Finalization of Audit: Always Precise Instruments Pty Limited - 2019

VerifiedAdded on 2023/03/20

|14

|3162

|78

Report

AI Summary

This report, prepared by an audit manager at Samway Baker Fitzgerald (SBF), details the audit finalization for Always Precise Instruments Pty Limited (API), a manufacturer of military equipment. The report identifies potential audit risks through ratio analysis, including current ratio, quick asset ratio, return on equity, return on total assets, gross margin percentage, marketing expense, administrative expenses, times interest earned, days in inventory, days in accounts receivables, and debt to equity ratio. Each risk is assessed and paired with the corresponding audit procedure. The report also outlines internal control weaknesses related to inventory, raw material receipt, lack of emergency inventory, manufacture of finished goods, and purchase orders, along with associated audit procedures to mitigate these risks. The analysis is based on API's financial report, budget, and industry benchmarks, aiming to provide a comprehensive overview of the company's financial health and potential areas of concern.

AUDITING

2019

2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

MEMO TO: Wayne Wiadrowski

FROM: Audit manager at Samway Baker Fitzgerald (SBF)

DATE: May 12, 2019

SUBJECT: Audit finalization of Always Precise Instruments Pty Limited

1. Potential audit risk Identification

Potential audit risks have the ability to impact the overall functioning of an organization and

therefore, it is the duty of an auditor to conduct his audit processes in a manner that these

risks are easily traced. An auditor by means of employing various ratios such as current ratio,

acid test ratio, gross margin percentage, etc can detect the potential audit risks. Identification

of potential risks will allow the management of an organization to take necessary measures to

lessen or reduce the impact arising due to such risks. Potential audit risks are vulnerable for

the financial well being of an organization and therefore, an auditor must exercise due

caution while conducting audit procedure so as to trace the same (Mock et. al, 2013). An

auditor must also report such potential risks to the management of an organization so as to

encourage the latter in adopting such strategies that can reduce or eliminate the impact of the

same. In the following report, the explanation of various ratios together with the audit risk

and procedure is discussed.

1. Identification of Potential risk

Ratio Analysis Audit

Risk

Audit

procedure

Current ratio: The current ratio distinguishes between the current assets and

current liabilities. The current ratio of Always Precise Instruments

Private Limited is very low. The company must take necessary

measures so as to leverage its current ratio. In order to uplift its

current ratio, the company needs to have more current assets and

less current liabilities. The current ratio is the skills of the current

company’s current assets to absorb its current liabilities or short

Low Risk The

management

of the

company

must adopt

significant

changes in its

2

MEMO TO: Wayne Wiadrowski

FROM: Audit manager at Samway Baker Fitzgerald (SBF)

DATE: May 12, 2019

SUBJECT: Audit finalization of Always Precise Instruments Pty Limited

1. Potential audit risk Identification

Potential audit risks have the ability to impact the overall functioning of an organization and

therefore, it is the duty of an auditor to conduct his audit processes in a manner that these

risks are easily traced. An auditor by means of employing various ratios such as current ratio,

acid test ratio, gross margin percentage, etc can detect the potential audit risks. Identification

of potential risks will allow the management of an organization to take necessary measures to

lessen or reduce the impact arising due to such risks. Potential audit risks are vulnerable for

the financial well being of an organization and therefore, an auditor must exercise due

caution while conducting audit procedure so as to trace the same (Mock et. al, 2013). An

auditor must also report such potential risks to the management of an organization so as to

encourage the latter in adopting such strategies that can reduce or eliminate the impact of the

same. In the following report, the explanation of various ratios together with the audit risk

and procedure is discussed.

1. Identification of Potential risk

Ratio Analysis Audit

Risk

Audit

procedure

Current ratio: The current ratio distinguishes between the current assets and

current liabilities. The current ratio of Always Precise Instruments

Private Limited is very low. The company must take necessary

measures so as to leverage its current ratio. In order to uplift its

current ratio, the company needs to have more current assets and

less current liabilities. The current ratio is the skills of the current

company’s current assets to absorb its current liabilities or short

Low Risk The

management

of the

company

must adopt

significant

changes in its

2

Audit

term debt obligations. An enhanced current ratio is always

desirable as it allows the company to uplift its volume of sales and

minimize its trade receivables. This will immediately enhance the

cash flows of the company. An enhanced current ratio shall allow

the company to earn more revenues and have a significant drop in

its debts. When it comes to API Private Limited, the current ratio

has enhanced in the present year in comparison to the bygone

year. The current ratio of API Private Limited was at 1.54 for the

previous year while the same is at 1.64 for the current year. The

improvement in the current ratio is highly favorable for the

company and it depicts the area of low risk.

current assets

and current

liabilities in

the ongoing

year so as to

enhance its

current ratio.

The

responsibility

of the auditor

is to use

analytical

procedures so

as to draw a

comparison

between the

current assets

and current

liabilities of

the company

(Merchant,

2012).

Quick asset

ratio:

Quick asset ratio is also a kind of liquidity ratio and it is popularly

known as acid test ratio. With the help of quick asset ratio, it

becomes easier to ascertain if there are sufficient liquid resources

available with an entity to tackle its current liabilities. In order to

enhance the cash and cash equivalents along with the reduction or

elimination of debts, an entity must always exercise due focus on

its current ratio and quick ratio. The quick asset ratio of API

Private Limited indicated that there are sufficient liquid assets

available in the same for the absorption of its short term debt

obligations (Matthew, 2015). Hence, it seems to be an area of low

Low Risk An auditor

must not only

follow

analytical

procedure but

also draw

comparisons

with the last

year so as to

look for any

3

term debt obligations. An enhanced current ratio is always

desirable as it allows the company to uplift its volume of sales and

minimize its trade receivables. This will immediately enhance the

cash flows of the company. An enhanced current ratio shall allow

the company to earn more revenues and have a significant drop in

its debts. When it comes to API Private Limited, the current ratio

has enhanced in the present year in comparison to the bygone

year. The current ratio of API Private Limited was at 1.54 for the

previous year while the same is at 1.64 for the current year. The

improvement in the current ratio is highly favorable for the

company and it depicts the area of low risk.

current assets

and current

liabilities in

the ongoing

year so as to

enhance its

current ratio.

The

responsibility

of the auditor

is to use

analytical

procedures so

as to draw a

comparison

between the

current assets

and current

liabilities of

the company

(Merchant,

2012).

Quick asset

ratio:

Quick asset ratio is also a kind of liquidity ratio and it is popularly

known as acid test ratio. With the help of quick asset ratio, it

becomes easier to ascertain if there are sufficient liquid resources

available with an entity to tackle its current liabilities. In order to

enhance the cash and cash equivalents along with the reduction or

elimination of debts, an entity must always exercise due focus on

its current ratio and quick ratio. The quick asset ratio of API

Private Limited indicated that there are sufficient liquid assets

available in the same for the absorption of its short term debt

obligations (Matthew, 2015). Hence, it seems to be an area of low

Low Risk An auditor

must not only

follow

analytical

procedure but

also draw

comparisons

with the last

year so as to

look for any

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

risk. shortcomings

in the same

which can be

rectified in

the coming

year to

ascertain a

better quick

asset ratio

(Matthew,

2015).

Return on

equity %

The return on equity percentage for API Private Limited dropped

down to 14.7% in 2018 while the same was 18.4% in the previous

year. Such a significant drop in the return on equity percentage of

the company depicts a moderate area of risk. The current return

on equity percentage is even lower than the industry standards.

An underperforming return on equity percentage highlights the

fact that the company is unable to employ effective strategies and

there is a need for the same to carry out a proper evaluation. This

will allow the management to locate the reasons behind the fall in

ROE percentage and rectify the same through the implementation

of necessary strategies (Lapsley, 2012).

Moderate

Risk

An auditor

must conduct

a detailed

analysis of its

return on

equity

percentage

and must also

opt for

property

valuation so

as to trace

any

shortcomings

in the same.

Return on

total assets %

The ROTA of API Private Limited dropped from 14.9% to 12.5%

in the current year while the budgeted figure of the same for the

ongoing year is 16%. It is an area of moderate risk. The company

must clearly assess its overall assets so as to enhance its return on

Moderate

Risk

The auditor

must trace the

actual

reasons

4

risk. shortcomings

in the same

which can be

rectified in

the coming

year to

ascertain a

better quick

asset ratio

(Matthew,

2015).

Return on

equity %

The return on equity percentage for API Private Limited dropped

down to 14.7% in 2018 while the same was 18.4% in the previous

year. Such a significant drop in the return on equity percentage of

the company depicts a moderate area of risk. The current return

on equity percentage is even lower than the industry standards.

An underperforming return on equity percentage highlights the

fact that the company is unable to employ effective strategies and

there is a need for the same to carry out a proper evaluation. This

will allow the management to locate the reasons behind the fall in

ROE percentage and rectify the same through the implementation

of necessary strategies (Lapsley, 2012).

Moderate

Risk

An auditor

must conduct

a detailed

analysis of its

return on

equity

percentage

and must also

opt for

property

valuation so

as to trace

any

shortcomings

in the same.

Return on

total assets %

The ROTA of API Private Limited dropped from 14.9% to 12.5%

in the current year while the budgeted figure of the same for the

ongoing year is 16%. It is an area of moderate risk. The company

must clearly assess its overall assets so as to enhance its return on

Moderate

Risk

The auditor

must trace the

actual

reasons

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

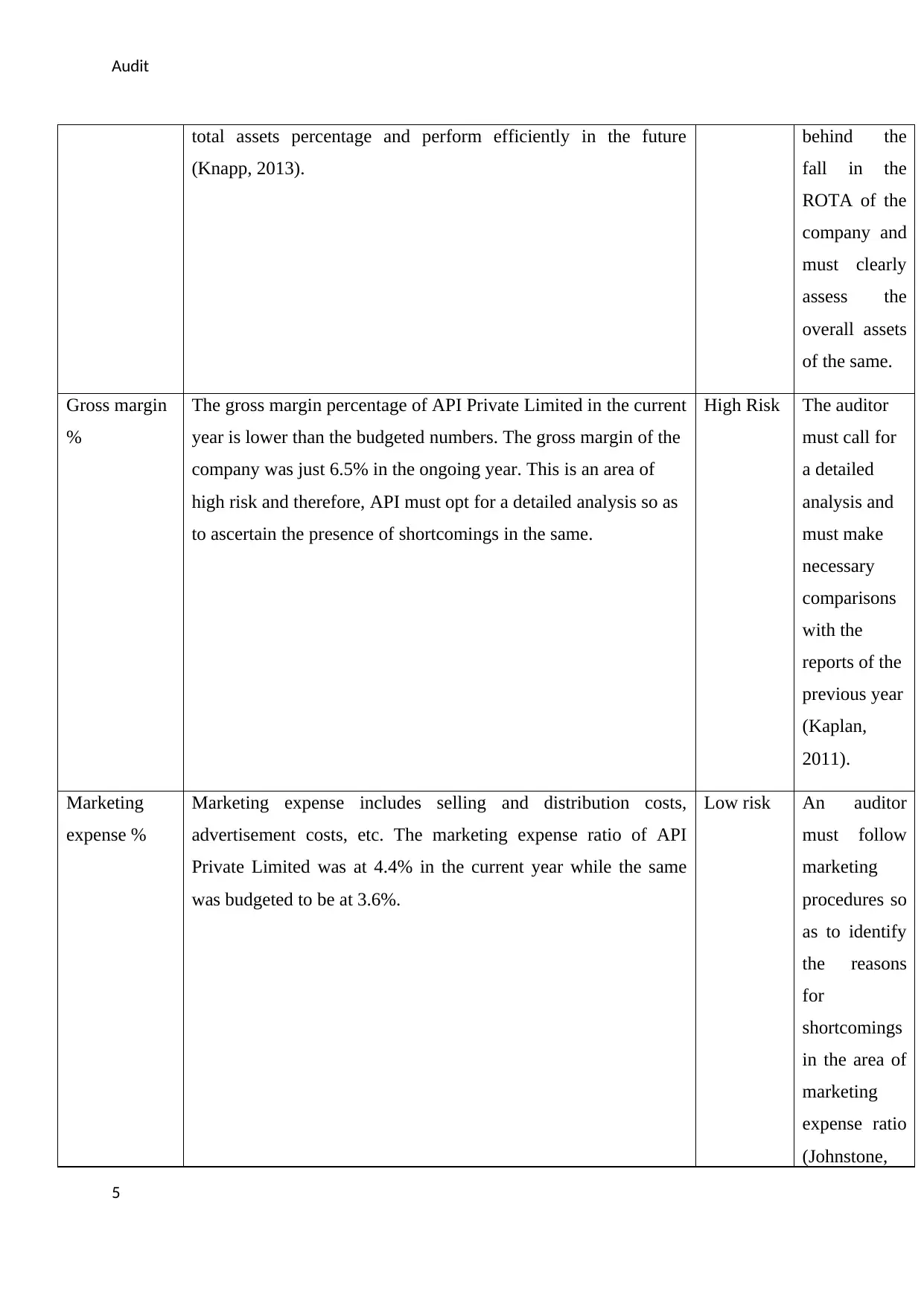

total assets percentage and perform efficiently in the future

(Knapp, 2013).

behind the

fall in the

ROTA of the

company and

must clearly

assess the

overall assets

of the same.

Gross margin

%

The gross margin percentage of API Private Limited in the current

year is lower than the budgeted numbers. The gross margin of the

company was just 6.5% in the ongoing year. This is an area of

high risk and therefore, API must opt for a detailed analysis so as

to ascertain the presence of shortcomings in the same.

High Risk The auditor

must call for

a detailed

analysis and

must make

necessary

comparisons

with the

reports of the

previous year

(Kaplan,

2011).

Marketing

expense %

Marketing expense includes selling and distribution costs,

advertisement costs, etc. The marketing expense ratio of API

Private Limited was at 4.4% in the current year while the same

was budgeted to be at 3.6%.

Low risk An auditor

must follow

marketing

procedures so

as to identify

the reasons

for

shortcomings

in the area of

marketing

expense ratio

(Johnstone,

5

total assets percentage and perform efficiently in the future

(Knapp, 2013).

behind the

fall in the

ROTA of the

company and

must clearly

assess the

overall assets

of the same.

Gross margin

%

The gross margin percentage of API Private Limited in the current

year is lower than the budgeted numbers. The gross margin of the

company was just 6.5% in the ongoing year. This is an area of

high risk and therefore, API must opt for a detailed analysis so as

to ascertain the presence of shortcomings in the same.

High Risk The auditor

must call for

a detailed

analysis and

must make

necessary

comparisons

with the

reports of the

previous year

(Kaplan,

2011).

Marketing

expense %

Marketing expense includes selling and distribution costs,

advertisement costs, etc. The marketing expense ratio of API

Private Limited was at 4.4% in the current year while the same

was budgeted to be at 3.6%.

Low risk An auditor

must follow

marketing

procedures so

as to identify

the reasons

for

shortcomings

in the area of

marketing

expense ratio

(Johnstone,

5

Audit

Gramling &

Rittenberg,

2014).

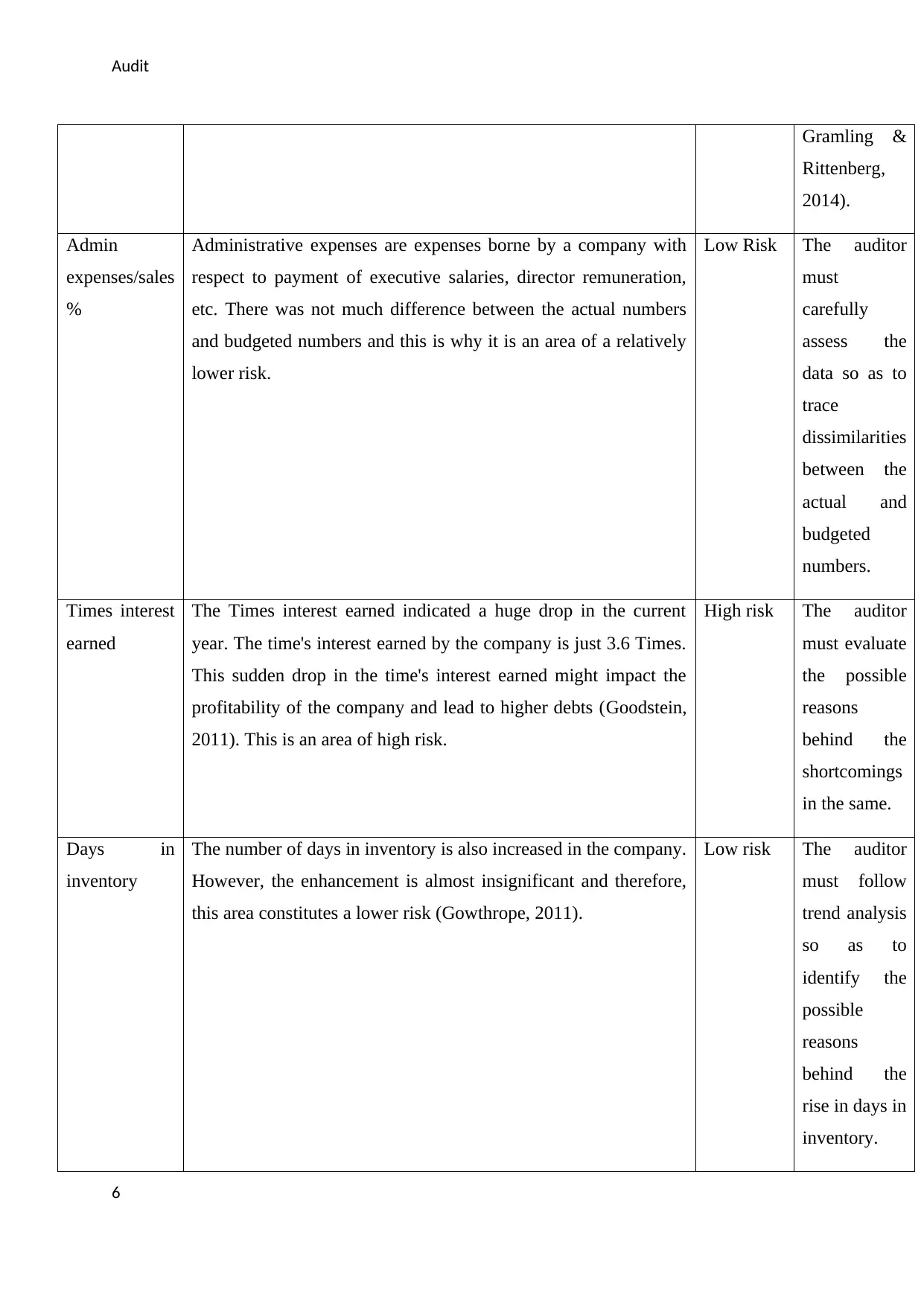

Admin

expenses/sales

%

Administrative expenses are expenses borne by a company with

respect to payment of executive salaries, director remuneration,

etc. There was not much difference between the actual numbers

and budgeted numbers and this is why it is an area of a relatively

lower risk.

Low Risk The auditor

must

carefully

assess the

data so as to

trace

dissimilarities

between the

actual and

budgeted

numbers.

Times interest

earned

The Times interest earned indicated a huge drop in the current

year. The time's interest earned by the company is just 3.6 Times.

This sudden drop in the time's interest earned might impact the

profitability of the company and lead to higher debts (Goodstein,

2011). This is an area of high risk.

High risk The auditor

must evaluate

the possible

reasons

behind the

shortcomings

in the same.

Days in

inventory

The number of days in inventory is also increased in the company.

However, the enhancement is almost insignificant and therefore,

this area constitutes a lower risk (Gowthrope, 2011).

Low risk The auditor

must follow

trend analysis

so as to

identify the

possible

reasons

behind the

rise in days in

inventory.

6

Gramling &

Rittenberg,

2014).

Admin

expenses/sales

%

Administrative expenses are expenses borne by a company with

respect to payment of executive salaries, director remuneration,

etc. There was not much difference between the actual numbers

and budgeted numbers and this is why it is an area of a relatively

lower risk.

Low Risk The auditor

must

carefully

assess the

data so as to

trace

dissimilarities

between the

actual and

budgeted

numbers.

Times interest

earned

The Times interest earned indicated a huge drop in the current

year. The time's interest earned by the company is just 3.6 Times.

This sudden drop in the time's interest earned might impact the

profitability of the company and lead to higher debts (Goodstein,

2011). This is an area of high risk.

High risk The auditor

must evaluate

the possible

reasons

behind the

shortcomings

in the same.

Days in

inventory

The number of days in inventory is also increased in the company.

However, the enhancement is almost insignificant and therefore,

this area constitutes a lower risk (Gowthrope, 2011).

Low risk The auditor

must follow

trend analysis

so as to

identify the

possible

reasons

behind the

rise in days in

inventory.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

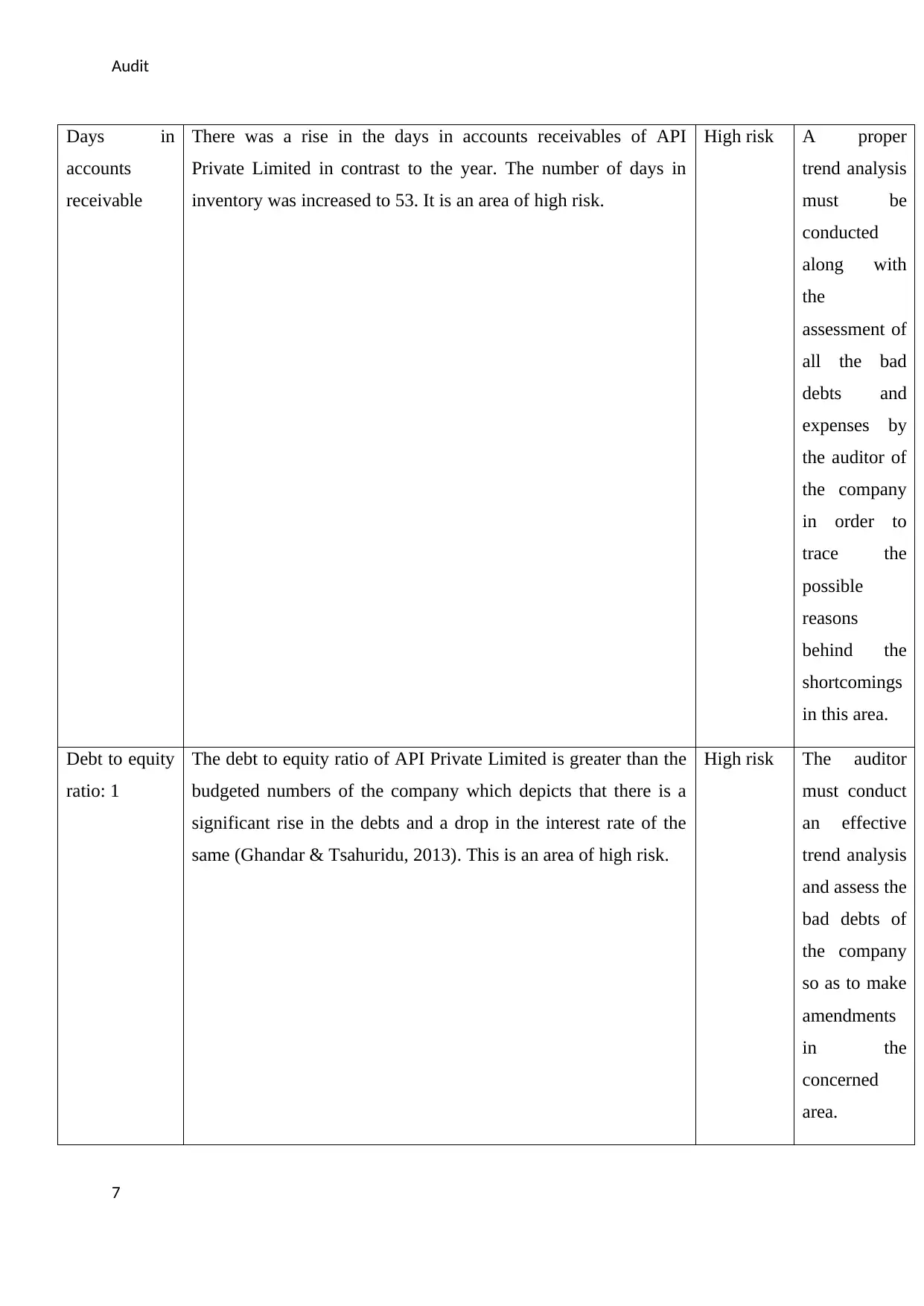

Days in

accounts

receivable

There was a rise in the days in accounts receivables of API

Private Limited in contrast to the year. The number of days in

inventory was increased to 53. It is an area of high risk.

High risk A proper

trend analysis

must be

conducted

along with

the

assessment of

all the bad

debts and

expenses by

the auditor of

the company

in order to

trace the

possible

reasons

behind the

shortcomings

in this area.

Debt to equity

ratio: 1

The debt to equity ratio of API Private Limited is greater than the

budgeted numbers of the company which depicts that there is a

significant rise in the debts and a drop in the interest rate of the

same (Ghandar & Tsahuridu, 2013). This is an area of high risk.

High risk The auditor

must conduct

an effective

trend analysis

and assess the

bad debts of

the company

so as to make

amendments

in the

concerned

area.

7

Days in

accounts

receivable

There was a rise in the days in accounts receivables of API

Private Limited in contrast to the year. The number of days in

inventory was increased to 53. It is an area of high risk.

High risk A proper

trend analysis

must be

conducted

along with

the

assessment of

all the bad

debts and

expenses by

the auditor of

the company

in order to

trace the

possible

reasons

behind the

shortcomings

in this area.

Debt to equity

ratio: 1

The debt to equity ratio of API Private Limited is greater than the

budgeted numbers of the company which depicts that there is a

significant rise in the debts and a drop in the interest rate of the

same (Ghandar & Tsahuridu, 2013). This is an area of high risk.

High risk The auditor

must conduct

an effective

trend analysis

and assess the

bad debts of

the company

so as to make

amendments

in the

concerned

area.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

2. Identification of internal control weaknesses

Internal control weakness Audit risk Audit procedure to reduce

risk

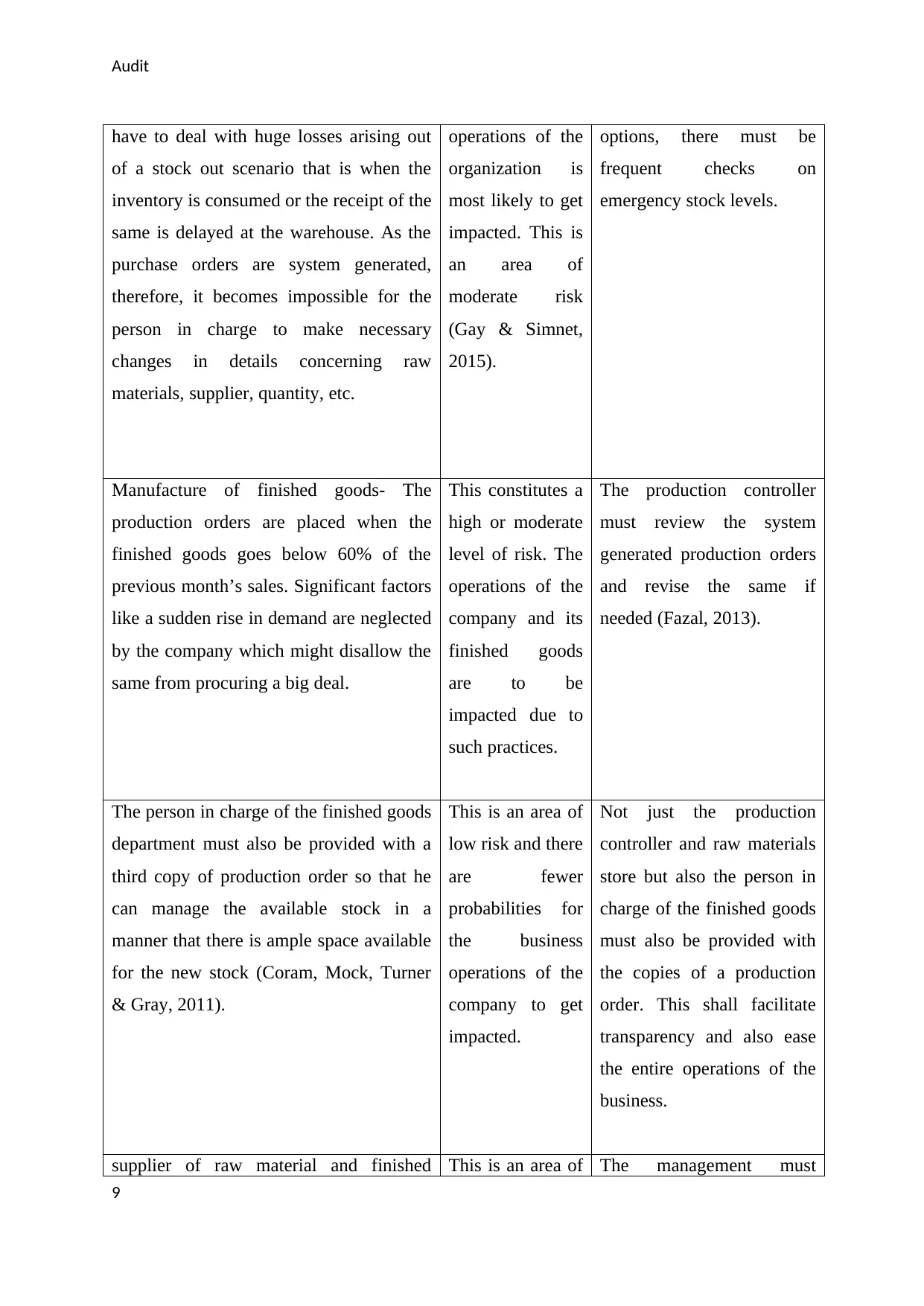

Triggering purchase related orders- The

purchase orders are generated when the

raw material stock falls below 70% of the

last month’s consumption. If the last

month’s consumption is wrongly recorded

or not recorded at all by the store’s staff in

the required documents then the purchase

orders might be inappropriately triggered

or might not be triggered at all depending

on the requirements of the factory. It can

highly lead to an understock, stock out or

overstock scenario.

The inventory

value, purchase

orders, purchases

and the business

activities of the

company can

suffer due to over

stock, stock out

or under stock

scenario. Here,

the audit risk

involved is

moderate or low.

The store’s staff must

determine, analyse and

report the values of the

overall consumption of raw

materials in the necessary

documents as and when

needed.

Receipt of raw material- There are high

chances for the raw materials received by

the company to be of different quality then

what has been ordered and paid for. Also,

the shortage of raw materials received is

also most likely to happen. Therefore, the

company must opt for physical inspection

and manual counting as soon as the raw

material is received instead of recording

the same direction in the system.

This is an area of

low or moderate

risk. The quality

of raw materials

received is most

likely to raise

concerns in the

absence of

manual

inspection and

checking of the

same as and

when received.

The person in charge must

physically count and inspect

the raw materials as and

when received so as to

minimise the risks

associated with the same.

Lack of emergency inventory options: The

company is devoid of emergency

inventory options. The company might

The value of

inventories along

with the

In order to deal with the

mishaps caused as a result of

lack of emergency inventory

8

2. Identification of internal control weaknesses

Internal control weakness Audit risk Audit procedure to reduce

risk

Triggering purchase related orders- The

purchase orders are generated when the

raw material stock falls below 70% of the

last month’s consumption. If the last

month’s consumption is wrongly recorded

or not recorded at all by the store’s staff in

the required documents then the purchase

orders might be inappropriately triggered

or might not be triggered at all depending

on the requirements of the factory. It can

highly lead to an understock, stock out or

overstock scenario.

The inventory

value, purchase

orders, purchases

and the business

activities of the

company can

suffer due to over

stock, stock out

or under stock

scenario. Here,

the audit risk

involved is

moderate or low.

The store’s staff must

determine, analyse and

report the values of the

overall consumption of raw

materials in the necessary

documents as and when

needed.

Receipt of raw material- There are high

chances for the raw materials received by

the company to be of different quality then

what has been ordered and paid for. Also,

the shortage of raw materials received is

also most likely to happen. Therefore, the

company must opt for physical inspection

and manual counting as soon as the raw

material is received instead of recording

the same direction in the system.

This is an area of

low or moderate

risk. The quality

of raw materials

received is most

likely to raise

concerns in the

absence of

manual

inspection and

checking of the

same as and

when received.

The person in charge must

physically count and inspect

the raw materials as and

when received so as to

minimise the risks

associated with the same.

Lack of emergency inventory options: The

company is devoid of emergency

inventory options. The company might

The value of

inventories along

with the

In order to deal with the

mishaps caused as a result of

lack of emergency inventory

8

Audit

have to deal with huge losses arising out

of a stock out scenario that is when the

inventory is consumed or the receipt of the

same is delayed at the warehouse. As the

purchase orders are system generated,

therefore, it becomes impossible for the

person in charge to make necessary

changes in details concerning raw

materials, supplier, quantity, etc.

operations of the

organization is

most likely to get

impacted. This is

an area of

moderate risk

(Gay & Simnet,

2015).

options, there must be

frequent checks on

emergency stock levels.

Manufacture of finished goods- The

production orders are placed when the

finished goods goes below 60% of the

previous month’s sales. Significant factors

like a sudden rise in demand are neglected

by the company which might disallow the

same from procuring a big deal.

This constitutes a

high or moderate

level of risk. The

operations of the

company and its

finished goods

are to be

impacted due to

such practices.

The production controller

must review the system

generated production orders

and revise the same if

needed (Fazal, 2013).

The person in charge of the finished goods

department must also be provided with a

third copy of production order so that he

can manage the available stock in a

manner that there is ample space available

for the new stock (Coram, Mock, Turner

& Gray, 2011).

This is an area of

low risk and there

are fewer

probabilities for

the business

operations of the

company to get

impacted.

Not just the production

controller and raw materials

store but also the person in

charge of the finished goods

must also be provided with

the copies of a production

order. This shall facilitate

transparency and also ease

the entire operations of the

business.

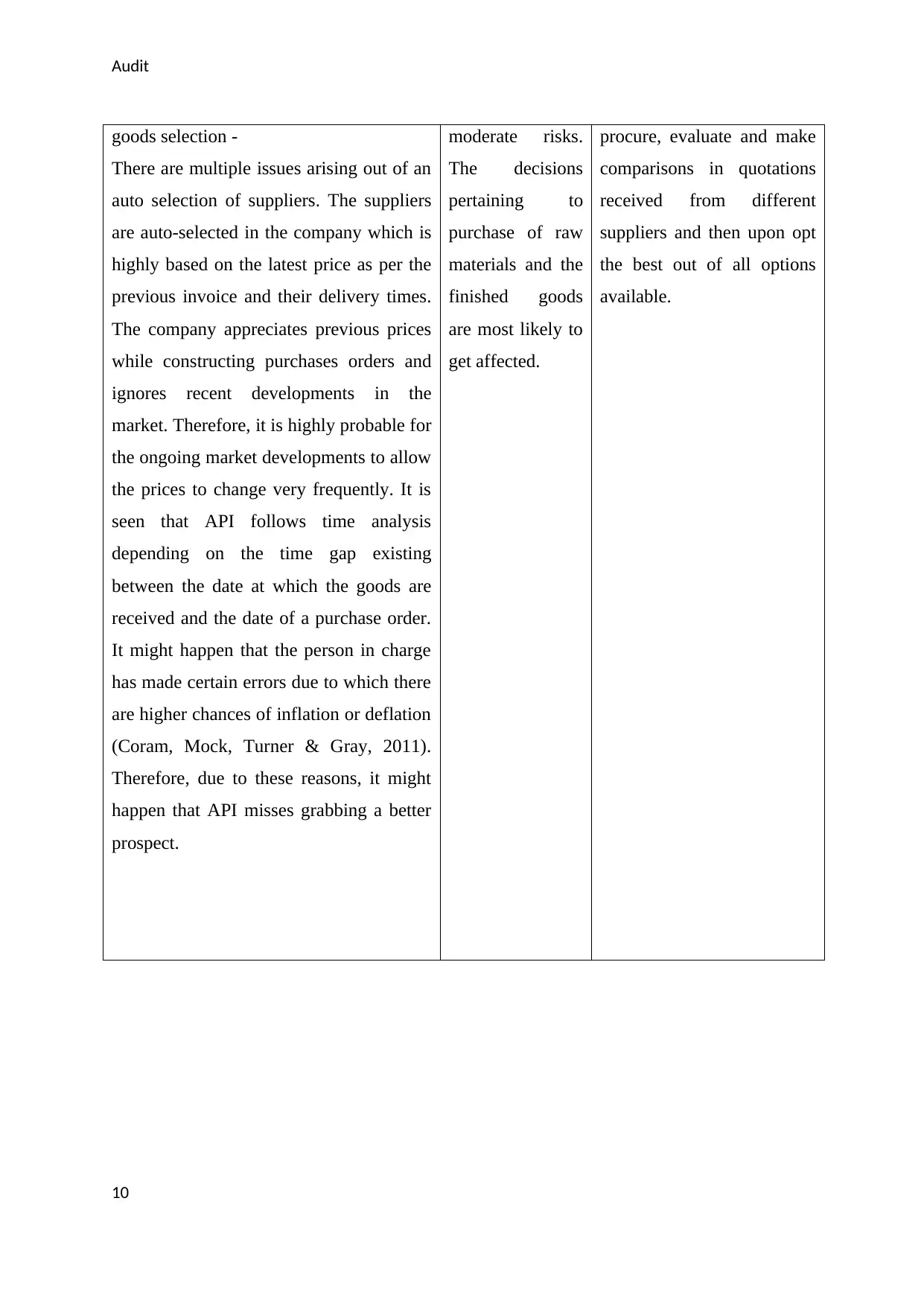

supplier of raw material and finished This is an area of The management must

9

have to deal with huge losses arising out

of a stock out scenario that is when the

inventory is consumed or the receipt of the

same is delayed at the warehouse. As the

purchase orders are system generated,

therefore, it becomes impossible for the

person in charge to make necessary

changes in details concerning raw

materials, supplier, quantity, etc.

operations of the

organization is

most likely to get

impacted. This is

an area of

moderate risk

(Gay & Simnet,

2015).

options, there must be

frequent checks on

emergency stock levels.

Manufacture of finished goods- The

production orders are placed when the

finished goods goes below 60% of the

previous month’s sales. Significant factors

like a sudden rise in demand are neglected

by the company which might disallow the

same from procuring a big deal.

This constitutes a

high or moderate

level of risk. The

operations of the

company and its

finished goods

are to be

impacted due to

such practices.

The production controller

must review the system

generated production orders

and revise the same if

needed (Fazal, 2013).

The person in charge of the finished goods

department must also be provided with a

third copy of production order so that he

can manage the available stock in a

manner that there is ample space available

for the new stock (Coram, Mock, Turner

& Gray, 2011).

This is an area of

low risk and there

are fewer

probabilities for

the business

operations of the

company to get

impacted.

Not just the production

controller and raw materials

store but also the person in

charge of the finished goods

must also be provided with

the copies of a production

order. This shall facilitate

transparency and also ease

the entire operations of the

business.

supplier of raw material and finished This is an area of The management must

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

goods selection -

There are multiple issues arising out of an

auto selection of suppliers. The suppliers

are auto-selected in the company which is

highly based on the latest price as per the

previous invoice and their delivery times.

The company appreciates previous prices

while constructing purchases orders and

ignores recent developments in the

market. Therefore, it is highly probable for

the ongoing market developments to allow

the prices to change very frequently. It is

seen that API follows time analysis

depending on the time gap existing

between the date at which the goods are

received and the date of a purchase order.

It might happen that the person in charge

has made certain errors due to which there

are higher chances of inflation or deflation

(Coram, Mock, Turner & Gray, 2011).

Therefore, due to these reasons, it might

happen that API misses grabbing a better

prospect.

moderate risks.

The decisions

pertaining to

purchase of raw

materials and the

finished goods

are most likely to

get affected.

procure, evaluate and make

comparisons in quotations

received from different

suppliers and then upon opt

the best out of all options

available.

10

goods selection -

There are multiple issues arising out of an

auto selection of suppliers. The suppliers

are auto-selected in the company which is

highly based on the latest price as per the

previous invoice and their delivery times.

The company appreciates previous prices

while constructing purchases orders and

ignores recent developments in the

market. Therefore, it is highly probable for

the ongoing market developments to allow

the prices to change very frequently. It is

seen that API follows time analysis

depending on the time gap existing

between the date at which the goods are

received and the date of a purchase order.

It might happen that the person in charge

has made certain errors due to which there

are higher chances of inflation or deflation

(Coram, Mock, Turner & Gray, 2011).

Therefore, due to these reasons, it might

happen that API misses grabbing a better

prospect.

moderate risks.

The decisions

pertaining to

purchase of raw

materials and the

finished goods

are most likely to

get affected.

procure, evaluate and make

comparisons in quotations

received from different

suppliers and then upon opt

the best out of all options

available.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

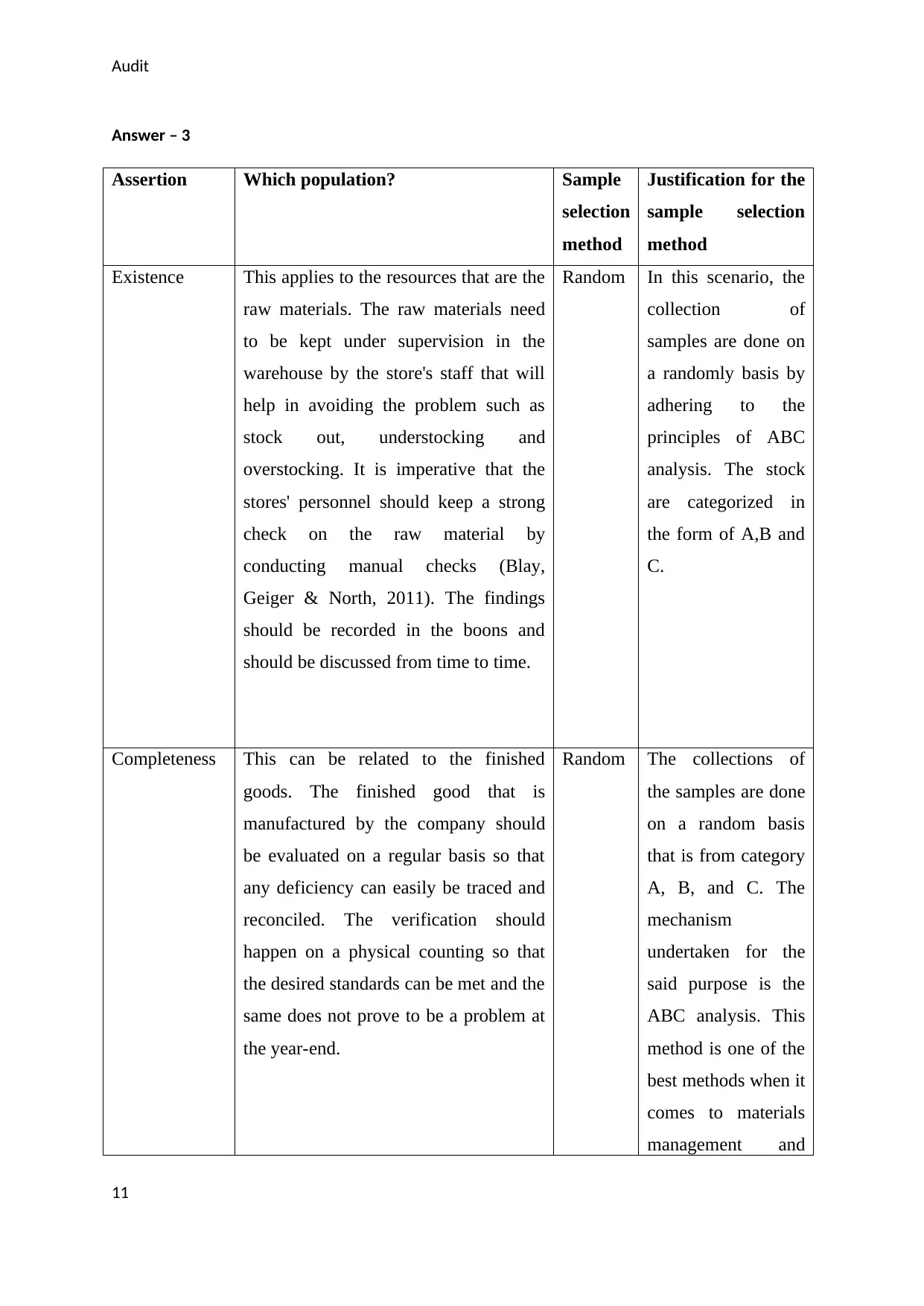

Answer – 3

Assertion Which population? Sample

selection

method

Justification for the

sample selection

method

Existence This applies to the resources that are the

raw materials. The raw materials need

to be kept under supervision in the

warehouse by the store's staff that will

help in avoiding the problem such as

stock out, understocking and

overstocking. It is imperative that the

stores' personnel should keep a strong

check on the raw material by

conducting manual checks (Blay,

Geiger & North, 2011). The findings

should be recorded in the boons and

should be discussed from time to time.

Random In this scenario, the

collection of

samples are done on

a randomly basis by

adhering to the

principles of ABC

analysis. The stock

are categorized in

the form of A,B and

C.

Completeness This can be related to the finished

goods. The finished good that is

manufactured by the company should

be evaluated on a regular basis so that

any deficiency can easily be traced and

reconciled. The verification should

happen on a physical counting so that

the desired standards can be met and the

same does not prove to be a problem at

the year-end.

Random The collections of

the samples are done

on a random basis

that is from category

A, B, and C. The

mechanism

undertaken for the

said purpose is the

ABC analysis. This

method is one of the

best methods when it

comes to materials

management and

11

Answer – 3

Assertion Which population? Sample

selection

method

Justification for the

sample selection

method

Existence This applies to the resources that are the

raw materials. The raw materials need

to be kept under supervision in the

warehouse by the store's staff that will

help in avoiding the problem such as

stock out, understocking and

overstocking. It is imperative that the

stores' personnel should keep a strong

check on the raw material by

conducting manual checks (Blay,

Geiger & North, 2011). The findings

should be recorded in the boons and

should be discussed from time to time.

Random In this scenario, the

collection of

samples are done on

a randomly basis by

adhering to the

principles of ABC

analysis. The stock

are categorized in

the form of A,B and

C.

Completeness This can be related to the finished

goods. The finished good that is

manufactured by the company should

be evaluated on a regular basis so that

any deficiency can easily be traced and

reconciled. The verification should

happen on a physical counting so that

the desired standards can be met and the

same does not prove to be a problem at

the year-end.

Random The collections of

the samples are done

on a random basis

that is from category

A, B, and C. The

mechanism

undertaken for the

said purpose is the

ABC analysis. This

method is one of the

best methods when it

comes to materials

management and

11

Audit

defines the priority

of the segment

(Baldwin, 2010).

12

defines the priority

of the segment

(Baldwin, 2010).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.