Comprehensive Analysis: Corporate Accounting & Financial Reporting

VerifiedAdded on 2023/04/23

|8

|1496

|214

Report

AI Summary

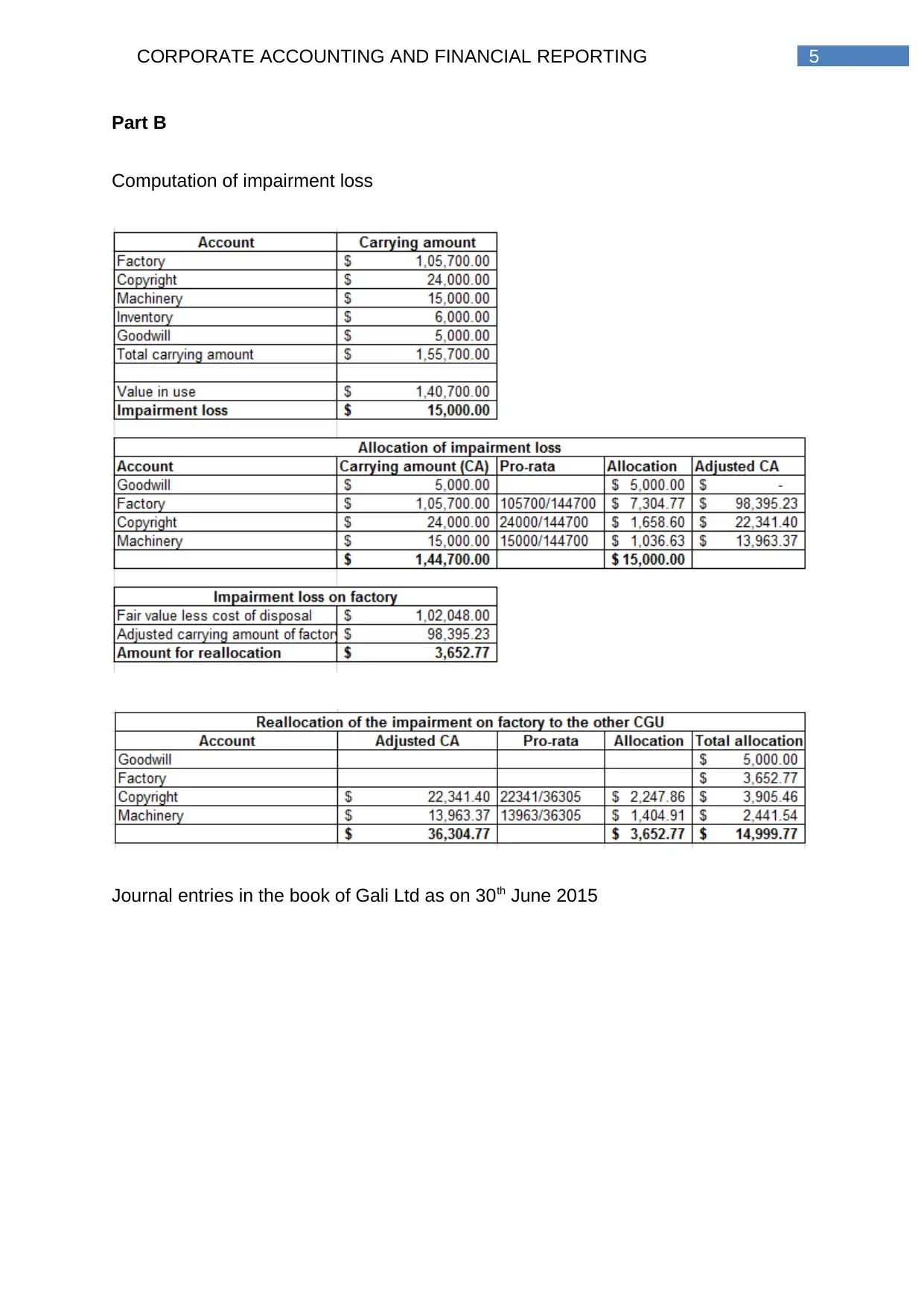

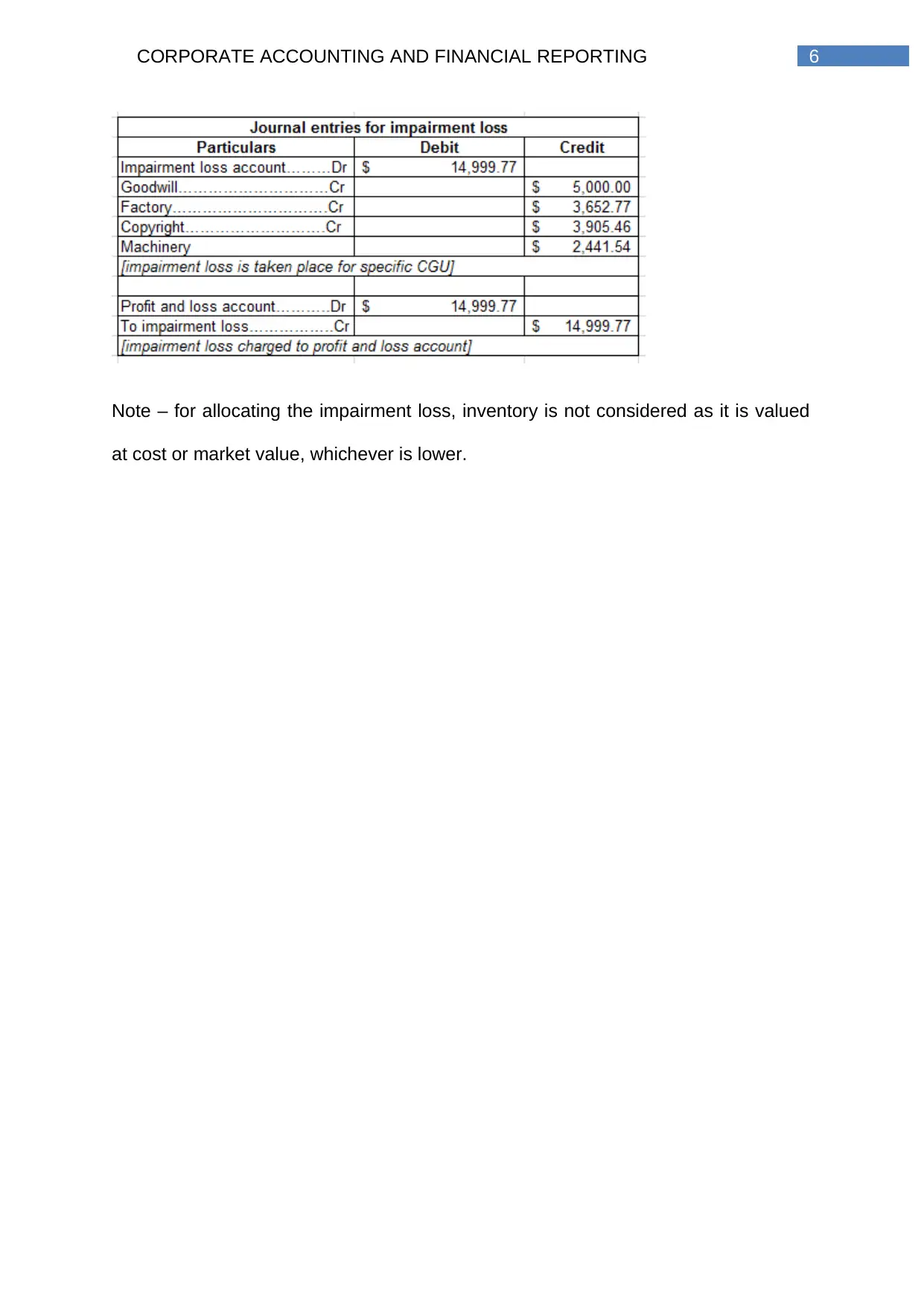

This report provides a detailed analysis of corporate accounting and financial reporting, focusing on the computation of recoverable amounts, value in use (VIU), and fair value less cost of disposal. It explains how to determine impairment loss when the carrying amount of an asset exceeds its recoverable amount, referencing AASB 136 standards. The report outlines the steps for measuring VIU, including projecting future cash flows and applying appropriate discount rates. It also discusses how to measure fair value less cost of disposal, considering factors like binding agreements and active market prices. Furthermore, the report includes a practical application with journal entries for Gali Ltd, demonstrating the allocation of impairment loss across various assets, excluding inventory. The analysis is supported by academic references, providing a comprehensive overview of the principles and practices involved in corporate accounting and financial reporting.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.