Amana Limited: Budget Analysis, Performance Evaluation, and Strategies

VerifiedAdded on 2023/06/06

|12

|3090

|144

Report

AI Summary

This report presents a comprehensive analysis of Amana Limited's financial performance, focusing on its monthly control report, budget variances, and overall business strategy. The report begins with an introduction to management accounting and budgeting, followed by the preparation of a detailed monthly control report for Amana Limited, comparing its original budget, flexible budget, and actual performance. An in-depth evaluation of the company's performance for the year 2019-20 is provided, highlighting key variances in revenue, cost of goods sold, and expenses. The analysis includes suggestions for the CEO to improve business operations and achieve profit maximization. Furthermore, the report assesses the decision of Mr. Amana regarding online sales, comparing the costs and benefits of selling through a company-owned website versus Amazon. The report concludes with recommendations for improving Amana Limited's financial outcomes and strategic direction.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1.Prepare the monthly control report of Amana Limited displaying the flexible budget, original

budget and budget variances........................................................................................................3

......................................................................................................................................................5

2. Evaluate the performance and activity of Amana Limited for the year 2019-20 using the

control report prepared above......................................................................................................6

3. Propose suggestions for the CEO of Amana Limited to accelerate the business towards

better path.....................................................................................................................................7

PART B............................................................................................................................................9

1. Assess and evaluate the decision of Mr. Amana of bringing in company's online websites

and measure the two decisions of either selling on company owned online website or trade

with Amazon in consideration of the total costs involved...........................................................9

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1.Prepare the monthly control report of Amana Limited displaying the flexible budget, original

budget and budget variances........................................................................................................3

......................................................................................................................................................5

2. Evaluate the performance and activity of Amana Limited for the year 2019-20 using the

control report prepared above......................................................................................................6

3. Propose suggestions for the CEO of Amana Limited to accelerate the business towards

better path.....................................................................................................................................7

PART B............................................................................................................................................9

1. Assess and evaluate the decision of Mr. Amana of bringing in company's online websites

and measure the two decisions of either selling on company owned online website or trade

with Amazon in consideration of the total costs involved...........................................................9

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting involves a method of accounting which is responsible for

creating reports, statements and documents that assists the management to take better decisions

relating to the performance of the business. A budget is an approximation of the revenues as well

as the costs of the business prepared in advance which will occur in the future and is checked

upon frequently when executed (Căpușneanu and et.al., 2020). In the report below, a case study

of Amana Limited is presented below where a brief explanation of budgets and different type

budgets is mentioned. the preparation of a control report for the organisation is also given based

on which an analysis of the financial situation of Amana Limited is given. Along with this

recommendations are provided to the organisation of Amana Limited for improving their results

and business operations by focussing upon the variations which occurred in their budgets and

achieve the objective of profot maximisation along with customer satisfaction.

MAIN BODY

1.Prepare the monthly control report of Amana Limited displaying the flexible budget, original

budget and budget variances. Control report: The control reports are prepared for the purpose of establishing

management control. These reports are supposed to figure out the deviations and

variances which have taken place when compared to the budgeted performance of the

organisation. This is done so that the corrective actions can be brought into effect as and

when needed and on an immediate basis to avoid any losses. The control reports are used

The control report has two dimensions: the first dimension deals with to evaluate and

determine the individual particular performances of the employees and departments as

per the standard performances set by the business to measure the variations. The second

dimension of control report is concerned with measuring the business performances in

economic terms and assess the deviations that may come about (G'iyosov, 2019). Original budget: An original budget is the detailed form of budget with an onward

looking outlook as it is the most initial form of budget which is authorized for the budget

period. This budget displays the most initial form of budget including all the estimation

of revenues and expenses that have been decided by the business as standards. It also

includes the written premises involved in the budget and for its preparation. By using the

Management accounting involves a method of accounting which is responsible for

creating reports, statements and documents that assists the management to take better decisions

relating to the performance of the business. A budget is an approximation of the revenues as well

as the costs of the business prepared in advance which will occur in the future and is checked

upon frequently when executed (Căpușneanu and et.al., 2020). In the report below, a case study

of Amana Limited is presented below where a brief explanation of budgets and different type

budgets is mentioned. the preparation of a control report for the organisation is also given based

on which an analysis of the financial situation of Amana Limited is given. Along with this

recommendations are provided to the organisation of Amana Limited for improving their results

and business operations by focussing upon the variations which occurred in their budgets and

achieve the objective of profot maximisation along with customer satisfaction.

MAIN BODY

1.Prepare the monthly control report of Amana Limited displaying the flexible budget, original

budget and budget variances. Control report: The control reports are prepared for the purpose of establishing

management control. These reports are supposed to figure out the deviations and

variances which have taken place when compared to the budgeted performance of the

organisation. This is done so that the corrective actions can be brought into effect as and

when needed and on an immediate basis to avoid any losses. The control reports are used

The control report has two dimensions: the first dimension deals with to evaluate and

determine the individual particular performances of the employees and departments as

per the standard performances set by the business to measure the variations. The second

dimension of control report is concerned with measuring the business performances in

economic terms and assess the deviations that may come about (G'iyosov, 2019). Original budget: An original budget is the detailed form of budget with an onward

looking outlook as it is the most initial form of budget which is authorized for the budget

period. This budget displays the most initial form of budget including all the estimation

of revenues and expenses that have been decided by the business as standards. It also

includes the written premises involved in the budget and for its preparation. By using the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

original budget, it acts as an assistance to analyse, evaluate and determine the business

performances and asses profits for future. It even regards with the deviations that occur

between static budget and the actual potential of business with regards to business

expenses and revenue generation. Flexible budget: A flexible budget is a type of budget which can adjust according to the

changes that take place in the business on actual revenue levels (Golyagina and Valuckas,

2020). The actual revenues and numbers are used and the flexible budget then provides

generation of budget which is specific to the level of input which has occurred actually.

The flexible budget is not rigid in nature like a fixed budget and hence can be adjusted

according to the changes in the level of input in the organisation. The flexible budget

mainly includes various variable costs that are flexible in nature and changes according to

output levels also as and when the output changes, the flexible budget assist to provide

for all the deviation that occurred as per the actual budget previously formulated.

Budget variance: The budget variances refers to the situations in which the actual

budgeted units and the standard budgeted units vary in numbers. It may occur that the

standards decided by the business either are lower than or higher than the actual output

realised by the business organisation. The deviations in the numbers are evaluated

effectively to measure these variations accordingly and the reasons due to which this

happened may occur to be internal or external to the business. A negative variation

displays that the business has incurred higher expenses s compared to the expenditure

previously decided by business as standards. A positive budget variance displays that the

revenue generated by the business in actual are higher than the standard revenues or costs

incurred are lower than the expected costs and hence is profitable for the business

(Hiromoto, 2019).

performances and asses profits for future. It even regards with the deviations that occur

between static budget and the actual potential of business with regards to business

expenses and revenue generation. Flexible budget: A flexible budget is a type of budget which can adjust according to the

changes that take place in the business on actual revenue levels (Golyagina and Valuckas,

2020). The actual revenues and numbers are used and the flexible budget then provides

generation of budget which is specific to the level of input which has occurred actually.

The flexible budget is not rigid in nature like a fixed budget and hence can be adjusted

according to the changes in the level of input in the organisation. The flexible budget

mainly includes various variable costs that are flexible in nature and changes according to

output levels also as and when the output changes, the flexible budget assist to provide

for all the deviation that occurred as per the actual budget previously formulated.

Budget variance: The budget variances refers to the situations in which the actual

budgeted units and the standard budgeted units vary in numbers. It may occur that the

standards decided by the business either are lower than or higher than the actual output

realised by the business organisation. The deviations in the numbers are evaluated

effectively to measure these variations accordingly and the reasons due to which this

happened may occur to be internal or external to the business. A negative variation

displays that the business has incurred higher expenses s compared to the expenditure

previously decided by business as standards. A positive budget variance displays that the

revenue generated by the business in actual are higher than the standard revenues or costs

incurred are lower than the expected costs and hence is profitable for the business

(Hiromoto, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

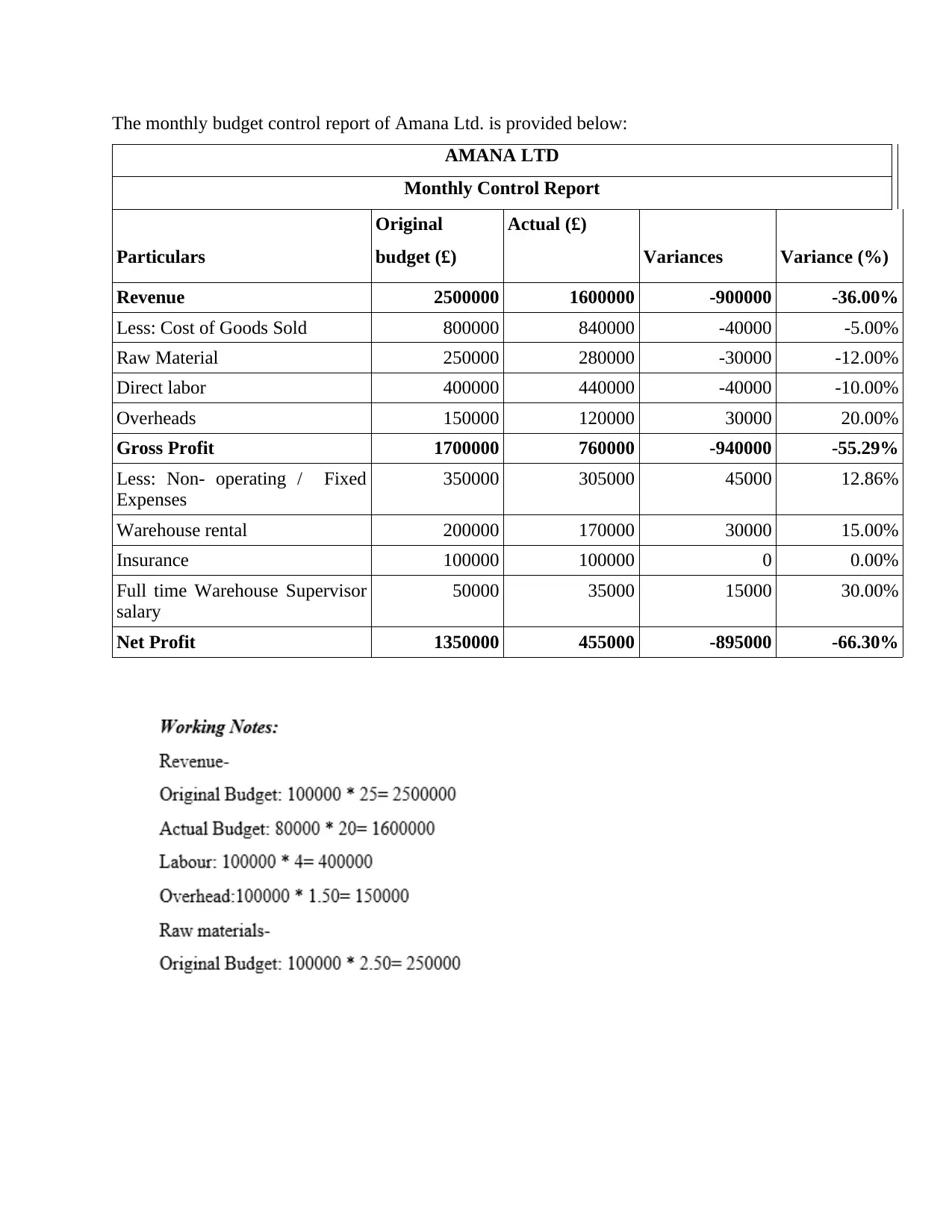

The monthly budget control report of Amana Ltd. is provided below:

AMANA LTD

Monthly Control Report

Particulars

Original

budget (£)

Actual (£)

Variances Variance (%)

Revenue 2500000 1600000 -900000 -36.00%

Less: Cost of Goods Sold 800000 840000 -40000 -5.00%

Raw Material 250000 280000 -30000 -12.00%

Direct labor 400000 440000 -40000 -10.00%

Overheads 150000 120000 30000 20.00%

Gross Profit 1700000 760000 -940000 -55.29%

Less: Non- operating / Fixed

Expenses

350000 305000 45000 12.86%

Warehouse rental 200000 170000 30000 15.00%

Insurance 100000 100000 0 0.00%

Full time Warehouse Supervisor

salary

50000 35000 15000 30.00%

Net Profit 1350000 455000 -895000 -66.30%

AMANA LTD

Monthly Control Report

Particulars

Original

budget (£)

Actual (£)

Variances Variance (%)

Revenue 2500000 1600000 -900000 -36.00%

Less: Cost of Goods Sold 800000 840000 -40000 -5.00%

Raw Material 250000 280000 -30000 -12.00%

Direct labor 400000 440000 -40000 -10.00%

Overheads 150000 120000 30000 20.00%

Gross Profit 1700000 760000 -940000 -55.29%

Less: Non- operating / Fixed

Expenses

350000 305000 45000 12.86%

Warehouse rental 200000 170000 30000 15.00%

Insurance 100000 100000 0 0.00%

Full time Warehouse Supervisor

salary

50000 35000 15000 30.00%

Net Profit 1350000 455000 -895000 -66.30%

2. Evaluate the performance and activity of Amana Limited for the year 2019-20 using the

control report prepared above.

Analysis for Amana Ltd.'s budget report:

The flexible budget showcases decrease in the business operations when compared with

the actual budgets prepared by the company (Ismail, Isa and Mia, 2018). This shows that

the company should focus on selling more units of the products of the organisation as

well as increase the prices of the products so that higher profit margin could be achieved

for each unit of good sold. This should be done ensuring that the high per unit prices do

not result in reduction in revenues generated. This would assist Amana Limited with the

objective of profit maximisation in upcoming years.

The selling price of the products of Amana Limited is £25 and standard units assumed to

be sold in the marketplace is 100000 units whereas in actual scenario the cost of selling

per article is £20 and the actual number of units retailed in the market is 80000 units as

per the actual numbers. This shows that the revenue generated by Amana Limited

therefore is lower than the standards that the company had set. Hence there is a negative

deviation when the actual results are compared with standards set an a high variance in

costs.

The gross profit realised by Amana Limited is lower than the standard gross profit

decided by the company. There is a negative deviation of £940000 from the standards

decided which is primarily due to the reason that the revenue earned by the company is

also very low as compared to standard revenue (Horton and de Araujo Wanderley,

2018).

The per unit costs of Amana Limited could be reduced significantly if the company aims

at economies of scale which is producing higher units of products so that the costs could

be distributed over a higher production units and hence could be reduced significantly.

control report prepared above.

Analysis for Amana Ltd.'s budget report:

The flexible budget showcases decrease in the business operations when compared with

the actual budgets prepared by the company (Ismail, Isa and Mia, 2018). This shows that

the company should focus on selling more units of the products of the organisation as

well as increase the prices of the products so that higher profit margin could be achieved

for each unit of good sold. This should be done ensuring that the high per unit prices do

not result in reduction in revenues generated. This would assist Amana Limited with the

objective of profit maximisation in upcoming years.

The selling price of the products of Amana Limited is £25 and standard units assumed to

be sold in the marketplace is 100000 units whereas in actual scenario the cost of selling

per article is £20 and the actual number of units retailed in the market is 80000 units as

per the actual numbers. This shows that the revenue generated by Amana Limited

therefore is lower than the standards that the company had set. Hence there is a negative

deviation when the actual results are compared with standards set an a high variance in

costs.

The gross profit realised by Amana Limited is lower than the standard gross profit

decided by the company. There is a negative deviation of £940000 from the standards

decided which is primarily due to the reason that the revenue earned by the company is

also very low as compared to standard revenue (Horton and de Araujo Wanderley,

2018).

The per unit costs of Amana Limited could be reduced significantly if the company aims

at economies of scale which is producing higher units of products so that the costs could

be distributed over a higher production units and hence could be reduced significantly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Propose suggestions for the CEO of Amana Limited to accelerate the business towards better

path.

The suggestions for the CEO of Amana Limited for the purpose f accelerating the business and

grow it towards a better path are given below. The organisation can utilise some of these

suggestions to improve the effeciency in operations and achieve better profits for Amana

Limited.

Management of effective execution of objectives with utilization of Continuous

Performance Management.

The CEO of Amana Limited is advised to start with continuous performance evaluation of

employees as well as the company departments so that the performances can be evaluated

effectively and corrective actions could be taken when needed in a fast manner ensuring least

problems in company operations (Kapiyangoda and Gooneratne, 2021).

Establish alignment of objectives effectively overall in the company.

The CEO of Amana Limited is advised to work on an effective alignment of company objectives

and its standard goals which it intents to achieve in future. Aligning the departmental goals along

with company's bigger goals is also advised so that there is harmony in the results achieved

along with effective appointment of business strategies (Bedford and Speklé, 2018).

Ensuring weekly 1-on-1 meetings of managers and departmental heads with team

members appointed as individuals.

This process will assist the company to be informed about the individual employee performances

relating to the business operations as this weekly meetings will make the employees cognizant of

their performances and will enable the managers to know and assist employees with areas that

are either lacking or which need special attention from the management. Adhering to this process

will help business to evaluate and asses the performances easily and take necessary actions

suitable for the business.

Following proper risk management planning.

The CEO and the management at Amana limited is advised to implement effective risk

management policies so that the future financial loss or issues could be solved effectively

(Mariina and Tjahjadi, 2020). This could be done by making the management aware for such

path.

The suggestions for the CEO of Amana Limited for the purpose f accelerating the business and

grow it towards a better path are given below. The organisation can utilise some of these

suggestions to improve the effeciency in operations and achieve better profits for Amana

Limited.

Management of effective execution of objectives with utilization of Continuous

Performance Management.

The CEO of Amana Limited is advised to start with continuous performance evaluation of

employees as well as the company departments so that the performances can be evaluated

effectively and corrective actions could be taken when needed in a fast manner ensuring least

problems in company operations (Kapiyangoda and Gooneratne, 2021).

Establish alignment of objectives effectively overall in the company.

The CEO of Amana Limited is advised to work on an effective alignment of company objectives

and its standard goals which it intents to achieve in future. Aligning the departmental goals along

with company's bigger goals is also advised so that there is harmony in the results achieved

along with effective appointment of business strategies (Bedford and Speklé, 2018).

Ensuring weekly 1-on-1 meetings of managers and departmental heads with team

members appointed as individuals.

This process will assist the company to be informed about the individual employee performances

relating to the business operations as this weekly meetings will make the employees cognizant of

their performances and will enable the managers to know and assist employees with areas that

are either lacking or which need special attention from the management. Adhering to this process

will help business to evaluate and asses the performances easily and take necessary actions

suitable for the business.

Following proper risk management planning.

The CEO and the management at Amana limited is advised to implement effective risk

management policies so that the future financial loss or issues could be solved effectively

(Mariina and Tjahjadi, 2020). This could be done by making the management aware for such

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

issues prior to them actually occurring with the help of effective management. This will help the

organisation to avoid many such situations which could prove to be of loss for Amana Limited.

organisation to avoid many such situations which could prove to be of loss for Amana Limited.

PART B

1. Assess and evaluate the decision of Mr. Amana of bringing in company's online websites and

measure the two decisions of either selling on company owned online website or trade with

Amazon in consideration of the total costs involved.

The analysis and assessment of the two alternatives available to the CEO of Amana limited are

assessed below along with their respective benefits and drawbacks:

Option 1- If Mr. Amana commences selling on the company’s own website, following cost

would be suffered.

Website maintenance cost: £50000

Salary of full time IT employer: £35000

setting up delivery network: £150000

Total cost: (50000+35000+150000) = £235000

Assured sales of 100000 units. Shutdown of physical outlets will affect 50% revenues online (Amoako and et.al., 2021).

Benefits of commencing personal website:

The control and freedom of maintaining the website according top the organisation needs

and market demand for the particular product is in the hands of company owner and the

management.

There is no such competition involved on the sales that occur on company's own website

and hence no such effects on business revenues of Amana Limited. Mr. Amana can choose among the various factors whether to provide the discounts,

website sale or other featured and in what capacity (Nielsen, 2018).

Disadvantages of commencing personal website:

Comparatively expensive with the alternative of selling on Amazon.

No presence of any prior customer data and hence there can be delay in bringing business

revenues. High risk with failure to achieve desired revenues units and sale figures.

Option 2- Selling over online platform Amazon, cost incurred would be following.

Amazon fulfilment fees: £50000

Total cost= £50000

1. Assess and evaluate the decision of Mr. Amana of bringing in company's online websites and

measure the two decisions of either selling on company owned online website or trade with

Amazon in consideration of the total costs involved.

The analysis and assessment of the two alternatives available to the CEO of Amana limited are

assessed below along with their respective benefits and drawbacks:

Option 1- If Mr. Amana commences selling on the company’s own website, following cost

would be suffered.

Website maintenance cost: £50000

Salary of full time IT employer: £35000

setting up delivery network: £150000

Total cost: (50000+35000+150000) = £235000

Assured sales of 100000 units. Shutdown of physical outlets will affect 50% revenues online (Amoako and et.al., 2021).

Benefits of commencing personal website:

The control and freedom of maintaining the website according top the organisation needs

and market demand for the particular product is in the hands of company owner and the

management.

There is no such competition involved on the sales that occur on company's own website

and hence no such effects on business revenues of Amana Limited. Mr. Amana can choose among the various factors whether to provide the discounts,

website sale or other featured and in what capacity (Nielsen, 2018).

Disadvantages of commencing personal website:

Comparatively expensive with the alternative of selling on Amazon.

No presence of any prior customer data and hence there can be delay in bringing business

revenues. High risk with failure to achieve desired revenues units and sale figures.

Option 2- Selling over online platform Amazon, cost incurred would be following.

Amazon fulfilment fees: £50000

Total cost= £50000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assured sales of 65000 units.

Lack of control on prices and return policy. High level of competition.

Benefits of selling through Amazon:

Guarantee of enough revenues due to the goodwill and renowned image of Amazon as an

online selling platform.

Cost effective when compared to the cost involved in setting up company's own website

due to which it is more preferable for the business of Amana Limited (Pelz, 2019). Huge customer data available which assist in generating faster and higher revenues and

better profitability for the business.

Disadvantages of selling through Amazon:

Absence of any control on the return and exchange policies of the platform which makes

it less effective for Amana Limited for stimulating its revenues.

No confidentiality related to company's secretive policies and plans for future which may

lead to leakage of some essential business plans and operations that Amana Limited is

planning for in future. Amazon has a customer driven approach which may not prove to be profitable for Amana

Limited as an organisation and may fail to achieve its moto of profit maximisation.

Overall Analysis:

The two options available with Amana limited have been effectively analysed and

measured above in the report. The first option of building the company's own website will cost

Amana limited with £235000 and the second option of Amazon will involve £50000 investment.

The conclusions which can be made from these factors are that although starting Amana Limited

own website has a high involvement of cost setup but the after results will be beneficial when

compared to selling on Amazon (Saeidi and et.al., 2018). As there is an initial guarantee of

100000 unit of sales, the company can take this as the profitable point and should initiate with

building the company owned website for future operations. This will also help the company to

reach a global market and higher customer base which will make the organisation to be known in

other countries and city areas too. Also company owned website will surely save Amana Limited

from high competition other wise present on Amazon as a word renowned website for selling

products (Vakhrushina and et.al., 2018).

Lack of control on prices and return policy. High level of competition.

Benefits of selling through Amazon:

Guarantee of enough revenues due to the goodwill and renowned image of Amazon as an

online selling platform.

Cost effective when compared to the cost involved in setting up company's own website

due to which it is more preferable for the business of Amana Limited (Pelz, 2019). Huge customer data available which assist in generating faster and higher revenues and

better profitability for the business.

Disadvantages of selling through Amazon:

Absence of any control on the return and exchange policies of the platform which makes

it less effective for Amana Limited for stimulating its revenues.

No confidentiality related to company's secretive policies and plans for future which may

lead to leakage of some essential business plans and operations that Amana Limited is

planning for in future. Amazon has a customer driven approach which may not prove to be profitable for Amana

Limited as an organisation and may fail to achieve its moto of profit maximisation.

Overall Analysis:

The two options available with Amana limited have been effectively analysed and

measured above in the report. The first option of building the company's own website will cost

Amana limited with £235000 and the second option of Amazon will involve £50000 investment.

The conclusions which can be made from these factors are that although starting Amana Limited

own website has a high involvement of cost setup but the after results will be beneficial when

compared to selling on Amazon (Saeidi and et.al., 2018). As there is an initial guarantee of

100000 unit of sales, the company can take this as the profitable point and should initiate with

building the company owned website for future operations. This will also help the company to

reach a global market and higher customer base which will make the organisation to be known in

other countries and city areas too. Also company owned website will surely save Amana Limited

from high competition other wise present on Amazon as a word renowned website for selling

products (Vakhrushina and et.al., 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it can be concluded that formulation of budgets is an essential part

of a business organisation and its operations. As it helps the organisation of Amana Limited to

ensure an efficient and effective flow of business operations and accurate analysis of the

standards and actual results of the business. The next part of the report helps to conclude upon

the financial position of Amana Limited through its control report and the analysis of that which

showed that the organisation as been incurring high costs but the revenues are not enough and

hence there is absence in profit generation for the business. The section 2 of the report helped to

conclude that Amana Limited should initiate building company's own website so that it can

accelerate its revenues and make higher profits for the business as compared to selling on

Amazon.

From the above report it can be concluded that formulation of budgets is an essential part

of a business organisation and its operations. As it helps the organisation of Amana Limited to

ensure an efficient and effective flow of business operations and accurate analysis of the

standards and actual results of the business. The next part of the report helps to conclude upon

the financial position of Amana Limited through its control report and the analysis of that which

showed that the organisation as been incurring high costs but the revenues are not enough and

hence there is absence in profit generation for the business. The section 2 of the report helped to

conclude that Amana Limited should initiate building company's own website so that it can

accelerate its revenues and make higher profits for the business as compared to selling on

Amazon.

REFERENCES

Books and Journals:

Amoako, G.K., and et.al., 2021. Institutional isomorphism, environmental management

accounting and environmental accountability: a review. Environment, Development and

Sustainability. 23(8). pp.11201-11216.

Bedford, D.S. and Speklé, R.F., 2018. Constructs in survey-based management accounting and

control research: An inventory from 1996 to 2015. Journal of Management Accounting

Research. 30(2). pp.269-322.

Căpușneanu, S., and et.al., 2020. Management accounting in the digital economy: evolution and

perspectives. In Improving business performance through innovation in the digital

economy (pp. 156-176). IGI Global.

G'iyosov, I.K., 2019. THE THEORICAL FEATURES OF THE ORGANIZATION OF THE

STRATEGIC MANAGEMENT ACCOUNTING IN BUSINESS. Theoretical & Applied

Science, (9), pp.260-266.'

Golyagina, A. and Valuckas, D., 2020. Boundary-work in management accounting: The case of

hybrid professionalism. The British Accounting Review, 52(2), p.100841.

Hiromoto, T., 2019. Restoring the relevance of management accounting. In Management Control

Theory (pp. 273-288). Routledge.

Horton, K.E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: Adding a new piece to the theoretical

jigsaw. Management Accounting Research, 38, pp.39-50.

Ismail, K., Isa, C.R. and Mia, L., 2018. Evidence on the usefulness of management accounting

systems in integrated manufacturing environment. Pacific Accounting Review.

Kapiyangoda, K. and Gooneratne, T., 2021. Management accounting research in family

businesses: a review of the status quo and future agenda. Journal of Accounting &

Organizational Change.

Mariina, E. and Tjahjadi, B., 2020. Strategic management accounting and university

performance: a critical review. Academy of Strategic Management Journal, 19(2), pp.1-5.

Nielsen, S., 2018. Reflections on the applicability of business analytics for management

accounting–and future perspectives for the accountant. Journal of Accounting &

Organizational Change.

Pelz, M., 2019. Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management Reviews. 21(2).

pp.256-274.

Saeidi, S.P., and et.al., 2018. The moderating role of environmental management accounting

between environmental innovation and firm financial performance. International Journal

of Business Performance Management. 19(3). pp.326-348.

Vakhrushina, M.A., and et.al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(3). pp.808-813.

Books and Journals:

Amoako, G.K., and et.al., 2021. Institutional isomorphism, environmental management

accounting and environmental accountability: a review. Environment, Development and

Sustainability. 23(8). pp.11201-11216.

Bedford, D.S. and Speklé, R.F., 2018. Constructs in survey-based management accounting and

control research: An inventory from 1996 to 2015. Journal of Management Accounting

Research. 30(2). pp.269-322.

Căpușneanu, S., and et.al., 2020. Management accounting in the digital economy: evolution and

perspectives. In Improving business performance through innovation in the digital

economy (pp. 156-176). IGI Global.

G'iyosov, I.K., 2019. THE THEORICAL FEATURES OF THE ORGANIZATION OF THE

STRATEGIC MANAGEMENT ACCOUNTING IN BUSINESS. Theoretical & Applied

Science, (9), pp.260-266.'

Golyagina, A. and Valuckas, D., 2020. Boundary-work in management accounting: The case of

hybrid professionalism. The British Accounting Review, 52(2), p.100841.

Hiromoto, T., 2019. Restoring the relevance of management accounting. In Management Control

Theory (pp. 273-288). Routledge.

Horton, K.E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: Adding a new piece to the theoretical

jigsaw. Management Accounting Research, 38, pp.39-50.

Ismail, K., Isa, C.R. and Mia, L., 2018. Evidence on the usefulness of management accounting

systems in integrated manufacturing environment. Pacific Accounting Review.

Kapiyangoda, K. and Gooneratne, T., 2021. Management accounting research in family

businesses: a review of the status quo and future agenda. Journal of Accounting &

Organizational Change.

Mariina, E. and Tjahjadi, B., 2020. Strategic management accounting and university

performance: a critical review. Academy of Strategic Management Journal, 19(2), pp.1-5.

Nielsen, S., 2018. Reflections on the applicability of business analytics for management

accounting–and future perspectives for the accountant. Journal of Accounting &

Organizational Change.

Pelz, M., 2019. Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management Reviews. 21(2).

pp.256-274.

Saeidi, S.P., and et.al., 2018. The moderating role of environmental management accounting

between environmental innovation and firm financial performance. International Journal

of Business Performance Management. 19(3). pp.326-348.

Vakhrushina, M.A., and et.al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(3). pp.808-813.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.