Financial Analysis: AMP and CBA Share Prices and Capital Budgeting

VerifiedAdded on 2023/06/07

|17

|3828

|250

Report

AI Summary

This report provides a financial analysis of AMP and CBA share prices, examining their performance over a five-year period. It delves into key financial metrics, including daily changes, volume, market capitalization, and dividend information. The report explores the impact of the Royal Commission on the financial institutions, discussing the challenges of misalignment between customers and financial service providers, loss of trust, and potential risks within the financial system. The report then transitions into capital budgeting techniques, providing an overview of the Required Rate of Return (RRR), Internal Rate of Return (IRR), and Net Present Value (NPV). It includes the decision rules associated with each method and demonstrates calculations of NPV and IRR for two hypothetical projects, assessing their viability based on the given financial data. The report concludes by highlighting the significance of these financial tools in investment decision-making.

AMP AND CBA SHARE PRICES 1

AMP and CBA share price and Capital budget

By (Student’s Name)

Course

Tutor

University

[Date Submitted]

AMP and CBA share price and Capital budget

By (Student’s Name)

Course

Tutor

University

[Date Submitted]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AMP AND CBA SHARE PRICES 2

Part A

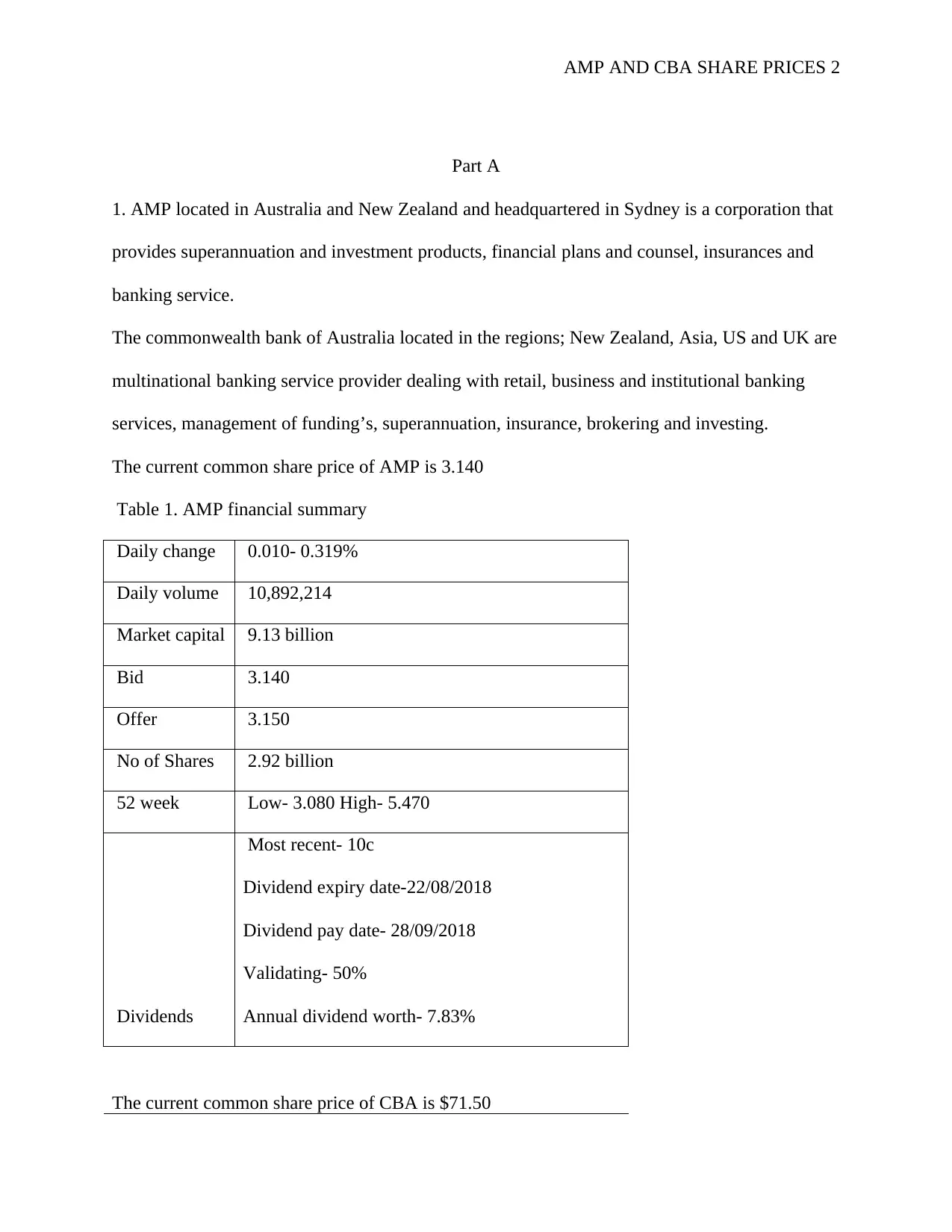

1. AMP located in Australia and New Zealand and headquartered in Sydney is a corporation that

provides superannuation and investment products, financial plans and counsel, insurances and

banking service.

The commonwealth bank of Australia located in the regions; New Zealand, Asia, US and UK are

multinational banking service provider dealing with retail, business and institutional banking

services, management of funding’s, superannuation, insurance, brokering and investing.

The current common share price of AMP is 3.140

Table 1. AMP financial summary

Daily change 0.010- 0.319%

Daily volume 10,892,214

Market capital 9.13 billion

Bid 3.140

Offer 3.150

No of Shares 2.92 billion

52 week Low- 3.080 High- 5.470

Dividends

Most recent- 10c

Dividend expiry date-22/08/2018

Dividend pay date- 28/09/2018

Validating- 50%

Annual dividend worth- 7.83%

The current common share price of CBA is $71.50

Part A

1. AMP located in Australia and New Zealand and headquartered in Sydney is a corporation that

provides superannuation and investment products, financial plans and counsel, insurances and

banking service.

The commonwealth bank of Australia located in the regions; New Zealand, Asia, US and UK are

multinational banking service provider dealing with retail, business and institutional banking

services, management of funding’s, superannuation, insurance, brokering and investing.

The current common share price of AMP is 3.140

Table 1. AMP financial summary

Daily change 0.010- 0.319%

Daily volume 10,892,214

Market capital 9.13 billion

Bid 3.140

Offer 3.150

No of Shares 2.92 billion

52 week Low- 3.080 High- 5.470

Dividends

Most recent- 10c

Dividend expiry date-22/08/2018

Dividend pay date- 28/09/2018

Validating- 50%

Annual dividend worth- 7.83%

The current common share price of CBA is $71.50

14.5

0

10

20

30

2016201520142013 2017

12.5

14

14

14.5

13.5

14

14

26

28

28

29

11.5 11.5 23

201 5 201742013201

6201

$884m

m

$972m

$848m

$672m

0

250

500

750

1,000

1,250

0

250

500

750

1,000

1,250

201520142013 2016 2017

$1,045m

$1,120m

$486m

$1,040m

$849m

AMP AND CBA SHARE PRICES 3

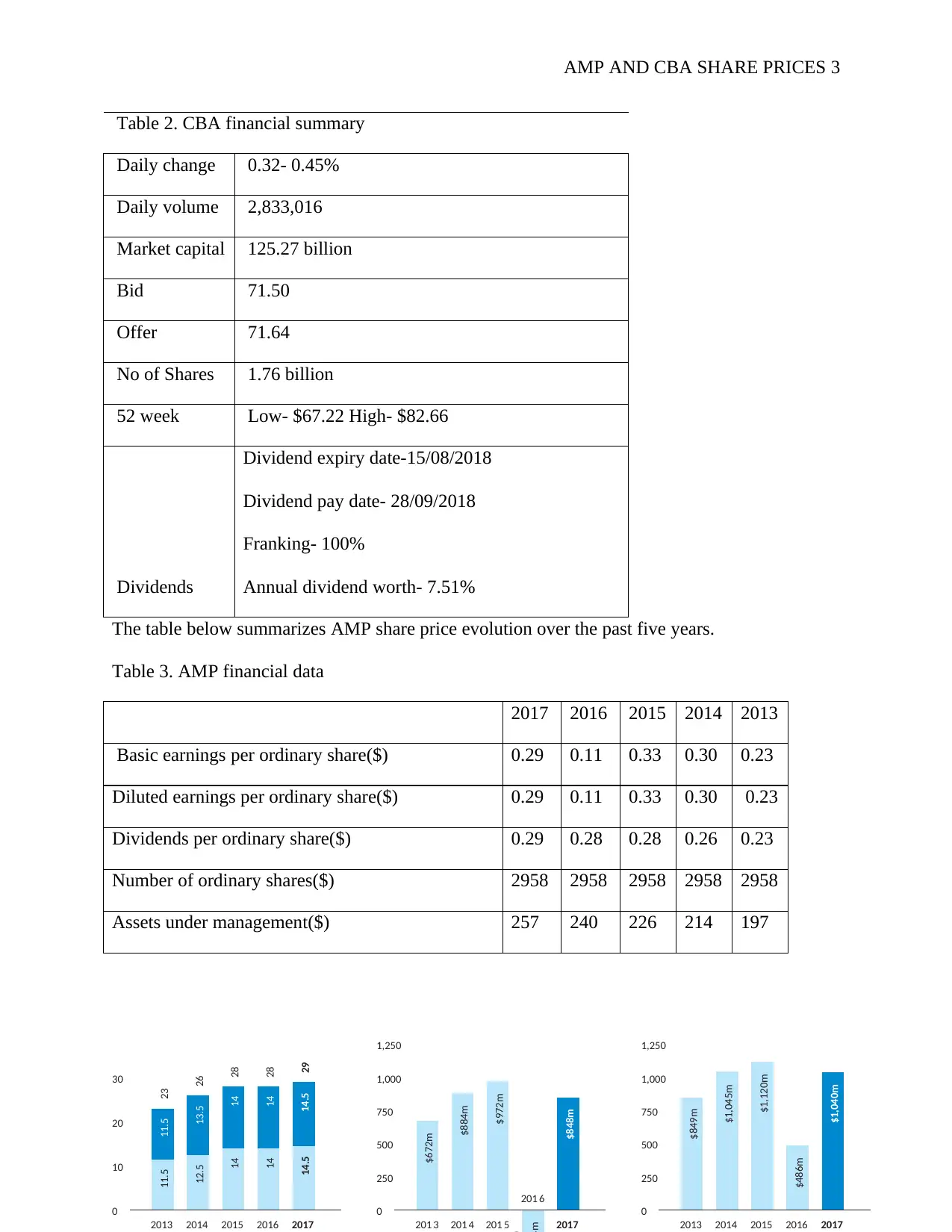

Table 2. CBA financial summary

Daily change 0.32- 0.45%

Daily volume 2,833,016

Market capital 125.27 billion

Bid 71.50

Offer 71.64

No of Shares 1.76 billion

52 week Low- $67.22 High- $82.66

Dividends

Dividend expiry date-15/08/2018

Dividend pay date- 28/09/2018

Franking- 100%

Annual dividend worth- 7.51%

The table below summarizes AMP share price evolution over the past five years.

Table 3. AMP financial data

2017 2016 2015 2014 2013

Basic earnings per ordinary share($) 0.29 0.11 0.33 0.30 0.23

Diluted earnings per ordinary share($) 0.29 0.11 0.33 0.30 0.23

Dividends per ordinary share($) 0.29 0.28 0.28 0.26 0.23

Number of ordinary shares($) 2958 2958 2958 2958 2958

Assets under management($) 257 240 226 214 197

0

10

20

30

2016201520142013 2017

12.5

14

14

14.5

13.5

14

14

26

28

28

29

11.5 11.5 23

201 5 201742013201

6201

$884m

m

$972m

$848m

$672m

0

250

500

750

1,000

1,250

0

250

500

750

1,000

1,250

201520142013 2016 2017

$1,045m

$1,120m

$486m

$1,040m

$849m

AMP AND CBA SHARE PRICES 3

Table 2. CBA financial summary

Daily change 0.32- 0.45%

Daily volume 2,833,016

Market capital 125.27 billion

Bid 71.50

Offer 71.64

No of Shares 1.76 billion

52 week Low- $67.22 High- $82.66

Dividends

Dividend expiry date-15/08/2018

Dividend pay date- 28/09/2018

Franking- 100%

Annual dividend worth- 7.51%

The table below summarizes AMP share price evolution over the past five years.

Table 3. AMP financial data

2017 2016 2015 2014 2013

Basic earnings per ordinary share($) 0.29 0.11 0.33 0.30 0.23

Diluted earnings per ordinary share($) 0.29 0.11 0.33 0.30 0.23

Dividends per ordinary share($) 0.29 0.28 0.28 0.26 0.23

Number of ordinary shares($) 2958 2958 2958 2958 2958

Assets under management($) 257 240 226 214 197

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(

AMP AND CBA SHARE PRICES 4

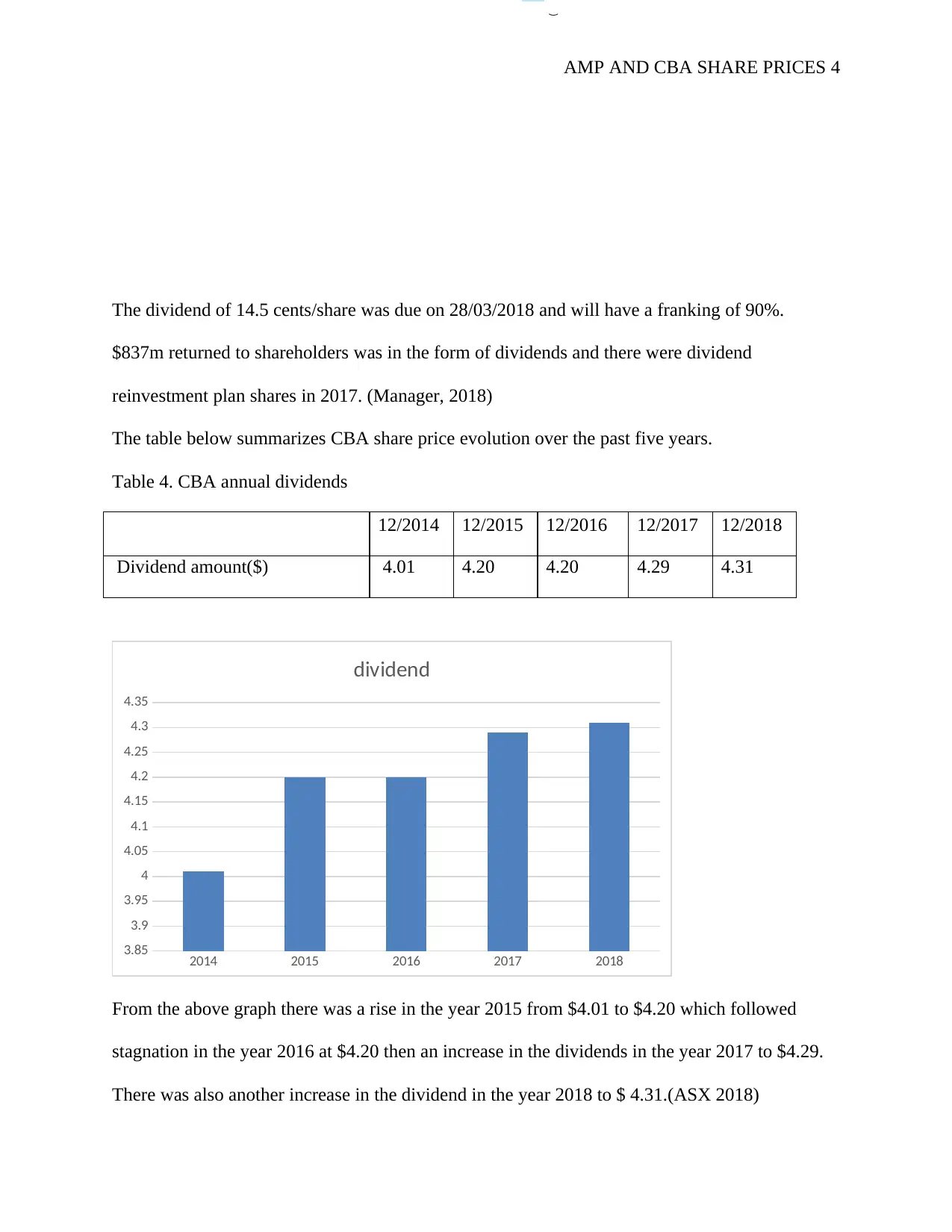

The dividend of 14.5 cents/share was due on 28/03/2018 and will have a franking of 90%.

$837m returned to shareholders was in the form of dividends and there were dividend

reinvestment plan shares in 2017. (Manager, 2018)

The table below summarizes CBA share price evolution over the past five years.

Table 4. CBA annual dividends

12/2014 12/2015 12/2016 12/2017 12/2018

Dividend amount($) 4.01 4.20 4.20 4.29 4.31

2014 2015 2016 2017 2018

3.85

3.9

3.95

4

4.05

4.1

4.15

4.2

4.25

4.3

4.35

dividend

From the above graph there was a rise in the year 2015 from $4.01 to $4.20 which followed

stagnation in the year 2016 at $4.20 then an increase in the dividends in the year 2017 to $4.29.

There was also another increase in the dividend in the year 2018 to $ 4.31.(ASX 2018)

AMP AND CBA SHARE PRICES 4

The dividend of 14.5 cents/share was due on 28/03/2018 and will have a franking of 90%.

$837m returned to shareholders was in the form of dividends and there were dividend

reinvestment plan shares in 2017. (Manager, 2018)

The table below summarizes CBA share price evolution over the past five years.

Table 4. CBA annual dividends

12/2014 12/2015 12/2016 12/2017 12/2018

Dividend amount($) 4.01 4.20 4.20 4.29 4.31

2014 2015 2016 2017 2018

3.85

3.9

3.95

4

4.05

4.1

4.15

4.2

4.25

4.3

4.35

dividend

From the above graph there was a rise in the year 2015 from $4.01 to $4.20 which followed

stagnation in the year 2016 at $4.20 then an increase in the dividends in the year 2017 to $4.29.

There was also another increase in the dividend in the year 2018 to $ 4.31.(ASX 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AMP AND CBA SHARE PRICES 5

2. Royal commission objective was to restore trust and confidence and maintain the already

existing stability in the economic sector. Banks are vulnerable to economic fluctuations because

of their reliance on higher financial leverage. Banks are opaque to most of their customers

therefore the royal commission results in loss of confidence hence expected less deposits. This

may be because the royal commission inquiries into the following matters.

First is misconduct in financial service providers. Secondly is any conduct by a financial service

provider that stoops below the population’s expectations and also superannuation of an

individual retirement savings that do not coordinate with the community’s expectations among

others.

From the royal commission the following can be observed from both the systematic and

unsystematic risk.

First there is a challenge of misalignment in relation to the customer and their financial service

provider.

There is loss of trust in the financial system due to less effective powers in the tackling of illegal

behaviors.

Lastly there is a potential risk that of negative sentiment spilling in the larger finances system.

The main aim of royal commission is tackling misconduct which includes fairness and

fulfillment of a community’s expectations. Complaints resulting from financial counsel will and

insurance claims will result in compensations and this will also elevate ASIC

Inquiring by the royal commission has led to attacks on the banks by political principles. .

The impactful role by the royal commission is regarding the costs placed on consumers,

competition and financial stability of the system is key in provision of financial counsel and

insurance matters and it is most impactful when it comes to loans.

2. Royal commission objective was to restore trust and confidence and maintain the already

existing stability in the economic sector. Banks are vulnerable to economic fluctuations because

of their reliance on higher financial leverage. Banks are opaque to most of their customers

therefore the royal commission results in loss of confidence hence expected less deposits. This

may be because the royal commission inquiries into the following matters.

First is misconduct in financial service providers. Secondly is any conduct by a financial service

provider that stoops below the population’s expectations and also superannuation of an

individual retirement savings that do not coordinate with the community’s expectations among

others.

From the royal commission the following can be observed from both the systematic and

unsystematic risk.

First there is a challenge of misalignment in relation to the customer and their financial service

provider.

There is loss of trust in the financial system due to less effective powers in the tackling of illegal

behaviors.

Lastly there is a potential risk that of negative sentiment spilling in the larger finances system.

The main aim of royal commission is tackling misconduct which includes fairness and

fulfillment of a community’s expectations. Complaints resulting from financial counsel will and

insurance claims will result in compensations and this will also elevate ASIC

Inquiring by the royal commission has led to attacks on the banks by political principles. .

The impactful role by the royal commission is regarding the costs placed on consumers,

competition and financial stability of the system is key in provision of financial counsel and

insurance matters and it is most impactful when it comes to loans.

AMP AND CBA SHARE PRICES 6

The royal commission’s findings by Hayne could result in permanent damage of AMP’s

franchise. There was a fall in stock by 4.4% which will lead to a price of $4.55. $600 billion as

deleted from the company’s asset worth 13 billion having recently traded 18 million shares.

From the finding a cost less than $4 million was utilized in the company’s customer remediating

procedure. The company also faced a major challenge as 15000 of its clients were being charged

not following the protocol while giving financial counsel. There were also charges of charging

for services not rendered.

There is a possibility of long-term scar on the AMP’ image resulting from Hayne’s findings.

AMP require major changes which fall among the responsibilities of the new.

The royal commission has produced evidence indicating that CBA has been charging already

dead clientele for financial counsel which has been done for the past ten years. The executive

general manager also recently admitted that the CBA financial planning still kept accepting

commissions from clients registered after July 2013 although the Fofa laws had been enacted.

Findings by the royal commission also revealed that there were ignored complaints by customers

about services not rendered being charged for over six years. This followed by CBA admitting to

charging for financial advice not given. From this revelation it is clear that both CBA and AMP’s

images have been tarnished and there is unexpected reduction in their share prices in the near

future.

Part B

Overview of Required Rate of Return (RRR) and the Internal Rate of Return (IRR)

Both are metrics used to account for the performance of particular investment overtime (Robson,

2017). In as much as they sound similar, it is worth noting that they describe the investment

performance in very different terms altogether. In simple terms, the RRR is the least return that a

The royal commission’s findings by Hayne could result in permanent damage of AMP’s

franchise. There was a fall in stock by 4.4% which will lead to a price of $4.55. $600 billion as

deleted from the company’s asset worth 13 billion having recently traded 18 million shares.

From the finding a cost less than $4 million was utilized in the company’s customer remediating

procedure. The company also faced a major challenge as 15000 of its clients were being charged

not following the protocol while giving financial counsel. There were also charges of charging

for services not rendered.

There is a possibility of long-term scar on the AMP’ image resulting from Hayne’s findings.

AMP require major changes which fall among the responsibilities of the new.

The royal commission has produced evidence indicating that CBA has been charging already

dead clientele for financial counsel which has been done for the past ten years. The executive

general manager also recently admitted that the CBA financial planning still kept accepting

commissions from clients registered after July 2013 although the Fofa laws had been enacted.

Findings by the royal commission also revealed that there were ignored complaints by customers

about services not rendered being charged for over six years. This followed by CBA admitting to

charging for financial advice not given. From this revelation it is clear that both CBA and AMP’s

images have been tarnished and there is unexpected reduction in their share prices in the near

future.

Part B

Overview of Required Rate of Return (RRR) and the Internal Rate of Return (IRR)

Both are metrics used to account for the performance of particular investment overtime (Robson,

2017). In as much as they sound similar, it is worth noting that they describe the investment

performance in very different terms altogether. In simple terms, the RRR is the least return that a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AMP AND CBA SHARE PRICES 7

particular company requires on its investments or projects that compensates them for a given

level of risk before proceeding with such investments. It is also known as the hurdle rate.

Essentially, the required rate of return is often an arbitrary figure that often differs from company

to company. Nevertheless, the required rate of return is often unrelated to the cost of funds

(Robson, 2017). On the other hand, the internal rate of return is the discount rate that when

functional to a series of cash flows outcome in a net present value of zero.

Decision Rule of RRR and IRR

There are certain decision rules that are used hand in hand with the RRR and the IRR. In essence,

the decision rule in the required rate of return is such that if the NPV of the required rate of

return is greater than zero for a given project, then the project passes the test and hence qualifies

to be evaluated further, if the RRR is a lesser amount than zero then the project fails the test and

hence is discarded in as much as it could be a great project. On the other hand, the rule that is

used as decision in the IRR is such that when the computed internal rate of return is greater than

the cost of capital, then the project should be taken and if the IRR is the same to the cost of

capital, then the managers should be indifferent, and if the IRR is a lesser amount of than the cost

of capital, then the project should be cast off. Hence, while selecting two projects that are equally

elite, the one with the highest internal rate of return ought to be chosen as long as the computed

rate is more than the cost of capital.

Overview of Net Present Value (NPV)

The Net Present Value (NPV) is a metric used to indicate the expected impact of a particular

project on the value of a firm or company (Zen Wealth, 2016). Essentially, projects with a

positive NPV are viewed with the expectation that they shall increase the value of the firm while

particular company requires on its investments or projects that compensates them for a given

level of risk before proceeding with such investments. It is also known as the hurdle rate.

Essentially, the required rate of return is often an arbitrary figure that often differs from company

to company. Nevertheless, the required rate of return is often unrelated to the cost of funds

(Robson, 2017). On the other hand, the internal rate of return is the discount rate that when

functional to a series of cash flows outcome in a net present value of zero.

Decision Rule of RRR and IRR

There are certain decision rules that are used hand in hand with the RRR and the IRR. In essence,

the decision rule in the required rate of return is such that if the NPV of the required rate of

return is greater than zero for a given project, then the project passes the test and hence qualifies

to be evaluated further, if the RRR is a lesser amount than zero then the project fails the test and

hence is discarded in as much as it could be a great project. On the other hand, the rule that is

used as decision in the IRR is such that when the computed internal rate of return is greater than

the cost of capital, then the project should be taken and if the IRR is the same to the cost of

capital, then the managers should be indifferent, and if the IRR is a lesser amount of than the cost

of capital, then the project should be cast off. Hence, while selecting two projects that are equally

elite, the one with the highest internal rate of return ought to be chosen as long as the computed

rate is more than the cost of capital.

Overview of Net Present Value (NPV)

The Net Present Value (NPV) is a metric used to indicate the expected impact of a particular

project on the value of a firm or company (Zen Wealth, 2016). Essentially, projects with a

positive NPV are viewed with the expectation that they shall increase the value of the firm while

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AMP AND CBA SHARE PRICES 8

those with a negative NPV are considered to be of a negative impact on the firm’s value (Zen

Wealth, 2016). Thus, the NPV decision rule is such that all independent projects whose NPV is

positive should be accepted. Nevertheless, when faced with the decision to choose among

projects that are mutually exclusive, the project that generates the largest/highest (positive)

should be chosen.

Calculation of Net Present Value (NPV)

The formula is such that:

Where: CFt = the cash flow at time t and r = the cost of capital.

Computing NPV for project X at a discounting rate of 12%

NPV = -300,000 + 80,000 / (1 + 0.12)1 + 140,000 / (1 + 0.12)2 + 130,000 / (1 + 0.12)3 + 160,000 /

(1 + 0.12)4

NPV = -300,000 + 71,428.6 + 111,607.1 + 92,531.4 + 101,682.9

NPV = $ 77,250

Computing NPV for project Y at a discounting rate of 12%

NPV = -300,000 + 160,000 / (1 + 0.12)1 + 160,000 / (1 + 0.12)2 + 160,000 / (1 + 0.12)3 +

160,000 / (1 + 0.12)4 + 160,000 / (1 + 0.12)5 160,000 / (1 + 0.12)6

NPV = -300,000 + 142,857.1 + 127,551 + 113,884.8 + 101,682.9 + 90,788.3 + 81,061

those with a negative NPV are considered to be of a negative impact on the firm’s value (Zen

Wealth, 2016). Thus, the NPV decision rule is such that all independent projects whose NPV is

positive should be accepted. Nevertheless, when faced with the decision to choose among

projects that are mutually exclusive, the project that generates the largest/highest (positive)

should be chosen.

Calculation of Net Present Value (NPV)

The formula is such that:

Where: CFt = the cash flow at time t and r = the cost of capital.

Computing NPV for project X at a discounting rate of 12%

NPV = -300,000 + 80,000 / (1 + 0.12)1 + 140,000 / (1 + 0.12)2 + 130,000 / (1 + 0.12)3 + 160,000 /

(1 + 0.12)4

NPV = -300,000 + 71,428.6 + 111,607.1 + 92,531.4 + 101,682.9

NPV = $ 77,250

Computing NPV for project Y at a discounting rate of 12%

NPV = -300,000 + 160,000 / (1 + 0.12)1 + 160,000 / (1 + 0.12)2 + 160,000 / (1 + 0.12)3 +

160,000 / (1 + 0.12)4 + 160,000 / (1 + 0.12)5 160,000 / (1 + 0.12)6

NPV = -300,000 + 142,857.1 + 127,551 + 113,884.8 + 101,682.9 + 90,788.3 + 81,061

AMP AND CBA SHARE PRICES 9

NPV = $357,825.1 ≈ $357,825

Decision Rule of NPV:

Both projects should be accepted because they yield a positive Net Present Value as calculated

above.

Calculation of IRR

The IRR formula is such that:

IRR = lower rate + [(NPV at the lower rate) / (Absolute sum of NPVs)] x Difference in the rates

Here, we already have the NPV at 12% for both projects. Hence, we can calculate the NPV at a

lower rate of 7% and also NPV at a higher rate of 16%.

NPV at a lower rate of 7%

PROJECT X:

NPV @ 7% = -300,000 + 80,000 / (1 + 0.07)1 + 140,000 / (1 + 0.07)2 + 130,000 / (1 + 0.07)3 +

160,000 / (1 + 0.07)4

NPV = -300,000 + 74,766.4 + 122,281.4 + 106,118.7 + 122,063.2

NPV = $ 125,229.7 ≈ $125,230

PROJECT Y

NPV = $357,825.1 ≈ $357,825

Decision Rule of NPV:

Both projects should be accepted because they yield a positive Net Present Value as calculated

above.

Calculation of IRR

The IRR formula is such that:

IRR = lower rate + [(NPV at the lower rate) / (Absolute sum of NPVs)] x Difference in the rates

Here, we already have the NPV at 12% for both projects. Hence, we can calculate the NPV at a

lower rate of 7% and also NPV at a higher rate of 16%.

NPV at a lower rate of 7%

PROJECT X:

NPV @ 7% = -300,000 + 80,000 / (1 + 0.07)1 + 140,000 / (1 + 0.07)2 + 130,000 / (1 + 0.07)3 +

160,000 / (1 + 0.07)4

NPV = -300,000 + 74,766.4 + 122,281.4 + 106,118.7 + 122,063.2

NPV = $ 125,229.7 ≈ $125,230

PROJECT Y

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AMP AND CBA SHARE PRICES 10

NPV @ 7 = -300,000 + 160,000 / (1 + 0.07)1 + 160,000 / (1 + 0.07)2 + 160,000 / (1 + 0.07)3 +

160,000 / (1 + 0.07)4 + 160,000 / (1 + 0.07)5 160,000 / (1 + 0.07)6

NPV = -300,000 + 149,532.7 + 139,750.2 + 130,607.7 + 122,063.2 + 114,077.8 + 106,614.8

NPV = $462,646.4 ≈ $462,646

Higher rate of NPV @ 16%

PROJECT X

NPV @ 16% = -300,000 + 80,000 / (1 + 0.16)1 + 140,000 / (1 + 0.16)2 + 130,000 / (1 + 0.16)3 +

160,000 / (1 + 0.16)4

NPV = -300,000 + 68,965.5 + 104,042.8 + 83,285.5 + 88,366.6

NPV = $ 44,660.4 ≈ $44,660

PROJECT Y

NPV @ 16 = -300,000 + 160,000 / (1 + 0.16)1 + 160,000 / (1 + 0.16)2 + 160,000 / (1 + 0.16)3 +

160,000 / (1 + 0.16)4 + 160,000 / (1 + 0.16)5 160,000 / (1 + 0.16)6

NPV = - 300,000 + 137,931 + 118,906.1 + 102,505.2 + 88,366.6 + 76,178.1 + 65,670.8

NPV = 289,557.8 ≈ 289,558

Determination of IRR for PROJECT X is as follows:

IRR = lower rate + [(NPV at the lower rate) / (Absolute sum of NPVs)] x Difference in the rates

NPV @ 7 = -300,000 + 160,000 / (1 + 0.07)1 + 160,000 / (1 + 0.07)2 + 160,000 / (1 + 0.07)3 +

160,000 / (1 + 0.07)4 + 160,000 / (1 + 0.07)5 160,000 / (1 + 0.07)6

NPV = -300,000 + 149,532.7 + 139,750.2 + 130,607.7 + 122,063.2 + 114,077.8 + 106,614.8

NPV = $462,646.4 ≈ $462,646

Higher rate of NPV @ 16%

PROJECT X

NPV @ 16% = -300,000 + 80,000 / (1 + 0.16)1 + 140,000 / (1 + 0.16)2 + 130,000 / (1 + 0.16)3 +

160,000 / (1 + 0.16)4

NPV = -300,000 + 68,965.5 + 104,042.8 + 83,285.5 + 88,366.6

NPV = $ 44,660.4 ≈ $44,660

PROJECT Y

NPV @ 16 = -300,000 + 160,000 / (1 + 0.16)1 + 160,000 / (1 + 0.16)2 + 160,000 / (1 + 0.16)3 +

160,000 / (1 + 0.16)4 + 160,000 / (1 + 0.16)5 160,000 / (1 + 0.16)6

NPV = - 300,000 + 137,931 + 118,906.1 + 102,505.2 + 88,366.6 + 76,178.1 + 65,670.8

NPV = 289,557.8 ≈ 289,558

Determination of IRR for PROJECT X is as follows:

IRR = lower rate + [(NPV at the lower rate) / (Absolute sum of NPVs)] x Difference in the rates

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AMP AND CBA SHARE PRICES 11

I.R.R = 7% + [(125,230) / (125,230 + 44,660)] x (16 – 7)

I.R.R = 7% + 6.63%

I.R.R = 13.63%

Determination of IRR for PROJECT Y is as follows:

IRR = lower rate + [(NPV at the lower rate) / (Absolute sum of NPVs)] x Difference in the rates

I.R.R = 7% + [(462,646) / (462,646 + 289,558)] x (16 – 7)

I.R.R = 7% + 5.54%

I.R.R = 12.54%

Decision Rule:

Both projects should be accepted because their computed internal rates of return are greater than

the cost of capital of 12%. However, the managers ought to be indifferent with regards to project

Y because the IRR is more or less equal to 12% hence further analysis of project Y ought to be

conducted to determine its feasibility.

Fundamentally, a change in the required rate of return will affect the decision or the conclusion

that will be arrived at, but it would not affect the IRR. Essentially, the IRR will be the same

despite the changes that are made to the required rate of return. It is worth noting that changes in

the required rate of return only affect how the decisions will be made but not the NPV or the

IRR.

I.R.R = 7% + [(125,230) / (125,230 + 44,660)] x (16 – 7)

I.R.R = 7% + 6.63%

I.R.R = 13.63%

Determination of IRR for PROJECT Y is as follows:

IRR = lower rate + [(NPV at the lower rate) / (Absolute sum of NPVs)] x Difference in the rates

I.R.R = 7% + [(462,646) / (462,646 + 289,558)] x (16 – 7)

I.R.R = 7% + 5.54%

I.R.R = 12.54%

Decision Rule:

Both projects should be accepted because their computed internal rates of return are greater than

the cost of capital of 12%. However, the managers ought to be indifferent with regards to project

Y because the IRR is more or less equal to 12% hence further analysis of project Y ought to be

conducted to determine its feasibility.

Fundamentally, a change in the required rate of return will affect the decision or the conclusion

that will be arrived at, but it would not affect the IRR. Essentially, the IRR will be the same

despite the changes that are made to the required rate of return. It is worth noting that changes in

the required rate of return only affect how the decisions will be made but not the NPV or the

IRR.

AMP AND CBA SHARE PRICES 12

In this case, computing the NPV of the projects using the required rate of return of 10% would

be as follows:

PROJECT X

NPV = -300,000 + 80,000 / (1 + 0.10)1 + 140,000 / (1 + 0.10)2 + 130,000 / (1 + 0.10)3 + 160,000 /

(1 + 0.10)4

NPV = -300,000 + 72,727.3 + 115,702.5 + 97,670.9 + 109,282.2

NPV = $ 95,382.9 ≈ $ 95,383

PROJECT Y

NPV = -300,000 + 160,000 / (1 + 0.10)1 + 160,000 / (1 + 0.10)2 + 160,000 / (1 + 0.10)3 +

160,000 / (1 + 0.10)4 + 160,000 / (1 + 0.10)5 160,000 / (1 + 0.10)6

NPV = -300,000 + 145,454.5 + 132,231.4 + 120,210.4 + 109,282.2 + 99,347.4 + 90,315.8

NPV = $ 396,841.7 ≈ $ 396,842

It is worth noting that if the above projects were of an equal duration, then the change in required

rate of return would influence the final decision based on the NPV criterion.

If the same required rate of return @ 10% is used in the computation of IRR, then there IRR

would not change but the decision to be made would be influenced. In this case, the IRR would

be computed as follows:

First compute the NPV at a lower rate of 6% and NPV at a higher rate of 13%

In this case, computing the NPV of the projects using the required rate of return of 10% would

be as follows:

PROJECT X

NPV = -300,000 + 80,000 / (1 + 0.10)1 + 140,000 / (1 + 0.10)2 + 130,000 / (1 + 0.10)3 + 160,000 /

(1 + 0.10)4

NPV = -300,000 + 72,727.3 + 115,702.5 + 97,670.9 + 109,282.2

NPV = $ 95,382.9 ≈ $ 95,383

PROJECT Y

NPV = -300,000 + 160,000 / (1 + 0.10)1 + 160,000 / (1 + 0.10)2 + 160,000 / (1 + 0.10)3 +

160,000 / (1 + 0.10)4 + 160,000 / (1 + 0.10)5 160,000 / (1 + 0.10)6

NPV = -300,000 + 145,454.5 + 132,231.4 + 120,210.4 + 109,282.2 + 99,347.4 + 90,315.8

NPV = $ 396,841.7 ≈ $ 396,842

It is worth noting that if the above projects were of an equal duration, then the change in required

rate of return would influence the final decision based on the NPV criterion.

If the same required rate of return @ 10% is used in the computation of IRR, then there IRR

would not change but the decision to be made would be influenced. In this case, the IRR would

be computed as follows:

First compute the NPV at a lower rate of 6% and NPV at a higher rate of 13%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.