Audit Report: Analytical Procedures and Risk Factors Analysis

VerifiedAdded on 2020/03/01

|16

|3451

|31

Report

AI Summary

This report provides an in-depth analysis of the financial accounting and reporting system of Double Ink Printers Limited, focusing on the perspective of auditors. It begins with an executive summary and an introduction that outlines the objectives of the report, which include analyzing financial statements and identifying associated risk factors. The report then delves into analytical procedures, examining key financial ratios such as current ratio, quick ratio, inventory turnover, return on assets, and debt/equity ratio, along with their audit implications. The analysis highlights significant changes in these ratios and their potential impact on the audit plan. The report further explores inherent risk factors, particularly focusing on inventory valuation methods and their influence on financial statement accuracy. Finally, the report addresses fraudulent risk factors, offering recommendations based on the overall findings. This comprehensive analysis aims to provide a thorough understanding of the audit process and the importance of risk assessment in financial reporting.

ANALYTICAL PROCEDURES AND THE RISK FACTORS

Student Name

Student ID

8/25/2017

Student Name

Student ID

8/25/2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

From the past so many decades, the financial accounting and reporting has been playing a very

important role in the industry. Every companies operating in the different industries are

mandatorily required to account for each and every transaction entered into by the company and

accordingly disclose the financial results for the particular period. Similarly Double Ink Printers

Limited, being a printing company, has a sound financial reporting system and the same have

been analysed in the report. The main objective of the report is to analyze the financial

accounting and reporting system of the company from point of view of the auditors of the

company. The analysis includes not only the financial statements but also the risk factors that

come during the audit. The role of the auditor in planning his audit considering the various risk

factors has been detailed in the report. With these objectives and the frames in mind the report

has been prepared.

2

From the past so many decades, the financial accounting and reporting has been playing a very

important role in the industry. Every companies operating in the different industries are

mandatorily required to account for each and every transaction entered into by the company and

accordingly disclose the financial results for the particular period. Similarly Double Ink Printers

Limited, being a printing company, has a sound financial reporting system and the same have

been analysed in the report. The main objective of the report is to analyze the financial

accounting and reporting system of the company from point of view of the auditors of the

company. The analysis includes not only the financial statements but also the risk factors that

come during the audit. The role of the auditor in planning his audit considering the various risk

factors has been detailed in the report. With these objectives and the frames in mind the report

has been prepared.

2

Table of Contents

Executive Summary 2

Introduction 4

Question1 – Analytical Procedures 5

Question 2 – Inherent Risk Factors 8

Question 3 – Fraudulent Risk Factors 9

Conclusion and Recommendation 10

References 11

3

Executive Summary 2

Introduction 4

Question1 – Analytical Procedures 5

Question 2 – Inherent Risk Factors 8

Question 3 – Fraudulent Risk Factors 9

Conclusion and Recommendation 10

References 11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The details of every company can be checked and verified from the basic document of the

company which is known as Annual Report. Annual report provides all the information which is

very useful for all the stakeholders of the company whether it is the employees or it is the

shareholders of the company. Each stakeholder wants to have more and more information about

the company so as to take the decision in relation to the company. Like, shareholder of the

company like to know whether he should invest in the company or not. For taking such decision

he should be available with the information pertaining to the financial position and the financial

performance of the company. This information are reflected and detailed with the note of the

directors of the company in the Financial Statements of the company forming part of the Annual

Report.

The report has been started with the executive summary detailing the main aims of the report.

Then it has detailed the answer to the question number one which is related to analytical

procedures adopted by the auditor before starting of the audit. The information of Double Ink

Printers Limited has been considered. The company is in the business of printing books and

magazines. In this it has been explained as to how the results of the procedures so performed

have affected the audit plan of the auditors. Then the answer to the second question has been

detailed which is related to the inherent risk factors. These risks are notified by the auditor while

reading the background information and the financial information and the internal control

procedures of the company. Similarly in the last question the risk factors which have led to

fraudulent reporting of the financial information have been detailed. At the last conclusion and

recommendation has been given for the whole study.

4

The details of every company can be checked and verified from the basic document of the

company which is known as Annual Report. Annual report provides all the information which is

very useful for all the stakeholders of the company whether it is the employees or it is the

shareholders of the company. Each stakeholder wants to have more and more information about

the company so as to take the decision in relation to the company. Like, shareholder of the

company like to know whether he should invest in the company or not. For taking such decision

he should be available with the information pertaining to the financial position and the financial

performance of the company. This information are reflected and detailed with the note of the

directors of the company in the Financial Statements of the company forming part of the Annual

Report.

The report has been started with the executive summary detailing the main aims of the report.

Then it has detailed the answer to the question number one which is related to analytical

procedures adopted by the auditor before starting of the audit. The information of Double Ink

Printers Limited has been considered. The company is in the business of printing books and

magazines. In this it has been explained as to how the results of the procedures so performed

have affected the audit plan of the auditors. Then the answer to the second question has been

detailed which is related to the inherent risk factors. These risks are notified by the auditor while

reading the background information and the financial information and the internal control

procedures of the company. Similarly in the last question the risk factors which have led to

fraudulent reporting of the financial information have been detailed. At the last conclusion and

recommendation has been given for the whole study.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

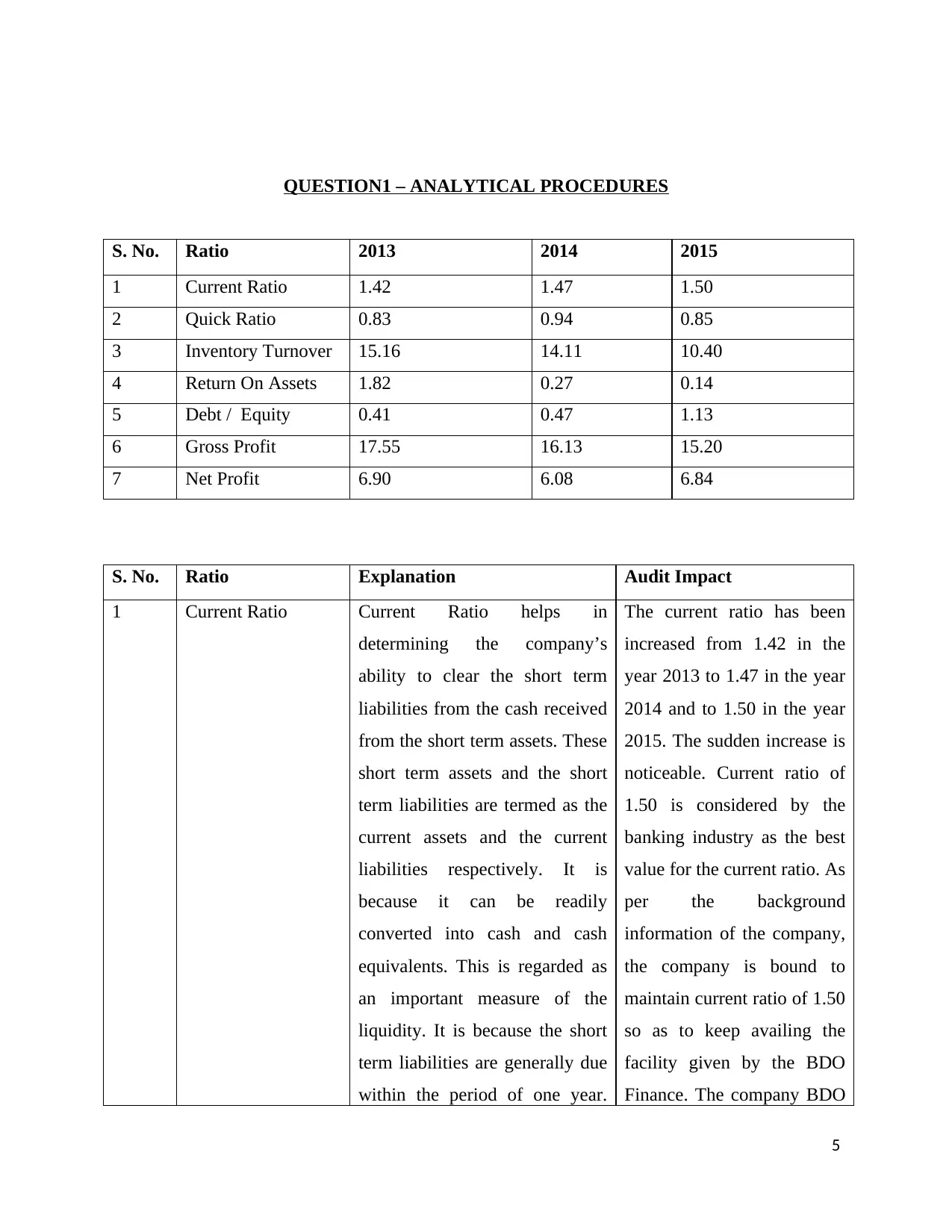

QUESTION1 – ANALYTICAL PROCEDURES

S. No. Ratio 2013 2014 2015

1 Current Ratio 1.42 1.47 1.50

2 Quick Ratio 0.83 0.94 0.85

3 Inventory Turnover 15.16 14.11 10.40

4 Return On Assets 1.82 0.27 0.14

5 Debt / Equity 0.41 0.47 1.13

6 Gross Profit 17.55 16.13 15.20

7 Net Profit 6.90 6.08 6.84

S. No. Ratio Explanation Audit Impact

1 Current Ratio Current Ratio helps in

determining the company’s

ability to clear the short term

liabilities from the cash received

from the short term assets. These

short term assets and the short

term liabilities are termed as the

current assets and the current

liabilities respectively. It is

because it can be readily

converted into cash and cash

equivalents. This is regarded as

an important measure of the

liquidity. It is because the short

term liabilities are generally due

within the period of one year.

The current ratio has been

increased from 1.42 in the

year 2013 to 1.47 in the year

2014 and to 1.50 in the year

2015. The sudden increase is

noticeable. Current ratio of

1.50 is considered by the

banking industry as the best

value for the current ratio. As

per the background

information of the company,

the company is bound to

maintain current ratio of 1.50

so as to keep availing the

facility given by the BDO

Finance. The company BDO

5

S. No. Ratio 2013 2014 2015

1 Current Ratio 1.42 1.47 1.50

2 Quick Ratio 0.83 0.94 0.85

3 Inventory Turnover 15.16 14.11 10.40

4 Return On Assets 1.82 0.27 0.14

5 Debt / Equity 0.41 0.47 1.13

6 Gross Profit 17.55 16.13 15.20

7 Net Profit 6.90 6.08 6.84

S. No. Ratio Explanation Audit Impact

1 Current Ratio Current Ratio helps in

determining the company’s

ability to clear the short term

liabilities from the cash received

from the short term assets. These

short term assets and the short

term liabilities are termed as the

current assets and the current

liabilities respectively. It is

because it can be readily

converted into cash and cash

equivalents. This is regarded as

an important measure of the

liquidity. It is because the short

term liabilities are generally due

within the period of one year.

The current ratio has been

increased from 1.42 in the

year 2013 to 1.47 in the year

2014 and to 1.50 in the year

2015. The sudden increase is

noticeable. Current ratio of

1.50 is considered by the

banking industry as the best

value for the current ratio. As

per the background

information of the company,

the company is bound to

maintain current ratio of 1.50

so as to keep availing the

facility given by the BDO

Finance. The company BDO

5

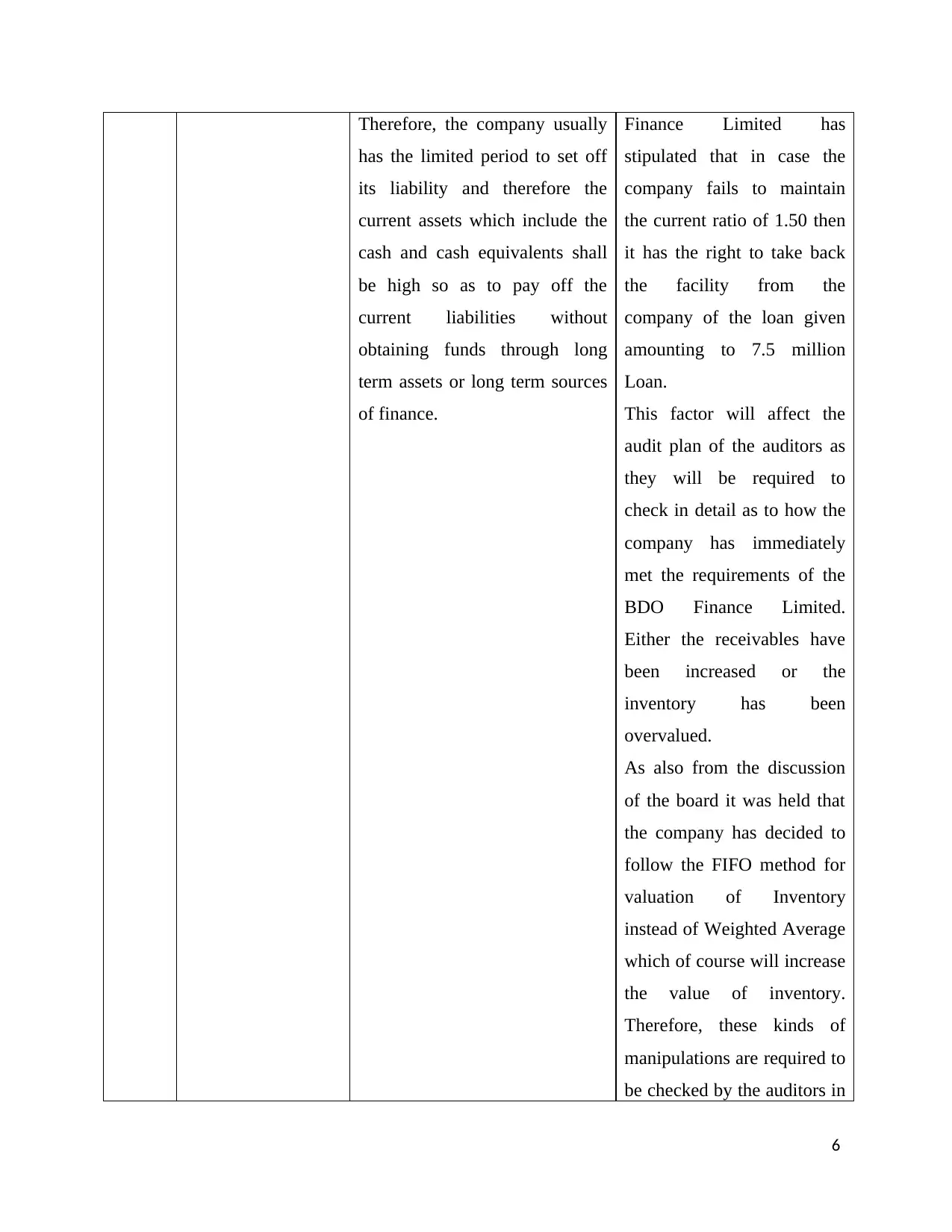

Therefore, the company usually

has the limited period to set off

its liability and therefore the

current assets which include the

cash and cash equivalents shall

be high so as to pay off the

current liabilities without

obtaining funds through long

term assets or long term sources

of finance.

Finance Limited has

stipulated that in case the

company fails to maintain

the current ratio of 1.50 then

it has the right to take back

the facility from the

company of the loan given

amounting to 7.5 million

Loan.

This factor will affect the

audit plan of the auditors as

they will be required to

check in detail as to how the

company has immediately

met the requirements of the

BDO Finance Limited.

Either the receivables have

been increased or the

inventory has been

overvalued.

As also from the discussion

of the board it was held that

the company has decided to

follow the FIFO method for

valuation of Inventory

instead of Weighted Average

which of course will increase

the value of inventory.

Therefore, these kinds of

manipulations are required to

be checked by the auditors in

6

has the limited period to set off

its liability and therefore the

current assets which include the

cash and cash equivalents shall

be high so as to pay off the

current liabilities without

obtaining funds through long

term assets or long term sources

of finance.

Finance Limited has

stipulated that in case the

company fails to maintain

the current ratio of 1.50 then

it has the right to take back

the facility from the

company of the loan given

amounting to 7.5 million

Loan.

This factor will affect the

audit plan of the auditors as

they will be required to

check in detail as to how the

company has immediately

met the requirements of the

BDO Finance Limited.

Either the receivables have

been increased or the

inventory has been

overvalued.

As also from the discussion

of the board it was held that

the company has decided to

follow the FIFO method for

valuation of Inventory

instead of Weighted Average

which of course will increase

the value of inventory.

Therefore, these kinds of

manipulations are required to

be checked by the auditors in

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

detail and hence their audit

plan needs to be modified.

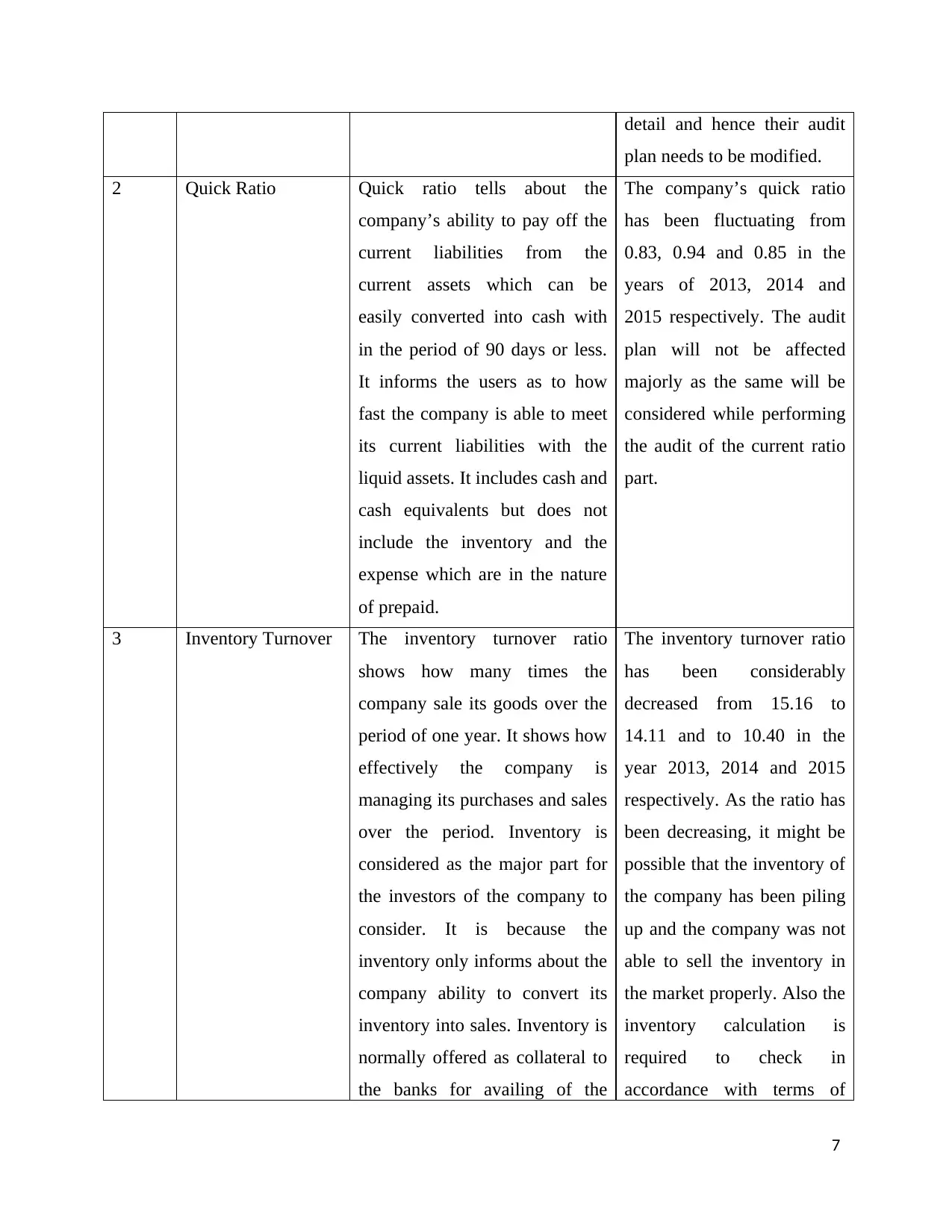

2 Quick Ratio Quick ratio tells about the

company’s ability to pay off the

current liabilities from the

current assets which can be

easily converted into cash with

in the period of 90 days or less.

It informs the users as to how

fast the company is able to meet

its current liabilities with the

liquid assets. It includes cash and

cash equivalents but does not

include the inventory and the

expense which are in the nature

of prepaid.

The company’s quick ratio

has been fluctuating from

0.83, 0.94 and 0.85 in the

years of 2013, 2014 and

2015 respectively. The audit

plan will not be affected

majorly as the same will be

considered while performing

the audit of the current ratio

part.

3 Inventory Turnover The inventory turnover ratio

shows how many times the

company sale its goods over the

period of one year. It shows how

effectively the company is

managing its purchases and sales

over the period. Inventory is

considered as the major part for

the investors of the company to

consider. It is because the

inventory only informs about the

company ability to convert its

inventory into sales. Inventory is

normally offered as collateral to

the banks for availing of the

The inventory turnover ratio

has been considerably

decreased from 15.16 to

14.11 and to 10.40 in the

year 2013, 2014 and 2015

respectively. As the ratio has

been decreasing, it might be

possible that the inventory of

the company has been piling

up and the company was not

able to sell the inventory in

the market properly. Also the

inventory calculation is

required to check in

accordance with terms of

7

plan needs to be modified.

2 Quick Ratio Quick ratio tells about the

company’s ability to pay off the

current liabilities from the

current assets which can be

easily converted into cash with

in the period of 90 days or less.

It informs the users as to how

fast the company is able to meet

its current liabilities with the

liquid assets. It includes cash and

cash equivalents but does not

include the inventory and the

expense which are in the nature

of prepaid.

The company’s quick ratio

has been fluctuating from

0.83, 0.94 and 0.85 in the

years of 2013, 2014 and

2015 respectively. The audit

plan will not be affected

majorly as the same will be

considered while performing

the audit of the current ratio

part.

3 Inventory Turnover The inventory turnover ratio

shows how many times the

company sale its goods over the

period of one year. It shows how

effectively the company is

managing its purchases and sales

over the period. Inventory is

considered as the major part for

the investors of the company to

consider. It is because the

inventory only informs about the

company ability to convert its

inventory into sales. Inventory is

normally offered as collateral to

the banks for availing of the

The inventory turnover ratio

has been considerably

decreased from 15.16 to

14.11 and to 10.40 in the

year 2013, 2014 and 2015

respectively. As the ratio has

been decreasing, it might be

possible that the inventory of

the company has been piling

up and the company was not

able to sell the inventory in

the market properly. Also the

inventory calculation is

required to check in

accordance with terms of

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

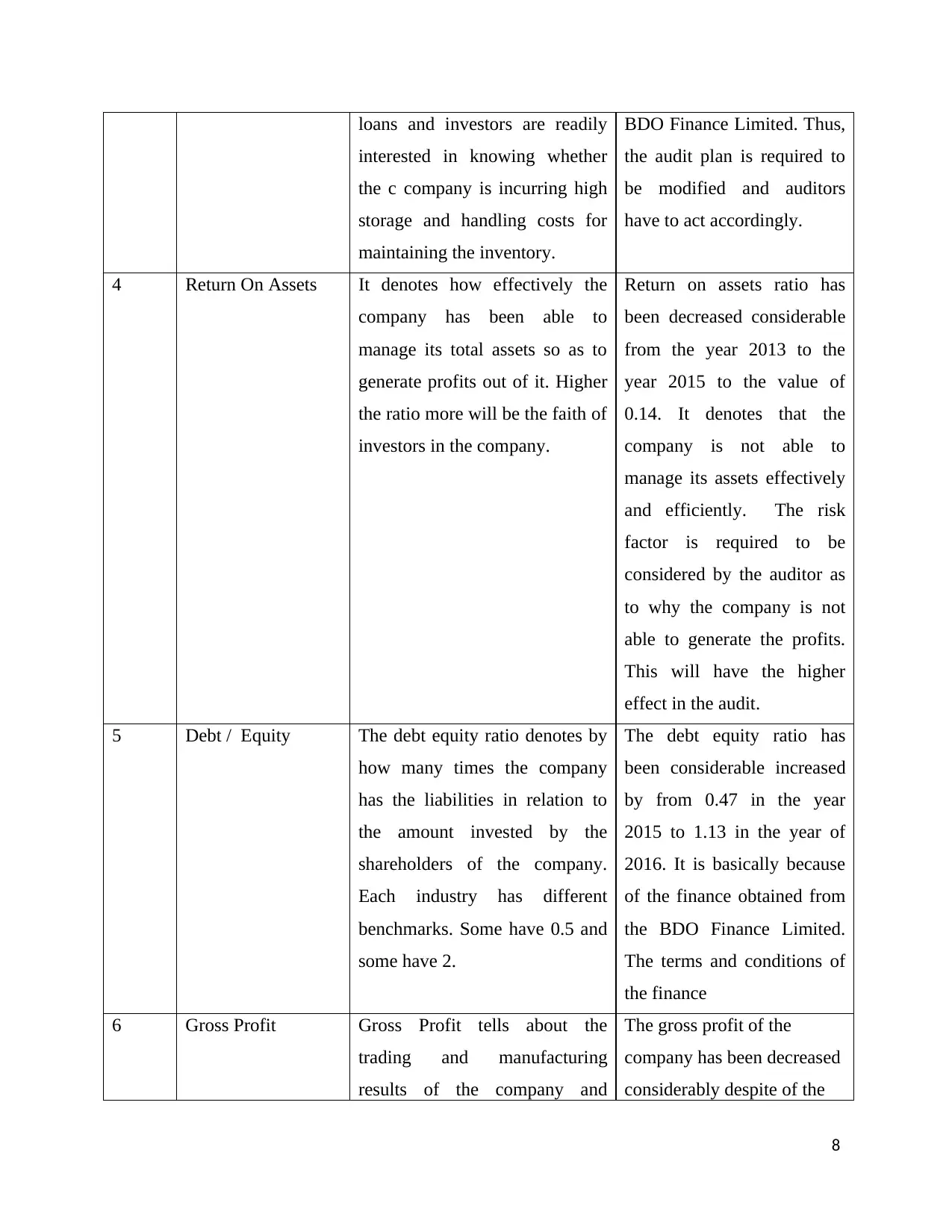

loans and investors are readily

interested in knowing whether

the c company is incurring high

storage and handling costs for

maintaining the inventory.

BDO Finance Limited. Thus,

the audit plan is required to

be modified and auditors

have to act accordingly.

4 Return On Assets It denotes how effectively the

company has been able to

manage its total assets so as to

generate profits out of it. Higher

the ratio more will be the faith of

investors in the company.

Return on assets ratio has

been decreased considerable

from the year 2013 to the

year 2015 to the value of

0.14. It denotes that the

company is not able to

manage its assets effectively

and efficiently. The risk

factor is required to be

considered by the auditor as

to why the company is not

able to generate the profits.

This will have the higher

effect in the audit.

5 Debt / Equity The debt equity ratio denotes by

how many times the company

has the liabilities in relation to

the amount invested by the

shareholders of the company.

Each industry has different

benchmarks. Some have 0.5 and

some have 2.

The debt equity ratio has

been considerable increased

by from 0.47 in the year

2015 to 1.13 in the year of

2016. It is basically because

of the finance obtained from

the BDO Finance Limited.

The terms and conditions of

the finance

6 Gross Profit Gross Profit tells about the

trading and manufacturing

results of the company and

The gross profit of the

company has been decreased

considerably despite of the

8

interested in knowing whether

the c company is incurring high

storage and handling costs for

maintaining the inventory.

BDO Finance Limited. Thus,

the audit plan is required to

be modified and auditors

have to act accordingly.

4 Return On Assets It denotes how effectively the

company has been able to

manage its total assets so as to

generate profits out of it. Higher

the ratio more will be the faith of

investors in the company.

Return on assets ratio has

been decreased considerable

from the year 2013 to the

year 2015 to the value of

0.14. It denotes that the

company is not able to

manage its assets effectively

and efficiently. The risk

factor is required to be

considered by the auditor as

to why the company is not

able to generate the profits.

This will have the higher

effect in the audit.

5 Debt / Equity The debt equity ratio denotes by

how many times the company

has the liabilities in relation to

the amount invested by the

shareholders of the company.

Each industry has different

benchmarks. Some have 0.5 and

some have 2.

The debt equity ratio has

been considerable increased

by from 0.47 in the year

2015 to 1.13 in the year of

2016. It is basically because

of the finance obtained from

the BDO Finance Limited.

The terms and conditions of

the finance

6 Gross Profit Gross Profit tells about the

trading and manufacturing

results of the company and

The gross profit of the

company has been decreased

considerably despite of the

8

shows how effectively the

company is managing its

operations.

fact that the inventory has

been overvalued and hence

the audit plan is affected and

will needs modification

accordingly.

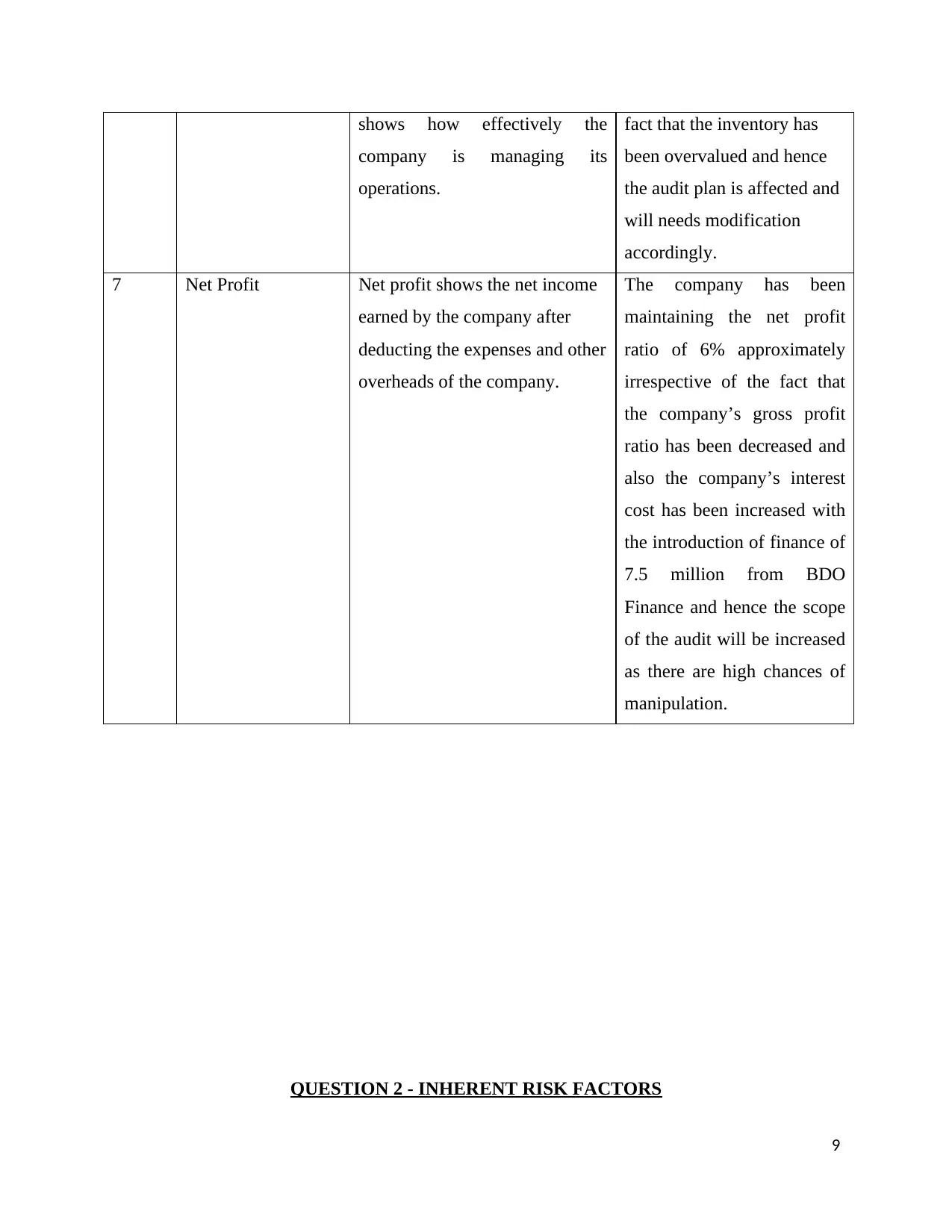

7 Net Profit Net profit shows the net income

earned by the company after

deducting the expenses and other

overheads of the company.

The company has been

maintaining the net profit

ratio of 6% approximately

irrespective of the fact that

the company’s gross profit

ratio has been decreased and

also the company’s interest

cost has been increased with

the introduction of finance of

7.5 million from BDO

Finance and hence the scope

of the audit will be increased

as there are high chances of

manipulation.

QUESTION 2 - INHERENT RISK FACTORS

9

company is managing its

operations.

fact that the inventory has

been overvalued and hence

the audit plan is affected and

will needs modification

accordingly.

7 Net Profit Net profit shows the net income

earned by the company after

deducting the expenses and other

overheads of the company.

The company has been

maintaining the net profit

ratio of 6% approximately

irrespective of the fact that

the company’s gross profit

ratio has been decreased and

also the company’s interest

cost has been increased with

the introduction of finance of

7.5 million from BDO

Finance and hence the scope

of the audit will be increased

as there are high chances of

manipulation.

QUESTION 2 - INHERENT RISK FACTORS

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

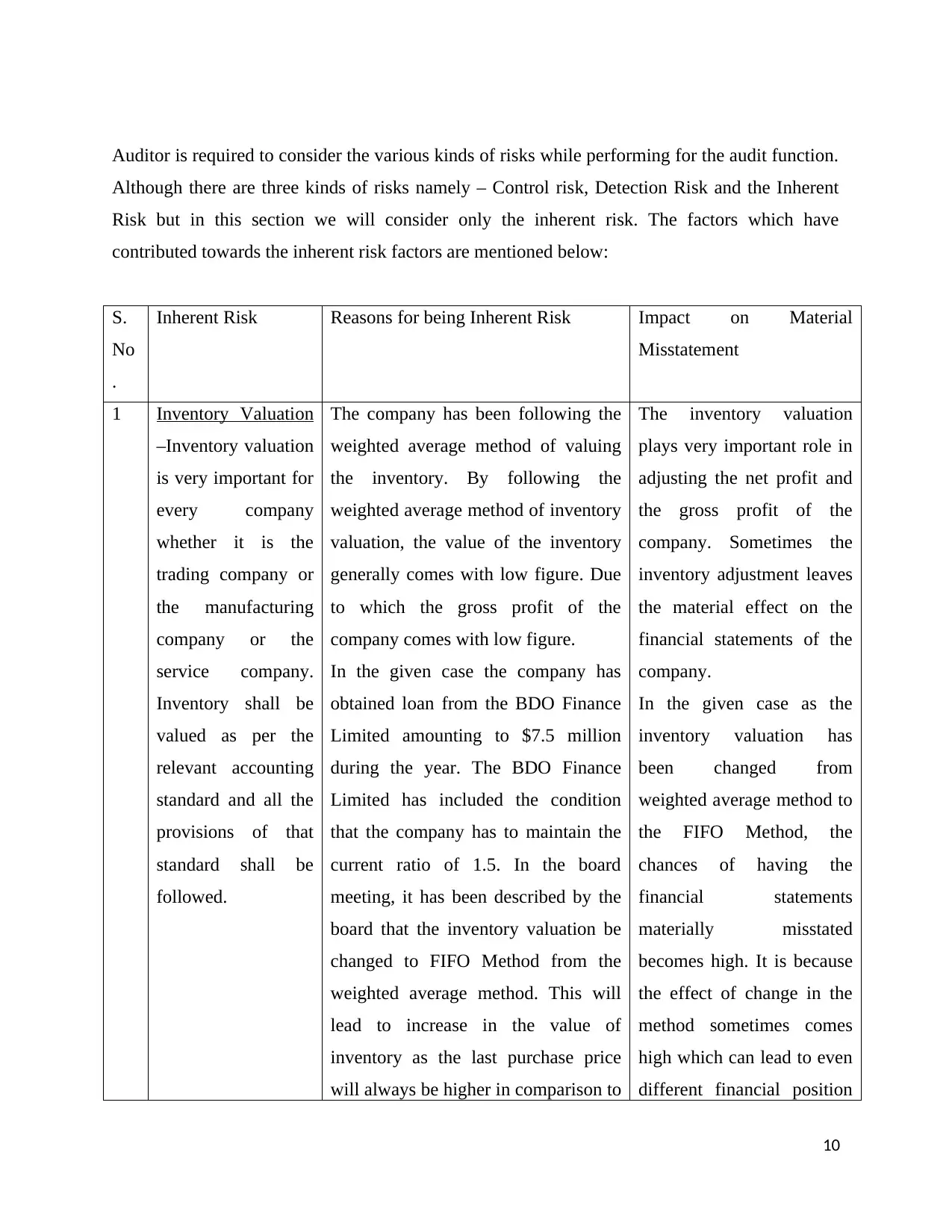

Auditor is required to consider the various kinds of risks while performing for the audit function.

Although there are three kinds of risks namely – Control risk, Detection Risk and the Inherent

Risk but in this section we will consider only the inherent risk. The factors which have

contributed towards the inherent risk factors are mentioned below:

S.

No

.

Inherent Risk Reasons for being Inherent Risk Impact on Material

Misstatement

1 Inventory Valuation

–Inventory valuation

is very important for

every company

whether it is the

trading company or

the manufacturing

company or the

service company.

Inventory shall be

valued as per the

relevant accounting

standard and all the

provisions of that

standard shall be

followed.

The company has been following the

weighted average method of valuing

the inventory. By following the

weighted average method of inventory

valuation, the value of the inventory

generally comes with low figure. Due

to which the gross profit of the

company comes with low figure.

In the given case the company has

obtained loan from the BDO Finance

Limited amounting to $7.5 million

during the year. The BDO Finance

Limited has included the condition

that the company has to maintain the

current ratio of 1.5. In the board

meeting, it has been described by the

board that the inventory valuation be

changed to FIFO Method from the

weighted average method. This will

lead to increase in the value of

inventory as the last purchase price

will always be higher in comparison to

The inventory valuation

plays very important role in

adjusting the net profit and

the gross profit of the

company. Sometimes the

inventory adjustment leaves

the material effect on the

financial statements of the

company.

In the given case as the

inventory valuation has

been changed from

weighted average method to

the FIFO Method, the

chances of having the

financial statements

materially misstated

becomes high. It is because

the effect of change in the

method sometimes comes

high which can lead to even

different financial position

10

Although there are three kinds of risks namely – Control risk, Detection Risk and the Inherent

Risk but in this section we will consider only the inherent risk. The factors which have

contributed towards the inherent risk factors are mentioned below:

S.

No

.

Inherent Risk Reasons for being Inherent Risk Impact on Material

Misstatement

1 Inventory Valuation

–Inventory valuation

is very important for

every company

whether it is the

trading company or

the manufacturing

company or the

service company.

Inventory shall be

valued as per the

relevant accounting

standard and all the

provisions of that

standard shall be

followed.

The company has been following the

weighted average method of valuing

the inventory. By following the

weighted average method of inventory

valuation, the value of the inventory

generally comes with low figure. Due

to which the gross profit of the

company comes with low figure.

In the given case the company has

obtained loan from the BDO Finance

Limited amounting to $7.5 million

during the year. The BDO Finance

Limited has included the condition

that the company has to maintain the

current ratio of 1.5. In the board

meeting, it has been described by the

board that the inventory valuation be

changed to FIFO Method from the

weighted average method. This will

lead to increase in the value of

inventory as the last purchase price

will always be higher in comparison to

The inventory valuation

plays very important role in

adjusting the net profit and

the gross profit of the

company. Sometimes the

inventory adjustment leaves

the material effect on the

financial statements of the

company.

In the given case as the

inventory valuation has

been changed from

weighted average method to

the FIFO Method, the

chances of having the

financial statements

materially misstated

becomes high. It is because

the effect of change in the

method sometimes comes

high which can lead to even

different financial position

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the weighted average price. Therefore,

In order to maintain the current ratio,

the company might have indulged in

such practice.

As the company has been following

the weighted average method since its

inception and also from the above

factors, the inventory valuation has

been considered as the major factor

which has led to the inherent risk in

the business.

and the performance of the

company.

Also the condition that the

BDO Finance Limited has

given to the company to

maintain the current ratio of

1.50. It will lead the

company to indulge in the

manipulating practices so as

to maintain the current ratio

and will strive to keep

enjoying the banking

facilities from the company.

Thus, in this way, this factor

will lead to material

misstatement in the

financial statements of the

company.

2 Acquisition of

Nuclear Publishing

Limited –

Acquisition of any

business shall be

done after taking

due diligence and

various feasibility

reports from the

professionals and

the management of

the company. The

acquisition shall be

In the given case the company has

acquired the company – Nuclear

Publishing Limited during the year.

Along with that the company has

acquired the printing rights of the

company. After the acquisition, one

article has been published stating that

the new technology has come and will

make the earlier books and theories

non useful for the students and the

readers.

This article has created a wave in the

market as the company will be in

The acquisition will have

the greater impact on the

material misstatement of the

company. It is because the

company that has been

acquired will be loss

making deal for the

company as all the theories

will get expired and the

company’s major

investment will be

depreciated with higher

amount in the future years.

11

In order to maintain the current ratio,

the company might have indulged in

such practice.

As the company has been following

the weighted average method since its

inception and also from the above

factors, the inventory valuation has

been considered as the major factor

which has led to the inherent risk in

the business.

and the performance of the

company.

Also the condition that the

BDO Finance Limited has

given to the company to

maintain the current ratio of

1.50. It will lead the

company to indulge in the

manipulating practices so as

to maintain the current ratio

and will strive to keep

enjoying the banking

facilities from the company.

Thus, in this way, this factor

will lead to material

misstatement in the

financial statements of the

company.

2 Acquisition of

Nuclear Publishing

Limited –

Acquisition of any

business shall be

done after taking

due diligence and

various feasibility

reports from the

professionals and

the management of

the company. The

acquisition shall be

In the given case the company has

acquired the company – Nuclear

Publishing Limited during the year.

Along with that the company has

acquired the printing rights of the

company. After the acquisition, one

article has been published stating that

the new technology has come and will

make the earlier books and theories

non useful for the students and the

readers.

This article has created a wave in the

market as the company will be in

The acquisition will have

the greater impact on the

material misstatement of the

company. It is because the

company that has been

acquired will be loss

making deal for the

company as all the theories

will get expired and the

company’s major

investment will be

depreciated with higher

amount in the future years.

11

done after

considering the

market conditions of

the target company

also.

failure if the same thing has happened.

In order to be safe and sound the

company will get themselves engaged

in the manipulating practices.

In this way, the same acquisition has

been considered as one of the factor

contributing towards the inherent risk

of the company.

In order to maintain the

position of the company, the

company may be engaged in

manipulating the revenue

figures so as to show higher

profits with high earnings

per share.

The same fact has been

supported by the fact that

the company has been able

to generate profit equal to

percentage of sales as

equivalent to the profits

shown in the previous two

years. In this way the

financial statements are

materially misstated and the

auditor are required to

increase their scope and

plan of the audit.

QUESTION 3- FRAUDULENT RISK FACTORS

S. No. Fraud Risk Identification of Fraud

Risk

Audit Impact

1 Development of New

Software – The company

has decided to implement

the new system in which all

functions of the company

The risk that has been

identified in this condition

is that chances of having

the expenditure reported

during the particular period

Audit will be greatly

affected by the introduction

of new system. It is because

the auditors will have to

apply the additional audit

12

considering the

market conditions of

the target company

also.

failure if the same thing has happened.

In order to be safe and sound the

company will get themselves engaged

in the manipulating practices.

In this way, the same acquisition has

been considered as one of the factor

contributing towards the inherent risk

of the company.

In order to maintain the

position of the company, the

company may be engaged in

manipulating the revenue

figures so as to show higher

profits with high earnings

per share.

The same fact has been

supported by the fact that

the company has been able

to generate profit equal to

percentage of sales as

equivalent to the profits

shown in the previous two

years. In this way the

financial statements are

materially misstated and the

auditor are required to

increase their scope and

plan of the audit.

QUESTION 3- FRAUDULENT RISK FACTORS

S. No. Fraud Risk Identification of Fraud

Risk

Audit Impact

1 Development of New

Software – The company

has decided to implement

the new system in which all

functions of the company

The risk that has been

identified in this condition

is that chances of having

the expenditure reported

during the particular period

Audit will be greatly

affected by the introduction

of new system. It is because

the auditors will have to

apply the additional audit

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.