In-Depth Financial Analysis of Delta Air Lines Company

VerifiedAdded on 2023/06/15

|13

|3107

|207

Report

AI Summary

This report provides a comprehensive financial analysis of Delta Air Lines, examining its history, business strategy, and financial performance from 2014 to 2016. It assesses short-term liquidity, long-term solvency, asset efficiency, profitability, and cash flow, highlighting key financial ratios and trends. The analysis includes an evaluation of the firm's earnings quality and stock price per share, utilizing technical analysis to predict future price movements. Ultimately, the report offers recommendations based on the financial viability of Delta Air Lines, suggesting potential investment opportunities for investors. Desklib provides access to similar solved assignments for students seeking study resources.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Authors Note:

Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

1

Table of Contents

a. Analysis overview of the company:.......................................................................................2

i. Summary of firm’s history:.....................................................................................................2

ii. Firms main competition and customers:................................................................................2

iii. Providing relevant information on management and management compensation:..............2

b. Depicting summary of the firm’s business strategy:..............................................................3

c. Financial analysis of the company:........................................................................................3

i. Analysis of the short term liquidity and longer term solvency:..............................................3

ii. Analysis of asset efficiency:..................................................................................................4

iii. Analysis of profitability:.......................................................................................................5

iv. Analysis of cash flow:...........................................................................................................6

d. Accounting analysis of the firm’s earnings quality:..............................................................6

e. An evaluation of firm’s stock price per share:.......................................................................7

f. Depicting relevant recommendations and conclusion:...........................................................9

Reference and Bibliography:....................................................................................................10

1

Table of Contents

a. Analysis overview of the company:.......................................................................................2

i. Summary of firm’s history:.....................................................................................................2

ii. Firms main competition and customers:................................................................................2

iii. Providing relevant information on management and management compensation:..............2

b. Depicting summary of the firm’s business strategy:..............................................................3

c. Financial analysis of the company:........................................................................................3

i. Analysis of the short term liquidity and longer term solvency:..............................................3

ii. Analysis of asset efficiency:..................................................................................................4

iii. Analysis of profitability:.......................................................................................................5

iv. Analysis of cash flow:...........................................................................................................6

d. Accounting analysis of the firm’s earnings quality:..............................................................6

e. An evaluation of firm’s stock price per share:.......................................................................7

f. Depicting relevant recommendations and conclusion:...........................................................9

Reference and Bibliography:....................................................................................................10

ACCOUNTING

2

a. Analysis overview of the company:

i. Summary of firm’s history:

Delta Air Lines is mainly identified to be one of the major American airlines, whose

overall net income amount to $4.373 billion in 2016. The company has a large history, where

it started the operations of crop dusting during 1925. Moreover, from 1928 the overall Delta

Air Lines mainly started its flight operations in 1928, where the first operations began in

1929 with the flights between Dallas, Texas and Jackson. The company during 1980 started

the pacific and internal flight operations (Ir.delta.com, 2017). However, during 2007 the

company faced bankruptcy but the merger with Northwest Airlines allowed Delta Airlines to

become world’s largest Airline. Lastly, the combining of website and reservation system

mainly retired the Northwest Airlines name and brand from Delta Air Lines.

ii. Firms main competition and customers:

The competitors of Delta Air Lines, are Southwest Airlines Co, American Airlines

Group Inc and United Continental Holdings Inc. The competitors of the organisation can be

identified from the Market Cap that is enjoyed by the companies. The overall competitors of

the company have mainly increased the intense competition in the market, which intensifies

the competition level in the airline industry. The main target customer of Delta Air Lines

ranges from first class facilities to basic economy, where high end customer and as well as

low income earning customers are targeted by the company (Ir.delta.com, 2017).

iii. Providing relevant information on management and management compensation:

The top management of Delta Air Line is Ed Bastian (Chief Executive Officer), Glen

Hauenstein (President), Gil West (S.E.V.P. and Chief Operating Officer), and Paul Jacobson

2

a. Analysis overview of the company:

i. Summary of firm’s history:

Delta Air Lines is mainly identified to be one of the major American airlines, whose

overall net income amount to $4.373 billion in 2016. The company has a large history, where

it started the operations of crop dusting during 1925. Moreover, from 1928 the overall Delta

Air Lines mainly started its flight operations in 1928, where the first operations began in

1929 with the flights between Dallas, Texas and Jackson. The company during 1980 started

the pacific and internal flight operations (Ir.delta.com, 2017). However, during 2007 the

company faced bankruptcy but the merger with Northwest Airlines allowed Delta Airlines to

become world’s largest Airline. Lastly, the combining of website and reservation system

mainly retired the Northwest Airlines name and brand from Delta Air Lines.

ii. Firms main competition and customers:

The competitors of Delta Air Lines, are Southwest Airlines Co, American Airlines

Group Inc and United Continental Holdings Inc. The competitors of the organisation can be

identified from the Market Cap that is enjoyed by the companies. The overall competitors of

the company have mainly increased the intense competition in the market, which intensifies

the competition level in the airline industry. The main target customer of Delta Air Lines

ranges from first class facilities to basic economy, where high end customer and as well as

low income earning customers are targeted by the company (Ir.delta.com, 2017).

iii. Providing relevant information on management and management compensation:

The top management of Delta Air Line is Ed Bastian (Chief Executive Officer), Glen

Hauenstein (President), Gil West (S.E.V.P. and Chief Operating Officer), and Paul Jacobson

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING

3

(E.V.P. and Chief Financial Officer). These identified top management personnel mainly

conduct the relevant operations for improving profitability of the organization. The

management information mainly helps in identifying the relevant income, which could be

generated from the operations (Ir.delta.com, 2017).

b. Depicting summary of the firm’s business strategy:

From the overall evaluation of company’s performance, the relevant business strategy

of Delta Air Line could be identified. This could eventually allow the company to generate

the required level of profitability and attain sustainable growth. The main business strategy of

Delta Air Lines is to attract more customer for their Airbus, which helps in generating higher

revenue from investment (Ir.delta.com, 2017). In addition, merger is also one of the major

activities and strategy of Delta Air Lines, which has allowed the organisation to increase its

activities and become one of the largest Airlines in United States.

c. Financial analysis of the company:

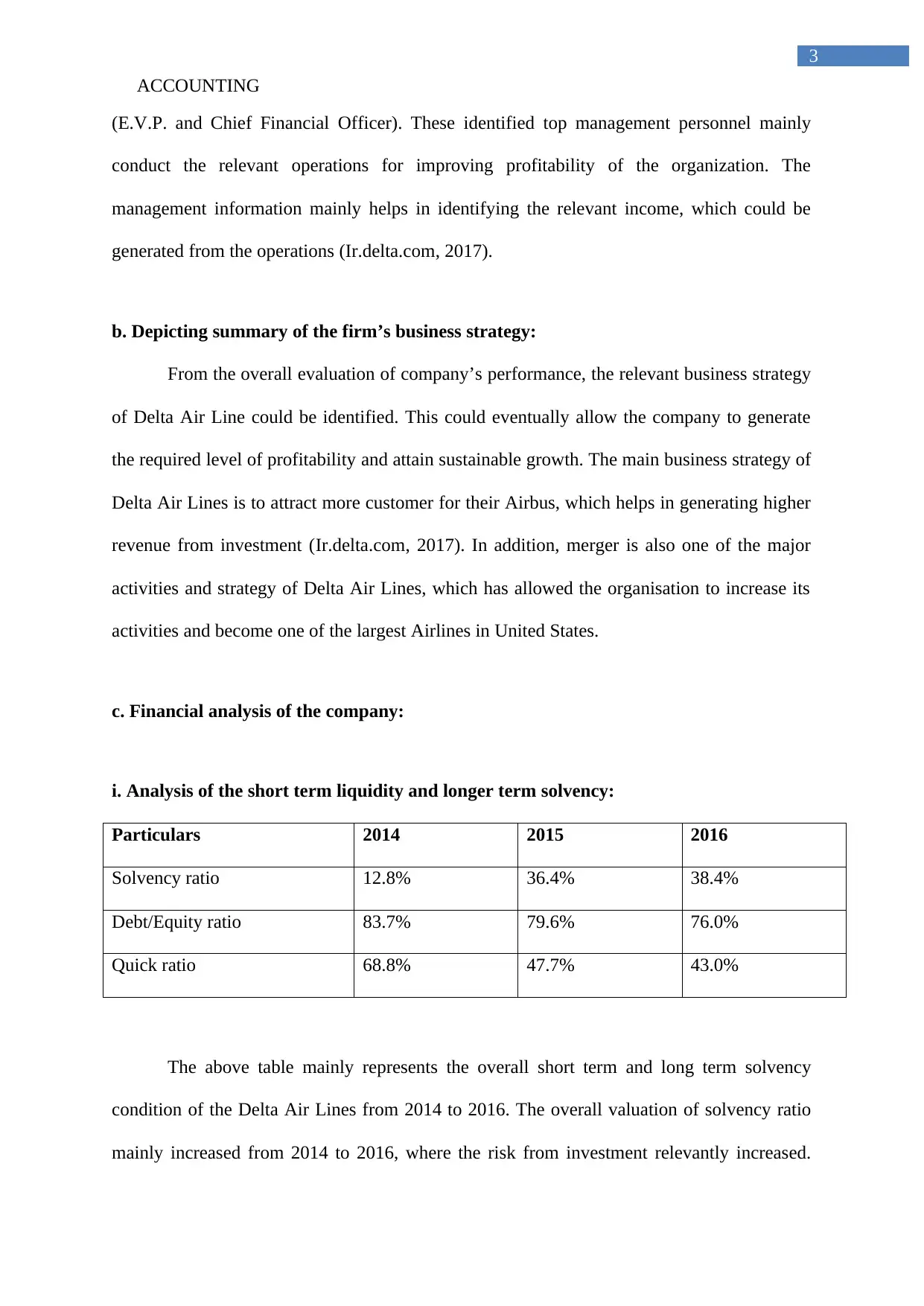

i. Analysis of the short term liquidity and longer term solvency:

Particulars 2014 2015 2016

Solvency ratio 12.8% 36.4% 38.4%

Debt/Equity ratio 83.7% 79.6% 76.0%

Quick ratio 68.8% 47.7% 43.0%

The above table mainly represents the overall short term and long term solvency

condition of the Delta Air Lines from 2014 to 2016. The overall valuation of solvency ratio

mainly increased from 2014 to 2016, where the risk from investment relevantly increased.

3

(E.V.P. and Chief Financial Officer). These identified top management personnel mainly

conduct the relevant operations for improving profitability of the organization. The

management information mainly helps in identifying the relevant income, which could be

generated from the operations (Ir.delta.com, 2017).

b. Depicting summary of the firm’s business strategy:

From the overall evaluation of company’s performance, the relevant business strategy

of Delta Air Line could be identified. This could eventually allow the company to generate

the required level of profitability and attain sustainable growth. The main business strategy of

Delta Air Lines is to attract more customer for their Airbus, which helps in generating higher

revenue from investment (Ir.delta.com, 2017). In addition, merger is also one of the major

activities and strategy of Delta Air Lines, which has allowed the organisation to increase its

activities and become one of the largest Airlines in United States.

c. Financial analysis of the company:

i. Analysis of the short term liquidity and longer term solvency:

Particulars 2014 2015 2016

Solvency ratio 12.8% 36.4% 38.4%

Debt/Equity ratio 83.7% 79.6% 76.0%

Quick ratio 68.8% 47.7% 43.0%

The above table mainly represents the overall short term and long term solvency

condition of the Delta Air Lines from 2014 to 2016. The overall valuation of solvency ratio

mainly increased from 2014 to 2016, where the risk from investment relevantly increased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

4

This problem in solvency condition mainly increased over time, which raised the problems in

company’s financial attribute. The relevant debt/equity ratio decline rapidly indicating

relevant reduction in debt accumulation, which is been conducted by the company. The

relevant evaluation of debt to equity ratio and solvency ratio mainly helps in understanding

the overall long term and short term solvency condition of the company. Abdul-Baki,

Uthman & Sannia (2014) mentioned that with adequate ratio investor are able to detect the

financial condition of the company, where relevant investments could be conducted.

The overall liquidity conduction of the company is also evaluated with the help of

quick ratio, where ability of the company to support short term obligations is greatly reduced.

The overall financial ability of the company mainly declined, where its quick ratio declined

from 0.69 in 2014 to 0.43 in 2016. This mainly indicates that the company’s ability to support

short term obligations has relevantly declined in 2016. Hence, the Delta Air Line is not able

to support the relevant financial obligations and conduct relevant operations. Baños-

Caballero, García-Teruel, & Martínez-Solano (2014) mentioned that the use of liquidity ratio

could eventually allow the investor to detect viability of the current assets. Therefore, the

problems in the overall financial stability of the organisation could be detected from the

valuation of the financial condition.

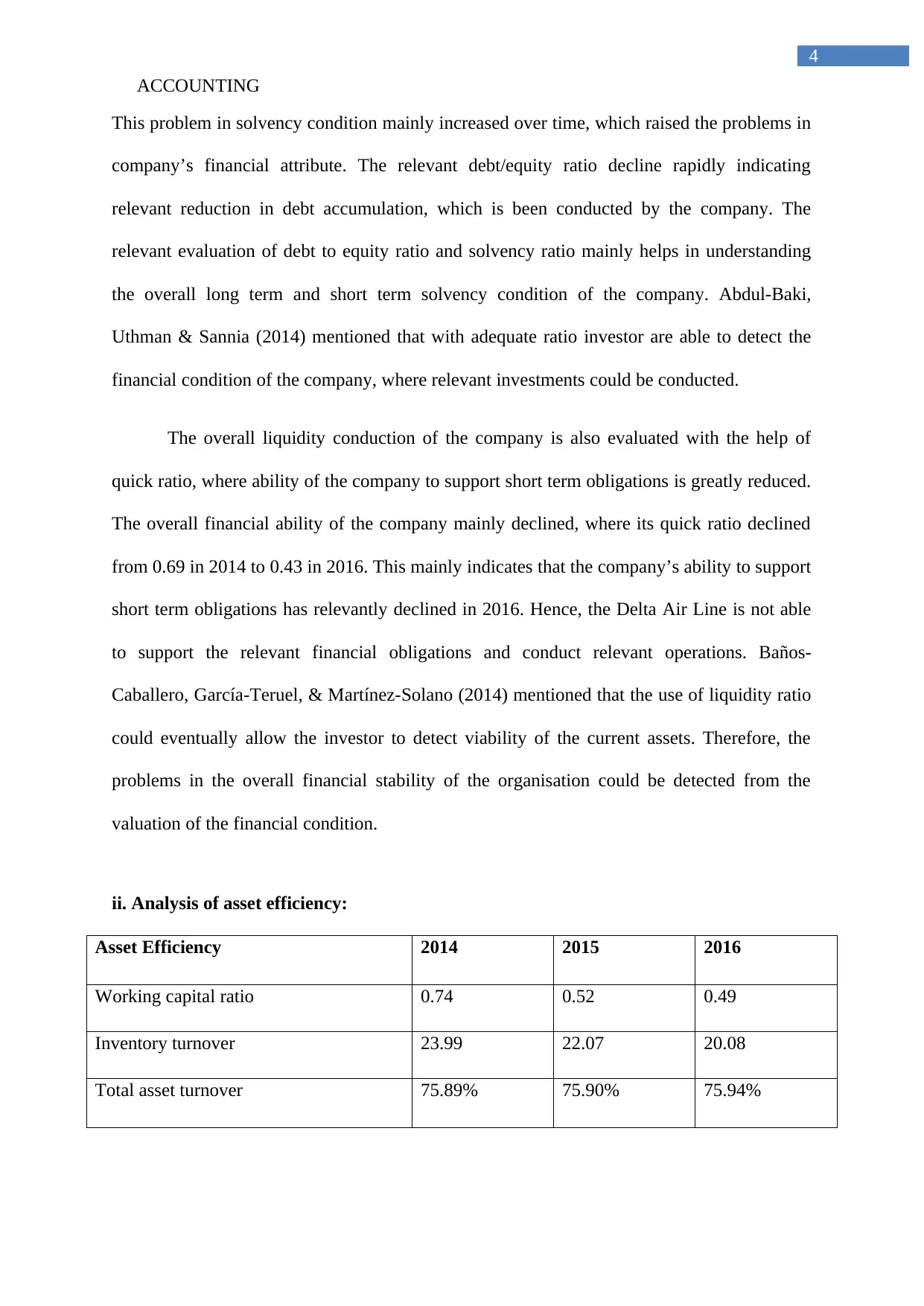

ii. Analysis of asset efficiency:

Asset Efficiency 2014 2015 2016

Working capital ratio 0.74 0.52 0.49

Inventory turnover 23.99 22.07 20.08

Total asset turnover 75.89% 75.90% 75.94%

4

This problem in solvency condition mainly increased over time, which raised the problems in

company’s financial attribute. The relevant debt/equity ratio decline rapidly indicating

relevant reduction in debt accumulation, which is been conducted by the company. The

relevant evaluation of debt to equity ratio and solvency ratio mainly helps in understanding

the overall long term and short term solvency condition of the company. Abdul-Baki,

Uthman & Sannia (2014) mentioned that with adequate ratio investor are able to detect the

financial condition of the company, where relevant investments could be conducted.

The overall liquidity conduction of the company is also evaluated with the help of

quick ratio, where ability of the company to support short term obligations is greatly reduced.

The overall financial ability of the company mainly declined, where its quick ratio declined

from 0.69 in 2014 to 0.43 in 2016. This mainly indicates that the company’s ability to support

short term obligations has relevantly declined in 2016. Hence, the Delta Air Line is not able

to support the relevant financial obligations and conduct relevant operations. Baños-

Caballero, García-Teruel, & Martínez-Solano (2014) mentioned that the use of liquidity ratio

could eventually allow the investor to detect viability of the current assets. Therefore, the

problems in the overall financial stability of the organisation could be detected from the

valuation of the financial condition.

ii. Analysis of asset efficiency:

Asset Efficiency 2014 2015 2016

Working capital ratio 0.74 0.52 0.49

Inventory turnover 23.99 22.07 20.08

Total asset turnover 75.89% 75.90% 75.94%

ACCOUNTING

5

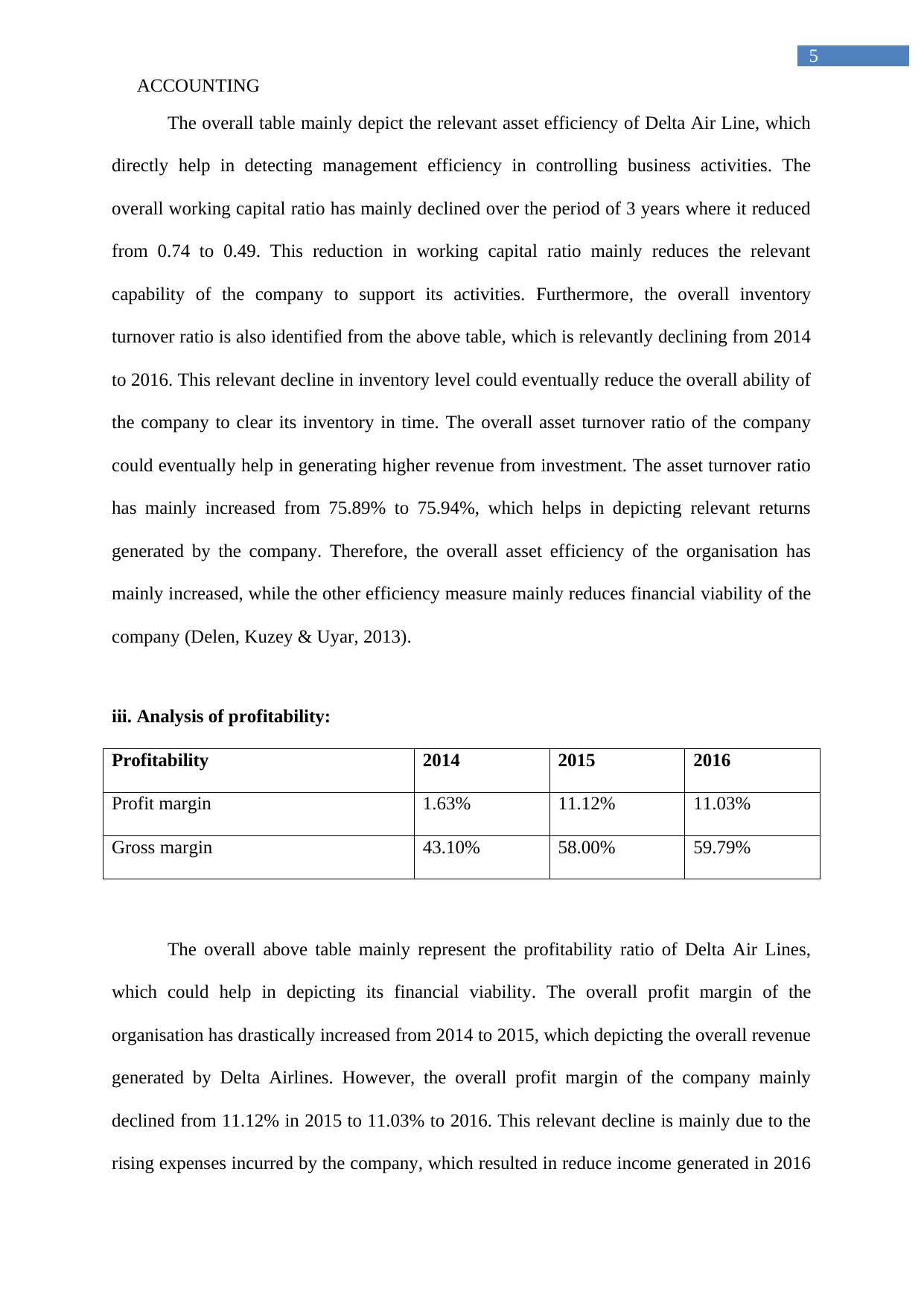

The overall table mainly depict the relevant asset efficiency of Delta Air Line, which

directly help in detecting management efficiency in controlling business activities. The

overall working capital ratio has mainly declined over the period of 3 years where it reduced

from 0.74 to 0.49. This reduction in working capital ratio mainly reduces the relevant

capability of the company to support its activities. Furthermore, the overall inventory

turnover ratio is also identified from the above table, which is relevantly declining from 2014

to 2016. This relevant decline in inventory level could eventually reduce the overall ability of

the company to clear its inventory in time. The overall asset turnover ratio of the company

could eventually help in generating higher revenue from investment. The asset turnover ratio

has mainly increased from 75.89% to 75.94%, which helps in depicting relevant returns

generated by the company. Therefore, the overall asset efficiency of the organisation has

mainly increased, while the other efficiency measure mainly reduces financial viability of the

company (Delen, Kuzey & Uyar, 2013).

iii. Analysis of profitability:

Profitability 2014 2015 2016

Profit margin 1.63% 11.12% 11.03%

Gross margin 43.10% 58.00% 59.79%

The overall above table mainly represent the profitability ratio of Delta Air Lines,

which could help in depicting its financial viability. The overall profit margin of the

organisation has drastically increased from 2014 to 2015, which depicting the overall revenue

generated by Delta Airlines. However, the overall profit margin of the company mainly

declined from 11.12% in 2015 to 11.03% to 2016. This relevant decline is mainly due to the

rising expenses incurred by the company, which resulted in reduce income generated in 2016

5

The overall table mainly depict the relevant asset efficiency of Delta Air Line, which

directly help in detecting management efficiency in controlling business activities. The

overall working capital ratio has mainly declined over the period of 3 years where it reduced

from 0.74 to 0.49. This reduction in working capital ratio mainly reduces the relevant

capability of the company to support its activities. Furthermore, the overall inventory

turnover ratio is also identified from the above table, which is relevantly declining from 2014

to 2016. This relevant decline in inventory level could eventually reduce the overall ability of

the company to clear its inventory in time. The overall asset turnover ratio of the company

could eventually help in generating higher revenue from investment. The asset turnover ratio

has mainly increased from 75.89% to 75.94%, which helps in depicting relevant returns

generated by the company. Therefore, the overall asset efficiency of the organisation has

mainly increased, while the other efficiency measure mainly reduces financial viability of the

company (Delen, Kuzey & Uyar, 2013).

iii. Analysis of profitability:

Profitability 2014 2015 2016

Profit margin 1.63% 11.12% 11.03%

Gross margin 43.10% 58.00% 59.79%

The overall above table mainly represent the profitability ratio of Delta Air Lines,

which could help in depicting its financial viability. The overall profit margin of the

organisation has drastically increased from 2014 to 2015, which depicting the overall revenue

generated by Delta Airlines. However, the overall profit margin of the company mainly

declined from 11.12% in 2015 to 11.03% to 2016. This relevant decline is mainly due to the

rising expenses incurred by the company, which resulted in reduce income generated in 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING

6

as compared to 2015. The overall gross profit margin of the company has mainly inclined

adequately from 2014 to 2016, which could help in depicting its revenue generation capacity.

However, from the overall evaluation it could be seen that net profit margin did not increase

adequately, as the gross profit margin, which relatively depicts the increased administrative

expense incurred by the company. In this context, Duchin & Sosyura (2014) mentioned that

investor with the help of profitability ratio is able to detect trend on revenue generation

capacity of the company. This detection of the revenue and expense trend mainly allow the

investors to detect financial viability of the investment.

iv. Analysis of cash flow:

Cash flow analysis 2014 2015 2016

Operating cash flow 0.13 0.45 0.46

The overall operating cash flow ratio is mainly identified from the above table, which

is relatively seen to be rising in nature. This relevant increment in the operating cash flow of

the company is mainly high, as the overall revenue increased exponentially. From the

evaluation it could be identified that operating cash flow increased exponentially from 0.13 in

2014 to 0.45 in 2015. However, the increment in operating cash flow from 2015 to 2016 was

nominal at 0.01. This relevantly indicates that the company’s overall expenses increased in

2016, which relevantly reduce the overall operations cash flow of the organisation (Erdogan,

2014).

d. Accounting analysis of the firm’s earnings quality:

The overall firm’s earnings quality mainly inclined from 2014 to 2016, which

relatively depicts the overall management control for generating higher revenue from

6

as compared to 2015. The overall gross profit margin of the company has mainly inclined

adequately from 2014 to 2016, which could help in depicting its revenue generation capacity.

However, from the overall evaluation it could be seen that net profit margin did not increase

adequately, as the gross profit margin, which relatively depicts the increased administrative

expense incurred by the company. In this context, Duchin & Sosyura (2014) mentioned that

investor with the help of profitability ratio is able to detect trend on revenue generation

capacity of the company. This detection of the revenue and expense trend mainly allow the

investors to detect financial viability of the investment.

iv. Analysis of cash flow:

Cash flow analysis 2014 2015 2016

Operating cash flow 0.13 0.45 0.46

The overall operating cash flow ratio is mainly identified from the above table, which

is relatively seen to be rising in nature. This relevant increment in the operating cash flow of

the company is mainly high, as the overall revenue increased exponentially. From the

evaluation it could be identified that operating cash flow increased exponentially from 0.13 in

2014 to 0.45 in 2015. However, the increment in operating cash flow from 2015 to 2016 was

nominal at 0.01. This relevantly indicates that the company’s overall expenses increased in

2016, which relevantly reduce the overall operations cash flow of the organisation (Erdogan,

2014).

d. Accounting analysis of the firm’s earnings quality:

The overall firm’s earnings quality mainly inclined from 2014 to 2016, which

relatively depicts the overall management control for generating higher revenue from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

7

investment. The company after completion of 2014 mainly ended the expenses incurred from

the operations, which in turn help in generating higher earnings from operation. In addition,

the relevant increment in total revenue earned by the organisation and the overall cost of sales

could be evaluated from the annual report. The overall reduction in cost of revenue could be

conducted, which might help in increasing the overall gross profit of the organisation. This

relevant increment in the overall revenue mainly indicates the profits that is generated by the

organisation by conducting low expenses. The restructuration of merger and acquisition

expense after 2014 mainly declined to nil in 2016. This relevantly helped in improving

profitability of the company, which in turn generate higher revenue from investment. The

relevant decline in cost of capital is mainly conducted by the management for increasing the

profits of the organisation. Grinblatt & Titman (2016) mentioned that the overall valuation of

earnings per share could help ion depicting the relevant growth, which might be attained by

the company in future.

e. An evaluation of firm’s stock price per share:

Figure 1: Depicting the Share price of the company

7

investment. The company after completion of 2014 mainly ended the expenses incurred from

the operations, which in turn help in generating higher earnings from operation. In addition,

the relevant increment in total revenue earned by the organisation and the overall cost of sales

could be evaluated from the annual report. The overall reduction in cost of revenue could be

conducted, which might help in increasing the overall gross profit of the organisation. This

relevant increment in the overall revenue mainly indicates the profits that is generated by the

organisation by conducting low expenses. The restructuration of merger and acquisition

expense after 2014 mainly declined to nil in 2016. This relevantly helped in improving

profitability of the company, which in turn generate higher revenue from investment. The

relevant decline in cost of capital is mainly conducted by the management for increasing the

profits of the organisation. Grinblatt & Titman (2016) mentioned that the overall valuation of

earnings per share could help ion depicting the relevant growth, which might be attained by

the company in future.

e. An evaluation of firm’s stock price per share:

Figure 1: Depicting the Share price of the company

ACCOUNTING

8

(Source: Us.finance.yahoo.com, 2017)

From the overall evaluation of the above figure relevant share price of the stock can

be denitrified, which is relatively seen to be in an uptrend. The long term trend of the

organisation is relatively in uptrend, while the short term trend is relatively in consolidation.

This overall evaluation of the share price mainly indicates that share price valuation of the

company is currently declining. The levels of 51.40 is mainly identified to be the relevant

support level for the share price, which could directly increase over time. Le & Viviani

(2017) mentioned that with the help of share price valuation investors are mainly able to

detect the price range and trend, which could help in making adequate investment decisions.

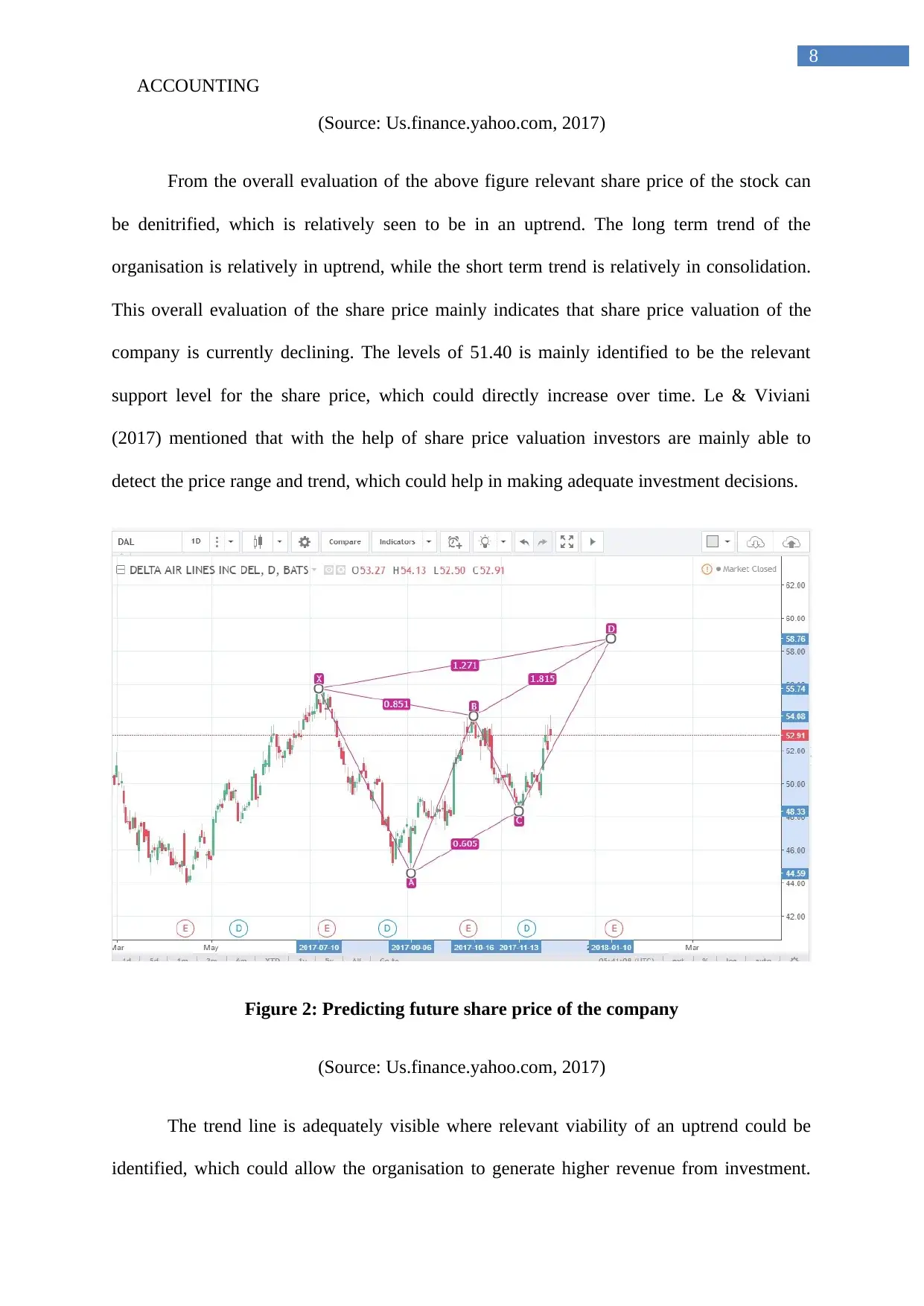

Figure 2: Predicting future share price of the company

(Source: Us.finance.yahoo.com, 2017)

The trend line is adequately visible where relevant viability of an uptrend could be

identified, which could allow the organisation to generate higher revenue from investment.

8

(Source: Us.finance.yahoo.com, 2017)

From the overall evaluation of the above figure relevant share price of the stock can

be denitrified, which is relatively seen to be in an uptrend. The long term trend of the

organisation is relatively in uptrend, while the short term trend is relatively in consolidation.

This overall evaluation of the share price mainly indicates that share price valuation of the

company is currently declining. The levels of 51.40 is mainly identified to be the relevant

support level for the share price, which could directly increase over time. Le & Viviani

(2017) mentioned that with the help of share price valuation investors are mainly able to

detect the price range and trend, which could help in making adequate investment decisions.

Figure 2: Predicting future share price of the company

(Source: Us.finance.yahoo.com, 2017)

The trend line is adequately visible where relevant viability of an uptrend could be

identified, which could allow the organisation to generate higher revenue from investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING

9

Hence, the use of technical analysis could mainly help in identifying the relevant share price

of the company, which could help in making adequate investment decisions. The above

figure mainly represents the relevant future price predictions that could estimate the relevant

price of current Delta shares. The levels of 48.33 is mainly identified to be the stop loss with

the relevant target of 58.76 in future. This move could mainly help in improving returns that

will be generated from investment. Leary & Roberts (2014) argued that technical analysis

valuation is only viable if the investors are able to accurately estimate the price trend and

generate higher revenue from investment. Therefore, with the help technical analysis relevant

price level of Delta Air Line could be identified.

f. Depicting relevant recommendations and conclusion:

The overall evaluation of the assignment mainly helps in depicting the current

financial performance of Delta Air Lines company. This relevant valuation of the company

could help in depicting the investment option, which might help in generating higher revenue

from investment. The evaluation of all relevant issues mainly help in identifying financial

viability of Delta Airlines, which could help in generating higher returns from investment for

the investors. Technical analysis conducted in the above section also depict the relevant

financial Trend of the organization, which might provide higher returns from investment in

future. The evaluation of earnings per share also depict relevant growth, which could be

obtained by the organization in near future. Hence, it advisable for investors to relatively

invest in Delta Airlines, as it might help in generating higher revenue for them in near future

and create wealth. Therefore, from the overall evaluation financial viability of delta Airlines

could be identified, which might help investors in making adequate investment decisions.

9

Hence, the use of technical analysis could mainly help in identifying the relevant share price

of the company, which could help in making adequate investment decisions. The above

figure mainly represents the relevant future price predictions that could estimate the relevant

price of current Delta shares. The levels of 48.33 is mainly identified to be the stop loss with

the relevant target of 58.76 in future. This move could mainly help in improving returns that

will be generated from investment. Leary & Roberts (2014) argued that technical analysis

valuation is only viable if the investors are able to accurately estimate the price trend and

generate higher revenue from investment. Therefore, with the help technical analysis relevant

price level of Delta Air Line could be identified.

f. Depicting relevant recommendations and conclusion:

The overall evaluation of the assignment mainly helps in depicting the current

financial performance of Delta Air Lines company. This relevant valuation of the company

could help in depicting the investment option, which might help in generating higher revenue

from investment. The evaluation of all relevant issues mainly help in identifying financial

viability of Delta Airlines, which could help in generating higher returns from investment for

the investors. Technical analysis conducted in the above section also depict the relevant

financial Trend of the organization, which might provide higher returns from investment in

future. The evaluation of earnings per share also depict relevant growth, which could be

obtained by the organization in near future. Hence, it advisable for investors to relatively

invest in Delta Airlines, as it might help in generating higher revenue for them in near future

and create wealth. Therefore, from the overall evaluation financial viability of delta Airlines

could be identified, which might help investors in making adequate investment decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

10

Reference and Bibliography:

Abdul-Baki, Z., Uthman, A. B., & Sannia, M. (2014). Financial ratios as performance

measure: A comparison of IFRS and Nigerian GAAP. Accounting and Management

Information Systems, 13(1), 82.

Baños-Caballero, S., García-Teruel, P. J., & Martínez-Solano, P. (2014). Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), 332-338.

Carlino, L., Coppens, F., González, J., Ortega, M., Pérez-Duarte, S., Rubbrecht, I., & Vennix,

S. (2017). Decomposition techniques for financial ratios of European non-financial

listed groups (No. 21). European Central Bank.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Duchin, R., & Sosyura, D. (2014). Safer ratios, riskier portfolios: Banks׳ response to

government aid. Journal of Financial Economics, 113(1), 1-28.

Erdogan, A. I. (2014). Applying factor analysis on the financial ratios of Turkey's top 500

industrial enterprises.

Grinblatt, M., & Titman, S. (2016). Financial markets & corporate strategy.

Ir.delta.com. (2017). Ir.delta.com. Retrieved 5 December 2017, from http://ir.delta.com/

Le, H. H., & Viviani, J. L. (2017). Predicting bank failure: An improvement by implementing

machine learning approach on classical financial ratios. Research in International

Business and Finance.

10

Reference and Bibliography:

Abdul-Baki, Z., Uthman, A. B., & Sannia, M. (2014). Financial ratios as performance

measure: A comparison of IFRS and Nigerian GAAP. Accounting and Management

Information Systems, 13(1), 82.

Baños-Caballero, S., García-Teruel, P. J., & Martínez-Solano, P. (2014). Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), 332-338.

Carlino, L., Coppens, F., González, J., Ortega, M., Pérez-Duarte, S., Rubbrecht, I., & Vennix,

S. (2017). Decomposition techniques for financial ratios of European non-financial

listed groups (No. 21). European Central Bank.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Duchin, R., & Sosyura, D. (2014). Safer ratios, riskier portfolios: Banks׳ response to

government aid. Journal of Financial Economics, 113(1), 1-28.

Erdogan, A. I. (2014). Applying factor analysis on the financial ratios of Turkey's top 500

industrial enterprises.

Grinblatt, M., & Titman, S. (2016). Financial markets & corporate strategy.

Ir.delta.com. (2017). Ir.delta.com. Retrieved 5 December 2017, from http://ir.delta.com/

Le, H. H., & Viviani, J. L. (2017). Predicting bank failure: An improvement by implementing

machine learning approach on classical financial ratios. Research in International

Business and Finance.

ACCOUNTING

11

Leary, M. T., & Roberts, M. R. (2014). Do peer firms affect corporate financial policy?. The

Journal of Finance, 69(1), 139-178.

Najjar, N. J. (2013). Can Financial Ratios Reliably Measure the Performance of Banks in

Bahrain?. International Journal of Economics and Finance, 5(3), 152.

Nezlobin, A., Rajan, M. V., & Reichelstein, S. (2014). Capital Investments and Financial

Ratios (No. 3052).

Ongore, V. O., & Kusa, G. B. (2013). Determinants of financial performance of commercial

banks in Kenya. International Journal of Economics and Financial Issues, 3(1), 237.

Robin, T., Canquin, C., Uy, D., & Villagracia, A. R. (2015). Developing a Stock Price Model

Using Investment Valuation Ratios for the Financial Industry Of the Philippine Stock

Market.

Robin, T., Canquin, C., Uy, D., & Villagracia, A. R. (2015). Developing a Stock Price Model

Using Investment Valuation Ratios for the Financial Industry Of the Philippine Stock

Market.

Shaikh, A. S., Kashif, M., & Shaikh, S. (2017). MEASURING STOCK MARKET

PREDICTABILITY WITH IMPLICATIONS OF FINANCIAL RATIOS: AN

EMPIRICAL INVESTIGATION OF PAKISTAN STOCK MARKET. Journal of

Business Strategies, 11(1), 41.

Shaverdi, M., Ramezani, I., Tahmasebi, R., & Rostamy, A. A. A. (2016). Combining fuzzy

AHP and fuzzy TOPSIS with financial ratios to design a novel performance

evaluation model. International Journal of Fuzzy Systems, 18(2), 248-262.

11

Leary, M. T., & Roberts, M. R. (2014). Do peer firms affect corporate financial policy?. The

Journal of Finance, 69(1), 139-178.

Najjar, N. J. (2013). Can Financial Ratios Reliably Measure the Performance of Banks in

Bahrain?. International Journal of Economics and Finance, 5(3), 152.

Nezlobin, A., Rajan, M. V., & Reichelstein, S. (2014). Capital Investments and Financial

Ratios (No. 3052).

Ongore, V. O., & Kusa, G. B. (2013). Determinants of financial performance of commercial

banks in Kenya. International Journal of Economics and Financial Issues, 3(1), 237.

Robin, T., Canquin, C., Uy, D., & Villagracia, A. R. (2015). Developing a Stock Price Model

Using Investment Valuation Ratios for the Financial Industry Of the Philippine Stock

Market.

Robin, T., Canquin, C., Uy, D., & Villagracia, A. R. (2015). Developing a Stock Price Model

Using Investment Valuation Ratios for the Financial Industry Of the Philippine Stock

Market.

Shaikh, A. S., Kashif, M., & Shaikh, S. (2017). MEASURING STOCK MARKET

PREDICTABILITY WITH IMPLICATIONS OF FINANCIAL RATIOS: AN

EMPIRICAL INVESTIGATION OF PAKISTAN STOCK MARKET. Journal of

Business Strategies, 11(1), 41.

Shaverdi, M., Ramezani, I., Tahmasebi, R., & Rostamy, A. A. A. (2016). Combining fuzzy

AHP and fuzzy TOPSIS with financial ratios to design a novel performance

evaluation model. International Journal of Fuzzy Systems, 18(2), 248-262.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.