Financial Misconduct at AMP Limited: A Business and Ethical Report

VerifiedAdded on 2021/04/21

|7

|1549

|250

Report

AI Summary

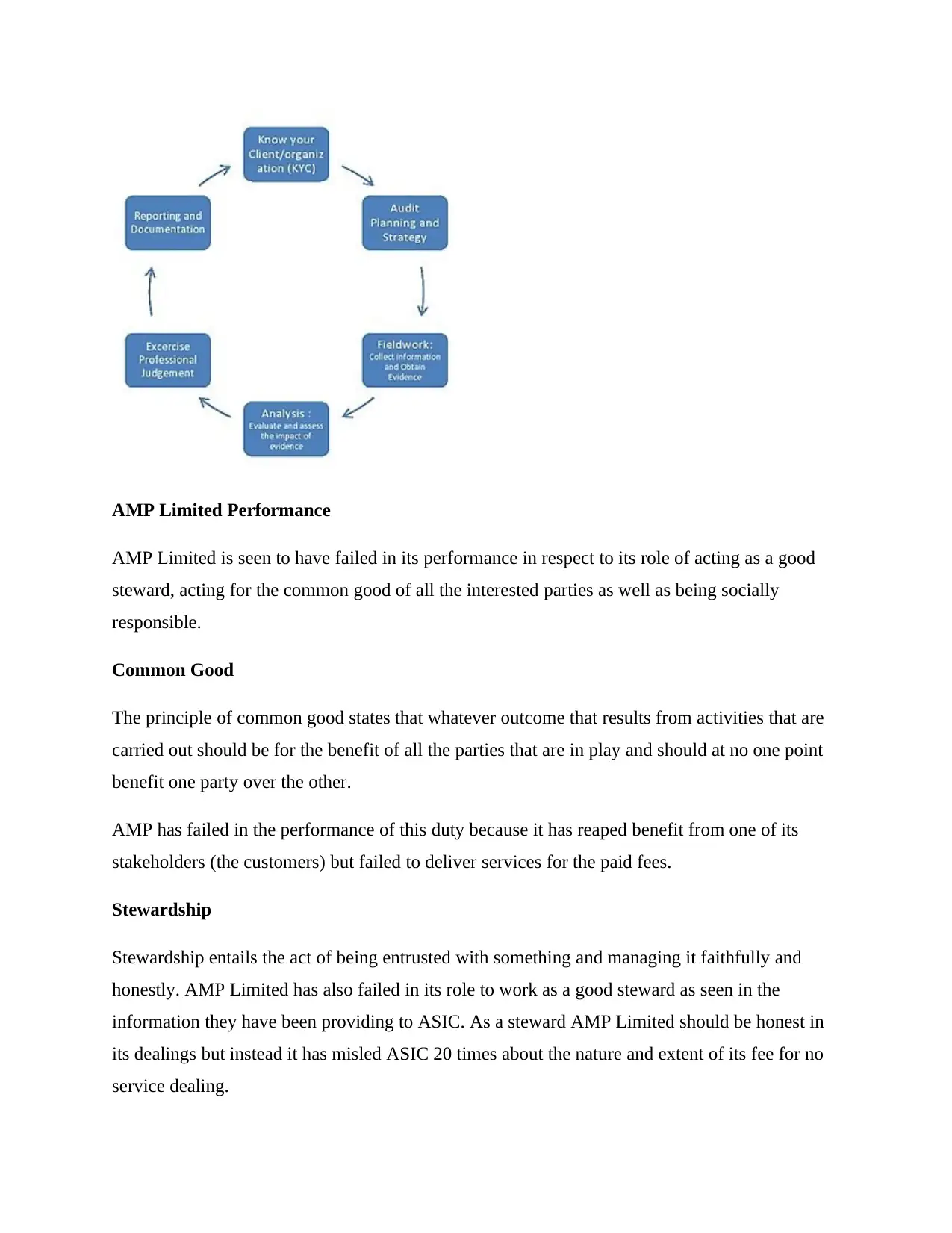

This report examines the financial misconduct perpetrated by AMP Limited, focusing on its failure to act as a good steward, uphold common good principles, and maintain social responsibility. The company charged clients fees for no service, leading to significant financial losses and reputational damage. The report assesses the ethical conduct of AMP Limited's accountants in relation to APES110 and APES230, highlighting violations of ethical codes. It explores the purpose of auditing in exposing misconduct and promoting socially responsible outcomes. The analysis covers the company's performance, ethical breaches, and the role of auditing in uncovering these issues. The report concludes with recommendations for improving internal controls and regaining public trust. References to various academic sources support the findings and analysis of AMP Limited's failures.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.