AML/CTF Risk Assessment and Control Plan: Business Solution Limited

VerifiedAdded on 2022/10/15

|22

|7394

|30

Report

AI Summary

This report provides a comprehensive AML/CTF risk assessment for Business Solution Limited (BSL) considering the acquisition of Frontline Financing (FF). It outlines risk factors such as money laundering, terrorism financing, and loss of intellectual property. The assessment utilizes tools like customer profiling, product analysis, channel evaluation, and country risk assessment. The report details risk criteria, measurement, and treatment, including risk monitoring and control mechanisms. It also explores industry typologies, BSL's risk appetite, and vulnerabilities related to online trade financing and offshore operations. The report concludes with a discussion of the need for a robust monitoring system and adherence to regulations, emphasizing the importance of initial and ongoing AML/CTF controls, stakeholder consultation, and a review of ML/TF assessment.

1

Anti-money laundering and terrorism financing

University name

Word count

Anti-money laundering and terrorism financing

University name

Word count

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Introduction

The organization considered in this paper is Business solution Limited that provides over the

counter finance for businesses (Alexeev, 2018). This paper aims to prepare a document for

the board of BSL related to the acquisition of Frontline Financing (FF) which deals with

online trade financing as a major service (Amor et al., 2016). The frontline financing is the

first offshore investment to be considered by BSL as it is confined to Australia only as of

now (Anthopoulos, 2016). As a consultant regarding the AML/CTF, risk assessment

methodology is provided in this paper (Bakumenko & Sigal, 2018). The Frontline Financing

is an entity of New Zealand which is regulated under Anti-money laundering and countering

financing of Terrorism Act, 2009 (NZ)

Risk assessment methodology

Risk factors

a) Loss of potential customer due to rigorous identification procedures

b) Loss of intellectual property rights to competitors

c) Loss of market to new entrants

d) Money laundering by fraudulent means

e) Terrorists funding through hawala transactions

Risk criteria

The criteria to be considered to assess the risk are as follows:

1. What is the transparency level of financial operations conducted by FF- good, bad or

excellent?

2. How much amount goes to countries providing a haven to terrorists and associated

organizations/

3. What is the disclosure level of FF to the Government of New Zealand and other

international financial institutions concerned with money laundering and terrorist financing?

4. Is there a sound record of money traded online by FF?

Introduction

The organization considered in this paper is Business solution Limited that provides over the

counter finance for businesses (Alexeev, 2018). This paper aims to prepare a document for

the board of BSL related to the acquisition of Frontline Financing (FF) which deals with

online trade financing as a major service (Amor et al., 2016). The frontline financing is the

first offshore investment to be considered by BSL as it is confined to Australia only as of

now (Anthopoulos, 2016). As a consultant regarding the AML/CTF, risk assessment

methodology is provided in this paper (Bakumenko & Sigal, 2018). The Frontline Financing

is an entity of New Zealand which is regulated under Anti-money laundering and countering

financing of Terrorism Act, 2009 (NZ)

Risk assessment methodology

Risk factors

a) Loss of potential customer due to rigorous identification procedures

b) Loss of intellectual property rights to competitors

c) Loss of market to new entrants

d) Money laundering by fraudulent means

e) Terrorists funding through hawala transactions

Risk criteria

The criteria to be considered to assess the risk are as follows:

1. What is the transparency level of financial operations conducted by FF- good, bad or

excellent?

2. How much amount goes to countries providing a haven to terrorists and associated

organizations/

3. What is the disclosure level of FF to the Government of New Zealand and other

international financial institutions concerned with money laundering and terrorist financing?

4. Is there a sound record of money traded online by FF?

3

Tools to be used in the risk assessment

There are 4 tools to be used

Risk identification-

Customer- For the purposes of assessing the inherent money laundering risk of a

business division, unit or business line, the client base and business relationship

should be assessed.

Product- Increasingly complex product offerings complicate risk assessment

activities, as these offerings, by their very nature, are more difficult to assess than

traditional banking products and services.

Channel- online account openings present challenges in verifying the account holder's

true identity and geographic origin or business footprint; All these issues affect an

institution's ability to predict the type and frequency of transactions the customer is

likely to make; without a firm understanding of the customer's risk profile,

monitoring for suspicious activity and, by extension, the reporting of suspicious

activity can be more challenging.

Country- Geography/Country risk will be important in any Sanctions Risk

Assessment, not only with respect to sanctioned countries themselves, but also those

which may have well known/important links or other significant connections to

sanctioned countries

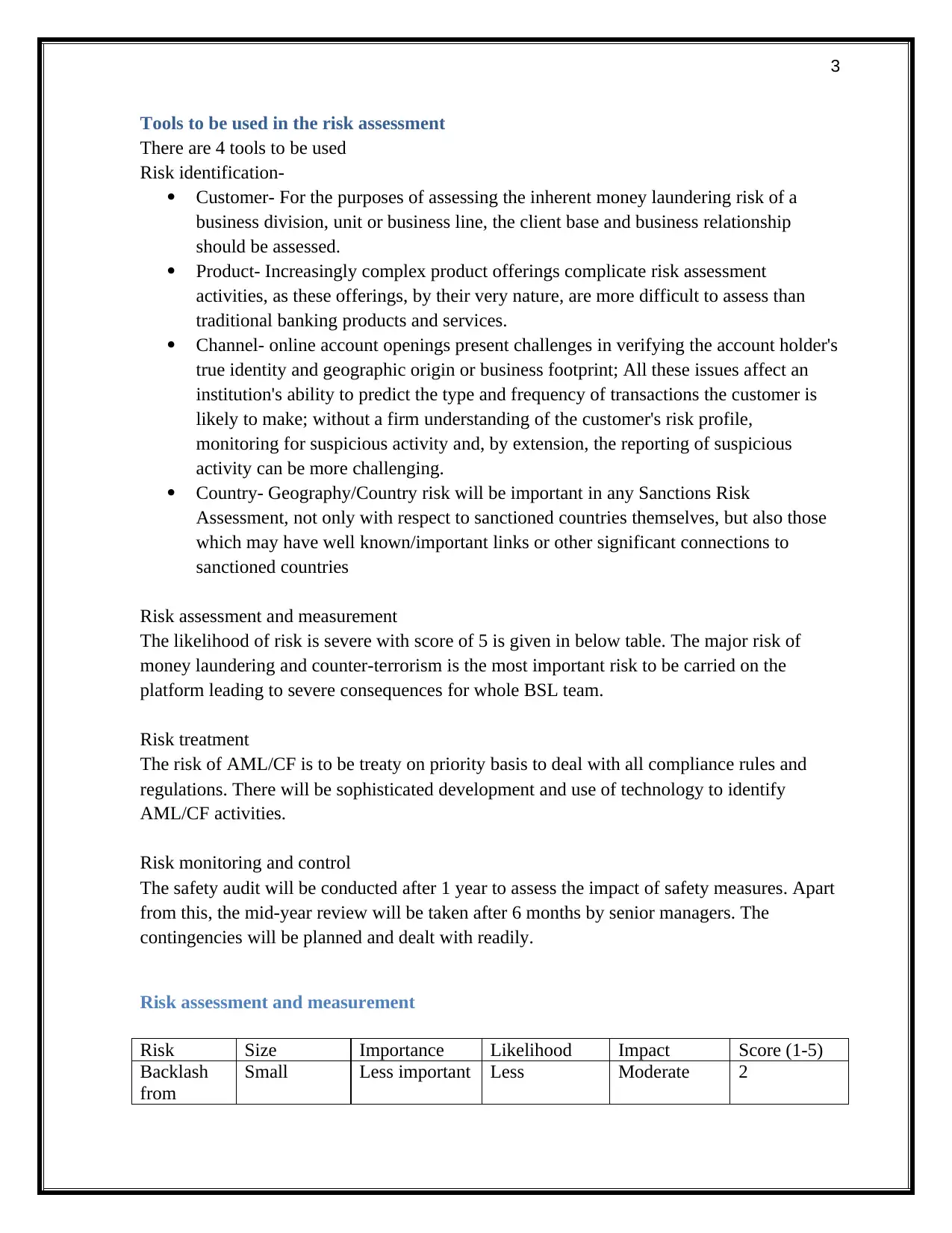

Risk assessment and measurement

The likelihood of risk is severe with score of 5 is given in below table. The major risk of

money laundering and counter-terrorism is the most important risk to be carried on the

platform leading to severe consequences for whole BSL team.

Risk treatment

The risk of AML/CF is to be treaty on priority basis to deal with all compliance rules and

regulations. There will be sophisticated development and use of technology to identify

AML/CF activities.

Risk monitoring and control

The safety audit will be conducted after 1 year to assess the impact of safety measures. Apart

from this, the mid-year review will be taken after 6 months by senior managers. The

contingencies will be planned and dealt with readily.

Risk assessment and measurement

Risk Size Importance Likelihood Impact Score (1-5)

Backlash

from

Small Less important Less Moderate 2

Tools to be used in the risk assessment

There are 4 tools to be used

Risk identification-

Customer- For the purposes of assessing the inherent money laundering risk of a

business division, unit or business line, the client base and business relationship

should be assessed.

Product- Increasingly complex product offerings complicate risk assessment

activities, as these offerings, by their very nature, are more difficult to assess than

traditional banking products and services.

Channel- online account openings present challenges in verifying the account holder's

true identity and geographic origin or business footprint; All these issues affect an

institution's ability to predict the type and frequency of transactions the customer is

likely to make; without a firm understanding of the customer's risk profile,

monitoring for suspicious activity and, by extension, the reporting of suspicious

activity can be more challenging.

Country- Geography/Country risk will be important in any Sanctions Risk

Assessment, not only with respect to sanctioned countries themselves, but also those

which may have well known/important links or other significant connections to

sanctioned countries

Risk assessment and measurement

The likelihood of risk is severe with score of 5 is given in below table. The major risk of

money laundering and counter-terrorism is the most important risk to be carried on the

platform leading to severe consequences for whole BSL team.

Risk treatment

The risk of AML/CF is to be treaty on priority basis to deal with all compliance rules and

regulations. There will be sophisticated development and use of technology to identify

AML/CF activities.

Risk monitoring and control

The safety audit will be conducted after 1 year to assess the impact of safety measures. Apart

from this, the mid-year review will be taken after 6 months by senior managers. The

contingencies will be planned and dealt with readily.

Risk assessment and measurement

Risk Size Importance Likelihood Impact Score (1-5)

Backlash

from

Small Less important Less Moderate 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

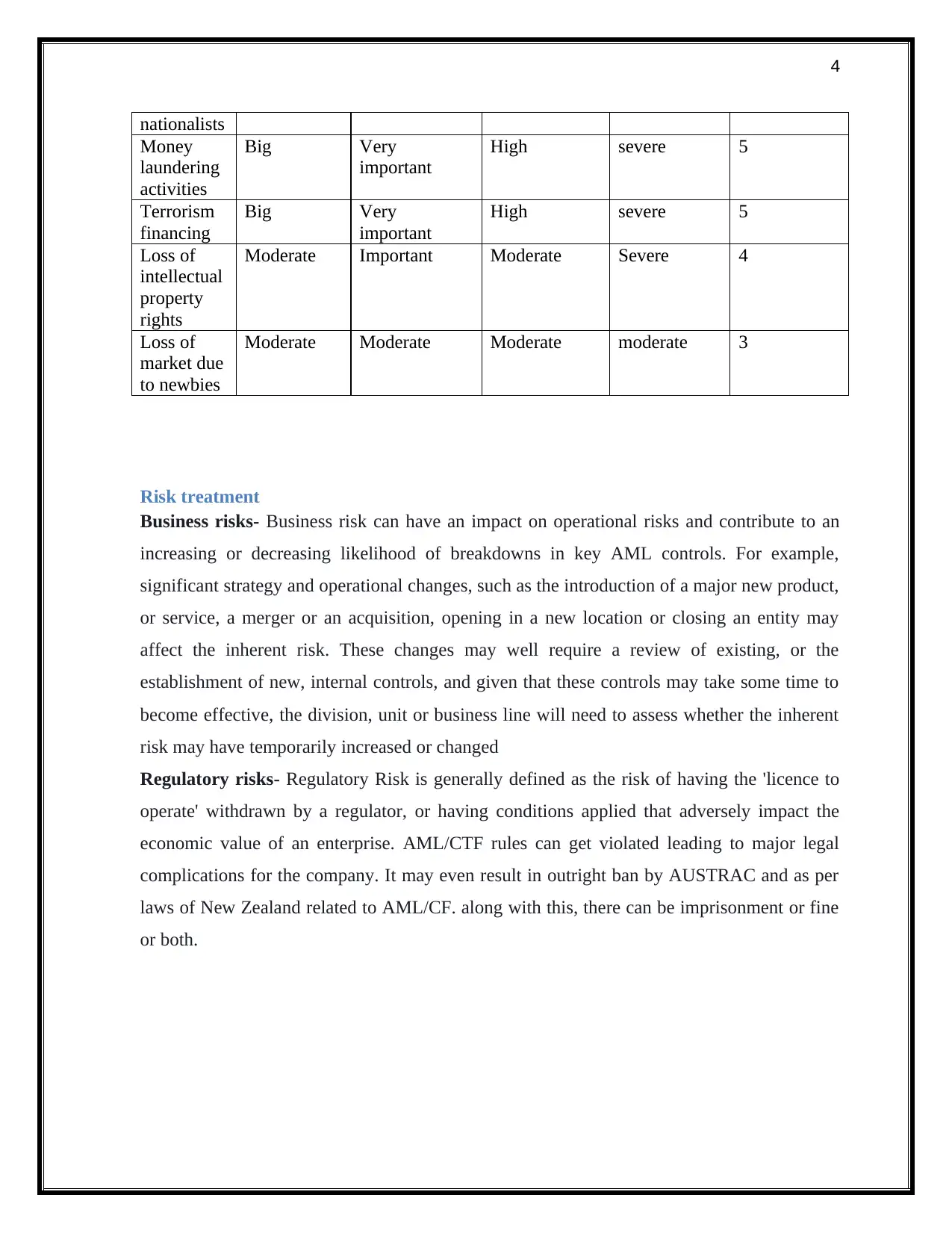

nationalists

Money

laundering

activities

Big Very

important

High severe 5

Terrorism

financing

Big Very

important

High severe 5

Loss of

intellectual

property

rights

Moderate Important Moderate Severe 4

Loss of

market due

to newbies

Moderate Moderate Moderate moderate 3

Risk treatment

Business risks- Business risk can have an impact on operational risks and contribute to an

increasing or decreasing likelihood of breakdowns in key AML controls. For example,

significant strategy and operational changes, such as the introduction of a major new product,

or service, a merger or an acquisition, opening in a new location or closing an entity may

affect the inherent risk. These changes may well require a review of existing, or the

establishment of new, internal controls, and given that these controls may take some time to

become effective, the division, unit or business line will need to assess whether the inherent

risk may have temporarily increased or changed

Regulatory risks- Regulatory Risk is generally defined as the risk of having the 'licence to

operate' withdrawn by a regulator, or having conditions applied that adversely impact the

economic value of an enterprise. AML/CTF rules can get violated leading to major legal

complications for the company. It may even result in outright ban by AUSTRAC and as per

laws of New Zealand related to AML/CF. along with this, there can be imprisonment or fine

or both.

nationalists

Money

laundering

activities

Big Very

important

High severe 5

Terrorism

financing

Big Very

important

High severe 5

Loss of

intellectual

property

rights

Moderate Important Moderate Severe 4

Loss of

market due

to newbies

Moderate Moderate Moderate moderate 3

Risk treatment

Business risks- Business risk can have an impact on operational risks and contribute to an

increasing or decreasing likelihood of breakdowns in key AML controls. For example,

significant strategy and operational changes, such as the introduction of a major new product,

or service, a merger or an acquisition, opening in a new location or closing an entity may

affect the inherent risk. These changes may well require a review of existing, or the

establishment of new, internal controls, and given that these controls may take some time to

become effective, the division, unit or business line will need to assess whether the inherent

risk may have temporarily increased or changed

Regulatory risks- Regulatory Risk is generally defined as the risk of having the 'licence to

operate' withdrawn by a regulator, or having conditions applied that adversely impact the

economic value of an enterprise. AML/CTF rules can get violated leading to major legal

complications for the company. It may even result in outright ban by AUSTRAC and as per

laws of New Zealand related to AML/CF. along with this, there can be imprisonment or fine

or both.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

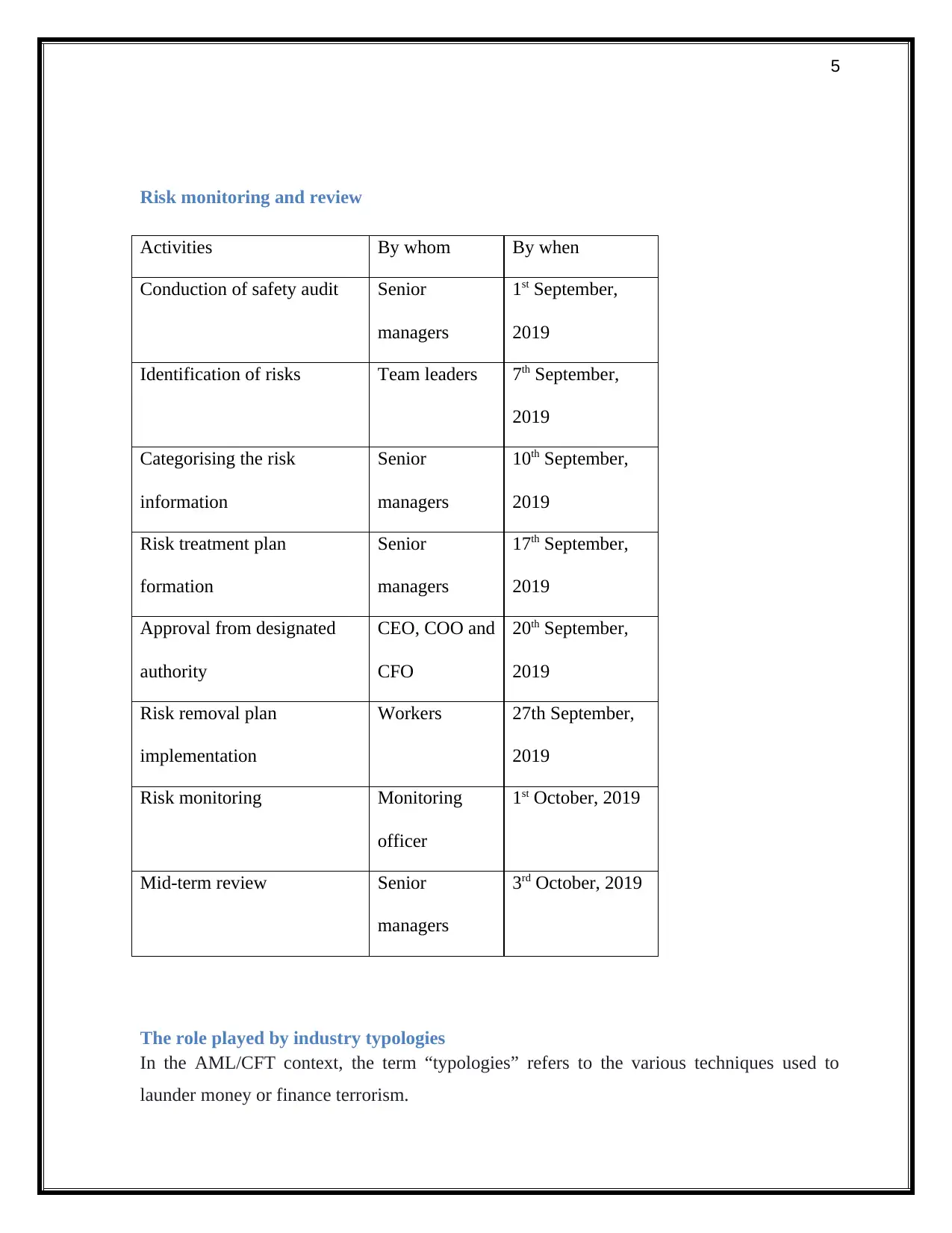

Risk monitoring and review

Activities By whom By when

Conduction of safety audit Senior

managers

1st September,

2019

Identification of risks Team leaders 7th September,

2019

Categorising the risk

information

Senior

managers

10th September,

2019

Risk treatment plan

formation

Senior

managers

17th September,

2019

Approval from designated

authority

CEO, COO and

CFO

20th September,

2019

Risk removal plan

implementation

Workers 27th September,

2019

Risk monitoring Monitoring

officer

1st October, 2019

Mid-term review Senior

managers

3rd October, 2019

The role played by industry typologies

In the AML/CFT context, the term “typologies” refers to the various techniques used to

launder money or finance terrorism.

Risk monitoring and review

Activities By whom By when

Conduction of safety audit Senior

managers

1st September,

2019

Identification of risks Team leaders 7th September,

2019

Categorising the risk

information

Senior

managers

10th September,

2019

Risk treatment plan

formation

Senior

managers

17th September,

2019

Approval from designated

authority

CEO, COO and

CFO

20th September,

2019

Risk removal plan

implementation

Workers 27th September,

2019

Risk monitoring Monitoring

officer

1st October, 2019

Mid-term review Senior

managers

3rd October, 2019

The role played by industry typologies

In the AML/CFT context, the term “typologies” refers to the various techniques used to

launder money or finance terrorism.

6

New Payment technologies: use of emerging payment technologies for money laundering

and terrorist financing. Examples include cell phone-based remittance and payment systems.

Here BSl will be using of using New Payment Technology as Frontline financing is an

Online leasing company.

Trade-based money laundering and terrorist financing usually involves invoice

manipulation and uses trade finance routes and commodities to avoid financial transparency

laws and regulations. This is also one of the threats from Frontline Financing as it is solely

dependent on online platform.

Identity fraud / false identification: used to obscure identification of those involved in

many methods of money laundering and terrorist financing. The risk rate is very high as the

KYC and CDD is done through online platform.

Role of BSL’s risk appetite

The amount of risk an entity is willing to accept or retain in order to achieve its objectives. It

is a statement or series of statements that describes the entity’s attitude towards risk taking.

Determining an entity’s risk appetite occurs through the development of risk appetite

statements which clearly set out what the executive consider to be acceptable risk-taking.

Risk appetite statements are usually aligned to categories of risk e.g. financial, people and

reputation risks.

In every merger and acquisitions, there are certain risks which the premier institutions must

take. BSL is an Australian company, never exposed to the outside environment (Ha, 2019).

Along with this, BSL has never handled the business of such type in Australia (Harbitz et al.,

2016). After the acquisition, there will be a complete overhaul of administration in BSL so

there is a need to consider the risk appetite of BSL without which no decision can be taken

(Hartung, 2017).

How to review the ML/TF assessment?

There would be mid-term review of ML/TF assessment to cater to new needs of the

organization. There is need of timely review of assessment method (Hsu et al., 2017) so the

ML/TF assessment will be reviewed after every 3 year along with mid-term reviews

New Payment technologies: use of emerging payment technologies for money laundering

and terrorist financing. Examples include cell phone-based remittance and payment systems.

Here BSl will be using of using New Payment Technology as Frontline financing is an

Online leasing company.

Trade-based money laundering and terrorist financing usually involves invoice

manipulation and uses trade finance routes and commodities to avoid financial transparency

laws and regulations. This is also one of the threats from Frontline Financing as it is solely

dependent on online platform.

Identity fraud / false identification: used to obscure identification of those involved in

many methods of money laundering and terrorist financing. The risk rate is very high as the

KYC and CDD is done through online platform.

Role of BSL’s risk appetite

The amount of risk an entity is willing to accept or retain in order to achieve its objectives. It

is a statement or series of statements that describes the entity’s attitude towards risk taking.

Determining an entity’s risk appetite occurs through the development of risk appetite

statements which clearly set out what the executive consider to be acceptable risk-taking.

Risk appetite statements are usually aligned to categories of risk e.g. financial, people and

reputation risks.

In every merger and acquisitions, there are certain risks which the premier institutions must

take. BSL is an Australian company, never exposed to the outside environment (Ha, 2019).

Along with this, BSL has never handled the business of such type in Australia (Harbitz et al.,

2016). After the acquisition, there will be a complete overhaul of administration in BSL so

there is a need to consider the risk appetite of BSL without which no decision can be taken

(Hartung, 2017).

How to review the ML/TF assessment?

There would be mid-term review of ML/TF assessment to cater to new needs of the

organization. There is need of timely review of assessment method (Hsu et al., 2017) so the

ML/TF assessment will be reviewed after every 3 year along with mid-term reviews

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

depending on need of the hour. Top review the likelihood, impact and score related to

potential of risk will be assessed using above mentioned tools identified in previous section

(Jedrzychowska & Poprawska, 2016). Along with this the risk assessment will be done

considering standards mandated by AUSTRAC and financial intelligence agencies of New

Zealand (Laryea et al., 2018). This will make the process comprehensive enough to fulfill all

needs associated with risk methodology (Lema et al., 2016).

ML/TF vulnerabilities

1. Vulnerabilities arising due to online trade financing and leasing products

Due to the online method of transactions, BSL can get mired into controversies related to the

funding of banned organizations over the world like Taliban, Jaish-e-Mohammed, ISIS, etc.

Along with this cryptocurrency and blockchain technology is not legal in some countries. the

online nature of transactions may lead to an exchange of Cryptocurrencies (Lever & Kifayat,

2016). Thus, the company may be accused of illegal financing. Along with this many shell

firms trade and lease online so BSL can be a victim of the issue of black money (Locke et al.,

2017).

2. vulnerabilities arising due to running an offshore branch that provides products and

services to New Zealand customers

There can be monitoring problem due to the offshore nature of the entity leading to bad work

culture (Management, 2017). To be more concerned with, the illegal activities can be funded

by FF due to the lack of effective monitoring. Terrorism financing and many scandals can

happen due to lack of administrative accountability. There can be illegal funding for elections

occurring all over the world (Mansour & Jaaron, 2018). The bogus shell companies may get

registered on the online trading platform leading to the parking of black money.

Discussion of conclusions due to the impact of different strategies

There is a need to do situational analysis before arriving at any decision related to the

acquisition. If BSL decides to acquire the FF, it will have to set up a robust monitoring

depending on need of the hour. Top review the likelihood, impact and score related to

potential of risk will be assessed using above mentioned tools identified in previous section

(Jedrzychowska & Poprawska, 2016). Along with this the risk assessment will be done

considering standards mandated by AUSTRAC and financial intelligence agencies of New

Zealand (Laryea et al., 2018). This will make the process comprehensive enough to fulfill all

needs associated with risk methodology (Lema et al., 2016).

ML/TF vulnerabilities

1. Vulnerabilities arising due to online trade financing and leasing products

Due to the online method of transactions, BSL can get mired into controversies related to the

funding of banned organizations over the world like Taliban, Jaish-e-Mohammed, ISIS, etc.

Along with this cryptocurrency and blockchain technology is not legal in some countries. the

online nature of transactions may lead to an exchange of Cryptocurrencies (Lever & Kifayat,

2016). Thus, the company may be accused of illegal financing. Along with this many shell

firms trade and lease online so BSL can be a victim of the issue of black money (Locke et al.,

2017).

2. vulnerabilities arising due to running an offshore branch that provides products and

services to New Zealand customers

There can be monitoring problem due to the offshore nature of the entity leading to bad work

culture (Management, 2017). To be more concerned with, the illegal activities can be funded

by FF due to the lack of effective monitoring. Terrorism financing and many scandals can

happen due to lack of administrative accountability. There can be illegal funding for elections

occurring all over the world (Mansour & Jaaron, 2018). The bogus shell companies may get

registered on the online trading platform leading to the parking of black money.

Discussion of conclusions due to the impact of different strategies

There is a need to do situational analysis before arriving at any decision related to the

acquisition. If BSL decides to acquire the FF, it will have to set up a robust monitoring

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

system because of offshore trading of money (Masterov et al., 2016) (McBride, 2017). The

company will have to abide all the rules and regulations laid by Reserve bank of New

Zealand and Financial Market Authority (FMA) to enter to its new market.

Part 2

Introduction

The assessment 1 carried in previous paper considered a company named BSL. BSL was

considering acquiring new business in New Zealand named FF. In assessment one, the

research methodology for risk assessment was identified and presented. In this part of the

project, it is assumed that the company has decided to acquire the online trading business of

FF. so there is a need to place controls which are identified and implemented in this part of

the project (Fitzpatrick et al., 2017). BSL is an Australian company trying to expand in other

markets. It is in the process of acquiring new business, but that new business has certain risks

which have been identified in assessment one. This assessment caters to the need of

placement of controls to avert the risks identified in the previous paper.

AML/CTF controls

Initial controls required

1. Controls on number of transactions done by a single company or individual

2. Controls on the amount of money traded on the platform along with a restriction on an

extra amount of leasing

3. Controls on type of countries to be provided facility especially safe havens for money

laundering and terrorism financing

4. Controls on any unauthorized transaction

system because of offshore trading of money (Masterov et al., 2016) (McBride, 2017). The

company will have to abide all the rules and regulations laid by Reserve bank of New

Zealand and Financial Market Authority (FMA) to enter to its new market.

Part 2

Introduction

The assessment 1 carried in previous paper considered a company named BSL. BSL was

considering acquiring new business in New Zealand named FF. In assessment one, the

research methodology for risk assessment was identified and presented. In this part of the

project, it is assumed that the company has decided to acquire the online trading business of

FF. so there is a need to place controls which are identified and implemented in this part of

the project (Fitzpatrick et al., 2017). BSL is an Australian company trying to expand in other

markets. It is in the process of acquiring new business, but that new business has certain risks

which have been identified in assessment one. This assessment caters to the need of

placement of controls to avert the risks identified in the previous paper.

AML/CTF controls

Initial controls required

1. Controls on number of transactions done by a single company or individual

2. Controls on the amount of money traded on the platform along with a restriction on an

extra amount of leasing

3. Controls on type of countries to be provided facility especially safe havens for money

laundering and terrorism financing

4. Controls on any unauthorized transaction

9

Controls required on an ongoing basis

The controls required on an ongoing basis are a restriction to countries acting as safe havens

for money laundering and terrorism financing (Essabbar et al., 2016). The suspected

individuals or companies should be barred from trading and acquiring services of BSL. There

must be control on suspected or wrongfully earned amount.

Current controls to be used

Currently, BSL provides services to its customer only after proper authentication of identity

documents and recognizing the source of money. These controls will be used after acquiring

the FF also. Along with this BSL has control on recordkeeping whereby every transaction is

recorded in an electronic system. The limited number of individuals can access these records

so there are very fewer chances of tempering (Farughi et al., 2016). There have been controls

over the number of persons entering the premises of the office. This control will also be kept

the same after the acquisition.

Stakeholders to be consulted

All financiers of the company will be consulted for approval of plans related to controls.

They will be persuaded to provide money for placing the necessary internal and external

controls in the company (Elboshy et al., 2019). Other stakeholders will be executive. Before

implementing any plan, there will need to take concerned executive authorities in confidence

so that change is implemented. Employees will also be taken into confidence as there can be

older employees who may be reluctant to place new controls or make earlier controls get

regulated strictly. There will need to consult experts on the matter so that the plan is

adequately formed and implemented.

Status of current controls

There will need to modify current controls according to new needs with the acquisition of a

new company (Ritter et al., 2017). Some current controls like identification of person

availing the financial service of BSL, restriction on the amount to be raised, etc. will work

adequately as such but the one related to online trading and leasing must be modified to cater

Controls required on an ongoing basis

The controls required on an ongoing basis are a restriction to countries acting as safe havens

for money laundering and terrorism financing (Essabbar et al., 2016). The suspected

individuals or companies should be barred from trading and acquiring services of BSL. There

must be control on suspected or wrongfully earned amount.

Current controls to be used

Currently, BSL provides services to its customer only after proper authentication of identity

documents and recognizing the source of money. These controls will be used after acquiring

the FF also. Along with this BSL has control on recordkeeping whereby every transaction is

recorded in an electronic system. The limited number of individuals can access these records

so there are very fewer chances of tempering (Farughi et al., 2016). There have been controls

over the number of persons entering the premises of the office. This control will also be kept

the same after the acquisition.

Stakeholders to be consulted

All financiers of the company will be consulted for approval of plans related to controls.

They will be persuaded to provide money for placing the necessary internal and external

controls in the company (Elboshy et al., 2019). Other stakeholders will be executive. Before

implementing any plan, there will need to take concerned executive authorities in confidence

so that change is implemented. Employees will also be taken into confidence as there can be

older employees who may be reluctant to place new controls or make earlier controls get

regulated strictly. There will need to consult experts on the matter so that the plan is

adequately formed and implemented.

Status of current controls

There will need to modify current controls according to new needs with the acquisition of a

new company (Ritter et al., 2017). Some current controls like identification of person

availing the financial service of BSL, restriction on the amount to be raised, etc. will work

adequately as such but the one related to online trading and leasing must be modified to cater

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

to new needs with new responsibilities due to the acquisition of new organization (Phadtare

et al., 2018). Along with this, certain new controls need to be established for example

recognizing the channels of financial trading online, recognition of the origin of trading,

regular identification of bogus companies, etc.

Required new controls

There is a need for new controls with the changing nature of work of the company. The

priority among new control is to identify the individual or entity involved in online trading.

This will result in the recognition of bogus companies leading to the prevention of money

laundering. Along with this, there must be other controls (Ryabinin, 2015). As mentioned

above the channels of routing of money in the company must be recognized so that no illegal

trading and leasing take place while executing the work related to day to day business of the

company. There must be adequate control of recognition of the origin of the money so that

the money traded on the online platform may be recognized as legal or illegal. There is a

need for effective monitoring for which digital means of communication will help the most.

There must be a digital transformation of the company so that the company can monitor each

relevant activity from the office of Australia. The customers need to be identified so that no

criminal or terrorist can access the platform. There must be a prudent information system to

regulate the activities as per standards of AUSTRAC.

B) Assumption of approved control

It is assumed that the priority control of identification of person or entity trading online has

been approved. There is a need to identify each individual and entity which is associated with

trading and leasing activities of the company. This will make BSL effectively monitored

company with sound fiscal management (Ryabinin & Strukov, 2018). There must be

effective communication channels to deal with the issue of distance-based business or

offshore location of headquarters of FF. this will make the company recognize each

individual associated and it will be able to eliminate the chances of money laundering and

terrorism financing through its platform.

to new needs with new responsibilities due to the acquisition of new organization (Phadtare

et al., 2018). Along with this, certain new controls need to be established for example

recognizing the channels of financial trading online, recognition of the origin of trading,

regular identification of bogus companies, etc.

Required new controls

There is a need for new controls with the changing nature of work of the company. The

priority among new control is to identify the individual or entity involved in online trading.

This will result in the recognition of bogus companies leading to the prevention of money

laundering. Along with this, there must be other controls (Ryabinin, 2015). As mentioned

above the channels of routing of money in the company must be recognized so that no illegal

trading and leasing take place while executing the work related to day to day business of the

company. There must be adequate control of recognition of the origin of the money so that

the money traded on the online platform may be recognized as legal or illegal. There is a

need for effective monitoring for which digital means of communication will help the most.

There must be a digital transformation of the company so that the company can monitor each

relevant activity from the office of Australia. The customers need to be identified so that no

criminal or terrorist can access the platform. There must be a prudent information system to

regulate the activities as per standards of AUSTRAC.

B) Assumption of approved control

It is assumed that the priority control of identification of person or entity trading online has

been approved. There is a need to identify each individual and entity which is associated with

trading and leasing activities of the company. This will make BSL effectively monitored

company with sound fiscal management (Ryabinin & Strukov, 2018). There must be

effective communication channels to deal with the issue of distance-based business or

offshore location of headquarters of FF. this will make the company recognize each

individual associated and it will be able to eliminate the chances of money laundering and

terrorism financing through its platform.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

How to design the approved control?

The approved control must be designed appropriately so that the risk associated with online

money trading can be removed. There will be setting up of a desk authority which will cater

to the need of identification of persons using the services of the company. The online

registration system would be set up which will provide different long in ID for each person or

entity availing the services of the company. The concerned person will have to submit the

relevant documents like address proof, citizenship, source of money, etc. these documents

will be scanned by the desk authority (Scannella, 2016) Only after complete recognition of

the individual, the login ID will be provided. Thus, every person who avails the services of

the company will have to identify himself or herself. For authenticating the documents, the

experts would be hired who will identify the persons associated with transactions happening

online (Sandal, 2018).

Working with stakeholders

The plan will be formulated by the chief manager with the consultation of all stakeholders.

The desk authority will be set up with the help of all stakeholders associated with the day to

day working in the company. The plan will be approved by financiers to set up a desk

authority and pay him or her monthly with adequate provisions to hire talented persons as

experts (Selim et al., 2019). There will be approval from executive so that plan gets

authorized from the company and there is set up of desk authority catering to the need of

identification of each individual. The local level employees will be consulted and given a

presentation of the plan so that change is implemented without any hiccup. Not taking

employees into confidence may result in resentment among employees that may culminate

into the severe situation like strike or loss of key employees. The plan will be presented to

government authorities in the form mandated by AUSTRAC so that all legal requirements

are complied with. This will prevent future legal complications which cost a huge amount of

profit once litigation is filed against any company (Singh & Siwach, 2018). To prevent that

happening in the future, all legal requirements related to AML/CTF activities will be met

(Shafiee, 2016).

How to design the approved control?

The approved control must be designed appropriately so that the risk associated with online

money trading can be removed. There will be setting up of a desk authority which will cater

to the need of identification of persons using the services of the company. The online

registration system would be set up which will provide different long in ID for each person or

entity availing the services of the company. The concerned person will have to submit the

relevant documents like address proof, citizenship, source of money, etc. these documents

will be scanned by the desk authority (Scannella, 2016) Only after complete recognition of

the individual, the login ID will be provided. Thus, every person who avails the services of

the company will have to identify himself or herself. For authenticating the documents, the

experts would be hired who will identify the persons associated with transactions happening

online (Sandal, 2018).

Working with stakeholders

The plan will be formulated by the chief manager with the consultation of all stakeholders.

The desk authority will be set up with the help of all stakeholders associated with the day to

day working in the company. The plan will be approved by financiers to set up a desk

authority and pay him or her monthly with adequate provisions to hire talented persons as

experts (Selim et al., 2019). There will be approval from executive so that plan gets

authorized from the company and there is set up of desk authority catering to the need of

identification of each individual. The local level employees will be consulted and given a

presentation of the plan so that change is implemented without any hiccup. Not taking

employees into confidence may result in resentment among employees that may culminate

into the severe situation like strike or loss of key employees. The plan will be presented to

government authorities in the form mandated by AUSTRAC so that all legal requirements

are complied with. This will prevent future legal complications which cost a huge amount of

profit once litigation is filed against any company (Singh & Siwach, 2018). To prevent that

happening in the future, all legal requirements related to AML/CTF activities will be met

(Shafiee, 2016).

12

Allocation of responsibility

The senior manager of the concerned regional branch in New Zealand will be allocated

responsibility to formulate a plan for the mentioned control and implement the changes as

required. The senior manager will be able to persuade higher authorities as well as local

employees. The concerned branch manager must have intellectual knowledge related to

business to be conducted in a foreign country (New Zealand). This will lead to the

implementation of change without any major problem (Singh & Sur, 2018). The

contingencies will be planned according to the situation so that they are sorted out at the right

time by the right person.

Monitoring the control

Money Laundering Reporting Officer (MLRO) will be appointed to cater to the need of

monitoring an offshore entity. MLRO will comply with the requirements related to regular

update about money laundering activities to government authorities and board of BSL. There

will be need of accessing the transaction files and other relevant material so MLRO will be

provide adequate authority to conduct his work without any fear, favor or ill-will. The senior

person with impeccable character and integrity will be appointed for the purpose of

monitoring work in FF in NewZealand. This will make the organization flexible enough to

cater to the need of monitoring an offshore entity without any hassle.

c) System designing for regular update

Senior manager of each regional branch will be given the responsibility to monitor the

changes. He will be asked to authorize the desk authority to maintain a record of persons

identified (Solozhentsev, 2018). Each person who comes online for trading and leasing will

be identified so bogus companies and individuals will be identified in the system. Their

information will get registered into the electronic system of the company. So if that person

tries to register again, he or she will be recognized by the system leading to the withdrawal of

his application to avail the services of BSL. The branch senior manager will be asked to

Allocation of responsibility

The senior manager of the concerned regional branch in New Zealand will be allocated

responsibility to formulate a plan for the mentioned control and implement the changes as

required. The senior manager will be able to persuade higher authorities as well as local

employees. The concerned branch manager must have intellectual knowledge related to

business to be conducted in a foreign country (New Zealand). This will lead to the

implementation of change without any major problem (Singh & Sur, 2018). The

contingencies will be planned according to the situation so that they are sorted out at the right

time by the right person.

Monitoring the control

Money Laundering Reporting Officer (MLRO) will be appointed to cater to the need of

monitoring an offshore entity. MLRO will comply with the requirements related to regular

update about money laundering activities to government authorities and board of BSL. There

will be need of accessing the transaction files and other relevant material so MLRO will be

provide adequate authority to conduct his work without any fear, favor or ill-will. The senior

person with impeccable character and integrity will be appointed for the purpose of

monitoring work in FF in NewZealand. This will make the organization flexible enough to

cater to the need of monitoring an offshore entity without any hassle.

c) System designing for regular update

Senior manager of each regional branch will be given the responsibility to monitor the

changes. He will be asked to authorize the desk authority to maintain a record of persons

identified (Solozhentsev, 2018). Each person who comes online for trading and leasing will

be identified so bogus companies and individuals will be identified in the system. Their

information will get registered into the electronic system of the company. So if that person

tries to register again, he or she will be recognized by the system leading to the withdrawal of

his application to avail the services of BSL. The branch senior manager will be asked to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.