Contemporary Accounting Issues: Alumina Limited Financial Analysis

VerifiedAdded on 2023/01/19

|11

|2027

|87

Report

AI Summary

This report examines the compliance of Alumina Limited with the International Accounting Standards Board (IASB) standards, focusing on the conceptual accounting framework (CF). It analyzes the company's financial reporting, including measurement criteria, qualitative characteristics (relevance and faithful representation), and enhancing qualitative characteristics (comparability, verifiability, timeliness, and understandability). The report evaluates the users of financial reports, the knowledge required by them, and how Alumina Limited meets the requirements of general-purpose financial reporting. The analysis references Alumina Limited's annual reports and relevant accounting standards, concluding that the company effectively complies with IFRS and the CF, thereby providing useful information for investors, lenders, and creditors in their decision-making processes. The report emphasizes the importance of understanding accounting principles for effective financial analysis and decision-making.

Contemporary Issues in Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report has been developed for examining the compliance of CF of accounting as per

the IASB standards of a selected case company, that is, Alumina Limited. In this context, it has

been inferred from evaluation of the financial report of the company that it has followed all the

qualitative principles and essential requirements of conceptual accounting framework.

2

This report has been developed for examining the compliance of CF of accounting as per

the IASB standards of a selected case company, that is, Alumina Limited. In this context, it has

been inferred from evaluation of the financial report of the company that it has followed all the

qualitative principles and essential requirements of conceptual accounting framework.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Critical Analysis of General Purpose Financial Reporting by Alumina Limited............................4

Part 1: Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements................................................................................................................4

Part 2: Fundamental Qualitative Characteristics of Conceptual Framework Applied by Alumina

Limited.............................................................................................................................................6

Part 3: Enhancing Qualitative Characteristics of Conceptual Framework Applied by Company...7

Part 4: Users of Financial Reports in Making Financial Decisions.................................................9

Part 5: Knowledge Required by End-Users for Analysis of Financial Reports............................10

Part 6: Requirements of general Purpose Financial Reporting met by the Company...................10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Critical Analysis of General Purpose Financial Reporting by Alumina Limited............................4

Part 1: Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements................................................................................................................4

Part 2: Fundamental Qualitative Characteristics of Conceptual Framework Applied by Alumina

Limited.............................................................................................................................................6

Part 3: Enhancing Qualitative Characteristics of Conceptual Framework Applied by Company...7

Part 4: Users of Financial Reports in Making Financial Decisions.................................................9

Part 5: Knowledge Required by End-Users for Analysis of Financial Reports............................10

Part 6: Requirements of general Purpose Financial Reporting met by the Company...................10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The IASB (International Accounting Standards Board) is placing large emphasis on

improving the quality of financial reporting by business entities for the sake of protecting the

interest of the investors. IASB has developed and established conceptual accounting framework

(CF) that has provided the essential qualitative principles that businesses complying with IASB

reporting standards need to follow for development of their financial reports. As such, this report

examines the extent of adoption of CF of accounting by an ASX listed company Alumina

Limited, involved in mining of bauxite and extraction of alumina.

Critical Analysis of General Purpose Financial Reporting by Alumina Limited

Part 1: Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements

Information is useful for users when it is comparable with other factors or companies and

understandable which is possible only when the accounting and financial reporting done by the

companies are prepared in the same way following same principles. However there are several

methods of accounting which are followed by companies in preparation of their financial

statements. To make this kind of practice consistent the Financial Accounting Standard Board

has given a defined set of rules and standard which has to be followed by reporting companies in

preparation of their financial statements (AASB Exposure Draft, 2015).

Conceptual Framework provides two measurement bases on which each financial item in

the financial statement of the reporting company is to be measured.

Historical Cost

Current Value

Historical cost is the cost which is incurred by the company during initial acquisition of

its assets and liabilities by taking into account any impairment or amortization that they have

undergone. This means that the measurement of a financial item on historical cost implies

measuring the amount spent to acquire the financial item less depreciation and any amortization

cost or any impairment. On the other hand, current value is the updated value of a financial item

at which two genuine persons are willing to buy or sell at current market price on reporting date.

Current value is further divided in to fair value, current cost and value in use. The entity has the

option to choose any of the measurement basis or more than one measurement basis for different

financial items reflecting in a financial statement.

The annual report of Alumina Limited shows that the fixed assets of Alumina Limited is

measured on historical cost basis which is tested for impairment and any needful changes have

4

The IASB (International Accounting Standards Board) is placing large emphasis on

improving the quality of financial reporting by business entities for the sake of protecting the

interest of the investors. IASB has developed and established conceptual accounting framework

(CF) that has provided the essential qualitative principles that businesses complying with IASB

reporting standards need to follow for development of their financial reports. As such, this report

examines the extent of adoption of CF of accounting by an ASX listed company Alumina

Limited, involved in mining of bauxite and extraction of alumina.

Critical Analysis of General Purpose Financial Reporting by Alumina Limited

Part 1: Measurement Criteria Adopted by the Company & its Compliance with Conceptual

Framework Requirements

Information is useful for users when it is comparable with other factors or companies and

understandable which is possible only when the accounting and financial reporting done by the

companies are prepared in the same way following same principles. However there are several

methods of accounting which are followed by companies in preparation of their financial

statements. To make this kind of practice consistent the Financial Accounting Standard Board

has given a defined set of rules and standard which has to be followed by reporting companies in

preparation of their financial statements (AASB Exposure Draft, 2015).

Conceptual Framework provides two measurement bases on which each financial item in

the financial statement of the reporting company is to be measured.

Historical Cost

Current Value

Historical cost is the cost which is incurred by the company during initial acquisition of

its assets and liabilities by taking into account any impairment or amortization that they have

undergone. This means that the measurement of a financial item on historical cost implies

measuring the amount spent to acquire the financial item less depreciation and any amortization

cost or any impairment. On the other hand, current value is the updated value of a financial item

at which two genuine persons are willing to buy or sell at current market price on reporting date.

Current value is further divided in to fair value, current cost and value in use. The entity has the

option to choose any of the measurement basis or more than one measurement basis for different

financial items reflecting in a financial statement.

The annual report of Alumina Limited shows that the fixed assets of Alumina Limited is

measured on historical cost basis which is tested for impairment and any needful changes have

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

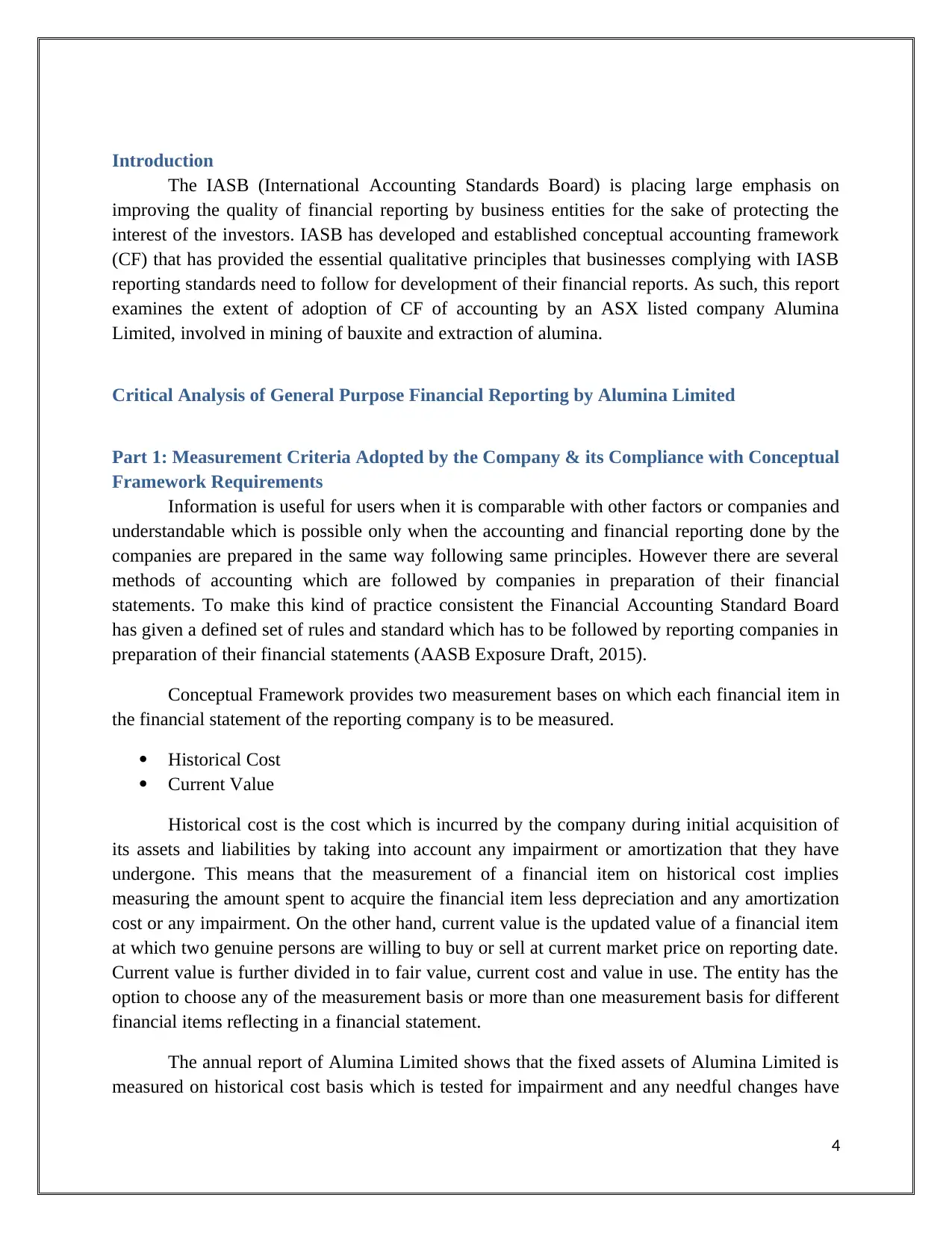

been made as a result of impairment and borrowings are recognized at fair value initially and

subsequently measured at amortized cost. Derivatives are measured at fair value. Liabilities for

salary and annual leave are measured at current provisions. Alumina Limited complied with

International Financial Reporting Standards (IFRS) issued by the International Accounting

Standards Board (Annual Report, 2017).

(Annual Report, 2017)

(Annual Report, 2017)

5

subsequently measured at amortized cost. Derivatives are measured at fair value. Liabilities for

salary and annual leave are measured at current provisions. Alumina Limited complied with

International Financial Reporting Standards (IFRS) issued by the International Accounting

Standards Board (Annual Report, 2017).

(Annual Report, 2017)

(Annual Report, 2017)

5

(Annual Report, 2017)

Part 2: Fundamental Qualitative Characteristics of Conceptual Framework Applied by

Alumina Limited

An interest party to the reporting company always seeks information which is placed at

one place and is understandable, comparable or useful. Considering these issues International

Accounting Standard Board has issued International Financial Reporting Standards (IFRS) which

states some fundamental qualitative characteristics to be exist in financial reporting. The

fundamental qualitative characteristics are relevance and faithful representation (AASB

Exposure Draft, 2015).

Relevant information always gives a user a predictive value or confirmatoryvalue or both

and if it doesn’t provide any of such value then such information is of no use. It is a data only.

Relevant information can be used by different users or same user for different matters. In short

information is relevant and material it can change users view on the financial statement

(Complied Framework, 2015).

Annual report of Alumina Limited indicates that it has provided all the relevant

information to its users which can be useful for their analysis of financial statements as can be

seen from its consolidated Profit and loss account. Alumina Limited is a profit making company.

by analyzing the below statement it can be said that it has the growth perspective in future also as

it has come from a loss making company to a profit making company (Annual Report, 2017).

6

Part 2: Fundamental Qualitative Characteristics of Conceptual Framework Applied by

Alumina Limited

An interest party to the reporting company always seeks information which is placed at

one place and is understandable, comparable or useful. Considering these issues International

Accounting Standard Board has issued International Financial Reporting Standards (IFRS) which

states some fundamental qualitative characteristics to be exist in financial reporting. The

fundamental qualitative characteristics are relevance and faithful representation (AASB

Exposure Draft, 2015).

Relevant information always gives a user a predictive value or confirmatoryvalue or both

and if it doesn’t provide any of such value then such information is of no use. It is a data only.

Relevant information can be used by different users or same user for different matters. In short

information is relevant and material it can change users view on the financial statement

(Complied Framework, 2015).

Annual report of Alumina Limited indicates that it has provided all the relevant

information to its users which can be useful for their analysis of financial statements as can be

seen from its consolidated Profit and loss account. Alumina Limited is a profit making company.

by analyzing the below statement it can be said that it has the growth perspective in future also as

it has come from a loss making company to a profit making company (Annual Report, 2017).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Annual Report, 2017)

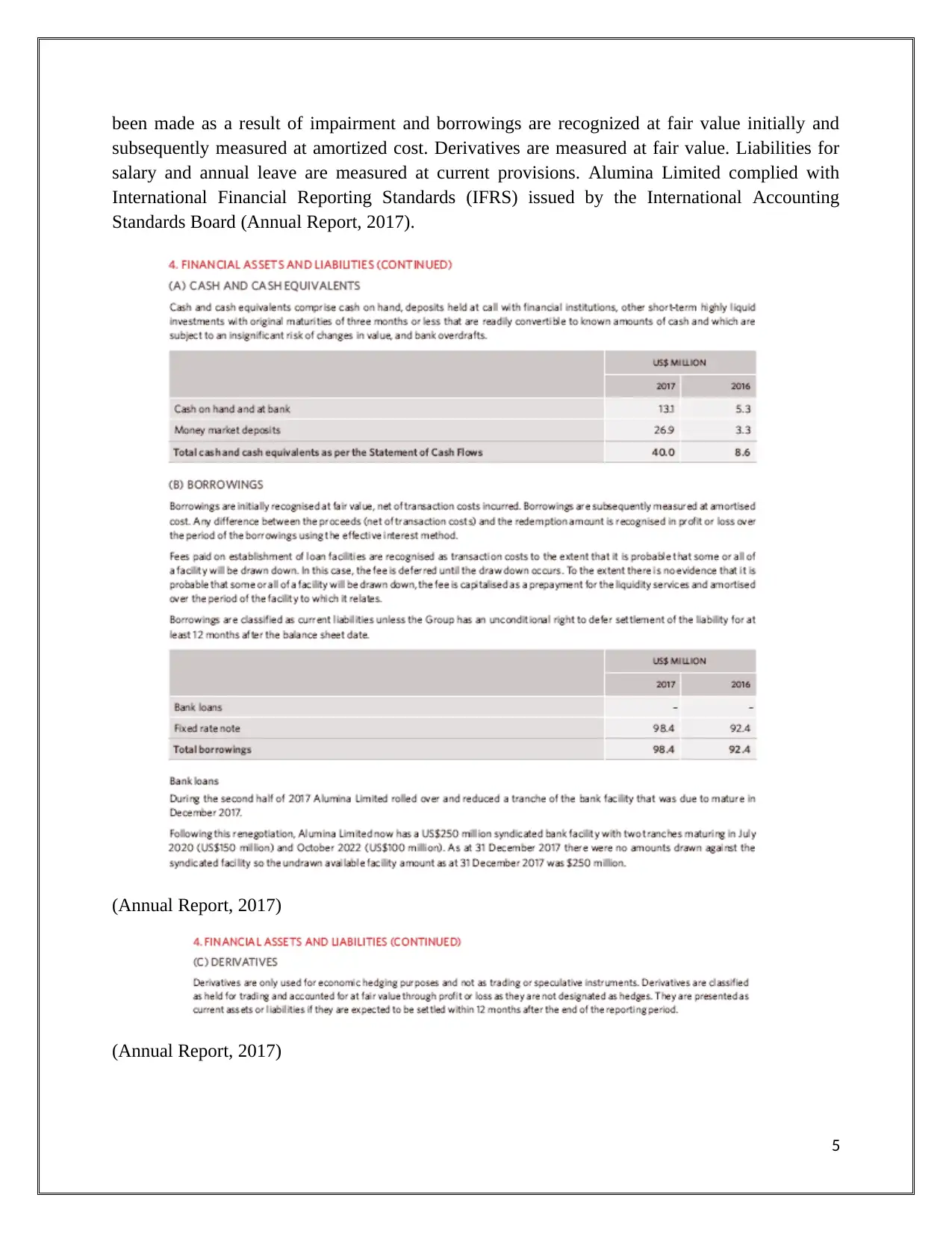

The second fundamental qualitative characteristic in preparation of a financial statement

is faithful representation. Information is faithfully represented if it considers the representing

company’s financial position and performance over presenting its legal form only. Companies

tend to show their financial statement very rich just by window dressing.Faithfully represented

information is complete, neutral and free form errors and misstatements. Alumina Limited has

followed the fundamental qualitative characteristics in preparation of its financial statements can

be seen from its independent audit report prepared by PWC (Annual Report, 2017).

(Annual Report, 2017)

Part 3: Enhancing Qualitative Characteristics of Conceptual Framework Applied by

Company

To enhance the quality of the information which is relevant and faithfully represented to

the user in the financial report of the reporting company, it should adopt some other qualitative

7

The second fundamental qualitative characteristic in preparation of a financial statement

is faithful representation. Information is faithfully represented if it considers the representing

company’s financial position and performance over presenting its legal form only. Companies

tend to show their financial statement very rich just by window dressing.Faithfully represented

information is complete, neutral and free form errors and misstatements. Alumina Limited has

followed the fundamental qualitative characteristics in preparation of its financial statements can

be seen from its independent audit report prepared by PWC (Annual Report, 2017).

(Annual Report, 2017)

Part 3: Enhancing Qualitative Characteristics of Conceptual Framework Applied by

Company

To enhance the quality of the information which is relevant and faithfully represented to

the user in the financial report of the reporting company, it should adopt some other qualitative

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

characteristics in preparation of its financial statements. These are Comparability, Verifiability,

Timeliness and understandability (Macve, 2015).

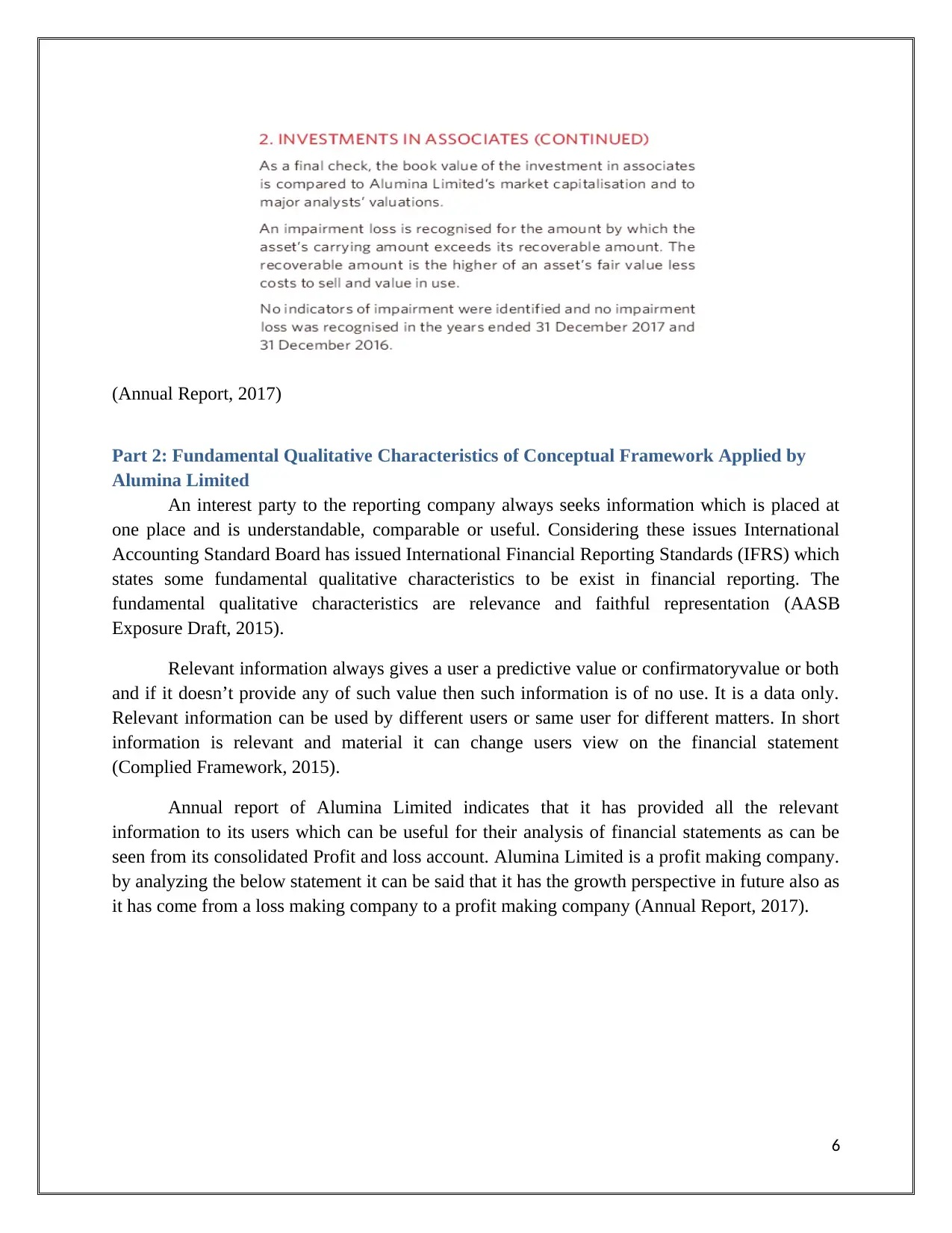

As stated earlier in this report useful information is useful only if it comparable with

previous year’s data or data of other company to make investment decisions by users. Whether

Alumina Limited has provided comparable information or not is reflected by its cash flow

statement (Annual Report, 2017).

(Annual Report, 2017)

The understandability criteria require that the financial information of a reporting entity

should be relatively easy to understand. This requires adequate explanation of the accounting

methods and policies that are followed for preparation of the financial reports. As such, Alumina

8

Timeliness and understandability (Macve, 2015).

As stated earlier in this report useful information is useful only if it comparable with

previous year’s data or data of other company to make investment decisions by users. Whether

Alumina Limited has provided comparable information or not is reflected by its cash flow

statement (Annual Report, 2017).

(Annual Report, 2017)

The understandability criteria require that the financial information of a reporting entity

should be relatively easy to understand. This requires adequate explanation of the accounting

methods and policies that are followed for preparation of the financial reports. As such, Alumina

8

Limited has presented explanation regarding the accounting policies adopted for development of

financial statements in the notes section (Annual Report, 2017).

(Annual Report, 2017)

The verifiability requires that financial information should be disclosed in the financial

statements in a quantitative format so that it can be easily verified through direct observation. It

has also followed timeliness feature of the financial reporting by presenting information on an

annual basis (PKF International Ltd, 2017).

Part 4: Users of Financial Reports in Making Financial Decisions

The annual report of Alumina limited has been prepared in accordance with the AASB

(Australian Accounting Standards Board) that complies with the IFRS and as such present the

financial information as per the needs and requirements of the CF of financial reporting. This has

enhanced the usefulness of its financial report for the end-users such as investors, lenders and

creditors. For example, the financial statements of the company has disclosed adequate

information in relation to the revenue, assets, liabilities, expenses, sales and other such key

financial items that are required by the present and potential investors before making any

investment decision (Schroeder, Clark and Cathey, 2016). The lenders and creditors requires

information about the liquidity and solvency position of the company that can be analyzed with

the use of calculating ratios such as current ratio or debt-equity ratio. The ratio can be effectively

evaluated with the use of value of key financial items such as assets, debt and equity disclosed

within the financial statements of the company (Annual Report, 2017).

Part 5: Knowledge Required by End-Users for Analysis of Financial Reports

It has been stated by the CF of accounting that end-user of financial reports such as

investors, creditors, lenders and other borrowers require a basic knowledge of accounting for

9

financial statements in the notes section (Annual Report, 2017).

(Annual Report, 2017)

The verifiability requires that financial information should be disclosed in the financial

statements in a quantitative format so that it can be easily verified through direct observation. It

has also followed timeliness feature of the financial reporting by presenting information on an

annual basis (PKF International Ltd, 2017).

Part 4: Users of Financial Reports in Making Financial Decisions

The annual report of Alumina limited has been prepared in accordance with the AASB

(Australian Accounting Standards Board) that complies with the IFRS and as such present the

financial information as per the needs and requirements of the CF of financial reporting. This has

enhanced the usefulness of its financial report for the end-users such as investors, lenders and

creditors. For example, the financial statements of the company has disclosed adequate

information in relation to the revenue, assets, liabilities, expenses, sales and other such key

financial items that are required by the present and potential investors before making any

investment decision (Schroeder, Clark and Cathey, 2016). The lenders and creditors requires

information about the liquidity and solvency position of the company that can be analyzed with

the use of calculating ratios such as current ratio or debt-equity ratio. The ratio can be effectively

evaluated with the use of value of key financial items such as assets, debt and equity disclosed

within the financial statements of the company (Annual Report, 2017).

Part 5: Knowledge Required by End-Users for Analysis of Financial Reports

It has been stated by the CF of accounting that end-user of financial reports such as

investors, creditors, lenders and other borrowers require a basic knowledge of accounting for

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

developing an understanding of the information presented within the financial statements.

However, it can be said that end-users such as general public, government and other stakeholders

who only want to gain an analysis of the future performance of an entity requires only a basic

knowledge (Schroeder, Clark and Cathey, 2016). The end-users such as financial analysts and

other investors who want to examine the present as well as future trends of a company require

specific expertise for implementing the use of techniques such as ratio and trend analysis to gain

an estimate of its future growth prospects (Annual Report, 2017).

Part 6: Requirements of general Purpose Financial Reporting met by the Company

The CF of financial accounting requires that the business entities complying with IFRS

need to meet the criteria of presenting and disclosing all the financial statements such as

statement of changes in equity, income statement, cash flow statement and balance sheet. In

addition with this, a financial reporting entity also needs to provide proper disclosure regarding

the accounting policies and methods adopted for calculating and evaluating the value of key

financial items. The company, Alumina Limited, is complying effectively with the IFRS

requirements as it ahs adequately met all the criteria discussed above for developing and

presenting the general purpose financial report (Annual Report, 2017).

Conclusion

It can be stated from the overall discussion held in the report that compliance with the CF

of accounting helps the business entities to comply with standard accounting policies and

methods stated by the IASB. This helps in enriching the financial information that is presented to

the end-users and assist in their decision-making process.

10

However, it can be said that end-users such as general public, government and other stakeholders

who only want to gain an analysis of the future performance of an entity requires only a basic

knowledge (Schroeder, Clark and Cathey, 2016). The end-users such as financial analysts and

other investors who want to examine the present as well as future trends of a company require

specific expertise for implementing the use of techniques such as ratio and trend analysis to gain

an estimate of its future growth prospects (Annual Report, 2017).

Part 6: Requirements of general Purpose Financial Reporting met by the Company

The CF of financial accounting requires that the business entities complying with IFRS

need to meet the criteria of presenting and disclosing all the financial statements such as

statement of changes in equity, income statement, cash flow statement and balance sheet. In

addition with this, a financial reporting entity also needs to provide proper disclosure regarding

the accounting policies and methods adopted for calculating and evaluating the value of key

financial items. The company, Alumina Limited, is complying effectively with the IFRS

requirements as it ahs adequately met all the criteria discussed above for developing and

presenting the general purpose financial report (Annual Report, 2017).

Conclusion

It can be stated from the overall discussion held in the report that compliance with the CF

of accounting helps the business entities to comply with standard accounting policies and

methods stated by the IASB. This helps in enriching the financial information that is presented to

the end-users and assist in their decision-making process.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

AASB Exposure Draft. 2015. Conceptual Framework for Financial Reporting. [Online].

Available at: https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf

[Accessed on: 16 April 2019].

Annual Report. 2017. Alumina Limited. [Online]. Available at:

https://www.aluminalimited.com/uploads/ALU8484-2017-Annual-Report-WEB.pdf [Accessed

on: 21 April, 2019].

Complied Framework. 2015. Australian accounting standards Board. [Online]. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed on: 16

April 2019].

Macve, R. 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision

Tool, or Threat. UK: Routledge.

PKF International Ltd. 2017. Wiley IFRS 2017: Interpretation and Application of IFRS

Standards. US: John Wiley & Sons.

Schroeder, R.G., Clark, M. and Cathey, J.M. 2016. Financial Accounting Theory and Analysis:

Text and Cases. US: Wiley.

11

AASB Exposure Draft. 2015. Conceptual Framework for Financial Reporting. [Online].

Available at: https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf

[Accessed on: 16 April 2019].

Annual Report. 2017. Alumina Limited. [Online]. Available at:

https://www.aluminalimited.com/uploads/ALU8484-2017-Annual-Report-WEB.pdf [Accessed

on: 21 April, 2019].

Complied Framework. 2015. Australian accounting standards Board. [Online]. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed on: 16

April 2019].

Macve, R. 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision

Tool, or Threat. UK: Routledge.

PKF International Ltd. 2017. Wiley IFRS 2017: Interpretation and Application of IFRS

Standards. US: John Wiley & Sons.

Schroeder, R.G., Clark, M. and Cathey, J.M. 2016. Financial Accounting Theory and Analysis:

Text and Cases. US: Wiley.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.