Analyzing RBS's Sustainability Failure: A Detailed Case Study

VerifiedAdded on 2023/06/13

|15

|626

|474

Case Study

AI Summary

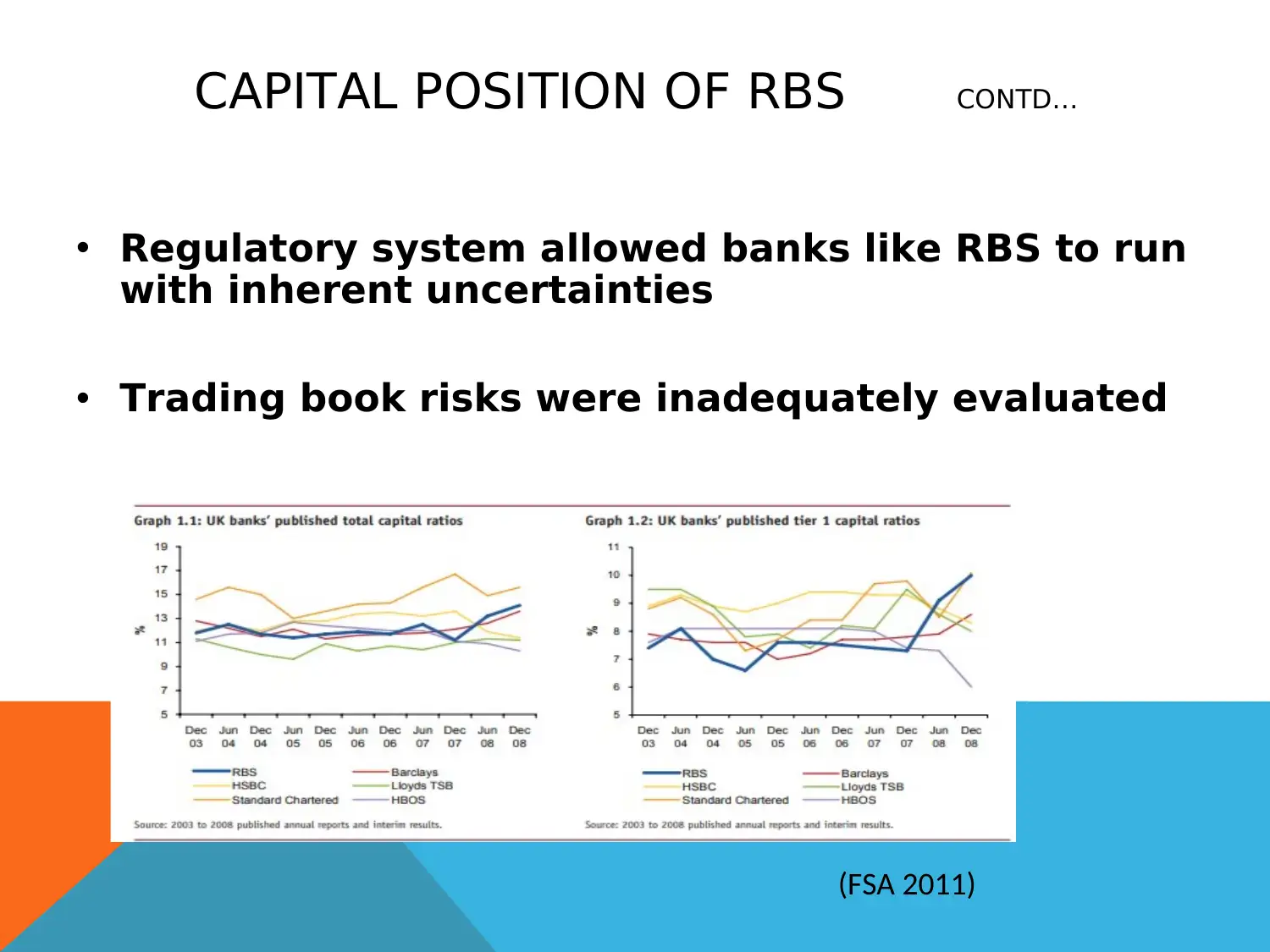

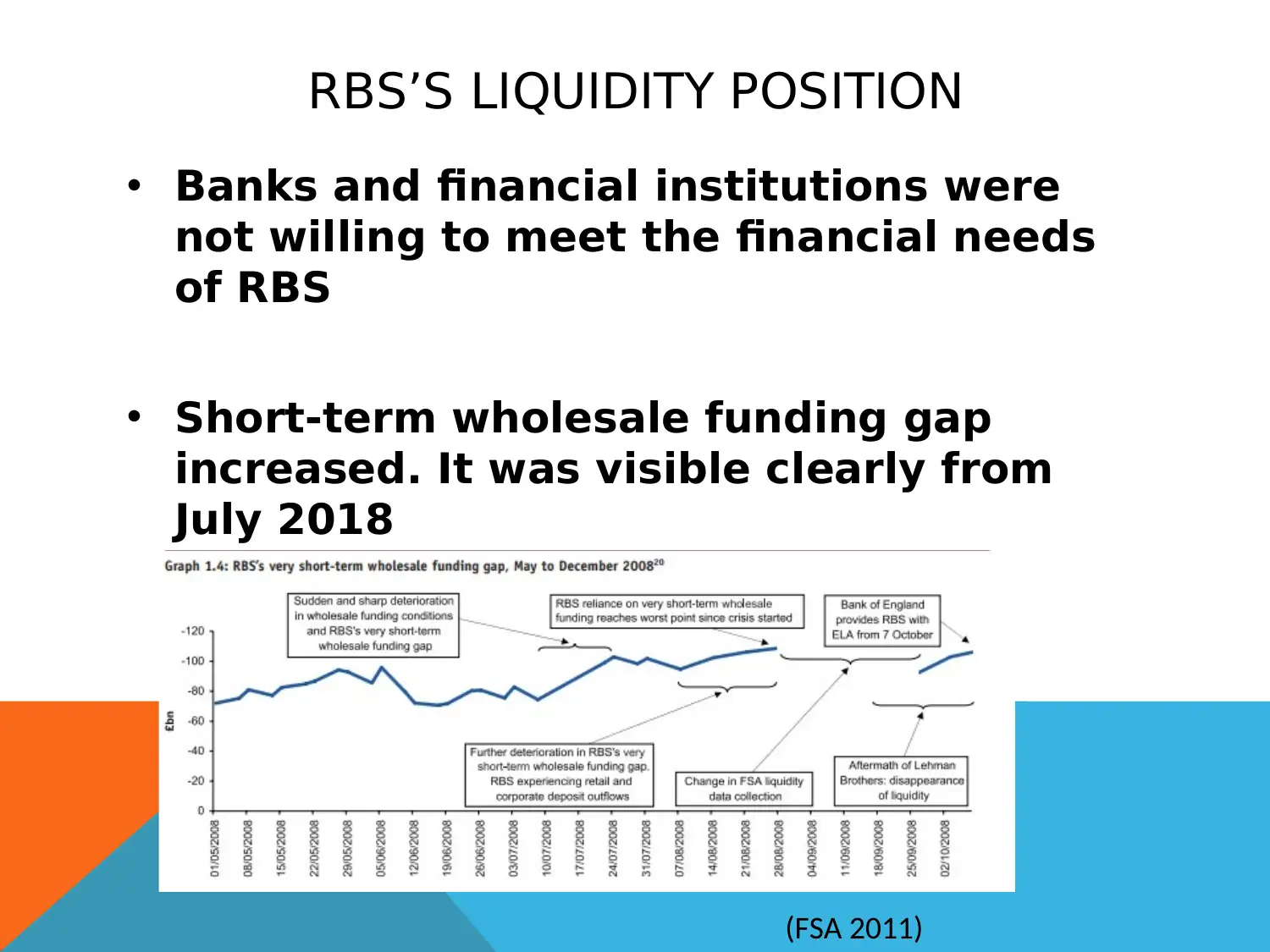

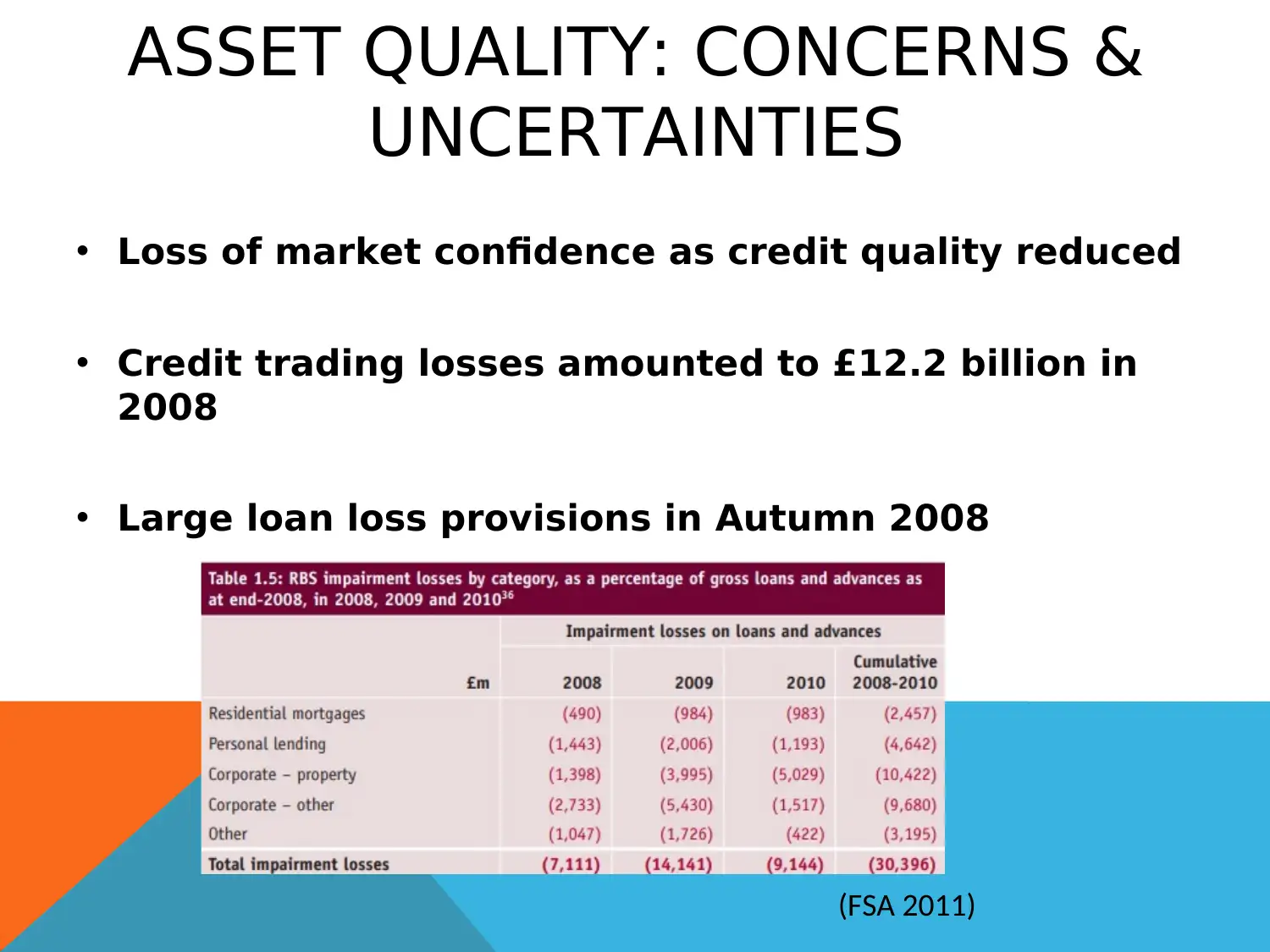

This case study examines the sustainability failure of the Royal Bank of Scotland (RBS), tracing its roots back to its establishment in 1727 and subsequent expansion. The analysis identifies key factors contributing to the bank's collapse, including its capital and liquidity positions, uncertainties in asset quality, losses in credit trading activities, and the acquisition of ABN AMRO. The study highlights the inadequate capital levels, reliance on short-term wholesale funding, deterioration in market confidence, and poor management decisions as critical vulnerabilities. Ultimately, the case study provides valuable lessons regarding risk assessment, decision-making processes, and the importance of maintaining a strong equity base, emphasizing the need for institutions to prioritize liquidity and seek independent advice on significant transactions. Desklib provides access to similar case studies and solved assignments for students.

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.