Management Accounting Report: Amana Ltd. Performance Analysis

VerifiedAdded on 2022/12/05

|10

|2540

|155

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Amana Ltd., a tourist business in England. The report begins with an introduction emphasizing the importance of management accounting in decision-making, planning, and performance monitoring. It then presents a detailed cost report, comparing original, flexed, and actual budgets, highlighting variances and their impact. The performance evaluation section discusses the effects of the COVID-19 pandemic on the company's revenue and profitability, including an analysis of unfavorable variances and their causes. The report offers recommendations for managing the budget, focusing on key performance indicators, cost-cutting strategies, and adapting to changing market conditions. Task 2 examines the company's options for online sales, comparing the costs and potential benefits of upgrading its website versus registering with Amazon, ultimately recommending the latter for its lower cost and potential for quicker revenue generation. The conclusion reiterates the importance of cost and accounting management and the impact of uncontrollable factors on the company's budget, while emphasizing the need for strategic decision-making and adaptation in a dynamic business environment.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction-................................................................................................................................................3

Task 1-.........................................................................................................................................................3

Task 2-.........................................................................................................................................................5

Conclusion-.................................................................................................................................................6

References-..................................................................................................................................................8

Introduction-................................................................................................................................................3

Task 1-.........................................................................................................................................................3

Task 2-.........................................................................................................................................................5

Conclusion-.................................................................................................................................................6

References-..................................................................................................................................................8

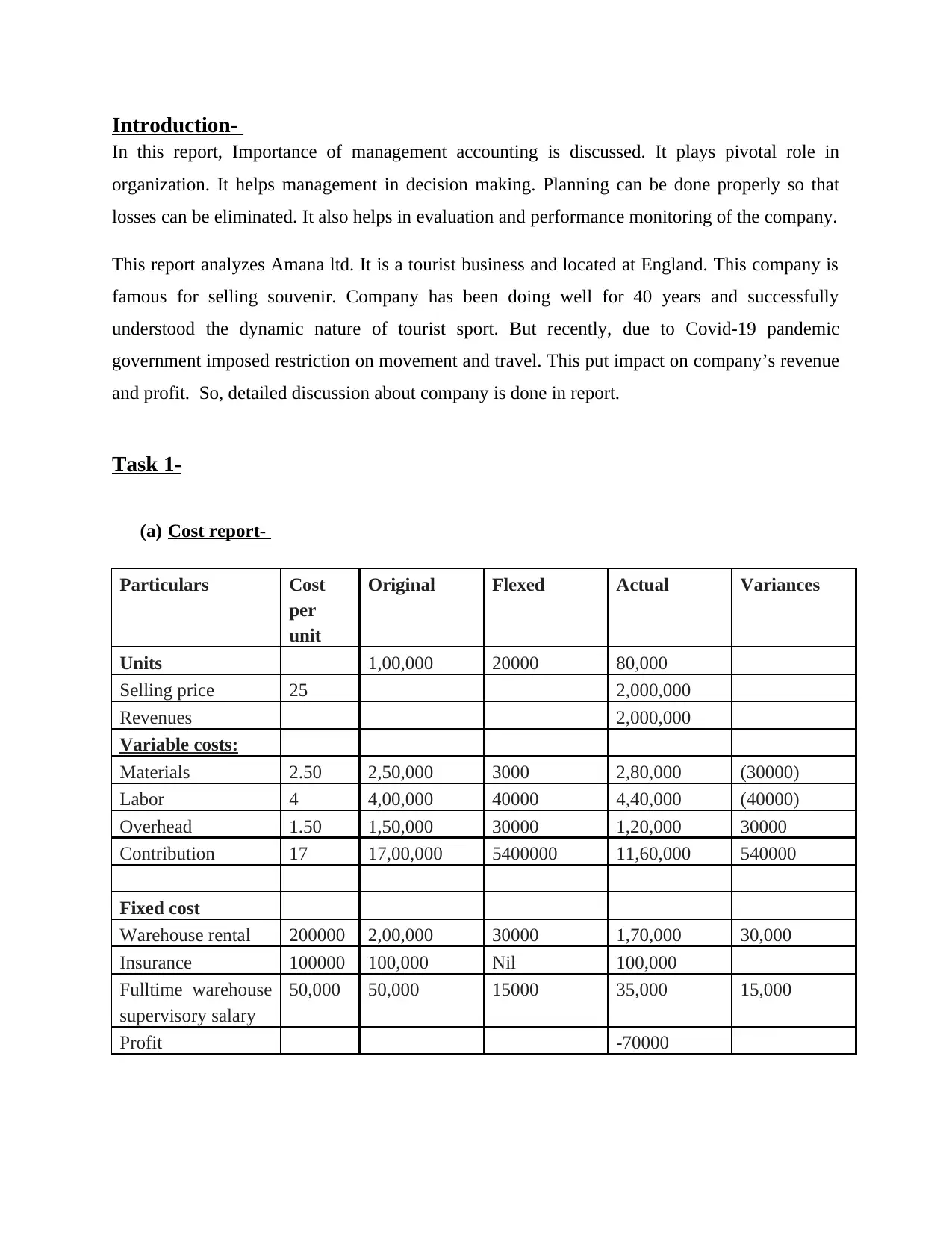

Introduction-

In this report, Importance of management accounting is discussed. It plays pivotal role in

organization. It helps management in decision making. Planning can be done properly so that

losses can be eliminated. It also helps in evaluation and performance monitoring of the company.

This report analyzes Amana ltd. It is a tourist business and located at England. This company is

famous for selling souvenir. Company has been doing well for 40 years and successfully

understood the dynamic nature of tourist sport. But recently, due to Covid-19 pandemic

government imposed restriction on movement and travel. This put impact on company’s revenue

and profit. So, detailed discussion about company is done in report.

Task 1-

(a) Cost report-

Particulars Cost

per

unit

Original Flexed Actual Variances

Units 1,00,000 20000 80,000

Selling price 25 2,000,000

Revenues 2,000,000

Variable costs:

Materials 2.50 2,50,000 3000 2,80,000 (30000)

Labor 4 4,00,000 40000 4,40,000 (40000)

Overhead 1.50 1,50,000 30000 1,20,000 30000

Contribution 17 17,00,000 5400000 11,60,000 540000

Fixed cost

Warehouse rental 200000 2,00,000 30000 1,70,000 30,000

Insurance 100000 100,000 Nil 100,000

Fulltime warehouse

supervisory salary

50,000 50,000 15000 35,000 15,000

Profit -70000

In this report, Importance of management accounting is discussed. It plays pivotal role in

organization. It helps management in decision making. Planning can be done properly so that

losses can be eliminated. It also helps in evaluation and performance monitoring of the company.

This report analyzes Amana ltd. It is a tourist business and located at England. This company is

famous for selling souvenir. Company has been doing well for 40 years and successfully

understood the dynamic nature of tourist sport. But recently, due to Covid-19 pandemic

government imposed restriction on movement and travel. This put impact on company’s revenue

and profit. So, detailed discussion about company is done in report.

Task 1-

(a) Cost report-

Particulars Cost

per

unit

Original Flexed Actual Variances

Units 1,00,000 20000 80,000

Selling price 25 2,000,000

Revenues 2,000,000

Variable costs:

Materials 2.50 2,50,000 3000 2,80,000 (30000)

Labor 4 4,00,000 40000 4,40,000 (40000)

Overhead 1.50 1,50,000 30000 1,20,000 30000

Contribution 17 17,00,000 5400000 11,60,000 540000

Fixed cost

Warehouse rental 200000 2,00,000 30000 1,70,000 30,000

Insurance 100000 100,000 Nil 100,000

Fulltime warehouse

supervisory salary

50,000 50,000 15000 35,000 15,000

Profit -70000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

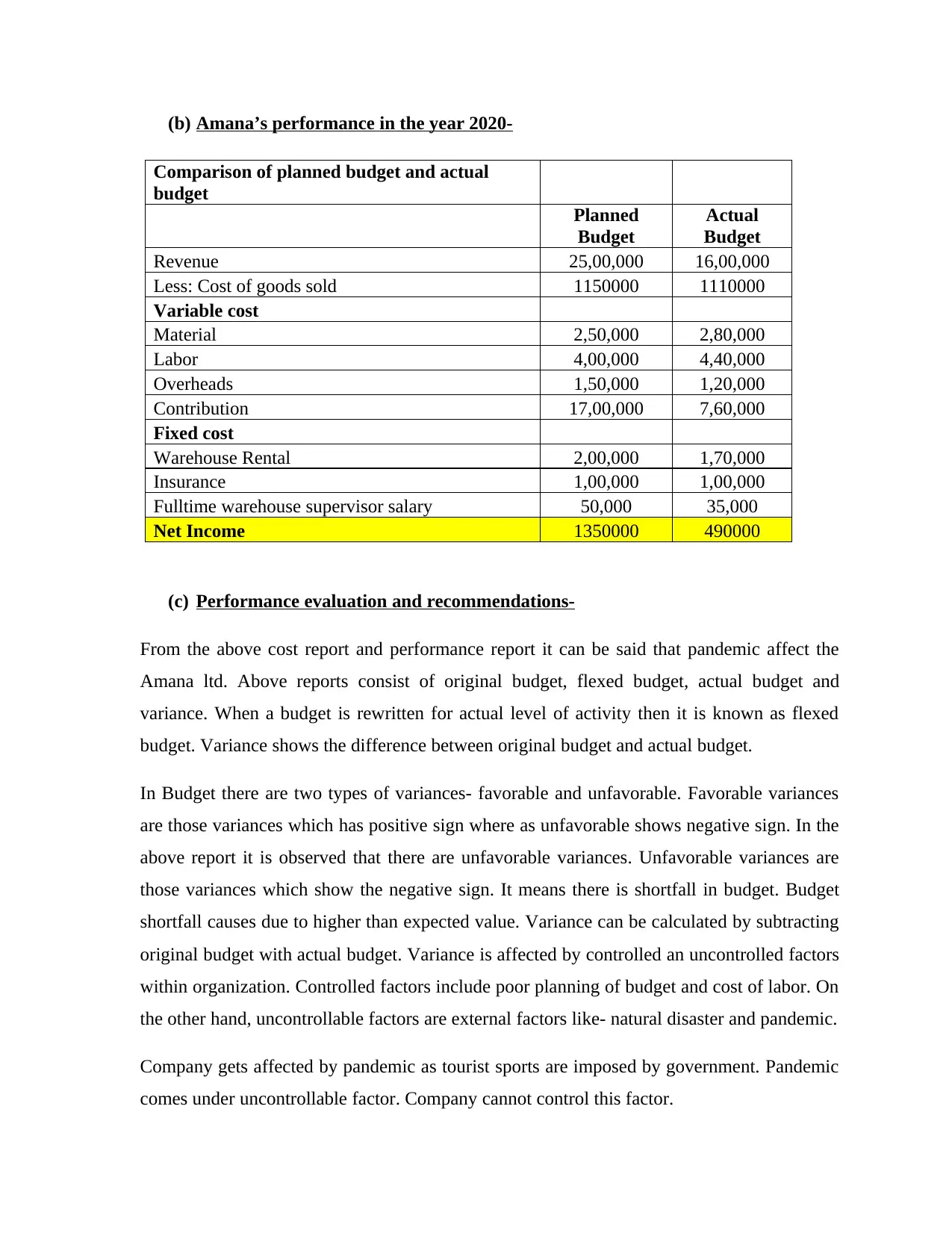

(b) Amana’s performance in the year 2020-

Comparison of planned budget and actual

budget

Planned

Budget

Actual

Budget

Revenue 25,00,000 16,00,000

Less: Cost of goods sold 1150000 1110000

Variable cost

Material 2,50,000 2,80,000

Labor 4,00,000 4,40,000

Overheads 1,50,000 1,20,000

Contribution 17,00,000 7,60,000

Fixed cost

Warehouse Rental 2,00,000 1,70,000

Insurance 1,00,000 1,00,000

Fulltime warehouse supervisor salary 50,000 35,000

Net Income 1350000 490000

(c) Performance evaluation and recommendations-

From the above cost report and performance report it can be said that pandemic affect the

Amana ltd. Above reports consist of original budget, flexed budget, actual budget and

variance. When a budget is rewritten for actual level of activity then it is known as flexed

budget. Variance shows the difference between original budget and actual budget.

In Budget there are two types of variances- favorable and unfavorable. Favorable variances

are those variances which has positive sign where as unfavorable shows negative sign. In the

above report it is observed that there are unfavorable variances. Unfavorable variances are

those variances which show the negative sign. It means there is shortfall in budget. Budget

shortfall causes due to higher than expected value. Variance can be calculated by subtracting

original budget with actual budget. Variance is affected by controlled an uncontrolled factors

within organization. Controlled factors include poor planning of budget and cost of labor. On

the other hand, uncontrollable factors are external factors like- natural disaster and pandemic.

Company gets affected by pandemic as tourist sports are imposed by government. Pandemic

comes under uncontrollable factor. Company cannot control this factor.

Comparison of planned budget and actual

budget

Planned

Budget

Actual

Budget

Revenue 25,00,000 16,00,000

Less: Cost of goods sold 1150000 1110000

Variable cost

Material 2,50,000 2,80,000

Labor 4,00,000 4,40,000

Overheads 1,50,000 1,20,000

Contribution 17,00,000 7,60,000

Fixed cost

Warehouse Rental 2,00,000 1,70,000

Insurance 1,00,000 1,00,000

Fulltime warehouse supervisor salary 50,000 35,000

Net Income 1350000 490000

(c) Performance evaluation and recommendations-

From the above cost report and performance report it can be said that pandemic affect the

Amana ltd. Above reports consist of original budget, flexed budget, actual budget and

variance. When a budget is rewritten for actual level of activity then it is known as flexed

budget. Variance shows the difference between original budget and actual budget.

In Budget there are two types of variances- favorable and unfavorable. Favorable variances

are those variances which has positive sign where as unfavorable shows negative sign. In the

above report it is observed that there are unfavorable variances. Unfavorable variances are

those variances which show the negative sign. It means there is shortfall in budget. Budget

shortfall causes due to higher than expected value. Variance can be calculated by subtracting

original budget with actual budget. Variance is affected by controlled an uncontrolled factors

within organization. Controlled factors include poor planning of budget and cost of labor. On

the other hand, uncontrollable factors are external factors like- natural disaster and pandemic.

Company gets affected by pandemic as tourist sports are imposed by government. Pandemic

comes under uncontrollable factor. Company cannot control this factor.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the performance report, it is observed that actual income is less than planned budget.

Units price in the year 2020 are less than planning and also units produced in the year is less

than expected. This thing affected the whole revenue.

Variable cost and fixed cost are considered in making budget. Variable cost can be defined as

it changes in proportion to production or sales. On the other hand fixed cost does not change

with the change in production or sales. Like- rent, insurance etc.

In the report, there are three types of variable costs included which are material, labor and

overheads. In fixed cost it includes warehouse rental, insurance and salary of the employees

and workers. Contribution can be calculated by revenue minus variable cost. There is huge

difference in contribution of planned and actual budget. Planned budget’s contribution is

17,60,000 whereas contribution of actual budget is 7,00,000. Main cause of this difference is

covid-19 pandemic. Due to pandemic there is increase in material cost and labor cost also

increased because company is not able to find workers. And this thing affected income

earned by company.

Recommendations-

In this hard time company needs to indentify the changes and should manage them

accordingly. Change in net income impacts the stakeholders. So, company needs to

keep them up to date regarding total sales and profit earned by the company.

Company also needs to share details of change in management to share holders.

Company can effectively manage its budget if company focuses on key performance

indicators. Key performance indicators help in determining that how much planned

budget is different from the actual budget. There are some KPI’s which are used in

budget management such as- actual cost, cost variance, earned value, planned value

and return on investment.

A company which is running without budget management often leads to failure. After

doing budget management it is also necessary for the company to manage it

frequently. If budget is overrunning up to 10% then it is controllable for the company.

But if budget is overrunning up to 50% then it cannot be controlled by the company

Units price in the year 2020 are less than planning and also units produced in the year is less

than expected. This thing affected the whole revenue.

Variable cost and fixed cost are considered in making budget. Variable cost can be defined as

it changes in proportion to production or sales. On the other hand fixed cost does not change

with the change in production or sales. Like- rent, insurance etc.

In the report, there are three types of variable costs included which are material, labor and

overheads. In fixed cost it includes warehouse rental, insurance and salary of the employees

and workers. Contribution can be calculated by revenue minus variable cost. There is huge

difference in contribution of planned and actual budget. Planned budget’s contribution is

17,60,000 whereas contribution of actual budget is 7,00,000. Main cause of this difference is

covid-19 pandemic. Due to pandemic there is increase in material cost and labor cost also

increased because company is not able to find workers. And this thing affected income

earned by company.

Recommendations-

In this hard time company needs to indentify the changes and should manage them

accordingly. Change in net income impacts the stakeholders. So, company needs to

keep them up to date regarding total sales and profit earned by the company.

Company also needs to share details of change in management to share holders.

Company can effectively manage its budget if company focuses on key performance

indicators. Key performance indicators help in determining that how much planned

budget is different from the actual budget. There are some KPI’s which are used in

budget management such as- actual cost, cost variance, earned value, planned value

and return on investment.

A company which is running without budget management often leads to failure. After

doing budget management it is also necessary for the company to manage it

frequently. If budget is overrunning up to 10% then it is controllable for the company.

But if budget is overrunning up to 50% then it cannot be controlled by the company

and organization may faces losses in future. Hence, budget management plays an

important role in company.

To maintain company’s presence it needs to focus on cost cutting. Cost cutting can be

done by 5 ways which are as follows-

Suspension of bill- It includes Loans, rent, credit cards and suppliers. Company

needs to contact banks and lenders so that they can suspend their payment. Before

postponing the bills, company should understand the suspension period, repayment

due date and interest rates. Company should ask their landlord for suspension about

payment. Company needs to talk with suppliers about the negotiation in prices of

material.

Reduced unnecessary expenses- Cost cutting can be done by reducing unnecessary

spending. It includes equipments taken on lease, Travelling, Office space and

software.

Payroll spending- It is counted under largest expense of the company. Company can

terminate some employees to save money. Instead of terminating employees company

needs to think about innovative ideas. Company can reduce the working hours of the

employees to save the payroll. Company should give opportunity to employees to

work from home so that cleaning cost, energy and other costs can be cut. Company

needs to suspend some benefits in order to maintain the budget.

Cheaper options- In order to increase the sales company should move to online

sales. Digital is new trend now- a-days. Digital marketing of the products is the best

option to increase sales. If company uses this option then it helps in reducing

overheads and marketing cost. Company needs to focus on internet service providers

to get the cheaper plan than its competitors.

Investment in affordable marketing- Company needs to cut the marketing expenses

in such conditions. Company needs to prioritize its marketing strategies. Campaigns

which are not performing good company should eliminate them. Company needs to

start new campaigns which provide more efficiency to the business. Managers need to

do free publicity of the product to increase the sales of the company. To increase sales

company can give postcard or coupon to every resident.

important role in company.

To maintain company’s presence it needs to focus on cost cutting. Cost cutting can be

done by 5 ways which are as follows-

Suspension of bill- It includes Loans, rent, credit cards and suppliers. Company

needs to contact banks and lenders so that they can suspend their payment. Before

postponing the bills, company should understand the suspension period, repayment

due date and interest rates. Company should ask their landlord for suspension about

payment. Company needs to talk with suppliers about the negotiation in prices of

material.

Reduced unnecessary expenses- Cost cutting can be done by reducing unnecessary

spending. It includes equipments taken on lease, Travelling, Office space and

software.

Payroll spending- It is counted under largest expense of the company. Company can

terminate some employees to save money. Instead of terminating employees company

needs to think about innovative ideas. Company can reduce the working hours of the

employees to save the payroll. Company should give opportunity to employees to

work from home so that cleaning cost, energy and other costs can be cut. Company

needs to suspend some benefits in order to maintain the budget.

Cheaper options- In order to increase the sales company should move to online

sales. Digital is new trend now- a-days. Digital marketing of the products is the best

option to increase sales. If company uses this option then it helps in reducing

overheads and marketing cost. Company needs to focus on internet service providers

to get the cheaper plan than its competitors.

Investment in affordable marketing- Company needs to cut the marketing expenses

in such conditions. Company needs to prioritize its marketing strategies. Campaigns

which are not performing good company should eliminate them. Company needs to

start new campaigns which provide more efficiency to the business. Managers need to

do free publicity of the product to increase the sales of the company. To increase sales

company can give postcard or coupon to every resident.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 2-

In this part Mr. Amana noticed that its competitors are going online in order to increase sales.

Here company has two options either up gradation of company’s website by programmer or

company needs to get registered itself with Amazon. This decision is very difficult for the

company as there are many factors which are affecting sales of the company.

Scenario 1-

If company chooses this scenario then cost estimation would be -

Scenario 1 Cost (in £)

Setting delivery network 1,50,000

Website up gradation 50,000

IT programmer fees 35,000

Net Charges 4,35,000

Here three types of costs are included which are setting internet service provider, website up

gradation and fees of IT programmer. So, here net charges are 4, 35,000 (in £). According to the

market research, this option will be providing the guaranteed sales of 10,000 annually.

Scenario 2- Cost estimation in this scenario is only 50,000(in £). It is registration fees of

Amazon. In this scenario company just needs to get itself registered with Amazon and online

sales of the product will be started. Guaranteed sales with this scenario are 65,000 units and

company can not control prices and return policy.

After analyzing both the scenario it can be said that company should go with the second option.

As company is already facing pandemic. This is not controllable. There is more safety with

option A but right now company is not in good condition. Company cannot invest 4, 35,000 to

In this part Mr. Amana noticed that its competitors are going online in order to increase sales.

Here company has two options either up gradation of company’s website by programmer or

company needs to get registered itself with Amazon. This decision is very difficult for the

company as there are many factors which are affecting sales of the company.

Scenario 1-

If company chooses this scenario then cost estimation would be -

Scenario 1 Cost (in £)

Setting delivery network 1,50,000

Website up gradation 50,000

IT programmer fees 35,000

Net Charges 4,35,000

Here three types of costs are included which are setting internet service provider, website up

gradation and fees of IT programmer. So, here net charges are 4, 35,000 (in £). According to the

market research, this option will be providing the guaranteed sales of 10,000 annually.

Scenario 2- Cost estimation in this scenario is only 50,000(in £). It is registration fees of

Amazon. In this scenario company just needs to get itself registered with Amazon and online

sales of the product will be started. Guaranteed sales with this scenario are 65,000 units and

company can not control prices and return policy.

After analyzing both the scenario it can be said that company should go with the second option.

As company is already facing pandemic. This is not controllable. There is more safety with

option A but right now company is not in good condition. Company cannot invest 4, 35,000 to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

generate online sales. At first company needs to earn profits so it should start from small

platform. Amazon registration fees is very lower than all the charges in scenario 1. As pandemic

is for uncertain time period. No one is able to know when it will be end. Amazon sales can be

increased if there is increase in demand of the product. It is also providing guaranteed sales of

products which is also a plus point for the company. Company will make good profits with this

option with less investment. After earning profits from this scenario company can move to

option one. Option one will help company more in increasing sales. But option one can be

choose by company after everything gets normalized. Otherwise company will be facing more

problems in generating revenues and it will also be hard for company to survive in such

condition.

Scenario 1 is more costly than scenario 2. Right now company is looking at cost cutting factors

and it will be very hard for company to invest such a big amount in the online sales. Hence,

Scenario two is best fitted for the company according to present condition.

Company should also notice their competitors move. Competitors’ moves affect the company

revenue. If rivals are performing better then it is drawback for the company. Company should

track performance of the competitors. In today’s world in every stream competition is very high.

To track the performance of rivals, company should analyze their financial ratios. Financial

ratios tell the whole story. Company should also analyze the path which rivals are using. If that

path is also fruitful according to company’s budget then company should use such path.

Hence, it can be said that first of all company should go with option number two. Then company

needs to track the performance of its competitors. When sales of the company come to stable

condition then company should go with first scenario. Because first scenario is giving 10,000

unit guaranteed sales which is higher than second scenario. Company will also be having control

over prices and return policy.

Conclusion-

From the above report, it can be said that cost and accounting management is very important for

every company. If all the costs are properly managed then company can achieve its goals or

objectives. Budget plays an important role in company. In this report, budget of Amana ltd. was

not meeting expectations. This happened because of some factors which are uncontrollable.

platform. Amazon registration fees is very lower than all the charges in scenario 1. As pandemic

is for uncertain time period. No one is able to know when it will be end. Amazon sales can be

increased if there is increase in demand of the product. It is also providing guaranteed sales of

products which is also a plus point for the company. Company will make good profits with this

option with less investment. After earning profits from this scenario company can move to

option one. Option one will help company more in increasing sales. But option one can be

choose by company after everything gets normalized. Otherwise company will be facing more

problems in generating revenues and it will also be hard for company to survive in such

condition.

Scenario 1 is more costly than scenario 2. Right now company is looking at cost cutting factors

and it will be very hard for company to invest such a big amount in the online sales. Hence,

Scenario two is best fitted for the company according to present condition.

Company should also notice their competitors move. Competitors’ moves affect the company

revenue. If rivals are performing better then it is drawback for the company. Company should

track performance of the competitors. In today’s world in every stream competition is very high.

To track the performance of rivals, company should analyze their financial ratios. Financial

ratios tell the whole story. Company should also analyze the path which rivals are using. If that

path is also fruitful according to company’s budget then company should use such path.

Hence, it can be said that first of all company should go with option number two. Then company

needs to track the performance of its competitors. When sales of the company come to stable

condition then company should go with first scenario. Because first scenario is giving 10,000

unit guaranteed sales which is higher than second scenario. Company will also be having control

over prices and return policy.

Conclusion-

From the above report, it can be said that cost and accounting management is very important for

every company. If all the costs are properly managed then company can achieve its goals or

objectives. Budget plays an important role in company. In this report, budget of Amana ltd. was

not meeting expectations. This happened because of some factors which are uncontrollable.

Company is facing pandemic in country which is affecting business badly. Company can

maintain budget by using various methods. All the methods are discussed in the report. With the

help of recommendations company can increase its sales. It is also discussed that which path

company should use to increase the sales. As sales is main income source of the company. Due

to lockdown in the country company cannot sell its products offline. So, after seeing its

competitors company decided to sell its products online. In this case, company had two scenarios

and it is very difficult for company to choose one as every scenario has its drawback. But

Company goes with first scenario as company has to maintain its sales. Hence, it can be said that

uncontrollable factors affected company’s budget but however company can maintain its budget

by using various techniques and methods.

References-

Gupta, M., Pevzner, M. and Seethamraju, C., 2010. The implications of absorption

cost accounting and production decisions for future firm performance and

valuation. Contemporary Accounting Research, 27(3), pp.889-922.

Robertson, G.P. and Grace, P.R., 2004. Greenhouse gas fluxes in tropical and

temperate agriculture: the need for a full-cost accounting of global warming

potentials. In Tropical Agriculture in Transition—Opportunities for Mitigating

Greenhouse Gas Emissions? (pp. 51-63). Springer, Dordrecht.

Järvinen, J., 2006. Institutional pressures for adopting new cost accounting systems in

Finnish hospitals: two longitudinal case studies. Financial Accountability &

Management, 22(1).

Ward, D.M., 1999. Cost accounting for health care organizations: concepts and

applications. Jones & Bartlett Learning.

Passarini, K.C., Pereira, M.A., de Brito Farias, T.M., Calarge, F.A. and Santana, C.C.,

2014. Assessment of the viability and sustainability of an integrated waste

management system for the city of Campinas (Brazil), by means of ecological cost

accounting. Journal of cleaner production, 65, pp.479-488.

McCoy, L., 1998. Producing" what the Deans know": Cost accounting and the

restructuring of post-secondary education". Human Studies, 21(4), pp.395-418.

maintain budget by using various methods. All the methods are discussed in the report. With the

help of recommendations company can increase its sales. It is also discussed that which path

company should use to increase the sales. As sales is main income source of the company. Due

to lockdown in the country company cannot sell its products offline. So, after seeing its

competitors company decided to sell its products online. In this case, company had two scenarios

and it is very difficult for company to choose one as every scenario has its drawback. But

Company goes with first scenario as company has to maintain its sales. Hence, it can be said that

uncontrollable factors affected company’s budget but however company can maintain its budget

by using various techniques and methods.

References-

Gupta, M., Pevzner, M. and Seethamraju, C., 2010. The implications of absorption

cost accounting and production decisions for future firm performance and

valuation. Contemporary Accounting Research, 27(3), pp.889-922.

Robertson, G.P. and Grace, P.R., 2004. Greenhouse gas fluxes in tropical and

temperate agriculture: the need for a full-cost accounting of global warming

potentials. In Tropical Agriculture in Transition—Opportunities for Mitigating

Greenhouse Gas Emissions? (pp. 51-63). Springer, Dordrecht.

Järvinen, J., 2006. Institutional pressures for adopting new cost accounting systems in

Finnish hospitals: two longitudinal case studies. Financial Accountability &

Management, 22(1).

Ward, D.M., 1999. Cost accounting for health care organizations: concepts and

applications. Jones & Bartlett Learning.

Passarini, K.C., Pereira, M.A., de Brito Farias, T.M., Calarge, F.A. and Santana, C.C.,

2014. Assessment of the viability and sustainability of an integrated waste

management system for the city of Campinas (Brazil), by means of ecological cost

accounting. Journal of cleaner production, 65, pp.479-488.

McCoy, L., 1998. Producing" what the Deans know": Cost accounting and the

restructuring of post-secondary education". Human Studies, 21(4), pp.395-418.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lemke, K.W. and Page, M.J., 1992. Economic determinants of accounting policy

choice: The case of current cost accounting in the UK. Journal of Accounting and

Economics, 15(1), pp.87-114.

Fleischman, R.K. and Parker, L.D., 1992. The cost-accounting environment in the

British industrial revolution iron industry. Accounting, Business & Financial

History, 2(2), pp.141-160.

Barnes, P., 2000. The identification of UK takeover targets using published historical

cost accounting data Some empirical evidence comparing logit with linear

discriminant analysis and raw financial ratios with industry-relative

ratios. International Review of Financial Analysis, 9(2), pp.147-162.

choice: The case of current cost accounting in the UK. Journal of Accounting and

Economics, 15(1), pp.87-114.

Fleischman, R.K. and Parker, L.D., 1992. The cost-accounting environment in the

British industrial revolution iron industry. Accounting, Business & Financial

History, 2(2), pp.141-160.

Barnes, P., 2000. The identification of UK takeover targets using published historical

cost accounting data Some empirical evidence comparing logit with linear

discriminant analysis and raw financial ratios with industry-relative

ratios. International Review of Financial Analysis, 9(2), pp.147-162.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.