Financial Management Project Report: Analyzing Oslo Chocolate Business

VerifiedAdded on 2023/06/04

|26

|6259

|155

Report

AI Summary

This report assesses Benjamin's plan to start a chocolate business in Oslo after retiring from an oil and gas company. Using a lump sum of $1.7 million, Benjamin aims to import and sell gourmet chocolates from Zurich, leveraging innovative flavors and a less competitive market. The report includes a break-even analysis, profit and loss statement, balance sheet, and cash flow projections to determine the venture's viability. Assumptions about sales growth, inventory management, and cost structures are outlined. Sensitivity analysis is also conducted to evaluate the business's resilience to changes in key variables. The analysis concludes with recommendations on whether Benjamin should proceed with the venture, considering both online sales and direct sales to a friend, Liv.

Running Head: Financial Management

1

Project Report: Financial Management

1

Project Report: Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

2

Contents

Executive Summary..........................................................................................................3

Introduction.......................................................................................................................4

Case overview...................................................................................................................4

Assumption and findings summary..................................................................................5

Break even analysis..........................................................................................................7

Profit and loss statement...................................................................................................9

Revenues.....................................................................................................................11

Expenditures...............................................................................................................11

Balance sheet..................................................................................................................12

Monthly cash flow..........................................................................................................13

Annual cash flow............................................................................................................18

Capital required..............................................................................................................19

Sensitivity analysis.........................................................................................................20

Undertake the venture.....................................................................................................21

Conclusion and recommendation...................................................................................21

Reflection........................................................................................................................21

References.......................................................................................................................23

2

Contents

Executive Summary..........................................................................................................3

Introduction.......................................................................................................................4

Case overview...................................................................................................................4

Assumption and findings summary..................................................................................5

Break even analysis..........................................................................................................7

Profit and loss statement...................................................................................................9

Revenues.....................................................................................................................11

Expenditures...............................................................................................................11

Balance sheet..................................................................................................................12

Monthly cash flow..........................................................................................................13

Annual cash flow............................................................................................................18

Capital required..............................................................................................................19

Sensitivity analysis.........................................................................................................20

Undertake the venture.....................................................................................................21

Conclusion and recommendation...................................................................................21

Reflection........................................................................................................................21

References.......................................................................................................................23

Financial Management

3

Executive Summary

The report explains about a business which is planned by Benjamin after his

retirement from the oil and gas company. A lum sum amount of $ 1.7 million has been got by

Benjamin after his retirement and now he is planning to open a chocolates business in the

Oslo market. The case explains that the sales of the business would be 50 units at first place

which would be improved to 420 units at the end of the year. The sales units of the company

could be improved along with the time and the entire sales would be done by the business

through an online portal. The revenue of the business would be improved by an increased

rate as well as the expenses of the company would be different on the basis of sales and

purchase of the business. The Benjamin would buy the chocolates on kilogram basis from the

Sprindt and Lungi (S&L) which is manufacturing company in the market of Zurich. The

chocolates are unusual and offer innovative flavours.

The main visions of the company are to offer the quality chocolates to the customers of Oslo

market. The competition level in the Oslo market in chocolate industry is lower which

explains that the company would be able to improve the sales and the profitability level of the

business would also be higher in that case.

3

Executive Summary

The report explains about a business which is planned by Benjamin after his

retirement from the oil and gas company. A lum sum amount of $ 1.7 million has been got by

Benjamin after his retirement and now he is planning to open a chocolates business in the

Oslo market. The case explains that the sales of the business would be 50 units at first place

which would be improved to 420 units at the end of the year. The sales units of the company

could be improved along with the time and the entire sales would be done by the business

through an online portal. The revenue of the business would be improved by an increased

rate as well as the expenses of the company would be different on the basis of sales and

purchase of the business. The Benjamin would buy the chocolates on kilogram basis from the

Sprindt and Lungi (S&L) which is manufacturing company in the market of Zurich. The

chocolates are unusual and offer innovative flavours.

The main visions of the company are to offer the quality chocolates to the customers of Oslo

market. The competition level in the Oslo market in chocolate industry is lower which

explains that the company would be able to improve the sales and the profitability level of the

business would also be higher in that case.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

4

Introduction:

Management over the financial transactions and activities of a business is an effective

and efficient approach. This approach is applied by the financial managers, suppliers,

customers, debtors, creditors, shareholders and other stakeholders of the business in order to

make a decision about the performance of the business. the financial analysis approach makes

it simple and easier for the internal and external stakeholders to measure the financial

position and make decision about the performance of the business that whether the allocation

of the resources must be done in the business or not (Palicka, 2011). The approach of

financial evaluation takes huge effort to collect the financial information, measure the

financial information and make a decision that whether the information are offering positive

result about the company (Schlichting, 2013). The crucial factors of the financial

management approach are that it does not take the concern on the financial transactions and

activities only; it measures all the related factors which could affect the business and the

financial performance of the business.

The approach of financial management contains various tools which is applied by the

business through identifying the base of the decisions making, such as in case of preparing a

business plan, it is important for the business to estimate the cash requirement, profit

statement, financial performance evaluation, breakeven level of the business, sensitivity

analysis on the business etc to measure that whether the business would be able to meet the

demands of the company or not.

Case overview:

In the report, the study has been done on a business plan which would be planned and

started by Benjamin. He has been retired from his job in an oil and gas company and after his

retirement, he is planning to open a business. A lum sum amount of $ 1.7 million has been

got by Benjamin after his retirement and now he is planning to open a chocolates business in

the Oslo market. He has a friend in Zurich market who manufactures the chocolates with

innovative flavours and different taste. If the chocolates would been sold in the Oslo market

than the competition level is lower in the market and the demand of the chocolates are higher

which would lead towards the profitability position to the business.

The case explains that the sales of the business would be 50 units at first place which

would be improved to 420 units at the end of the year. An online portal would be prepared by

4

Introduction:

Management over the financial transactions and activities of a business is an effective

and efficient approach. This approach is applied by the financial managers, suppliers,

customers, debtors, creditors, shareholders and other stakeholders of the business in order to

make a decision about the performance of the business. the financial analysis approach makes

it simple and easier for the internal and external stakeholders to measure the financial

position and make decision about the performance of the business that whether the allocation

of the resources must be done in the business or not (Palicka, 2011). The approach of

financial evaluation takes huge effort to collect the financial information, measure the

financial information and make a decision that whether the information are offering positive

result about the company (Schlichting, 2013). The crucial factors of the financial

management approach are that it does not take the concern on the financial transactions and

activities only; it measures all the related factors which could affect the business and the

financial performance of the business.

The approach of financial management contains various tools which is applied by the

business through identifying the base of the decisions making, such as in case of preparing a

business plan, it is important for the business to estimate the cash requirement, profit

statement, financial performance evaluation, breakeven level of the business, sensitivity

analysis on the business etc to measure that whether the business would be able to meet the

demands of the company or not.

Case overview:

In the report, the study has been done on a business plan which would be planned and

started by Benjamin. He has been retired from his job in an oil and gas company and after his

retirement, he is planning to open a business. A lum sum amount of $ 1.7 million has been

got by Benjamin after his retirement and now he is planning to open a chocolates business in

the Oslo market. He has a friend in Zurich market who manufactures the chocolates with

innovative flavours and different taste. If the chocolates would been sold in the Oslo market

than the competition level is lower in the market and the demand of the chocolates are higher

which would lead towards the profitability position to the business.

The case explains that the sales of the business would be 50 units at first place which

would be improved to 420 units at the end of the year. An online portal would be prepared by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

5

the business to sell the chocolates to the customers. Though, a friend of Benjamin also wants

to do chocolates business and he agreed to buy 100 boxes of chocolate from the Benjamin at

the rate of NOK 220 each box. The revenue of the business would be improved by an

increased rate as well as the expenses of the company would be different on the basis of sales

and purchase of the business.

The main visions of the company are to offer the quality chocolates to the customers

of Oslo market. The company is using the innovative strategies and advances technology to

capture the market and improve the overall performance of the business.

Assumption and findings summary:

On the basis of the case evaluation, various estimations and the financial statements

are required to measure the viability of the business plan. The financial statements and other

estimations make it easier for the business planner to make better decision. In order to

prepare the profit and loss statement, statement of financial position, cash flow statement,

break even analysis etc. (Oliver and Schoff, 2017) few assumptions and estimations have

been made which are given as follows:

i. As the business is planning to manage inventory level of 1 month and the shipment

time of inventory is 2 weeks so it has been estimated that in the month of December,

the inventory order has been placed and received by the business.

ii. The sales of the business would be improved with a great growth rate from 50 units in

the first month to 420 units in the last month.

iii. The purchase of the chocolates would be done by the business after estimating the

future sales of the business and the entire purchased inventory for that particular

month would be sold in the same month.

iv. The website will not be treated as an asset of the business but because of the up-

gradated nature of the website (Weaver, Weston and Weaver, 2011).

v. All the personalized box of chocolates would be bought by Liv from the very first

month of sales.

vi. Exchange rate of CHF to NOK is 8 (Xe.com, 2018).

vii. Website cost has been treated as an expense.

viii. The initial investment of the business would be NOK 5,00,000.

ix. BEP level of each of the sales (online sales and Liv sales) would be calculated

differently.

5

the business to sell the chocolates to the customers. Though, a friend of Benjamin also wants

to do chocolates business and he agreed to buy 100 boxes of chocolate from the Benjamin at

the rate of NOK 220 each box. The revenue of the business would be improved by an

increased rate as well as the expenses of the company would be different on the basis of sales

and purchase of the business.

The main visions of the company are to offer the quality chocolates to the customers

of Oslo market. The company is using the innovative strategies and advances technology to

capture the market and improve the overall performance of the business.

Assumption and findings summary:

On the basis of the case evaluation, various estimations and the financial statements

are required to measure the viability of the business plan. The financial statements and other

estimations make it easier for the business planner to make better decision. In order to

prepare the profit and loss statement, statement of financial position, cash flow statement,

break even analysis etc. (Oliver and Schoff, 2017) few assumptions and estimations have

been made which are given as follows:

i. As the business is planning to manage inventory level of 1 month and the shipment

time of inventory is 2 weeks so it has been estimated that in the month of December,

the inventory order has been placed and received by the business.

ii. The sales of the business would be improved with a great growth rate from 50 units in

the first month to 420 units in the last month.

iii. The purchase of the chocolates would be done by the business after estimating the

future sales of the business and the entire purchased inventory for that particular

month would be sold in the same month.

iv. The website will not be treated as an asset of the business but because of the up-

gradated nature of the website (Weaver, Weston and Weaver, 2011).

v. All the personalized box of chocolates would be bought by Liv from the very first

month of sales.

vi. Exchange rate of CHF to NOK is 8 (Xe.com, 2018).

vii. Website cost has been treated as an expense.

viii. The initial investment of the business would be NOK 5,00,000.

ix. BEP level of each of the sales (online sales and Liv sales) would be calculated

differently.

Financial Management

6

x. Company does not have any liability.

xi. Capital of the business has been generated from the investment by Benjamin only

(Ward, 2012).

`

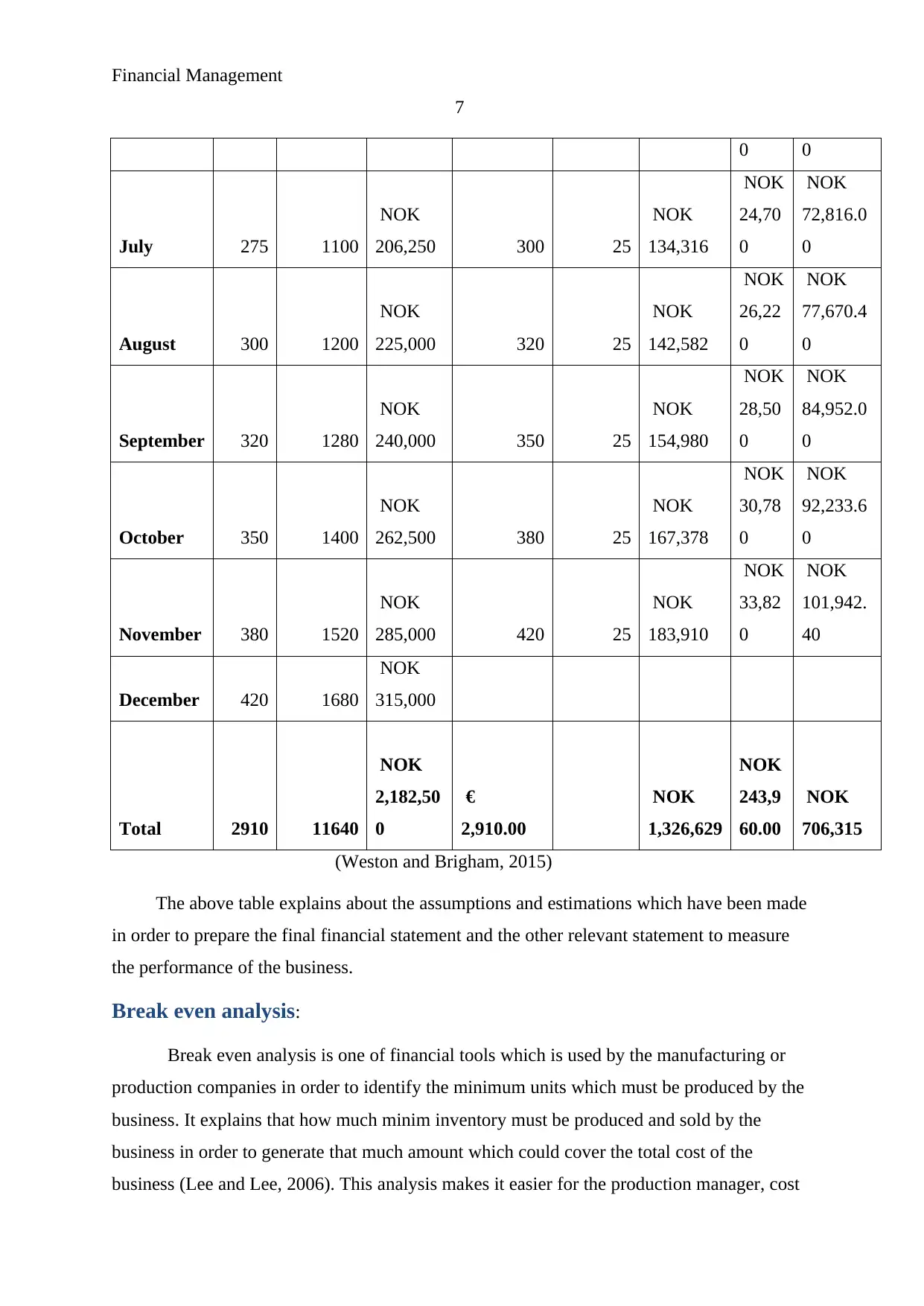

On the basis of the above assumptions following sales and purchase sheet of the

business has been prepared:

Sales

(units

)

Sales

(Packets)

Sales

(NOK)

Purchase

(units)

Purchas

e (units

for

personal

ized

sales)

Purchase

cost

Ship

ment

Discount

received

December 0 50 25

NOK

30,996

NOK

5,700

NOK

12,136.0

0

January 50 200

NOK

37,500 90 25

NOK

47,527

NOK

8,740

NOK

21,844.8

0

February 90 360

NOK

67,500 115 25

NOK

57,859

NOK

10,64

0

NOK

27,912.8

0

March 115 460

NOK

86,250 160 25

NOK

76,457

NOK

14,06

0

NOK

38,835.2

0

April 160 640

NOK

120,000 200 25

NOK

92,988

NOK

17,10

0

NOK

48,544.0

0

May 200 800

NOK

150,000 250 25

NOK

113,652

NOK

20,90

0

NOK

60,680.0

0

June 250 1000 NOK

187,500

275 25 NOK

123,984

NOK

22,80

NOK

66,748.0

6

x. Company does not have any liability.

xi. Capital of the business has been generated from the investment by Benjamin only

(Ward, 2012).

`

On the basis of the above assumptions following sales and purchase sheet of the

business has been prepared:

Sales

(units

)

Sales

(Packets)

Sales

(NOK)

Purchase

(units)

Purchas

e (units

for

personal

ized

sales)

Purchase

cost

Ship

ment

Discount

received

December 0 50 25

NOK

30,996

NOK

5,700

NOK

12,136.0

0

January 50 200

NOK

37,500 90 25

NOK

47,527

NOK

8,740

NOK

21,844.8

0

February 90 360

NOK

67,500 115 25

NOK

57,859

NOK

10,64

0

NOK

27,912.8

0

March 115 460

NOK

86,250 160 25

NOK

76,457

NOK

14,06

0

NOK

38,835.2

0

April 160 640

NOK

120,000 200 25

NOK

92,988

NOK

17,10

0

NOK

48,544.0

0

May 200 800

NOK

150,000 250 25

NOK

113,652

NOK

20,90

0

NOK

60,680.0

0

June 250 1000 NOK

187,500

275 25 NOK

123,984

NOK

22,80

NOK

66,748.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

7

0 0

July 275 1100

NOK

206,250 300 25

NOK

134,316

NOK

24,70

0

NOK

72,816.0

0

August 300 1200

NOK

225,000 320 25

NOK

142,582

NOK

26,22

0

NOK

77,670.4

0

September 320 1280

NOK

240,000 350 25

NOK

154,980

NOK

28,50

0

NOK

84,952.0

0

October 350 1400

NOK

262,500 380 25

NOK

167,378

NOK

30,78

0

NOK

92,233.6

0

November 380 1520

NOK

285,000 420 25

NOK

183,910

NOK

33,82

0

NOK

101,942.

40

December 420 1680

NOK

315,000

Total 2910 11640

NOK

2,182,50

0

€

2,910.00

NOK

1,326,629

NOK

243,9

60.00

NOK

706,315

(Weston and Brigham, 2015)

The above table explains about the assumptions and estimations which have been made

in order to prepare the final financial statement and the other relevant statement to measure

the performance of the business.

Break even analysis:

Break even analysis is one of financial tools which is used by the manufacturing or

production companies in order to identify the minimum units which must be produced by the

business. It explains that how much minim inventory must be produced and sold by the

business in order to generate that much amount which could cover the total cost of the

business (Lee and Lee, 2006). This analysis makes it easier for the production manager, cost

7

0 0

July 275 1100

NOK

206,250 300 25

NOK

134,316

NOK

24,70

0

NOK

72,816.0

0

August 300 1200

NOK

225,000 320 25

NOK

142,582

NOK

26,22

0

NOK

77,670.4

0

September 320 1280

NOK

240,000 350 25

NOK

154,980

NOK

28,50

0

NOK

84,952.0

0

October 350 1400

NOK

262,500 380 25

NOK

167,378

NOK

30,78

0

NOK

92,233.6

0

November 380 1520

NOK

285,000 420 25

NOK

183,910

NOK

33,82

0

NOK

101,942.

40

December 420 1680

NOK

315,000

Total 2910 11640

NOK

2,182,50

0

€

2,910.00

NOK

1,326,629

NOK

243,9

60.00

NOK

706,315

(Weston and Brigham, 2015)

The above table explains about the assumptions and estimations which have been made

in order to prepare the final financial statement and the other relevant statement to measure

the performance of the business.

Break even analysis:

Break even analysis is one of financial tools which is used by the manufacturing or

production companies in order to identify the minimum units which must be produced by the

business. It explains that how much minim inventory must be produced and sold by the

business in order to generate that much amount which could cover the total cost of the

business (Lee and Lee, 2006). This analysis makes it easier for the production manager, cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

8

manager and other managers to identify that whether the business should run the operations

line or not. If yes, than how many changes are required to be done in order to cover the

associated cost and improve the margin of profit of the business. The sales, price, variable

cost, contribution marginal and fixed cost are the main components in a business to measure

the breakeven point level of the business.

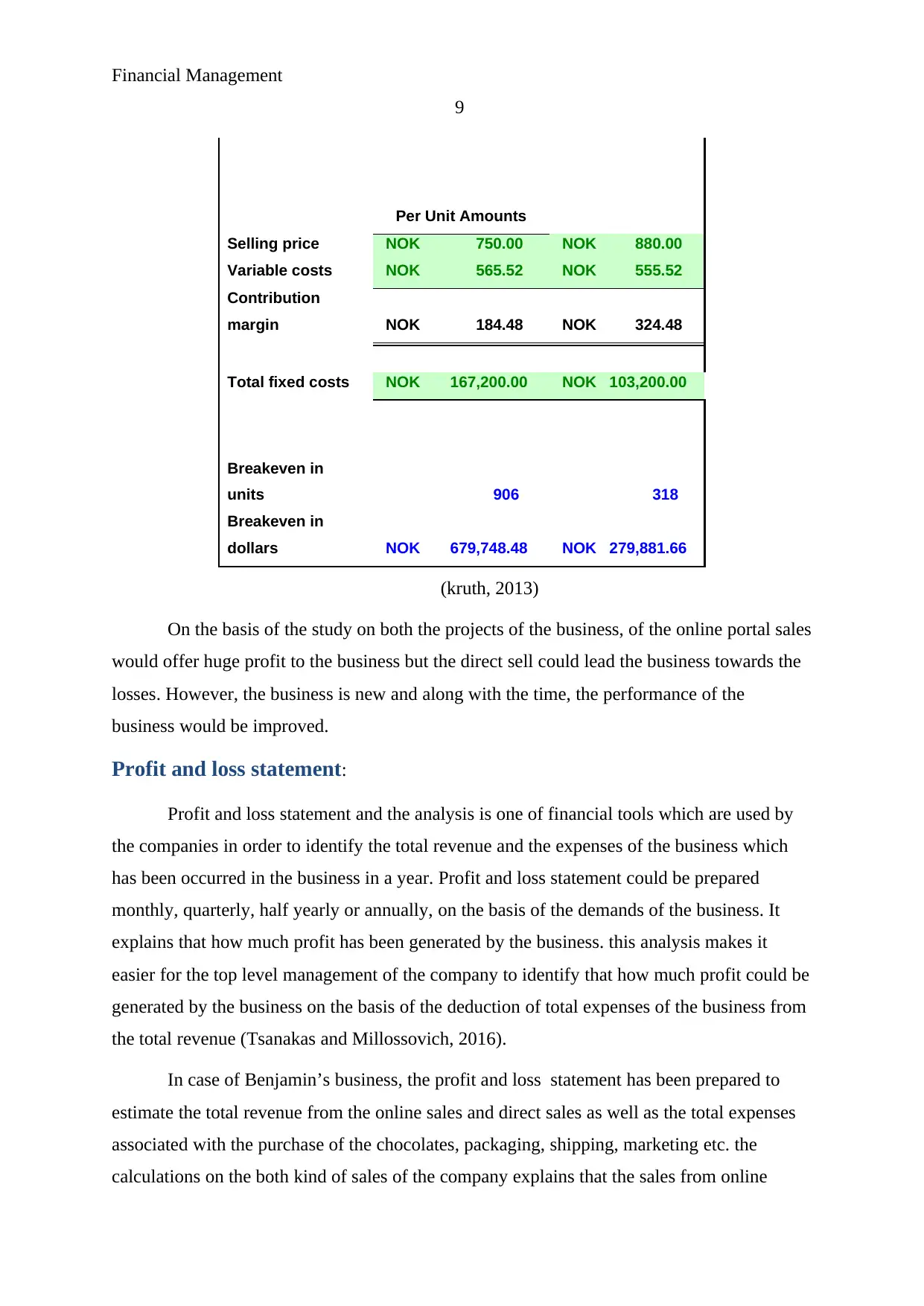

On the basis of the calculations on Benjamin’s business, it has been measured that the

business would be operated in the Oslo market where the chocolates would be sold by the

business through 2 different sources i.e. through online portal and through direct sell. In case

of sale through online portal, it has been found that the selling price per unit of the business is

NOK 750 which consist NOK 565.52 variable cost. That leads to the study that the

contribution pr margin of the business is NOK 184.48 (Zabarankin, Pavlikov and Uryasev,

2014). Further, the associated foxed cost with the business project is NOK 1,67,200. It

explains that the business is required to sell around 906 units in order to generate the revenue

which could cover all the expenses and cost of the business. In terms of amount, NOK

6,79,748.48 is required to earn by the business through selling the chocolates in the market. If

the more units would be sold by the business than the extra revenue would denote the profit

level of the business (Lord, 2007). The evaluation on total sales unit of the business explains

that the 2910 kg of chocolates would be sold by the business which is higher than the break

even sales of the business.

Further, in case of direct sell to Liv, it has been found that the selling price per unit of

the business is NOK 880 which consist NOK 555.52 variable cost. That leads to the study

that the contribution pr margin of the business is NOK 324.28. Further, the associated fixed

cost with the business project is NOK 103,200. It explains that the business is required to sell

around 318 units in order to generate the revenue which could cover all the expenses and cost

of the business. In terms of amount, NOK 279,881.66 is required to earn by the business

through selling the chocolates in the market. If the more units would be sold by the business

than the extra revenue would denote the profit level of the business (Zimmerman and Yahya-

Zadeh, 2011). The evaluation on total sales unit of the business explains that the 300 kg of

chocolates would be sold by the business which is lower than the break even sales of the

business. It explains that this process would lead to the business towards huge loss. However,

the business is new and the future demand would decrease the loss position of the business.

Cost-Volume-Profit Relationships - Breakeven

8

manager and other managers to identify that whether the business should run the operations

line or not. If yes, than how many changes are required to be done in order to cover the

associated cost and improve the margin of profit of the business. The sales, price, variable

cost, contribution marginal and fixed cost are the main components in a business to measure

the breakeven point level of the business.

On the basis of the calculations on Benjamin’s business, it has been measured that the

business would be operated in the Oslo market where the chocolates would be sold by the

business through 2 different sources i.e. through online portal and through direct sell. In case

of sale through online portal, it has been found that the selling price per unit of the business is

NOK 750 which consist NOK 565.52 variable cost. That leads to the study that the

contribution pr margin of the business is NOK 184.48 (Zabarankin, Pavlikov and Uryasev,

2014). Further, the associated foxed cost with the business project is NOK 1,67,200. It

explains that the business is required to sell around 906 units in order to generate the revenue

which could cover all the expenses and cost of the business. In terms of amount, NOK

6,79,748.48 is required to earn by the business through selling the chocolates in the market. If

the more units would be sold by the business than the extra revenue would denote the profit

level of the business (Lord, 2007). The evaluation on total sales unit of the business explains

that the 2910 kg of chocolates would be sold by the business which is higher than the break

even sales of the business.

Further, in case of direct sell to Liv, it has been found that the selling price per unit of

the business is NOK 880 which consist NOK 555.52 variable cost. That leads to the study

that the contribution pr margin of the business is NOK 324.28. Further, the associated fixed

cost with the business project is NOK 103,200. It explains that the business is required to sell

around 318 units in order to generate the revenue which could cover all the expenses and cost

of the business. In terms of amount, NOK 279,881.66 is required to earn by the business

through selling the chocolates in the market. If the more units would be sold by the business

than the extra revenue would denote the profit level of the business (Zimmerman and Yahya-

Zadeh, 2011). The evaluation on total sales unit of the business explains that the 300 kg of

chocolates would be sold by the business which is lower than the break even sales of the

business. It explains that this process would lead to the business towards huge loss. However,

the business is new and the future demand would decrease the loss position of the business.

Cost-Volume-Profit Relationships - Breakeven

Financial Management

9

Per Unit Amounts

Selling price NOK 750.00 NOK 880.00

Variable costs NOK 565.52 NOK 555.52

Contribution

margin NOK 184.48 NOK 324.48

Total fixed costs NOK 167,200.00 NOK 103,200.00

Breakeven in

units 906 318

Breakeven in

dollars NOK 679,748.48 NOK 279,881.66

(kruth, 2013)

On the basis of the study on both the projects of the business, of the online portal sales

would offer huge profit to the business but the direct sell could lead the business towards the

losses. However, the business is new and along with the time, the performance of the

business would be improved.

Profit and loss statement:

Profit and loss statement and the analysis is one of financial tools which are used by

the companies in order to identify the total revenue and the expenses of the business which

has been occurred in the business in a year. Profit and loss statement could be prepared

monthly, quarterly, half yearly or annually, on the basis of the demands of the business. It

explains that how much profit has been generated by the business. this analysis makes it

easier for the top level management of the company to identify that how much profit could be

generated by the business on the basis of the deduction of total expenses of the business from

the total revenue (Tsanakas and Millossovich, 2016).

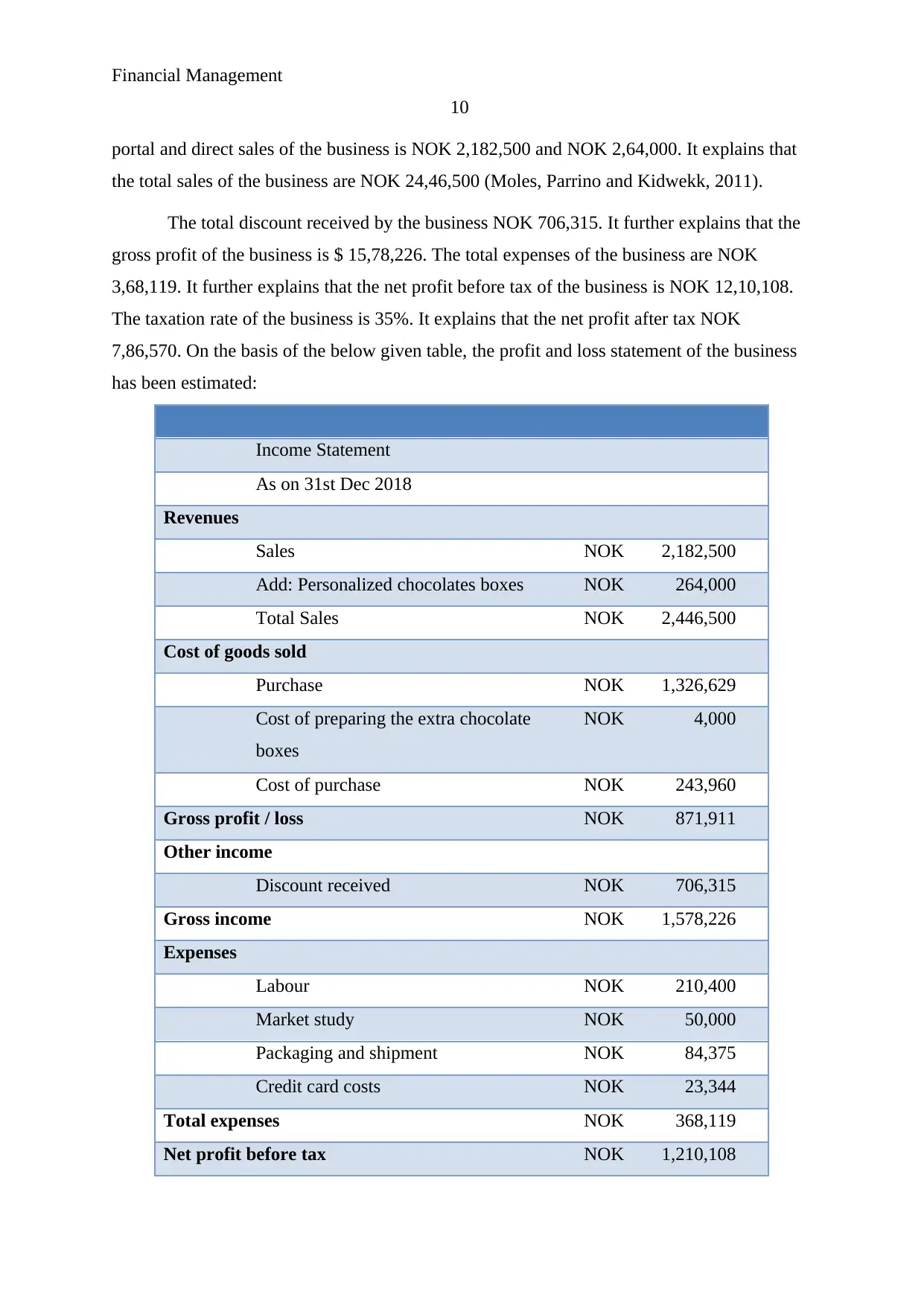

In case of Benjamin’s business, the profit and loss statement has been prepared to

estimate the total revenue from the online sales and direct sales as well as the total expenses

associated with the purchase of the chocolates, packaging, shipping, marketing etc. the

calculations on the both kind of sales of the company explains that the sales from online

9

Per Unit Amounts

Selling price NOK 750.00 NOK 880.00

Variable costs NOK 565.52 NOK 555.52

Contribution

margin NOK 184.48 NOK 324.48

Total fixed costs NOK 167,200.00 NOK 103,200.00

Breakeven in

units 906 318

Breakeven in

dollars NOK 679,748.48 NOK 279,881.66

(kruth, 2013)

On the basis of the study on both the projects of the business, of the online portal sales

would offer huge profit to the business but the direct sell could lead the business towards the

losses. However, the business is new and along with the time, the performance of the

business would be improved.

Profit and loss statement:

Profit and loss statement and the analysis is one of financial tools which are used by

the companies in order to identify the total revenue and the expenses of the business which

has been occurred in the business in a year. Profit and loss statement could be prepared

monthly, quarterly, half yearly or annually, on the basis of the demands of the business. It

explains that how much profit has been generated by the business. this analysis makes it

easier for the top level management of the company to identify that how much profit could be

generated by the business on the basis of the deduction of total expenses of the business from

the total revenue (Tsanakas and Millossovich, 2016).

In case of Benjamin’s business, the profit and loss statement has been prepared to

estimate the total revenue from the online sales and direct sales as well as the total expenses

associated with the purchase of the chocolates, packaging, shipping, marketing etc. the

calculations on the both kind of sales of the company explains that the sales from online

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

10

portal and direct sales of the business is NOK 2,182,500 and NOK 2,64,000. It explains that

the total sales of the business are NOK 24,46,500 (Moles, Parrino and Kidwekk, 2011).

The total discount received by the business NOK 706,315. It further explains that the

gross profit of the business is $ 15,78,226. The total expenses of the business are NOK

3,68,119. It further explains that the net profit before tax of the business is NOK 12,10,108.

The taxation rate of the business is 35%. It explains that the net profit after tax NOK

7,86,570. On the basis of the below given table, the profit and loss statement of the business

has been estimated:

Income Statement

As on 31st Dec 2018

Revenues

Sales NOK 2,182,500

Add: Personalized chocolates boxes NOK 264,000

Total Sales NOK 2,446,500

Cost of goods sold

Purchase NOK 1,326,629

Cost of preparing the extra chocolate

boxes

NOK 4,000

Cost of purchase NOK 243,960

Gross profit / loss NOK 871,911

Other income

Discount received NOK 706,315

Gross income NOK 1,578,226

Expenses

Labour NOK 210,400

Market study NOK 50,000

Packaging and shipment NOK 84,375

Credit card costs NOK 23,344

Total expenses NOK 368,119

Net profit before tax NOK 1,210,108

10

portal and direct sales of the business is NOK 2,182,500 and NOK 2,64,000. It explains that

the total sales of the business are NOK 24,46,500 (Moles, Parrino and Kidwekk, 2011).

The total discount received by the business NOK 706,315. It further explains that the

gross profit of the business is $ 15,78,226. The total expenses of the business are NOK

3,68,119. It further explains that the net profit before tax of the business is NOK 12,10,108.

The taxation rate of the business is 35%. It explains that the net profit after tax NOK

7,86,570. On the basis of the below given table, the profit and loss statement of the business

has been estimated:

Income Statement

As on 31st Dec 2018

Revenues

Sales NOK 2,182,500

Add: Personalized chocolates boxes NOK 264,000

Total Sales NOK 2,446,500

Cost of goods sold

Purchase NOK 1,326,629

Cost of preparing the extra chocolate

boxes

NOK 4,000

Cost of purchase NOK 243,960

Gross profit / loss NOK 871,911

Other income

Discount received NOK 706,315

Gross income NOK 1,578,226

Expenses

Labour NOK 210,400

Market study NOK 50,000

Packaging and shipment NOK 84,375

Credit card costs NOK 23,344

Total expenses NOK 368,119

Net profit before tax NOK 1,210,108

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

11

Less: 35% tax NOK 423,538

Net profit after tax NOK 786,570

(Madura, 2014)

Revenues

The revenue of the business has been estimated on the basis of the given case and the

assumptions and it has been found that the calculations on the both kind of sales of the

company explains that the sales from online portal and direct sales of the business is NOK

2,182,500 and NOK 2,64,000. It explains that the total sales of the business are NOK

24,46,500. The revenue per unit of the company in case of online portal and direct sales are

NOK 750 and NOK 880.

Expenditures

Further, the expenses of the business has been estimated on the basis of the given case

and the assumptions and it has been found that the calculations on the both kind of sales of

the company explains that the total expenses of the business is NOK 3,68,119 while the cost

of purchase of the company and the shipping cost of the material of the business is NOK

13,26,629 and NOK 243,960 (Kinsky, 2011). It explains that the total sales of the business

are NOK 24,46,500. The revenue per unit of the company in case of online portal and direct

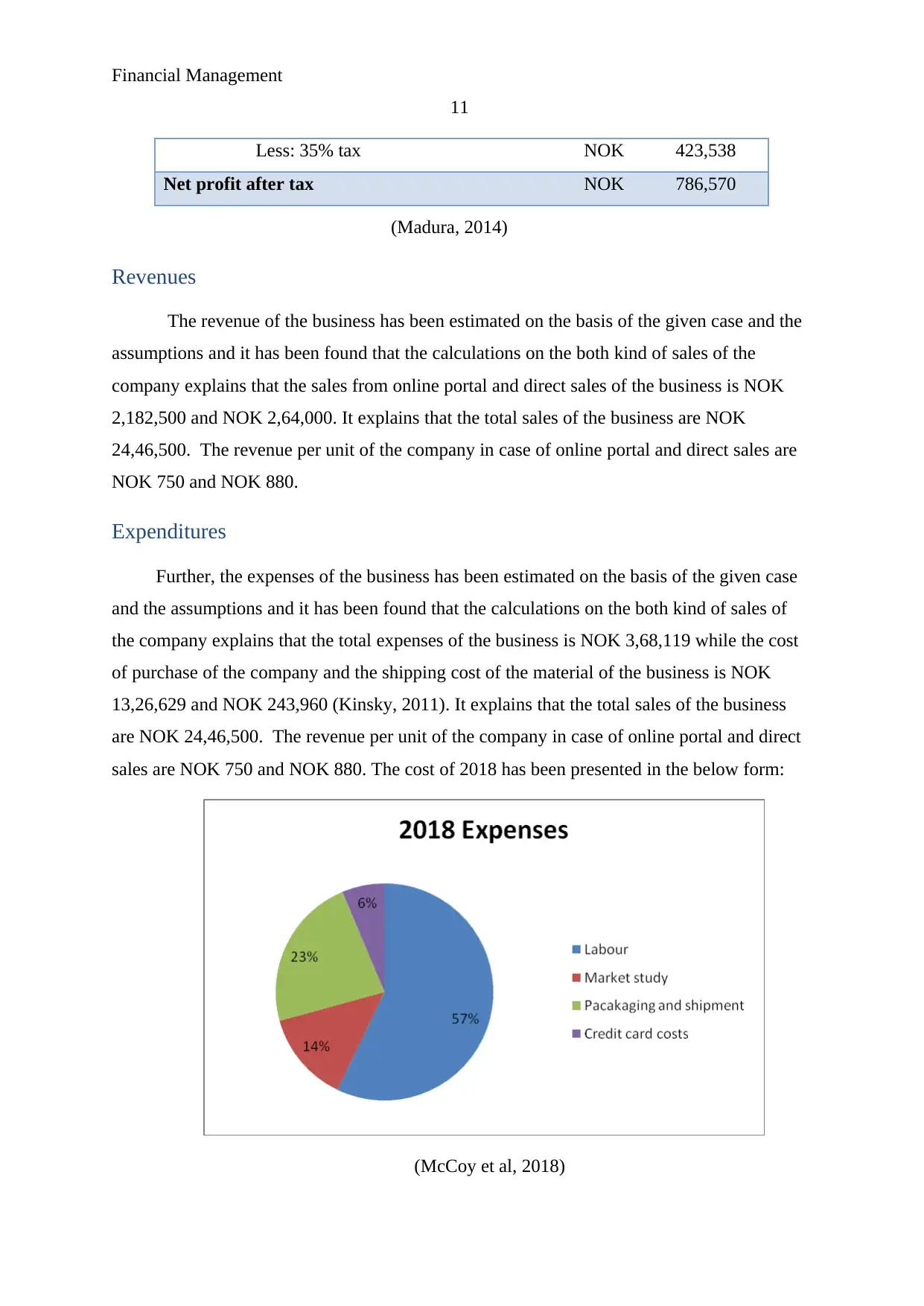

sales are NOK 750 and NOK 880. The cost of 2018 has been presented in the below form:

(McCoy et al, 2018)

11

Less: 35% tax NOK 423,538

Net profit after tax NOK 786,570

(Madura, 2014)

Revenues

The revenue of the business has been estimated on the basis of the given case and the

assumptions and it has been found that the calculations on the both kind of sales of the

company explains that the sales from online portal and direct sales of the business is NOK

2,182,500 and NOK 2,64,000. It explains that the total sales of the business are NOK

24,46,500. The revenue per unit of the company in case of online portal and direct sales are

NOK 750 and NOK 880.

Expenditures

Further, the expenses of the business has been estimated on the basis of the given case

and the assumptions and it has been found that the calculations on the both kind of sales of

the company explains that the total expenses of the business is NOK 3,68,119 while the cost

of purchase of the company and the shipping cost of the material of the business is NOK

13,26,629 and NOK 243,960 (Kinsky, 2011). It explains that the total sales of the business

are NOK 24,46,500. The revenue per unit of the company in case of online portal and direct

sales are NOK 750 and NOK 880. The cost of 2018 has been presented in the below form:

(McCoy et al, 2018)

Financial Management

12

On the basis of the above graph of 2018 expenses, it has been found that highest share

of expenses is hold by the labour expenses. Labour expenses of the business are 57% of the

total expenses of the business. Further, 23% of the expenses are hold by the packaging and

shipment charges and 14% and 6% are hold by the market study and credit card cost of the

business. It explains that if the labour cost of the business could be controlled by the business

than the profitability level of the business would be improved more.

Balance sheet:

Balance sheet statement and the analysis is one of financial tools which are used by

the companies in order to identify the total assets, liabilities and equity capital of the business

which is managed by the business on a particular date. Statement of financial performance

could be prepared monthly, quarterly, half yearly or annually, on the basis of the demands of

the business (Krnatz, 2016). It explains that how much resources have been managed by the

business. this analysis makes it easier for the top level management of the company to

identify that how much the company is financial strong as well as it also depicts about the

liquidity and financial gearing risk of the business.

Balance Sheet

As on 31st Dec 2018

Assets

Current assets

Cash at hand NOK

12

On the basis of the above graph of 2018 expenses, it has been found that highest share

of expenses is hold by the labour expenses. Labour expenses of the business are 57% of the

total expenses of the business. Further, 23% of the expenses are hold by the packaging and

shipment charges and 14% and 6% are hold by the market study and credit card cost of the

business. It explains that if the labour cost of the business could be controlled by the business

than the profitability level of the business would be improved more.

Balance sheet:

Balance sheet statement and the analysis is one of financial tools which are used by

the companies in order to identify the total assets, liabilities and equity capital of the business

which is managed by the business on a particular date. Statement of financial performance

could be prepared monthly, quarterly, half yearly or annually, on the basis of the demands of

the business (Krnatz, 2016). It explains that how much resources have been managed by the

business. this analysis makes it easier for the top level management of the company to

identify that how much the company is financial strong as well as it also depicts about the

liquidity and financial gearing risk of the business.

Balance Sheet

As on 31st Dec 2018

Assets

Current assets

Cash at hand NOK

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.