Financial Statement Analysis of Amcor Corporation: A Detailed Report

VerifiedAdded on 2024/06/03

|9

|2373

|109

Report

AI Summary

This report provides a detailed financial analysis of Amcor Corporation from 2015 to 2017, focusing on the cash flow statement, other comprehensive income (OCI), and corporate tax. The cash flow analysis reveals trends in operating, investing, and financing activities, highlighting key receipts and payments. The OCI analysis examines exchange differences and their impact. The corporate tax calculation reconciles the reported income tax expense with the expected tax based on profit before tax, exploring deferred tax implications and adjustments. The analysis uses data sourced directly from Amcor's annual reports to provide a comprehensive overview of the company's financial performance during the specified period. Desklib offers a range of study tools, including solved assignments, to assist students in their academic pursuits.

Table of Contents

Introduction.................................................................................................................................................2

Significant analysis of Cash flow statement for Amcor...............................................................................2

Critical analysis of OCI...............................................................................................................................6

Calculation of Corporate tax........................................................................................................................7

References...................................................................................................................................................9

Introduction.................................................................................................................................................2

Significant analysis of Cash flow statement for Amcor...............................................................................2

Critical analysis of OCI...............................................................................................................................6

Calculation of Corporate tax........................................................................................................................7

References...................................................................................................................................................9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

This task is focused to understand and apprehend the annual report of a chosen company which

is listed in Ausralian stock exchange, the student has to source the annual report of the company

for a period of 3 years from 2015 to 2017 and then perform a detailed analysis using them. The

analysis is focused to present in detail the cash flow statement of the company and a comparative

analysis for those 3 years, the next part of the analysis is to perform an anlysis on the other

comprehensive income of the company and its impact in the income statement and then the last

task is to understand the income tax expense of the company and the tax paid by the

company.The company which is chosen for the study is Amcor Corporation, which is a leading

packaging company around the world, the company produces various packages, container and

custom made cartoons for various industries which includes food & beverages, medical aspects,

home care, personal care, beverages etc. The company has its head office in Victoria and

operates around the world, moreover the company employs more than 35,000 people and posted

revenue of more than 8.5 billion in sales.

Significant analysis of Cash flow statement for Amcor

.

The cash flow statement shall be treated as a full balance sheet and statement of financial

position account. The cash flow statement can be classified into categories such as cash flow

from operations, cash flow from investing activities, cash flow from financing activities and cash

flows. train. The main purpose of the cash flow statement is to provide more information and

information on total revenues and payments over a period of time, usually one year. This

statement helps the company understand the company's overall liquidity, evaluates periodic

credit quality, predicts future cash flows and seeks resources. The most important components of

the cash flow statement are mainly based on accounting resources based on comparisons

between revenue and expenses. (Brealy, 2011). It should be noted that the cash flow statement

contains only funds and cash funds that have been released. These statements generally exclude a

transaction that does not include money. The cash flow analysis generally differentiates the

company's liquidity funds and their uses during the three-year period: cash flow from operating

activities, cash flow from investing activities and cash flow from operations. cash flow related to

financing activities.

Based on the analysis of the cash flow statement of the company, it is noted that the opening

balance of cash as of 2015 is 505 million whereas it was 697 million in 2016 and in 2017 the

opening balance of cash was 513 million.

Cash from operating activities:

This task is focused to understand and apprehend the annual report of a chosen company which

is listed in Ausralian stock exchange, the student has to source the annual report of the company

for a period of 3 years from 2015 to 2017 and then perform a detailed analysis using them. The

analysis is focused to present in detail the cash flow statement of the company and a comparative

analysis for those 3 years, the next part of the analysis is to perform an anlysis on the other

comprehensive income of the company and its impact in the income statement and then the last

task is to understand the income tax expense of the company and the tax paid by the

company.The company which is chosen for the study is Amcor Corporation, which is a leading

packaging company around the world, the company produces various packages, container and

custom made cartoons for various industries which includes food & beverages, medical aspects,

home care, personal care, beverages etc. The company has its head office in Victoria and

operates around the world, moreover the company employs more than 35,000 people and posted

revenue of more than 8.5 billion in sales.

Significant analysis of Cash flow statement for Amcor

.

The cash flow statement shall be treated as a full balance sheet and statement of financial

position account. The cash flow statement can be classified into categories such as cash flow

from operations, cash flow from investing activities, cash flow from financing activities and cash

flows. train. The main purpose of the cash flow statement is to provide more information and

information on total revenues and payments over a period of time, usually one year. This

statement helps the company understand the company's overall liquidity, evaluates periodic

credit quality, predicts future cash flows and seeks resources. The most important components of

the cash flow statement are mainly based on accounting resources based on comparisons

between revenue and expenses. (Brealy, 2011). It should be noted that the cash flow statement

contains only funds and cash funds that have been released. These statements generally exclude a

transaction that does not include money. The cash flow analysis generally differentiates the

company's liquidity funds and their uses during the three-year period: cash flow from operating

activities, cash flow from investing activities and cash flow from operations. cash flow related to

financing activities.

Based on the analysis of the cash flow statement of the company, it is noted that the opening

balance of cash as of 2015 is 505 million whereas it was 697 million in 2016 and in 2017 the

opening balance of cash was 513 million.

Cash from operating activities:

The cash from operating activities in the year 2015 was 1,002 million but it raised to 1,099

million in 2016 and in 2017 the overall cash from operating activities stood at 1,027 million.

(Amcor, 2017)

The main cash receipts of the company was from net profits generated by the business, this was

around 707 million in 2015, but in 2016 the profit reduced to a level of 273 million in 2016 but

in 2017 the profits increased to 614 million. The net finance cost is a higher expense which has

been identified in the operating activities, this is nearly 169 million in 2015, 167 million in 2016

and 187 million in 2017, this shows that the finance cost has increased from 2016 to 2017. The

depreciation and amortisation losses were around 376 million in 2015, increased to 390 million

in 2016 and reduced to a level of 387 million in 2017.

2015 2016 2017

Cash flow from the overall operating activities 1002.3 1099.4 1027.4

2015 2016 2017

940

960

980

1000

1020

1040

1060

1080

1100

1120

Cash flow from the overall operating

activities

Cash flow from the overall

operating activities

Cash from investing activities

The next part is to analyse the cash employed by the business through the investing activities, the

overall cash applied by the business in the investment activities is 335 million in 2015, 997

million in 2016 and decreased to a few level to 632.6 million.

The major investment was made to a level of 323 million in 2015 this has increased to 349

million in 2016 and increased to 379 million in 2017, the next part noted is that the business paid

for the acquisition of various controlled entities etc. the invested amount was around 98 million

in 2015, increased investment spending to a level of 498 million in 2016 and decreased to a level

of 336 million in 2017. The next aspect considered in the investment activities is the proceeds

million in 2016 and in 2017 the overall cash from operating activities stood at 1,027 million.

(Amcor, 2017)

The main cash receipts of the company was from net profits generated by the business, this was

around 707 million in 2015, but in 2016 the profit reduced to a level of 273 million in 2016 but

in 2017 the profits increased to 614 million. The net finance cost is a higher expense which has

been identified in the operating activities, this is nearly 169 million in 2015, 167 million in 2016

and 187 million in 2017, this shows that the finance cost has increased from 2016 to 2017. The

depreciation and amortisation losses were around 376 million in 2015, increased to 390 million

in 2016 and reduced to a level of 387 million in 2017.

2015 2016 2017

Cash flow from the overall operating activities 1002.3 1099.4 1027.4

2015 2016 2017

940

960

980

1000

1020

1040

1060

1080

1100

1120

Cash flow from the overall operating

activities

Cash flow from the overall

operating activities

Cash from investing activities

The next part is to analyse the cash employed by the business through the investing activities, the

overall cash applied by the business in the investment activities is 335 million in 2015, 997

million in 2016 and decreased to a few level to 632.6 million.

The major investment was made to a level of 323 million in 2015 this has increased to 349

million in 2016 and increased to 379 million in 2017, the next part noted is that the business paid

for the acquisition of various controlled entities etc. the invested amount was around 98 million

in 2015, increased investment spending to a level of 498 million in 2016 and decreased to a level

of 336 million in 2017. The next aspect considered in the investment activities is the proceeds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generate from the sale of assets which was 83 million in 2015 decreased in the year 2016 to a

level of 30 million and again increased to 82 million in 2016

2015 2016 2017

Cash flow from the overall Investment activities 335 997 633

2015 2016 2017

0

200

400

600

800

1000

1200

Cash flow from the overall

Investment activities

Cash flow from the overall

Investment activities

Cash from financing activities

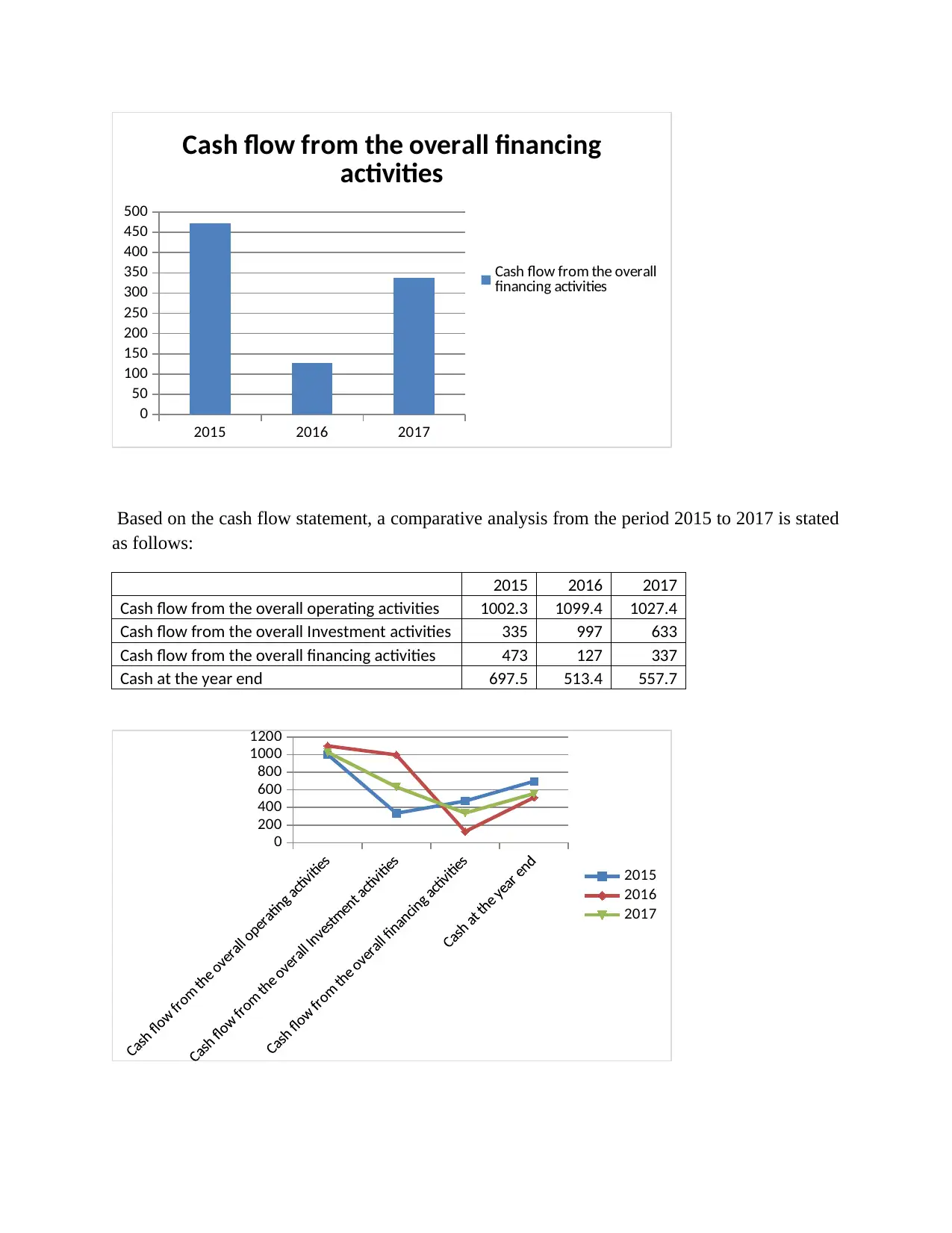

The company has possessed the net cash from the financing activities to a tune of 473 million in

2015, decreased to a level of 126 million in 2016 and raised again to a level of 337 million.

The company has sourced the capital through the issue of shares for 46 million in 2015, the

proceeds from sale was 39.5 million and decreased again in 2017 to a level of 23.8 million. The

management has decided to purchase the share in the market which was around 343 million in

2015, this has been in the level of 296 million in 2016 and reduced to 43.6 million in 2017. The

company made repayment on the borrowings which was around 5,698 million in 2015, similarly

an equal amount of 5,036 million in 2016 and this has reduced to 3,745 million in 2017.

2015 2016 2017

Cash flow from the overall financing activities 473 127 337

level of 30 million and again increased to 82 million in 2016

2015 2016 2017

Cash flow from the overall Investment activities 335 997 633

2015 2016 2017

0

200

400

600

800

1000

1200

Cash flow from the overall

Investment activities

Cash flow from the overall

Investment activities

Cash from financing activities

The company has possessed the net cash from the financing activities to a tune of 473 million in

2015, decreased to a level of 126 million in 2016 and raised again to a level of 337 million.

The company has sourced the capital through the issue of shares for 46 million in 2015, the

proceeds from sale was 39.5 million and decreased again in 2017 to a level of 23.8 million. The

management has decided to purchase the share in the market which was around 343 million in

2015, this has been in the level of 296 million in 2016 and reduced to 43.6 million in 2017. The

company made repayment on the borrowings which was around 5,698 million in 2015, similarly

an equal amount of 5,036 million in 2016 and this has reduced to 3,745 million in 2017.

2015 2016 2017

Cash flow from the overall financing activities 473 127 337

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 2016 2017

0

50

100

150

200

250

300

350

400

450

500

Cash flow from the overall financing

activities

Cash flow from the overall

financing activities

Based on the cash flow statement, a comparative analysis from the period 2015 to 2017 is stated

as follows:

2015 2016 2017

Cash flow from the overall operating activities 1002.3 1099.4 1027.4

Cash flow from the overall Investment activities 335 997 633

Cash flow from the overall financing activities 473 127 337

Cash at the year end 697.5 513.4 557.7

0

200

400

600

800

1000

1200

2015

2016

2017

0

50

100

150

200

250

300

350

400

450

500

Cash flow from the overall financing

activities

Cash flow from the overall

financing activities

Based on the cash flow statement, a comparative analysis from the period 2015 to 2017 is stated

as follows:

2015 2016 2017

Cash flow from the overall operating activities 1002.3 1099.4 1027.4

Cash flow from the overall Investment activities 335 997 633

Cash flow from the overall financing activities 473 127 337

Cash at the year end 697.5 513.4 557.7

0

200

400

600

800

1000

1200

2015

2016

2017

Critical analysis of OCI

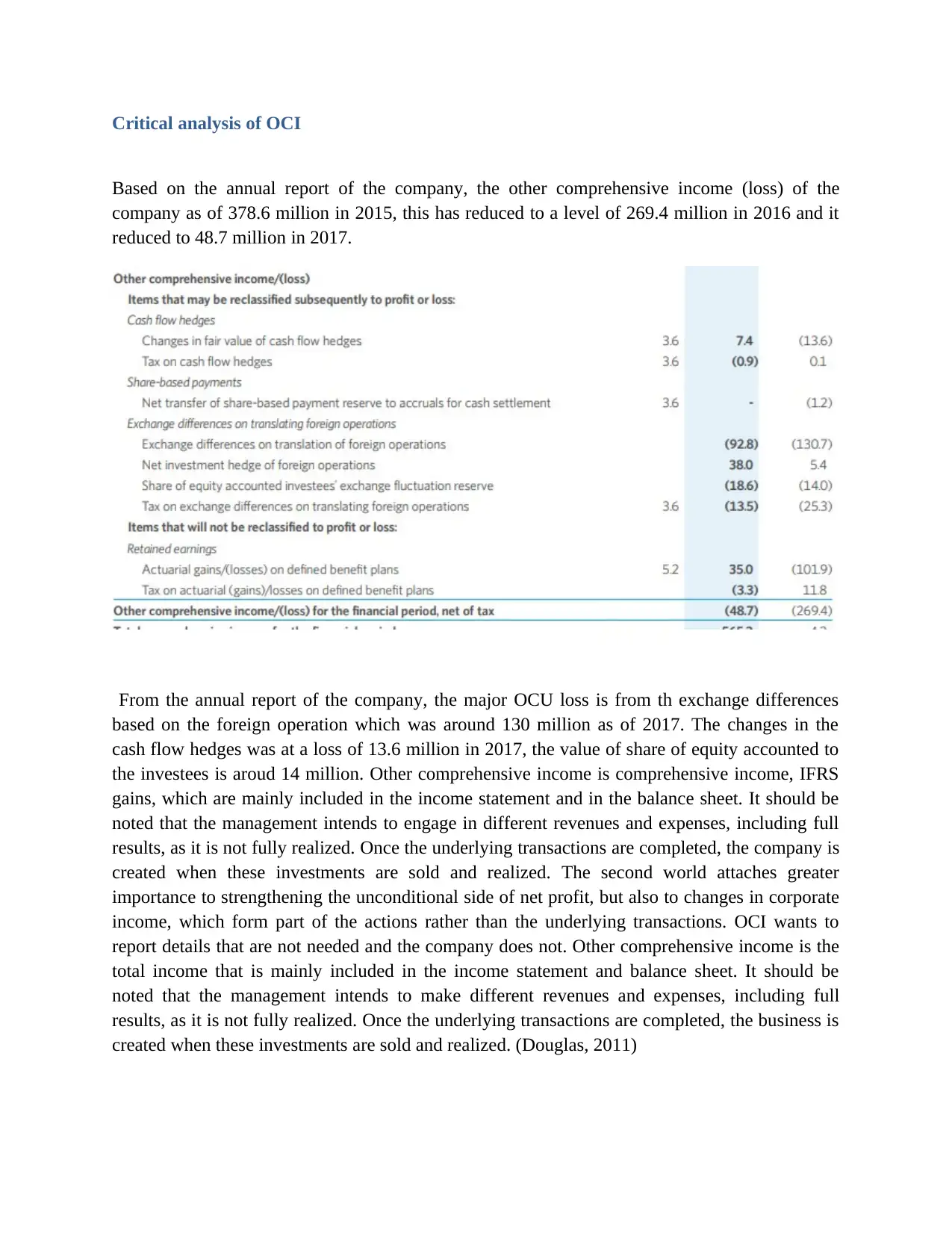

Based on the annual report of the company, the other comprehensive income (loss) of the

company as of 378.6 million in 2015, this has reduced to a level of 269.4 million in 2016 and it

reduced to 48.7 million in 2017.

From the annual report of the company, the major OCU loss is from th exchange differences

based on the foreign operation which was around 130 million as of 2017. The changes in the

cash flow hedges was at a loss of 13.6 million in 2017, the value of share of equity accounted to

the investees is aroud 14 million. Other comprehensive income is comprehensive income, IFRS

gains, which are mainly included in the income statement and in the balance sheet. It should be

noted that the management intends to engage in different revenues and expenses, including full

results, as it is not fully realized. Once the underlying transactions are completed, the company is

created when these investments are sold and realized. The second world attaches greater

importance to strengthening the unconditional side of net profit, but also to changes in corporate

income, which form part of the actions rather than the underlying transactions. OCI wants to

report details that are not needed and the company does not. Other comprehensive income is the

total income that is mainly included in the income statement and balance sheet. It should be

noted that the management intends to make different revenues and expenses, including full

results, as it is not fully realized. Once the underlying transactions are completed, the business is

created when these investments are sold and realized. (Douglas, 2011)

Based on the annual report of the company, the other comprehensive income (loss) of the

company as of 378.6 million in 2015, this has reduced to a level of 269.4 million in 2016 and it

reduced to 48.7 million in 2017.

From the annual report of the company, the major OCU loss is from th exchange differences

based on the foreign operation which was around 130 million as of 2017. The changes in the

cash flow hedges was at a loss of 13.6 million in 2017, the value of share of equity accounted to

the investees is aroud 14 million. Other comprehensive income is comprehensive income, IFRS

gains, which are mainly included in the income statement and in the balance sheet. It should be

noted that the management intends to engage in different revenues and expenses, including full

results, as it is not fully realized. Once the underlying transactions are completed, the company is

created when these investments are sold and realized. The second world attaches greater

importance to strengthening the unconditional side of net profit, but also to changes in corporate

income, which form part of the actions rather than the underlying transactions. OCI wants to

report details that are not needed and the company does not. Other comprehensive income is the

total income that is mainly included in the income statement and balance sheet. It should be

noted that the management intends to make different revenues and expenses, including full

results, as it is not fully realized. Once the underlying transactions are completed, the business is

created when these investments are sold and realized. (Douglas, 2011)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation of Corporate tax

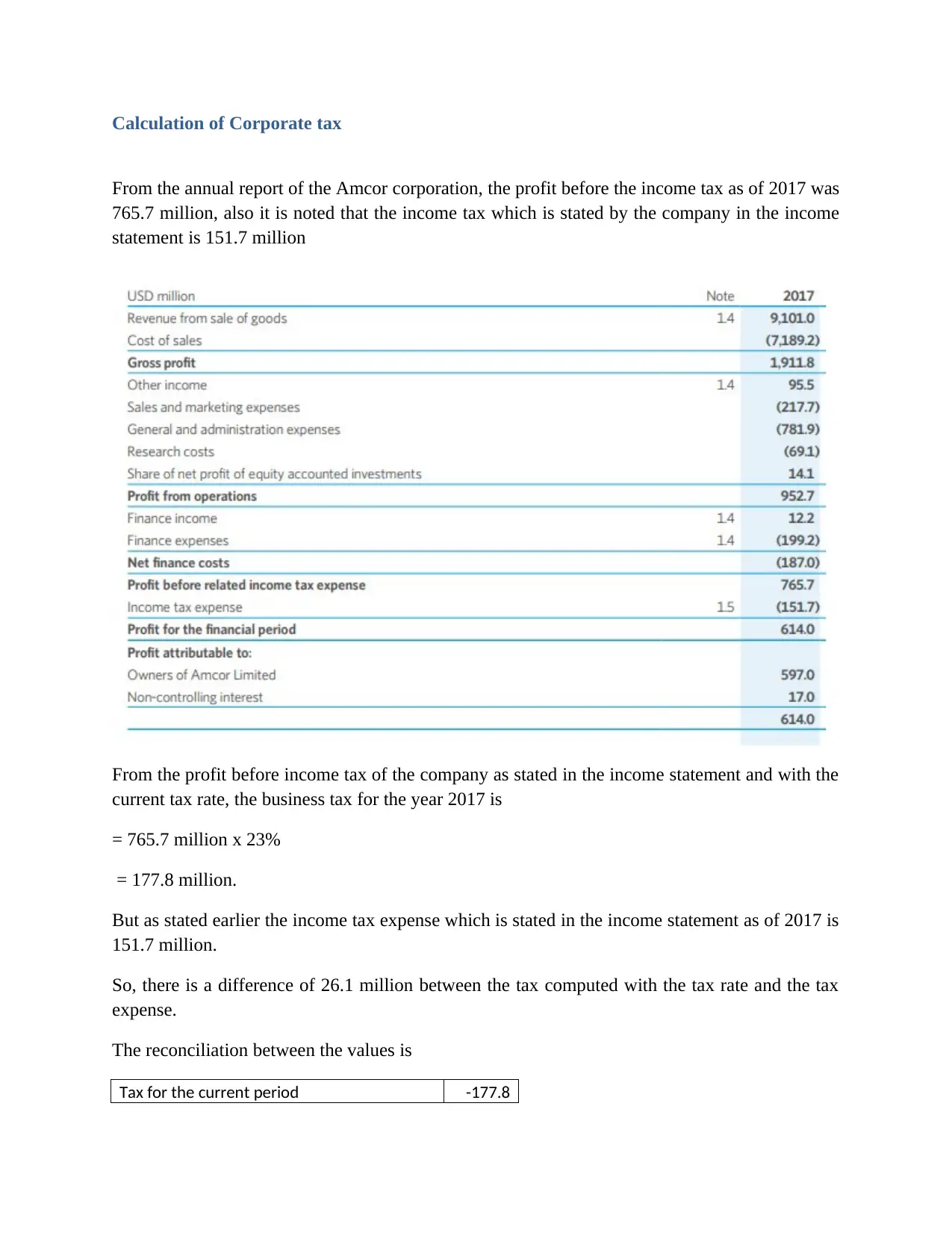

From the annual report of the Amcor corporation, the profit before the income tax as of 2017 was

765.7 million, also it is noted that the income tax which is stated by the company in the income

statement is 151.7 million

From the profit before income tax of the company as stated in the income statement and with the

current tax rate, the business tax for the year 2017 is

= 765.7 million x 23%

= 177.8 million.

But as stated earlier the income tax expense which is stated in the income statement as of 2017 is

151.7 million.

So, there is a difference of 26.1 million between the tax computed with the tax rate and the tax

expense.

The reconciliation between the values is

Tax for the current period -177.8

From the annual report of the Amcor corporation, the profit before the income tax as of 2017 was

765.7 million, also it is noted that the income tax which is stated by the company in the income

statement is 151.7 million

From the profit before income tax of the company as stated in the income statement and with the

current tax rate, the business tax for the year 2017 is

= 765.7 million x 23%

= 177.8 million.

But as stated earlier the income tax expense which is stated in the income statement as of 2017 is

151.7 million.

So, there is a difference of 26.1 million between the tax computed with the tax rate and the tax

expense.

The reconciliation between the values is

Tax for the current period -177.8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

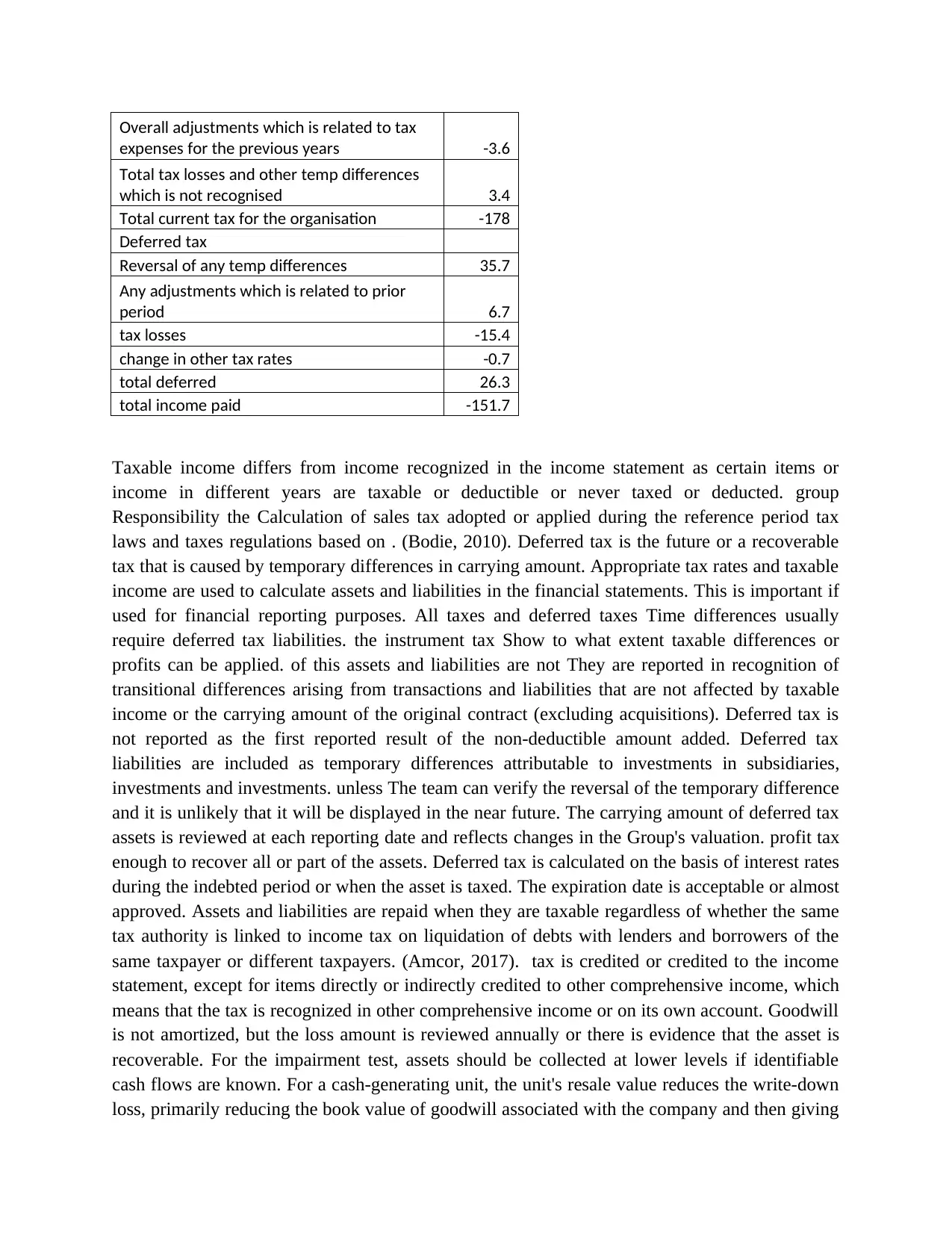

Overall adjustments which is related to tax

expenses for the previous years -3.6

Total tax losses and other temp differences

which is not recognised 3.4

Total current tax for the organisation -178

Deferred tax

Reversal of any temp differences 35.7

Any adjustments which is related to prior

period 6.7

tax losses -15.4

change in other tax rates -0.7

total deferred 26.3

total income paid -151.7

Taxable income differs from income recognized in the income statement as certain items or

income in different years are taxable or deductible or never taxed or deducted. group

Responsibility the Calculation of sales tax adopted or applied during the reference period tax

laws and taxes regulations based on . (Bodie, 2010). Deferred tax is the future or a recoverable

tax that is caused by temporary differences in carrying amount. Appropriate tax rates and taxable

income are used to calculate assets and liabilities in the financial statements. This is important if

used for financial reporting purposes. All taxes and deferred taxes Time differences usually

require deferred tax liabilities. the instrument tax Show to what extent taxable differences or

profits can be applied. of this assets and liabilities are not They are reported in recognition of

transitional differences arising from transactions and liabilities that are not affected by taxable

income or the carrying amount of the original contract (excluding acquisitions). Deferred tax is

not reported as the first reported result of the non-deductible amount added. Deferred tax

liabilities are included as temporary differences attributable to investments in subsidiaries,

investments and investments. unless The team can verify the reversal of the temporary difference

and it is unlikely that it will be displayed in the near future. The carrying amount of deferred tax

assets is reviewed at each reporting date and reflects changes in the Group's valuation. profit tax

enough to recover all or part of the assets. Deferred tax is calculated on the basis of interest rates

during the indebted period or when the asset is taxed. The expiration date is acceptable or almost

approved. Assets and liabilities are repaid when they are taxable regardless of whether the same

tax authority is linked to income tax on liquidation of debts with lenders and borrowers of the

same taxpayer or different taxpayers. (Amcor, 2017). tax is credited or credited to the income

statement, except for items directly or indirectly credited to other comprehensive income, which

means that the tax is recognized in other comprehensive income or on its own account. Goodwill

is not amortized, but the loss amount is reviewed annually or there is evidence that the asset is

recoverable. For the impairment test, assets should be collected at lower levels if identifiable

cash flows are known. For a cash-generating unit, the unit's resale value reduces the write-down

loss, primarily reducing the book value of goodwill associated with the company and then giving

expenses for the previous years -3.6

Total tax losses and other temp differences

which is not recognised 3.4

Total current tax for the organisation -178

Deferred tax

Reversal of any temp differences 35.7

Any adjustments which is related to prior

period 6.7

tax losses -15.4

change in other tax rates -0.7

total deferred 26.3

total income paid -151.7

Taxable income differs from income recognized in the income statement as certain items or

income in different years are taxable or deductible or never taxed or deducted. group

Responsibility the Calculation of sales tax adopted or applied during the reference period tax

laws and taxes regulations based on . (Bodie, 2010). Deferred tax is the future or a recoverable

tax that is caused by temporary differences in carrying amount. Appropriate tax rates and taxable

income are used to calculate assets and liabilities in the financial statements. This is important if

used for financial reporting purposes. All taxes and deferred taxes Time differences usually

require deferred tax liabilities. the instrument tax Show to what extent taxable differences or

profits can be applied. of this assets and liabilities are not They are reported in recognition of

transitional differences arising from transactions and liabilities that are not affected by taxable

income or the carrying amount of the original contract (excluding acquisitions). Deferred tax is

not reported as the first reported result of the non-deductible amount added. Deferred tax

liabilities are included as temporary differences attributable to investments in subsidiaries,

investments and investments. unless The team can verify the reversal of the temporary difference

and it is unlikely that it will be displayed in the near future. The carrying amount of deferred tax

assets is reviewed at each reporting date and reflects changes in the Group's valuation. profit tax

enough to recover all or part of the assets. Deferred tax is calculated on the basis of interest rates

during the indebted period or when the asset is taxed. The expiration date is acceptable or almost

approved. Assets and liabilities are repaid when they are taxable regardless of whether the same

tax authority is linked to income tax on liquidation of debts with lenders and borrowers of the

same taxpayer or different taxpayers. (Amcor, 2017). tax is credited or credited to the income

statement, except for items directly or indirectly credited to other comprehensive income, which

means that the tax is recognized in other comprehensive income or on its own account. Goodwill

is not amortized, but the loss amount is reviewed annually or there is evidence that the asset is

recoverable. For the impairment test, assets should be collected at lower levels if identifiable

cash flows are known. For a cash-generating unit, the unit's resale value reduces the write-down

loss, primarily reducing the book value of goodwill associated with the company and then giving

access to other assets. The impairment loss recognized in goodwill can not be changed in

subsequent periods. The recoverable amount is the fair value, the sale price and the value in use.

Existing financial market assessments and estimates of future cash flows for discount rates

updated in current values are special tools for which future cash flow analyzes have not been

modified. (Eun, 2015)

References

Amcor (2017). Annual report of Amcor

Bodie, Z., Kane, A., Marcus, A. J., Perrakis, S., & Ryan, P. J. (2010). Investments. Canada:

McGraw-Hill Ryerson.

Brealy, R & Myers, S (2011). Principles of Corporate Finance. New York: McGraw-Hill.

Damodaran, A. (2016). Valuation approaches and metrics: A survey of the theory and evidence,

Stern School of Business.

Douglas Hubbard. (2011). The Failure of Risk Management: Why It's Broken and How to

Fix It. pg. 46, John Wiley & Sons

Eun, C & Resnick, B (2015). International Financial Management. New York: McGraw-Hill.

subsequent periods. The recoverable amount is the fair value, the sale price and the value in use.

Existing financial market assessments and estimates of future cash flows for discount rates

updated in current values are special tools for which future cash flow analyzes have not been

modified. (Eun, 2015)

References

Amcor (2017). Annual report of Amcor

Bodie, Z., Kane, A., Marcus, A. J., Perrakis, S., & Ryan, P. J. (2010). Investments. Canada:

McGraw-Hill Ryerson.

Brealy, R & Myers, S (2011). Principles of Corporate Finance. New York: McGraw-Hill.

Damodaran, A. (2016). Valuation approaches and metrics: A survey of the theory and evidence,

Stern School of Business.

Douglas Hubbard. (2011). The Failure of Risk Management: Why It's Broken and How to

Fix It. pg. 46, John Wiley & Sons

Eun, C & Resnick, B (2015). International Financial Management. New York: McGraw-Hill.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.