Amana Ltd: Performance Analysis and Improvement Recommendations Report

VerifiedAdded on 2023/06/06

|12

|3330

|276

Report

AI Summary

This report presents a management accounting analysis of Amana Ltd, a family-owned souvenir business in England, focusing on its performance in 2020 amidst the pandemic. Part A includes a monthly control report detailing original, flexed, and actual budgets, highlighting variances in sales revenue, variable costs (materials, labor, overheads), and fixed overheads. The analysis reveals unfavorable revenue conditions, primarily due to the pandemic's impact, necessitating adjustments in pricing, volumes, and marketing. Recommendations include adding products, entering forward contracts, providing employee training, and potentially raising prices. Part B compares two online sales options: establishing an own online shop versus selling on Amazon, with a financial analysis favoring the former due to higher guaranteed sales. The report concludes with a recommendation to establish an own online shop for better profitability.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(i) Presenting preparation of monthly control report showing original budget, flexed budget

and variance of Amana Ltd..........................................................................................................3

(ii) Presentation report on the performance of Amana Ltd, as per the control report of the year

2020.............................................................................................................................................5

(iii) Recommendation to Amana Ltd CEO regarding different areas of improvement...............6

PART B...........................................................................................................................................7

Comparative analysis of two options for Amana Ltd..................................................................7

Recommendation to Mr Amana...................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(i) Presenting preparation of monthly control report showing original budget, flexed budget

and variance of Amana Ltd..........................................................................................................3

(ii) Presentation report on the performance of Amana Ltd, as per the control report of the year

2020.............................................................................................................................................5

(iii) Recommendation to Amana Ltd CEO regarding different areas of improvement...............6

PART B...........................................................................................................................................7

Comparative analysis of two options for Amana Ltd..................................................................7

Recommendation to Mr Amana...................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is a vast concept. It basically means the evaluation and also the

communication of the financial information or the financial records to the managers of the

businesses to take the informative decisions efficiently. The concept of management accounting

is different from the concept of financial accounting in particular. The major focus of

management accounting is on the cost as well as the sales information of the particular

organization's commodities in particular. The report below provides information regarding the

company Amana Ltd. A business in England that is owned by a family. The business is mainly

of selling the souvenirs to the travellers in particular. The report highlights the issues the

business has particularly been facing due to the occurrence of the pandemic and this has

impacted the business in various ways which is mainly stated in this report in particular.

PART A

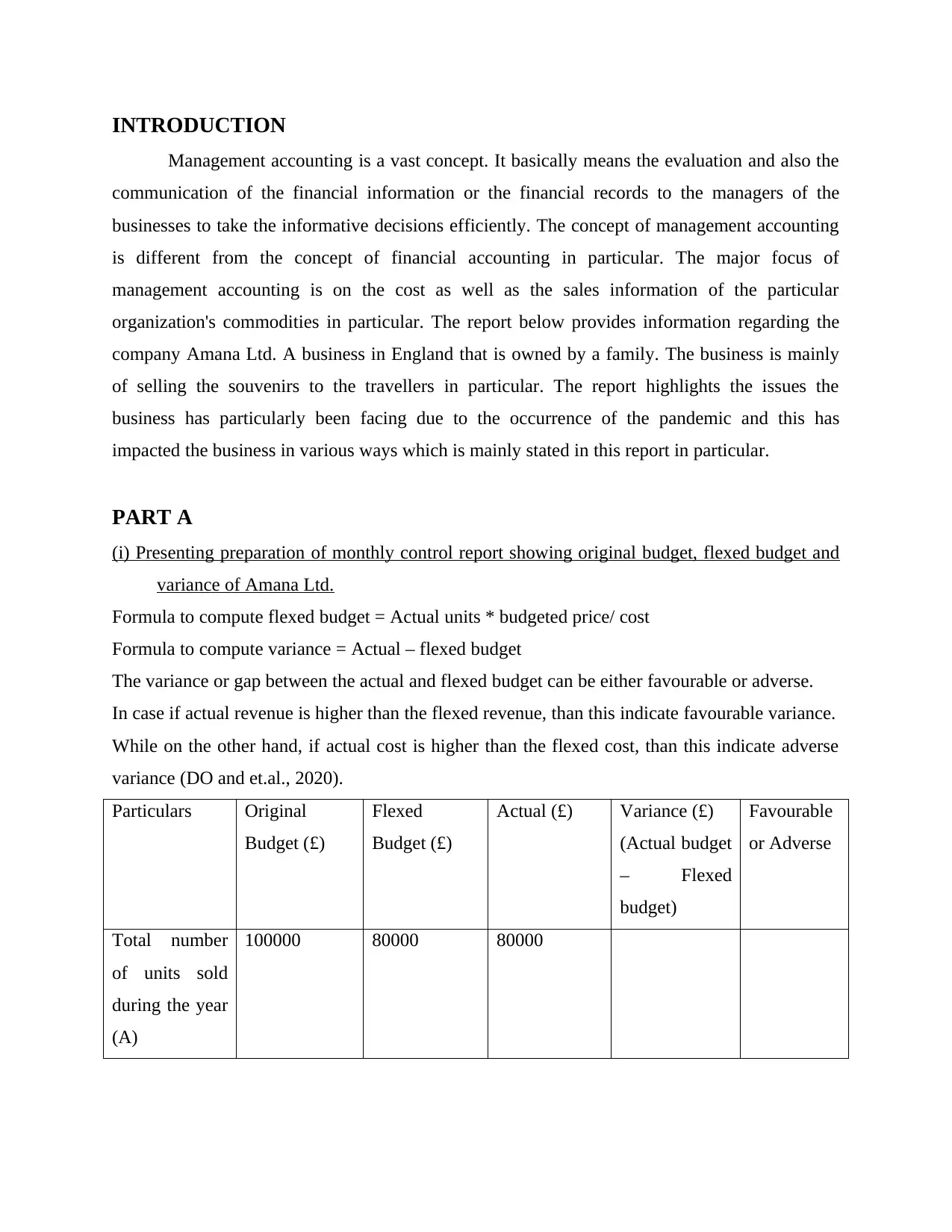

(i) Presenting preparation of monthly control report showing original budget, flexed budget and

variance of Amana Ltd.

Formula to compute flexed budget = Actual units * budgeted price/ cost

Formula to compute variance = Actual – flexed budget

The variance or gap between the actual and flexed budget can be either favourable or adverse.

In case if actual revenue is higher than the flexed revenue, than this indicate favourable variance.

While on the other hand, if actual cost is higher than the flexed cost, than this indicate adverse

variance (DO and et.al., 2020).

Particulars Original

Budget (£)

Flexed

Budget (£)

Actual (£) Variance (£)

(Actual budget

– Flexed

budget)

Favourable

or Adverse

Total number

of units sold

during the year

(A)

100000 80000 80000

Management accounting is a vast concept. It basically means the evaluation and also the

communication of the financial information or the financial records to the managers of the

businesses to take the informative decisions efficiently. The concept of management accounting

is different from the concept of financial accounting in particular. The major focus of

management accounting is on the cost as well as the sales information of the particular

organization's commodities in particular. The report below provides information regarding the

company Amana Ltd. A business in England that is owned by a family. The business is mainly

of selling the souvenirs to the travellers in particular. The report highlights the issues the

business has particularly been facing due to the occurrence of the pandemic and this has

impacted the business in various ways which is mainly stated in this report in particular.

PART A

(i) Presenting preparation of monthly control report showing original budget, flexed budget and

variance of Amana Ltd.

Formula to compute flexed budget = Actual units * budgeted price/ cost

Formula to compute variance = Actual – flexed budget

The variance or gap between the actual and flexed budget can be either favourable or adverse.

In case if actual revenue is higher than the flexed revenue, than this indicate favourable variance.

While on the other hand, if actual cost is higher than the flexed cost, than this indicate adverse

variance (DO and et.al., 2020).

Particulars Original

Budget (£)

Flexed

Budget (£)

Actual (£) Variance (£)

(Actual budget

– Flexed

budget)

Favourable

or Adverse

Total number

of units sold

during the year

(A)

100000 80000 80000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

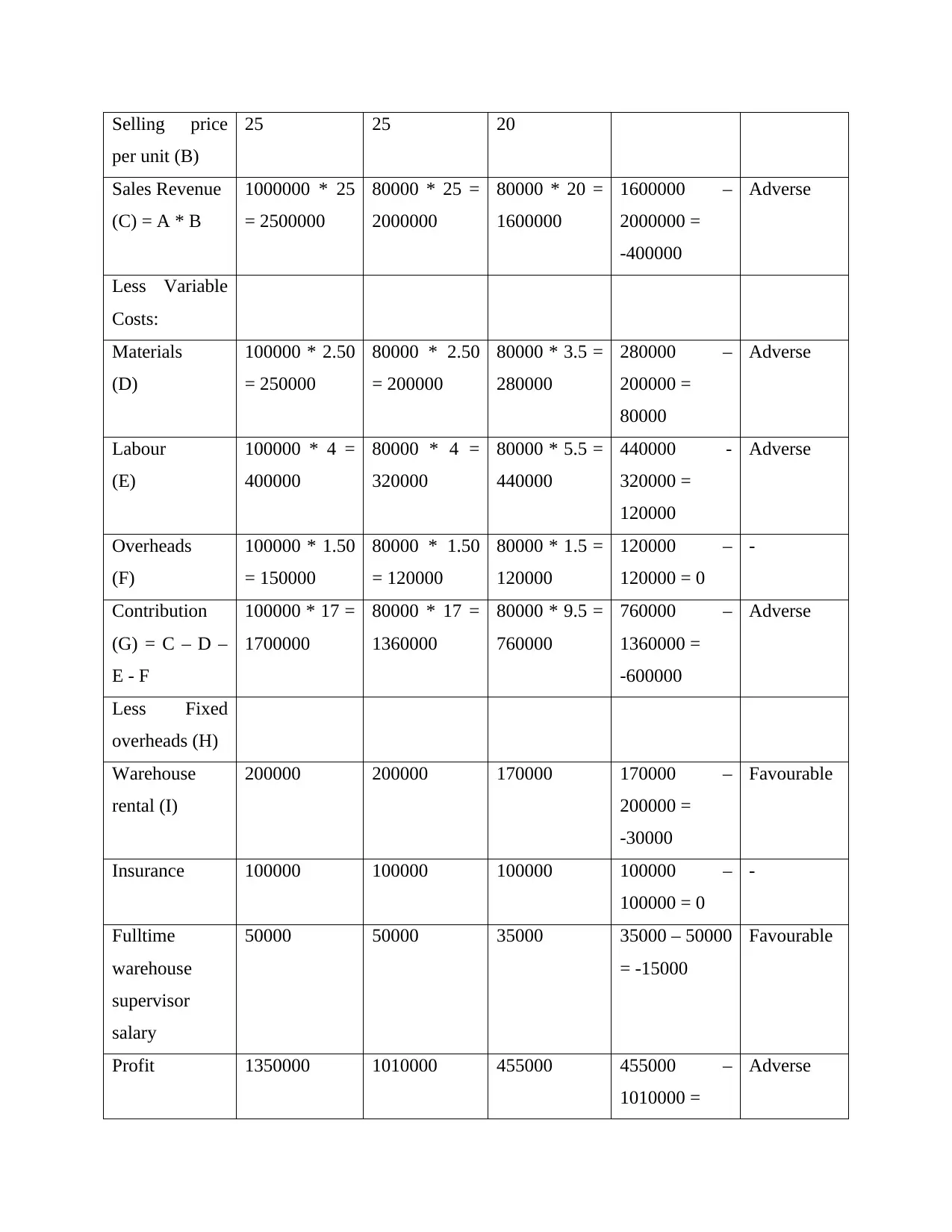

Selling price

per unit (B)

25 25 20

Sales Revenue

(C) = A * B

1000000 * 25

= 2500000

80000 * 25 =

2000000

80000 * 20 =

1600000

1600000 –

2000000 =

-400000

Adverse

Less Variable

Costs:

Materials

(D)

100000 * 2.50

= 250000

80000 * 2.50

= 200000

80000 * 3.5 =

280000

280000 –

200000 =

80000

Adverse

Labour

(E)

100000 * 4 =

400000

80000 * 4 =

320000

80000 * 5.5 =

440000

440000 -

320000 =

120000

Adverse

Overheads

(F)

100000 * 1.50

= 150000

80000 * 1.50

= 120000

80000 * 1.5 =

120000

120000 –

120000 = 0

-

Contribution

(G) = C – D –

E - F

100000 * 17 =

1700000

80000 * 17 =

1360000

80000 * 9.5 =

760000

760000 –

1360000 =

-600000

Adverse

Less Fixed

overheads (H)

Warehouse

rental (I)

200000 200000 170000 170000 –

200000 =

-30000

Favourable

Insurance 100000 100000 100000 100000 –

100000 = 0

-

Fulltime

warehouse

supervisor

salary

50000 50000 35000 35000 – 50000

= -15000

Favourable

Profit 1350000 1010000 455000 455000 –

1010000 =

Adverse

per unit (B)

25 25 20

Sales Revenue

(C) = A * B

1000000 * 25

= 2500000

80000 * 25 =

2000000

80000 * 20 =

1600000

1600000 –

2000000 =

-400000

Adverse

Less Variable

Costs:

Materials

(D)

100000 * 2.50

= 250000

80000 * 2.50

= 200000

80000 * 3.5 =

280000

280000 –

200000 =

80000

Adverse

Labour

(E)

100000 * 4 =

400000

80000 * 4 =

320000

80000 * 5.5 =

440000

440000 -

320000 =

120000

Adverse

Overheads

(F)

100000 * 1.50

= 150000

80000 * 1.50

= 120000

80000 * 1.5 =

120000

120000 –

120000 = 0

-

Contribution

(G) = C – D –

E - F

100000 * 17 =

1700000

80000 * 17 =

1360000

80000 * 9.5 =

760000

760000 –

1360000 =

-600000

Adverse

Less Fixed

overheads (H)

Warehouse

rental (I)

200000 200000 170000 170000 –

200000 =

-30000

Favourable

Insurance 100000 100000 100000 100000 –

100000 = 0

-

Fulltime

warehouse

supervisor

salary

50000 50000 35000 35000 – 50000

= -15000

Favourable

Profit 1350000 1010000 455000 455000 –

1010000 =

Adverse

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

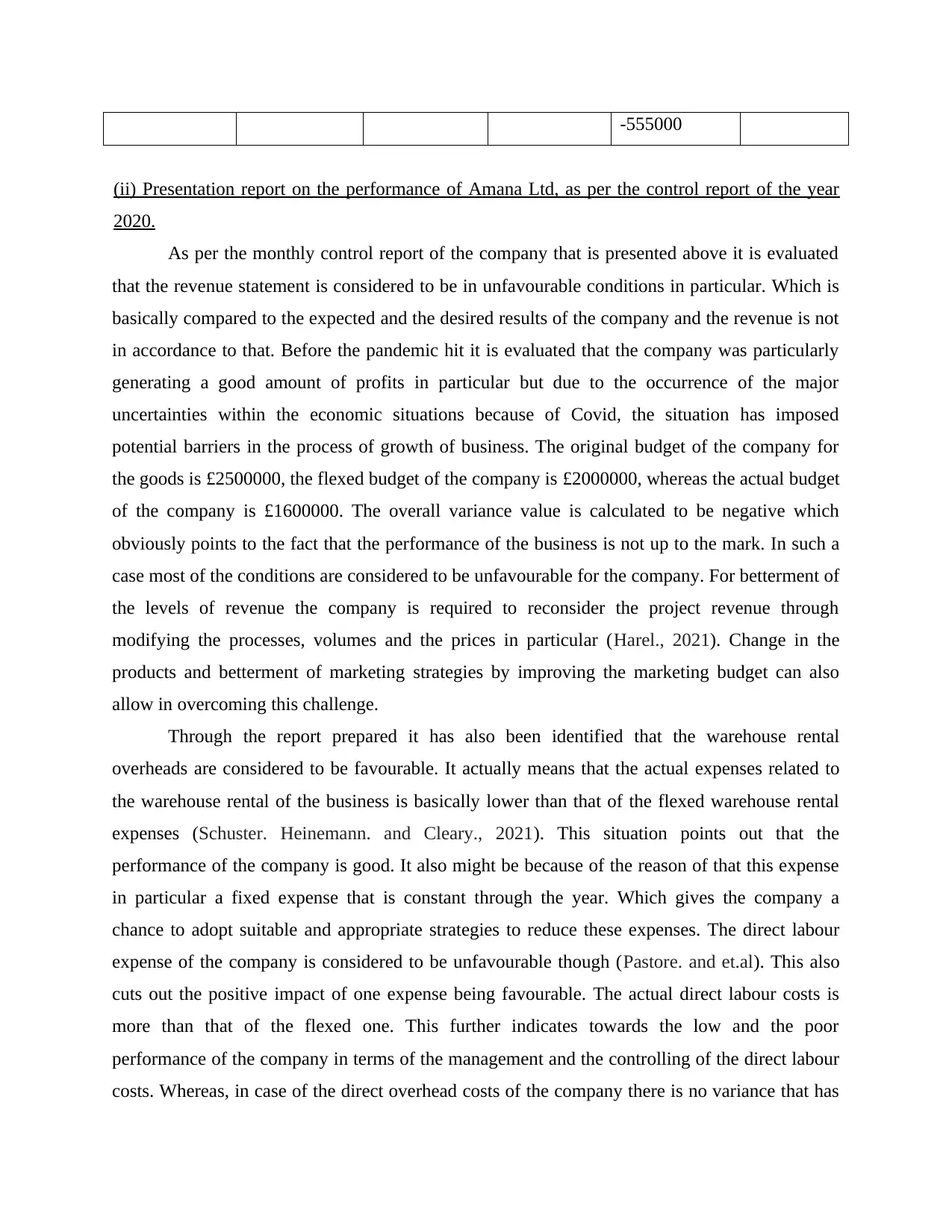

-555000

(ii) Presentation report on the performance of Amana Ltd, as per the control report of the year

2020.

As per the monthly control report of the company that is presented above it is evaluated

that the revenue statement is considered to be in unfavourable conditions in particular. Which is

basically compared to the expected and the desired results of the company and the revenue is not

in accordance to that. Before the pandemic hit it is evaluated that the company was particularly

generating a good amount of profits in particular but due to the occurrence of the major

uncertainties within the economic situations because of Covid, the situation has imposed

potential barriers in the process of growth of business. The original budget of the company for

the goods is £2500000, the flexed budget of the company is £2000000, whereas the actual budget

of the company is £1600000. The overall variance value is calculated to be negative which

obviously points to the fact that the performance of the business is not up to the mark. In such a

case most of the conditions are considered to be unfavourable for the company. For betterment of

the levels of revenue the company is required to reconsider the project revenue through

modifying the processes, volumes and the prices in particular (Harel., 2021). Change in the

products and betterment of marketing strategies by improving the marketing budget can also

allow in overcoming this challenge.

Through the report prepared it has also been identified that the warehouse rental

overheads are considered to be favourable. It actually means that the actual expenses related to

the warehouse rental of the business is basically lower than that of the flexed warehouse rental

expenses (Schuster. Heinemann. and Cleary., 2021). This situation points out that the

performance of the company is good. It also might be because of the reason of that this expense

in particular a fixed expense that is constant through the year. Which gives the company a

chance to adopt suitable and appropriate strategies to reduce these expenses. The direct labour

expense of the company is considered to be unfavourable though (Pastore. and et.al). This also

cuts out the positive impact of one expense being favourable. The actual direct labour costs is

more than that of the flexed one. This further indicates towards the low and the poor

performance of the company in terms of the management and the controlling of the direct labour

costs. Whereas, in case of the direct overhead costs of the company there is no variance that has

(ii) Presentation report on the performance of Amana Ltd, as per the control report of the year

2020.

As per the monthly control report of the company that is presented above it is evaluated

that the revenue statement is considered to be in unfavourable conditions in particular. Which is

basically compared to the expected and the desired results of the company and the revenue is not

in accordance to that. Before the pandemic hit it is evaluated that the company was particularly

generating a good amount of profits in particular but due to the occurrence of the major

uncertainties within the economic situations because of Covid, the situation has imposed

potential barriers in the process of growth of business. The original budget of the company for

the goods is £2500000, the flexed budget of the company is £2000000, whereas the actual budget

of the company is £1600000. The overall variance value is calculated to be negative which

obviously points to the fact that the performance of the business is not up to the mark. In such a

case most of the conditions are considered to be unfavourable for the company. For betterment of

the levels of revenue the company is required to reconsider the project revenue through

modifying the processes, volumes and the prices in particular (Harel., 2021). Change in the

products and betterment of marketing strategies by improving the marketing budget can also

allow in overcoming this challenge.

Through the report prepared it has also been identified that the warehouse rental

overheads are considered to be favourable. It actually means that the actual expenses related to

the warehouse rental of the business is basically lower than that of the flexed warehouse rental

expenses (Schuster. Heinemann. and Cleary., 2021). This situation points out that the

performance of the company is good. It also might be because of the reason of that this expense

in particular a fixed expense that is constant through the year. Which gives the company a

chance to adopt suitable and appropriate strategies to reduce these expenses. The direct labour

expense of the company is considered to be unfavourable though (Pastore. and et.al). This also

cuts out the positive impact of one expense being favourable. The actual direct labour costs is

more than that of the flexed one. This further indicates towards the low and the poor

performance of the company in terms of the management and the controlling of the direct labour

costs. Whereas, in case of the direct overhead costs of the company there is no variance that has

been indicated in the year 2020 in particular. Which again indicates towards the good

performance of the company. As per the evaluation of three major costs or expenses that were

incurred by the company, the major requirement is to do better market evaluation and research

(Portillo. and Stinn., 2018). Also, increase in the levels of focus on the internal control system of

the company for the purpose of meeting the expected standards of budget is required.

The expenses related to the direct materials which is basically the expenses made by the

company to purchase the direct materials for the purpose of production (). This information as

per the control report is also considered to be unfavourable for the company. This is mainly due

to the deficiency in the quality of the market research and also other factors present in the market

that the company is operating within. The original budget or the actual budget of the company

for specifically the direct materials was £250000 as well as the flexed budget was £200000, still

the results that were expected by the company were not achieved. Hence, the company is

required to change the strategies and implement better strategies for the purpose of maintenance

of their position in the market.

Therefore, as per the evaluation of the major factors of the company's financial records

the major requirement of the company is to implement strategies that allow in decreasing the

costs and further improving the sales revenue levels (Bartik. And et.al., 2020). For elimination of

the variance, the major necessities that the company can focus on and implement are, analysis f

every element of budget that are leading to creation of variance. As per the control report the

company has still earned profit during the year but it is less than what was expected by the

company. This variance is majorly occurring due to the pandemic and through the

implementation of the right strategies at the right time it can be eliminated too.

(iii) Recommendation to Amana Ltd CEO regarding different areas of improvement

After analysing the performance of Amana Ltd during the year 2020 using the monthly

control report, it has been identified that there are many areas where company is lacking such as

sales, purchase of material, labour cost maintenance. In order to improve these areas, the

following strategies has been recommended to Amana Ltd are as follows:

Add products and service in portfolio: This is one of the strategy which is recommended

to Amana Ltd. As per this strategy, it is recommended to company that they should

performance of the company. As per the evaluation of three major costs or expenses that were

incurred by the company, the major requirement is to do better market evaluation and research

(Portillo. and Stinn., 2018). Also, increase in the levels of focus on the internal control system of

the company for the purpose of meeting the expected standards of budget is required.

The expenses related to the direct materials which is basically the expenses made by the

company to purchase the direct materials for the purpose of production (). This information as

per the control report is also considered to be unfavourable for the company. This is mainly due

to the deficiency in the quality of the market research and also other factors present in the market

that the company is operating within. The original budget or the actual budget of the company

for specifically the direct materials was £250000 as well as the flexed budget was £200000, still

the results that were expected by the company were not achieved. Hence, the company is

required to change the strategies and implement better strategies for the purpose of maintenance

of their position in the market.

Therefore, as per the evaluation of the major factors of the company's financial records

the major requirement of the company is to implement strategies that allow in decreasing the

costs and further improving the sales revenue levels (Bartik. And et.al., 2020). For elimination of

the variance, the major necessities that the company can focus on and implement are, analysis f

every element of budget that are leading to creation of variance. As per the control report the

company has still earned profit during the year but it is less than what was expected by the

company. This variance is majorly occurring due to the pandemic and through the

implementation of the right strategies at the right time it can be eliminated too.

(iii) Recommendation to Amana Ltd CEO regarding different areas of improvement

After analysing the performance of Amana Ltd during the year 2020 using the monthly

control report, it has been identified that there are many areas where company is lacking such as

sales, purchase of material, labour cost maintenance. In order to improve these areas, the

following strategies has been recommended to Amana Ltd are as follows:

Add products and service in portfolio: This is one of the strategy which is recommended

to Amana Ltd. As per this strategy, it is recommended to company that they should

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

include more products as well as services in their product portfolio in order to cover large

market or customer demand. By adding different products and services in the portfolio,

Amana Ltd able to solve attract more customer all over the world (Jovanović, Dražić-

Lutilsky and Vašiček, 2019). The impact of which overall sales revenue of company will

improve without increasing the selling price of products and services.

Enter into forward contract: This is another strategic action advisable to Amana Ltd

under which the company need to enter in a forward agreement with the suppliers of raw

material. It will help the company to deal with the issue regarding increase in price of raw

material. In this strategy, Amana Ltd is required to set a price at which they will purchase

the raw material from supplier in future as well with mutual agreement.

Provide proper training and development session: This is also one of the strategy which

indicate that Amana Ltd should provide proper training and development program to its

employees in order to keep them motivated. The impact of which the overall efficiency

and productivity of employee will enhance and the cost of wastage of resources will

reduce (Jermsittiparsert, 2020). Hence, to maintain and control the labour cost at

workplace, the company should adopt and implement this strategy.

Raising prices of products: The increase in the price of goods and services will

ultimately increase the sales revenue of the company which helps in the overall budget

maintenance. As per this strategy, the company is required to do proper market analysis

with the help of which company such as Amana Ltd can identify the rate through which

they can enhance its prices of products as well as services. However, this strategy can

affect the company in term of customer loss.

PART B

Comparative analysis of two options for Amana Ltd

Option 1: Own online shop setting

Particulars Amount in £

No of units will be sold by company

(Guaranteed)

£2000000

(100000 * £20)

Less: Relevant costs associated with option

setting up own online shop:

market or customer demand. By adding different products and services in the portfolio,

Amana Ltd able to solve attract more customer all over the world (Jovanović, Dražić-

Lutilsky and Vašiček, 2019). The impact of which overall sales revenue of company will

improve without increasing the selling price of products and services.

Enter into forward contract: This is another strategic action advisable to Amana Ltd

under which the company need to enter in a forward agreement with the suppliers of raw

material. It will help the company to deal with the issue regarding increase in price of raw

material. In this strategy, Amana Ltd is required to set a price at which they will purchase

the raw material from supplier in future as well with mutual agreement.

Provide proper training and development session: This is also one of the strategy which

indicate that Amana Ltd should provide proper training and development program to its

employees in order to keep them motivated. The impact of which the overall efficiency

and productivity of employee will enhance and the cost of wastage of resources will

reduce (Jermsittiparsert, 2020). Hence, to maintain and control the labour cost at

workplace, the company should adopt and implement this strategy.

Raising prices of products: The increase in the price of goods and services will

ultimately increase the sales revenue of the company which helps in the overall budget

maintenance. As per this strategy, the company is required to do proper market analysis

with the help of which company such as Amana Ltd can identify the rate through which

they can enhance its prices of products as well as services. However, this strategy can

affect the company in term of customer loss.

PART B

Comparative analysis of two options for Amana Ltd

Option 1: Own online shop setting

Particulars Amount in £

No of units will be sold by company

(Guaranteed)

£2000000

(100000 * £20)

Less: Relevant costs associated with option

setting up own online shop:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

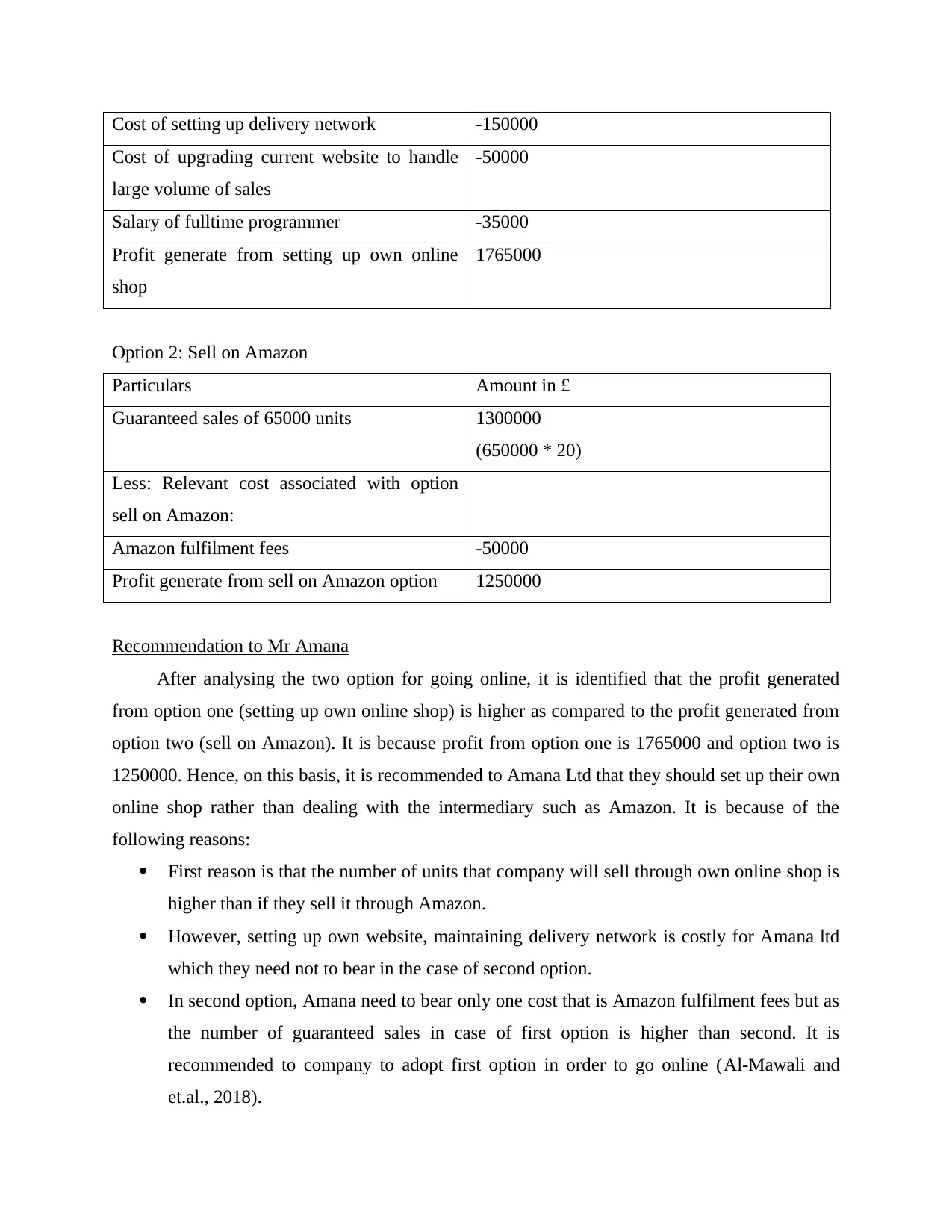

Cost of setting up delivery network -150000

Cost of upgrading current website to handle

large volume of sales

-50000

Salary of fulltime programmer -35000

Profit generate from setting up own online

shop

1765000

Option 2: Sell on Amazon

Particulars Amount in £

Guaranteed sales of 65000 units 1300000

(650000 * 20)

Less: Relevant cost associated with option

sell on Amazon:

Amazon fulfilment fees -50000

Profit generate from sell on Amazon option 1250000

Recommendation to Mr Amana

After analysing the two option for going online, it is identified that the profit generated

from option one (setting up own online shop) is higher as compared to the profit generated from

option two (sell on Amazon). It is because profit from option one is 1765000 and option two is

1250000. Hence, on this basis, it is recommended to Amana Ltd that they should set up their own

online shop rather than dealing with the intermediary such as Amazon. It is because of the

following reasons:

First reason is that the number of units that company will sell through own online shop is

higher than if they sell it through Amazon.

However, setting up own website, maintaining delivery network is costly for Amana ltd

which they need not to bear in the case of second option.

In second option, Amana need to bear only one cost that is Amazon fulfilment fees but as

the number of guaranteed sales in case of first option is higher than second. It is

recommended to company to adopt first option in order to go online (Al-Mawali and

et.al., 2018).

Cost of upgrading current website to handle

large volume of sales

-50000

Salary of fulltime programmer -35000

Profit generate from setting up own online

shop

1765000

Option 2: Sell on Amazon

Particulars Amount in £

Guaranteed sales of 65000 units 1300000

(650000 * 20)

Less: Relevant cost associated with option

sell on Amazon:

Amazon fulfilment fees -50000

Profit generate from sell on Amazon option 1250000

Recommendation to Mr Amana

After analysing the two option for going online, it is identified that the profit generated

from option one (setting up own online shop) is higher as compared to the profit generated from

option two (sell on Amazon). It is because profit from option one is 1765000 and option two is

1250000. Hence, on this basis, it is recommended to Amana Ltd that they should set up their own

online shop rather than dealing with the intermediary such as Amazon. It is because of the

following reasons:

First reason is that the number of units that company will sell through own online shop is

higher than if they sell it through Amazon.

However, setting up own website, maintaining delivery network is costly for Amana ltd

which they need not to bear in the case of second option.

In second option, Amana need to bear only one cost that is Amazon fulfilment fees but as

the number of guaranteed sales in case of first option is higher than second. It is

recommended to company to adopt first option in order to go online (Al-Mawali and

et.al., 2018).

To critically justify the decision recommended to Amana Ltd, it is important that Amana should

understand the advantage as well as disadvantage of both option.

Benefits of setting own online shop:

Fastest buying process: This is one of the biggest advantage of setting own online shop

to Amana Ltd. It is because it provides company to take fast orders of customer and

complete it quickly. This strategy is best to keep customers happy and satisfied

throughout the buying process.

Access to customer information: In order to access the important information regarding

the customers such as customer order rate, highly preferred product etc. the setting up

own online store is best (Alhatabat 2020). It will also help the management of Amana to

understand the taste and preferences of customer.

Affordable advertising and marketing options: Setting own online store provide the

company with the different options regarding advertising and marketing options. This

options are easily affordable to small and medium size organizations. Hence, setting

online store is highly recommendable to Amana Ltd in the present scenario. Fastest

response to customer query is also one of the benefit.

Drawback of setting own online shop:

High cost: The high cost of setting own online store is a drawback for the Amana ltd if

they follow first option. It is because in case if the company fails to generate appropriate

return from this source, in that case the high investment in first option will vanish the

reputation of company (Alhatabat, 2020).

Low sales during a site crash: In case of setting up online store, a site crash is the major

issue that Amana company will face. The impact of which customer unable to place an

order which ultimately result into the loss of order and lower sales revenue.

Benefit of selling through Amazon:

Helpful in identifying the buyers all over the world: It means that, with the help of

selling the products and services through Amazon, company able to identify the

understand the advantage as well as disadvantage of both option.

Benefits of setting own online shop:

Fastest buying process: This is one of the biggest advantage of setting own online shop

to Amana Ltd. It is because it provides company to take fast orders of customer and

complete it quickly. This strategy is best to keep customers happy and satisfied

throughout the buying process.

Access to customer information: In order to access the important information regarding

the customers such as customer order rate, highly preferred product etc. the setting up

own online store is best (Alhatabat 2020). It will also help the management of Amana to

understand the taste and preferences of customer.

Affordable advertising and marketing options: Setting own online store provide the

company with the different options regarding advertising and marketing options. This

options are easily affordable to small and medium size organizations. Hence, setting

online store is highly recommendable to Amana Ltd in the present scenario. Fastest

response to customer query is also one of the benefit.

Drawback of setting own online shop:

High cost: The high cost of setting own online store is a drawback for the Amana ltd if

they follow first option. It is because in case if the company fails to generate appropriate

return from this source, in that case the high investment in first option will vanish the

reputation of company (Alhatabat, 2020).

Low sales during a site crash: In case of setting up online store, a site crash is the major

issue that Amana company will face. The impact of which customer unable to place an

order which ultimately result into the loss of order and lower sales revenue.

Benefit of selling through Amazon:

Helpful in identifying the buyers all over the world: It means that, with the help of

selling the products and services through Amazon, company able to identify the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

customers from all over the world. This will ultimately enhance the international

customer base for the company.

Minimum cost: The strategy of choosing Amazon as an intermediary for moving the

business online, will help Amana Ltd to keep the markets working smoothly. Also, it will

help the company create share value and spread the name of company not only in

domestic but also in foreign countries (PHORNLAPHATRACHAKORN and

PEEMANEE, 2020). The company can save logistic or transportation cost.

Drawback of selling through Amazon:

Massive competition: One of the major drawback of opting second option that is sell on

Amazon is massive competition. It means there are many other companies that involve in

the selling through Amazon to reach larger customer base. Hence, the high level of

competition is one of the major drawback for Amana if they opt for second option.

Limited personalised options: This strategy provides very limited personalized options to

their customers (Tashakor Appuhami and Munir, 2019). The impact of which company

unable to assess the taste and preferences of its customer with the aim to enhance the

customer satisfaction.

CONCLUSION

This report in particular concludes that it is necessary and essential for a company to have

proper and efficient management accounting which supports the growth decisions of the business

and sue to this it becomes easy for the companies to compare the actual performance and the

future objectives of the company in particular. The above report has particularly illustrated

regarding the topic related to the requirement and the relevance of management accounting. The

report provides information regarding the monthly control report of the business and then further

analyses of the overall control report is done in the report above. The report also provides

information regarding the ways through which the aspects the company is lacking behind in can

be covered and taken care of.

customer base for the company.

Minimum cost: The strategy of choosing Amazon as an intermediary for moving the

business online, will help Amana Ltd to keep the markets working smoothly. Also, it will

help the company create share value and spread the name of company not only in

domestic but also in foreign countries (PHORNLAPHATRACHAKORN and

PEEMANEE, 2020). The company can save logistic or transportation cost.

Drawback of selling through Amazon:

Massive competition: One of the major drawback of opting second option that is sell on

Amazon is massive competition. It means there are many other companies that involve in

the selling through Amazon to reach larger customer base. Hence, the high level of

competition is one of the major drawback for Amana if they opt for second option.

Limited personalised options: This strategy provides very limited personalized options to

their customers (Tashakor Appuhami and Munir, 2019). The impact of which company

unable to assess the taste and preferences of its customer with the aim to enhance the

customer satisfaction.

CONCLUSION

This report in particular concludes that it is necessary and essential for a company to have

proper and efficient management accounting which supports the growth decisions of the business

and sue to this it becomes easy for the companies to compare the actual performance and the

future objectives of the company in particular. The above report has particularly illustrated

regarding the topic related to the requirement and the relevance of management accounting. The

report provides information regarding the monthly control report of the business and then further

analyses of the overall control report is done in the report above. The report also provides

information regarding the ways through which the aspects the company is lacking behind in can

be covered and taken care of.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Alhatabat, Z., 2020. The impact of ERP system's adoption on management accounting practices

in the Jordanian manufacturing companies. International Journal of Business Information

Systems. 33(2). pp.267-284.

Al-Mawali, H. and et.al., 2018. Environmental strategy, environmental management accounting

and organizational performance: Evidence from The United Arab Emirates

Market. Journal of Environmental Accounting and Management. 6(2). pp.105-114.

Bartik, A.W. And et.al., 2020. The impact of COVID-19 on small business outcomes and

expectations. Proceedings of the national academy of sciences. 117(30). pp.17656-

DO, T. H. and et.al., 2020. Relationship between the management accounting information usage,

market orientation and performance: Evidence from Vietnamese tourism firms. The

Journal of Asian Finance, Economics and Business. 7(10). pp.707-716.

Harel, R., 2021. The impact of COVID-19 on small businesses’ performance and innovation.

Global Business Review. p.09721509211039145.

Jermsittiparsert, K., 2020. Factors affecting firm's energy efficiency and environmental

performance: the role of environmental management accounting, green innovation and

environmental proactivity. 670216917.

Jovanović, T., Dražić-Lutilsky, I. and Vašiček, D., 2019. Implementation of cost accounting as

the economic pillar of management accounting systems in public hospitals–the case of

Slovenia and Croatia. Economic research-Ekonomska istraživanja. 32(1). pp.3754-3772.

Pastore, R. and et.al., Differential Variance Analysis.

PHORNLAPHATRACHAKORN, K. and PEEMANEE, J., 2020. Integrated performance

measurement as a strategic management accounting approach: A case of beverage

businesses in Thailand. The Journal of Asian Finance, Economics and Business. 7(8).

pp.247-257.

Portillo, J.E. and Stinn, J., 2018. Overhead aversion: Do some types of overhead matter more

than others?. Journal of behavioral and experimental economics. 72. pp.40-50.

Schuster, P., Heinemann, M. and Cleary, P., 2021. Variance Analysis and Control. In

Management Accounting (pp. 173-214). Springer, Cham.

Tashakor, S., Appuhami, R. and Munir, R., 2019. Environmental management accounting

practices in Australian cotton farming: the use of the theory of planned

behaviour. Accounting, Auditing & Accountability Journal.

1

Books and journals

Alhatabat, Z., 2020. The impact of ERP system's adoption on management accounting practices

in the Jordanian manufacturing companies. International Journal of Business Information

Systems. 33(2). pp.267-284.

Al-Mawali, H. and et.al., 2018. Environmental strategy, environmental management accounting

and organizational performance: Evidence from The United Arab Emirates

Market. Journal of Environmental Accounting and Management. 6(2). pp.105-114.

Bartik, A.W. And et.al., 2020. The impact of COVID-19 on small business outcomes and

expectations. Proceedings of the national academy of sciences. 117(30). pp.17656-

DO, T. H. and et.al., 2020. Relationship between the management accounting information usage,

market orientation and performance: Evidence from Vietnamese tourism firms. The

Journal of Asian Finance, Economics and Business. 7(10). pp.707-716.

Harel, R., 2021. The impact of COVID-19 on small businesses’ performance and innovation.

Global Business Review. p.09721509211039145.

Jermsittiparsert, K., 2020. Factors affecting firm's energy efficiency and environmental

performance: the role of environmental management accounting, green innovation and

environmental proactivity. 670216917.

Jovanović, T., Dražić-Lutilsky, I. and Vašiček, D., 2019. Implementation of cost accounting as

the economic pillar of management accounting systems in public hospitals–the case of

Slovenia and Croatia. Economic research-Ekonomska istraživanja. 32(1). pp.3754-3772.

Pastore, R. and et.al., Differential Variance Analysis.

PHORNLAPHATRACHAKORN, K. and PEEMANEE, J., 2020. Integrated performance

measurement as a strategic management accounting approach: A case of beverage

businesses in Thailand. The Journal of Asian Finance, Economics and Business. 7(8).

pp.247-257.

Portillo, J.E. and Stinn, J., 2018. Overhead aversion: Do some types of overhead matter more

than others?. Journal of behavioral and experimental economics. 72. pp.40-50.

Schuster, P., Heinemann, M. and Cleary, P., 2021. Variance Analysis and Control. In

Management Accounting (pp. 173-214). Springer, Cham.

Tashakor, S., Appuhami, R. and Munir, R., 2019. Environmental management accounting

practices in Australian cotton farming: the use of the theory of planned

behaviour. Accounting, Auditing & Accountability Journal.

1

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.