement.

The cash flow statement shows the inflow and the outflow of cash in the organization so

the payment of the tax means that the cash has been deducted from the total amount by

the flow of cash components (ALS Global Limited, 2018). While in case of the tax

expense which is an income so is shown on the income statement. The income statement

records all the transactions from which the income has been received to the organization.

(XI) There were the parts which were quite confusing to evaluate while evaluating the

treatment of taxes in the firm’s financial statements (Frank and James, 2014). The

biggest confusion was about the evaluation of deferred tax that why these taxes are

treated in the balance sheet and why the amount of the deferred taxes assets and the

deferred tax liability varies. With this confusion there were interesting facts as well. The

interesting part was that it gave the understanding about how the various taxes are

treated in various statements and what are their implications in the organization. With

that it was also seen that there was transparency in the reporting of taxation of ALS

Global Limited (ALS Global Limited, 2018).

With confusing and interesting there was the surprising fact also involved. The most surprising

fact was that the amount of the tax payable is not same as that of tax expense (Frank and James,

2014). There should not be the difference between the two as there both are the tax liabilities that

have to be taken by the organizations. There was difficulty in analyzing the financial statements

as the treatment of the taxes in these statements are bit complex to evaluate (ALS Global

Limited, 2018). With this the difficulty was also faced by analyzing the difference between the

tax payable and the tax expenses (Frank and James, 2014).

The new insight was also gained from the analysis of taxes that all the taxes are treated under the

different heads and the taxes are not only treated as the liability but they are also treated as the

income (Devalle and Magarini, 2012).

10

The cash flow statement shows the inflow and the outflow of cash in the organization so

the payment of the tax means that the cash has been deducted from the total amount by

the flow of cash components (ALS Global Limited, 2018). While in case of the tax

expense which is an income so is shown on the income statement. The income statement

records all the transactions from which the income has been received to the organization.

(XI) There were the parts which were quite confusing to evaluate while evaluating the

treatment of taxes in the firm’s financial statements (Frank and James, 2014). The

biggest confusion was about the evaluation of deferred tax that why these taxes are

treated in the balance sheet and why the amount of the deferred taxes assets and the

deferred tax liability varies. With this confusion there were interesting facts as well. The

interesting part was that it gave the understanding about how the various taxes are

treated in various statements and what are their implications in the organization. With

that it was also seen that there was transparency in the reporting of taxation of ALS

Global Limited (ALS Global Limited, 2018).

With confusing and interesting there was the surprising fact also involved. The most surprising

fact was that the amount of the tax payable is not same as that of tax expense (Frank and James,

2014). There should not be the difference between the two as there both are the tax liabilities that

have to be taken by the organizations. There was difficulty in analyzing the financial statements

as the treatment of the taxes in these statements are bit complex to evaluate (ALS Global

Limited, 2018). With this the difficulty was also faced by analyzing the difference between the

tax payable and the tax expenses (Frank and James, 2014).

The new insight was also gained from the analysis of taxes that all the taxes are treated under the

different heads and the taxes are not only treated as the liability but they are also treated as the

income (Devalle and Magarini, 2012).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

From the above discussion it can be concluded that the financial statement of the company shows

the financial performance of the organization in the competitive market. The cash flow

statements are analyzed so that the flow of the cash in the economy can be evaluated and

understanding about items which are placed in the financial accounts can be gained. The

comprehensive income statement records those transactions which are not realized till the date of

the final accounting period. Besides this the report also provides the understanding about various

taxes which are used and the corporate and their treatment so that the knowledge about the

taxation can be gained and the treatment of the taxes can be examined. These all the aspects are

covered in the report so that the overall analysis of the ASL Global Limited can be determined.

11

From the above discussion it can be concluded that the financial statement of the company shows

the financial performance of the organization in the competitive market. The cash flow

statements are analyzed so that the flow of the cash in the economy can be evaluated and

understanding about items which are placed in the financial accounts can be gained. The

comprehensive income statement records those transactions which are not realized till the date of

the final accounting period. Besides this the report also provides the understanding about various

taxes which are used and the corporate and their treatment so that the knowledge about the

taxation can be gained and the treatment of the taxes can be examined. These all the aspects are

covered in the report so that the overall analysis of the ASL Global Limited can be determined.

11

References

ALS Global Limited, 2018. Annual Reports. [Online]. ALS Global Limited. Available at:

https://www.alsglobal.com/myals/investors. [Accessed On 16 May 2018]

Frank, B.P. and James, O.K., 2014. Cashflow and Corporate Performance: A Study of

Selected Food and Beverage Companies in Nigeria. European Journal of Accounting

Auditing and Finance Research, 2(2), pp.77-87.

Muthuvelan, M., 2015. A STUDY ON CASH FLOW ANALYSIS IN M/S.

PANTALOON RETAIL (INDIA) LIMITED. International Journal of Management

Research and Reviews, 5(5), p.315.

Sözbilir, H., Kula, V. and Baykut, L.E., 2015. A Research on Deferred Taxes: A Case

Study of BIST Listed Banks in Turkey. European Journal of Business and Management,

7(2), pp.1-10.

Safonova, M.F., Kalinina, I.N., Vasilieva, N.K., Bershitskiy, Y.I. and Kiselevich, T.I.,

2016. Methodology of Planning Tax Expenses. International Journal of Economics and

Financial Issues, 6(4).

Devalle, A. and Magarini, R., 2012. Assessing the value relevance of total comprehensive

income under IFRS: an empirical evidence from European stock exchanges. International

Journal of Accounting, Auditing and Performance Evaluation, 8(1), pp.43-68.

De Cristofaro, T. and Falzago, B., 2014. What trend for Comprehensive Income

Presentation? Evidence from Italy. International Journal, 2(3), pp.17-40.

12

ALS Global Limited, 2018. Annual Reports. [Online]. ALS Global Limited. Available at:

https://www.alsglobal.com/myals/investors. [Accessed On 16 May 2018]

Frank, B.P. and James, O.K., 2014. Cashflow and Corporate Performance: A Study of

Selected Food and Beverage Companies in Nigeria. European Journal of Accounting

Auditing and Finance Research, 2(2), pp.77-87.

Muthuvelan, M., 2015. A STUDY ON CASH FLOW ANALYSIS IN M/S.

PANTALOON RETAIL (INDIA) LIMITED. International Journal of Management

Research and Reviews, 5(5), p.315.

Sözbilir, H., Kula, V. and Baykut, L.E., 2015. A Research on Deferred Taxes: A Case

Study of BIST Listed Banks in Turkey. European Journal of Business and Management,

7(2), pp.1-10.

Safonova, M.F., Kalinina, I.N., Vasilieva, N.K., Bershitskiy, Y.I. and Kiselevich, T.I.,

2016. Methodology of Planning Tax Expenses. International Journal of Economics and

Financial Issues, 6(4).

Devalle, A. and Magarini, R., 2012. Assessing the value relevance of total comprehensive

income under IFRS: an empirical evidence from European stock exchanges. International

Journal of Accounting, Auditing and Performance Evaluation, 8(1), pp.43-68.

De Cristofaro, T. and Falzago, B., 2014. What trend for Comprehensive Income

Presentation? Evidence from Italy. International Journal, 2(3), pp.17-40.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.