Analysis of Wonga's Activities and Subsequent Collapse: An Essay

VerifiedAdded on 2022/09/13

|12

|2434

|35

Essay

AI Summary

This essay provides a detailed analysis of Wonga, a payday loan company that collapsed due to unethical business practices. The essay examines the company's history, the events leading to its downfall, and the ethical theories and objections that apply to the situation. It explores the ethical failures of Wonga, including high-interest loans, data breaches, and violations of Financial Conduct Authority (FCA) regulations. The analysis includes discussions of Utilitarianism, Justice theory, Psychological Egotism, and Legal-moralism. The essay also considers the impact on stakeholders, including customers, shareholders, and the economy. Furthermore, it reviews the regulations that Wonga violated and provides recommendations for preventing similar failures in the future, emphasizing the importance of ethical conduct and regulatory compliance in the financial sector. The essay concludes by highlighting the key takeaways from Wonga's collapse and the lessons it offers for businesses and regulators.

Running head: ANALYSIS OF WONGA

ANALYSIS OF WONGA

Name of Student

Name of the University

Author Notes

ANALYSIS OF WONGA

Name of Student

Name of the University

Author Notes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ANALYSIS OF WONGA

Executive summary

The purpose of the study is to analyses the condition of Wonga. Different ethical theories

such as Utilitarianism theory and Justice theory has been analyzed with ethical objections

such as Psychological Egotism and Legal-moralism. From the study, it has been found that

Wonga was unethically providing their customers with high interest loans, which resulted

into their collapse. It has been perceived that FCA protected the interest of the customers. It is

been also reported that Wonga has breached the data of their customers and violated the code

of conduct of their customers.

Executive summary

The purpose of the study is to analyses the condition of Wonga. Different ethical theories

such as Utilitarianism theory and Justice theory has been analyzed with ethical objections

such as Psychological Egotism and Legal-moralism. From the study, it has been found that

Wonga was unethically providing their customers with high interest loans, which resulted

into their collapse. It has been perceived that FCA protected the interest of the customers. It is

been also reported that Wonga has breached the data of their customers and violated the code

of conduct of their customers.

2ANALYSIS OF WONGA

Table of Contents

Introduction................................................................................................................................3

Ethics of the process...................................................................................................................4

Ethics applied to outcome..........................................................................................................5

Regulations.................................................................................................................................6

Factors........................................................................................................................................6

External view.............................................................................................................................7

Recommendation........................................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Ethics of the process...................................................................................................................4

Ethics applied to outcome..........................................................................................................5

Regulations.................................................................................................................................6

Factors........................................................................................................................................6

External view.............................................................................................................................7

Recommendation........................................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ANALYSIS OF WONGA

Introduction

Wonga was founded in 2006 by Errol Damelin and Jonathan Hurwitz and launched

their short term loan products. Wonga provides online loan services to the business. Payday

lender Wonga collapsed under the claims for rebates and compensation from its borrowers

(Brookes and Harvey 2017). Wonga collapsed on august 2018 with 200000 customers still

owing more than £400 million in short term loans. In 2014, FCA crackdown prompted Haste

to write off £220 million in debts and interest to 330000 customers (Hembruff and

Soederberg 2019). Just after things started in favour of Wonga, it emerged in august that the

payday lenders had to rescue it with £10 million capital injection. The debt crisis of Wonga

relates to the British debt crisis, which impacted the economy of the UK massively. This

happened as customers were asking for compensation claims from Wonga. The cap on

interest rates ruined the business model of Wonga, resulting in the collapse. Wonga was

targeting vulnerable borrowers with small loans which quickly got out of control and the

collapse happened. The fraud happened in the United Kingdom In the year 2018. After the

scam, the administration of Wonga decided to shut down their business from August 31 2018.

Internal stakeholders were involved in the scandal such as executives, chairman and

employees. The existing CEO left the company in 2013 as their financial condition was going

against them. Financial Conduct Authority stated that before shutting down, Wonga must pay

off their borrowers. The stakeholders requested their customers to continue to use their

services; however, it will not accept any new loan applications. FCA stated that Wonga has

several problems in their finance from the very beginning; however, they continued with the

problems, and the scandal happened. Andy Haste, the former CEO, said that they would

overcome this situation and make Wonga profitable again. The new cases of Wonga were

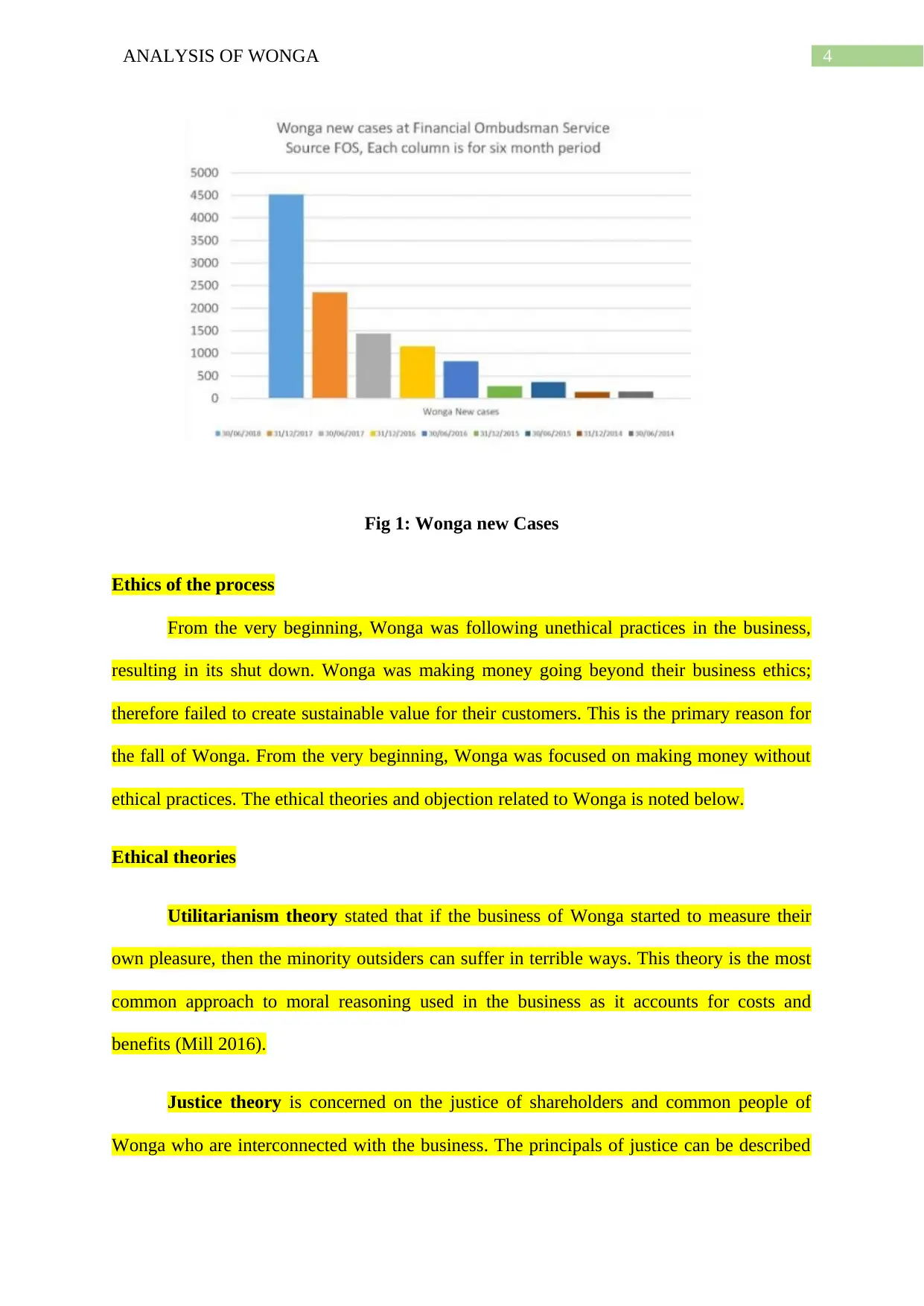

risking from 2014 and reached 4500 at the end of 2017 (Becker and Allayannis 2019).

Introduction

Wonga was founded in 2006 by Errol Damelin and Jonathan Hurwitz and launched

their short term loan products. Wonga provides online loan services to the business. Payday

lender Wonga collapsed under the claims for rebates and compensation from its borrowers

(Brookes and Harvey 2017). Wonga collapsed on august 2018 with 200000 customers still

owing more than £400 million in short term loans. In 2014, FCA crackdown prompted Haste

to write off £220 million in debts and interest to 330000 customers (Hembruff and

Soederberg 2019). Just after things started in favour of Wonga, it emerged in august that the

payday lenders had to rescue it with £10 million capital injection. The debt crisis of Wonga

relates to the British debt crisis, which impacted the economy of the UK massively. This

happened as customers were asking for compensation claims from Wonga. The cap on

interest rates ruined the business model of Wonga, resulting in the collapse. Wonga was

targeting vulnerable borrowers with small loans which quickly got out of control and the

collapse happened. The fraud happened in the United Kingdom In the year 2018. After the

scam, the administration of Wonga decided to shut down their business from August 31 2018.

Internal stakeholders were involved in the scandal such as executives, chairman and

employees. The existing CEO left the company in 2013 as their financial condition was going

against them. Financial Conduct Authority stated that before shutting down, Wonga must pay

off their borrowers. The stakeholders requested their customers to continue to use their

services; however, it will not accept any new loan applications. FCA stated that Wonga has

several problems in their finance from the very beginning; however, they continued with the

problems, and the scandal happened. Andy Haste, the former CEO, said that they would

overcome this situation and make Wonga profitable again. The new cases of Wonga were

risking from 2014 and reached 4500 at the end of 2017 (Becker and Allayannis 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ANALYSIS OF WONGA

Fig 1: Wonga new Cases

Ethics of the process

From the very beginning, Wonga was following unethical practices in the business,

resulting in its shut down. Wonga was making money going beyond their business ethics;

therefore failed to create sustainable value for their customers. This is the primary reason for

the fall of Wonga. From the very beginning, Wonga was focused on making money without

ethical practices. The ethical theories and objection related to Wonga is noted below.

Ethical theories

Utilitarianism theory stated that if the business of Wonga started to measure their

own pleasure, then the minority outsiders can suffer in terrible ways. This theory is the most

common approach to moral reasoning used in the business as it accounts for costs and

benefits (Mill 2016).

Justice theory is concerned on the justice of shareholders and common people of

Wonga who are interconnected with the business. The principals of justice can be described

Fig 1: Wonga new Cases

Ethics of the process

From the very beginning, Wonga was following unethical practices in the business,

resulting in its shut down. Wonga was making money going beyond their business ethics;

therefore failed to create sustainable value for their customers. This is the primary reason for

the fall of Wonga. From the very beginning, Wonga was focused on making money without

ethical practices. The ethical theories and objection related to Wonga is noted below.

Ethical theories

Utilitarianism theory stated that if the business of Wonga started to measure their

own pleasure, then the minority outsiders can suffer in terrible ways. This theory is the most

common approach to moral reasoning used in the business as it accounts for costs and

benefits (Mill 2016).

Justice theory is concerned on the justice of shareholders and common people of

Wonga who are interconnected with the business. The principals of justice can be described

5ANALYSIS OF WONGA

as a moral obligation to act based on fair adjudication between competing claims. Justice

theory states that in the business of Wonga, every individual should have equal right and

should be treated ethically (Sabbagh and Schmitt 2016).

Ethical objections

Psychological egoism is the view that human is always motivated by self-interest and

selfishness. It claims that if people or business is helping others, they do to fulfil their

personal benefits. This approach can be perceived from the analysis of Wonga as they were

primarily focused on self-interest rather than customers satisfaction.

Legal-moralism states that law must be used to prohibit or restrict business from

doing immoral activities to the society (Kaur and Ehrlich 2018). The business of Wonga also

objects with this ethics as they have forced their customers to provide high-interest rates

which are immoral.

Ethics applied to the outcome

Wonga did not follow business ethics, and as a result, their business collapsed with

1000 of customer complains. They forced their customers unethically to borrow from their

business and charged a heavy amount of interest from them. However, Wonga assured its

customers that they would pay the existing customers. Despite a move to focus on long term

loans with flexible repayment, Wonga lost £65 million in 2016, and this is primarily caused

by unethical practices (Jiya 2019). The internal and external shareholders were affected by

the huge loss of Wonga. Internal shareholders such as employees, executives and

shareholders were badly affected, and the external shareholders such as customers and the

government were not satisfied with Wonga (Trevino and Nelson 2016). As per the study,

most of the people borrow from the unethical organization. Wonga approached the society

based on Utilitarianism theory as they were only focused on their personal benefits other than

as a moral obligation to act based on fair adjudication between competing claims. Justice

theory states that in the business of Wonga, every individual should have equal right and

should be treated ethically (Sabbagh and Schmitt 2016).

Ethical objections

Psychological egoism is the view that human is always motivated by self-interest and

selfishness. It claims that if people or business is helping others, they do to fulfil their

personal benefits. This approach can be perceived from the analysis of Wonga as they were

primarily focused on self-interest rather than customers satisfaction.

Legal-moralism states that law must be used to prohibit or restrict business from

doing immoral activities to the society (Kaur and Ehrlich 2018). The business of Wonga also

objects with this ethics as they have forced their customers to provide high-interest rates

which are immoral.

Ethics applied to the outcome

Wonga did not follow business ethics, and as a result, their business collapsed with

1000 of customer complains. They forced their customers unethically to borrow from their

business and charged a heavy amount of interest from them. However, Wonga assured its

customers that they would pay the existing customers. Despite a move to focus on long term

loans with flexible repayment, Wonga lost £65 million in 2016, and this is primarily caused

by unethical practices (Jiya 2019). The internal and external shareholders were affected by

the huge loss of Wonga. Internal shareholders such as employees, executives and

shareholders were badly affected, and the external shareholders such as customers and the

government were not satisfied with Wonga (Trevino and Nelson 2016). As per the study,

most of the people borrow from the unethical organization. Wonga approached the society

based on Utilitarianism theory as they were only focused on their personal benefits other than

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ANALYSIS OF WONGA

customers benefits. Justice theory can also be applied to this organization as it has been

perceived that Wonga risked the claims of the common people and shareholders.

Regulations

The fraud of Wonga violated the regulations of the Financial Conduct Authority.

They also breached the guidelines of the Office of Fair Trading. FCA uncovered widespread

failing of Wonga in April 2014 and put ‘redress scheme’ for 45000 customers who had been

subject to unfair debt collection practices and in last quarter of October, FCA provided

redress to 375000 customers who have been given loans by Wonga without proper

affordability assessment (Brookes and Harvey 2017). FCA issued a press release related to

this stating that Wonga must write off all outstanding amounts and interest for all customers

before 30 days after the announcement. However, Wonga violated the code of conduct by

FCA, and as a result, fraud in 2015 happened.

Further, after the fraud, FCA announced that Wonga must refund the interest rates and

charges to their customers in respect of loans (Gardner 2016). Wonga provided wrong data

breach across 250000 UK customers, which is illegal and unauthorized. The data breach

resulted in Wonga to have a pre-tax loss of £80.2 million. Wonga was using customers’

private personal information unethically into their business (Gunter 2017).

Similar to this, SameDayCash, a payday lender, also faced the same issue in 2015,

when their default rates have gone high to 50%. This primary reason for this was unethical

business and violating code on conducts.

Factors

From the fraud of Wonga, the customers were the most affected as they took a loan

from Wonga and provided cash to them. Most of the customers of Wonga faced several

financial issues after the fraud. The fraud of Wonga also affected the internal and external

customers benefits. Justice theory can also be applied to this organization as it has been

perceived that Wonga risked the claims of the common people and shareholders.

Regulations

The fraud of Wonga violated the regulations of the Financial Conduct Authority.

They also breached the guidelines of the Office of Fair Trading. FCA uncovered widespread

failing of Wonga in April 2014 and put ‘redress scheme’ for 45000 customers who had been

subject to unfair debt collection practices and in last quarter of October, FCA provided

redress to 375000 customers who have been given loans by Wonga without proper

affordability assessment (Brookes and Harvey 2017). FCA issued a press release related to

this stating that Wonga must write off all outstanding amounts and interest for all customers

before 30 days after the announcement. However, Wonga violated the code of conduct by

FCA, and as a result, fraud in 2015 happened.

Further, after the fraud, FCA announced that Wonga must refund the interest rates and

charges to their customers in respect of loans (Gardner 2016). Wonga provided wrong data

breach across 250000 UK customers, which is illegal and unauthorized. The data breach

resulted in Wonga to have a pre-tax loss of £80.2 million. Wonga was using customers’

private personal information unethically into their business (Gunter 2017).

Similar to this, SameDayCash, a payday lender, also faced the same issue in 2015,

when their default rates have gone high to 50%. This primary reason for this was unethical

business and violating code on conducts.

Factors

From the fraud of Wonga, the customers were the most affected as they took a loan

from Wonga and provided cash to them. Most of the customers of Wonga faced several

financial issues after the fraud. The fraud of Wonga also affected the internal and external

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ANALYSIS OF WONGA

shareholders as their shares were involved in the business of Wonga. The financial loss

affected the shareholders of Wonga massively after the fraud in 2015. The taxpayers and

authority were also concerned with Wonga as their company was shutting down as Wonga

was one of the top payday lending organization in the UK. This fraud impacted on the

economy of UK massively. The customers and shareholders are primary threats of this fraud

as they invested they cash into the organization. If the organization shut down without

repaying it, they will face a massive amount of loss and can go default. Ombudsman services

are also receiving payday loan complaints from their customers; however, the number of new

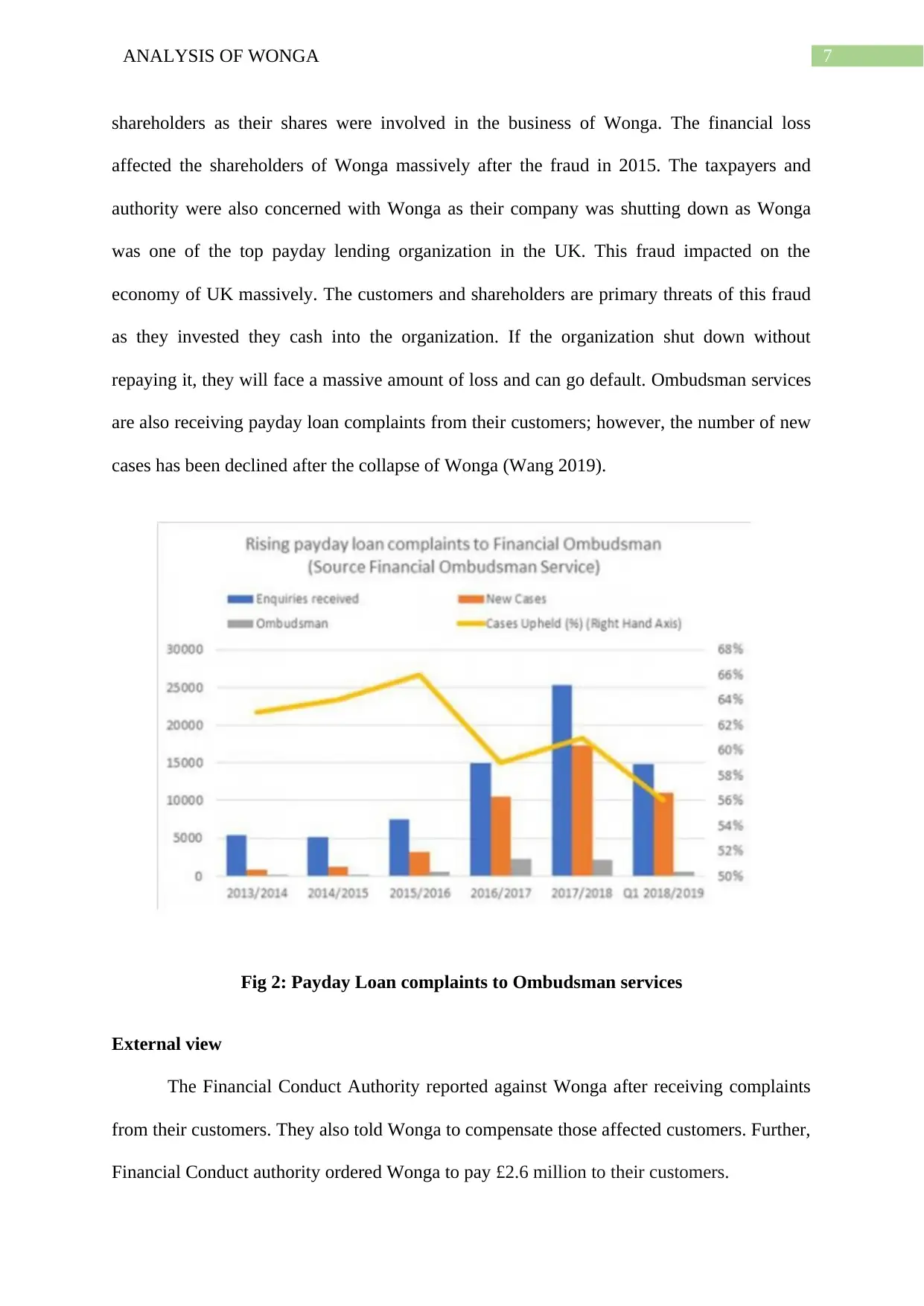

cases has been declined after the collapse of Wonga (Wang 2019).

Fig 2: Payday Loan complaints to Ombudsman services

External view

The Financial Conduct Authority reported against Wonga after receiving complaints

from their customers. They also told Wonga to compensate those affected customers. Further,

Financial Conduct authority ordered Wonga to pay £2.6 million to their customers.

shareholders as their shares were involved in the business of Wonga. The financial loss

affected the shareholders of Wonga massively after the fraud in 2015. The taxpayers and

authority were also concerned with Wonga as their company was shutting down as Wonga

was one of the top payday lending organization in the UK. This fraud impacted on the

economy of UK massively. The customers and shareholders are primary threats of this fraud

as they invested they cash into the organization. If the organization shut down without

repaying it, they will face a massive amount of loss and can go default. Ombudsman services

are also receiving payday loan complaints from their customers; however, the number of new

cases has been declined after the collapse of Wonga (Wang 2019).

Fig 2: Payday Loan complaints to Ombudsman services

External view

The Financial Conduct Authority reported against Wonga after receiving complaints

from their customers. They also told Wonga to compensate those affected customers. Further,

Financial Conduct authority ordered Wonga to pay £2.6 million to their customers.

8ANALYSIS OF WONGA

The Ombudsman reported that giving borrowers more time to bring cases is putting

further pressure on Wonga and will impact on company’s survival if they do not compensate

their customers on time.

James Daley, the managing director of the campaign group, said that Wonga exploited

the market which was loosely regulated and as a result, Wonga is in this problematic

situation. He added that Wonga does not serve their customers well as Wonga was giving

quick credit to people at a high price and high fees.

Wonga claimed its customers were web-savvy people who do not choose big banks,

and the Guardian found that the customers were hard-pressed borrowers who were not being

able to find loan somewhere else.

Actor Michael Sheen warned the customers about the scam of Wonga, and he further

added that putting money on Wonga will result in a scam for these customers. He also said

that ministers must protect the interest of these customers who still owe money from Wonga

by ensuring they are transferred to the ethical provider (Dayson, Vik and Curtis 2020).

The shareholders of Wonga remained fully supportive of the company, providing £10

million cash injection during its hard times and said they would remain fully supportive of

the business during its hard times.

Recommendation

From the study, it can be perceived that Wonga was unethically providing payday

loan services to the people which resulted in their collapse; therefore, certain

recommendations are given following which Wonga will be able to regain their customers in

the market and improve their market position. It is recommended that Wonga should repay all

the existing customers with higher interest rates to keep their trust in the organization. Wonga

The Ombudsman reported that giving borrowers more time to bring cases is putting

further pressure on Wonga and will impact on company’s survival if they do not compensate

their customers on time.

James Daley, the managing director of the campaign group, said that Wonga exploited

the market which was loosely regulated and as a result, Wonga is in this problematic

situation. He added that Wonga does not serve their customers well as Wonga was giving

quick credit to people at a high price and high fees.

Wonga claimed its customers were web-savvy people who do not choose big banks,

and the Guardian found that the customers were hard-pressed borrowers who were not being

able to find loan somewhere else.

Actor Michael Sheen warned the customers about the scam of Wonga, and he further

added that putting money on Wonga will result in a scam for these customers. He also said

that ministers must protect the interest of these customers who still owe money from Wonga

by ensuring they are transferred to the ethical provider (Dayson, Vik and Curtis 2020).

The shareholders of Wonga remained fully supportive of the company, providing £10

million cash injection during its hard times and said they would remain fully supportive of

the business during its hard times.

Recommendation

From the study, it can be perceived that Wonga was unethically providing payday

loan services to the people which resulted in their collapse; therefore, certain

recommendations are given following which Wonga will be able to regain their customers in

the market and improve their market position. It is recommended that Wonga should repay all

the existing customers with higher interest rates to keep their trust in the organization. Wonga

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ANALYSIS OF WONGA

should follow certain ethical practices to their organization which will help them to comply

with the government rules and regulations and remain in the market. Wonga should comply

with regulations provided by FCA and repay its customers as soon as possible. To improve

the financial position during the downtime, Wonga should ask their existing customers and

stakeholders to invest money into their organization. Wonga should restore the

communication service effectively by which they will be able to reach its customers. To

improve the ethics of the business, it is recommended that Wonga should measure the

effectiveness of the existing ethical programme and improve it.

Conclusion

From the study, it has been found that Wonga was unethically providing payday loan

services to their customers at a high price, and it resulted in the collapse of their business in

august 2018. Wonga was targeting customers who want a quick loan and has not served them

well. It has been found that they have breached the data of their customers as well as has not

followed the recommendations of FCA, therefore, it has been recommended that Wonga

should repay their customers ethically to improve the condition of the business.

should follow certain ethical practices to their organization which will help them to comply

with the government rules and regulations and remain in the market. Wonga should comply

with regulations provided by FCA and repay its customers as soon as possible. To improve

the financial position during the downtime, Wonga should ask their existing customers and

stakeholders to invest money into their organization. Wonga should restore the

communication service effectively by which they will be able to reach its customers. To

improve the ethics of the business, it is recommended that Wonga should measure the

effectiveness of the existing ethical programme and improve it.

Conclusion

From the study, it has been found that Wonga was unethically providing payday loan

services to their customers at a high price, and it resulted in the collapse of their business in

august 2018. Wonga was targeting customers who want a quick loan and has not served them

well. It has been found that they have breached the data of their customers as well as has not

followed the recommendations of FCA, therefore, it has been recommended that Wonga

should repay their customers ethically to improve the condition of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ANALYSIS OF WONGA

References

Brookes, G. and Harvey, K., 2017. Just plain Wronga? A multimodal critical analysis of

online payday loan discourse. Critical Discourse Studies, 14(2), pp.167-187.

Becker, J.M. and Allayannis, G.Y., 2019. A Global Fintech Overview. Darden Case No.

UVA-F-1860.

Mill, J.S., 2016. Utilitarianism. In Seven masterpieces of philosophy (pp. 337-383).

Routledge.

Sabbagh, C. and Schmitt, M., 2016. Past, present, and future of social justice theory and

research. In Handbook of social justice theory and research (pp. 1-11). Springer, New York,

NY.

Kaur, H. and Ehrlich, M.A., 2018. Are Angel Investors Egotists? Evaluating Name-Letter

Preferences as Implicit Egotism. Proceedings of the Northeast Business & Economics

Association.

Jiya, T., 2019. Ethical Implications of Predictive Risk Intelligence.

Trevino, L.K. and Nelson, K.A., 2016. Managing business ethics: Straight talk about how to

do it right. John Wiley & Sons.

Brookes, G. and Harvey, K., 2017. Just plain Wronga? A multimodal critical analysis of

online payday loan discourse. Critical Discourse Studies, 14(2), pp.167-187.

Gardner, J., 2016. High-cost credit in the UK: a philosophical justification for government

intervention. In Credit, Consumers and the Law (pp. 156-176). Routledge.

Gunter, S., 2017. Digitally secure transformation. ITNOW, 59(2), pp.12-13.

References

Brookes, G. and Harvey, K., 2017. Just plain Wronga? A multimodal critical analysis of

online payday loan discourse. Critical Discourse Studies, 14(2), pp.167-187.

Becker, J.M. and Allayannis, G.Y., 2019. A Global Fintech Overview. Darden Case No.

UVA-F-1860.

Mill, J.S., 2016. Utilitarianism. In Seven masterpieces of philosophy (pp. 337-383).

Routledge.

Sabbagh, C. and Schmitt, M., 2016. Past, present, and future of social justice theory and

research. In Handbook of social justice theory and research (pp. 1-11). Springer, New York,

NY.

Kaur, H. and Ehrlich, M.A., 2018. Are Angel Investors Egotists? Evaluating Name-Letter

Preferences as Implicit Egotism. Proceedings of the Northeast Business & Economics

Association.

Jiya, T., 2019. Ethical Implications of Predictive Risk Intelligence.

Trevino, L.K. and Nelson, K.A., 2016. Managing business ethics: Straight talk about how to

do it right. John Wiley & Sons.

Brookes, G. and Harvey, K., 2017. Just plain Wronga? A multimodal critical analysis of

online payday loan discourse. Critical Discourse Studies, 14(2), pp.167-187.

Gardner, J., 2016. High-cost credit in the UK: a philosophical justification for government

intervention. In Credit, Consumers and the Law (pp. 156-176). Routledge.

Gunter, S., 2017. Digitally secure transformation. ITNOW, 59(2), pp.12-13.

11ANALYSIS OF WONGA

Dayson, K.T., Vik, P.M. and Curtis, J.M., 2020. Scaling up the UK personal lending CDFI

sector: from£ 20m to£ 200m in lending by 2027.

Hembruff, J. and Soederberg, S., 2019, January. Debtfarism and the Violence of Financial

Inclusion: The Case of the Payday Lending Industry. In Forum for Social Economics (Vol.

48, No. 1, pp. 49-68). Routledge.

Wang, Y., Fintech Payday Lending: The Case of Wonga September 18, 2019.

Dayson, K.T., Vik, P.M. and Curtis, J.M., 2020. Scaling up the UK personal lending CDFI

sector: from£ 20m to£ 200m in lending by 2027.

Hembruff, J. and Soederberg, S., 2019, January. Debtfarism and the Violence of Financial

Inclusion: The Case of the Payday Lending Industry. In Forum for Social Economics (Vol.

48, No. 1, pp. 49-68). Routledge.

Wang, Y., Fintech Payday Lending: The Case of Wonga September 18, 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.