ACCT6006: Auditing and Financial Analysis of Dick Smith's Collapse

VerifiedAdded on 2021/11/10

|11

|3213

|30

Report

AI Summary

This report provides a comprehensive analysis of the Dick Smith collapse, examining the various factors that contributed to its failure. It begins with a brief history of the company and identifies the primary reasons for its downfall, including excessive inventory buildup and accounting irregularities. The report then delves into the accusations against the directors for breaching Australian Accounting Standards, particularly focusing on the use of fraudulent accounting methods like 'Real Activities Management.' It further explores the signs that auditors should have considered when identifying the going concern problem and analyzes the 2014/15 annual report to provide evidence that the company might not be a going concern. The report also discusses the reasons behind Deloitte's unmodified audit opinion and the auditor's legal liability in this context. The analysis covers key issues like inventory valuation, cash flow problems, and the role of management in the company's failure. The report concludes by highlighting the importance of ethical accounting practices and the responsibilities of auditors in ensuring the accuracy and reliability of financial statements.

1

ACCT6006 Auditing

ACCT6006 Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Introduction......................................................................................................................................3

Part 1: Brief History of Dick Smith and reasons that causes its failure..........................................3

Part 2: Accusation against the Directors of Dick Smith for Breach of Australian Accounting

Standards..........................................................................................................................................4

Part 3: Signs to be taken into account by Auditors for Identifying Going Concern Problem.........5

Part 4: Analyse of Dick Smith annual report 2014/15 to provide the evidence that company

might not be going concern.............................................................................................................7

Part 5: Reason behind giving the unmodified audit opinion by Deloitte for the financial year

ended 30June, 2015.........................................................................................................................8

Part 6: Auditor’s Legal Liability in the case of Dick Smith Electronics Ltd for providing answer

to an unmodified audit opinion for the financial year 30 June 2015...............................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

Contents

Introduction......................................................................................................................................3

Part 1: Brief History of Dick Smith and reasons that causes its failure..........................................3

Part 2: Accusation against the Directors of Dick Smith for Breach of Australian Accounting

Standards..........................................................................................................................................4

Part 3: Signs to be taken into account by Auditors for Identifying Going Concern Problem.........5

Part 4: Analyse of Dick Smith annual report 2014/15 to provide the evidence that company

might not be going concern.............................................................................................................7

Part 5: Reason behind giving the unmodified audit opinion by Deloitte for the financial year

ended 30June, 2015.........................................................................................................................8

Part 6: Auditor’s Legal Liability in the case of Dick Smith Electronics Ltd for providing answer

to an unmodified audit opinion for the financial year 30 June 2015...............................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

3

Introduction

Dick Smith was the renowned entity of Australia that collapsed in year 2016 due to

unethical accounting practices. There are many issues that have been found in financial report of

the company and same has been reported by liquidator in his report. Some of the values of

financial elements of the company have been wrongly reported in annual report that causes

undue increase in profits but it was not actually earned. Similarly there are many accounting

issues that will discussed in this essay and all these issues were the reason behind the failure of

Dick Smith.

The purpose of this essay is to examine the financial reports and relevant news articles

for identifying the probable causes and reasons for the collapse of the Dick Smith in very short

span of time. The essay will specifically highlight the accounting standards that have been

breached by the director of the company. Identification of signs that indicate that auditors

provided in the annual report that there was going concern problem of Dick Smith. This essay

also reports the evidences from the annual report for depicting the fraudulent accounting

practices followed by Dick Smith. Further there will be discussion on reasons that has caused

auditors to give unmodified audit opinion on the financial statements ended 30 June, 2015.

Lastly, there will be discussion on auditor’s legal liability for not providing the modified opinion

on the financial statements of Dick Smith for year ended 30June, 2015.

Part 1: Brief History of Dick Smith and reasons that causes its failure

Dick Smith Holdings was the subsidiary of Woolworth and it is known as Dick Smith

Electronics or DSE. Dick Smith had large number of electronic retails stores that sold wide

variety of electronic goods for domestic as well as industrial purpose. Dick Smith was formerly

listed on Australian Stock Exchange and it has successfully expanded its business in New

Zealand as well as many parts of Australia. Dick Smith Electronics has been founded by Dick

Smith in year 1968 and since then company has grown rapidly and Woolworth has purchased its

100% shares that makes the Dick Smith, subsidiary of Woolworth.

There are many reasons that have caused the failure of Dick Smith in year 2016 but the

exact reason was not clearly known as it was management act which was not easy to identify.

Introduction

Dick Smith was the renowned entity of Australia that collapsed in year 2016 due to

unethical accounting practices. There are many issues that have been found in financial report of

the company and same has been reported by liquidator in his report. Some of the values of

financial elements of the company have been wrongly reported in annual report that causes

undue increase in profits but it was not actually earned. Similarly there are many accounting

issues that will discussed in this essay and all these issues were the reason behind the failure of

Dick Smith.

The purpose of this essay is to examine the financial reports and relevant news articles

for identifying the probable causes and reasons for the collapse of the Dick Smith in very short

span of time. The essay will specifically highlight the accounting standards that have been

breached by the director of the company. Identification of signs that indicate that auditors

provided in the annual report that there was going concern problem of Dick Smith. This essay

also reports the evidences from the annual report for depicting the fraudulent accounting

practices followed by Dick Smith. Further there will be discussion on reasons that has caused

auditors to give unmodified audit opinion on the financial statements ended 30 June, 2015.

Lastly, there will be discussion on auditor’s legal liability for not providing the modified opinion

on the financial statements of Dick Smith for year ended 30June, 2015.

Part 1: Brief History of Dick Smith and reasons that causes its failure

Dick Smith Holdings was the subsidiary of Woolworth and it is known as Dick Smith

Electronics or DSE. Dick Smith had large number of electronic retails stores that sold wide

variety of electronic goods for domestic as well as industrial purpose. Dick Smith was formerly

listed on Australian Stock Exchange and it has successfully expanded its business in New

Zealand as well as many parts of Australia. Dick Smith Electronics has been founded by Dick

Smith in year 1968 and since then company has grown rapidly and Woolworth has purchased its

100% shares that makes the Dick Smith, subsidiary of Woolworth.

There are many reasons that have caused the failure of Dick Smith in year 2016 but the

exact reason was not clearly known as it was management act which was not easy to identify.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

The Administrator appointed in case of Dick Smith has successfully found the possible causes of

collapse of Dick Smith and has provided in its report. The main reason behind the collapse of

Dick Smith is excessive buying to build up the stock of inventory for the purpose of expansion.

In addition to inventory buildup, there were many accounting issues that were reported by the

administrator in his report. In last few months of collapse of the Dick Smith it has been found

that company was undergoing in losses and the main reason behind this was decrease in sales

and excessive inventory (The Conversation, 2016). The decision of directors to built up the

inventory and get rebates on the bulk purchases has forced to maintain inventory at very low cost

in their accounts and also the non availability cash surplus also affected liquidity position of the

company. During the last few month of collapse of Dick Smith it was found that company has

failed to pay its liabilities and also struggling with the working capital.

Another big mistake that has been committed was fraud performed by Anchorage

Capital. Anchorage Capital was involved accounting fraud through creating the hype in the stock

market and making millions of dollars through sales of shares at very high price. A year back of

Dick Smith collapse it was found that books of accounts has been manipulated and high profits

are being reported that helps in increasing the market value of shares. The increasing trend in

share price had attracted millions of potential shareholders to invest in company that raised the

value of company to $500 million. But company fails to meet the commitment made to

shareholders as revenue growth was not as expected and profits are declined and lead to losses.

This has left company with significant level of stocks and outdated products that has very low

value in the market. So the reasons like shortage of cash, accounting frauds, increase in debt and

continue losses are the main reasons behind the collapse of Dick Smith in starting of year 2016

(News.com.au, 2016).

Part 2: Accusation against the Directors of Dick Smith for Breach of Australian

Accounting Standards

Dick Smith directors are accused of adopting the use of fraudulent accounting methods

that are known within the industry as ‘Real Activities Management’. This accounting practice

involves the use of manipulation of sales figures and inventories of stock in which it purchases

excessive amount of inventory for rapid expansion of its stores and obtaining bank rebates from

The Administrator appointed in case of Dick Smith has successfully found the possible causes of

collapse of Dick Smith and has provided in its report. The main reason behind the collapse of

Dick Smith is excessive buying to build up the stock of inventory for the purpose of expansion.

In addition to inventory buildup, there were many accounting issues that were reported by the

administrator in his report. In last few months of collapse of the Dick Smith it has been found

that company was undergoing in losses and the main reason behind this was decrease in sales

and excessive inventory (The Conversation, 2016). The decision of directors to built up the

inventory and get rebates on the bulk purchases has forced to maintain inventory at very low cost

in their accounts and also the non availability cash surplus also affected liquidity position of the

company. During the last few month of collapse of Dick Smith it was found that company has

failed to pay its liabilities and also struggling with the working capital.

Another big mistake that has been committed was fraud performed by Anchorage

Capital. Anchorage Capital was involved accounting fraud through creating the hype in the stock

market and making millions of dollars through sales of shares at very high price. A year back of

Dick Smith collapse it was found that books of accounts has been manipulated and high profits

are being reported that helps in increasing the market value of shares. The increasing trend in

share price had attracted millions of potential shareholders to invest in company that raised the

value of company to $500 million. But company fails to meet the commitment made to

shareholders as revenue growth was not as expected and profits are declined and lead to losses.

This has left company with significant level of stocks and outdated products that has very low

value in the market. So the reasons like shortage of cash, accounting frauds, increase in debt and

continue losses are the main reasons behind the collapse of Dick Smith in starting of year 2016

(News.com.au, 2016).

Part 2: Accusation against the Directors of Dick Smith for Breach of Australian

Accounting Standards

Dick Smith directors are accused of adopting the use of fraudulent accounting methods

that are known within the industry as ‘Real Activities Management’. This accounting practice

involves the use of manipulation of sales figures and inventories of stock in which it purchases

excessive amount of inventory for rapid expansion of its stores and obtaining bank rebates from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

its suppliers for inflation of its earnings. The strategy intends to raise the share prices of the

company and the director’s receives incentives for pursuing of excessive growth for increase in

the stock (The ugly story of Dick Smith, from float to failure, 2016). The directors are accused

for not complying effective with the Corporations Law by the use of faulty accounting practices

such as RAM (Real Activities Management). It involves structuring the financial transactions in

a manner that ultimately results in manipulating the financial information for misleading the end-

users. The activities involves mainly achieving a reduction in the expenses involved in research

and development activities, price discounts for meeting short-term earnings targets, stimulating

overproduction for generating excess inventory for reducing the cost of goods sold (Some

answers, more questions over Dick Smith failure, 2016).

The directors of the company are mainly accused for violating the various provisions of

the Corporations Act that also includes continuous disclosure obligations. It has been stated in

the context of the company that the directors decision to buy stock is mainly based on the rebate

obtained from the suppliers and not taking into account the needs and requirements of the

customers (Clarke, 2003). This has resulted in increasing the bad stock of the company and

ultimately raising its debt obligations. It has been claimed by the shareholders of the company

that its directors were aware of the potential problems but them also violated the continuous

disclosure obligations by not presenting the realistic and fair financial information to them. The

directors had adopted the use of false accounting practices to deceive the investors and reflecting

the inflated share prices that have negatively impacted the interest of the stakeholders. The

avoidance of continuous disclosure obligation by its directors is held largely responsible for

making it bankrupt by not selling profitably the excessive inventory purchases and thus resulting

in shortage of cash flow. The directors and executives of the Dick Smith were legally claimed by

its shareholders on account of their failure to implement adequate system related to rebates and

management of inventory (The Conversation, 2016).

Part 3: Signs to be taken into account by Auditors for Identifying Going Concern Problem

A business entity need to prepare the financial statements in accordance with the going

concern basis that directs an entity to view its business to be carried out on a continuing basis in

the future context. Thus, in this context it is essential that management by expecting that the

its suppliers for inflation of its earnings. The strategy intends to raise the share prices of the

company and the director’s receives incentives for pursuing of excessive growth for increase in

the stock (The ugly story of Dick Smith, from float to failure, 2016). The directors are accused

for not complying effective with the Corporations Law by the use of faulty accounting practices

such as RAM (Real Activities Management). It involves structuring the financial transactions in

a manner that ultimately results in manipulating the financial information for misleading the end-

users. The activities involves mainly achieving a reduction in the expenses involved in research

and development activities, price discounts for meeting short-term earnings targets, stimulating

overproduction for generating excess inventory for reducing the cost of goods sold (Some

answers, more questions over Dick Smith failure, 2016).

The directors of the company are mainly accused for violating the various provisions of

the Corporations Act that also includes continuous disclosure obligations. It has been stated in

the context of the company that the directors decision to buy stock is mainly based on the rebate

obtained from the suppliers and not taking into account the needs and requirements of the

customers (Clarke, 2003). This has resulted in increasing the bad stock of the company and

ultimately raising its debt obligations. It has been claimed by the shareholders of the company

that its directors were aware of the potential problems but them also violated the continuous

disclosure obligations by not presenting the realistic and fair financial information to them. The

directors had adopted the use of false accounting practices to deceive the investors and reflecting

the inflated share prices that have negatively impacted the interest of the stakeholders. The

avoidance of continuous disclosure obligation by its directors is held largely responsible for

making it bankrupt by not selling profitably the excessive inventory purchases and thus resulting

in shortage of cash flow. The directors and executives of the Dick Smith were legally claimed by

its shareholders on account of their failure to implement adequate system related to rebates and

management of inventory (The Conversation, 2016).

Part 3: Signs to be taken into account by Auditors for Identifying Going Concern Problem

A business entity need to prepare the financial statements in accordance with the going

concern basis that directs an entity to view its business to be carried out on a continuing basis in

the future context. Thus, in this context it is essential that management by expecting that the

6

entity can become insolvent in the future should not prepare the financial statement under the

going concern basis but with the use of a different basis such as break-up basis. The

responsibility of an auditor is highly important in this regard for determining whether the

financial statements can be prepared by the use of going concern assumption. The auditing

standards of ISA 570 has been developed in this regard for obtaining appropriate audit evidence

about the adequacy of the management use of going concern assumption. It is therefore the

responsibility of the auditor in determining whether there is presence of any material uncertainty

in the financial statements of an entity. As such, the auditors holds an important obligation to

protect the interests of the stakeholders by ensuring that an entity would continue to run its

operations in the foreseeable future and this forms the basis of their decision-making process

(Putra, 2017).

It has been argued in the case of Dick Smiths that Deloitte, the auditing firm of the

company, has questioned its rebates and over-valuation of its inventory. The auditing firm has

also provided advise to the directors for controlling the weaknesses in their management control

systems but the question arises how did they value the company as a going concern despite of

identification such accounting issues. Therefore, the auditor of Dick Smith should have also

considered the following points for identifying the going concern problem:

Analytical Procedures: The procedures are used as a substantive test for determining nay

negative trend within the financial statement of a firm. This can involve identifying any

liquidity or solvency issues by assessing the adverse conditions indicated in the balance

sheet.

Internal matters: The presence of an inadequate control system characterized by weak

accounting system can also be used the auditor for identifying the issue of going concern

Financial issues: The financial difficulties faced by the firm such as increasing debt

liabilities as in the case of Dick Smith also serves as a potential sign to indicate the

problem relating to the continuing operations of the company in the future context (Going

concern- who is responsible, 2017).

entity can become insolvent in the future should not prepare the financial statement under the

going concern basis but with the use of a different basis such as break-up basis. The

responsibility of an auditor is highly important in this regard for determining whether the

financial statements can be prepared by the use of going concern assumption. The auditing

standards of ISA 570 has been developed in this regard for obtaining appropriate audit evidence

about the adequacy of the management use of going concern assumption. It is therefore the

responsibility of the auditor in determining whether there is presence of any material uncertainty

in the financial statements of an entity. As such, the auditors holds an important obligation to

protect the interests of the stakeholders by ensuring that an entity would continue to run its

operations in the foreseeable future and this forms the basis of their decision-making process

(Putra, 2017).

It has been argued in the case of Dick Smiths that Deloitte, the auditing firm of the

company, has questioned its rebates and over-valuation of its inventory. The auditing firm has

also provided advise to the directors for controlling the weaknesses in their management control

systems but the question arises how did they value the company as a going concern despite of

identification such accounting issues. Therefore, the auditor of Dick Smith should have also

considered the following points for identifying the going concern problem:

Analytical Procedures: The procedures are used as a substantive test for determining nay

negative trend within the financial statement of a firm. This can involve identifying any

liquidity or solvency issues by assessing the adverse conditions indicated in the balance

sheet.

Internal matters: The presence of an inadequate control system characterized by weak

accounting system can also be used the auditor for identifying the issue of going concern

Financial issues: The financial difficulties faced by the firm such as increasing debt

liabilities as in the case of Dick Smith also serves as a potential sign to indicate the

problem relating to the continuing operations of the company in the future context (Going

concern- who is responsible, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Part 4: Analyse of Dick Smith annual report 2014/15 to provide the evidence that company

might not be going concern

It is highly important for the companies to be going concern to sustain in the market for

the long term. Going concern refers to the most important fundamental accounting principle that

very company must follow. This accounting principle is based on the assumption that company

will carry out its business for foreseeable future with no perception to close it down in future. It

is highly important to report about the going concern in the annual report. It is management duty

to verify and report in annual report that company has no intention to close the down the

business or any of business units in future. It is highly important there must be enough evidences

in the annual report that proves that company is going concern and will survive for long run

(Seyam & Brickman, 2016).

On evaluation of annual report of Dick Smith for year 2014-15 it has been found that

there are few evidences that show that company will not be going concern in future. The annual

report clearly shows that huge amount of cash has been provided to the suppliers in order to have

surplus stock but this strategy of directors has not worked as there was cash shortage for longer

period of time. The shortage of cash was due to decrease in demand of the electronics products

and company has failed to collect the account receivable on time. The annual report of year

2014-15 shows the increase in sales revenue but fails to generate the free cash flows which have

increased the debt liabilities (Annual Report, 2015). The director’s intention of stock piling does

not work in favor of company but it was main reason behind the shortage of working capital.

Through analyzing the liquidator report it was found that directors and management had

purchased the large volume of inventory in order to satisfy the needs of new stores. In doing so,

management has taken a huge bank loan and also received the rebates from the suppliers. The

impact of this was increased debt at one side of balance sheet and lower cost inventory on other

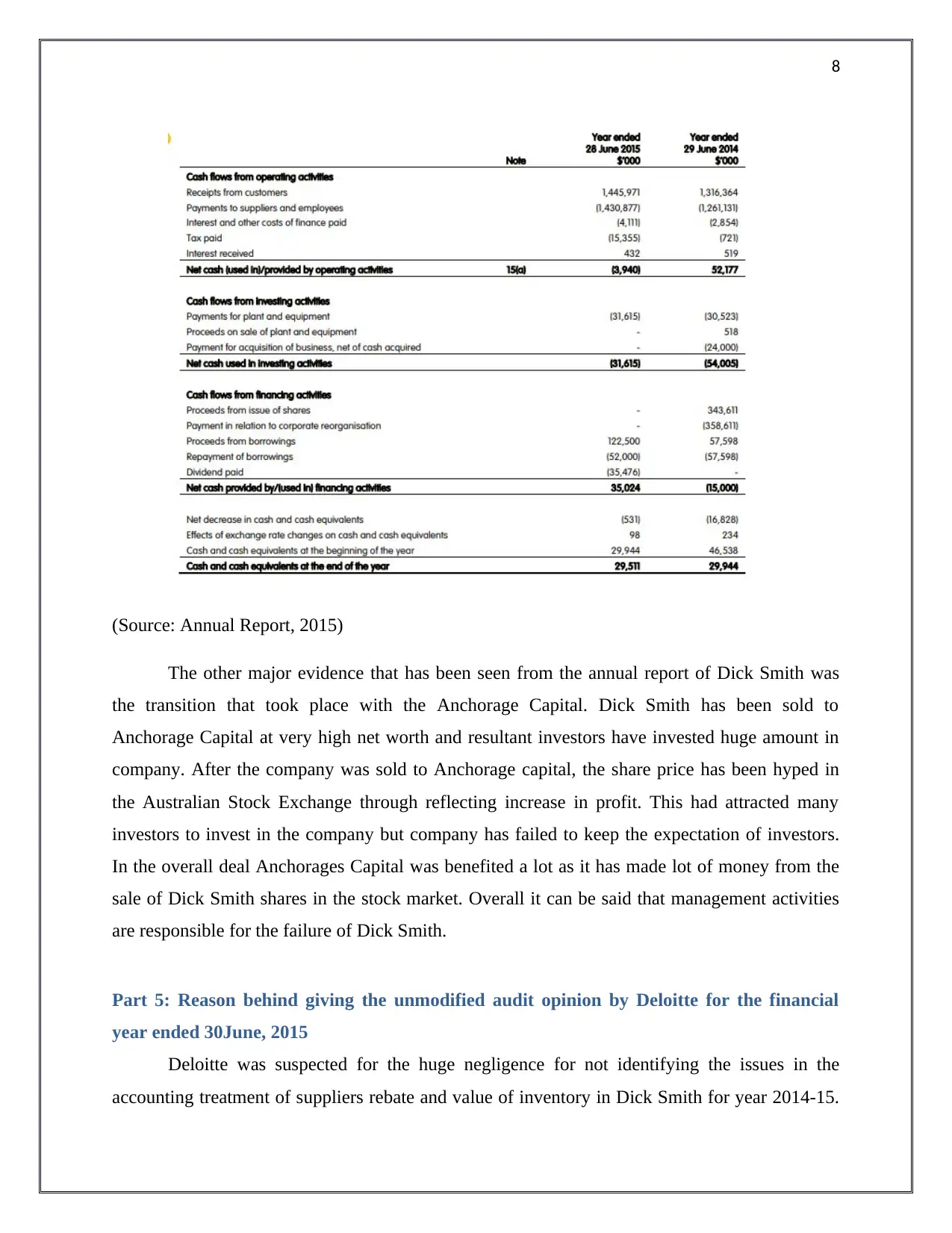

hand that has lost its value due to change in technology. Below is extracts of cash flow statement

from the annual report 2014-15 that clearly shows there was no cash surplus from the operating

activity in year 2015 (Annual Report, 2015).

Part 4: Analyse of Dick Smith annual report 2014/15 to provide the evidence that company

might not be going concern

It is highly important for the companies to be going concern to sustain in the market for

the long term. Going concern refers to the most important fundamental accounting principle that

very company must follow. This accounting principle is based on the assumption that company

will carry out its business for foreseeable future with no perception to close it down in future. It

is highly important to report about the going concern in the annual report. It is management duty

to verify and report in annual report that company has no intention to close the down the

business or any of business units in future. It is highly important there must be enough evidences

in the annual report that proves that company is going concern and will survive for long run

(Seyam & Brickman, 2016).

On evaluation of annual report of Dick Smith for year 2014-15 it has been found that

there are few evidences that show that company will not be going concern in future. The annual

report clearly shows that huge amount of cash has been provided to the suppliers in order to have

surplus stock but this strategy of directors has not worked as there was cash shortage for longer

period of time. The shortage of cash was due to decrease in demand of the electronics products

and company has failed to collect the account receivable on time. The annual report of year

2014-15 shows the increase in sales revenue but fails to generate the free cash flows which have

increased the debt liabilities (Annual Report, 2015). The director’s intention of stock piling does

not work in favor of company but it was main reason behind the shortage of working capital.

Through analyzing the liquidator report it was found that directors and management had

purchased the large volume of inventory in order to satisfy the needs of new stores. In doing so,

management has taken a huge bank loan and also received the rebates from the suppliers. The

impact of this was increased debt at one side of balance sheet and lower cost inventory on other

hand that has lost its value due to change in technology. Below is extracts of cash flow statement

from the annual report 2014-15 that clearly shows there was no cash surplus from the operating

activity in year 2015 (Annual Report, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

(Source: Annual Report, 2015)

The other major evidence that has been seen from the annual report of Dick Smith was

the transition that took place with the Anchorage Capital. Dick Smith has been sold to

Anchorage Capital at very high net worth and resultant investors have invested huge amount in

company. After the company was sold to Anchorage capital, the share price has been hyped in

the Australian Stock Exchange through reflecting increase in profit. This had attracted many

investors to invest in the company but company has failed to keep the expectation of investors.

In the overall deal Anchorages Capital was benefited a lot as it has made lot of money from the

sale of Dick Smith shares in the stock market. Overall it can be said that management activities

are responsible for the failure of Dick Smith.

Part 5: Reason behind giving the unmodified audit opinion by Deloitte for the financial

year ended 30June, 2015

Deloitte was suspected for the huge negligence for not identifying the issues in the

accounting treatment of suppliers rebate and value of inventory in Dick Smith for year 2014-15.

(Source: Annual Report, 2015)

The other major evidence that has been seen from the annual report of Dick Smith was

the transition that took place with the Anchorage Capital. Dick Smith has been sold to

Anchorage Capital at very high net worth and resultant investors have invested huge amount in

company. After the company was sold to Anchorage capital, the share price has been hyped in

the Australian Stock Exchange through reflecting increase in profit. This had attracted many

investors to invest in the company but company has failed to keep the expectation of investors.

In the overall deal Anchorages Capital was benefited a lot as it has made lot of money from the

sale of Dick Smith shares in the stock market. Overall it can be said that management activities

are responsible for the failure of Dick Smith.

Part 5: Reason behind giving the unmodified audit opinion by Deloitte for the financial

year ended 30June, 2015

Deloitte was suspected for the huge negligence for not identifying the issues in the

accounting treatment of suppliers rebate and value of inventory in Dick Smith for year 2014-15.

9

The fact that was represented by Deloitte was that it has conducted the complete audit procedure

for accounting of rebates but has failed to locate and report the material issues in the accounting

system and processes of Dick Smith (Legal Liability of Auditors, 2017). To be on safer side and

to remain as an external auditor of Dick Smith for longer run, Deloitte has not taken considerable

steps to check the manipulation in the accounting standards and use test controls to check the

material misstatement by the management. This has caused Deloitte to make the unmodified

audit opinion for the financial year ended 30 June, 2015 (Annual Report, 2015).

Part 6: Auditor’s Legal Liability in the case of Dick Smith Electronics Ltd for providing

answer to an unmodified audit opinion for the financial year 30 June 2015

Deloitte, the auditor of Dick Smith Electronics, has been alleged due to providing

unmodified audit opinion for the financial year 2015 despite of identifying various accounting

issues present within its financial reports. Deloitte ahs raised questions on the management of the

firm regarding the over-valuation of its inventory and manipulation of the sales figure for

meeting the expected budget. Thus, despite of knowing the financial issues present within the

company its auditors can be regarded as legally responsible for providing a justification to give

unmodified audit opinions (Spencer, 2017). This is because as per the IAS 570 the auditors

before classifying an entity as a going concern need to accurately assess the information

provided by the management for protecting the interest of the stakeholders. However, Deloitte

has been legally claimed by Dick Smith shareholders of intentionally providing unmodified audit

opinions and therefore they have a case to answer. This is because it has not reported any

material deficiency in the controls and systems within the company in respect of identifying,

calculating and recognition of debates. Therefore, the legal claim can be filed against the

auditing firm of the company in addition to its former directors and executives (Clarke, 2003).

Conclusion

The overall assessment of collapse of Dick Smith has helped to learn the lesson on

accounting fraud that management and auditors carried out to earn the huge profits. From the

case of Dick Smith it was clearly held the real activities of management are hard to identify and

such material misstatement can cause severe damage to the going concern accounting principle.

It is the duty of auditor to test the misstatement of management and report them in annual report.

The fact that was represented by Deloitte was that it has conducted the complete audit procedure

for accounting of rebates but has failed to locate and report the material issues in the accounting

system and processes of Dick Smith (Legal Liability of Auditors, 2017). To be on safer side and

to remain as an external auditor of Dick Smith for longer run, Deloitte has not taken considerable

steps to check the manipulation in the accounting standards and use test controls to check the

material misstatement by the management. This has caused Deloitte to make the unmodified

audit opinion for the financial year ended 30 June, 2015 (Annual Report, 2015).

Part 6: Auditor’s Legal Liability in the case of Dick Smith Electronics Ltd for providing

answer to an unmodified audit opinion for the financial year 30 June 2015

Deloitte, the auditor of Dick Smith Electronics, has been alleged due to providing

unmodified audit opinion for the financial year 2015 despite of identifying various accounting

issues present within its financial reports. Deloitte ahs raised questions on the management of the

firm regarding the over-valuation of its inventory and manipulation of the sales figure for

meeting the expected budget. Thus, despite of knowing the financial issues present within the

company its auditors can be regarded as legally responsible for providing a justification to give

unmodified audit opinions (Spencer, 2017). This is because as per the IAS 570 the auditors

before classifying an entity as a going concern need to accurately assess the information

provided by the management for protecting the interest of the stakeholders. However, Deloitte

has been legally claimed by Dick Smith shareholders of intentionally providing unmodified audit

opinions and therefore they have a case to answer. This is because it has not reported any

material deficiency in the controls and systems within the company in respect of identifying,

calculating and recognition of debates. Therefore, the legal claim can be filed against the

auditing firm of the company in addition to its former directors and executives (Clarke, 2003).

Conclusion

The overall assessment of collapse of Dick Smith has helped to learn the lesson on

accounting fraud that management and auditors carried out to earn the huge profits. From the

case of Dick Smith it was clearly held the real activities of management are hard to identify and

such material misstatement can cause severe damage to the going concern accounting principle.

It is the duty of auditor to test the misstatement of management and report them in annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

Annual Report. (2015). Dick Smith. Retrieved on November 22, 2018, from

Clarke, F. (2003). Corporate Collapse: Accounting, Regulatory and Ethical Failure. Cambridge

University Press.

Going concern- who is responsible. (2017). Retrieved 22 November, 2018, from

Legal Liability of Auditors. (2017). Retrieved on November 22, 2018, from

News.com.au. (2016). McGrathNicol releases Dick Smith report. Retrieved on November 22,

2018, from

Putra, L. (2017). How Auditors Evaluate Entity Going Concern. Retrieved 22 November, 2018,

from

Seyam, A. & Brickman, S. (2016). The Going Concern Assumptions and Presentation on

Financial Statements. Retrieved on November 22, 2018, from

Some answers, more questions over Dick Smith failure. (2016). Retrieved 22 November, 2018,

from

Spencer, L. (2017). Deloitte dragged into Dick Smith directors’ legal battle. Retrieved 22

November, 2018, from

The Conversation. (2016). The ugly story of Dick Smith, from float to failure. Retrieved on

November 22, 2018, from

References

Annual Report. (2015). Dick Smith. Retrieved on November 22, 2018, from

Clarke, F. (2003). Corporate Collapse: Accounting, Regulatory and Ethical Failure. Cambridge

University Press.

Going concern- who is responsible. (2017). Retrieved 22 November, 2018, from

Legal Liability of Auditors. (2017). Retrieved on November 22, 2018, from

News.com.au. (2016). McGrathNicol releases Dick Smith report. Retrieved on November 22,

2018, from

Putra, L. (2017). How Auditors Evaluate Entity Going Concern. Retrieved 22 November, 2018,

from

Seyam, A. & Brickman, S. (2016). The Going Concern Assumptions and Presentation on

Financial Statements. Retrieved on November 22, 2018, from

Some answers, more questions over Dick Smith failure. (2016). Retrieved 22 November, 2018,

from

Spencer, L. (2017). Deloitte dragged into Dick Smith directors’ legal battle. Retrieved 22

November, 2018, from

The Conversation. (2016). The ugly story of Dick Smith, from float to failure. Retrieved on

November 22, 2018, from

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.