Analysis of Scholastic Corp's 2012 Financial Statements

VerifiedAdded on 2023/06/03

|8

|1935

|440

Homework Assignment

AI Summary

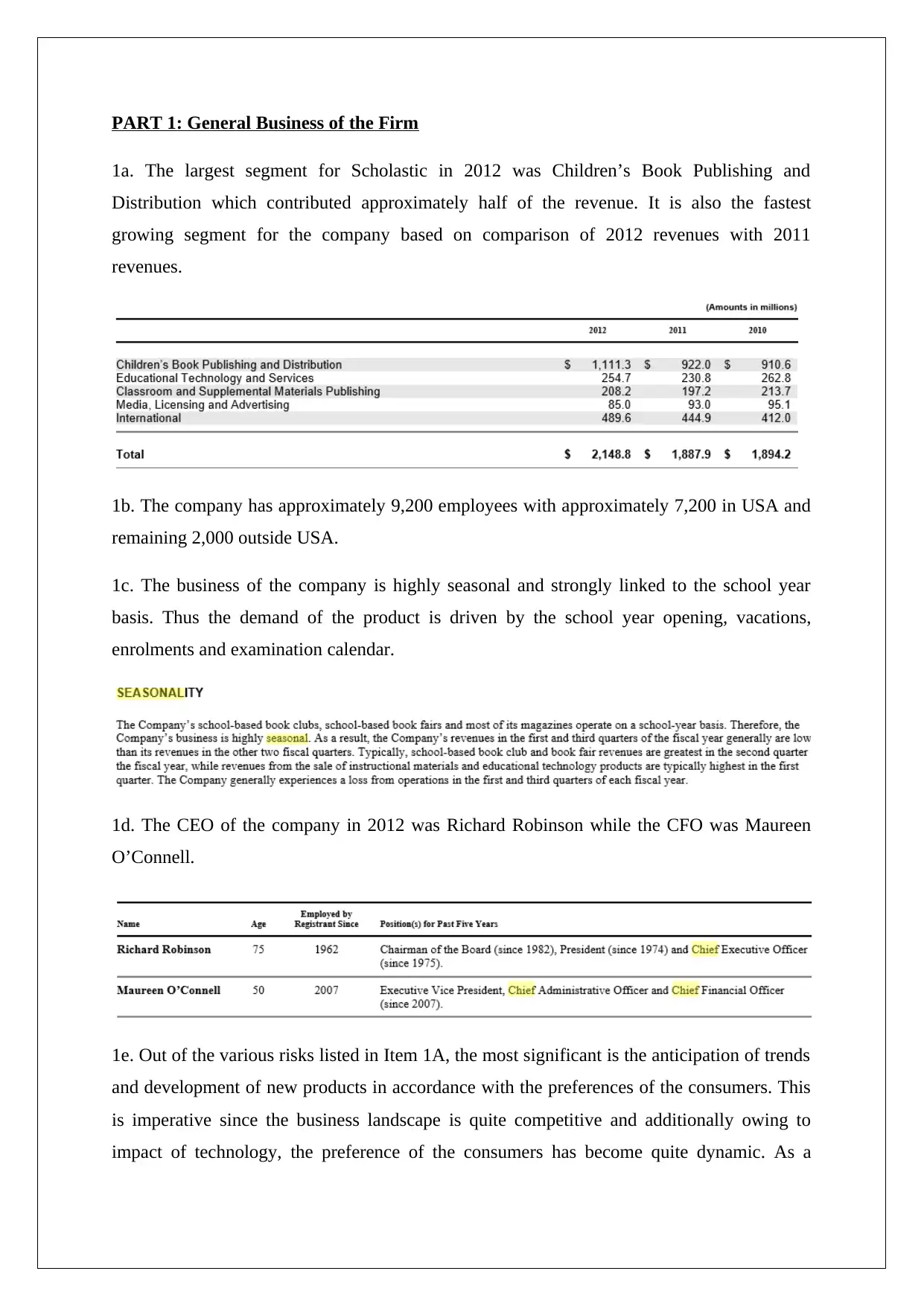

This assignment provides a comprehensive financial analysis of Scholastic Corporation based on its 2012 Form 10-K report, with comparative data from Wiley & Sons. It covers various aspects including the company's business segments, revenue analysis, balance sheet, income statement, and statement of cash flows. The analysis includes calculations of financial ratios such as net asset turnover and average collection period, along with explanations of accounting treatments for items like depreciation, accounts receivable, and revenue recognition policies. Risks associated with the business and the impact of potential estimation errors are also discussed. The assignment leverages information directly from the 10-K filings to provide detailed insights into Scholastic's financial performance and position.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.