Contribution Margin: Unveiling Company's Cost Structure

VerifiedAdded on 2020/04/21

|4

|820

|101

Homework Assignment

AI Summary

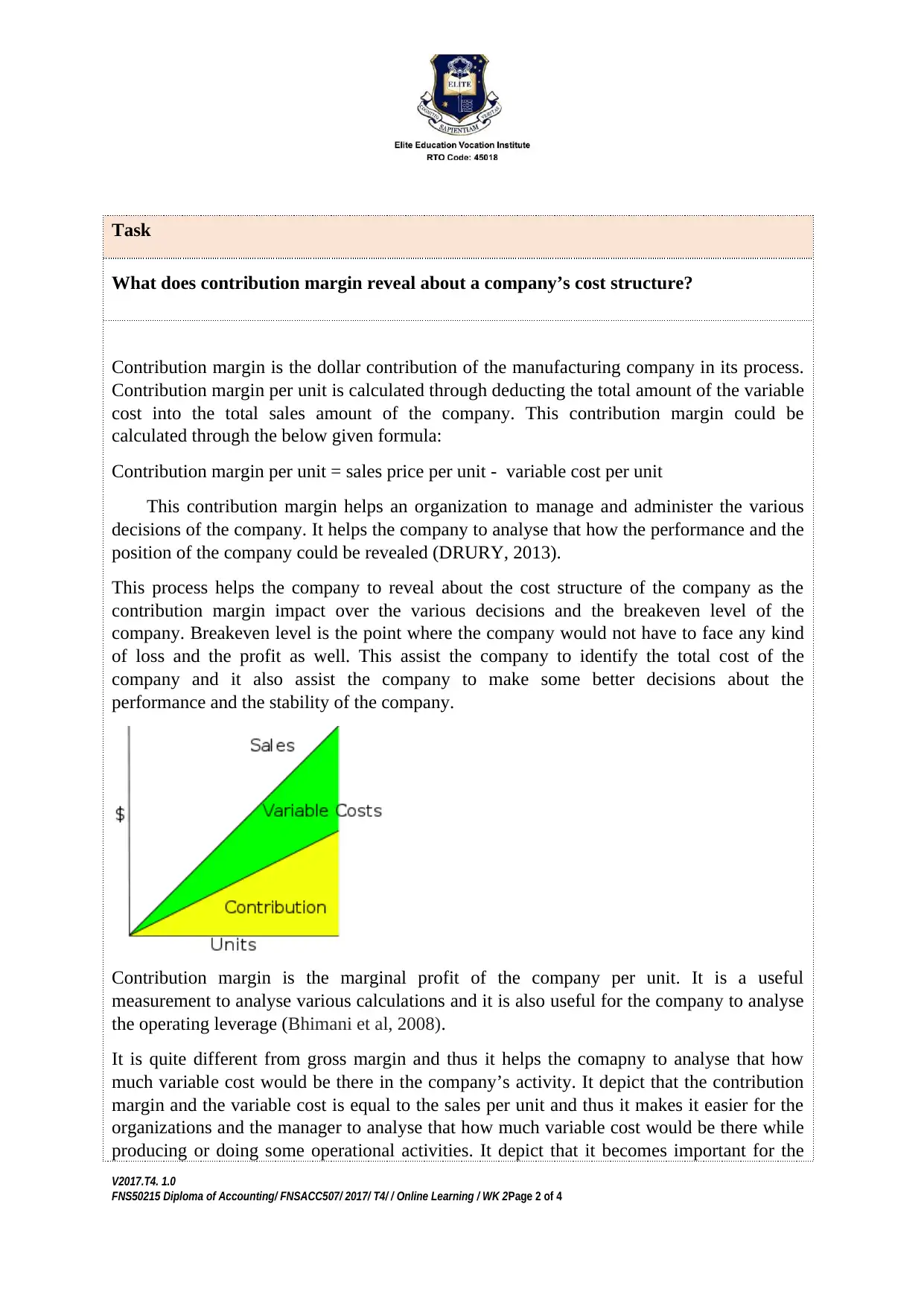

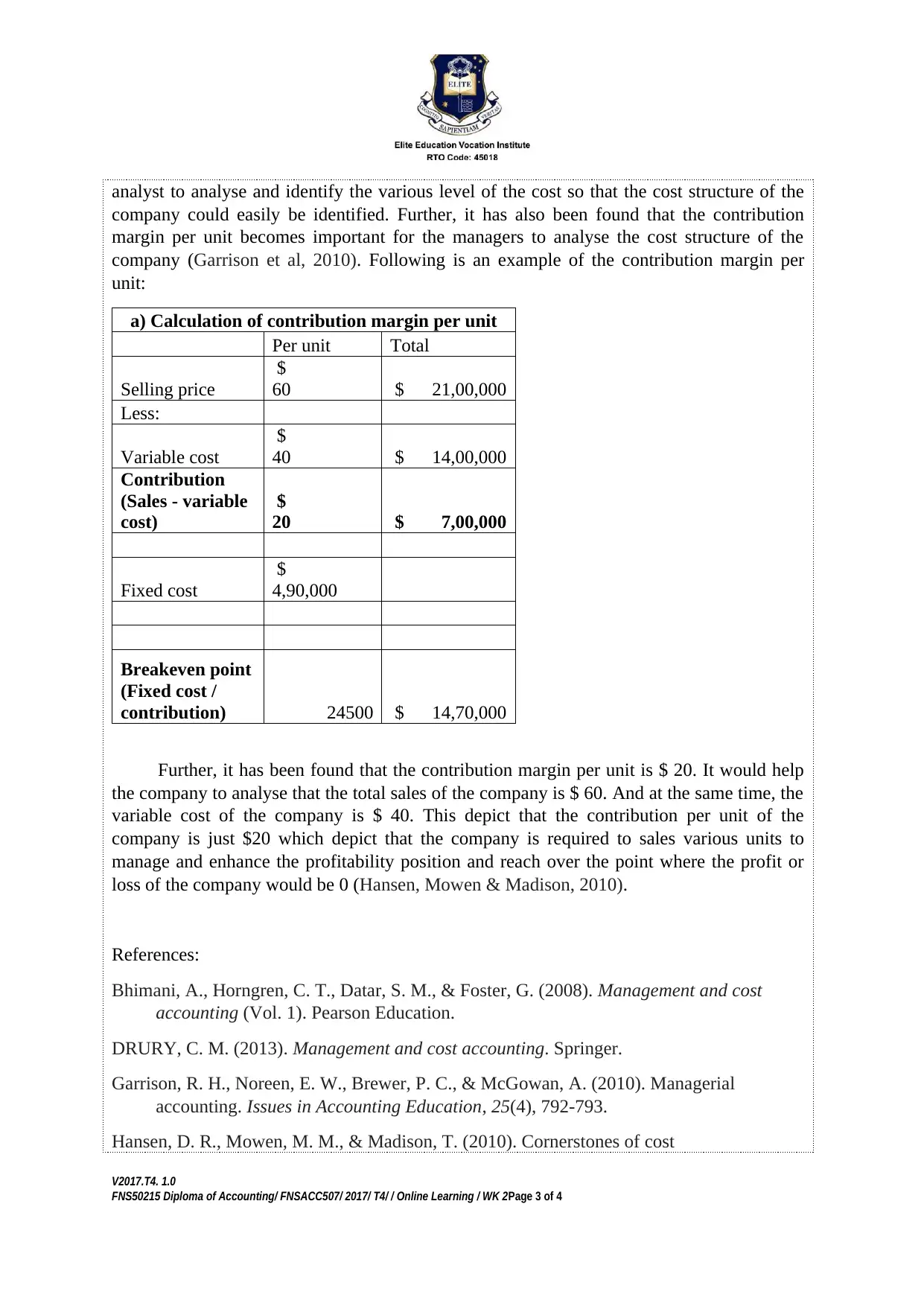

This assignment delves into the concept of contribution margin and its crucial role in understanding a company's cost structure. The analysis begins by defining contribution margin as the difference between sales revenue and variable costs, highlighting its significance in managerial decision-making. The assignment then explains how contribution margin reveals insights into a company's cost structure, particularly in relation to breakeven analysis, which is the point where total revenues equal total costs. The document provides a formula for calculating contribution margin per unit and illustrates the concept with a numerical example. It emphasizes how contribution margin helps in analyzing variable costs, assessing operating leverage, and making informed decisions about pricing, production levels, and overall profitability. The assignment references key accounting literature to support its concepts and provides a comprehensive understanding of contribution margin's importance in financial analysis.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.