Corporate and Financial Accounting: Alterra vs. Angel Seafood Report

VerifiedAdded on 2022/10/17

|11

|2923

|10

Report

AI Summary

This report presents a comparative analysis of Alterra Limited and Angel Seafood Holdings, focusing on their sources of funds and financial performance over a three-year period. The analysis examines the equity and liabilities sections of their financial statements, detailing the movements in issued capital, reserves, and retained earnings, as well as trade payables, borrowings, and other liabilities. The report then contrasts the funding strategies of the two companies, highlighting the role of equity share capital and debt. Furthermore, the report explores the classifications of entities for reporting purposes, differentiating between small proprietary companies, large proprietary companies, and reporting entities, and discussing the compliance requirements of large proprietary companies. The study uses financial data from annual reports to provide insights into the financial health and strategies of the two companies, relevant for corporate and financial accounting.

Corporate and Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alteraa vs. Angel

Abstract

The operations and the success of a company depends on the sources of funds to a major

extent. In this report, the different sources of funds in relation to Alterra Limited and Angel

Seafoods have been studied. The comparative analysis provides a clear understanding on

the movement of funds and the manner in which the funds are utilized by both the companies.

To conduct this analysis, a time span of 3 years is taken into consideration and the study is

conducted by considering the financial statements and annual report. The second part of the

report deals with entities classification for the purpose of reporting.

2

Abstract

The operations and the success of a company depends on the sources of funds to a major

extent. In this report, the different sources of funds in relation to Alterra Limited and Angel

Seafoods have been studied. The comparative analysis provides a clear understanding on

the movement of funds and the manner in which the funds are utilized by both the companies.

To conduct this analysis, a time span of 3 years is taken into consideration and the study is

conducted by considering the financial statements and annual report. The second part of the

report deals with entities classification for the purpose of reporting.

2

Alteraa vs. Angel

Contents

Introduction.................................................................................................................................3

1. Equity Section.......................................................................................................................3

2. Equity Section – Movements................................................................................................3

3. Liabilities Section..................................................................................................................4

4. Liabilities Section – Movements...........................................................................................4

5. Comparison of the sources of funds....................................................................................6

Part B..........................................................................................................................................7

Critical examination of small proprietary company, large proprietary company and reporting

entity............................................................................................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

3

Contents

Introduction.................................................................................................................................3

1. Equity Section.......................................................................................................................3

2. Equity Section – Movements................................................................................................3

3. Liabilities Section..................................................................................................................4

4. Liabilities Section – Movements...........................................................................................4

5. Comparison of the sources of funds....................................................................................6

Part B..........................................................................................................................................7

Critical examination of small proprietary company, large proprietary company and reporting

entity............................................................................................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Alteraa vs. Angel

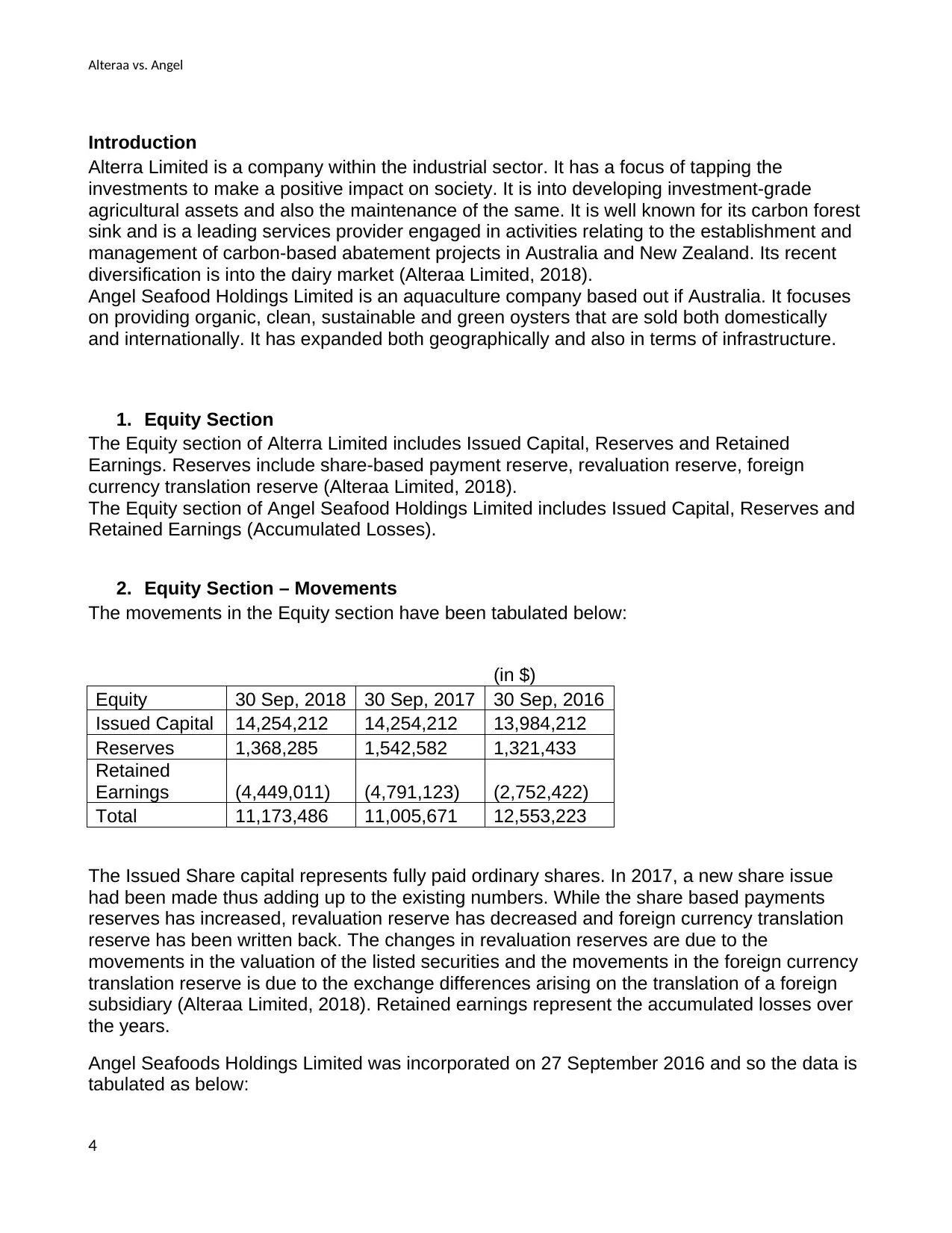

Introduction

Alterra Limited is a company within the industrial sector. It has a focus of tapping the

investments to make a positive impact on society. It is into developing investment-grade

agricultural assets and also the maintenance of the same. It is well known for its carbon forest

sink and is a leading services provider engaged in activities relating to the establishment and

management of carbon-based abatement projects in Australia and New Zealand. Its recent

diversification is into the dairy market (Alteraa Limited, 2018).

Angel Seafood Holdings Limited is an aquaculture company based out if Australia. It focuses

on providing organic, clean, sustainable and green oysters that are sold both domestically

and internationally. It has expanded both geographically and also in terms of infrastructure.

1. Equity Section

The Equity section of Alterra Limited includes Issued Capital, Reserves and Retained

Earnings. Reserves include share-based payment reserve, revaluation reserve, foreign

currency translation reserve (Alteraa Limited, 2018).

The Equity section of Angel Seafood Holdings Limited includes Issued Capital, Reserves and

Retained Earnings (Accumulated Losses).

2. Equity Section – Movements

The movements in the Equity section have been tabulated below:

(in $)

Equity 30 Sep, 2018 30 Sep, 2017 30 Sep, 2016

Issued Capital 14,254,212 14,254,212 13,984,212

Reserves 1,368,285 1,542,582 1,321,433

Retained

Earnings (4,449,011) (4,791,123) (2,752,422)

Total 11,173,486 11,005,671 12,553,223

The Issued Share capital represents fully paid ordinary shares. In 2017, a new share issue

had been made thus adding up to the existing numbers. While the share based payments

reserves has increased, revaluation reserve has decreased and foreign currency translation

reserve has been written back. The changes in revaluation reserves are due to the

movements in the valuation of the listed securities and the movements in the foreign currency

translation reserve is due to the exchange differences arising on the translation of a foreign

subsidiary (Alteraa Limited, 2018). Retained earnings represent the accumulated losses over

the years.

Angel Seafoods Holdings Limited was incorporated on 27 September 2016 and so the data is

tabulated as below:

4

Introduction

Alterra Limited is a company within the industrial sector. It has a focus of tapping the

investments to make a positive impact on society. It is into developing investment-grade

agricultural assets and also the maintenance of the same. It is well known for its carbon forest

sink and is a leading services provider engaged in activities relating to the establishment and

management of carbon-based abatement projects in Australia and New Zealand. Its recent

diversification is into the dairy market (Alteraa Limited, 2018).

Angel Seafood Holdings Limited is an aquaculture company based out if Australia. It focuses

on providing organic, clean, sustainable and green oysters that are sold both domestically

and internationally. It has expanded both geographically and also in terms of infrastructure.

1. Equity Section

The Equity section of Alterra Limited includes Issued Capital, Reserves and Retained

Earnings. Reserves include share-based payment reserve, revaluation reserve, foreign

currency translation reserve (Alteraa Limited, 2018).

The Equity section of Angel Seafood Holdings Limited includes Issued Capital, Reserves and

Retained Earnings (Accumulated Losses).

2. Equity Section – Movements

The movements in the Equity section have been tabulated below:

(in $)

Equity 30 Sep, 2018 30 Sep, 2017 30 Sep, 2016

Issued Capital 14,254,212 14,254,212 13,984,212

Reserves 1,368,285 1,542,582 1,321,433

Retained

Earnings (4,449,011) (4,791,123) (2,752,422)

Total 11,173,486 11,005,671 12,553,223

The Issued Share capital represents fully paid ordinary shares. In 2017, a new share issue

had been made thus adding up to the existing numbers. While the share based payments

reserves has increased, revaluation reserve has decreased and foreign currency translation

reserve has been written back. The changes in revaluation reserves are due to the

movements in the valuation of the listed securities and the movements in the foreign currency

translation reserve is due to the exchange differences arising on the translation of a foreign

subsidiary (Alteraa Limited, 2018). Retained earnings represent the accumulated losses over

the years.

Angel Seafoods Holdings Limited was incorporated on 27 September 2016 and so the data is

tabulated as below:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alteraa vs. Angel

(in $)

Equity 2018 2017

Issued Capital

14,007,06

1 6,300,973

Reserves 721,726 (432,000)

Retained

Earnings

(3,610,148

)

(1,667,519

)

Total

11,118,63

9 4,201,454

Issued capital refers to the ordinary equity shares. During the year the company has been

able to conduct a successful IPO due to which the share capital has increased in 2018.

Reserves include share-based payments reserve and common control reserve. Share-based

payments reserve has increased in 2018 due to transfers into the reserve by the exercise of

the vesting rights. The balance in common control reserve posted to accumulated losses and

thus this reserve in closed down in 2018. The company has acquired Halman Family Trust

and posting to common control reserve represents the consideration excess over the net

acquisition of assets. Due to the transaction ‘Debt for Equity swap’, the balance in this reserve

is transferred to accumulated losses. Accumulated losses are not just the current year losses

but also such transfers and adjustments (Angel Seafood, 2018).

3. Liabilities Section

The liabilities section comprises of current liabilities and non-current liabilities. Current

liabilities represent those that are repayable within a year or less like trade and other

payables, interest-bearing liabilities and provision for income tax (Bodie, Z., Kane & Marcus,

2014). Non-current liabilities represent those that are repayable after a year and include

interest-bearing liabilities, deferred tax liabilities and provisions (Alteraa Limited, 2018). The

liabilities section of Angel Seafoods is also similarly segregated into current and noncurrent

liabilities. Current liabilities comprises of trade and other payables, borrowings and employee

benefits whereas the noncurrent liabilities contains trade and other payables, borrowings,

deferred tax liabilities, and employee benefits (Angel Seafood, 2018).

4. Liabilities Section – Movements

The movements in the liabilities section of Alterra Limited have been tabulated below:

(in $)

Current Liabilities 30 Sep, 2018 30 Sep, 2017 30 Sep, 2016

Trade and Other Payables 191,816 204,609 160,605

Interest-bearing liabilities - 40,530 42,888

Provision for Income tax 124,596 - -

Total Current Liabilities 316,412 245,139 203,493

Non-Current Liabilities

Interest-bearing liabilities 1,750,000 1,790,552 81,083

5

(in $)

Equity 2018 2017

Issued Capital

14,007,06

1 6,300,973

Reserves 721,726 (432,000)

Retained

Earnings

(3,610,148

)

(1,667,519

)

Total

11,118,63

9 4,201,454

Issued capital refers to the ordinary equity shares. During the year the company has been

able to conduct a successful IPO due to which the share capital has increased in 2018.

Reserves include share-based payments reserve and common control reserve. Share-based

payments reserve has increased in 2018 due to transfers into the reserve by the exercise of

the vesting rights. The balance in common control reserve posted to accumulated losses and

thus this reserve in closed down in 2018. The company has acquired Halman Family Trust

and posting to common control reserve represents the consideration excess over the net

acquisition of assets. Due to the transaction ‘Debt for Equity swap’, the balance in this reserve

is transferred to accumulated losses. Accumulated losses are not just the current year losses

but also such transfers and adjustments (Angel Seafood, 2018).

3. Liabilities Section

The liabilities section comprises of current liabilities and non-current liabilities. Current

liabilities represent those that are repayable within a year or less like trade and other

payables, interest-bearing liabilities and provision for income tax (Bodie, Z., Kane & Marcus,

2014). Non-current liabilities represent those that are repayable after a year and include

interest-bearing liabilities, deferred tax liabilities and provisions (Alteraa Limited, 2018). The

liabilities section of Angel Seafoods is also similarly segregated into current and noncurrent

liabilities. Current liabilities comprises of trade and other payables, borrowings and employee

benefits whereas the noncurrent liabilities contains trade and other payables, borrowings,

deferred tax liabilities, and employee benefits (Angel Seafood, 2018).

4. Liabilities Section – Movements

The movements in the liabilities section of Alterra Limited have been tabulated below:

(in $)

Current Liabilities 30 Sep, 2018 30 Sep, 2017 30 Sep, 2016

Trade and Other Payables 191,816 204,609 160,605

Interest-bearing liabilities - 40,530 42,888

Provision for Income tax 124,596 - -

Total Current Liabilities 316,412 245,139 203,493

Non-Current Liabilities

Interest-bearing liabilities 1,750,000 1,790,552 81,083

5

Alteraa vs. Angel

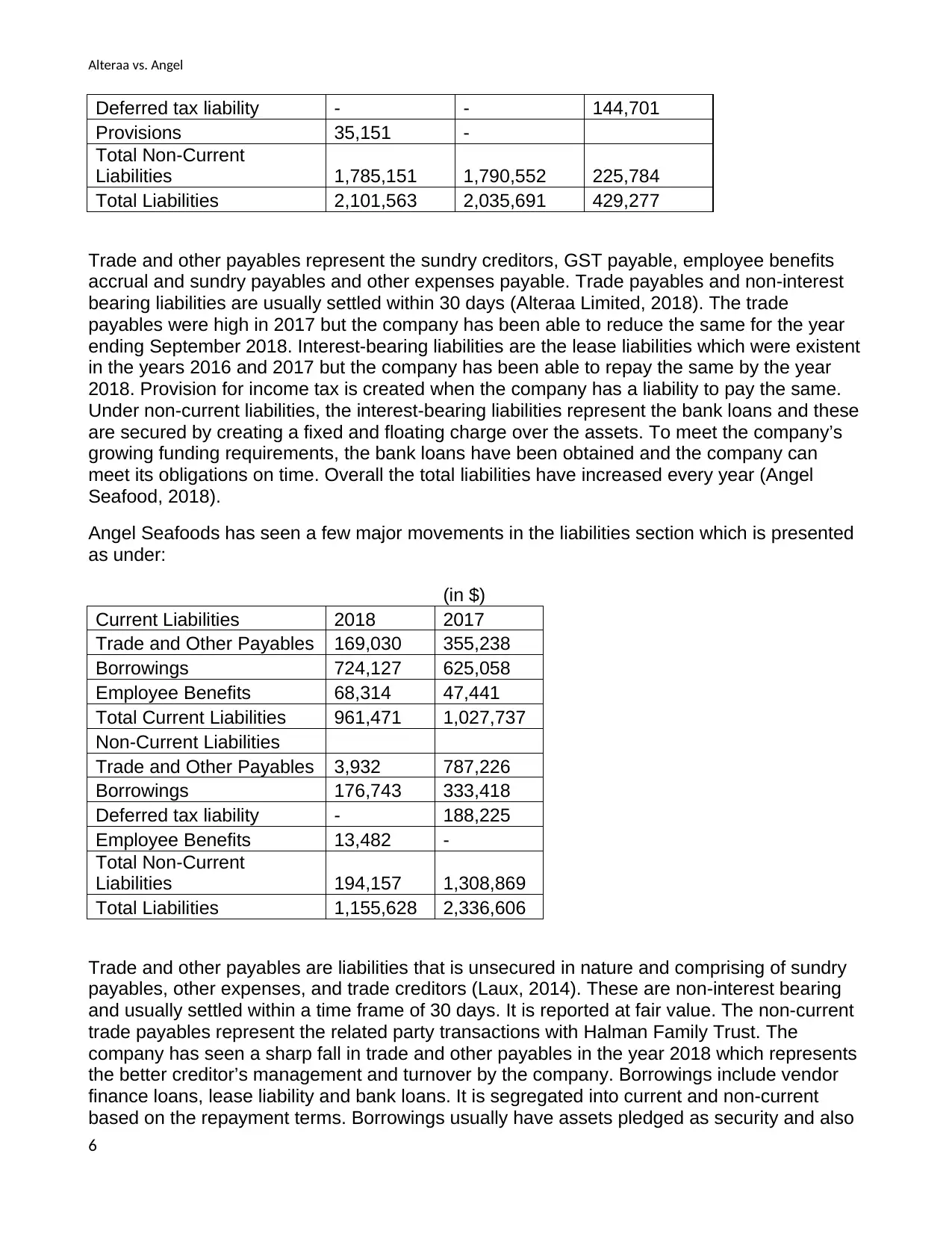

Deferred tax liability - - 144,701

Provisions 35,151 -

Total Non-Current

Liabilities 1,785,151 1,790,552 225,784

Total Liabilities 2,101,563 2,035,691 429,277

Trade and other payables represent the sundry creditors, GST payable, employee benefits

accrual and sundry payables and other expenses payable. Trade payables and non-interest

bearing liabilities are usually settled within 30 days (Alteraa Limited, 2018). The trade

payables were high in 2017 but the company has been able to reduce the same for the year

ending September 2018. Interest-bearing liabilities are the lease liabilities which were existent

in the years 2016 and 2017 but the company has been able to repay the same by the year

2018. Provision for income tax is created when the company has a liability to pay the same.

Under non-current liabilities, the interest-bearing liabilities represent the bank loans and these

are secured by creating a fixed and floating charge over the assets. To meet the company’s

growing funding requirements, the bank loans have been obtained and the company can

meet its obligations on time. Overall the total liabilities have increased every year (Angel

Seafood, 2018).

Angel Seafoods has seen a few major movements in the liabilities section which is presented

as under:

(in $)

Current Liabilities 2018 2017

Trade and Other Payables 169,030 355,238

Borrowings 724,127 625,058

Employee Benefits 68,314 47,441

Total Current Liabilities 961,471 1,027,737

Non-Current Liabilities

Trade and Other Payables 3,932 787,226

Borrowings 176,743 333,418

Deferred tax liability - 188,225

Employee Benefits 13,482 -

Total Non-Current

Liabilities 194,157 1,308,869

Total Liabilities 1,155,628 2,336,606

Trade and other payables are liabilities that is unsecured in nature and comprising of sundry

payables, other expenses, and trade creditors (Laux, 2014). These are non-interest bearing

and usually settled within a time frame of 30 days. It is reported at fair value. The non-current

trade payables represent the related party transactions with Halman Family Trust. The

company has seen a sharp fall in trade and other payables in the year 2018 which represents

the better creditor’s management and turnover by the company. Borrowings include vendor

finance loans, lease liability and bank loans. It is segregated into current and non-current

based on the repayment terms. Borrowings usually have assets pledged as security and also

6

Deferred tax liability - - 144,701

Provisions 35,151 -

Total Non-Current

Liabilities 1,785,151 1,790,552 225,784

Total Liabilities 2,101,563 2,035,691 429,277

Trade and other payables represent the sundry creditors, GST payable, employee benefits

accrual and sundry payables and other expenses payable. Trade payables and non-interest

bearing liabilities are usually settled within 30 days (Alteraa Limited, 2018). The trade

payables were high in 2017 but the company has been able to reduce the same for the year

ending September 2018. Interest-bearing liabilities are the lease liabilities which were existent

in the years 2016 and 2017 but the company has been able to repay the same by the year

2018. Provision for income tax is created when the company has a liability to pay the same.

Under non-current liabilities, the interest-bearing liabilities represent the bank loans and these

are secured by creating a fixed and floating charge over the assets. To meet the company’s

growing funding requirements, the bank loans have been obtained and the company can

meet its obligations on time. Overall the total liabilities have increased every year (Angel

Seafood, 2018).

Angel Seafoods has seen a few major movements in the liabilities section which is presented

as under:

(in $)

Current Liabilities 2018 2017

Trade and Other Payables 169,030 355,238

Borrowings 724,127 625,058

Employee Benefits 68,314 47,441

Total Current Liabilities 961,471 1,027,737

Non-Current Liabilities

Trade and Other Payables 3,932 787,226

Borrowings 176,743 333,418

Deferred tax liability - 188,225

Employee Benefits 13,482 -

Total Non-Current

Liabilities 194,157 1,308,869

Total Liabilities 1,155,628 2,336,606

Trade and other payables are liabilities that is unsecured in nature and comprising of sundry

payables, other expenses, and trade creditors (Laux, 2014). These are non-interest bearing

and usually settled within a time frame of 30 days. It is reported at fair value. The non-current

trade payables represent the related party transactions with Halman Family Trust. The

company has seen a sharp fall in trade and other payables in the year 2018 which represents

the better creditor’s management and turnover by the company. Borrowings include vendor

finance loans, lease liability and bank loans. It is segregated into current and non-current

based on the repayment terms. Borrowings usually have assets pledged as security and also

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Alteraa vs. Angel

have collateral provided (Ross et. al, 2014). The security of Lease liabilities are done by the

leased assets that are related and the other liabilities have non-current assets like land and

buildings, oyster leases, biological assets and leased plant and equipment pledged as

security (Brigham & Daves, 2012). Employee benefits are classified into current and non-

current. A current liability is a provision for annual leave and non-current liability is provided

for long service leave. The company has been able to efficiently reduce its total liabilities in a

year’s time frame which signifies the financial strong health of the company (Subramanyam &

Wild, 2014).

5. Comparison of the sources of funds

Alterra Limited is a company which is funded to a major extent by the equity share capital and

the proportion of debt is relatively low (Alteraa Limited, 2018). Thus it is a self-sufficient

company with not much third party obligations. Angel Seafoods is also on a similar track. A

majority of the company’s assets and investments have been supported by the equity share

capital. Loans and liabilities are to a limited extent which represents the financial strength of

the company (Angel Seafood, 2018).

7

have collateral provided (Ross et. al, 2014). The security of Lease liabilities are done by the

leased assets that are related and the other liabilities have non-current assets like land and

buildings, oyster leases, biological assets and leased plant and equipment pledged as

security (Brigham & Daves, 2012). Employee benefits are classified into current and non-

current. A current liability is a provision for annual leave and non-current liability is provided

for long service leave. The company has been able to efficiently reduce its total liabilities in a

year’s time frame which signifies the financial strong health of the company (Subramanyam &

Wild, 2014).

5. Comparison of the sources of funds

Alterra Limited is a company which is funded to a major extent by the equity share capital and

the proportion of debt is relatively low (Alteraa Limited, 2018). Thus it is a self-sufficient

company with not much third party obligations. Angel Seafoods is also on a similar track. A

majority of the company’s assets and investments have been supported by the equity share

capital. Loans and liabilities are to a limited extent which represents the financial strength of

the company (Angel Seafood, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alteraa vs. Angel

Part B

Critical examination of small proprietary company, large proprietary company and

reporting entity

Proprietary Companies

Not all companies provide options to the outsiders for investing in its share capital. A

proprietary concern is a fine example of such type of company. A proprietary establishment is

a private company that chooses not to go public. This type of establishment does not seek for

investment in its share capital from the public. A proprietary concern may or may not be

limited by shares (Leo, 2011). This means it can also be unlimited by shares. A proprietary

concern must have at least one shareholder and not more than fifty shareholders. The

shareholders of the proprietary concern must not be employed as personnel in the same.

Having a registered office is also compulsory for a proprietary concern. It must have at least

one director and may or may not appoint a company secretary (Lister, 2018).

The liability of equity holders is limited to their contribution in the share capital of the

proprietary concern which is limited by share capital. The liability of equity holders is unlimited

in a proprietary concern which is not limited by shares (ASIC, 2019).

Small Proprietary

A proprietary concern can be either large or small. A proprietary establishment must

necessarily qualify at least two requirements to be deemed as a small proprietary. The first

criteria being that a proprietary concern must not have more than 50 employees during the

time of the financial year ending. The second criteria being that the value of assets must not

exceed $12.5 million during the financial year ending. The last criteria being that during the

financial year, the proprietary must not have earned gross operating profits higher than 25

million dollars (Madura & Fox, 2011). As stated earlier, if a proprietary meets either of the two

requirements then the same shall be recognized as a small proprietary.

Large proprietary

A proprietary establishment must necessarily meet any of the two requirements to be deemed

as a large proprietary. The first criteria being that during the financial year-end, the

consolidated revenues earned by a proprietary and its subsidiaries must be a minimum of $50

million (Horngren, 2013). The second criteria being that during the financial year-end, the

gross value of consolidated tangible and intangible assets must not be less than $25 million.

The last criteria being that the number of employees working in the proprietary concern must

be 100 at least.

Reporting entity

A reporting entity can be defined as an entity where the public is dependent on its general

purpose financial report (GPFR) to determine its actual financial state of well being. The

financial reports are of great utility for various kinds of readers (Lister, 2018). These readers

can be potential investors, stakeholders, equity holders, lenders, creditors, suppliers,

debenture holders, employees, etc. The financial report of a company allows the users to

determine its financial well being and therefore, they can make appropriate decisions about

investment in the same. An entity where the users are not dependent on its general purpose

8

Part B

Critical examination of small proprietary company, large proprietary company and

reporting entity

Proprietary Companies

Not all companies provide options to the outsiders for investing in its share capital. A

proprietary concern is a fine example of such type of company. A proprietary establishment is

a private company that chooses not to go public. This type of establishment does not seek for

investment in its share capital from the public. A proprietary concern may or may not be

limited by shares (Leo, 2011). This means it can also be unlimited by shares. A proprietary

concern must have at least one shareholder and not more than fifty shareholders. The

shareholders of the proprietary concern must not be employed as personnel in the same.

Having a registered office is also compulsory for a proprietary concern. It must have at least

one director and may or may not appoint a company secretary (Lister, 2018).

The liability of equity holders is limited to their contribution in the share capital of the

proprietary concern which is limited by share capital. The liability of equity holders is unlimited

in a proprietary concern which is not limited by shares (ASIC, 2019).

Small Proprietary

A proprietary concern can be either large or small. A proprietary establishment must

necessarily qualify at least two requirements to be deemed as a small proprietary. The first

criteria being that a proprietary concern must not have more than 50 employees during the

time of the financial year ending. The second criteria being that the value of assets must not

exceed $12.5 million during the financial year ending. The last criteria being that during the

financial year, the proprietary must not have earned gross operating profits higher than 25

million dollars (Madura & Fox, 2011). As stated earlier, if a proprietary meets either of the two

requirements then the same shall be recognized as a small proprietary.

Large proprietary

A proprietary establishment must necessarily meet any of the two requirements to be deemed

as a large proprietary. The first criteria being that during the financial year-end, the

consolidated revenues earned by a proprietary and its subsidiaries must be a minimum of $50

million (Horngren, 2013). The second criteria being that during the financial year-end, the

gross value of consolidated tangible and intangible assets must not be less than $25 million.

The last criteria being that the number of employees working in the proprietary concern must

be 100 at least.

Reporting entity

A reporting entity can be defined as an entity where the public is dependent on its general

purpose financial report (GPFR) to determine its actual financial state of well being. The

financial reports are of great utility for various kinds of readers (Lister, 2018). These readers

can be potential investors, stakeholders, equity holders, lenders, creditors, suppliers,

debenture holders, employees, etc. The financial report of a company allows the users to

determine its financial well being and therefore, they can make appropriate decisions about

investment in the same. An entity where the users are not dependent on its general purpose

8

Alteraa vs. Angel

financial report is a nonreporting entity (Julia & Elizabeth, 2010). Such an entity makes an

SPFR (special purpose financial report) for its readers instead of GPFR.

Implications and Compliance of Large proprietary

Compliance is necessary for all companies. A proprietary company too must ensure that there

is full compliance with the Corporations Act, 2001. There must be a minimum of at least one

director who is an ordinary Australian resident in a proprietary concern. The directors of the

company must deliver his roles and responsibilities in full adherence with the statutory

requirements. It must be ensured that the financial accounts of the proprietary concern are

timely audited. Large proprietary concerns must have both financial and directors’ report

prepared and presented every F.Y. end.

The level of disclosures which is made to the (ASIC) depends on the size and type of an

entity. A public company has to raise funds from the public and for this purpose, it has to

allow its financial reports to be accessed by various groups of investors. This is why the level

of disclosures in the case of a public company is way higher as compared to a proprietary

company.

The large proprietary companies must submit its financial reports, directors’ report and

audited accounts to ASIC unless it contains an exception. Small proprietorships are mostly

exempted from submitting its financial reports, directors’ report and audited accounts to ASIC.

Large proprietorships are controlled by directors and owned by shareholders. This denotes

that the shareholders and directors are designated with different roles and responsibilities.

Shareholders are entitled to dividends on the gross profits earned by a proprietary while the

directors receive salaries (ASIC, 2019). A director may not have an interest in the shares of

the proprietary and the shareholder may not take part in regular operations of the proprietary.

Nobody has the right to claim the revenues earned by the proprietary for it entirely belongs to

the same.

For large proprietary companies, financial reports and directors’ report must be prepared and

audited before its submission to ASIC. For small proprietary companies, the financial

statements must be prepared and submitted to ATO.

9

financial report is a nonreporting entity (Julia & Elizabeth, 2010). Such an entity makes an

SPFR (special purpose financial report) for its readers instead of GPFR.

Implications and Compliance of Large proprietary

Compliance is necessary for all companies. A proprietary company too must ensure that there

is full compliance with the Corporations Act, 2001. There must be a minimum of at least one

director who is an ordinary Australian resident in a proprietary concern. The directors of the

company must deliver his roles and responsibilities in full adherence with the statutory

requirements. It must be ensured that the financial accounts of the proprietary concern are

timely audited. Large proprietary concerns must have both financial and directors’ report

prepared and presented every F.Y. end.

The level of disclosures which is made to the (ASIC) depends on the size and type of an

entity. A public company has to raise funds from the public and for this purpose, it has to

allow its financial reports to be accessed by various groups of investors. This is why the level

of disclosures in the case of a public company is way higher as compared to a proprietary

company.

The large proprietary companies must submit its financial reports, directors’ report and

audited accounts to ASIC unless it contains an exception. Small proprietorships are mostly

exempted from submitting its financial reports, directors’ report and audited accounts to ASIC.

Large proprietorships are controlled by directors and owned by shareholders. This denotes

that the shareholders and directors are designated with different roles and responsibilities.

Shareholders are entitled to dividends on the gross profits earned by a proprietary while the

directors receive salaries (ASIC, 2019). A director may not have an interest in the shares of

the proprietary and the shareholder may not take part in regular operations of the proprietary.

Nobody has the right to claim the revenues earned by the proprietary for it entirely belongs to

the same.

For large proprietary companies, financial reports and directors’ report must be prepared and

audited before its submission to ASIC. For small proprietary companies, the financial

statements must be prepared and submitted to ATO.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Alteraa vs. Angel

Conclusion

Alterra Limited has become a market leader in reforestation and in management of carbon

offset generating projects. Thus in the light of the current market conditions, its future can be

deemed to be bright. In case if Angel Seafoods, as a newly incorporated company, its

performance has been pretty good and the future also looks bright as per the forward-looking

statements of the company. Further from the report it becomes imperative that the level of

disclosures which is made to the ASIC depends on the size and type of an entity.

10

Conclusion

Alterra Limited has become a market leader in reforestation and in management of carbon

offset generating projects. Thus in the light of the current market conditions, its future can be

deemed to be bright. In case if Angel Seafoods, as a newly incorporated company, its

performance has been pretty good and the future also looks bright as per the forward-looking

statements of the company. Further from the report it becomes imperative that the level of

disclosures which is made to the ASIC depends on the size and type of an entity.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alteraa vs. Angel

References

Alteraa Limited 2018, Alteraa Limited 2018 annual report & accounts, viewed 26 September

2019, https://alterra.com.au/wp-content/uploads/2019/01/1AG_Annual_Report_2018_-

_FINAL_-_20181221.pdf

Angel Seafood 2018, Angel Seafood 2018 annual report & accounts, viewed 26 September

2019, https://angelseafood.com.au/wp-content/uploads/2018/10/Angel-Seafood_2018-

Annual-Report.pdf

ASIC 2019, Using 'Limited', 'No Liability' or 'Proprietary' in a name, viewed 26 September

2019, https://asic.gov.au/about-asic/contact-us/how-to-complain/using-limited-no-liability-or-

proprietary-in-a-name/

Bodie, Z., Kane, A. and Marcus, A. J 2014, Investments, McGraw Hill

Brigham, E. & Daves, P 2012, Intermediate Financial Management, USA: Cengage Learning.

Horngren, C 2013, Financial accounting, Frenchs Forest, N.S.W: Pearson Australia Group.

Julia, S.K & Elizabeth C. R 2010, Conflict Between Doing Well And Doing Good? Capital

Budgeting Case Study – Coors. Journal of Business Case Studies, vol. 6, no.6, p. 123-130

Laux, B 2014, Discussion of The role of revenue recognition in performance reporting.

Accounting and Business Research. 44(4), 380-382 viewed on 26 September 2019

<https://doi.org/10.1080/00014788.2014.897867>

Leo, K. J 2011, Company Accounting (9th ed), Boston:McGraw Hill

Lister, J 2018, Advantages and Disadvantages of Financial Risks Within Companies.

Retrieved from: https://smallbusiness.chron.com/advantages-disadvantages-financial-risks-

within-companies-16048.html

Madura, R., & Fox, J 2011, International financial management, South Western

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B 2014,

Shah, P 2013, Financial Accounting, London: Oxford University Press

Subramanyam, K & Wild, J 2014, Financial Statement Analysis, McGraw Hill

11

References

Alteraa Limited 2018, Alteraa Limited 2018 annual report & accounts, viewed 26 September

2019, https://alterra.com.au/wp-content/uploads/2019/01/1AG_Annual_Report_2018_-

_FINAL_-_20181221.pdf

Angel Seafood 2018, Angel Seafood 2018 annual report & accounts, viewed 26 September

2019, https://angelseafood.com.au/wp-content/uploads/2018/10/Angel-Seafood_2018-

Annual-Report.pdf

ASIC 2019, Using 'Limited', 'No Liability' or 'Proprietary' in a name, viewed 26 September

2019, https://asic.gov.au/about-asic/contact-us/how-to-complain/using-limited-no-liability-or-

proprietary-in-a-name/

Bodie, Z., Kane, A. and Marcus, A. J 2014, Investments, McGraw Hill

Brigham, E. & Daves, P 2012, Intermediate Financial Management, USA: Cengage Learning.

Horngren, C 2013, Financial accounting, Frenchs Forest, N.S.W: Pearson Australia Group.

Julia, S.K & Elizabeth C. R 2010, Conflict Between Doing Well And Doing Good? Capital

Budgeting Case Study – Coors. Journal of Business Case Studies, vol. 6, no.6, p. 123-130

Laux, B 2014, Discussion of The role of revenue recognition in performance reporting.

Accounting and Business Research. 44(4), 380-382 viewed on 26 September 2019

<https://doi.org/10.1080/00014788.2014.897867>

Leo, K. J 2011, Company Accounting (9th ed), Boston:McGraw Hill

Lister, J 2018, Advantages and Disadvantages of Financial Risks Within Companies.

Retrieved from: https://smallbusiness.chron.com/advantages-disadvantages-financial-risks-

within-companies-16048.html

Madura, R., & Fox, J 2011, International financial management, South Western

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B 2014,

Shah, P 2013, Financial Accounting, London: Oxford University Press

Subramanyam, K & Wild, J 2014, Financial Statement Analysis, McGraw Hill

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.