Comprehensive Financial Analysis of Tesco for Potential Investors

VerifiedAdded on 2023/06/13

|8

|2075

|424

Report

AI Summary

This report provides a detailed financial analysis of Tesco, a FTSE350 constituent, aimed at potential investors. It interprets Tesco's income statement, balance sheet, and cash flow statement, evaluating profitability through ratios like net profit margin and ROCE. The analysis extends to dividend distribution, asset and liability values, and cash flow liquidity. Key findings include a high dividend payout ratio in 2021, indicating a focus on short-term share price boosts, and liquidity ratios suggesting potential short-term cash flow issues. Despite a decline in some performance metrics compared to the previous year, the report concludes that Tesco remains a potentially attractive investment due to improved net earnings and future growth prospects, as reflected in investor willingness to pay more for the company's shares. The report references various financial analysis resources to support its findings.

A REPORT FOR

POTENTIAL INVESTORS

OF THE COMPANY

(TESCO)

Table of Contents

POTENTIAL INVESTORS

OF THE COMPANY

(TESCO)

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Basic interpretation of Tesco's financial statements....................................................................3

Profitability analysis of Tesco.....................................................................................................4

Analysis of Dividend distribution................................................................................................5

Analysis of value of assets and liabilities....................................................................................6

Analysis of cash flow of the company.........................................................................................6

Attractiveness of the company as future investment alternative.................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................1

MAIN BODY...................................................................................................................................3

Basic interpretation of Tesco's financial statements....................................................................3

Profitability analysis of Tesco.....................................................................................................4

Analysis of Dividend distribution................................................................................................5

Analysis of value of assets and liabilities....................................................................................6

Analysis of cash flow of the company.........................................................................................6

Attractiveness of the company as future investment alternative.................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................1

INTRODUCTION

The present report is based on Tesco, a publicly listed company which is also a

constituent of FTSE350 index. Tesco is a supermarket giant based in UK. The report will analyse

financial statements of the company which involves balance sheet, income statement and cash

flow statement. Whatever information will be gathered from these financial statements, the

analysis of company's profitability, dividend distribution, value of assets and liabilities and cash

flows will be done. Furthermore, as the report is meant for potential investors, with the help of

evaluation of company's share, potential investment opportunities will be identified for

suggesting future investment alternative.

MAIN BODY

Basic interpretation of Tesco's financial statements

Interpretation of income statement

In the year 2021, Tesco has generated £57887 million which cost around £53538 million

to attain these sales and accordingly, a gross profit amounted to £3965 million has been earned

by the company. The gross profit figures for the current year are less than what has been

achieved in the year 2020 that is, £58091 million sales has been generated against the cost of

£53810 million and as a result, gross profit of £4098 million has been earned by the company in

previous (Vernimmen, Quiry and Le Fur, 2022).

By reducing the administrative expenses amounted to 2229 million in 2021 and 1892 in

2020, operating profit of £1736 million and £2206 million has been obtained for both the years

respectively. From this operating income, non-operating expenses such as finance cost (£952

million) and non-operating income such as finance income (£41 million) has been subtracted and

added to the operation income to get profitability of the company before tax that is, £825 million

for the year 2021 (Benrqya and Jabbouri, 2021). Furthermore, tax expenses borne by the

company amounted to £105 million has been subtracted from profit before tax in order to arrive

at profit from continuing operations which came out as £721 million. At last, by adjusting the

profit and loss from discontinued operations that is, profit of £5426 million, the net income of the

company came out as £6147 million for the year 2021.

Interpretation of Balance sheet

The balance that is taken into consideration is related to the reporting period ended on 27th

February 2021 where comparison has been done with the similar reporting periods which came

The present report is based on Tesco, a publicly listed company which is also a

constituent of FTSE350 index. Tesco is a supermarket giant based in UK. The report will analyse

financial statements of the company which involves balance sheet, income statement and cash

flow statement. Whatever information will be gathered from these financial statements, the

analysis of company's profitability, dividend distribution, value of assets and liabilities and cash

flows will be done. Furthermore, as the report is meant for potential investors, with the help of

evaluation of company's share, potential investment opportunities will be identified for

suggesting future investment alternative.

MAIN BODY

Basic interpretation of Tesco's financial statements

Interpretation of income statement

In the year 2021, Tesco has generated £57887 million which cost around £53538 million

to attain these sales and accordingly, a gross profit amounted to £3965 million has been earned

by the company. The gross profit figures for the current year are less than what has been

achieved in the year 2020 that is, £58091 million sales has been generated against the cost of

£53810 million and as a result, gross profit of £4098 million has been earned by the company in

previous (Vernimmen, Quiry and Le Fur, 2022).

By reducing the administrative expenses amounted to 2229 million in 2021 and 1892 in

2020, operating profit of £1736 million and £2206 million has been obtained for both the years

respectively. From this operating income, non-operating expenses such as finance cost (£952

million) and non-operating income such as finance income (£41 million) has been subtracted and

added to the operation income to get profitability of the company before tax that is, £825 million

for the year 2021 (Benrqya and Jabbouri, 2021). Furthermore, tax expenses borne by the

company amounted to £105 million has been subtracted from profit before tax in order to arrive

at profit from continuing operations which came out as £721 million. At last, by adjusting the

profit and loss from discontinued operations that is, profit of £5426 million, the net income of the

company came out as £6147 million for the year 2021.

Interpretation of Balance sheet

The balance that is taken into consideration is related to the reporting period ended on 27th

February 2021 where comparison has been done with the similar reporting periods which came

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

prior to the current report period that is, 29 February 2020 and 23 February 2019 (Lokanan,

2021).

The total assets of the company has been identified as £45778 million which include

current assets and non-current assets amounted to £10807 million and £34971 million

respectively. On the other side, total liabilities of the company for the period ended 27th February

2021 has been identified as £33177 million, of which £15721 million belongs to current

liabilities and £17456 million belongs to non-current liabilities. Further, equity of the company is

constant from past three periods that is, 2019, 2020 and 2021 amounted to £490 million (Ren,

2021). However, retained earnings of the company has shown downfall continuously from last

three years that is, £4147 million to £4078 million to £3505 million in 2019, 2020 and 2021

respectively.

Interpretation of cash flow statement

The cash flow statement of the company shows that in the beginning, the company has £3031

million in hand as cash and cash equivalents.

Overall cash flows are derived through various activities which has been categorized into

three major categories that is, cash flow from operating activities, investing activities and

financing activities. Accordingly, the cash flow statement depicts that £602 million has been

brought into the business through the company's core operating activities. It is a better indicator

that net income derived from income statement because the latter includes non-cash earnings

which cannot be used for paying bills or debt that is outstanding (Lakshmi, 2021). Moreover,

investing activities has also generated a cash inflow of £6171 million which shows sales of

outdated assets of the business. Further, it has been found that the company has spent £7841

million towards it financing activities in which investors are usually interested in because it

indicates confidence of the company that is, whether the company is confident in its stock's

performance or it is dependent on its dividends for gaining investor's attention.

As a result, net decrease in cash flow of the company at the year-end amounts to £1068

million and the balance with the company at reporting date was £1978 million.

Profitability analysis of Tesco

With the help of following ratios, profitability of the company will be determined.

Ratios Formula 2020 2021

2021).

The total assets of the company has been identified as £45778 million which include

current assets and non-current assets amounted to £10807 million and £34971 million

respectively. On the other side, total liabilities of the company for the period ended 27th February

2021 has been identified as £33177 million, of which £15721 million belongs to current

liabilities and £17456 million belongs to non-current liabilities. Further, equity of the company is

constant from past three periods that is, 2019, 2020 and 2021 amounted to £490 million (Ren,

2021). However, retained earnings of the company has shown downfall continuously from last

three years that is, £4147 million to £4078 million to £3505 million in 2019, 2020 and 2021

respectively.

Interpretation of cash flow statement

The cash flow statement of the company shows that in the beginning, the company has £3031

million in hand as cash and cash equivalents.

Overall cash flows are derived through various activities which has been categorized into

three major categories that is, cash flow from operating activities, investing activities and

financing activities. Accordingly, the cash flow statement depicts that £602 million has been

brought into the business through the company's core operating activities. It is a better indicator

that net income derived from income statement because the latter includes non-cash earnings

which cannot be used for paying bills or debt that is outstanding (Lakshmi, 2021). Moreover,

investing activities has also generated a cash inflow of £6171 million which shows sales of

outdated assets of the business. Further, it has been found that the company has spent £7841

million towards it financing activities in which investors are usually interested in because it

indicates confidence of the company that is, whether the company is confident in its stock's

performance or it is dependent on its dividends for gaining investor's attention.

As a result, net decrease in cash flow of the company at the year-end amounts to £1068

million and the balance with the company at reporting date was £1978 million.

Profitability analysis of Tesco

With the help of following ratios, profitability of the company will be determined.

Ratios Formula 2020 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

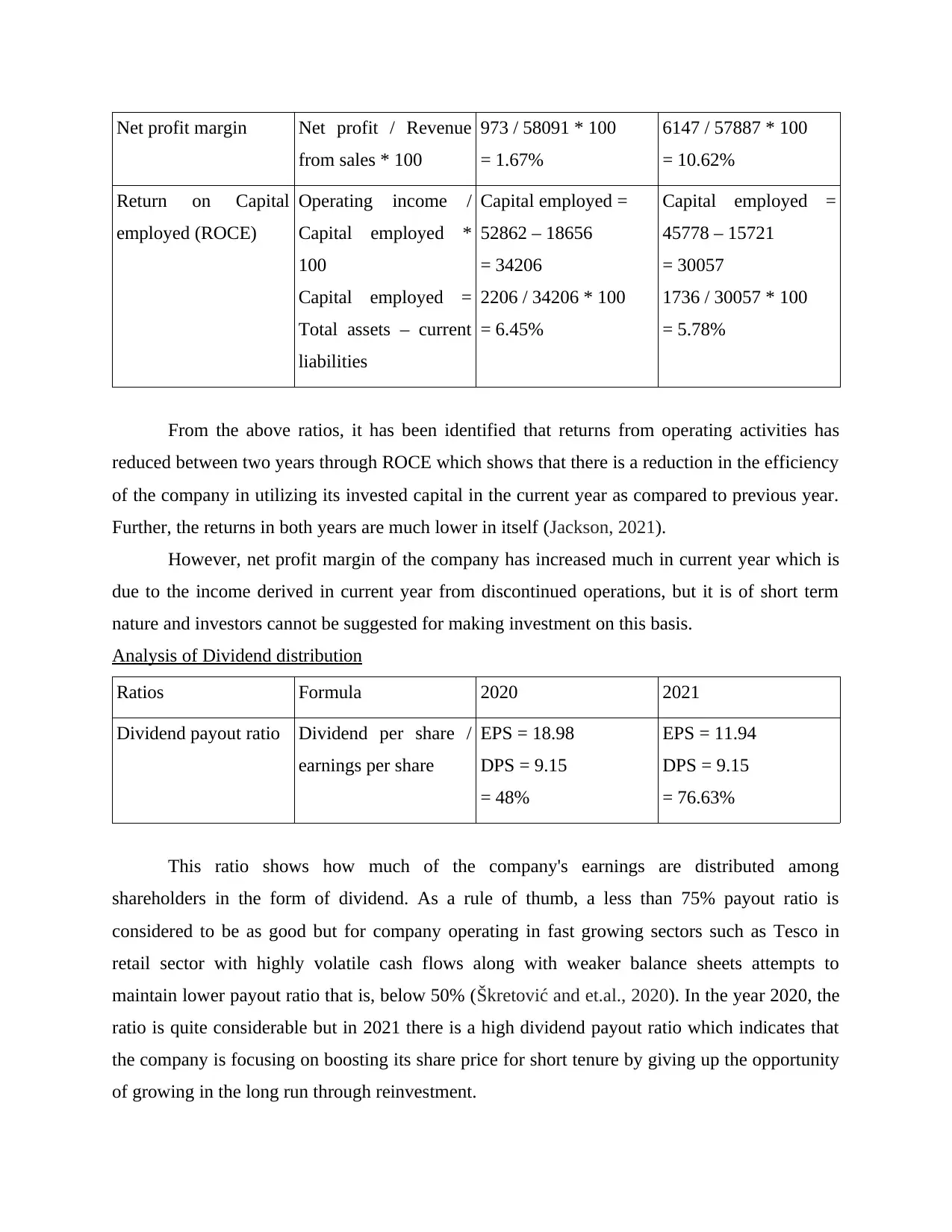

Net profit margin Net profit / Revenue

from sales * 100

973 / 58091 * 100

= 1.67%

6147 / 57887 * 100

= 10.62%

Return on Capital

employed (ROCE)

Operating income /

Capital employed *

100

Capital employed =

Total assets – current

liabilities

Capital employed =

52862 – 18656

= 34206

2206 / 34206 * 100

= 6.45%

Capital employed =

45778 – 15721

= 30057

1736 / 30057 * 100

= 5.78%

From the above ratios, it has been identified that returns from operating activities has

reduced between two years through ROCE which shows that there is a reduction in the efficiency

of the company in utilizing its invested capital in the current year as compared to previous year.

Further, the returns in both years are much lower in itself (Jackson, 2021).

However, net profit margin of the company has increased much in current year which is

due to the income derived in current year from discontinued operations, but it is of short term

nature and investors cannot be suggested for making investment on this basis.

Analysis of Dividend distribution

Ratios Formula 2020 2021

Dividend payout ratio Dividend per share /

earnings per share

EPS = 18.98

DPS = 9.15

= 48%

EPS = 11.94

DPS = 9.15

= 76.63%

This ratio shows how much of the company's earnings are distributed among

shareholders in the form of dividend. As a rule of thumb, a less than 75% payout ratio is

considered to be as good but for company operating in fast growing sectors such as Tesco in

retail sector with highly volatile cash flows along with weaker balance sheets attempts to

maintain lower payout ratio that is, below 50% (Škretović and et.al., 2020). In the year 2020, the

ratio is quite considerable but in 2021 there is a high dividend payout ratio which indicates that

the company is focusing on boosting its share price for short tenure by giving up the opportunity

of growing in the long run through reinvestment.

from sales * 100

973 / 58091 * 100

= 1.67%

6147 / 57887 * 100

= 10.62%

Return on Capital

employed (ROCE)

Operating income /

Capital employed *

100

Capital employed =

Total assets – current

liabilities

Capital employed =

52862 – 18656

= 34206

2206 / 34206 * 100

= 6.45%

Capital employed =

45778 – 15721

= 30057

1736 / 30057 * 100

= 5.78%

From the above ratios, it has been identified that returns from operating activities has

reduced between two years through ROCE which shows that there is a reduction in the efficiency

of the company in utilizing its invested capital in the current year as compared to previous year.

Further, the returns in both years are much lower in itself (Jackson, 2021).

However, net profit margin of the company has increased much in current year which is

due to the income derived in current year from discontinued operations, but it is of short term

nature and investors cannot be suggested for making investment on this basis.

Analysis of Dividend distribution

Ratios Formula 2020 2021

Dividend payout ratio Dividend per share /

earnings per share

EPS = 18.98

DPS = 9.15

= 48%

EPS = 11.94

DPS = 9.15

= 76.63%

This ratio shows how much of the company's earnings are distributed among

shareholders in the form of dividend. As a rule of thumb, a less than 75% payout ratio is

considered to be as good but for company operating in fast growing sectors such as Tesco in

retail sector with highly volatile cash flows along with weaker balance sheets attempts to

maintain lower payout ratio that is, below 50% (Škretović and et.al., 2020). In the year 2020, the

ratio is quite considerable but in 2021 there is a high dividend payout ratio which indicates that

the company is focusing on boosting its share price for short tenure by giving up the opportunity

of growing in the long run through reinvestment.

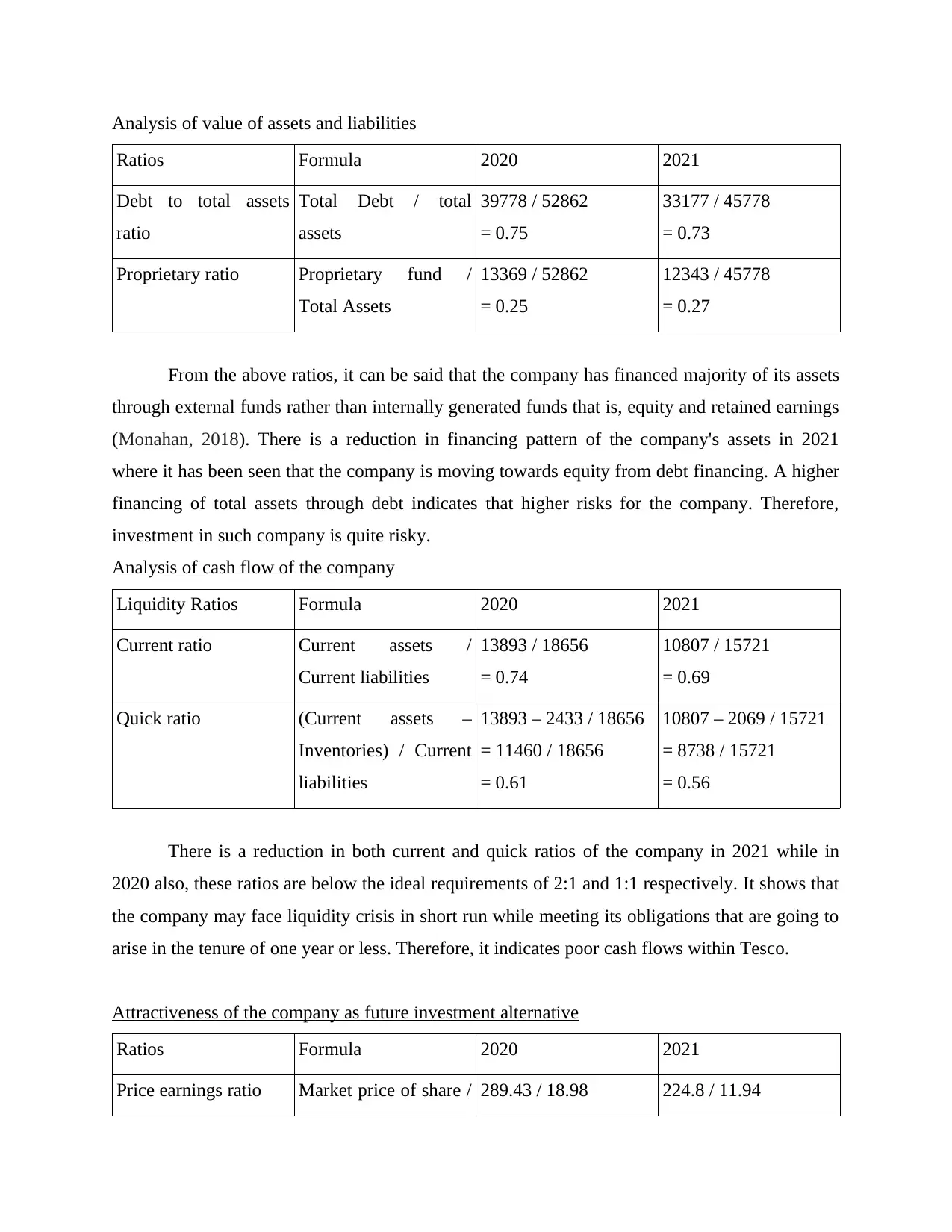

Analysis of value of assets and liabilities

Ratios Formula 2020 2021

Debt to total assets

ratio

Total Debt / total

assets

39778 / 52862

= 0.75

33177 / 45778

= 0.73

Proprietary ratio Proprietary fund /

Total Assets

13369 / 52862

= 0.25

12343 / 45778

= 0.27

From the above ratios, it can be said that the company has financed majority of its assets

through external funds rather than internally generated funds that is, equity and retained earnings

(Monahan, 2018). There is a reduction in financing pattern of the company's assets in 2021

where it has been seen that the company is moving towards equity from debt financing. A higher

financing of total assets through debt indicates that higher risks for the company. Therefore,

investment in such company is quite risky.

Analysis of cash flow of the company

Liquidity Ratios Formula 2020 2021

Current ratio Current assets /

Current liabilities

13893 / 18656

= 0.74

10807 / 15721

= 0.69

Quick ratio (Current assets –

Inventories) / Current

liabilities

13893 – 2433 / 18656

= 11460 / 18656

= 0.61

10807 – 2069 / 15721

= 8738 / 15721

= 0.56

There is a reduction in both current and quick ratios of the company in 2021 while in

2020 also, these ratios are below the ideal requirements of 2:1 and 1:1 respectively. It shows that

the company may face liquidity crisis in short run while meeting its obligations that are going to

arise in the tenure of one year or less. Therefore, it indicates poor cash flows within Tesco.

Attractiveness of the company as future investment alternative

Ratios Formula 2020 2021

Price earnings ratio Market price of share / 289.43 / 18.98 224.8 / 11.94

Ratios Formula 2020 2021

Debt to total assets

ratio

Total Debt / total

assets

39778 / 52862

= 0.75

33177 / 45778

= 0.73

Proprietary ratio Proprietary fund /

Total Assets

13369 / 52862

= 0.25

12343 / 45778

= 0.27

From the above ratios, it can be said that the company has financed majority of its assets

through external funds rather than internally generated funds that is, equity and retained earnings

(Monahan, 2018). There is a reduction in financing pattern of the company's assets in 2021

where it has been seen that the company is moving towards equity from debt financing. A higher

financing of total assets through debt indicates that higher risks for the company. Therefore,

investment in such company is quite risky.

Analysis of cash flow of the company

Liquidity Ratios Formula 2020 2021

Current ratio Current assets /

Current liabilities

13893 / 18656

= 0.74

10807 / 15721

= 0.69

Quick ratio (Current assets –

Inventories) / Current

liabilities

13893 – 2433 / 18656

= 11460 / 18656

= 0.61

10807 – 2069 / 15721

= 8738 / 15721

= 0.56

There is a reduction in both current and quick ratios of the company in 2021 while in

2020 also, these ratios are below the ideal requirements of 2:1 and 1:1 respectively. It shows that

the company may face liquidity crisis in short run while meeting its obligations that are going to

arise in the tenure of one year or less. Therefore, it indicates poor cash flows within Tesco.

Attractiveness of the company as future investment alternative

Ratios Formula 2020 2021

Price earnings ratio Market price of share / 289.43 / 18.98 224.8 / 11.94

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Earnings per share = 15.25 = 18.83

P/E ratio indicates the willingness of market to pay for company's share on the basis of its

past or potentiality of future earnings (Robinson, 2020). A high ratio indicates overvaluation of

company's stock where stock price is higher than the earnings the company is capable of

generating. A low ratio in 2020 indicates undervaluation of stock with regard to company's

ability to generate returns for its shareholders. Also, high ratio indicates better growth prospects

from the investment made in the company. Accordingly, it could be suggested on the basis of

this ratio that investors could go for investing in this company for the growth of their wealth.

CONCLUSION

From the above report, it has been concluded that Tesco is a good avenue for making

investment in it, however there is a decline in company's performance as compared to previous

year which is because of pandemic and other factors such as growing competition. Net earnings

of the company has improved in current year along with higher opportunities available in terms

of future benefits that the investor would be able to drive as the company has better growth

prospects as indicated through investor's willingness to pay more.

P/E ratio indicates the willingness of market to pay for company's share on the basis of its

past or potentiality of future earnings (Robinson, 2020). A high ratio indicates overvaluation of

company's stock where stock price is higher than the earnings the company is capable of

generating. A low ratio in 2020 indicates undervaluation of stock with regard to company's

ability to generate returns for its shareholders. Also, high ratio indicates better growth prospects

from the investment made in the company. Accordingly, it could be suggested on the basis of

this ratio that investors could go for investing in this company for the growth of their wealth.

CONCLUSION

From the above report, it has been concluded that Tesco is a good avenue for making

investment in it, however there is a decline in company's performance as compared to previous

year which is because of pandemic and other factors such as growing competition. Net earnings

of the company has improved in current year along with higher opportunities available in terms

of future benefits that the investor would be able to drive as the company has better growth

prospects as indicated through investor's willingness to pay more.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Monahan, S. J., 2018. Financial statement analysis and earnings forecasting. Foundations and

Trends® in Accounting, 12(2), pp.105-215.

Jackson, A. B., 2021. Financial statement analysis: a review and current issues. China Finance

Review International.

Lakshmi, S. V., 2021. Financial Statement Analysis of Tata Consultancy Services Limited. IUP

Journal of Accounting Research & Audit Practices, 20(4), pp.515-521.

Lokanan, M., 2021. Applying Four Quantitative Prediction Techniques to Detect Fraud in

Financial Statements. Journal of Forensic and Investigative Accounting, 13(2).

Ren, J., 2021, December. The Research of Tesco’s Current Investment Portfolio and Some

Recommendations. In 2021 3rd International Conference on Economic Management

and Cultural Industry (ICEMCI 2021) (pp. 1461-1465). Atlantis Press.

Benrqya, Y. and Jabbouri, I., 2021. Performance evaluation of European grocery retailers: a

financial statement analysis. International Journal of Logistics Economics and

Globalisation, 9(1), pp.24-39.

Vernimmen, P., Quiry, P. and Le Fur, Y., 2022. Corporate finance: theory and practice. John

Wiley & Sons.

Škretović, N., and et.al., 2020, May. FINANCIAL ANALYSIS IMPLICATIONS FROM

CORPORATE MANAGEMENT BASIS. In EASTERN EUROPEAN CONFERENCE

OF MANAGEMENT AND ECONOMICS (p. 99).

1

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Monahan, S. J., 2018. Financial statement analysis and earnings forecasting. Foundations and

Trends® in Accounting, 12(2), pp.105-215.

Jackson, A. B., 2021. Financial statement analysis: a review and current issues. China Finance

Review International.

Lakshmi, S. V., 2021. Financial Statement Analysis of Tata Consultancy Services Limited. IUP

Journal of Accounting Research & Audit Practices, 20(4), pp.515-521.

Lokanan, M., 2021. Applying Four Quantitative Prediction Techniques to Detect Fraud in

Financial Statements. Journal of Forensic and Investigative Accounting, 13(2).

Ren, J., 2021, December. The Research of Tesco’s Current Investment Portfolio and Some

Recommendations. In 2021 3rd International Conference on Economic Management

and Cultural Industry (ICEMCI 2021) (pp. 1461-1465). Atlantis Press.

Benrqya, Y. and Jabbouri, I., 2021. Performance evaluation of European grocery retailers: a

financial statement analysis. International Journal of Logistics Economics and

Globalisation, 9(1), pp.24-39.

Vernimmen, P., Quiry, P. and Le Fur, Y., 2022. Corporate finance: theory and practice. John

Wiley & Sons.

Škretović, N., and et.al., 2020, May. FINANCIAL ANALYSIS IMPLICATIONS FROM

CORPORATE MANAGEMENT BASIS. In EASTERN EUROPEAN CONFERENCE

OF MANAGEMENT AND ECONOMICS (p. 99).

1

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.