Auditing, Ethics, and Financial Analysis Report: Altium Limited

VerifiedAdded on 2020/12/10

|10

|3239

|362

Report

AI Summary

This report provides an analysis of auditing and ethics principles as applied to Altium Limited, a software company. It begins by defining auditing and its importance in ensuring accurate financial reporting. The report then examines the concept of materiality and its application to Altium, including materiality levels for operating profit, total assets, net profit, and shareholders' equity. A financial analysis of Altium is presented, covering the years 2015 to 2018, with key financial ratios such as current ratio, acid test ratio, debtor days, creditor days, operating profit margin, net profit margin, return on assets, and return on capital employed. Trends and changes in these ratios are interpreted. Finally, the report analyzes Altium's cash flow statements, identifying the major sources of cash inflows and outflows from operating, investing, and financing activities, and outlining the primary cash receipts and payments. The report concludes with a discussion of financial statement assertions, including accuracy, completeness, existence, understandability, and valuation.

Auditing and Ethics Answers for

questions given

questions given

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................2

MAIN BODY ......................................................................................................................................3

SECTION 1 Materiality Concept for Altium Limited..........................................................................3

SECTION 2. Financial Analysis of Altium Limited........................................................................4

SECTION 3 Cash Flow study..........................................................................................................7

CONCLUSION....................................................................................................................................9

REFERENCES.....................................................................................................................................9

INTRODUCTION................................................................................................................................2

MAIN BODY ......................................................................................................................................3

SECTION 1 Materiality Concept for Altium Limited..........................................................................3

SECTION 2. Financial Analysis of Altium Limited........................................................................4

SECTION 3 Cash Flow study..........................................................................................................7

CONCLUSION....................................................................................................................................9

REFERENCES.....................................................................................................................................9

INTRODUCTION

The term Auditing is defined as a process of making detailed examination or observation of the

financial statements, accounts, reports or records related to any business organization or company.

Auditing process helps the stakeholders as well as investors of the company in seeking confidence

related to the preparation of accounting reports and statements by ensuring that they are accurate,

correct and reliable for making investment related decision. Auditor should always comply with

applicable rules and acts while conducting audit. Also, auditor should conduct its auditing function

in an ethical manner by complying with code of conduct. The present report is based on Auditing

and Ethics norms related to Altium Limited which is an American, Australian domiciled owned

public software company which is engaged in business of PC based electronics design software for

those engineers who design the printed circuit boards. Report will discuss about materiality concept

and its relevant application in auditing procedure. Also, the report will provide financial analysis of

the company for the period 2015 to 2018. On the basis of financial ratios of last 4 years, a

preliminary analytical review on the financial information will be provided. At last, the report will

streamline about the Statement of Cash Flows related to the Company determining area creating the

highest inflow as well as outflow of cash.

MAIN BODY

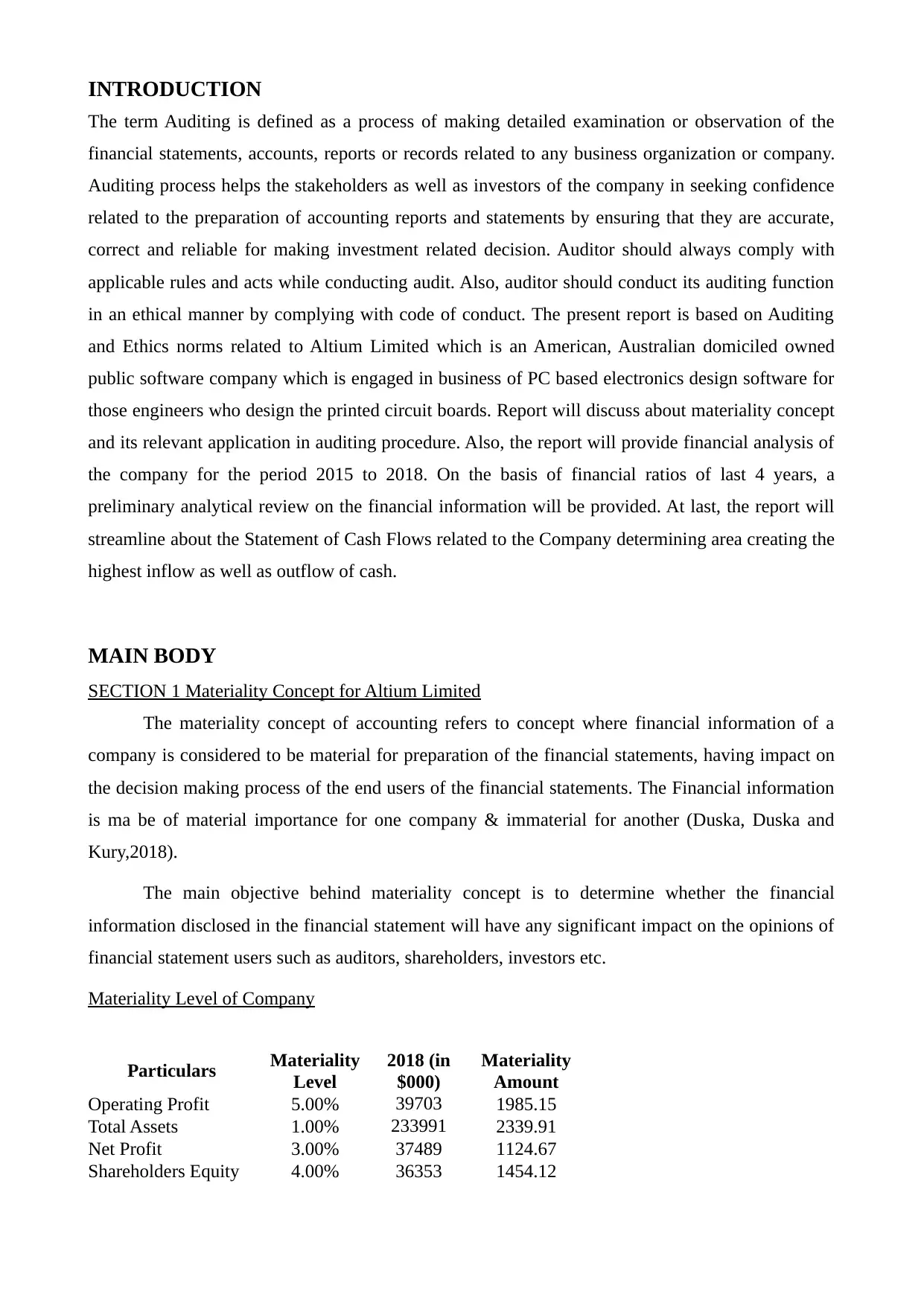

SECTION 1 Materiality Concept for Altium Limited

The materiality concept of accounting refers to concept where financial information of a

company is considered to be material for preparation of the financial statements, having impact on

the decision making process of the end users of the financial statements. The Financial information

is ma be of material importance for one company & immaterial for another (Duska, Duska and

Kury,2018).

The main objective behind materiality concept is to determine whether the financial

information disclosed in the financial statement will have any significant impact on the opinions of

financial statement users such as auditors, shareholders, investors etc.

Materiality Level of Company

Particulars Materiality

Level

2018 (in

$000)

Materiality

Amount

Operating Profit 5.00% 39703 1985.15

Total Assets 1.00% 233991 2339.91

Net Profit 3.00% 37489 1124.67

Shareholders Equity 4.00% 36353 1454.12

The term Auditing is defined as a process of making detailed examination or observation of the

financial statements, accounts, reports or records related to any business organization or company.

Auditing process helps the stakeholders as well as investors of the company in seeking confidence

related to the preparation of accounting reports and statements by ensuring that they are accurate,

correct and reliable for making investment related decision. Auditor should always comply with

applicable rules and acts while conducting audit. Also, auditor should conduct its auditing function

in an ethical manner by complying with code of conduct. The present report is based on Auditing

and Ethics norms related to Altium Limited which is an American, Australian domiciled owned

public software company which is engaged in business of PC based electronics design software for

those engineers who design the printed circuit boards. Report will discuss about materiality concept

and its relevant application in auditing procedure. Also, the report will provide financial analysis of

the company for the period 2015 to 2018. On the basis of financial ratios of last 4 years, a

preliminary analytical review on the financial information will be provided. At last, the report will

streamline about the Statement of Cash Flows related to the Company determining area creating the

highest inflow as well as outflow of cash.

MAIN BODY

SECTION 1 Materiality Concept for Altium Limited

The materiality concept of accounting refers to concept where financial information of a

company is considered to be material for preparation of the financial statements, having impact on

the decision making process of the end users of the financial statements. The Financial information

is ma be of material importance for one company & immaterial for another (Duska, Duska and

Kury,2018).

The main objective behind materiality concept is to determine whether the financial

information disclosed in the financial statement will have any significant impact on the opinions of

financial statement users such as auditors, shareholders, investors etc.

Materiality Level of Company

Particulars Materiality

Level

2018 (in

$000)

Materiality

Amount

Operating Profit 5.00% 39703 1985.15

Total Assets 1.00% 233991 2339.91

Net Profit 3.00% 37489 1124.67

Shareholders Equity 4.00% 36353 1454.12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to the Materiality concept,

1. Operating profit – The materiality level is 5% and the materiality amount is $1985.15,

which is considered as material and has to be disclose while preparing the financial

statement as it will help investor in assessing the financial position of the company.

2. Total Assets – The materiality amount for Company is $2339.91 which is of crucial nature

and disclosure has to be made about it in the financials, though the materiality level is only

1%.

2. Net profit – In case of net profit, investor can evaluate about the net amount of profit

available to them as profit, therefore it is required to be a part of financial statement.

3. Shareholders equity – With the help of shareholders equity, investors can determine the

amount of earning per share. So, it is required to have disclosure in financials of the

company.

SECTION 2. Financial Analysis of Altium Limited

Particulars 2015 (in $000) 2016 (in $000) 2017 (in $000) 2018 (in $000)

1. Current Ratio

Current Assets 84565 70093 79806 95429

Current Liabilities 41718 45703 57223 63692

Current Ratio = Current Assets/

Current Liabilities 2.03 1.53 1.39 1.50

2. Acid Test Ratio

Quick Asset 82365 67979 76904 91258

Current Liabilities 41718 45703 57223 63692

Acid Test Ratio = Current

Assets/ Current Liabilities 1.97 1.49 1.34 1.43

3.Debtor days

Trade Debtors 20459 29840 32631 38799

Revenue Sales 80535 93699 110957 140368

Debtor days = (Trade

Debtors/Revenue Sales) * 365 92.72 116.24 107.34 100.89

4. Creditor days

Trade Payables 5988 7137 10179 12147

Cost of Sales 80535 93699 110957 140368

Creditor days = (Trade

Payables/Cost of Sales)*365 27.14 27.80 33.48 31.59

5. Operating Profit Margin

Operating Profit 21587 24610 29472 39703

Total Revenue 80535 93699 110957 140368

1. Operating profit – The materiality level is 5% and the materiality amount is $1985.15,

which is considered as material and has to be disclose while preparing the financial

statement as it will help investor in assessing the financial position of the company.

2. Total Assets – The materiality amount for Company is $2339.91 which is of crucial nature

and disclosure has to be made about it in the financials, though the materiality level is only

1%.

2. Net profit – In case of net profit, investor can evaluate about the net amount of profit

available to them as profit, therefore it is required to be a part of financial statement.

3. Shareholders equity – With the help of shareholders equity, investors can determine the

amount of earning per share. So, it is required to have disclosure in financials of the

company.

SECTION 2. Financial Analysis of Altium Limited

Particulars 2015 (in $000) 2016 (in $000) 2017 (in $000) 2018 (in $000)

1. Current Ratio

Current Assets 84565 70093 79806 95429

Current Liabilities 41718 45703 57223 63692

Current Ratio = Current Assets/

Current Liabilities 2.03 1.53 1.39 1.50

2. Acid Test Ratio

Quick Asset 82365 67979 76904 91258

Current Liabilities 41718 45703 57223 63692

Acid Test Ratio = Current

Assets/ Current Liabilities 1.97 1.49 1.34 1.43

3.Debtor days

Trade Debtors 20459 29840 32631 38799

Revenue Sales 80535 93699 110957 140368

Debtor days = (Trade

Debtors/Revenue Sales) * 365 92.72 116.24 107.34 100.89

4. Creditor days

Trade Payables 5988 7137 10179 12147

Cost of Sales 80535 93699 110957 140368

Creditor days = (Trade

Payables/Cost of Sales)*365 27.14 27.80 33.48 31.59

5. Operating Profit Margin

Operating Profit 21587 24610 29472 39703

Total Revenue 80535 93699 110957 140368

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

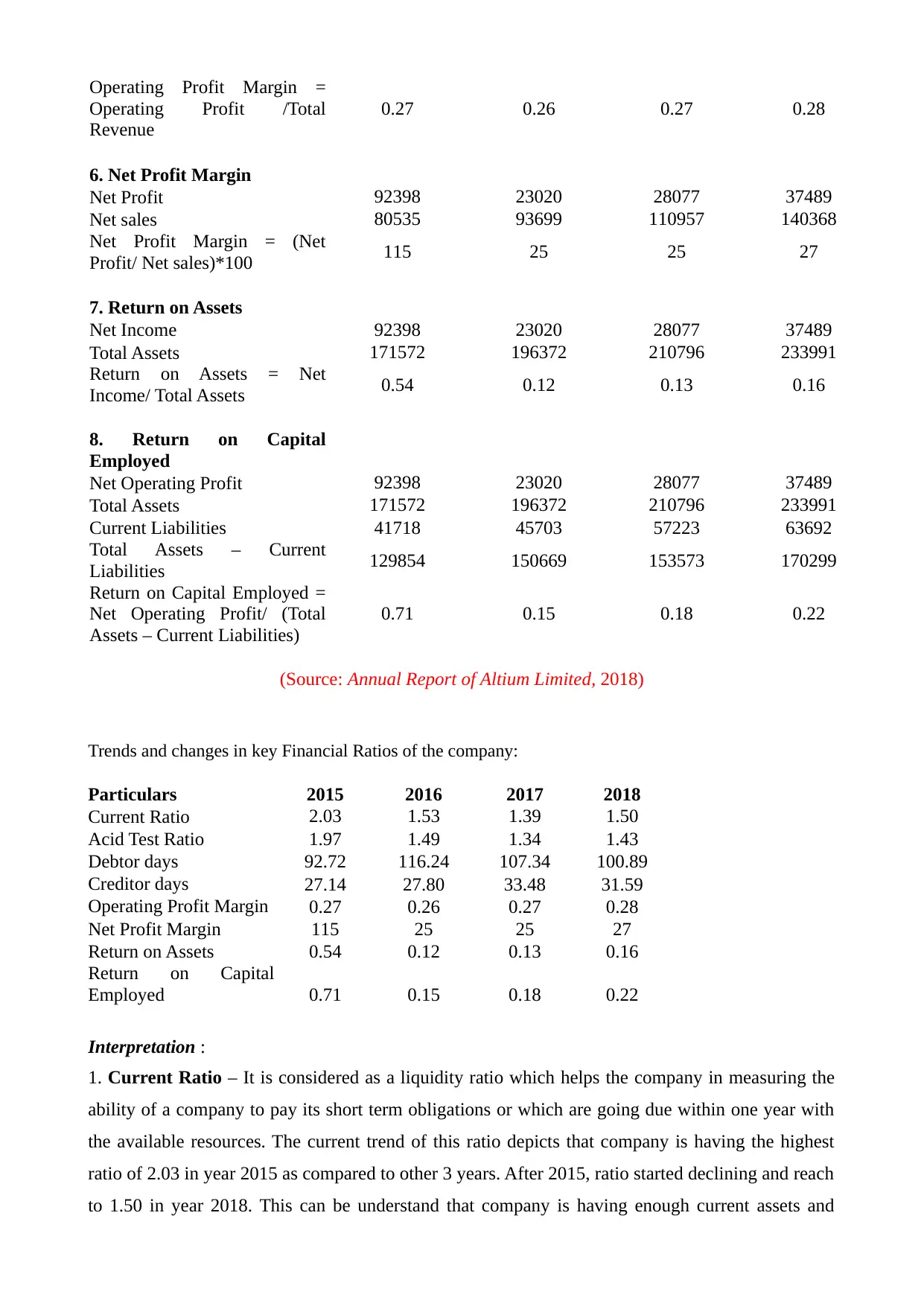

Operating Profit Margin =

Operating Profit /Total

Revenue

0.27 0.26 0.27 0.28

6. Net Profit Margin

Net Profit 92398 23020 28077 37489

Net sales 80535 93699 110957 140368

Net Profit Margin = (Net

Profit/ Net sales)*100 115 25 25 27

7. Return on Assets

Net Income 92398 23020 28077 37489

Total Assets 171572 196372 210796 233991

Return on Assets = Net

Income/ Total Assets 0.54 0.12 0.13 0.16

8. Return on Capital

Employed

Net Operating Profit 92398 23020 28077 37489

Total Assets 171572 196372 210796 233991

Current Liabilities 41718 45703 57223 63692

Total Assets – Current

Liabilities 129854 150669 153573 170299

Return on Capital Employed =

Net Operating Profit/ (Total

Assets – Current Liabilities)

0.71 0.15 0.18 0.22

(Source: Annual Report of Altium Limited, 2018)

Trends and changes in key Financial Ratios of the company:

Particulars 2015 2016 2017 2018

Current Ratio 2.03 1.53 1.39 1.50

Acid Test Ratio 1.97 1.49 1.34 1.43

Debtor days 92.72 116.24 107.34 100.89

Creditor days 27.14 27.80 33.48 31.59

Operating Profit Margin 0.27 0.26 0.27 0.28

Net Profit Margin 115 25 25 27

Return on Assets 0.54 0.12 0.13 0.16

Return on Capital

Employed 0.71 0.15 0.18 0.22

Interpretation :

1. Current Ratio – It is considered as a liquidity ratio which helps the company in measuring the

ability of a company to pay its short term obligations or which are going due within one year with

the available resources. The current trend of this ratio depicts that company is having the highest

ratio of 2.03 in year 2015 as compared to other 3 years. After 2015, ratio started declining and reach

to 1.50 in year 2018. This can be understand that company is having enough current assets and

Operating Profit /Total

Revenue

0.27 0.26 0.27 0.28

6. Net Profit Margin

Net Profit 92398 23020 28077 37489

Net sales 80535 93699 110957 140368

Net Profit Margin = (Net

Profit/ Net sales)*100 115 25 25 27

7. Return on Assets

Net Income 92398 23020 28077 37489

Total Assets 171572 196372 210796 233991

Return on Assets = Net

Income/ Total Assets 0.54 0.12 0.13 0.16

8. Return on Capital

Employed

Net Operating Profit 92398 23020 28077 37489

Total Assets 171572 196372 210796 233991

Current Liabilities 41718 45703 57223 63692

Total Assets – Current

Liabilities 129854 150669 153573 170299

Return on Capital Employed =

Net Operating Profit/ (Total

Assets – Current Liabilities)

0.71 0.15 0.18 0.22

(Source: Annual Report of Altium Limited, 2018)

Trends and changes in key Financial Ratios of the company:

Particulars 2015 2016 2017 2018

Current Ratio 2.03 1.53 1.39 1.50

Acid Test Ratio 1.97 1.49 1.34 1.43

Debtor days 92.72 116.24 107.34 100.89

Creditor days 27.14 27.80 33.48 31.59

Operating Profit Margin 0.27 0.26 0.27 0.28

Net Profit Margin 115 25 25 27

Return on Assets 0.54 0.12 0.13 0.16

Return on Capital

Employed 0.71 0.15 0.18 0.22

Interpretation :

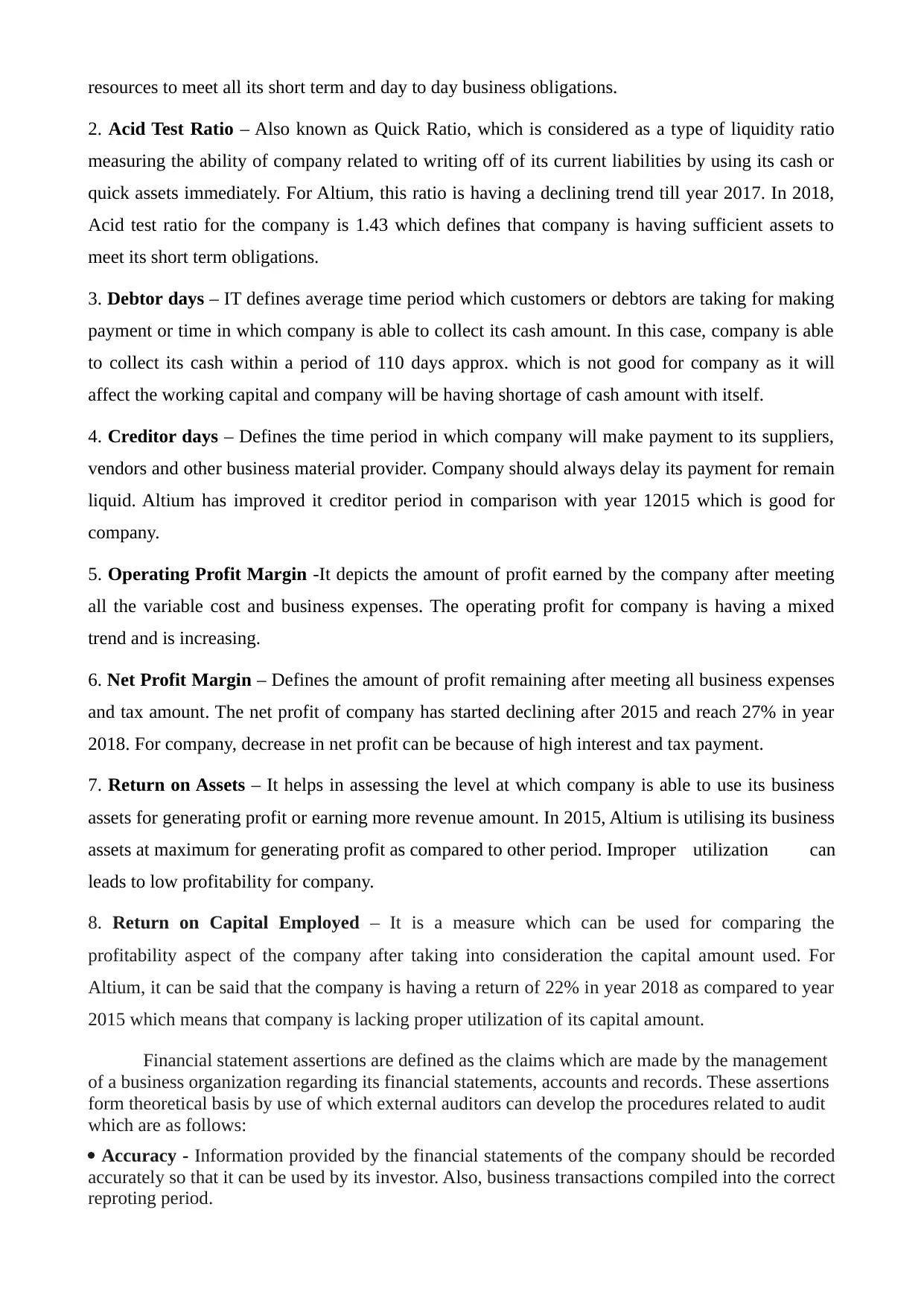

1. Current Ratio – It is considered as a liquidity ratio which helps the company in measuring the

ability of a company to pay its short term obligations or which are going due within one year with

the available resources. The current trend of this ratio depicts that company is having the highest

ratio of 2.03 in year 2015 as compared to other 3 years. After 2015, ratio started declining and reach

to 1.50 in year 2018. This can be understand that company is having enough current assets and

resources to meet all its short term and day to day business obligations.

2. Acid Test Ratio – Also known as Quick Ratio, which is considered as a type of liquidity ratio

measuring the ability of company related to writing off of its current liabilities by using its cash or

quick assets immediately. For Altium, this ratio is having a declining trend till year 2017. In 2018,

Acid test ratio for the company is 1.43 which defines that company is having sufficient assets to

meet its short term obligations.

3. Debtor days – IT defines average time period which customers or debtors are taking for making

payment or time in which company is able to collect its cash amount. In this case, company is able

to collect its cash within a period of 110 days approx. which is not good for company as it will

affect the working capital and company will be having shortage of cash amount with itself.

4. Creditor days – Defines the time period in which company will make payment to its suppliers,

vendors and other business material provider. Company should always delay its payment for remain

liquid. Altium has improved it creditor period in comparison with year 12015 which is good for

company.

5. Operating Profit Margin -It depicts the amount of profit earned by the company after meeting

all the variable cost and business expenses. The operating profit for company is having a mixed

trend and is increasing.

6. Net Profit Margin – Defines the amount of profit remaining after meeting all business expenses

and tax amount. The net profit of company has started declining after 2015 and reach 27% in year

2018. For company, decrease in net profit can be because of high interest and tax payment.

7. Return on Assets – It helps in assessing the level at which company is able to use its business

assets for generating profit or earning more revenue amount. In 2015, Altium is utilising its business

assets at maximum for generating profit as compared to other period. Improper utilization can

leads to low profitability for company.

8. Return on Capital Employed – It is a measure which can be used for comparing the

profitability aspect of the company after taking into consideration the capital amount used. For

Altium, it can be said that the company is having a return of 22% in year 2018 as compared to year

2015 which means that company is lacking proper utilization of its capital amount.

Financial statement assertions are defined as the claims which are made by the management

of a business organization regarding its financial statements, accounts and records. These assertions

form theoretical basis by use of which external auditors can develop the procedures related to audit

which are as follows:

Accuracy - Information provided by the financial statements of the company should be recorded

accurately so that it can be used by its investor. Also, business transactions compiled into the correct

reproting period.

2. Acid Test Ratio – Also known as Quick Ratio, which is considered as a type of liquidity ratio

measuring the ability of company related to writing off of its current liabilities by using its cash or

quick assets immediately. For Altium, this ratio is having a declining trend till year 2017. In 2018,

Acid test ratio for the company is 1.43 which defines that company is having sufficient assets to

meet its short term obligations.

3. Debtor days – IT defines average time period which customers or debtors are taking for making

payment or time in which company is able to collect its cash amount. In this case, company is able

to collect its cash within a period of 110 days approx. which is not good for company as it will

affect the working capital and company will be having shortage of cash amount with itself.

4. Creditor days – Defines the time period in which company will make payment to its suppliers,

vendors and other business material provider. Company should always delay its payment for remain

liquid. Altium has improved it creditor period in comparison with year 12015 which is good for

company.

5. Operating Profit Margin -It depicts the amount of profit earned by the company after meeting

all the variable cost and business expenses. The operating profit for company is having a mixed

trend and is increasing.

6. Net Profit Margin – Defines the amount of profit remaining after meeting all business expenses

and tax amount. The net profit of company has started declining after 2015 and reach 27% in year

2018. For company, decrease in net profit can be because of high interest and tax payment.

7. Return on Assets – It helps in assessing the level at which company is able to use its business

assets for generating profit or earning more revenue amount. In 2015, Altium is utilising its business

assets at maximum for generating profit as compared to other period. Improper utilization can

leads to low profitability for company.

8. Return on Capital Employed – It is a measure which can be used for comparing the

profitability aspect of the company after taking into consideration the capital amount used. For

Altium, it can be said that the company is having a return of 22% in year 2018 as compared to year

2015 which means that company is lacking proper utilization of its capital amount.

Financial statement assertions are defined as the claims which are made by the management

of a business organization regarding its financial statements, accounts and records. These assertions

form theoretical basis by use of which external auditors can develop the procedures related to audit

which are as follows:

Accuracy - Information provided by the financial statements of the company should be recorded

accurately so that it can be used by its investor. Also, business transactions compiled into the correct

reproting period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

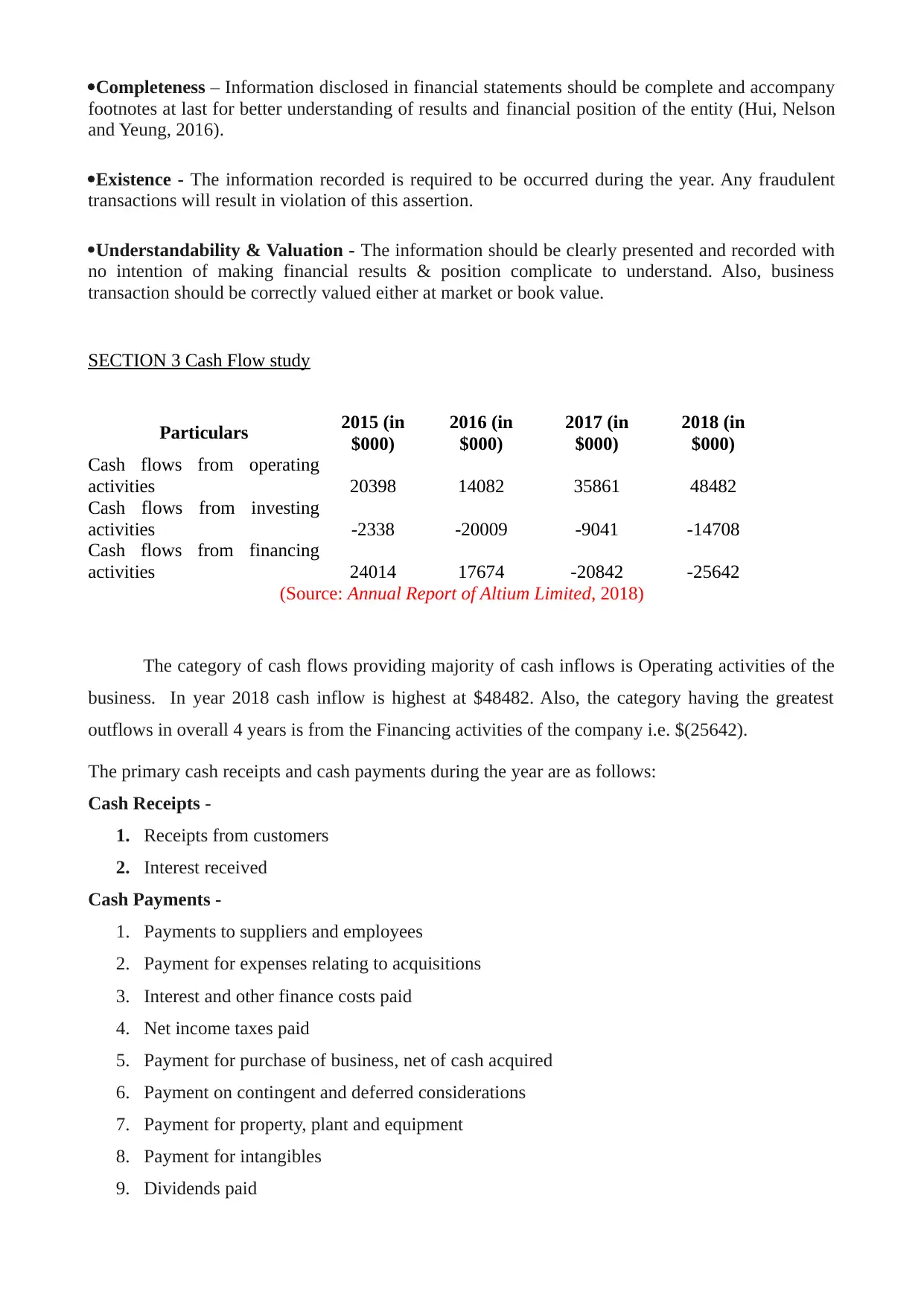

Completeness – Information disclosed in financial statements should be complete and accompany

footnotes at last for better understanding of results and financial position of the entity (Hui, Nelson

and Yeung, 2016).

Existence - The information recorded is required to be occurred during the year. Any fraudulent

transactions will result in violation of this assertion.

Understandability & Valuation - The information should be clearly presented and recorded with

no intention of making financial results & position complicate to understand. Also, business

transaction should be correctly valued either at market or book value.

SECTION 3 Cash Flow study

Particulars 2015 (in

$000)

2016 (in

$000)

2017 (in

$000)

2018 (in

$000)

Cash flows from operating

activities 20398 14082 35861 48482

Cash flows from investing

activities -2338 -20009 -9041 -14708

Cash flows from financing

activities 24014 17674 -20842 -25642

(Source: Annual Report of Altium Limited, 2018)

The category of cash flows providing majority of cash inflows is Operating activities of the

business. In year 2018 cash inflow is highest at $48482. Also, the category having the greatest

outflows in overall 4 years is from the Financing activities of the company i.e. $(25642).

The primary cash receipts and cash payments during the year are as follows:

Cash Receipts -

1. Receipts from customers

2. Interest received

Cash Payments -

1. Payments to suppliers and employees

2. Payment for expenses relating to acquisitions

3. Interest and other finance costs paid

4. Net income taxes paid

5. Payment for purchase of business, net of cash acquired

6. Payment on contingent and deferred considerations

7. Payment for property, plant and equipment

8. Payment for intangibles

9. Dividends paid

footnotes at last for better understanding of results and financial position of the entity (Hui, Nelson

and Yeung, 2016).

Existence - The information recorded is required to be occurred during the year. Any fraudulent

transactions will result in violation of this assertion.

Understandability & Valuation - The information should be clearly presented and recorded with

no intention of making financial results & position complicate to understand. Also, business

transaction should be correctly valued either at market or book value.

SECTION 3 Cash Flow study

Particulars 2015 (in

$000)

2016 (in

$000)

2017 (in

$000)

2018 (in

$000)

Cash flows from operating

activities 20398 14082 35861 48482

Cash flows from investing

activities -2338 -20009 -9041 -14708

Cash flows from financing

activities 24014 17674 -20842 -25642

(Source: Annual Report of Altium Limited, 2018)

The category of cash flows providing majority of cash inflows is Operating activities of the

business. In year 2018 cash inflow is highest at $48482. Also, the category having the greatest

outflows in overall 4 years is from the Financing activities of the company i.e. $(25642).

The primary cash receipts and cash payments during the year are as follows:

Cash Receipts -

1. Receipts from customers

2. Interest received

Cash Payments -

1. Payments to suppliers and employees

2. Payment for expenses relating to acquisitions

3. Interest and other finance costs paid

4. Net income taxes paid

5. Payment for purchase of business, net of cash acquired

6. Payment on contingent and deferred considerations

7. Payment for property, plant and equipment

8. Payment for intangibles

9. Dividends paid

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10. Repayment of borrowings

All the non cash transactions related to Investing and financing activities does not affect the

cash inflows or outflows of the company but takes into consideration only the equity of owners or

long term assets and liabilities of the company (Lewellen and Lewellen, 2016). It is mentioned at

the footnote of the cash flow statement. The main non cash financial and investing activities of the

business are as follows:

1. Depreciation and amortisation

2. Share based payments

3. Unrealised foreign exchange differences

The concept of Going concern defines that the company will carry own or continues its

business for longer period of time irrespective of its members. Company which is preparing its

financial statements on the going concern basis by taking assumption that they will continue their

business operations for the foreseeable future period. The assumption made by the company is

related to the fact that it does not have any intention of liquidating or winding up its business assets.

The Going concern risk means that business organisation will never be forced to halt its

business operations and/ or liquidate its business assets in near time period at the very low sale

prices. The Going concern risk for Altium Limited in this case is when the company has to conduct

its business operations by incurring a cash outflow of $(20009) in investing activity in the year

2016. With the help of following factors Going concern risk can be evaluated:

1. Negative trends such as decrease in sales level, increasing costs etc.

2. Internal matters such as work stoppages or other labour difficulties, inefficient accounting

system, inefficient accounting system etc.

3. External matters like legal proceedings, loss of principal customer or supplier, loss of

franchise, license or patent etc.

4. Other matters related to financial difficulties such as default on loan or similar agreements,

non compliance of statutory capital requirements etc.

Audit procedures for addressing the Going concern risk are as follows:

1. Analytical procedure of the company' business operations.

2. Making a review of occurring of all the Subsequent events such as Bankruptcy of major

customers, fall in the market price of inventory of company etc.

3. Reviewing the compliance made in respect of terms related to debt and loan agreements.

All the non cash transactions related to Investing and financing activities does not affect the

cash inflows or outflows of the company but takes into consideration only the equity of owners or

long term assets and liabilities of the company (Lewellen and Lewellen, 2016). It is mentioned at

the footnote of the cash flow statement. The main non cash financial and investing activities of the

business are as follows:

1. Depreciation and amortisation

2. Share based payments

3. Unrealised foreign exchange differences

The concept of Going concern defines that the company will carry own or continues its

business for longer period of time irrespective of its members. Company which is preparing its

financial statements on the going concern basis by taking assumption that they will continue their

business operations for the foreseeable future period. The assumption made by the company is

related to the fact that it does not have any intention of liquidating or winding up its business assets.

The Going concern risk means that business organisation will never be forced to halt its

business operations and/ or liquidate its business assets in near time period at the very low sale

prices. The Going concern risk for Altium Limited in this case is when the company has to conduct

its business operations by incurring a cash outflow of $(20009) in investing activity in the year

2016. With the help of following factors Going concern risk can be evaluated:

1. Negative trends such as decrease in sales level, increasing costs etc.

2. Internal matters such as work stoppages or other labour difficulties, inefficient accounting

system, inefficient accounting system etc.

3. External matters like legal proceedings, loss of principal customer or supplier, loss of

franchise, license or patent etc.

4. Other matters related to financial difficulties such as default on loan or similar agreements,

non compliance of statutory capital requirements etc.

Audit procedures for addressing the Going concern risk are as follows:

1. Analytical procedure of the company' business operations.

2. Making a review of occurring of all the Subsequent events such as Bankruptcy of major

customers, fall in the market price of inventory of company etc.

3. Reviewing the compliance made in respect of terms related to debt and loan agreements.

4. Having an overview of Minutes made of the meetings of the company (Baik and et.al.,

2016).

5. Responding to inquiry made by Legal counsel related to Litigation, claims, violations etc.

6. Seeking confirmation from the Related parties and third parties related to the financial

supports.

CONCLUSION

From the above report it can be concluded that for undertaking the auditing process, the

auditor should comply with all code of conducts and ethical norms. Also, it is the duty of auditor to

furnish accurate and correct financial information in the financial statements of the company so that

its investors and other stakeholders can make use of it in making decision related to the investment

options. The report has discussed that materiality concept is of very much importance for every

company in preparation of its financial statements and accounts, as all the material information has

to be disclosed in which are going to effect the decision making process of the investor. Further,

analytical review of the financial ratios form year 2015 to 2018 has been made for assessing the

trends. At last report has disclosed study made in context of the cash flow statement of Altium

Limited.

2016).

5. Responding to inquiry made by Legal counsel related to Litigation, claims, violations etc.

6. Seeking confirmation from the Related parties and third parties related to the financial

supports.

CONCLUSION

From the above report it can be concluded that for undertaking the auditing process, the

auditor should comply with all code of conducts and ethical norms. Also, it is the duty of auditor to

furnish accurate and correct financial information in the financial statements of the company so that

its investors and other stakeholders can make use of it in making decision related to the investment

options. The report has discussed that materiality concept is of very much importance for every

company in preparation of its financial statements and accounts, as all the material information has

to be disclosed in which are going to effect the decision making process of the investor. Further,

analytical review of the financial ratios form year 2015 to 2018 has been made for assessing the

trends. At last report has disclosed study made in context of the cash flow statement of Altium

Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Duska, R. F., Duska, B. S. and Kury, K. W., 2018. Accounting ethics. Wiley-Blackwell.

Helin, S. and Babri, M., 2015. Travelling with a code of ethics: a contextual study of a Swedish

MNC auditing a Chinese supplier. Journal of Cleaner Production.107. pp.41-53.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Routledge.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of Practice &

Theory. 35(3). pp.1-32.

Penman, S. H., 2015. Financial Ratios and Equity Valuation. Wiley Encyclopedia of Management.

pp.1-7.

Lakshan, A. I. and Wijekoon, W. M. H. N., 2017. The use of financial ratios in predicting corporate

failure in Sri Lanka. GSTF Journal on Business Review (GBR). 2(4).

Morales - Díaz, J. and Zamora - Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

a new methodological approach. Accounting in Europe. 15(1). pp.105-133.

Lukason, O., Laitinen, E. K. and Suvas, A., 2015. Growth patterns of small manufacturing firms

before failure: interconnections with financial ratios and nonfinancial variables. International

Journal of Industrial Engineering and Management. 6(2). pp.59-66.

Baik, B. and et.al., 2016. Who classifies interest payments as financing activities? An analysis of

classification shifting in the statement of cash flows at the adoption of IFRS. Journal of

Accounting and Public Policy. 35(4). pp.331-351.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal of Financial

and Quantitative Analysis. 51(4). pp.1135-1164.

Hui, K. W., Nelson, K. K. and Yeung, P. E., 2016. On the persistence and pricing of industry-wide

and firm-specific earnings, cash flows, and accruals. Journal of Accounting and Economics.

61(1). pp.185-202.

Online

Annual Report of Altium Limited. 2018. [Online]. Available through:

<http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_ALU_2016.pdf>.

Auditing of Small entities. 2017. [Online]. Available through:

<https://www.intheblack.com/articles/2017/03/16/live-chat-small-entities-audit-manual>.

Statement of cash flows. 2019. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/statement-of-cash-

flows/>.

Books and Journals

Duska, R. F., Duska, B. S. and Kury, K. W., 2018. Accounting ethics. Wiley-Blackwell.

Helin, S. and Babri, M., 2015. Travelling with a code of ethics: a contextual study of a Swedish

MNC auditing a Chinese supplier. Journal of Cleaner Production.107. pp.41-53.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk. Routledge.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of Practice &

Theory. 35(3). pp.1-32.

Penman, S. H., 2015. Financial Ratios and Equity Valuation. Wiley Encyclopedia of Management.

pp.1-7.

Lakshan, A. I. and Wijekoon, W. M. H. N., 2017. The use of financial ratios in predicting corporate

failure in Sri Lanka. GSTF Journal on Business Review (GBR). 2(4).

Morales - Díaz, J. and Zamora - Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

a new methodological approach. Accounting in Europe. 15(1). pp.105-133.

Lukason, O., Laitinen, E. K. and Suvas, A., 2015. Growth patterns of small manufacturing firms

before failure: interconnections with financial ratios and nonfinancial variables. International

Journal of Industrial Engineering and Management. 6(2). pp.59-66.

Baik, B. and et.al., 2016. Who classifies interest payments as financing activities? An analysis of

classification shifting in the statement of cash flows at the adoption of IFRS. Journal of

Accounting and Public Policy. 35(4). pp.331-351.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal of Financial

and Quantitative Analysis. 51(4). pp.1135-1164.

Hui, K. W., Nelson, K. K. and Yeung, P. E., 2016. On the persistence and pricing of industry-wide

and firm-specific earnings, cash flows, and accruals. Journal of Accounting and Economics.

61(1). pp.185-202.

Online

Annual Report of Altium Limited. 2018. [Online]. Available through:

<http://www.annualreports.com/HostedData/AnnualReportArchive/a/ASX_ALU_2016.pdf>.

Auditing of Small entities. 2017. [Online]. Available through:

<https://www.intheblack.com/articles/2017/03/16/live-chat-small-entities-audit-manual>.

Statement of cash flows. 2019. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/statement-of-cash-

flows/>.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.