A Comparative Analysis of Traditional and Activity-Based Costing

VerifiedAdded on 2023/06/11

|11

|2229

|346

Report

AI Summary

This report provides a comprehensive analysis of traditional costing methods versus activity-based costing (ABC). It examines the problems associated with traditional costing in modern manufacturing environments, where overhead allocation based on volume-driven cost drivers can lead to inaccuracies. The report highlights the benefits of adopting ABC, including more accurate product costing, better identification of cost drivers, and improved waste reduction. However, it also acknowledges the limitations of ABC, such as its complexity and the potential for over-concentration on process control. The analysis includes a practical application comparing the costs of basic and advanced telephone systems using both departmental rates and ABC. Ultimately, the report recommends that contemporary manufacturing entities adopt ABC systems for more accurate overhead allocation and product pricing. Desklib provides access to this and other solved assignments to aid students in their studies.

Running head: INTRODUCTORY MANAGEMENT ACCOUNTING

Introductory management accounting

Name of the student

Name of the university

Student ID

Author note

Introductory management accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTRODUCTORY MANAGEMENT ACCOUNTING

Executive summary

The main objective of the report is to analyse the traditional costing approach and activity

based costing approach to pricing the product and allocating the overheads. The report will

also focus on various limitations and advantages associated with the traditional approach and

activity based costing. On the basis of these the appropriate costing approach will be

recommended.

Executive summary

The main objective of the report is to analyse the traditional costing approach and activity

based costing approach to pricing the product and allocating the overheads. The report will

also focus on various limitations and advantages associated with the traditional approach and

activity based costing. On the basis of these the appropriate costing approach will be

recommended.

2INTRODUCTORY MANAGEMENT ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Part I...........................................................................................................................................2

Problems related to traditional costing system in modern environment................................2

Benefits of adopting activity based costing...........................................................................2

Limitations of Activity based costing....................................................................................4

Conclusion and recommendation...............................................................................................4

Part II..........................................................................................................................................6

Answer 1................................................................................................................................6

Answer 2................................................................................................................................6

Answer 3................................................................................................................................7

Answer 4................................................................................................................................8

References..................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Part I...........................................................................................................................................2

Problems related to traditional costing system in modern environment................................2

Benefits of adopting activity based costing...........................................................................2

Limitations of Activity based costing....................................................................................4

Conclusion and recommendation...............................................................................................4

Part II..........................................................................................................................................6

Answer 1................................................................................................................................6

Answer 2................................................................................................................................6

Answer 3................................................................................................................................7

Answer 4................................................................................................................................8

References..................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTRODUCTORY MANAGEMENT ACCOUNTING

Introduction

Traditional cost approach allocates overheads on variable cost drivers like labour

hour, volume or production department are considered inappropriate. The traditional

approach used the cost driver that varies with the production volume. To be more specific as

per the traditional approach there is only one cost driver like labour hour, machine hour or

material requirement. On the other hand, Activity based costing (ABC) offers more accurate

costing method for product and services which in turn assists in accurate pricing decisions. It

takes into consideration all the activities included in the manufacturing system to allocate the

overheads (Coase, 2013).

Part I

Problems related to traditional costing system in modern environment

Allocation of overhead based on traditional cost approach that allocates overheads on

variable cost drivers like labour hour, volume or production department are considered

inappropriate. The traditional approach used the cost driver that varies with the production

volume. to be more specific as per the traditional approach there is only one cost driver like

labour hour, machine hour or material requirement However, in reality various other cost

drivers are there those are needs to be taken into consideration while allocating the overheads

to the products. The cost driver increases with the diversity in customer demands and the

problem increases with the allocation of overheads. Under the traditional approach costs

required for performing all diverse activities are included under single cost pool and are

segregated by number of machine hour or labour hour. This average rate is applied to all the

products irrespective of the activities numbers and complexities of the activities. As all the

activities do not correlate with the machine hours or labour hours the allocation are often

misleading (Dale & Plunkett, 2017).

Under the modern environment for manufacturing, the above mentioned problems

have been increased owing to increase of automation, increase in overhead cost and increase

of various costs. Due to using of the traditional approach the volume based data creates more

problems while the overhead are misallocated.

Introduction

Traditional cost approach allocates overheads on variable cost drivers like labour

hour, volume or production department are considered inappropriate. The traditional

approach used the cost driver that varies with the production volume. To be more specific as

per the traditional approach there is only one cost driver like labour hour, machine hour or

material requirement. On the other hand, Activity based costing (ABC) offers more accurate

costing method for product and services which in turn assists in accurate pricing decisions. It

takes into consideration all the activities included in the manufacturing system to allocate the

overheads (Coase, 2013).

Part I

Problems related to traditional costing system in modern environment

Allocation of overhead based on traditional cost approach that allocates overheads on

variable cost drivers like labour hour, volume or production department are considered

inappropriate. The traditional approach used the cost driver that varies with the production

volume. to be more specific as per the traditional approach there is only one cost driver like

labour hour, machine hour or material requirement However, in reality various other cost

drivers are there those are needs to be taken into consideration while allocating the overheads

to the products. The cost driver increases with the diversity in customer demands and the

problem increases with the allocation of overheads. Under the traditional approach costs

required for performing all diverse activities are included under single cost pool and are

segregated by number of machine hour or labour hour. This average rate is applied to all the

products irrespective of the activities numbers and complexities of the activities. As all the

activities do not correlate with the machine hours or labour hours the allocation are often

misleading (Dale & Plunkett, 2017).

Under the modern environment for manufacturing, the above mentioned problems

have been increased owing to increase of automation, increase in overhead cost and increase

of various costs. Due to using of the traditional approach the volume based data creates more

problems while the overhead are misallocated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTRODUCTORY MANAGEMENT ACCOUNTING

Benefits of adopting activity based costing

Activity based costing (ABC) offers more accurate costing method for product and

services which in turn assists in accurate pricing decisions. It further enables the users to have

clear idea regarding the cost drivers and overheads which in turn makes the non-value adding

services more visible that allows the managers reducing them or eliminating them.

Traditional costing is regarded as less accurate and simpler as compared to the ABC approach

and it allocates the overheads on the basis of any arbitrary average rate (Mitchell & Nørreklit,

2017). On the other hand, through the ABC approach is more complex it is more accurate as

compared to the traditional approach. Various benefits associated with adoption of ABC

approach by the contemporary manufacturing companies are as follows –

Broad averages – as per the traditional approach the costing are depended upon the

broad averages and the overheads are allocated based on the average rate taking into

consideration single cost driver like machine hour rate or labour rate. On the contrary,

the ABC approach takes into consideration all the cost drivers and allocates it based

on the usage (Frazier, 2014).

Under or over costing – as per the traditional approach the overheads are either over

absorbed or under absorbed as it uses average rate. However, through the ABC

approach the relation between products – costs – activities are clearer.

Customizations of product – previously, less number of products were there for the

product. However, with the improvement in technologies and customer’s demand lot

of variations are there for weight, colour, durability and design. Products with all

these variations are manufactured under same setup. ABC approach helps in refined

costing system which in turn assists in pricing the products accurately.

Identification of wastes – generally the overheads include some wasteful products. All

these wastes can be recognized very easily with the ABC approach and can be

removed accordingly from the production process or can be minimized, if removal is

not possible (Estampe et al., 2013).

Applicable to entire business – it can be seemed like the ABC approach is only useful

for allocation of products related overhead efficiently and effectively. However, in

reality all the overhead costs associated with the business can be reduced through

using the ABC approach.

Transfer pricing – if a product involves various processes the cost of manufacturing

involved in process 1, process 2 and so on are very clear through adopting the ABC

Benefits of adopting activity based costing

Activity based costing (ABC) offers more accurate costing method for product and

services which in turn assists in accurate pricing decisions. It further enables the users to have

clear idea regarding the cost drivers and overheads which in turn makes the non-value adding

services more visible that allows the managers reducing them or eliminating them.

Traditional costing is regarded as less accurate and simpler as compared to the ABC approach

and it allocates the overheads on the basis of any arbitrary average rate (Mitchell & Nørreklit,

2017). On the other hand, through the ABC approach is more complex it is more accurate as

compared to the traditional approach. Various benefits associated with adoption of ABC

approach by the contemporary manufacturing companies are as follows –

Broad averages – as per the traditional approach the costing are depended upon the

broad averages and the overheads are allocated based on the average rate taking into

consideration single cost driver like machine hour rate or labour rate. On the contrary,

the ABC approach takes into consideration all the cost drivers and allocates it based

on the usage (Frazier, 2014).

Under or over costing – as per the traditional approach the overheads are either over

absorbed or under absorbed as it uses average rate. However, through the ABC

approach the relation between products – costs – activities are clearer.

Customizations of product – previously, less number of products were there for the

product. However, with the improvement in technologies and customer’s demand lot

of variations are there for weight, colour, durability and design. Products with all

these variations are manufactured under same setup. ABC approach helps in refined

costing system which in turn assists in pricing the products accurately.

Identification of wastes – generally the overheads include some wasteful products. All

these wastes can be recognized very easily with the ABC approach and can be

removed accordingly from the production process or can be minimized, if removal is

not possible (Estampe et al., 2013).

Applicable to entire business – it can be seemed like the ABC approach is only useful

for allocation of products related overhead efficiently and effectively. However, in

reality all the overhead costs associated with the business can be reduced through

using the ABC approach.

Transfer pricing – if a product involves various processes the cost of manufacturing

involved in process 1, process 2 and so on are very clear through adopting the ABC

5INTRODUCTORY MANAGEMENT ACCOUNTING

approach as the overheads allocation are systematic. This helps in fixing the transfer

price of the product.

Limitations of Activity based costing

ABC approach assists the managers to manage the overhead costs and understanding

the product profitability and therefore it is considered as powerful tool for the purpose of

decision making. However, the ABC approach has various disadvantages or limitations as

follows –

Complexity – most prominent limitation of ABC approach is its nature. The

complexity involves with the ABC approach prevents the widespread application of

this approach. Further, this approach is costly to operate and comprehend to

implement. It requires the management estimating of cost associated with each

activity and recognise the cost driver for the activities. It also requires measuring the

costs and updating it on continuous basis. On the other hand, the traditional approach

uses the single cost driver to allocate the overheads and the implementation of ABC

system requires segregation of costs into various cost pools. It requires more amounts

of organizational resources like costs and management time (Scheaffer et al., 2013).

Assumptions – major limitation associated with ABC system is it involves complex

methodology white it is implemented and the actual system remains far away from

being perfect. Further, the overhead like CEO’s salary are not possible to segregate

and allocate on the basis of product usage. Further, all the costs are not required to be

allocated based on the manufacturing of product. For example, the employee who

takes part in the awareness campaign does not add any value to end product or the

service.

Big picture – major limitation associated with ABC is that it concentrates more on

controlling process. It leads to various limitations like the management lose the

concentration on other long – term strategic objectives for short or small savings in

the quarter. For example, ABC may recognize one channel for distribution as non-

remunerative while in reality this channel can be used to attain the strategic depth

rather than the profits (Subramaniam, & Watson, 2016).

Owing to the above mentioned limitations implementation of ABC system is impeded.

approach as the overheads allocation are systematic. This helps in fixing the transfer

price of the product.

Limitations of Activity based costing

ABC approach assists the managers to manage the overhead costs and understanding

the product profitability and therefore it is considered as powerful tool for the purpose of

decision making. However, the ABC approach has various disadvantages or limitations as

follows –

Complexity – most prominent limitation of ABC approach is its nature. The

complexity involves with the ABC approach prevents the widespread application of

this approach. Further, this approach is costly to operate and comprehend to

implement. It requires the management estimating of cost associated with each

activity and recognise the cost driver for the activities. It also requires measuring the

costs and updating it on continuous basis. On the other hand, the traditional approach

uses the single cost driver to allocate the overheads and the implementation of ABC

system requires segregation of costs into various cost pools. It requires more amounts

of organizational resources like costs and management time (Scheaffer et al., 2013).

Assumptions – major limitation associated with ABC system is it involves complex

methodology white it is implemented and the actual system remains far away from

being perfect. Further, the overhead like CEO’s salary are not possible to segregate

and allocate on the basis of product usage. Further, all the costs are not required to be

allocated based on the manufacturing of product. For example, the employee who

takes part in the awareness campaign does not add any value to end product or the

service.

Big picture – major limitation associated with ABC is that it concentrates more on

controlling process. It leads to various limitations like the management lose the

concentration on other long – term strategic objectives for short or small savings in

the quarter. For example, ABC may recognize one channel for distribution as non-

remunerative while in reality this channel can be used to attain the strategic depth

rather than the profits (Subramaniam, & Watson, 2016).

Owing to the above mentioned limitations implementation of ABC system is impeded.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTRODUCTORY MANAGEMENT ACCOUNTING

Conclusion and recommendation

From the above analysis it is concluded that traditional method of costing is simple

and it considers the single cost driver to allocate the overheads. On the contrary, the ABC

system takes into consideration all the cost drivers while allocating the overheads. However,

the ABC system is costlier and more complex to implement as compared to the traditional

approach. Though the ABC system is costlier and complex it has various advantages that

allow the management to accurate overhead allocation and fixing the price of the product.

Therefore, the contemporary manufacturing entities are recommended to adopt ABC system.

Conclusion and recommendation

From the above analysis it is concluded that traditional method of costing is simple

and it considers the single cost driver to allocate the overheads. On the contrary, the ABC

system takes into consideration all the cost drivers while allocating the overheads. However,

the ABC system is costlier and more complex to implement as compared to the traditional

approach. Though the ABC system is costlier and complex it has various advantages that

allow the management to accurate overhead allocation and fixing the price of the product.

Therefore, the contemporary manufacturing entities are recommended to adopt ABC system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTRODUCTORY MANAGEMENT ACCOUNTING

Part II

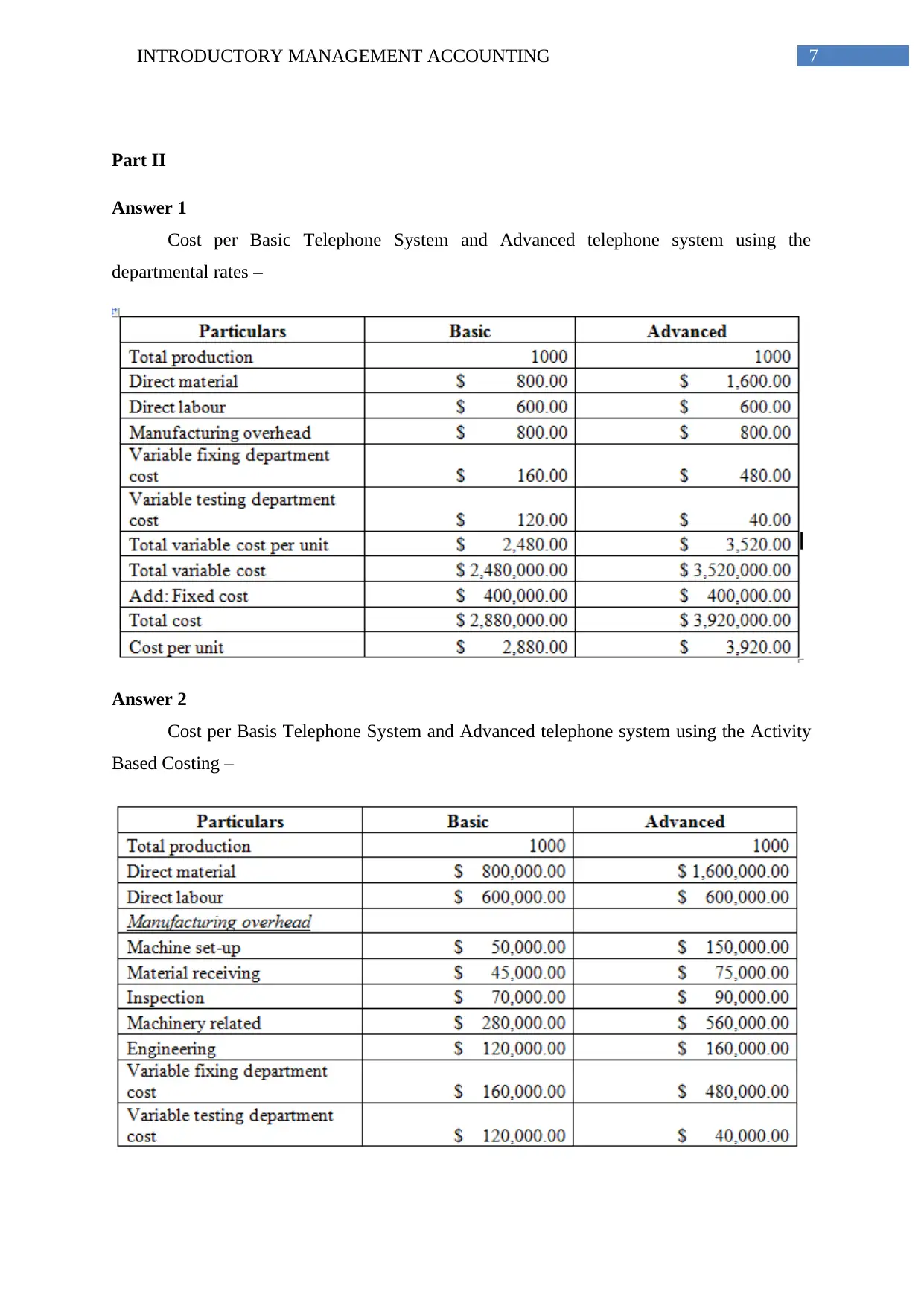

Answer 1

Cost per Basic Telephone System and Advanced telephone system using the

departmental rates –

Answer 2

Cost per Basis Telephone System and Advanced telephone system using the Activity

Based Costing –

Part II

Answer 1

Cost per Basic Telephone System and Advanced telephone system using the

departmental rates –

Answer 2

Cost per Basis Telephone System and Advanced telephone system using the Activity

Based Costing –

8INTRODUCTORY MANAGEMENT ACCOUNTING

Answer 3

Memo for management meeting

To: Management

From: Cost Analyst

Date: 2nd June 2018

Subject: Adoption of costing systems

This is to inform you that as per the requirement I have conducted the cost analysis as per the

traditional method as well the activity based costing systems. It has been identified that as per

the traditional method the cost per Basic telephone is $ 2,880 and cost per Advanced

telephone is $ 3,920. On the other hand, as per the activity based costing the cost per Basic

telephone is $ 2,645 and cost per Advanced telephone is $ 4,155.

It has been found that through the activity based costing is costlier and complex it has various

advantages that allow the management to accurate overhead allocation and fixing the price of

the product. On the contrary the traditional approach takes single cost driver to allocate the

overheads. Therefore, it is recommended that the ABC system will be most appropriate for

Singtel.

Answer 3

Memo for management meeting

To: Management

From: Cost Analyst

Date: 2nd June 2018

Subject: Adoption of costing systems

This is to inform you that as per the requirement I have conducted the cost analysis as per the

traditional method as well the activity based costing systems. It has been identified that as per

the traditional method the cost per Basic telephone is $ 2,880 and cost per Advanced

telephone is $ 3,920. On the other hand, as per the activity based costing the cost per Basic

telephone is $ 2,645 and cost per Advanced telephone is $ 4,155.

It has been found that through the activity based costing is costlier and complex it has various

advantages that allow the management to accurate overhead allocation and fixing the price of

the product. On the contrary the traditional approach takes single cost driver to allocate the

overheads. Therefore, it is recommended that the ABC system will be most appropriate for

Singtel.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTRODUCTORY MANAGEMENT ACCOUNTING

Answer 4

Implication of adopting traditional costing system

Under the traditional costing system overheads are allocated based on variable cost

drivers like labour hour, volume or production department. The traditional approach uses the

cost driver that varies with the production volume. to be more specific as per the traditional

approach there is only one cost driver like labour hour, machine hour or material requirement

However, in reality various other cost drivers are there those are needs to be taken into

consideration while allocating the overheads to the products (Drury, 2013). However, this is

used by the companies as it is simple, involves lower cost for implementation and less

complex as compared to ABC. The pricing decisions taken based on the traditional approach

are considered inappropriate as various cost drivers are not taken into consideration while

allocating the overheads.

Implication of adopting ABC system

ABC system enables the users to have clear idea regarding the cost drivers and

overheads as all the overheads are taken into consideration. Traditional costing is regarded as

less accurate and simpler as compared to the ABC approach as it allocates the overheads on

the basis of arbitrary average rate. On the other hand, though the ABC approach is more

complex it is more accurate as compared to the traditional approach (Hilton & Platt, 2013).

The pricing decisions taken based on the ABC approach are considered most appropriate as

all the cost drivers are taken into consideration while allocating the overheads.

Answer 4

Implication of adopting traditional costing system

Under the traditional costing system overheads are allocated based on variable cost

drivers like labour hour, volume or production department. The traditional approach uses the

cost driver that varies with the production volume. to be more specific as per the traditional

approach there is only one cost driver like labour hour, machine hour or material requirement

However, in reality various other cost drivers are there those are needs to be taken into

consideration while allocating the overheads to the products (Drury, 2013). However, this is

used by the companies as it is simple, involves lower cost for implementation and less

complex as compared to ABC. The pricing decisions taken based on the traditional approach

are considered inappropriate as various cost drivers are not taken into consideration while

allocating the overheads.

Implication of adopting ABC system

ABC system enables the users to have clear idea regarding the cost drivers and

overheads as all the overheads are taken into consideration. Traditional costing is regarded as

less accurate and simpler as compared to the ABC approach as it allocates the overheads on

the basis of arbitrary average rate. On the other hand, though the ABC approach is more

complex it is more accurate as compared to the traditional approach (Hilton & Platt, 2013).

The pricing decisions taken based on the ABC approach are considered most appropriate as

all the cost drivers are taken into consideration while allocating the overheads.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTRODUCTORY MANAGEMENT ACCOUNTING

References

Coase, R. H. (2013). The problem of social cost. The journal of Law and Economics, 56(4),

837-877.

Dale, B. G., & Plunkett, J. J. (2017). Quality costing. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Estampe, D., Lamouri, S., Paris, J. L., & Brahim-Djelloul, S. (2013). A framework for

analysing supply chain performance evaluation models. International Journal of

Production Economics, 142(2), 247-258.

Frazier, W. E. (2014). Metal additive manufacturing: a review. Journal of Materials

Engineering and Performance, 23(6), 1917-1928.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

MITCHELL, F., & NØRREKLIT, H. (2017). Introduction. In A Philosophy of Management

Accounting (pp. 15-34). Routledge.

Scheaffer, R. L., Witmer, J., Watkins, A., & Gnanadesikan, M. (2013). Activity-based

statistics: student guide. Springer Science & Business Media.

Subramaniam, C., & Watson, M. W. (2016). Additional evidence on the sticky behavior of

costs. In Advances in Management Accounting (pp. 275-305). Emerald Group

Publishing Limited.

References

Coase, R. H. (2013). The problem of social cost. The journal of Law and Economics, 56(4),

837-877.

Dale, B. G., & Plunkett, J. J. (2017). Quality costing. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Estampe, D., Lamouri, S., Paris, J. L., & Brahim-Djelloul, S. (2013). A framework for

analysing supply chain performance evaluation models. International Journal of

Production Economics, 142(2), 247-258.

Frazier, W. E. (2014). Metal additive manufacturing: a review. Journal of Materials

Engineering and Performance, 23(6), 1917-1928.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

MITCHELL, F., & NØRREKLIT, H. (2017). Introduction. In A Philosophy of Management

Accounting (pp. 15-34). Routledge.

Scheaffer, R. L., Witmer, J., Watkins, A., & Gnanadesikan, M. (2013). Activity-based

statistics: student guide. Springer Science & Business Media.

Subramaniam, C., & Watson, M. W. (2016). Additional evidence on the sticky behavior of

costs. In Advances in Management Accounting (pp. 275-305). Emerald Group

Publishing Limited.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.