Management Accounting: Amana's Performance and Online Strategy

VerifiedAdded on 2022/12/23

|11

|3051

|1

Report

AI Summary

This report provides a comprehensive analysis of Amana Ltd's performance using management accounting principles. Part A includes a monthly control report with original, flexed, and actual budgets, along with variance analysis. The report evaluates sales, material costs, labor costs, overheads, and contribution, offering detailed insights into areas of inefficiency and providing recommendations for improvement, such as increasing sales units, controlling costs, and exploring new opportunities. Part B analyzes Mr. Amana's decision to move the business online, comparing the costs and benefits of establishing a direct online shop versus selling through Amazon, considering factors like fulfillment fees, sales guarantees, and control over pricing and returns. The report recommends that Amana should sell its products through its own online platform, while also using Amazon, and gradually transition to its own website as the business becomes more popular. The report also provides a detailed financial comparison between both options and emphasizes the importance of marketing strategies and cost-effectiveness.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part A...............................................................................................................................................3

(i). Prepare the monthly control report:......................................................................................3

(ii). Report on Amana’s performance during the year 2020:......................................................4

Provide recommendations to Amana’s CEO on areas of improvement:....................................6

Part B...............................................................................................................................................7

Analysis of Mr Amana’s decision to go online:..........................................................................7

CONCLUSION..............................................................................................................................10

References......................................................................................................................................11

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part A...............................................................................................................................................3

(i). Prepare the monthly control report:......................................................................................3

(ii). Report on Amana’s performance during the year 2020:......................................................4

Provide recommendations to Amana’s CEO on areas of improvement:....................................6

Part B...............................................................................................................................................7

Analysis of Mr Amana’s decision to go online:..........................................................................7

CONCLUSION..............................................................................................................................10

References......................................................................................................................................11

2

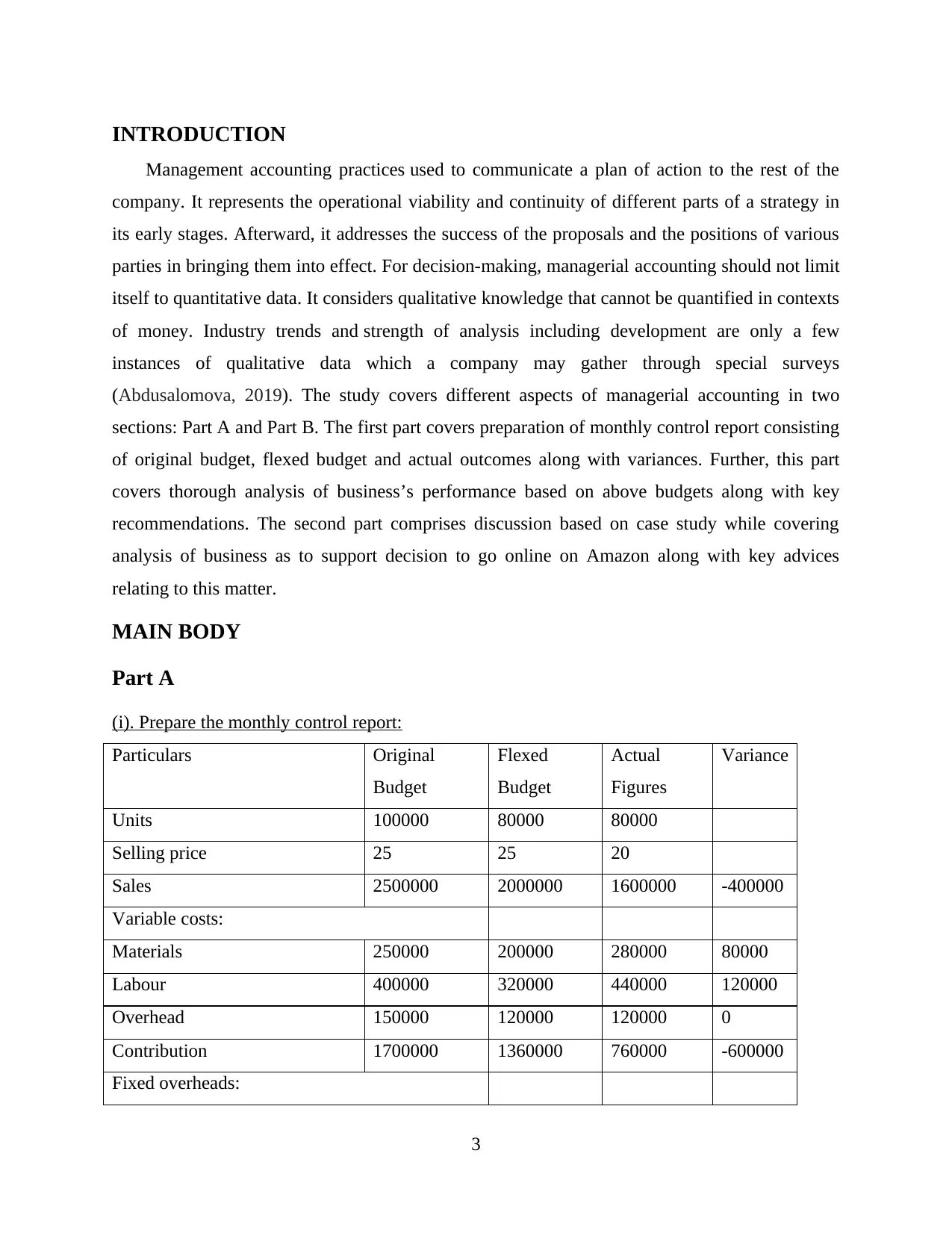

INTRODUCTION

Management accounting practices used to communicate a plan of action to the rest of the

company. It represents the operational viability and continuity of different parts of a strategy in

its early stages. Afterward, it addresses the success of the proposals and the positions of various

parties in bringing them into effect. For decision-making, managerial accounting should not limit

itself to quantitative data. It considers qualitative knowledge that cannot be quantified in contexts

of money. Industry trends and strength of analysis including development are only a few

instances of qualitative data which a company may gather through special surveys

(Abdusalomova, 2019). The study covers different aspects of managerial accounting in two

sections: Part A and Part B. The first part covers preparation of monthly control report consisting

of original budget, flexed budget and actual outcomes along with variances. Further, this part

covers thorough analysis of business’s performance based on above budgets along with key

recommendations. The second part comprises discussion based on case study while covering

analysis of business as to support decision to go online on Amazon along with key advices

relating to this matter.

MAIN BODY

Part A

(i). Prepare the monthly control report:

Particulars Original

Budget

Flexed

Budget

Actual

Figures

Variance

Units 100000 80000 80000

Selling price 25 25 20

Sales 2500000 2000000 1600000 -400000

Variable costs:

Materials 250000 200000 280000 80000

Labour 400000 320000 440000 120000

Overhead 150000 120000 120000 0

Contribution 1700000 1360000 760000 -600000

Fixed overheads:

3

Management accounting practices used to communicate a plan of action to the rest of the

company. It represents the operational viability and continuity of different parts of a strategy in

its early stages. Afterward, it addresses the success of the proposals and the positions of various

parties in bringing them into effect. For decision-making, managerial accounting should not limit

itself to quantitative data. It considers qualitative knowledge that cannot be quantified in contexts

of money. Industry trends and strength of analysis including development are only a few

instances of qualitative data which a company may gather through special surveys

(Abdusalomova, 2019). The study covers different aspects of managerial accounting in two

sections: Part A and Part B. The first part covers preparation of monthly control report consisting

of original budget, flexed budget and actual outcomes along with variances. Further, this part

covers thorough analysis of business’s performance based on above budgets along with key

recommendations. The second part comprises discussion based on case study while covering

analysis of business as to support decision to go online on Amazon along with key advices

relating to this matter.

MAIN BODY

Part A

(i). Prepare the monthly control report:

Particulars Original

Budget

Flexed

Budget

Actual

Figures

Variance

Units 100000 80000 80000

Selling price 25 25 20

Sales 2500000 2000000 1600000 -400000

Variable costs:

Materials 250000 200000 280000 80000

Labour 400000 320000 440000 120000

Overhead 150000 120000 120000 0

Contribution 1700000 1360000 760000 -600000

Fixed overheads:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Warehouse Rental 200000 160000 170000 10000

Insurance 100000 80000 100000 20000

Fulltime warehouse supervisor

salary

50000 40000 35000 -5000

Profit 1350000 1080000 455000 -625000

Working Note: Calculation of fixed overheads:

Fixed Overheads: Flexed Budget

Warehouse Rental 200000 / 100000 * 80000 = 160000

Insurance 100000 / 100000 * 80000 = 80000

Fulltime warehouse supervisor

salary

50000 / 100000 * 80000 = 40000

(ii). Report on Amana’s performance during the year 2020:

Amana’s Performance Report:

Income Statement

Particulars Amount

Sales 1600000 100.00%

Variable cost:

Materials 280000 17.50%

Labour 440000 27.50%

Overhead 120000 7.50%

Total Variable Costs 840000 52.50%

Contribution 760000 47.50%

Fixed Overheads:

Warehouse Rental 170000 10.63%

Insurance 100000 6.25%

Fulltime warehouse supervisor 35000 2.19%

4

Insurance 100000 80000 100000 20000

Fulltime warehouse supervisor

salary

50000 40000 35000 -5000

Profit 1350000 1080000 455000 -625000

Working Note: Calculation of fixed overheads:

Fixed Overheads: Flexed Budget

Warehouse Rental 200000 / 100000 * 80000 = 160000

Insurance 100000 / 100000 * 80000 = 80000

Fulltime warehouse supervisor

salary

50000 / 100000 * 80000 = 40000

(ii). Report on Amana’s performance during the year 2020:

Amana’s Performance Report:

Income Statement

Particulars Amount

Sales 1600000 100.00%

Variable cost:

Materials 280000 17.50%

Labour 440000 27.50%

Overhead 120000 7.50%

Total Variable Costs 840000 52.50%

Contribution 760000 47.50%

Fixed Overheads:

Warehouse Rental 170000 10.63%

Insurance 100000 6.25%

Fulltime warehouse supervisor 35000 2.19%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

salary

Total Fixed Costs 305000 19.06%

Net Profit 455000 28.44%

Amana Ltd has reported sales amounting 16,00,000 while the budgeted sales are 2500000

and sales estimated as per flexed budget is 20,00,000. Here is Adverse variance in sales is due to

lower sales price and lower units sold as compare to budgeted sales. This adverse variance in

sales shows that organisation is inefficient to generating sales.

Material costs actually incurred by business is 280000, while budgeted material costs are

250000 and material cost as per flexed budget is 200000. There is adverse variance in material

cost of 80000. This adverse variance in material costs shows inefficiency in production process

in terms of usage of raw materials (Ameen, Ahmed and Abd Hafez, 2018).

Actually incurred labour cost of business is 440000 while budgeted figure of labour cost

is 400000 and flexed budget based on actual outputs shows labour cost of 320000. In case of

Labour costs, there is adverse variance of 120000. This unfavourable variance in labour cost

indicates that labours are mismanaged and business is inefficient in controlling labour costs.

Other production overheads of business actually incurred is 120000 while originally

budgeted figure of other variable overheads is 150000. Here flexed budget shows same figure of

overheads as of actual. Thus, there is no variance in other variable overheads.

Company has reported contribution of 760000 which is around 47.50% of sales. While

business’s originally budgeted figure of contribution is 1700000 and contribution figure as per

flexed budget is 1360000. Thus, here is adverse variance in contribution which reflects that

business is inefficient to match actual contribution in comparison of budgeted contribution. This

also exhibits that business has not utilised production capacity to provide sufficient budgeted

contribution figure (Rikhardsson and Yigitbasioglu, 2018).

Fixed overheads of business includes Rent of warehouse, Insurance cost and Fulltime

warehouse supervisor salary. There is also variance in fixed overheads which impacted actual net

profit figure of business in comparison to budgeted net profit figure.

Budgeted Warehouse rental of business is 200,000 for 100,000 units while actual

warehouse rental allocated for 80000 units in flexed budget is 160000. But company has actually

5

Total Fixed Costs 305000 19.06%

Net Profit 455000 28.44%

Amana Ltd has reported sales amounting 16,00,000 while the budgeted sales are 2500000

and sales estimated as per flexed budget is 20,00,000. Here is Adverse variance in sales is due to

lower sales price and lower units sold as compare to budgeted sales. This adverse variance in

sales shows that organisation is inefficient to generating sales.

Material costs actually incurred by business is 280000, while budgeted material costs are

250000 and material cost as per flexed budget is 200000. There is adverse variance in material

cost of 80000. This adverse variance in material costs shows inefficiency in production process

in terms of usage of raw materials (Ameen, Ahmed and Abd Hafez, 2018).

Actually incurred labour cost of business is 440000 while budgeted figure of labour cost

is 400000 and flexed budget based on actual outputs shows labour cost of 320000. In case of

Labour costs, there is adverse variance of 120000. This unfavourable variance in labour cost

indicates that labours are mismanaged and business is inefficient in controlling labour costs.

Other production overheads of business actually incurred is 120000 while originally

budgeted figure of other variable overheads is 150000. Here flexed budget shows same figure of

overheads as of actual. Thus, there is no variance in other variable overheads.

Company has reported contribution of 760000 which is around 47.50% of sales. While

business’s originally budgeted figure of contribution is 1700000 and contribution figure as per

flexed budget is 1360000. Thus, here is adverse variance in contribution which reflects that

business is inefficient to match actual contribution in comparison of budgeted contribution. This

also exhibits that business has not utilised production capacity to provide sufficient budgeted

contribution figure (Rikhardsson and Yigitbasioglu, 2018).

Fixed overheads of business includes Rent of warehouse, Insurance cost and Fulltime

warehouse supervisor salary. There is also variance in fixed overheads which impacted actual net

profit figure of business in comparison to budgeted net profit figure.

Budgeted Warehouse rental of business is 200,000 for 100,000 units while actual

warehouse rental allocated for 80000 units in flexed budget is 160000. But company has actually

5

incurred warehouse rental of 170000, therefore there is adverse variance of 10000. This reflects

that business has over absorbed the warehouse rental.

Insurances costs actually incurred by business is 100000 at 80000 units’ capacity while

company has estimated 100000 insurance cost at 100000 units’ capacity. Thus, in comparison to

the flexed budget there is adverse variance of 20000 which indicates that organisation has over

absorbed the insurance costs.

Budgeted figure of Fulltime warehouse supervisor salary is 50000 while actually paid

salary is 35000 which is also lower than the figure computed in flexed budget. So, there is

favourable variance of -5000. This indicates that business is efficient to optimise supervisor

salary (Allain, Lemaire and Lux, 2021).

Company’s actual net profit reported is 455000 while company originally budgeted net

profit of 1350000. Based on actual capacity utilised flexed budget shows net profit of 1080000.

Thus there is adverse variance of 625000 in net profit. This shows that company is inefficient to

generate profitability as compare to budget net profit benchmark.

Provide recommendations to Amana’s CEO on areas of improvement:

Based on above analysis following are certain key recommendations for improving business

areas, as follows:

The first priority of company should be increase sales units as well as it is recommended to

company to increase their selling price where practicable. Company should extend the business

through searching for new opportunities or seeking ways to boost revenue.

Company should need to launch new products to grow business, increase marketing efforts, or

enhance customer services to increase revenue. As company is manufacturer, this might mean

improving productivity to keep up with demand. Changing prices, terms, or payment terms may

boost demand for products. Evaluate what business rivals are doing as well as own profitability

to see how company should lower costs. If business can't lower the price, enhancing an offer

with favorable terms can also sway customers (Abdusalomova, 2020). Company should

determine the one is most or least cost-effective. Company should reduce the amount of

money spend on products that don't pay back, and put more money into the ones that do.

Prioritize reducing variable costs like material and labour wages before focusing on

business's fixed costs such as rent and other fixed costs. Companies should not cut expenses to

shore-up a struggling company and afterwards stop tracking it until their short-term targets have

6

that business has over absorbed the warehouse rental.

Insurances costs actually incurred by business is 100000 at 80000 units’ capacity while

company has estimated 100000 insurance cost at 100000 units’ capacity. Thus, in comparison to

the flexed budget there is adverse variance of 20000 which indicates that organisation has over

absorbed the insurance costs.

Budgeted figure of Fulltime warehouse supervisor salary is 50000 while actually paid

salary is 35000 which is also lower than the figure computed in flexed budget. So, there is

favourable variance of -5000. This indicates that business is efficient to optimise supervisor

salary (Allain, Lemaire and Lux, 2021).

Company’s actual net profit reported is 455000 while company originally budgeted net

profit of 1350000. Based on actual capacity utilised flexed budget shows net profit of 1080000.

Thus there is adverse variance of 625000 in net profit. This shows that company is inefficient to

generate profitability as compare to budget net profit benchmark.

Provide recommendations to Amana’s CEO on areas of improvement:

Based on above analysis following are certain key recommendations for improving business

areas, as follows:

The first priority of company should be increase sales units as well as it is recommended to

company to increase their selling price where practicable. Company should extend the business

through searching for new opportunities or seeking ways to boost revenue.

Company should need to launch new products to grow business, increase marketing efforts, or

enhance customer services to increase revenue. As company is manufacturer, this might mean

improving productivity to keep up with demand. Changing prices, terms, or payment terms may

boost demand for products. Evaluate what business rivals are doing as well as own profitability

to see how company should lower costs. If business can't lower the price, enhancing an offer

with favorable terms can also sway customers (Abdusalomova, 2020). Company should

determine the one is most or least cost-effective. Company should reduce the amount of

money spend on products that don't pay back, and put more money into the ones that do.

Prioritize reducing variable costs like material and labour wages before focusing on

business's fixed costs such as rent and other fixed costs. Companies should not cut expenses to

shore-up a struggling company and afterwards stop tracking it until their short-term targets have

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

been reached. Still keep tracking of the company's finances and search for ways to save money.

The most compelling approach to cut overall costs is to pinch pennies as much as

possible. Company should learn to be frugal about business expenses. However, as a company

expands, it's easier to lose tracking of expenses. Also note that in order for business to be

successful, it must have a thrifty attitude in order to maximise profits (Zyznarska-Dworczak,

2018).

Part B

Analysis of Mr Amana’s decision to go online:

Amana has found that many of his rivals now market their products online to consumers in

the United Kingdom, Europe, and United States. He has considered closing divisions in

Brighton, the Birmingham city centre, including Manchester city centre in attempt to streamline

company operations and shift 50% of revenues online, while making, such decision several

considerations must be considered:

Costs Amount

Cost of setting up delivery network £150,000

Cost of upgrading current website to handle

large volume of sales

£50,000

Salary of a fulltime IT programmer £35,000

Total Cost £235000

From the market research this has been analysed that there would be guaranteed sales of

100,000 units yearly.

Factors to be considered if business alternatively sell its products directly on the Amazon:

Amazon fulfilment fees = £50,000

Guaranteed sales = 65,000 units on Amazon annually

Lack of control over pricing and return policy

Analysis of both these option indicates that total cost in case company sell their products

online through their own online-shop is 235000 and this alterative will provide guaranteed sales

of 100000. On other hand, if company sell their product through Amazon this this will cost to

company 50000 with a disadvantage of lack of control over pricing as well as returning policy.

7

The most compelling approach to cut overall costs is to pinch pennies as much as

possible. Company should learn to be frugal about business expenses. However, as a company

expands, it's easier to lose tracking of expenses. Also note that in order for business to be

successful, it must have a thrifty attitude in order to maximise profits (Zyznarska-Dworczak,

2018).

Part B

Analysis of Mr Amana’s decision to go online:

Amana has found that many of his rivals now market their products online to consumers in

the United Kingdom, Europe, and United States. He has considered closing divisions in

Brighton, the Birmingham city centre, including Manchester city centre in attempt to streamline

company operations and shift 50% of revenues online, while making, such decision several

considerations must be considered:

Costs Amount

Cost of setting up delivery network £150,000

Cost of upgrading current website to handle

large volume of sales

£50,000

Salary of a fulltime IT programmer £35,000

Total Cost £235000

From the market research this has been analysed that there would be guaranteed sales of

100,000 units yearly.

Factors to be considered if business alternatively sell its products directly on the Amazon:

Amazon fulfilment fees = £50,000

Guaranteed sales = 65,000 units on Amazon annually

Lack of control over pricing and return policy

Analysis of both these option indicates that total cost in case company sell their products

online through their own online-shop is 235000 and this alterative will provide guaranteed sales

of 100000. On other hand, if company sell their product through Amazon this this will cost to

company 50000 with a disadvantage of lack of control over pricing as well as returning policy.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For better comparison of both such alternatives, let consider the standard sale price £10 per unit

and compute the net estimated profit figure:

Case 1: In case company sell their products through own online-shop:

Particulars Amount

Sales (100000 *10) 1000000

Less: Costs

Cost of setting up delivery

network

150000

Cost of upgrading current

website

50000

Salary of a fulltime IT

programmer

35000

Total Costs 235000

Profit 765000

Case 2: In case company sell their products through Amazon:

Particulars Amounts

Sales (100000 *10) 1000000

Less: Costs

Amazon fulfilment fees 50000

Total Costs 50000

Profit 950000

Comparative analysis of both these cases shows that profit in case 1 if corporation sell

their products through their own online shop, estimated profit would be 765000 while in second

case if company sell their products through Amazon platform, expected profit would be 600000

which is lower than first alternative. Another notable aspect here is that in case of sell of

products through there is lack of control over return policy and pricing. Thus, comparative

analysis shows that company should go for selling their products through own online-shop

platform (Pelz, 2019).

Another recommendation here is to go for both, but company should gradually move to

their own online-shop website as company’s products become popular. Rented sites, such as

Amazon, are usually very famous and have a broad user base that is ready to link. Consider

8

and compute the net estimated profit figure:

Case 1: In case company sell their products through own online-shop:

Particulars Amount

Sales (100000 *10) 1000000

Less: Costs

Cost of setting up delivery

network

150000

Cost of upgrading current

website

50000

Salary of a fulltime IT

programmer

35000

Total Costs 235000

Profit 765000

Case 2: In case company sell their products through Amazon:

Particulars Amounts

Sales (100000 *10) 1000000

Less: Costs

Amazon fulfilment fees 50000

Total Costs 50000

Profit 950000

Comparative analysis of both these cases shows that profit in case 1 if corporation sell

their products through their own online shop, estimated profit would be 765000 while in second

case if company sell their products through Amazon platform, expected profit would be 600000

which is lower than first alternative. Another notable aspect here is that in case of sell of

products through there is lack of control over return policy and pricing. Thus, comparative

analysis shows that company should go for selling their products through own online-shop

platform (Pelz, 2019).

Another recommendation here is to go for both, but company should gradually move to

their own online-shop website as company’s products become popular. Rented sites, such as

Amazon, are usually very famous and have a broad user base that is ready to link. Consider

8

Social media as examples of platforms. Each one has millions of subscribers, and business can

instantly reach them by using the app. When it comes to establishing a digital identity, this is

extremely helpful (Hariyati, Tjahjadi and Soewarno, 2019).

Rather, business must gradually develop it through various marketing strategies. To do

so, you'll need both timing and efforts. As a result, amazon platform is by far best option if

business just getting started and want to hit a large pool of prospective customers or audiences

quickly. However, by utilizing amazon platform will provide business with access to vast

number of users, this will also limit their contact with those customers to inside the platform.

Remember Amazon: it deliberately conceals the contact details of someone who has

bought product so that business can only contact customers via Amazon (Pelz, 2019).

The amazon platform needs much less of time to manage and maintain. The framework

and resources business need to build stunning and well-designed shops or websites are already in

existence on Amazon. These platforms' architecture for helping you develop business presence is

not only quick to use, but it's also the product of thorough R&D and users research so it's fine.

Using amazon platform, on the other hand, needs business to do all of architecture and

configuration itself. This diverts time and attention away from key facets of business.

Although some techniques have rendered it simpler than ever before to build well-designed

ecommerce platform business would always need to recruit a skilled employee to customize site

and handle possible bugs, making them inconvenient to employ if one don't have budget. Using

amazon platform is a helpful way to proceed if business has small team without budget or

resources to run own platform. While amazon platform is simple to set-up and utilize. they are

limited in their versatility. If business use their delivery service (that means they handle their

stock), they have full control over warehouses where items are stored in (Bedford and Speklé,

2018).

Although this is usually not a problem, Amazon will sometimes transfer business inventory from

warehouses to warehouse without business's consent, rendering their goods unsellable while

being in transit. As result, when selling on Amazon, business must still keep a check

on inventory and ensure that their product doesn't face inadequacy of inventory owing to

Amazon's stocks control. Similar problems occur for Platform in terms of personalized styling,

Amazon in terms of architecture and design, but almost every other site in any manner.

Business would have the independence and versatility to do whatever they want whether run

9

instantly reach them by using the app. When it comes to establishing a digital identity, this is

extremely helpful (Hariyati, Tjahjadi and Soewarno, 2019).

Rather, business must gradually develop it through various marketing strategies. To do

so, you'll need both timing and efforts. As a result, amazon platform is by far best option if

business just getting started and want to hit a large pool of prospective customers or audiences

quickly. However, by utilizing amazon platform will provide business with access to vast

number of users, this will also limit their contact with those customers to inside the platform.

Remember Amazon: it deliberately conceals the contact details of someone who has

bought product so that business can only contact customers via Amazon (Pelz, 2019).

The amazon platform needs much less of time to manage and maintain. The framework

and resources business need to build stunning and well-designed shops or websites are already in

existence on Amazon. These platforms' architecture for helping you develop business presence is

not only quick to use, but it's also the product of thorough R&D and users research so it's fine.

Using amazon platform, on the other hand, needs business to do all of architecture and

configuration itself. This diverts time and attention away from key facets of business.

Although some techniques have rendered it simpler than ever before to build well-designed

ecommerce platform business would always need to recruit a skilled employee to customize site

and handle possible bugs, making them inconvenient to employ if one don't have budget. Using

amazon platform is a helpful way to proceed if business has small team without budget or

resources to run own platform. While amazon platform is simple to set-up and utilize. they are

limited in their versatility. If business use their delivery service (that means they handle their

stock), they have full control over warehouses where items are stored in (Bedford and Speklé,

2018).

Although this is usually not a problem, Amazon will sometimes transfer business inventory from

warehouses to warehouse without business's consent, rendering their goods unsellable while

being in transit. As result, when selling on Amazon, business must still keep a check

on inventory and ensure that their product doesn't face inadequacy of inventory owing to

Amazon's stocks control. Similar problems occur for Platform in terms of personalized styling,

Amazon in terms of architecture and design, but almost every other site in any manner.

Business would have the independence and versatility to do whatever they want whether run

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

their own stock or layout of business own website. Though customization can require additional

time and effort own platform is much more flexible than Amazon alternative. Since it's your

page, you have full power of everything from the text to the interface to the location of icon.

Business will have power of more than just the show and be able to pick how, whenever, and

where they present their items. Unlike Amazon, the business's own website is entirely dedicated

to business. Customers would be less distracted if business use their own website the go-to spot

for them to order from them. Since the web visitor can only be introduced to your goods, there

are no options like others viewed this and today's offer (Cescon, Costantini and Grassetti, 2019).

Based on overall analysis this has been recommended to respective company that it

should first prefer own website but use of Amazon’s platform will help to grow business more in

long term. Thus, business should adopt both alternatives as practicable. But quantitative analysis

shows that business should go for setup their own-online shop.

CONCLUSION

From the study this has been articulated that management accounting is crucial aspect which

covers all the key aspects of business like accounting, finance, management etc. MA helps to

define each operational and managerial task of business. This provide an assistive framework for

business executives to take effective decisions. As in given case study, MA approach helped in

analysis of decision of business to go for their own online shop or use amazon website.

10

time and effort own platform is much more flexible than Amazon alternative. Since it's your

page, you have full power of everything from the text to the interface to the location of icon.

Business will have power of more than just the show and be able to pick how, whenever, and

where they present their items. Unlike Amazon, the business's own website is entirely dedicated

to business. Customers would be less distracted if business use their own website the go-to spot

for them to order from them. Since the web visitor can only be introduced to your goods, there

are no options like others viewed this and today's offer (Cescon, Costantini and Grassetti, 2019).

Based on overall analysis this has been recommended to respective company that it

should first prefer own website but use of Amazon’s platform will help to grow business more in

long term. Thus, business should adopt both alternatives as practicable. But quantitative analysis

shows that business should go for setup their own-online shop.

CONCLUSION

From the study this has been articulated that management accounting is crucial aspect which

covers all the key aspects of business like accounting, finance, management etc. MA helps to

define each operational and managerial task of business. This provide an assistive framework for

business executives to take effective decisions. As in given case study, MA approach helped in

analysis of decision of business to go for their own online shop or use amazon website.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journal:

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting, 2019(3), p.2.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management, 2(1), p.02.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems, 29, pp.37-58.

Allain, E., Lemaire, C. and Lux, G., 2021. Managers' subtle resistance to neoliberal reforms

through and by means of management accounting. Accounting, Auditing &

Accountability Journal.

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований, (2).

Zyznarska-Dworczak, B., 2018. The development perspectives of sustainable management

accounting in central and Eastern European countries. Sustainability, 10(5), p.1445.

Pelz, M., 2019. Can management accounting Be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management

Reviews, 21(2), pp.256-274.

Bedford, D.S. and Speklé, R.F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting

Research, 30(2), pp.23-58.

Cescon, F., Costantini, A. and Grassetti, L., 2019. Strategic choices and strategic management

accounting in large manufacturing firms. Journal of Management and

Governance, 23(3), pp.605-636.

Hariyati, H., Tjahjadi, B. and Soewarno, N., 2019. The mediating effect of intellectual capital,

management accounting information systems, internal process performance, and

customer performance. International Journal of Productivity and Performance

Management.

11

Books and Journal:

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting, 2019(3), p.2.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management, 2(1), p.02.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems, 29, pp.37-58.

Allain, E., Lemaire, C. and Lux, G., 2021. Managers' subtle resistance to neoliberal reforms

through and by means of management accounting. Accounting, Auditing &

Accountability Journal.

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований, (2).

Zyznarska-Dworczak, B., 2018. The development perspectives of sustainable management

accounting in central and Eastern European countries. Sustainability, 10(5), p.1445.

Pelz, M., 2019. Can management accounting Be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management

Reviews, 21(2), pp.256-274.

Bedford, D.S. and Speklé, R.F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting

Research, 30(2), pp.23-58.

Cescon, F., Costantini, A. and Grassetti, L., 2019. Strategic choices and strategic management

accounting in large manufacturing firms. Journal of Management and

Governance, 23(3), pp.605-636.

Hariyati, H., Tjahjadi, B. and Soewarno, N., 2019. The mediating effect of intellectual capital,

management accounting information systems, internal process performance, and

customer performance. International Journal of Productivity and Performance

Management.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.