Comprehensive Financial Management Project: AME Case Study Analysis

VerifiedAdded on 2020/11/23

|18

|3632

|423

Report

AI Summary

This financial management project analyzes the case of AME, a company considering investment in a new business. The project begins with an introduction to financial management principles, followed by an analysis of relevant costs, including opportunity and cannibalization costs. It then explores depreciation methods, estimating cash flows, and calculating the payback period and Net Present Value (NPV) of the investment. Sensitivity analysis is performed to assess the impact of changes in sales, marketing campaigns, and operating costs. The project provides recommendations to AME's management based on the analysis, comparing different scenarios and advising on whether to invest in the new business or lease the building. The report concludes with a summary of findings and a list of references.

FINANCIAL MANAGEMENT WRITTEN

PROJECT

PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Costs which have relevance or not for evaluation of project.............................................1

2. Analysis of Possible Opportunity and Cannibalization costs.............................................2

3. Method of Depreciation......................................................................................................2

4. Estimation of Cash Flows for Evaluation of Project..........................................................3

5. Estimation of Pack Period of Capital Investment...............................................................4

6. Calculation of Net Present Value.......................................................................................4

7. Sensitivity analysis on given points-:.................................................................................4

8. Advising AME’s Management...........................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

1..............................................................................................................................................8

2..............................................................................................................................................9

3..............................................................................................................................................9

4............................................................................................................................................10

5............................................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Costs which have relevance or not for evaluation of project.............................................1

2. Analysis of Possible Opportunity and Cannibalization costs.............................................2

3. Method of Depreciation......................................................................................................2

4. Estimation of Cash Flows for Evaluation of Project..........................................................3

5. Estimation of Pack Period of Capital Investment...............................................................4

6. Calculation of Net Present Value.......................................................................................4

7. Sensitivity analysis on given points-:.................................................................................4

8. Advising AME’s Management...........................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

1..............................................................................................................................................8

2..............................................................................................................................................9

3..............................................................................................................................................9

4............................................................................................................................................10

5............................................................................................................................................12

INTRODUCTION

Financial management can be defined as the preparation, direction and management of monetary activities of any company

such as buying, selling and using cash for best results and maximizing wealth to produce best value of money (Harrison, 2017). It can

also be defined as management of finance in order to achieve financial objectives (DeFusco, 2015.). The report will provide

recommendations that will help in decision making to AME's Management.

TASK

1. Costs which have relevance or not for evaluation of project

Cost is the value of money that is used to manufacture something or to deliver a service (Gitman, 2015). It also refers to

monetary expenditure which firm incurs in order to purchase or to hire factors of production.

The given below are cost which helps in decision making.

Opportunity Cost-: It is cost of next best alternative that is sacrificed for pursuing the chosen action.

Sunk Cost-: These can be said as irrevocable cost of past business which has to be incurred and is irrelevant to current

business activity (Daunfeldt, 2014).

Replacement Cost-: Cost that are incurred for replacement of any asset. For Ex-: Setup of roofing for installing machinery.

Conversion Cost-: Cost that are involved in Transformation of raw material in finished goods.

Costs On the Basis of Nature-:

1. Fixed Cost-: These are cost of fixed inputs that are used in production. This does not vary with the change in volume of

production.

2. Variable Costs-: It can be said as cost of variable inputs used in production. These varies with change in volume of

production.

So, in the given case cost that are relevant for evaluation of project are-:

1

Financial management can be defined as the preparation, direction and management of monetary activities of any company

such as buying, selling and using cash for best results and maximizing wealth to produce best value of money (Harrison, 2017). It can

also be defined as management of finance in order to achieve financial objectives (DeFusco, 2015.). The report will provide

recommendations that will help in decision making to AME's Management.

TASK

1. Costs which have relevance or not for evaluation of project

Cost is the value of money that is used to manufacture something or to deliver a service (Gitman, 2015). It also refers to

monetary expenditure which firm incurs in order to purchase or to hire factors of production.

The given below are cost which helps in decision making.

Opportunity Cost-: It is cost of next best alternative that is sacrificed for pursuing the chosen action.

Sunk Cost-: These can be said as irrevocable cost of past business which has to be incurred and is irrelevant to current

business activity (Daunfeldt, 2014).

Replacement Cost-: Cost that are incurred for replacement of any asset. For Ex-: Setup of roofing for installing machinery.

Conversion Cost-: Cost that are involved in Transformation of raw material in finished goods.

Costs On the Basis of Nature-:

1. Fixed Cost-: These are cost of fixed inputs that are used in production. This does not vary with the change in volume of

production.

2. Variable Costs-: It can be said as cost of variable inputs used in production. These varies with change in volume of

production.

So, in the given case cost that are relevant for evaluation of project are-:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Annual Maintenance Cost-: These are incurred yearly for repairs of buildings lot and will be taken into

consideration as it directly affects cost of project.

Loss in cash flow of AME's regular business-: These are opportunity costs as because of new activity the regular

business is affected and there is loss of cash inflow

Marketing Cost-: These are operation costs of business which are to be considered for evaluation of the Net present

value of project.

Fixed Cost-: These costs are fixed that are compulsorily needed to run business.

Variable Cost-: They are directly associated with the volume of business,

Depreciation-: It is a non-cash expense but need to be considered in giving investment decision as it affects the cost

of project.

2. Analysis of Possible Opportunity and Cannibalization costs

Cannibalization Costs-: It refers to reduction in sales volume, revenue or market share of one articleas a result of introduction

of another product by same manufacturer (Andor, 2015).

Opportunity Cost-: It is loss of profit when one alternative is selected over another.

So in given case opportunity and cannibalization cost is loss of AME's regular car rental business where there is fall in cash flow of

$20000 per annum.

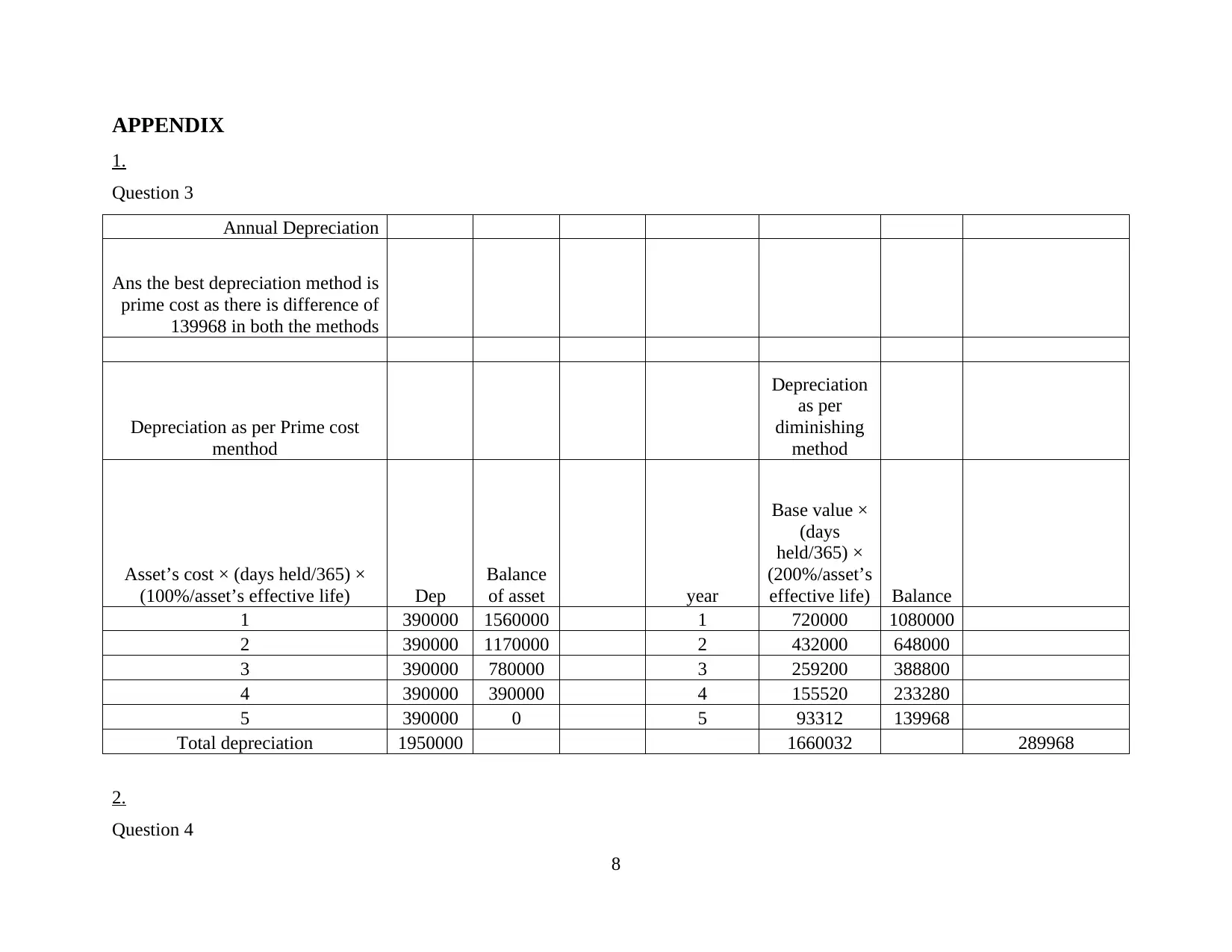

3. Method of Depreciation

Refer appendix 1

The methods that can be used for calculating depreciation

Prime Cost Method-: This method assumes that value of depreciating asset decreases uniformly over its useful life.

Diminishing Value Method-: It assumes that value of asset decreases more in early years of its effective life.

2

consideration as it directly affects cost of project.

Loss in cash flow of AME's regular business-: These are opportunity costs as because of new activity the regular

business is affected and there is loss of cash inflow

Marketing Cost-: These are operation costs of business which are to be considered for evaluation of the Net present

value of project.

Fixed Cost-: These costs are fixed that are compulsorily needed to run business.

Variable Cost-: They are directly associated with the volume of business,

Depreciation-: It is a non-cash expense but need to be considered in giving investment decision as it affects the cost

of project.

2. Analysis of Possible Opportunity and Cannibalization costs

Cannibalization Costs-: It refers to reduction in sales volume, revenue or market share of one articleas a result of introduction

of another product by same manufacturer (Andor, 2015).

Opportunity Cost-: It is loss of profit when one alternative is selected over another.

So in given case opportunity and cannibalization cost is loss of AME's regular car rental business where there is fall in cash flow of

$20000 per annum.

3. Method of Depreciation

Refer appendix 1

The methods that can be used for calculating depreciation

Prime Cost Method-: This method assumes that value of depreciating asset decreases uniformly over its useful life.

Diminishing Value Method-: It assumes that value of asset decreases more in early years of its effective life.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the evaluation of project, we have used Prime Cost Method as it has depreciated whole value of asset through which AME, s have

extra tax benefit as they have claimed more expenses than that of another. While if diminishing value method would have been

considered they would have claimed depreciation expenses more in early years. But as compared it is better to go for prime cost

method (CGT has not been considered here).

4. Estimation of Cash Flows for Evaluation of Project

Refer appendix 2

The following are inflows that are associated with evaluation of project-:

1. Initial Investment

1. Cost of Vehicle

2. Cost of improvements that are installed for Vehicle recovery system.

3. Cost of Buildings required for operations

4. Working Capital

Cost that are incurred on annual basis

5. Variable Costs

6. Fixed Costs

7. Administrative Cost

8. Annual Maintenance Costs

9. Marketing Costs

Depreciation is not considered here because it is a non-cash expense.

3

extra tax benefit as they have claimed more expenses than that of another. While if diminishing value method would have been

considered they would have claimed depreciation expenses more in early years. But as compared it is better to go for prime cost

method (CGT has not been considered here).

4. Estimation of Cash Flows for Evaluation of Project

Refer appendix 2

The following are inflows that are associated with evaluation of project-:

1. Initial Investment

1. Cost of Vehicle

2. Cost of improvements that are installed for Vehicle recovery system.

3. Cost of Buildings required for operations

4. Working Capital

Cost that are incurred on annual basis

5. Variable Costs

6. Fixed Costs

7. Administrative Cost

8. Annual Maintenance Costs

9. Marketing Costs

Depreciation is not considered here because it is a non-cash expense.

3

5. Estimation of Pack Period of Capital Investment.

Refer appendix 3

Pay Back Period-: It is calculation of time required to recover the cost of investment. It can be important to determine payback

period as by this they can estimate length of time to recover their initial investments (Storesletten, 2003). The better investments are

ones that have shorter payback period (Goyat,2016).

In the given case AME’s will recover their cost of capital investment in 2.86 Years which is approx. 2year and 11 months.

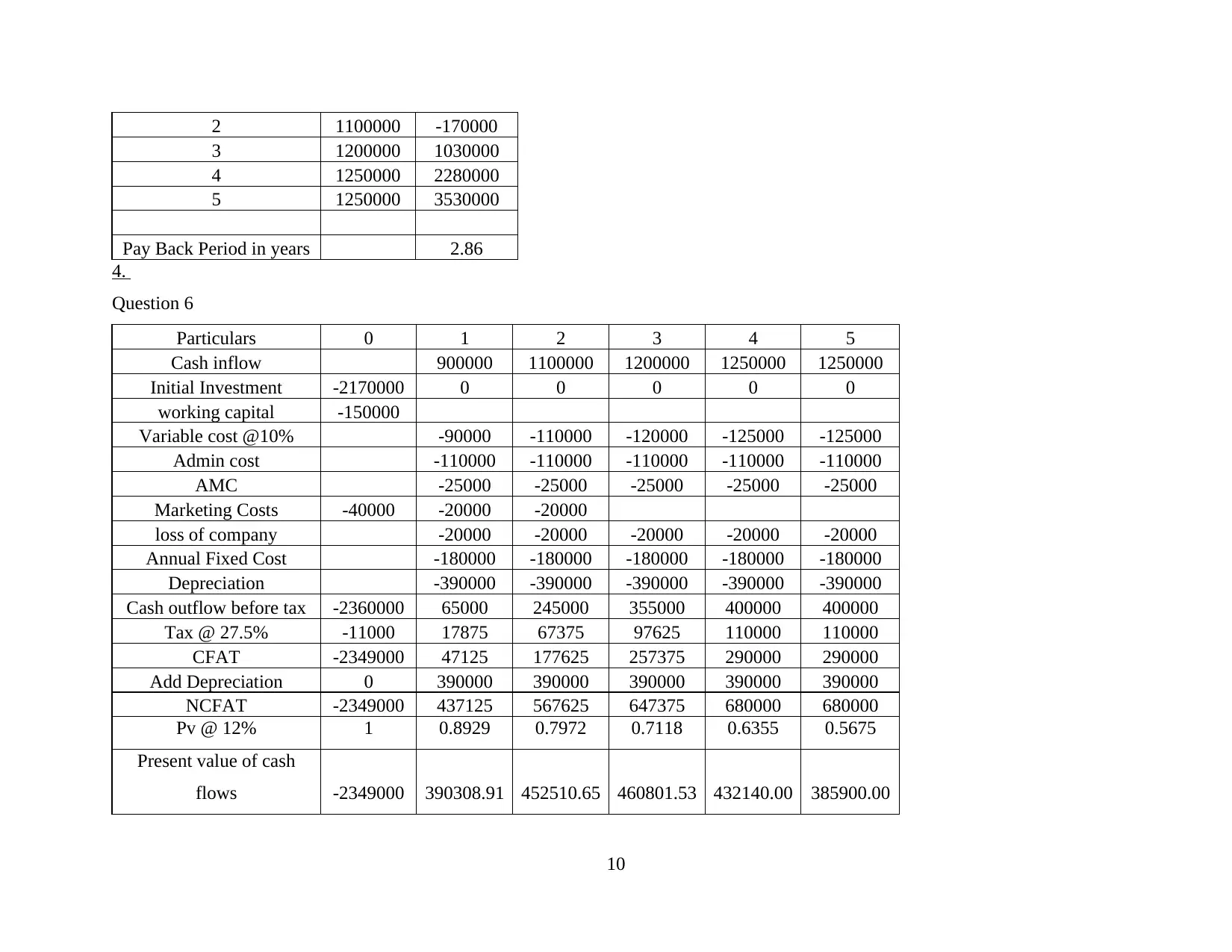

6. Calculation of Net Present Value

Refer appendix 4

NPV is computation of profits calculated by deducting PV of Cash outflows from PV of cash inflows over a period of time.

(Net Present Value, 2018.). If NPV is positive, it is better to accept project and vice versa if negative.

In the given case study there are two proposals that AME’s management is having with them one is regarding lease of building and

other one to start a new business of car rental.

So both the projects are compared with given data and found that NPV is positive for both cases but NPV of new business is excess

$69238.84 from NPV of Lease. So AME’s management must invest in new business rather than giving building on lease.

7. Sensitivity analysis on given points-:

Refer appendix 5

(i)If Projected Sales decrease by 10%

NPV calculated of both options and found that both projects are having positive but net present value but leases is having

excess of 223548.06 than starting a new business. So it is better to provide building on lease.

4

Refer appendix 3

Pay Back Period-: It is calculation of time required to recover the cost of investment. It can be important to determine payback

period as by this they can estimate length of time to recover their initial investments (Storesletten, 2003). The better investments are

ones that have shorter payback period (Goyat,2016).

In the given case AME’s will recover their cost of capital investment in 2.86 Years which is approx. 2year and 11 months.

6. Calculation of Net Present Value

Refer appendix 4

NPV is computation of profits calculated by deducting PV of Cash outflows from PV of cash inflows over a period of time.

(Net Present Value, 2018.). If NPV is positive, it is better to accept project and vice versa if negative.

In the given case study there are two proposals that AME’s management is having with them one is regarding lease of building and

other one to start a new business of car rental.

So both the projects are compared with given data and found that NPV is positive for both cases but NPV of new business is excess

$69238.84 from NPV of Lease. So AME’s management must invest in new business rather than giving building on lease.

7. Sensitivity analysis on given points-:

Refer appendix 5

(i)If Projected Sales decrease by 10%

NPV calculated of both options and found that both projects are having positive but net present value but leases is having

excess of 223548.06 than starting a new business. So it is better to provide building on lease.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(ii)If Marketing Campaign boosted by 100% and I.e. sales increase is 3%

NPV of both projects are positive as per given data by AME, s but NPV of Business is more of $103568.46. So it’s better to

start new business.

(iii)Operating Fixed and Variable Costs increase by 20%

NPV calculated with given data for business is negative so it’s better to reject option for business and simply provide building

for lease.

8. Advising AME’s Management

The acceptance and rejection of project totally depends upon on projects, So, in question (5 to 7) there are different situations

provided so calculations have been done regarding that situations and solutions are there and decisions taken are provided in below

table-:

Question No. Particulars Decision Reasons

5 Pay Pack period Reject There can be shorter period as in 5 years the

cost is recovered in 2 years 11 months

6 Business Accept As NPV is positive and excess of lease

7(i) Business Reject As NPV is Positive but not in excess of lease

7(ii) Business Accept As NPV is positive and excess of lease

7(iii) Business Reject NPV is Negative

5

NPV of both projects are positive as per given data by AME, s but NPV of Business is more of $103568.46. So it’s better to

start new business.

(iii)Operating Fixed and Variable Costs increase by 20%

NPV calculated with given data for business is negative so it’s better to reject option for business and simply provide building

for lease.

8. Advising AME’s Management

The acceptance and rejection of project totally depends upon on projects, So, in question (5 to 7) there are different situations

provided so calculations have been done regarding that situations and solutions are there and decisions taken are provided in below

table-:

Question No. Particulars Decision Reasons

5 Pay Pack period Reject There can be shorter period as in 5 years the

cost is recovered in 2 years 11 months

6 Business Accept As NPV is positive and excess of lease

7(i) Business Reject As NPV is Positive but not in excess of lease

7(ii) Business Accept As NPV is positive and excess of lease

7(iii) Business Reject NPV is Negative

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

This project report is solution for case study regarding investment in new business. So with data given by AME, management

the calculations have been done and provided decisions in different situations. There have been taken some assumptions where

needed. All the decisions are totally dependent on data given by AME’s management. The calculations have been made with different

techniques of capital budgeting.

6

This project report is solution for case study regarding investment in new business. So with data given by AME, management

the calculations have been done and provided decisions in different situations. There have been taken some assumptions where

needed. All the decisions are totally dependent on data given by AME’s management. The calculations have been made with different

techniques of capital budgeting.

6

REFERENCES

Books and Journals:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central and Eastern European firms. Emerging

Markets Review. 23.pp.148-172

Daunfeldt, S.O. and Hartwig, F. 2014. What determines the use of capital budgeting methods? Evidence from Swedish listed

companies. Journal of Finance and Economics.2(4). pp.101-112.

DeFusco, R.A., and et.al. 2015. Quantitative investment analysis. John Wiley & Sons.

Gitman, L.J., Juchau, R. and Flanagan, J. 2015. Principles of managerial finance. Pearson Higher Education AU.

Goyat, S. and Nain, A., 2016. Methods of Evaluating Investment Proposals. International Journal of Engineering and Management

Research (IJEMR).6(5). pp.278-280.

Harrison, F. and Lock, D. 2017. Advanced project management: a structured approach. Routledge

Storesletten, K., 2003. Fiscal implications of immigration—A net present value calculation. Scandinavian Journal of Economics.

105(3). pp.487-506.

Online:

Net Present Value. 2018. [Online]. Available through: <https://investinganswers.com/financial-dictionary/technical-analysis/

net-present-value-npv-2995>.

7

Books and Journals:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central and Eastern European firms. Emerging

Markets Review. 23.pp.148-172

Daunfeldt, S.O. and Hartwig, F. 2014. What determines the use of capital budgeting methods? Evidence from Swedish listed

companies. Journal of Finance and Economics.2(4). pp.101-112.

DeFusco, R.A., and et.al. 2015. Quantitative investment analysis. John Wiley & Sons.

Gitman, L.J., Juchau, R. and Flanagan, J. 2015. Principles of managerial finance. Pearson Higher Education AU.

Goyat, S. and Nain, A., 2016. Methods of Evaluating Investment Proposals. International Journal of Engineering and Management

Research (IJEMR).6(5). pp.278-280.

Harrison, F. and Lock, D. 2017. Advanced project management: a structured approach. Routledge

Storesletten, K., 2003. Fiscal implications of immigration—A net present value calculation. Scandinavian Journal of Economics.

105(3). pp.487-506.

Online:

Net Present Value. 2018. [Online]. Available through: <https://investinganswers.com/financial-dictionary/technical-analysis/

net-present-value-npv-2995>.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

1.

Question 3

Annual Depreciation

Ans the best depreciation method is

prime cost as there is difference of

139968 in both the methods

Depreciation as per Prime cost

menthod

Depreciation

as per

diminishing

method

Asset’s cost × (days held/365) ×

(100%/asset’s effective life) Dep

Balance

of asset year

Base value ×

(days

held/365) ×

(200%/asset’s

effective life) Balance

1 390000 1560000 1 720000 1080000

2 390000 1170000 2 432000 648000

3 390000 780000 3 259200 388800

4 390000 390000 4 155520 233280

5 390000 0 5 93312 139968

Total depreciation 1950000 1660032 289968

2.

Question 4

8

1.

Question 3

Annual Depreciation

Ans the best depreciation method is

prime cost as there is difference of

139968 in both the methods

Depreciation as per Prime cost

menthod

Depreciation

as per

diminishing

method

Asset’s cost × (days held/365) ×

(100%/asset’s effective life) Dep

Balance

of asset year

Base value ×

(days

held/365) ×

(200%/asset’s

effective life) Balance

1 390000 1560000 1 720000 1080000

2 390000 1170000 2 432000 648000

3 390000 780000 3 259200 388800

4 390000 390000 4 155520 233280

5 390000 0 5 93312 139968

Total depreciation 1950000 1660032 289968

2.

Question 4

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Initial Cash flows of Project Years

Cash

inflow

Variable

costs

10% of

revenue

Fixed

costs

Administrative

cost 20%

increase AMC

Marketing

costs

Working

capital

Initial

Cash out

Flow

Purchase of second hand car 1800000 0 0 40000 150000 2170000

Recover System 150000 1 900000 90000 180000 110000 25000 20000 0 0

Cost of Building 220000 2 1100000 110000 180000 110000 25000 20000 0 0

2170000 3 1200000 120000 180000 110000 25000 0 0 0

4 1250000 125000 180000 110000 25000 0 0 0

5 1250000 125000 180000 110000 25000 0 0 0

5700000 570000 900000 550000 125000 80000 150000 2170000

Total

cash

outflow

for the

project

for 5

years

will be 4545000

3.

Question 5

Payback period

initial investment/cash

inflow per period

As there is uneven cash

inflows then

negative

cumulative

cash flow

0 -2170000 -2170000

1 900000 -1270000

9

Cash

inflow

Variable

costs

10% of

revenue

Fixed

costs

Administrative

cost 20%

increase AMC

Marketing

costs

Working

capital

Initial

Cash out

Flow

Purchase of second hand car 1800000 0 0 40000 150000 2170000

Recover System 150000 1 900000 90000 180000 110000 25000 20000 0 0

Cost of Building 220000 2 1100000 110000 180000 110000 25000 20000 0 0

2170000 3 1200000 120000 180000 110000 25000 0 0 0

4 1250000 125000 180000 110000 25000 0 0 0

5 1250000 125000 180000 110000 25000 0 0 0

5700000 570000 900000 550000 125000 80000 150000 2170000

Total

cash

outflow

for the

project

for 5

years

will be 4545000

3.

Question 5

Payback period

initial investment/cash

inflow per period

As there is uneven cash

inflows then

negative

cumulative

cash flow

0 -2170000 -2170000

1 900000 -1270000

9

2 1100000 -170000

3 1200000 1030000

4 1250000 2280000

5 1250000 3530000

Pay Back Period in years 2.86

4.

Question 6

Particulars 0 1 2 3 4 5

Cash inflow 900000 1100000 1200000 1250000 1250000

Initial Investment -2170000 0 0 0 0 0

working capital -150000

Variable cost @10% -90000 -110000 -120000 -125000 -125000

Admin cost -110000 -110000 -110000 -110000 -110000

AMC -25000 -25000 -25000 -25000 -25000

Marketing Costs -40000 -20000 -20000

loss of company -20000 -20000 -20000 -20000 -20000

Annual Fixed Cost -180000 -180000 -180000 -180000 -180000

Depreciation -390000 -390000 -390000 -390000 -390000

Cash outflow before tax -2360000 65000 245000 355000 400000 400000

Tax @ 27.5% -11000 17875 67375 97625 110000 110000

CFAT -2349000 47125 177625 257375 290000 290000

Add Depreciation 0 390000 390000 390000 390000 390000

NCFAT -2349000 437125 567625 647375 680000 680000

Pv @ 12% 1 0.8929 0.7972 0.7118 0.6355 0.5675

Present value of cash

flows -2349000 390308.91 452510.65 460801.53 432140.00 385900.00

10

3 1200000 1030000

4 1250000 2280000

5 1250000 3530000

Pay Back Period in years 2.86

4.

Question 6

Particulars 0 1 2 3 4 5

Cash inflow 900000 1100000 1200000 1250000 1250000

Initial Investment -2170000 0 0 0 0 0

working capital -150000

Variable cost @10% -90000 -110000 -120000 -125000 -125000

Admin cost -110000 -110000 -110000 -110000 -110000

AMC -25000 -25000 -25000 -25000 -25000

Marketing Costs -40000 -20000 -20000

loss of company -20000 -20000 -20000 -20000 -20000

Annual Fixed Cost -180000 -180000 -180000 -180000 -180000

Depreciation -390000 -390000 -390000 -390000 -390000

Cash outflow before tax -2360000 65000 245000 355000 400000 400000

Tax @ 27.5% -11000 17875 67375 97625 110000 110000

CFAT -2349000 47125 177625 257375 290000 290000

Add Depreciation 0 390000 390000 390000 390000 390000

NCFAT -2349000 437125 567625 647375 680000 680000

Pv @ 12% 1 0.8929 0.7972 0.7118 0.6355 0.5675

Present value of cash

flows -2349000 390308.91 452510.65 460801.53 432140.00 385900.00

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.