Kaplan Business School FINM4000: Finance Individual Assignment

VerifiedAdded on 2022/08/16

|14

|2739

|13

Homework Assignment

AI Summary

This assignment analyzes Amazon's financial performance based on its annual reports and working capital management. It examines Amazon's cash conversion cycle, free cash flow, and the advantages and disadvantages of debt and equity financing. The solution includes calculations for cash flow, net present value (NPV), internal rate of return (IRR), and discounted payback period. It also assesses the financial risks faced by the company, including competition and data security. Furthermore, the assignment provides calculations for bond valuation and holding period return, concluding with a discussion on the project's feasibility based on discounted payback period. The analysis utilizes financial data to evaluate Amazon's performance and investment potential, offering insights into its financial strategies and risk management.

CORPORATE FINANCE 1

CORPORATE

FINANCE

CORPORATE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 2

Part A:

Part 1:

As per the source 2, the cash conversion cycle of Walmart is in single digits whereas in the

case of Amazon, the same was -30.6 days. The company has a free cash flow available in its

hands. Hence, in the case of the business, the free cash flow would remain positive when the

customers pay their dues quickly. The company is able to repay its suppliers and manage its

inventory efficiently. If the company has a negative cash conversion cycle, then it merely

means that the company requires a lesser amount of time in order to sell its inventory or to

produce the same from the raw materials. The company receives cash from the customers due

in time also that it is able to repay its suppliers for the raw materials that it has purchased.

The working capital like this is good since this means no blockage of capital in the business

(Soledea, 2020).

Part 2:

A negative cash conversion cycle would mean that the company has cash available cash in its

hand to use. All of this cash could be used for the purposes of financing the business

operations to ensure a continued growth for the company. Then the company does not need to

borrow funds from outside or issue stock. The company can keep on spending cash so as to

invest in new products and attack the new sectors and also upgrade new offerings. The

company would be able to experiment, launch new business, launch new products when it has

funds available with it which is possible through the working capital only.

Part 3:

The company operations could be financed either through debt or through equity.

The following are the advantages of using debt:

Through debt, the company is able to retain control over its finances. The lending

company does not intervene in the day to day business operations of the borrower

company (Small business chron, 2020).

The company pays interest on the amount borrowed which is liable for tax deduction.

Through debt, the company knows the exact and the precise amount of principal and

the interest which is payable at the end of each month. This helps in making the

budget much easy and also helps in making the financial plans.

Part A:

Part 1:

As per the source 2, the cash conversion cycle of Walmart is in single digits whereas in the

case of Amazon, the same was -30.6 days. The company has a free cash flow available in its

hands. Hence, in the case of the business, the free cash flow would remain positive when the

customers pay their dues quickly. The company is able to repay its suppliers and manage its

inventory efficiently. If the company has a negative cash conversion cycle, then it merely

means that the company requires a lesser amount of time in order to sell its inventory or to

produce the same from the raw materials. The company receives cash from the customers due

in time also that it is able to repay its suppliers for the raw materials that it has purchased.

The working capital like this is good since this means no blockage of capital in the business

(Soledea, 2020).

Part 2:

A negative cash conversion cycle would mean that the company has cash available cash in its

hand to use. All of this cash could be used for the purposes of financing the business

operations to ensure a continued growth for the company. Then the company does not need to

borrow funds from outside or issue stock. The company can keep on spending cash so as to

invest in new products and attack the new sectors and also upgrade new offerings. The

company would be able to experiment, launch new business, launch new products when it has

funds available with it which is possible through the working capital only.

Part 3:

The company operations could be financed either through debt or through equity.

The following are the advantages of using debt:

Through debt, the company is able to retain control over its finances. The lending

company does not intervene in the day to day business operations of the borrower

company (Small business chron, 2020).

The company pays interest on the amount borrowed which is liable for tax deduction.

Through debt, the company knows the exact and the precise amount of principal and

the interest which is payable at the end of each month. This helps in making the

budget much easy and also helps in making the financial plans.

CORPORATE FINANCE 3

The following are the disadvantages of financing through debt:

The company should have a credit rating before borrowing money from outside.

The company will be required to maintain a good financial discipline so that the

repayments of the capital and interest is made on time. When the company has only

debt invested into his business, then it is assumed to be at a more risk since it is prone

to fluctuating interest rates and this also, limits the access to equity financing by the

company at a certain point of time.

When taking loan, the company will have to provide a collateral to the lender. This

could lead to putting some business assets of the company at some risk which could

affect the company operations (the hart ford, 2020).

The following are the advantages of equity financing:

The equity raised is committed for some business operations and also for the intended

projects. The investors know that their hard money is doing well through the changes

in the share price in the stock market.

The company shall not have to keep incurring costs of the servicing banks or the debt

finance which allows the company to use the capital for the business activities.

The investors that invest into the business help the business in delivering value and

helps in the exploring and executing and undertaking new business expansions and

growth ideas.

The investors are somehow prepared to provide the follow up funding of the business

as it grows (Ni business info, 2020).

The following are the disadvantages of equity financing:

The process of raising capital is demanding, is very costly and also time consuming

and this may take up more time of the management due to which the management’s

focus may go hay wire.

The investors that invest into the business does background check of the companies in

which they invest their money into. They assess the past results, information about the

company and invest their money.

The management losses a certain power when they make they decide to raise funds

through equity.

The company will have to provide some regular information to the investor in return

for their money invested into the business.

The following are the disadvantages of financing through debt:

The company should have a credit rating before borrowing money from outside.

The company will be required to maintain a good financial discipline so that the

repayments of the capital and interest is made on time. When the company has only

debt invested into his business, then it is assumed to be at a more risk since it is prone

to fluctuating interest rates and this also, limits the access to equity financing by the

company at a certain point of time.

When taking loan, the company will have to provide a collateral to the lender. This

could lead to putting some business assets of the company at some risk which could

affect the company operations (the hart ford, 2020).

The following are the advantages of equity financing:

The equity raised is committed for some business operations and also for the intended

projects. The investors know that their hard money is doing well through the changes

in the share price in the stock market.

The company shall not have to keep incurring costs of the servicing banks or the debt

finance which allows the company to use the capital for the business activities.

The investors that invest into the business help the business in delivering value and

helps in the exploring and executing and undertaking new business expansions and

growth ideas.

The investors are somehow prepared to provide the follow up funding of the business

as it grows (Ni business info, 2020).

The following are the disadvantages of equity financing:

The process of raising capital is demanding, is very costly and also time consuming

and this may take up more time of the management due to which the management’s

focus may go hay wire.

The investors that invest into the business does background check of the companies in

which they invest their money into. They assess the past results, information about the

company and invest their money.

The management losses a certain power when they make they decide to raise funds

through equity.

The company will have to provide some regular information to the investor in return

for their money invested into the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 4

There are some legal and regulatory issues which have to be complied with when

raising finance (E finance management, 2020).

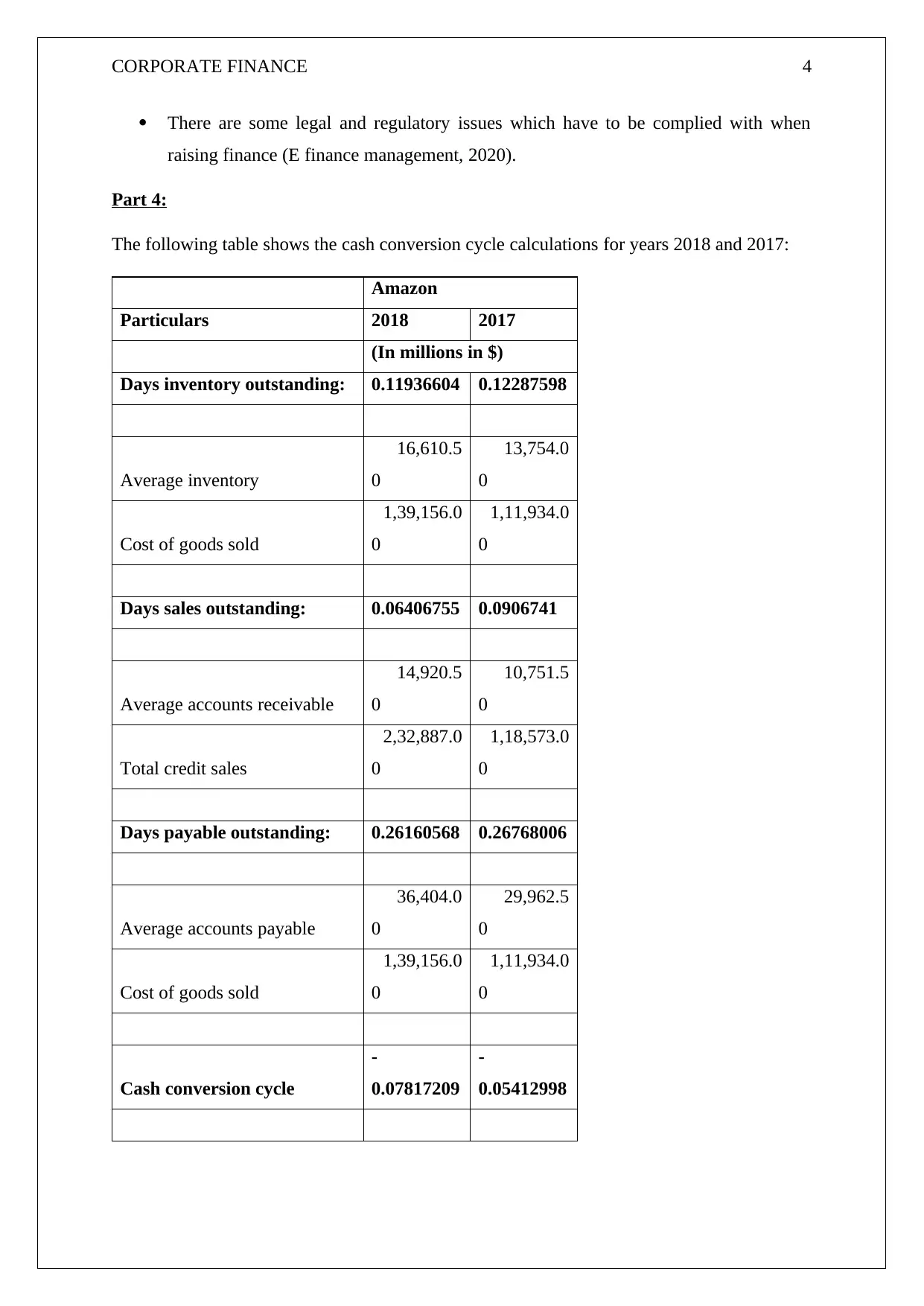

Part 4:

The following table shows the cash conversion cycle calculations for years 2018 and 2017:

Amazon

Particulars 2018 2017

(In millions in $)

Days inventory outstanding: 0.11936604 0.12287598

Average inventory

16,610.5

0

13,754.0

0

Cost of goods sold

1,39,156.0

0

1,11,934.0

0

Days sales outstanding: 0.06406755 0.0906741

Average accounts receivable

14,920.5

0

10,751.5

0

Total credit sales

2,32,887.0

0

1,18,573.0

0

Days payable outstanding: 0.26160568 0.26768006

Average accounts payable

36,404.0

0

29,962.5

0

Cost of goods sold

1,39,156.0

0

1,11,934.0

0

Cash conversion cycle

-

0.07817209

-

0.05412998

There are some legal and regulatory issues which have to be complied with when

raising finance (E finance management, 2020).

Part 4:

The following table shows the cash conversion cycle calculations for years 2018 and 2017:

Amazon

Particulars 2018 2017

(In millions in $)

Days inventory outstanding: 0.11936604 0.12287598

Average inventory

16,610.5

0

13,754.0

0

Cost of goods sold

1,39,156.0

0

1,11,934.0

0

Days sales outstanding: 0.06406755 0.0906741

Average accounts receivable

14,920.5

0

10,751.5

0

Total credit sales

2,32,887.0

0

1,18,573.0

0

Days payable outstanding: 0.26160568 0.26768006

Average accounts payable

36,404.0

0

29,962.5

0

Cost of goods sold

1,39,156.0

0

1,11,934.0

0

Cash conversion cycle

-

0.07817209

-

0.05412998

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

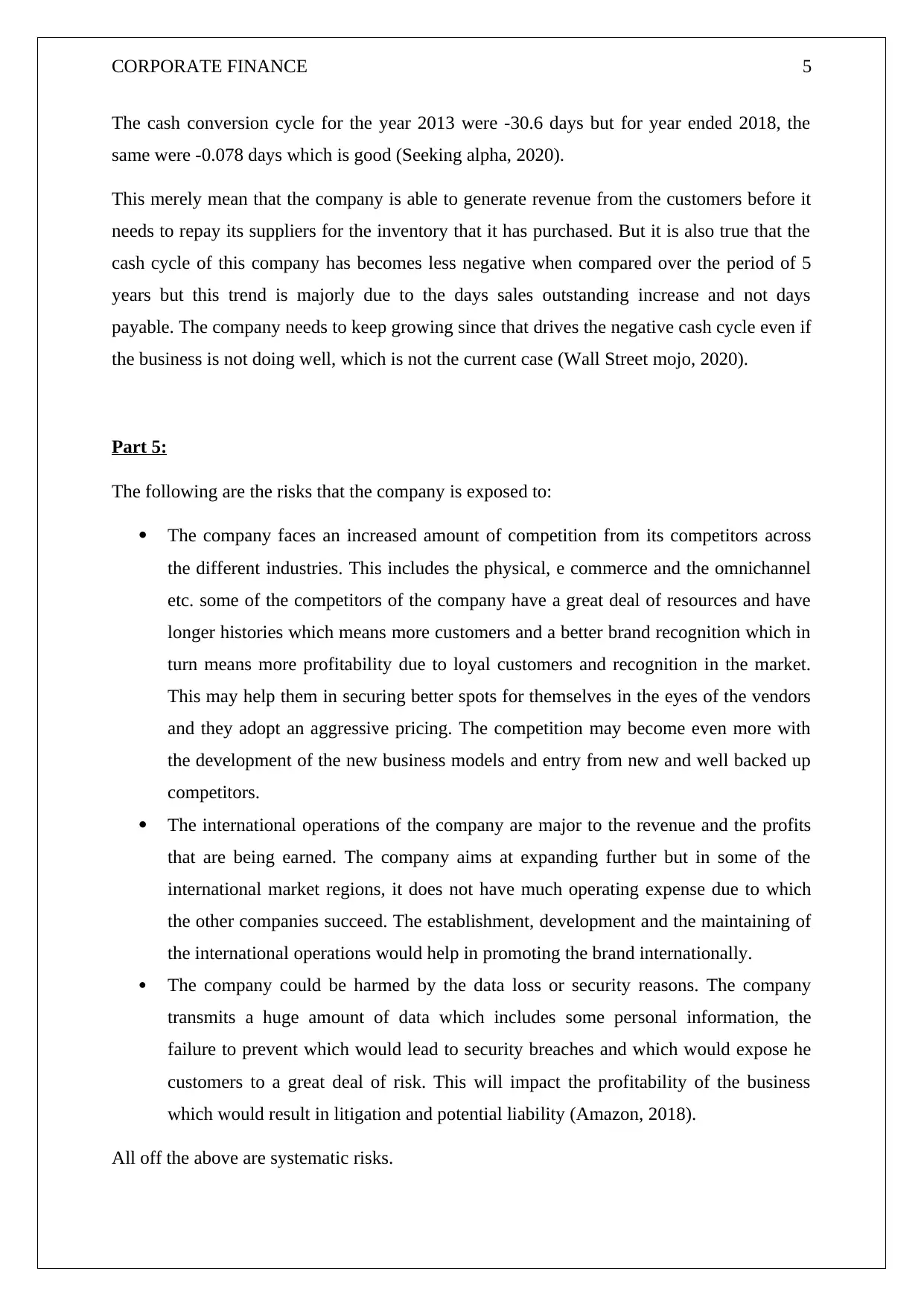

CORPORATE FINANCE 5

The cash conversion cycle for the year 2013 were -30.6 days but for year ended 2018, the

same were -0.078 days which is good (Seeking alpha, 2020).

This merely mean that the company is able to generate revenue from the customers before it

needs to repay its suppliers for the inventory that it has purchased. But it is also true that the

cash cycle of this company has becomes less negative when compared over the period of 5

years but this trend is majorly due to the days sales outstanding increase and not days

payable. The company needs to keep growing since that drives the negative cash cycle even if

the business is not doing well, which is not the current case (Wall Street mojo, 2020).

Part 5:

The following are the risks that the company is exposed to:

The company faces an increased amount of competition from its competitors across

the different industries. This includes the physical, e commerce and the omnichannel

etc. some of the competitors of the company have a great deal of resources and have

longer histories which means more customers and a better brand recognition which in

turn means more profitability due to loyal customers and recognition in the market.

This may help them in securing better spots for themselves in the eyes of the vendors

and they adopt an aggressive pricing. The competition may become even more with

the development of the new business models and entry from new and well backed up

competitors.

The international operations of the company are major to the revenue and the profits

that are being earned. The company aims at expanding further but in some of the

international market regions, it does not have much operating expense due to which

the other companies succeed. The establishment, development and the maintaining of

the international operations would help in promoting the brand internationally.

The company could be harmed by the data loss or security reasons. The company

transmits a huge amount of data which includes some personal information, the

failure to prevent which would lead to security breaches and which would expose he

customers to a great deal of risk. This will impact the profitability of the business

which would result in litigation and potential liability (Amazon, 2018).

All off the above are systematic risks.

The cash conversion cycle for the year 2013 were -30.6 days but for year ended 2018, the

same were -0.078 days which is good (Seeking alpha, 2020).

This merely mean that the company is able to generate revenue from the customers before it

needs to repay its suppliers for the inventory that it has purchased. But it is also true that the

cash cycle of this company has becomes less negative when compared over the period of 5

years but this trend is majorly due to the days sales outstanding increase and not days

payable. The company needs to keep growing since that drives the negative cash cycle even if

the business is not doing well, which is not the current case (Wall Street mojo, 2020).

Part 5:

The following are the risks that the company is exposed to:

The company faces an increased amount of competition from its competitors across

the different industries. This includes the physical, e commerce and the omnichannel

etc. some of the competitors of the company have a great deal of resources and have

longer histories which means more customers and a better brand recognition which in

turn means more profitability due to loyal customers and recognition in the market.

This may help them in securing better spots for themselves in the eyes of the vendors

and they adopt an aggressive pricing. The competition may become even more with

the development of the new business models and entry from new and well backed up

competitors.

The international operations of the company are major to the revenue and the profits

that are being earned. The company aims at expanding further but in some of the

international market regions, it does not have much operating expense due to which

the other companies succeed. The establishment, development and the maintaining of

the international operations would help in promoting the brand internationally.

The company could be harmed by the data loss or security reasons. The company

transmits a huge amount of data which includes some personal information, the

failure to prevent which would lead to security breaches and which would expose he

customers to a great deal of risk. This will impact the profitability of the business

which would result in litigation and potential liability (Amazon, 2018).

All off the above are systematic risks.

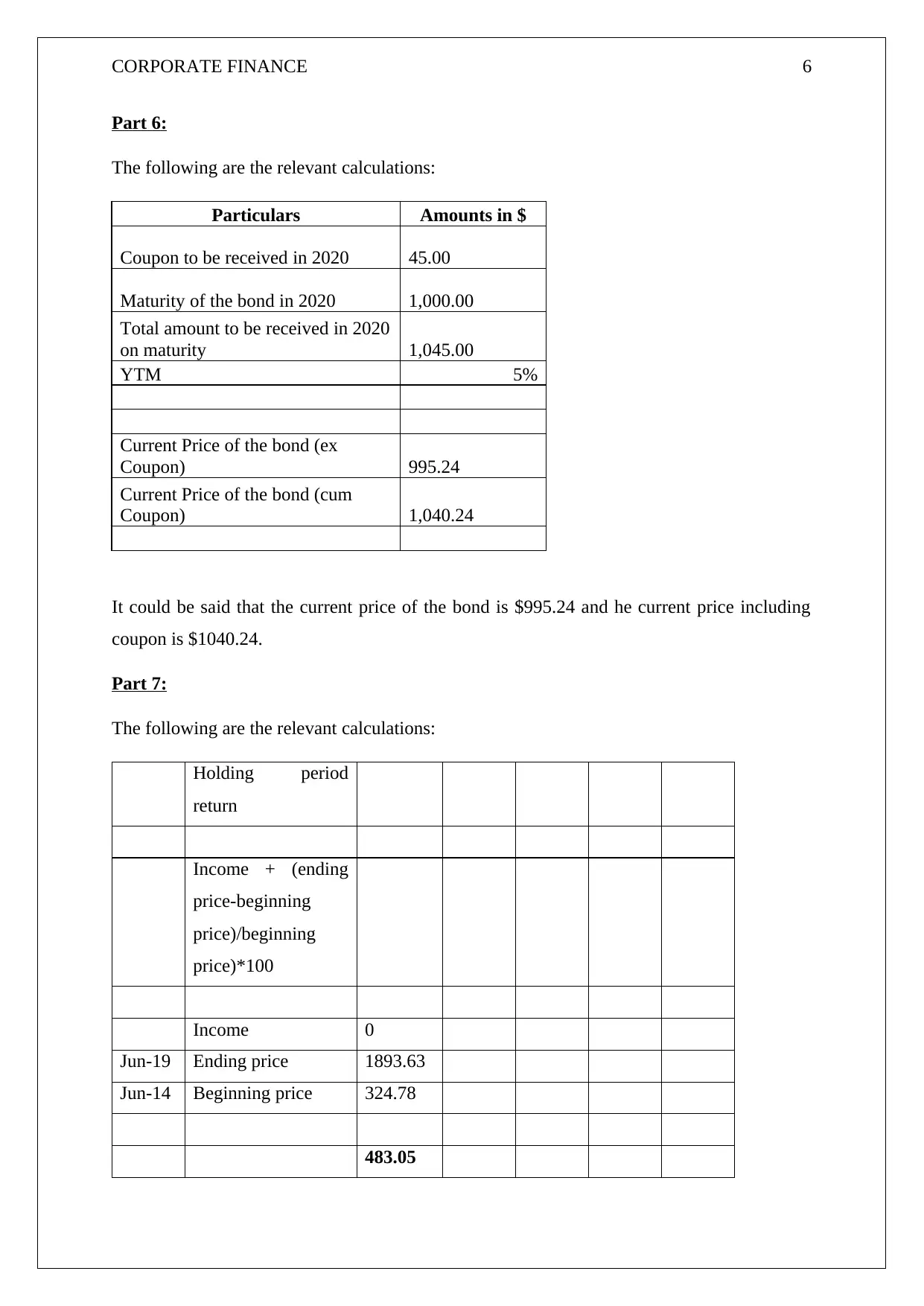

CORPORATE FINANCE 6

Part 6:

The following are the relevant calculations:

Particulars Amounts in $

Coupon to be received in 2020 45.00

Maturity of the bond in 2020 1,000.00

Total amount to be received in 2020

on maturity 1,045.00

YTM 5%

Current Price of the bond (ex

Coupon) 995.24

Current Price of the bond (cum

Coupon) 1,040.24

It could be said that the current price of the bond is $995.24 and he current price including

coupon is $1040.24.

Part 7:

The following are the relevant calculations:

Holding period

return

Income + (ending

price-beginning

price)/beginning

price)*100

Income 0

Jun-19 Ending price 1893.63

Jun-14 Beginning price 324.78

483.05

Part 6:

The following are the relevant calculations:

Particulars Amounts in $

Coupon to be received in 2020 45.00

Maturity of the bond in 2020 1,000.00

Total amount to be received in 2020

on maturity 1,045.00

YTM 5%

Current Price of the bond (ex

Coupon) 995.24

Current Price of the bond (cum

Coupon) 1,040.24

It could be said that the current price of the bond is $995.24 and he current price including

coupon is $1040.24.

Part 7:

The following are the relevant calculations:

Holding period

return

Income + (ending

price-beginning

price)/beginning

price)*100

Income 0

Jun-19 Ending price 1893.63

Jun-14 Beginning price 324.78

483.05

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 7

%

The holding period return comes out to be 483% which is very good and an investment into

the company should have been made.

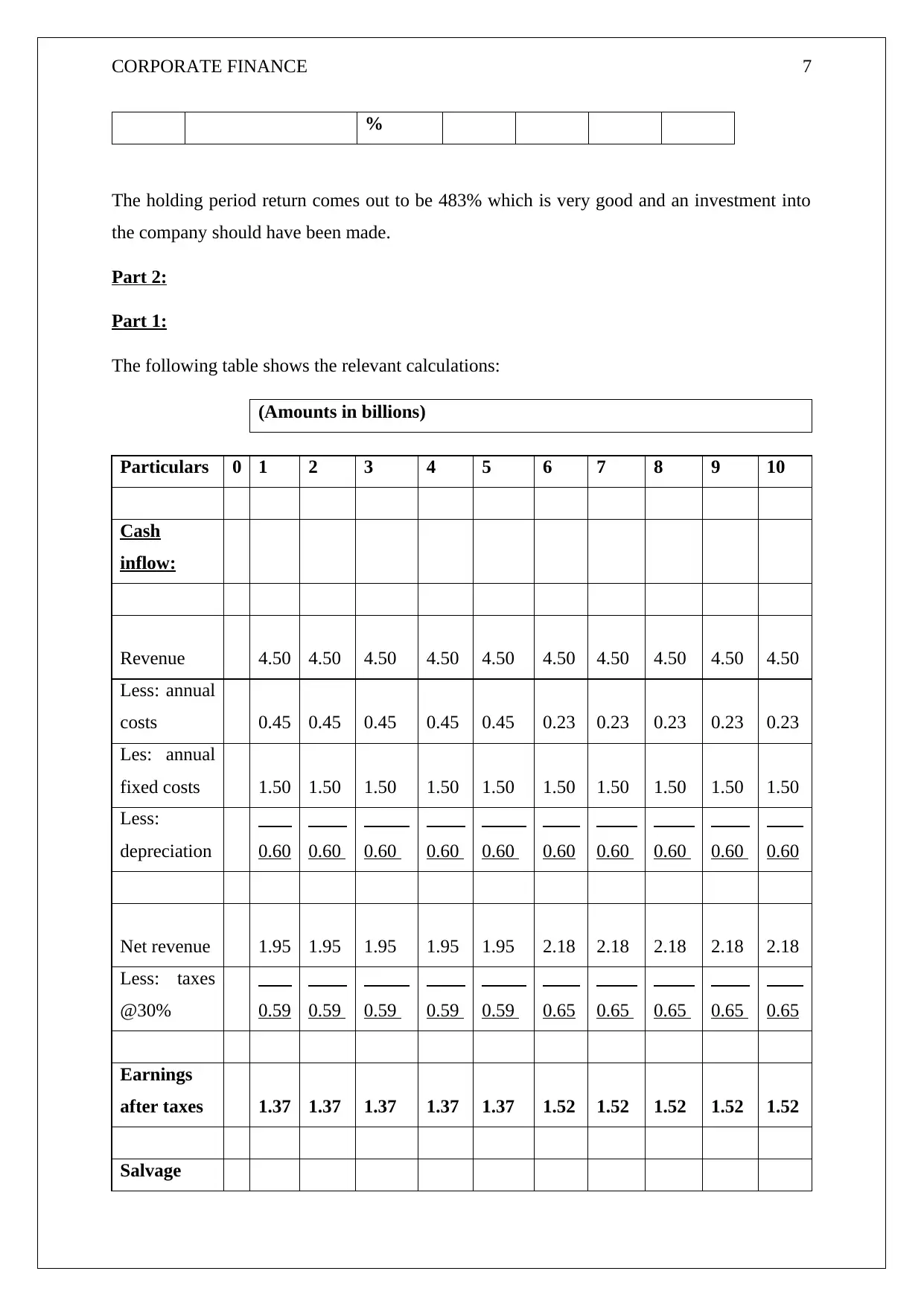

Part 2:

Part 1:

The following table shows the relevant calculations:

(Amounts in billions)

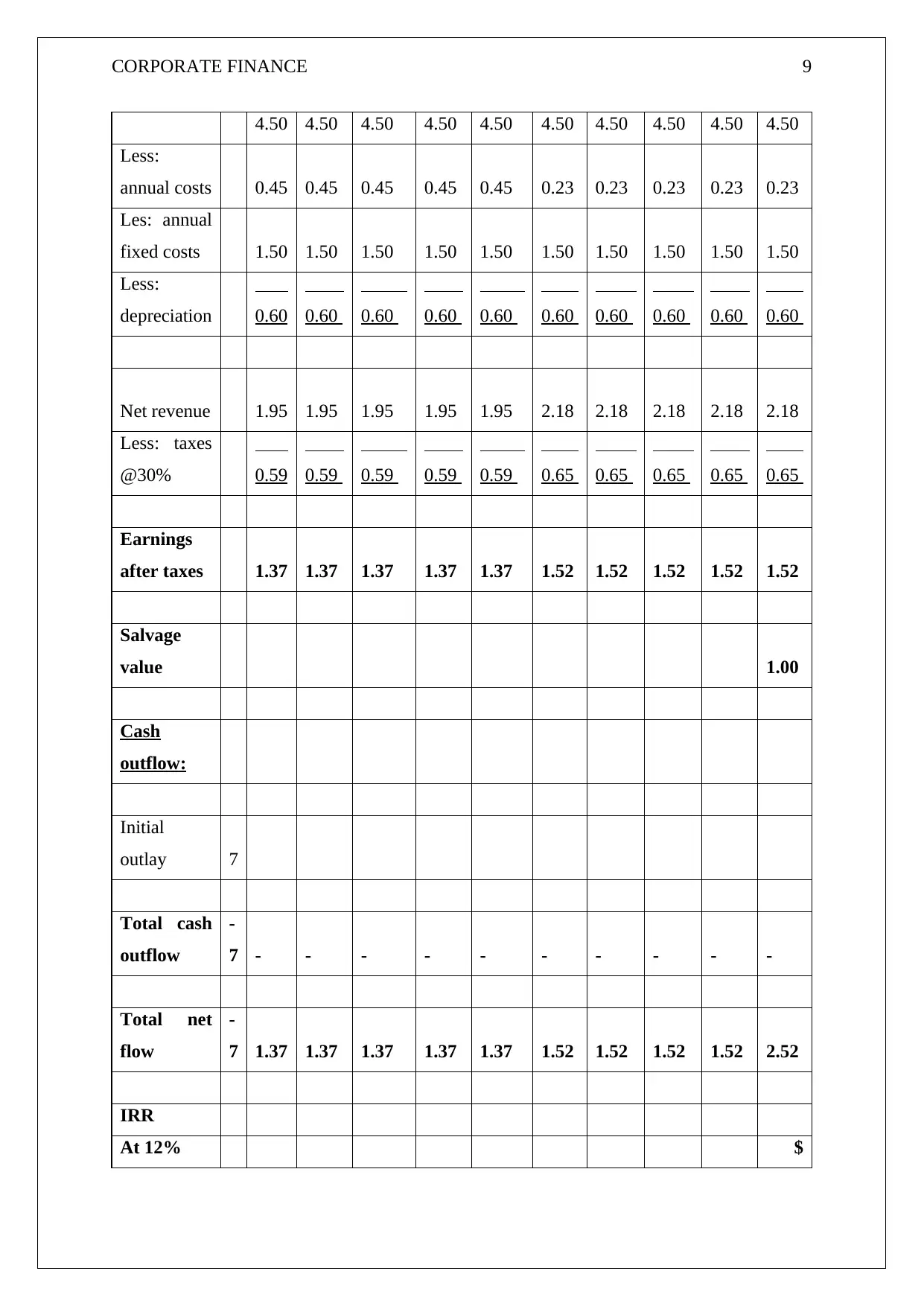

Particulars 0 1 2 3 4 5 6 7 8 9 10

Cash

inflow:

Revenue 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50

Less: annual

costs 0.45 0.45 0.45 0.45 0.45 0.23 0.23 0.23 0.23 0.23

Les: annual

fixed costs 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Less:

depreciation 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60

Net revenue 1.95 1.95 1.95 1.95 1.95 2.18 2.18 2.18 2.18 2.18

Less: taxes

@30% 0.59 0.59 0.59 0.59 0.59 0.65 0.65 0.65 0.65 0.65

Earnings

after taxes 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 1.52

Salvage

%

The holding period return comes out to be 483% which is very good and an investment into

the company should have been made.

Part 2:

Part 1:

The following table shows the relevant calculations:

(Amounts in billions)

Particulars 0 1 2 3 4 5 6 7 8 9 10

Cash

inflow:

Revenue 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50

Less: annual

costs 0.45 0.45 0.45 0.45 0.45 0.23 0.23 0.23 0.23 0.23

Les: annual

fixed costs 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Less:

depreciation 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60

Net revenue 1.95 1.95 1.95 1.95 1.95 2.18 2.18 2.18 2.18 2.18

Less: taxes

@30% 0.59 0.59 0.59 0.59 0.59 0.65 0.65 0.65 0.65 0.65

Earnings

after taxes 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 1.52

Salvage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

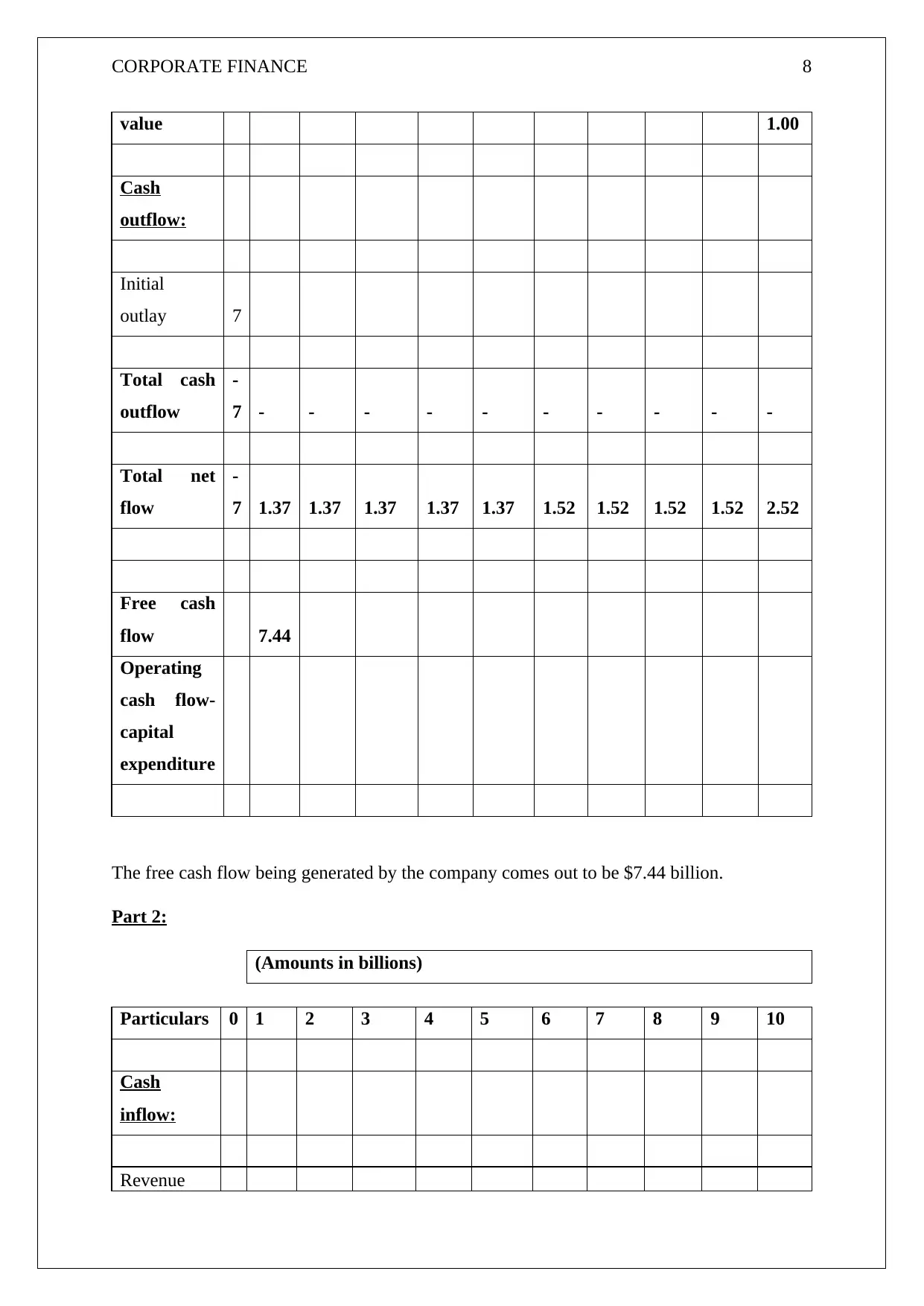

CORPORATE FINANCE 8

value 1.00

Cash

outflow:

Initial

outlay 7

Total cash

outflow

-

7 - - - - - - - - - -

Total net

flow

-

7 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 2.52

Free cash

flow 7.44

Operating

cash flow-

capital

expenditure

The free cash flow being generated by the company comes out to be $7.44 billion.

Part 2:

(Amounts in billions)

Particulars 0 1 2 3 4 5 6 7 8 9 10

Cash

inflow:

Revenue

value 1.00

Cash

outflow:

Initial

outlay 7

Total cash

outflow

-

7 - - - - - - - - - -

Total net

flow

-

7 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 2.52

Free cash

flow 7.44

Operating

cash flow-

capital

expenditure

The free cash flow being generated by the company comes out to be $7.44 billion.

Part 2:

(Amounts in billions)

Particulars 0 1 2 3 4 5 6 7 8 9 10

Cash

inflow:

Revenue

CORPORATE FINANCE 9

4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50

Less:

annual costs 0.45 0.45 0.45 0.45 0.45 0.23 0.23 0.23 0.23 0.23

Les: annual

fixed costs 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Less:

depreciation 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60

Net revenue 1.95 1.95 1.95 1.95 1.95 2.18 2.18 2.18 2.18 2.18

Less: taxes

@30% 0.59 0.59 0.59 0.59 0.59 0.65 0.65 0.65 0.65 0.65

Earnings

after taxes 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 1.52

Salvage

value 1.00

Cash

outflow:

Initial

outlay 7

Total cash

outflow

-

7 - - - - - - - - - -

Total net

flow

-

7 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 2.52

IRR

At 12% $

4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50

Less:

annual costs 0.45 0.45 0.45 0.45 0.45 0.23 0.23 0.23 0.23 0.23

Les: annual

fixed costs 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Less:

depreciation 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60

Net revenue 1.95 1.95 1.95 1.95 1.95 2.18 2.18 2.18 2.18 2.18

Less: taxes

@30% 0.59 0.59 0.59 0.59 0.59 0.65 0.65 0.65 0.65 0.65

Earnings

after taxes 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 1.52

Salvage

value 1.00

Cash

outflow:

Initial

outlay 7

Total cash

outflow

-

7 - - - - - - - - - -

Total net

flow

-

7 1.37 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 2.52

IRR

At 12% $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 10

1.36

At 5%

$

4.69

The NPV comes out to be $1.36 billion at 12% discount rate and $4.69 billion at 5% discount

rate. Keeping in mind the speculative nature, the discount arte of 5% should be considered.

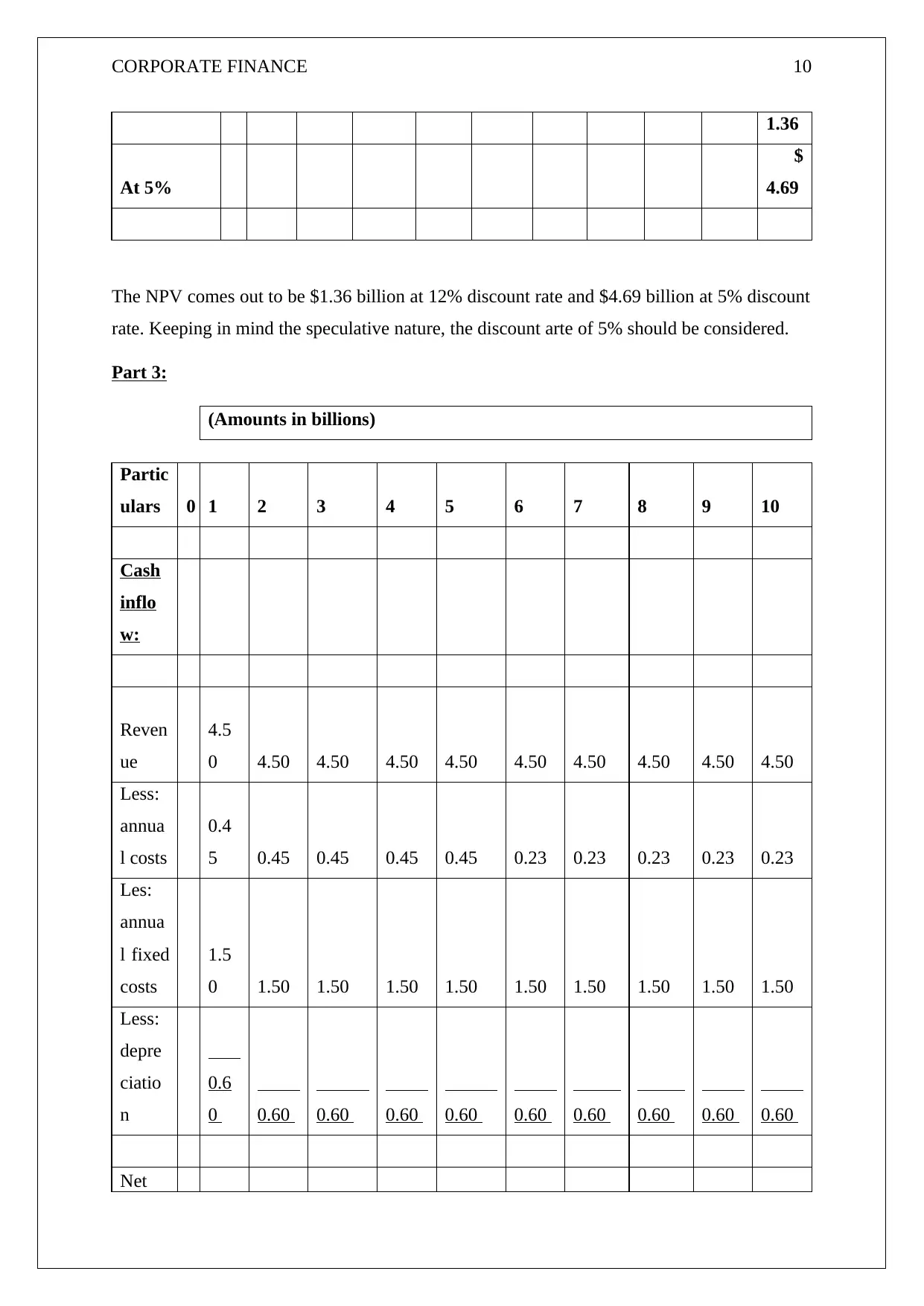

Part 3:

(Amounts in billions)

Partic

ulars 0 1 2 3 4 5 6 7 8 9 10

Cash

inflo

w:

Reven

ue

4.5

0 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50

Less:

annua

l costs

0.4

5 0.45 0.45 0.45 0.45 0.23 0.23 0.23 0.23 0.23

Les:

annua

l fixed

costs

1.5

0 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Less:

depre

ciatio

n

0.6

0 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60

Net

1.36

At 5%

$

4.69

The NPV comes out to be $1.36 billion at 12% discount rate and $4.69 billion at 5% discount

rate. Keeping in mind the speculative nature, the discount arte of 5% should be considered.

Part 3:

(Amounts in billions)

Partic

ulars 0 1 2 3 4 5 6 7 8 9 10

Cash

inflo

w:

Reven

ue

4.5

0 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50 4.50

Less:

annua

l costs

0.4

5 0.45 0.45 0.45 0.45 0.23 0.23 0.23 0.23 0.23

Les:

annua

l fixed

costs

1.5

0 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Less:

depre

ciatio

n

0.6

0 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60 0.60

Net

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 11

reven

ue

1.9

5 1.95 1.95 1.95 1.95 2.18 2.18 2.18 2.18 2.18

Less:

taxes

@30

%

0.5

9 0.59 0.59 0.59 0.59 0.65 0.65 0.65 0.65 0.65

Earni

ngs

after

taxes

1.3

7 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 1.52

Salva

ge

value 1.00

Cash

outflo

w:

Initial

outlay 7

Total

cash

outflo

w

-

7 - - - - - - - - - -

Total

net

flow

-

7

1.3

7 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 2.52

Disco

unted

reven

ue

1.9

5 1.95 1.95 1.95 1.95 2.18 2.18 2.18 2.18 2.18

Less:

taxes

@30

%

0.5

9 0.59 0.59 0.59 0.59 0.65 0.65 0.65 0.65 0.65

Earni

ngs

after

taxes

1.3

7 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 1.52

Salva

ge

value 1.00

Cash

outflo

w:

Initial

outlay 7

Total

cash

outflo

w

-

7 - - - - - - - - - -

Total

net

flow

-

7

1.3

7 1.37 1.37 1.37 1.37 1.52 1.52 1.52 1.52 2.52

Disco

unted

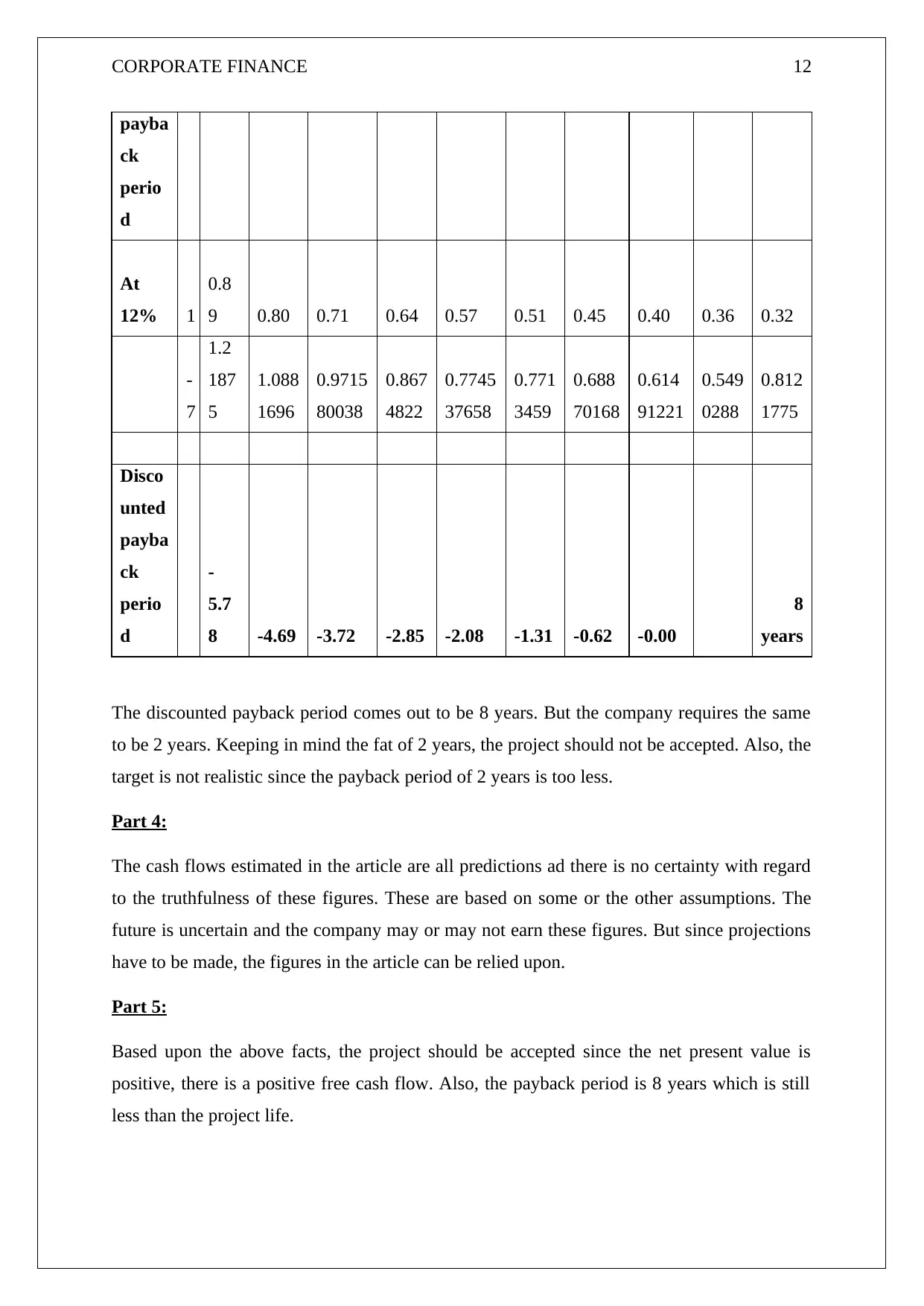

CORPORATE FINANCE 12

payba

ck

perio

d

At

12% 1

0.8

9 0.80 0.71 0.64 0.57 0.51 0.45 0.40 0.36 0.32

-

7

1.2

187

5

1.088

1696

0.9715

80038

0.867

4822

0.7745

37658

0.771

3459

0.688

70168

0.614

91221

0.549

0288

0.812

1775

Disco

unted

payba

ck

perio

d

-

5.7

8 -4.69 -3.72 -2.85 -2.08 -1.31 -0.62 -0.00

8

years

The discounted payback period comes out to be 8 years. But the company requires the same

to be 2 years. Keeping in mind the fat of 2 years, the project should not be accepted. Also, the

target is not realistic since the payback period of 2 years is too less.

Part 4:

The cash flows estimated in the article are all predictions ad there is no certainty with regard

to the truthfulness of these figures. These are based on some or the other assumptions. The

future is uncertain and the company may or may not earn these figures. But since projections

have to be made, the figures in the article can be relied upon.

Part 5:

Based upon the above facts, the project should be accepted since the net present value is

positive, there is a positive free cash flow. Also, the payback period is 8 years which is still

less than the project life.

payba

ck

perio

d

At

12% 1

0.8

9 0.80 0.71 0.64 0.57 0.51 0.45 0.40 0.36 0.32

-

7

1.2

187

5

1.088

1696

0.9715

80038

0.867

4822

0.7745

37658

0.771

3459

0.688

70168

0.614

91221

0.549

0288

0.812

1775

Disco

unted

payba

ck

perio

d

-

5.7

8 -4.69 -3.72 -2.85 -2.08 -1.31 -0.62 -0.00

8

years

The discounted payback period comes out to be 8 years. But the company requires the same

to be 2 years. Keeping in mind the fat of 2 years, the project should not be accepted. Also, the

target is not realistic since the payback period of 2 years is too less.

Part 4:

The cash flows estimated in the article are all predictions ad there is no certainty with regard

to the truthfulness of these figures. These are based on some or the other assumptions. The

future is uncertain and the company may or may not earn these figures. But since projections

have to be made, the figures in the article can be relied upon.

Part 5:

Based upon the above facts, the project should be accepted since the net present value is

positive, there is a positive free cash flow. Also, the payback period is 8 years which is still

less than the project life.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.