Report on Financial Statements and Indirect Equity Interest Analysis

VerifiedAdded on 2023/03/31

|17

|913

|241

Report

AI Summary

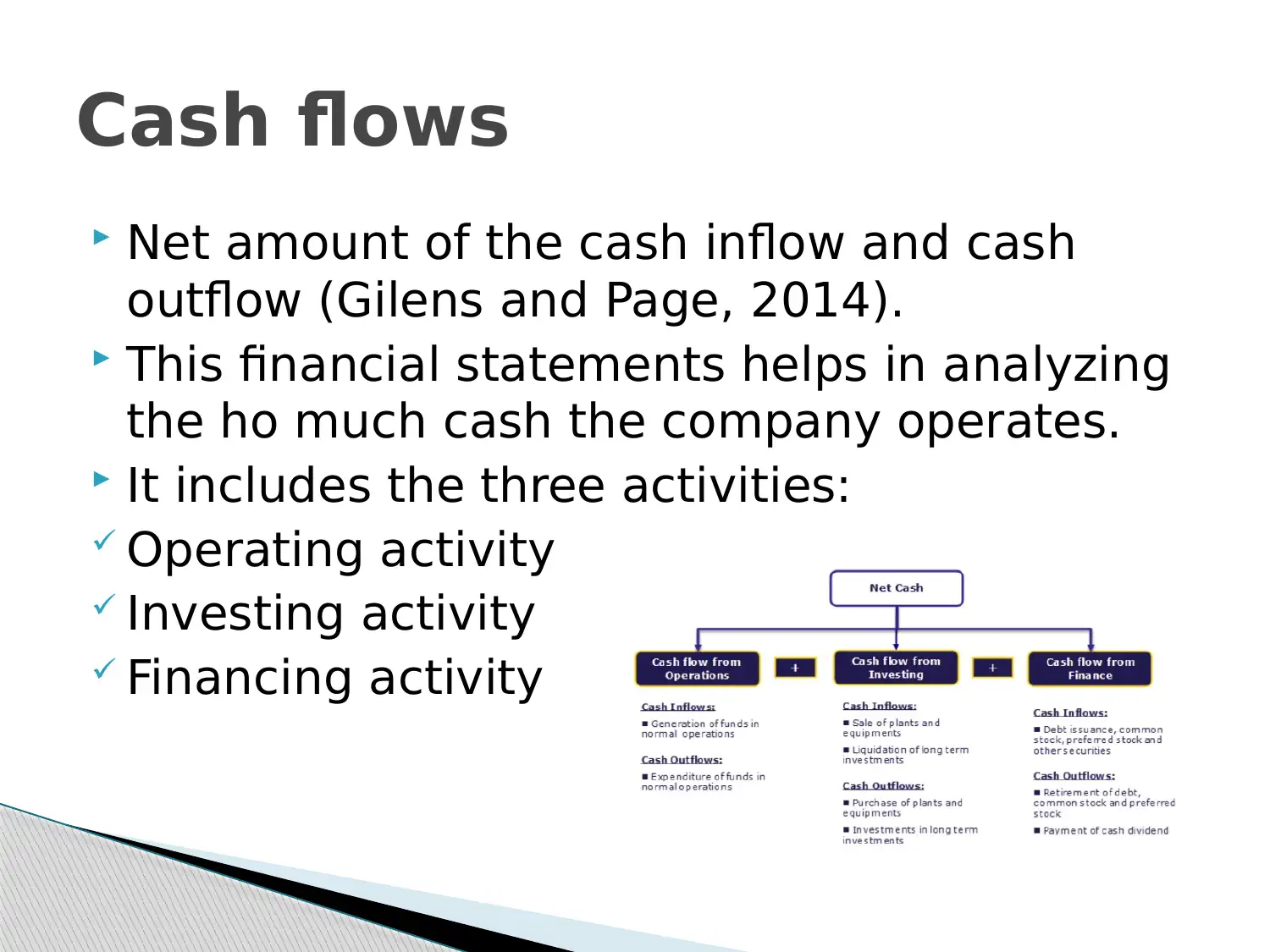

This report provides an overview of financial statements, specifically focusing on scenarios involving indirect equity interests. It begins by defining financial statements and their key components, including the balance sheet, income statement, and cash flow statement. The report then delves into consolidated financial statements, explaining how parent and subsidiary companies are presented as a single entity. The core of the report discusses indirect equity interest, its calculation, and differentiation from direct ownership interest. Furthermore, it addresses the accounting for non-sequential acquisitions and the concept of non-controlling interest, highlighting their impact on financial reporting. The report concludes by emphasizing the importance of financial statements in assessing a company's performance and provides references for further reading. Desklib offers a platform where students can find similar solved assignments and study resources.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.