Advanced Corporate Reporting: Financial Instruments & IFRS 9

VerifiedAdded on 2023/06/17

|9

|2273

|321

Report

AI Summary

This assignment provides a comprehensive analysis of advanced corporate reporting, covering key areas such as consolidated financial statements, IFRS compliance, and valuation methods. It includes the preparation of a consolidated statement of financial position for Camera Plc, applying IFRS 2 for share-based payments in Pulp plc, and discussing IFRS 9 for financial instruments. The report also explores the residual income valuation method, its advantages and disadvantages, and the importance of financial statements for equity investors. Furthermore, it discusses the application of IFRS for convertible bonds and lease agreements, comparing fair value and historical cost accounting methods. The document is a student contribution, and more solved assignments are available on Desklib.

Advanced Corporate

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

QUESTION 3...................................................................................................................................5

A..................................................................................................................................................5

B..................................................................................................................................................5

C..................................................................................................................................................6

D..................................................................................................................................................6

QUESTION 4...................................................................................................................................7

A..................................................................................................................................................7

B..................................................................................................................................................8

REFERENCES................................................................................................................................9

QUESTION 1...................................................................................................................................3

QUESTION 3...................................................................................................................................5

A..................................................................................................................................................5

B..................................................................................................................................................5

C..................................................................................................................................................6

D..................................................................................................................................................6

QUESTION 4...................................................................................................................................7

A..................................................................................................................................................7

B..................................................................................................................................................8

REFERENCES................................................................................................................................9

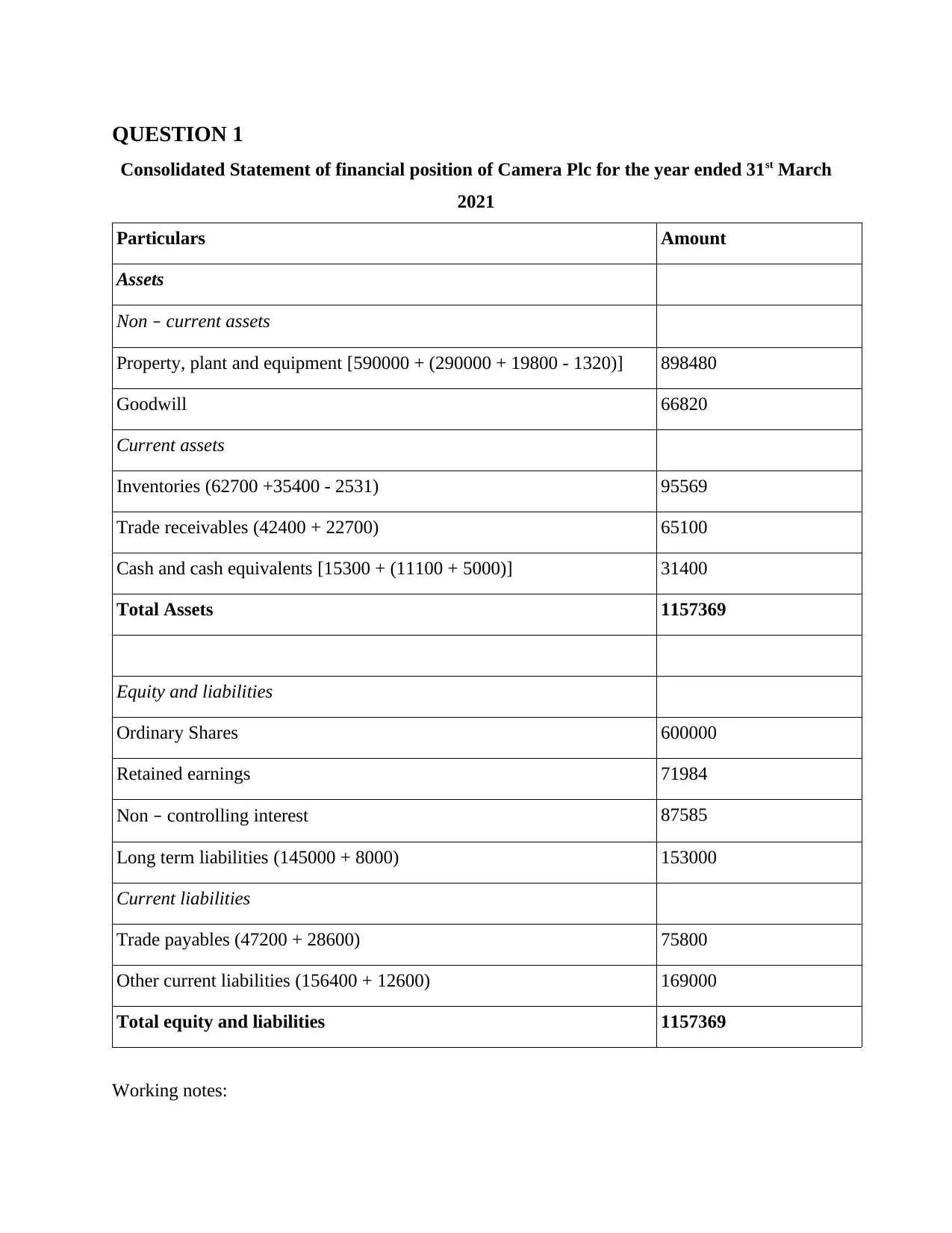

QUESTION 1

Consolidated Statement of financial position of Camera Plc for the year ended 31st March

2021

Particulars Amount

Assets

Non – current assets

Property, plant and equipment [590000 + (290000 + 19800 - 1320)] 898480

Goodwill 66820

Current assets

Inventories (62700 +35400 - 2531) 95569

Trade receivables (42400 + 22700) 65100

Cash and cash equivalents [15300 + (11100 + 5000)] 31400

Total Assets 1157369

Equity and liabilities

Ordinary Shares 600000

Retained earnings 71984

Non – controlling interest 87585

Long term liabilities (145000 + 8000) 153000

Current liabilities

Trade payables (47200 + 28600) 75800

Other current liabilities (156400 + 12600) 169000

Total equity and liabilities 1157369

Working notes:

Consolidated Statement of financial position of Camera Plc for the year ended 31st March

2021

Particulars Amount

Assets

Non – current assets

Property, plant and equipment [590000 + (290000 + 19800 - 1320)] 898480

Goodwill 66820

Current assets

Inventories (62700 +35400 - 2531) 95569

Trade receivables (42400 + 22700) 65100

Cash and cash equivalents [15300 + (11100 + 5000)] 31400

Total Assets 1157369

Equity and liabilities

Ordinary Shares 600000

Retained earnings 71984

Non – controlling interest 87585

Long term liabilities (145000 + 8000) 153000

Current liabilities

Trade payables (47200 + 28600) 75800

Other current liabilities (156400 + 12600) 169000

Total equity and liabilities 1157369

Working notes:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

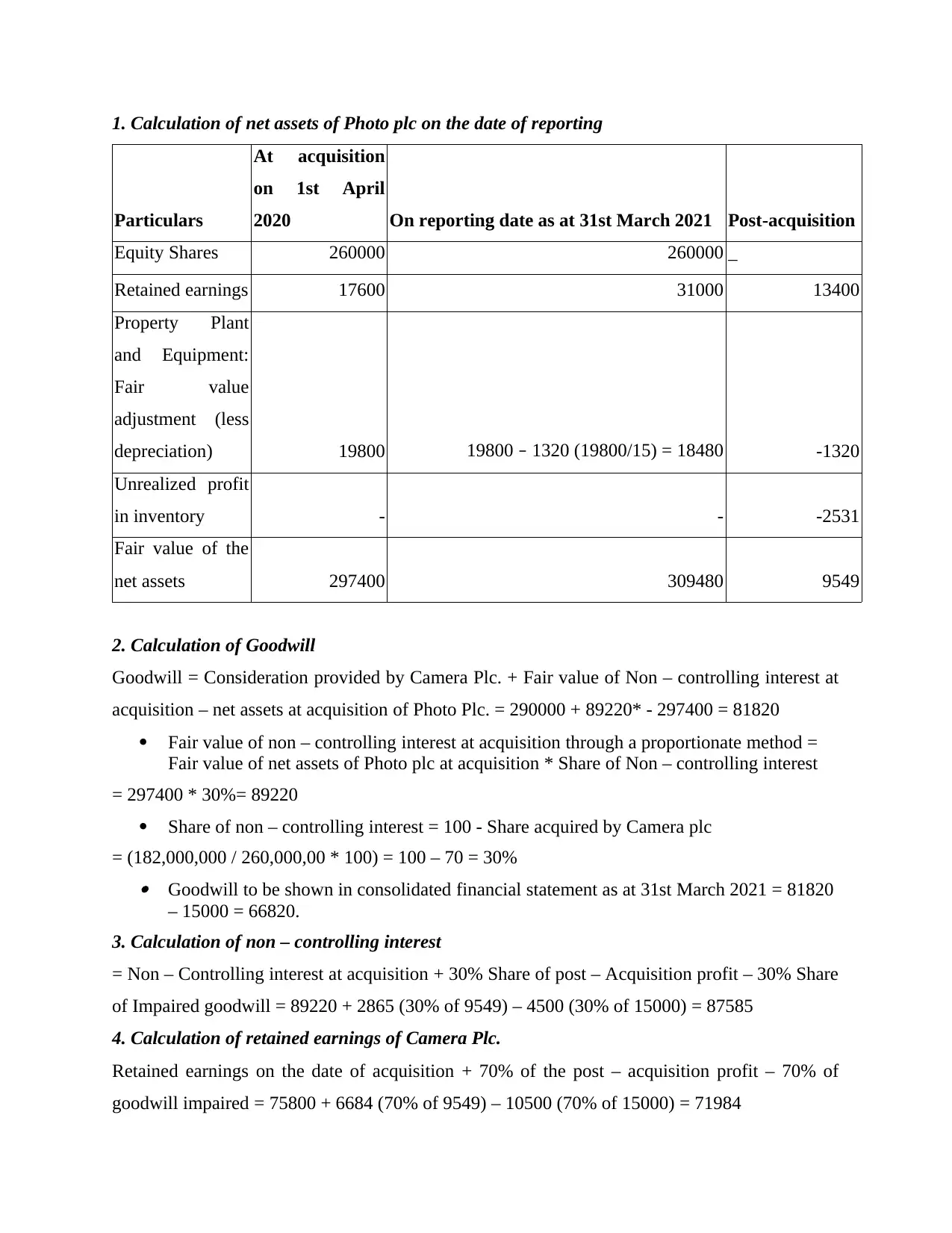

1. Calculation of net assets of Photo plc on the date of reporting

Particulars

At acquisition

on 1st April

2020 On reporting date as at 31st March 2021 Post-acquisition

Equity Shares 260000 260000 _

Retained earnings 17600 31000 13400

Property Plant

and Equipment:

Fair value

adjustment (less

depreciation) 19800 19800 – 1320 (19800/15) = 18480 -1320

Unrealized profit

in inventory - - -2531

Fair value of the

net assets 297400 309480 9549

2. Calculation of Goodwill

Goodwill = Consideration provided by Camera Plc. + Fair value of Non – controlling interest at

acquisition – net assets at acquisition of Photo Plc. = 290000 + 89220* - 297400 = 81820

Fair value of non – controlling interest at acquisition through a proportionate method =

Fair value of net assets of Photo plc at acquisition * Share of Non – controlling interest

= 297400 * 30%= 89220

Share of non – controlling interest = 100 - Share acquired by Camera plc

= (182,000,000 / 260,000,00 * 100) = 100 – 70 = 30% Goodwill to be shown in consolidated financial statement as at 31st March 2021 = 81820

– 15000 = 66820.

3. Calculation of non – controlling interest

= Non – Controlling interest at acquisition + 30% Share of post – Acquisition profit – 30% Share

of Impaired goodwill = 89220 + 2865 (30% of 9549) – 4500 (30% of 15000) = 87585

4. Calculation of retained earnings of Camera Plc.

Retained earnings on the date of acquisition + 70% of the post – acquisition profit – 70% of

goodwill impaired = 75800 + 6684 (70% of 9549) – 10500 (70% of 15000) = 71984

Particulars

At acquisition

on 1st April

2020 On reporting date as at 31st March 2021 Post-acquisition

Equity Shares 260000 260000 _

Retained earnings 17600 31000 13400

Property Plant

and Equipment:

Fair value

adjustment (less

depreciation) 19800 19800 – 1320 (19800/15) = 18480 -1320

Unrealized profit

in inventory - - -2531

Fair value of the

net assets 297400 309480 9549

2. Calculation of Goodwill

Goodwill = Consideration provided by Camera Plc. + Fair value of Non – controlling interest at

acquisition – net assets at acquisition of Photo Plc. = 290000 + 89220* - 297400 = 81820

Fair value of non – controlling interest at acquisition through a proportionate method =

Fair value of net assets of Photo plc at acquisition * Share of Non – controlling interest

= 297400 * 30%= 89220

Share of non – controlling interest = 100 - Share acquired by Camera plc

= (182,000,000 / 260,000,00 * 100) = 100 – 70 = 30% Goodwill to be shown in consolidated financial statement as at 31st March 2021 = 81820

– 15000 = 66820.

3. Calculation of non – controlling interest

= Non – Controlling interest at acquisition + 30% Share of post – Acquisition profit – 30% Share

of Impaired goodwill = 89220 + 2865 (30% of 9549) – 4500 (30% of 15000) = 87585

4. Calculation of retained earnings of Camera Plc.

Retained earnings on the date of acquisition + 70% of the post – acquisition profit – 70% of

goodwill impaired = 75800 + 6684 (70% of 9549) – 10500 (70% of 15000) = 71984

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

A

The IFRS 2 is based on share based payment on the basis of the financial reporting. The

company need to use the share based payment for evaluating the value of the shares. It is

necessary for the company to comply with the share based payment so that the shares are being

recorded in proper and effective manner. In case of Pulp plc, the transaction relating to shares

will be recorded on the basis of the IFRS 2 relating to the share based payment. In the case of

year 1, the record will be maintained and recorded with the 300 share to each employee that is

550 employees in total. but in the end of year 1, 25 employees have left and these will not be

provided with shares. Thus the total of 525 employees will be recorded and will be recorded at

15 % increased rate that is 13.8. But in the year 2 the record will again change as 34 more

employees will be leaving the company and due to this, in year 2 the number of employees will

be 491 and rate has increased by 14 % that is 15.801. Further in the year 3 there is not any of the

employee leaving the company. hence, in the last year that record within the company account

will be on basis of 491 employees and they will be provided with 300 shares each at rate of

18.80.

B

The IFRS 9 is the one which relates with ways in which the company classifies and

measures the financial asset and liabilities and contract relating to buying and selling of the non-

financial items. The use of IFRS 9 is very important for the reason that it recognizes the financial

asset and liabilities of the company at its fair value or not at fair value. Also the transaction cost

is being directly attributable to the acquisition of the asset or liability. For the recording of the

transaction within the financial statement according to IFRS 9 is as follows-

Bond issued = 1800000

Issue cost = 0

Net cash inflow = 1800000

Coupon rate @ 7 % = 75240

Interest rate @ 9 % = 162000

Bond obligation = 1886760

(1800000 +162000 – 75240)

A

The IFRS 2 is based on share based payment on the basis of the financial reporting. The

company need to use the share based payment for evaluating the value of the shares. It is

necessary for the company to comply with the share based payment so that the shares are being

recorded in proper and effective manner. In case of Pulp plc, the transaction relating to shares

will be recorded on the basis of the IFRS 2 relating to the share based payment. In the case of

year 1, the record will be maintained and recorded with the 300 share to each employee that is

550 employees in total. but in the end of year 1, 25 employees have left and these will not be

provided with shares. Thus the total of 525 employees will be recorded and will be recorded at

15 % increased rate that is 13.8. But in the year 2 the record will again change as 34 more

employees will be leaving the company and due to this, in year 2 the number of employees will

be 491 and rate has increased by 14 % that is 15.801. Further in the year 3 there is not any of the

employee leaving the company. hence, in the last year that record within the company account

will be on basis of 491 employees and they will be provided with 300 shares each at rate of

18.80.

B

The IFRS 9 is the one which relates with ways in which the company classifies and

measures the financial asset and liabilities and contract relating to buying and selling of the non-

financial items. The use of IFRS 9 is very important for the reason that it recognizes the financial

asset and liabilities of the company at its fair value or not at fair value. Also the transaction cost

is being directly attributable to the acquisition of the asset or liability. For the recording of the

transaction within the financial statement according to IFRS 9 is as follows-

Bond issued = 1800000

Issue cost = 0

Net cash inflow = 1800000

Coupon rate @ 7 % = 75240

Interest rate @ 9 % = 162000

Bond obligation = 1886760

(1800000 +162000 – 75240)

Interest expense @ 9 % = 169808

Bond obligation = 2056568

Finance cost = 169808

Hence, with the above evaluation it is clear that within the balance sheet the bond obligation will

be recorded at 2056568 and in the profit and loss account will be recorded as 169808 as the

finance cost.

C

Yes, it is true that the residual income valuation is having clear link with other valuation

methods like dividend discount model. The major benefits and drawbacks of residual income

valuation is as follows-

Advantages

The major benefit of using residual income valuation method is that this model

undertakes the use of readily available accounting data and this assist in providing better

evaluation. Thus, the readily available information will assist in less time taking.

Along with this, another benefit of using the residual income method is that this method

is being used to value the non- dividend paying companies.

Disadvantages

The major drawback of using the residual income method is that this method is based on

the accounting data and as a result of this the manipulation of the data can be taken place.

Hence, this can modify or manipulate the data and results of the company.

Along with this another drawback of using this method is that this method assumes that

the cost of debt is equal to the interest expense which is not good.

D

It is true that the financial statements are very important for the equity investor for

evaluation of the position of the company. these financial statements are important for the

investors as it provides for correct and accurate information relating to the business and its

financial stability and performance. the equity investors are the one who invest within the

company and becomes the shareholder of the company (Nitani, Riding and He, 2019). hence, for

them, before investing within the company it is necessary that they evaluate the performance and

operational capability of the company. Hence, for this purpose the use of financial statement is

being done. This is particularly because of the reason that in case the financial statements will

Bond obligation = 2056568

Finance cost = 169808

Hence, with the above evaluation it is clear that within the balance sheet the bond obligation will

be recorded at 2056568 and in the profit and loss account will be recorded as 169808 as the

finance cost.

C

Yes, it is true that the residual income valuation is having clear link with other valuation

methods like dividend discount model. The major benefits and drawbacks of residual income

valuation is as follows-

Advantages

The major benefit of using residual income valuation method is that this model

undertakes the use of readily available accounting data and this assist in providing better

evaluation. Thus, the readily available information will assist in less time taking.

Along with this, another benefit of using the residual income method is that this method

is being used to value the non- dividend paying companies.

Disadvantages

The major drawback of using the residual income method is that this method is based on

the accounting data and as a result of this the manipulation of the data can be taken place.

Hence, this can modify or manipulate the data and results of the company.

Along with this another drawback of using this method is that this method assumes that

the cost of debt is equal to the interest expense which is not good.

D

It is true that the financial statements are very important for the equity investor for

evaluation of the position of the company. these financial statements are important for the

investors as it provides for correct and accurate information relating to the business and its

financial stability and performance. the equity investors are the one who invest within the

company and becomes the shareholder of the company (Nitani, Riding and He, 2019). hence, for

them, before investing within the company it is necessary that they evaluate the performance and

operational capability of the company. Hence, for this purpose the use of financial statement is

being done. This is particularly because of the reason that in case the financial statements will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

not be providing better and effective view then this will affect the working and investment level

of the company.

Thus, for profession equity investors the financial statement is being used in order to

evaluate the financial performance of the company before doing the investment. Moreover, the

financial statement provides information relating to liquidity, efficiency, profitability, solvency

and other aspects of the business and its performance (Berisha and Asllanaj, 2017). Hence, this

will be requiring by the equity investors to analyse the performance of the company and then to

take proper decision relating to growth and development of the business. the equity investors are

also responsible for the effective decision making. Hence, for this, it is essential that the equity

investors analyse the financial statement in detailed manner and then take decision for the

betterment of the working of company.

QUESTION 4

A

For the company to operate in better and effective manner it is necessary that is comply

with all the working in accordance to IFRS. Hence, for the effective recording of the convertible

bonds the company will be recoding them on the basis of fair value only. This is pertaining to the

fact that in case of the five- year convertible bond the conversion of the bond into shares will be

raking place on the fair value only that is the rate prevailing at the time of conversion. Along

with this in the other case, of lease agreement, the recording of the transaction will be taking

place on basis of IFRS 16. This IFRS states that how the accounting for the lease will be done

and all the decision relating to the lease will be involved during the accounting period (Morales

Díaz and Zamora Ramírez, 2018). In the present case of Tent Plc, the lease agreement will have

made on the basis of five -year account. This is pertaining to the fact that the lease agreement is

for five years and no ownership is being transferred. In the case of Tent plc, the right to use the

asset will be recorded within the books of account. Hence, for this all the payment made to lessor

at, before and commencement date will be recorded. Along with this, all the initial direct cost

incurred by the lessee will also be recorded within the books of account along with depreciation.

B

The fair value accounting is being referred to as measuring the business assets and

liabilities at the current market value. On the other hand, the historical cost accounting is a

of the company.

Thus, for profession equity investors the financial statement is being used in order to

evaluate the financial performance of the company before doing the investment. Moreover, the

financial statement provides information relating to liquidity, efficiency, profitability, solvency

and other aspects of the business and its performance (Berisha and Asllanaj, 2017). Hence, this

will be requiring by the equity investors to analyse the performance of the company and then to

take proper decision relating to growth and development of the business. the equity investors are

also responsible for the effective decision making. Hence, for this, it is essential that the equity

investors analyse the financial statement in detailed manner and then take decision for the

betterment of the working of company.

QUESTION 4

A

For the company to operate in better and effective manner it is necessary that is comply

with all the working in accordance to IFRS. Hence, for the effective recording of the convertible

bonds the company will be recoding them on the basis of fair value only. This is pertaining to the

fact that in case of the five- year convertible bond the conversion of the bond into shares will be

raking place on the fair value only that is the rate prevailing at the time of conversion. Along

with this in the other case, of lease agreement, the recording of the transaction will be taking

place on basis of IFRS 16. This IFRS states that how the accounting for the lease will be done

and all the decision relating to the lease will be involved during the accounting period (Morales

Díaz and Zamora Ramírez, 2018). In the present case of Tent Plc, the lease agreement will have

made on the basis of five -year account. This is pertaining to the fact that the lease agreement is

for five years and no ownership is being transferred. In the case of Tent plc, the right to use the

asset will be recorded within the books of account. Hence, for this all the payment made to lessor

at, before and commencement date will be recorded. Along with this, all the initial direct cost

incurred by the lessee will also be recorded within the books of account along with depreciation.

B

The fair value accounting is being referred to as measuring the business assets and

liabilities at the current market value. On the other hand, the historical cost accounting is a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

measure of value which involves the use of original cost for recording the asset of the company.

Both the methods have their own distinct benefits and drawback of being used (Georgiou, 2018).

The major benefit of using the fair value accounting is that it provides more accurate value for

the asset and liabilities of the company. the reason pertaining to the fact is that when the fair

value is used then the assets and liabilities are recorded on basis of market value and not at the

value on which it was acquired. So this provides for better and effective valuation of the asset

and provides for fair value. In addition to this another benefit of using fair value method is that it

provides the true income of the company. this is basically because of the reason that all the

elements are recorded at fair value so it provides accurate and true income.

On the other hand, the major drawback of using the fair value method is that this might

create much ups and down within the value of asset and liabilities (Yao, and et.al., 2018). This is

pertaining to the fact that fair value is based on market condition and there is no stability within

the market condition.

In against of this, the historical cost is beneficial for the company is

that it provides for consistency and comparability of the financial

statements. On the other hand, the major drawback of using the historical

accounting is that there are many different types of changes which can be

seen within the asset like usage, depreciation, machinery damages and

many other different aspects (Druzhilovskaya, 2018). In the case of historical

cost is the asset or liability is recorded at the original cost only which does

not provide actual working.

Both the methods have their own distinct benefits and drawback of being used (Georgiou, 2018).

The major benefit of using the fair value accounting is that it provides more accurate value for

the asset and liabilities of the company. the reason pertaining to the fact is that when the fair

value is used then the assets and liabilities are recorded on basis of market value and not at the

value on which it was acquired. So this provides for better and effective valuation of the asset

and provides for fair value. In addition to this another benefit of using fair value method is that it

provides the true income of the company. this is basically because of the reason that all the

elements are recorded at fair value so it provides accurate and true income.

On the other hand, the major drawback of using the fair value method is that this might

create much ups and down within the value of asset and liabilities (Yao, and et.al., 2018). This is

pertaining to the fact that fair value is based on market condition and there is no stability within

the market condition.

In against of this, the historical cost is beneficial for the company is

that it provides for consistency and comparability of the financial

statements. On the other hand, the major drawback of using the historical

accounting is that there are many different types of changes which can be

seen within the asset like usage, depreciation, machinery damages and

many other different aspects (Druzhilovskaya, 2018). In the case of historical

cost is the asset or liability is recorded at the original cost only which does

not provide actual working.

REFERENCES

Books and Journals

Georgiou, O., 2018. The worth of fair value accounting: dissonance between users and standard

setters. Contemporary Accounting Research. 35(3). pp.1297-1331.

Yao, D., and et.al., 2018. Fair value accounting and earnings persistence: evidence from

international banks. Journal of International Accounting Research. 17(1). pp.47-68.

Druzhilovskaya, T.Y., 2018. The use of fair value to measure accounting items: Practical

issues. Mezhdunarodnyi bukhgalterskii uchet= International Accounting. 21(9). pp.1086-

1099.

Yusuf, Y. and Idris, S., 2021. An Analysis of the Strengths and Weaknesses of Fair Value

Accounting and Historical Cost Accounting Measures. Asian Journal of Economics,

Finance and Management, pp.73-79.

Berisha, V. and Asllanaj, R., 2017. Literature Review on Historical Development of

Accounting. Acta Universitatis Danubius. Œconomica. 13(6).

Morales Díaz, J. and Zamora Ramírez, C., 2018. IFRS 16 (leases) implementation: Impact of

entities’ decisions on financial statements. Aestimatio: The IEB International Journal of

Finance. 17. 60-97.

Nitani, M., Riding, A. and He, B., 2019. On equity crowdfunding: investor rationality and

success factors. Venture Capital. 21(2-3). pp.243-272.

Books and Journals

Georgiou, O., 2018. The worth of fair value accounting: dissonance between users and standard

setters. Contemporary Accounting Research. 35(3). pp.1297-1331.

Yao, D., and et.al., 2018. Fair value accounting and earnings persistence: evidence from

international banks. Journal of International Accounting Research. 17(1). pp.47-68.

Druzhilovskaya, T.Y., 2018. The use of fair value to measure accounting items: Practical

issues. Mezhdunarodnyi bukhgalterskii uchet= International Accounting. 21(9). pp.1086-

1099.

Yusuf, Y. and Idris, S., 2021. An Analysis of the Strengths and Weaknesses of Fair Value

Accounting and Historical Cost Accounting Measures. Asian Journal of Economics,

Finance and Management, pp.73-79.

Berisha, V. and Asllanaj, R., 2017. Literature Review on Historical Development of

Accounting. Acta Universitatis Danubius. Œconomica. 13(6).

Morales Díaz, J. and Zamora Ramírez, C., 2018. IFRS 16 (leases) implementation: Impact of

entities’ decisions on financial statements. Aestimatio: The IEB International Journal of

Finance. 17. 60-97.

Nitani, M., Riding, A. and He, B., 2019. On equity crowdfunding: investor rationality and

success factors. Venture Capital. 21(2-3). pp.243-272.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.