Analyzing Impact of WCM & CG on Firm Performance: Detailed Report

VerifiedAdded on 2023/06/10

|24

|6813

|72

Report

AI Summary

This report analyzes the impact of working capital management (WCM) and corporate governance (CG) on firm performance, using Return on Assets (ROA), Return on Equity (ROE), and Net Profit Margin (NPM) as key performance indicators. WCM is assessed through metrics like Cash Conversion Cycle (CCC), Average Collection Period (ACP), Average Inventory Period (AIP), and Average Payment Period (APP). CG is evaluated using Board Size (BSIZE), Non-Executive Directors (NEDs), and CEO Duality. The analysis incorporates control variables such as firm size (FSIZE), leverage, and liquidity. Descriptive statistics, correlation analysis, and linear regression models are employed to test hypotheses regarding the relationships between these variables. The findings suggest significant correlations between WCM components like ACP and APP, and firm performance, as well as between CG factors like BSIZE and CEO duality, and performance metrics. Leverage is found to have a negative correlation with firm performance, while liquidity and firm size show positive correlations.

Running head: IMPACT OF WCM AND CG ON FIRM PERFORMANCE

IMPACT OF WCM AND CG ON FIRM PERFORMANCE

Name of Student

Name of University

Author Note

IMPACT OF WCM AND CG ON FIRM PERFORMANCE

Name of Student

Name of University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1IMPACT OF WCM AND CG ON FIRM PERFORMANCE

Table of Contents

Chapter 4..........................................................................................................................................2

Analysis.......................................................................................................................................2

Descriptive Statistics...............................................................................................................3

Correlation...............................................................................................................................5

Regression................................................................................................................................8

Discussion..................................................................................................................................11

Chapter 5........................................................................................................................................15

Conclusion.................................................................................................................................15

Limitations.................................................................................................................................16

Further Research........................................................................................................................17

Table of Contents

Chapter 4..........................................................................................................................................2

Analysis.......................................................................................................................................2

Descriptive Statistics...............................................................................................................3

Correlation...............................................................................................................................5

Regression................................................................................................................................8

Discussion..................................................................................................................................11

Chapter 5........................................................................................................................................15

Conclusion.................................................................................................................................15

Limitations.................................................................................................................................16

Further Research........................................................................................................................17

2IMPACT OF WCM AND CG ON FIRM PERFORMANCE

Chapter 4

Analysis

The results of the analysis of the connection between firm performance and working

capital management and again on how the firm performance might be affected by corporate

governance of the firm are hence discussed. To study these two relationships the study first

defined firm performance using the Return on Asset or the ROA, the Return on Equity or the

ROE and the Net Profit Margin or NPM of the firm. The study then defined a number of

parameters to gauge the working capital management, using aspects such as, Cash Conversion

Cycle or CCC, the ACP or the Average Collection Period, the AIP or the Average Inventory

Period and the APP or Average Payment Period. The idea is to see how each of these aspects

may impact each of the parameters which represent firm performance. Again, the study defined a

number of parameters to gauge the corporate governance, using aspects such as, Board Size

denoted as BSIZE, Non-executive directors denoted as NEDs and CEO Duality. The study then

investigates the relationship between these parameters with those of firm performance.

Furthermore the study also considers a number of control variables such as firm size or FSIZE,

LEVERAGE and LIQUIDITY.

This section reports on the results of the tests for validity of the seven hypotheses as

defined for the purpose of the study. The analysis included a scrutiny of the descriptive measures

on all the variables defined. The correlation measure between each of the independent variables

with that of the dependent variable, firm performance was then computed to look for any

tentative linear relationship. The study further explores the veracity of the conjectures presuming

a linear relationship between the dependent and seven of the independent variables as specified

Chapter 4

Analysis

The results of the analysis of the connection between firm performance and working

capital management and again on how the firm performance might be affected by corporate

governance of the firm are hence discussed. To study these two relationships the study first

defined firm performance using the Return on Asset or the ROA, the Return on Equity or the

ROE and the Net Profit Margin or NPM of the firm. The study then defined a number of

parameters to gauge the working capital management, using aspects such as, Cash Conversion

Cycle or CCC, the ACP or the Average Collection Period, the AIP or the Average Inventory

Period and the APP or Average Payment Period. The idea is to see how each of these aspects

may impact each of the parameters which represent firm performance. Again, the study defined a

number of parameters to gauge the corporate governance, using aspects such as, Board Size

denoted as BSIZE, Non-executive directors denoted as NEDs and CEO Duality. The study then

investigates the relationship between these parameters with those of firm performance.

Furthermore the study also considers a number of control variables such as firm size or FSIZE,

LEVERAGE and LIQUIDITY.

This section reports on the results of the tests for validity of the seven hypotheses as

defined for the purpose of the study. The analysis included a scrutiny of the descriptive measures

on all the variables defined. The correlation measure between each of the independent variables

with that of the dependent variable, firm performance was then computed to look for any

tentative linear relationship. The study further explores the veracity of the conjectures presuming

a linear relationship between the dependent and seven of the independent variables as specified

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3IMPACT OF WCM AND CG ON FIRM PERFORMANCE

in the previous sections using linear regression analysis. It is in this part of the analysis that the

relationship is considered in light of the control variables as well.

Descriptive Statistics

A total of 400 firms were considered for the scope of the study. The mean ROA was of

all the firms considered was found to be 0.02387 that is 2.38%. The maximum was found to be

0.5489 or 54.89%, the minimum was -0.4569 or -45.69% that is a loss of 45.69%. The median

was 0.2271or 2.27% and the standard deviation 0.0944 which means that the estimate of mean is

quite consistent. Again the mean value of ROE of all the firms included in the study was

computed as 0.01751 that is 1.751% and the standard deviation 0.2005 which means that the

estimate of mean is quite consistent. The median value was found to be 0.0338 or 3.38%.Again,

the maximum ROE was found to be 0.781541 or 78.15% and the minimum ROE among the

observed firms was –1.987 or -198.76% that is a loss of 198.75%. The average NPM of all the

observed firms was found to be 0.02043 that is 2.043%. The maximum NPM was found to be

equal to -0.77325 or 77.325% and the minimum NPM was found to be equal to -1.38081 or -

138.081% that is a loss of 138.081%. The median of the NPM of the firms that were observed

was 0.0335 or 3.35% and the standard deviation of the NPM was 0.1966 implying that the

estimated mean is consistent. The mean ACP of all the firm sobserved in the study was found to

be equal to 100.56. The median was observed to be 73.5 , now this differs from the mean and the

standard deviation being equal to 83.30 suggests that the data is not that consistent and is

possibly negatively skewed. The maximum ACP of the firms was computed to be 608, the

minimum was found to be 0. The data for ACP is suspected to have outliers which is inflating

the mean. The average of AIP of all the firms considered in the sudy was found to be equal to

in the previous sections using linear regression analysis. It is in this part of the analysis that the

relationship is considered in light of the control variables as well.

Descriptive Statistics

A total of 400 firms were considered for the scope of the study. The mean ROA was of

all the firms considered was found to be 0.02387 that is 2.38%. The maximum was found to be

0.5489 or 54.89%, the minimum was -0.4569 or -45.69% that is a loss of 45.69%. The median

was 0.2271or 2.27% and the standard deviation 0.0944 which means that the estimate of mean is

quite consistent. Again the mean value of ROE of all the firms included in the study was

computed as 0.01751 that is 1.751% and the standard deviation 0.2005 which means that the

estimate of mean is quite consistent. The median value was found to be 0.0338 or 3.38%.Again,

the maximum ROE was found to be 0.781541 or 78.15% and the minimum ROE among the

observed firms was –1.987 or -198.76% that is a loss of 198.75%. The average NPM of all the

observed firms was found to be 0.02043 that is 2.043%. The maximum NPM was found to be

equal to -0.77325 or 77.325% and the minimum NPM was found to be equal to -1.38081 or -

138.081% that is a loss of 138.081%. The median of the NPM of the firms that were observed

was 0.0335 or 3.35% and the standard deviation of the NPM was 0.1966 implying that the

estimated mean is consistent. The mean ACP of all the firm sobserved in the study was found to

be equal to 100.56. The median was observed to be 73.5 , now this differs from the mean and the

standard deviation being equal to 83.30 suggests that the data is not that consistent and is

possibly negatively skewed. The maximum ACP of the firms was computed to be 608, the

minimum was found to be 0. The data for ACP is suspected to have outliers which is inflating

the mean. The average of AIP of all the firms considered in the sudy was found to be equal to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4IMPACT OF WCM AND CG ON FIRM PERFORMANCE

173.428. The maximum AIP among all the firms was 856 and the minimum was 0. The median

was found to be 149 implying that the estimated mean differs from median to a great degree and

the standard deviation of the AIP values was equal to 129.6942. This suggests that the data is not

that consistent.The data is suspected to have outliers which is inflating the mean.The mean APP

of all the firms considered was found to be 89.132. The maximum was found to be 642 the

minimum was 0. The median value of APP was found to be 65.The standard deviation was

computed as 83.098 which suggests that the data is not that consistent and the estimated mean

differs from median to a great degree. The data is suspected to have outliers which is inflating

the mean. The mean CCC of all the firms in the study that were considered was found to be

187.855. The maximum CCC was found to be 960 and the minimum of the CCC was computed

as -141. The median was found to be 154. The standard deviation of CCC is 154.7745 which

suggests that the estimate of mean CCC is not consistent.. The observations on CCC is suspected

to have outliers which is inflating the mean.The mean BSIZE of all the firms considered was

found to be 8.24 or approximately 8. The maximum was found to be 13 the minimum was 5. The

median was 9 standard deviation 2.178 which suggests that the data is consistent.The mean

number NEDs of all the firms considered was found to be 0.87 or approximately 1. The

maximum was found to be 1 the minimum was 0. The median was 0.88 which is also

approximately 1 standard deviation 0.112 which suggests that the data is consistent. CEO duality

has the mean 0.17 or approximately 0 and median is also 0. The standard deviation is 0.37 which

is low and so the estimate is believed to be consistent. The maximum is 1 and minimum 0. The

mean value of leverage of all the observed firms that were included in the analysis was found to

be 0.315 and the standard deviation was 0.1832 which suggests that the data is consistent. The

median was computed as 0.31558. The maximum was found to be 0.998 and the minimum was

173.428. The maximum AIP among all the firms was 856 and the minimum was 0. The median

was found to be 149 implying that the estimated mean differs from median to a great degree and

the standard deviation of the AIP values was equal to 129.6942. This suggests that the data is not

that consistent.The data is suspected to have outliers which is inflating the mean.The mean APP

of all the firms considered was found to be 89.132. The maximum was found to be 642 the

minimum was 0. The median value of APP was found to be 65.The standard deviation was

computed as 83.098 which suggests that the data is not that consistent and the estimated mean

differs from median to a great degree. The data is suspected to have outliers which is inflating

the mean. The mean CCC of all the firms in the study that were considered was found to be

187.855. The maximum CCC was found to be 960 and the minimum of the CCC was computed

as -141. The median was found to be 154. The standard deviation of CCC is 154.7745 which

suggests that the estimate of mean CCC is not consistent.. The observations on CCC is suspected

to have outliers which is inflating the mean.The mean BSIZE of all the firms considered was

found to be 8.24 or approximately 8. The maximum was found to be 13 the minimum was 5. The

median was 9 standard deviation 2.178 which suggests that the data is consistent.The mean

number NEDs of all the firms considered was found to be 0.87 or approximately 1. The

maximum was found to be 1 the minimum was 0. The median was 0.88 which is also

approximately 1 standard deviation 0.112 which suggests that the data is consistent. CEO duality

has the mean 0.17 or approximately 0 and median is also 0. The standard deviation is 0.37 which

is low and so the estimate is believed to be consistent. The maximum is 1 and minimum 0. The

mean value of leverage of all the observed firms that were included in the analysis was found to

be 0.315 and the standard deviation was 0.1832 which suggests that the data is consistent. The

median was computed as 0.31558. The maximum was found to be 0.998 and the minimum was

5IMPACT OF WCM AND CG ON FIRM PERFORMANCE

computed to be 0.2961. The mean liquidity of all the firms considered was found to be 2.855.

The maximum was found to be 28.09 the minimum was 0.37946. The median of the observed

liquidity of all the firms was 2.124 and the standard deviation of liquidity was 2.617 which

suggests that the data is consistent.

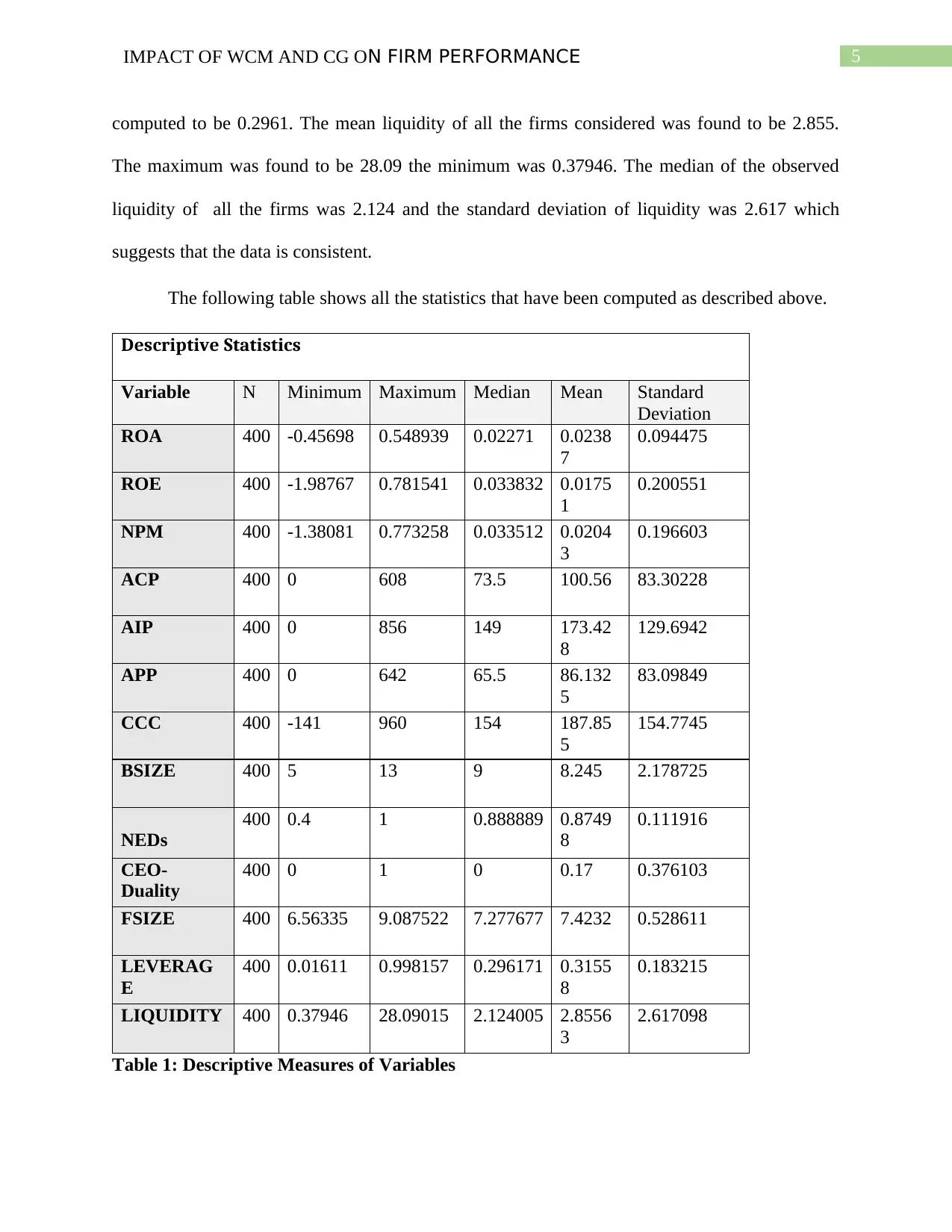

The following table shows all the statistics that have been computed as described above.

Descriptive Statistics

Variable N Minimum Maximum Median Mean Standard

Deviation

ROA 400 -0.45698 0.548939 0.02271 0.0238

7

0.094475

ROE 400 -1.98767 0.781541 0.033832 0.0175

1

0.200551

NPM 400 -1.38081 0.773258 0.033512 0.0204

3

0.196603

ACP 400 0 608 73.5 100.56 83.30228

AIP 400 0 856 149 173.42

8

129.6942

APP 400 0 642 65.5 86.132

5

83.09849

CCC 400 -141 960 154 187.85

5

154.7745

BSIZE 400 5 13 9 8.245 2.178725

NEDs

400 0.4 1 0.888889 0.8749

8

0.111916

CEO-

Duality

400 0 1 0 0.17 0.376103

FSIZE 400 6.56335 9.087522 7.277677 7.4232 0.528611

LEVERAG

E

400 0.01611 0.998157 0.296171 0.3155

8

0.183215

LIQUIDITY 400 0.37946 28.09015 2.124005 2.8556

3

2.617098

Table 1: Descriptive Measures of Variables

computed to be 0.2961. The mean liquidity of all the firms considered was found to be 2.855.

The maximum was found to be 28.09 the minimum was 0.37946. The median of the observed

liquidity of all the firms was 2.124 and the standard deviation of liquidity was 2.617 which

suggests that the data is consistent.

The following table shows all the statistics that have been computed as described above.

Descriptive Statistics

Variable N Minimum Maximum Median Mean Standard

Deviation

ROA 400 -0.45698 0.548939 0.02271 0.0238

7

0.094475

ROE 400 -1.98767 0.781541 0.033832 0.0175

1

0.200551

NPM 400 -1.38081 0.773258 0.033512 0.0204

3

0.196603

ACP 400 0 608 73.5 100.56 83.30228

AIP 400 0 856 149 173.42

8

129.6942

APP 400 0 642 65.5 86.132

5

83.09849

CCC 400 -141 960 154 187.85

5

154.7745

BSIZE 400 5 13 9 8.245 2.178725

NEDs

400 0.4 1 0.888889 0.8749

8

0.111916

CEO-

Duality

400 0 1 0 0.17 0.376103

FSIZE 400 6.56335 9.087522 7.277677 7.4232 0.528611

LEVERAG

E

400 0.01611 0.998157 0.296171 0.3155

8

0.183215

LIQUIDITY 400 0.37946 28.09015 2.124005 2.8556

3

2.617098

Table 1: Descriptive Measures of Variables

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6IMPACT OF WCM AND CG ON FIRM PERFORMANCE

Correlation

The Pearson’s correlation coefficient between the independent variable ACP with the

dependent variables ROA, ROE and NPM are -0.2299, -0.1948 and -0.363 respectively. All were

found to be significant at 5% level of significance. Hence it is suggested that ACP effects firm

performance is a negative and mild way, that is increase in ACP corresponds with decrease in

firm performance.The Pearson’s correlation coefficient between the independent variable P with

the dependent variables ROA, ROE and NPM are -0.1763, -0.09 and -0.209 respectively. All

except the correlation with ROE were found to be significant at 5% level of significance.The

Pearson’s correlation coefficient between the independent variable APP with the dependent

variables ROA, ROE and NPM are -0.2673, -0.2528 and -0.398 respectively. All were found to

be negatively correlated and significant at 5% level of significance. The Pearson’s correlation

coefficient between the independent variable CCC with the dependent variables ROA, ROE and

NPM are -0.1279, -0.047 and -0.156 respectively. All except the correlation with ROE were

found to be significant at 5% level of significance.

Correlation

The Pearson’s correlation coefficient between the independent variable ACP with the

dependent variables ROA, ROE and NPM are -0.2299, -0.1948 and -0.363 respectively. All were

found to be significant at 5% level of significance. Hence it is suggested that ACP effects firm

performance is a negative and mild way, that is increase in ACP corresponds with decrease in

firm performance.The Pearson’s correlation coefficient between the independent variable P with

the dependent variables ROA, ROE and NPM are -0.1763, -0.09 and -0.209 respectively. All

except the correlation with ROE were found to be significant at 5% level of significance.The

Pearson’s correlation coefficient between the independent variable APP with the dependent

variables ROA, ROE and NPM are -0.2673, -0.2528 and -0.398 respectively. All were found to

be negatively correlated and significant at 5% level of significance. The Pearson’s correlation

coefficient between the independent variable CCC with the dependent variables ROA, ROE and

NPM are -0.1279, -0.047 and -0.156 respectively. All except the correlation with ROE were

found to be significant at 5% level of significance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7IMPACT OF WCM AND CG ON FIRM PERFORMANCE

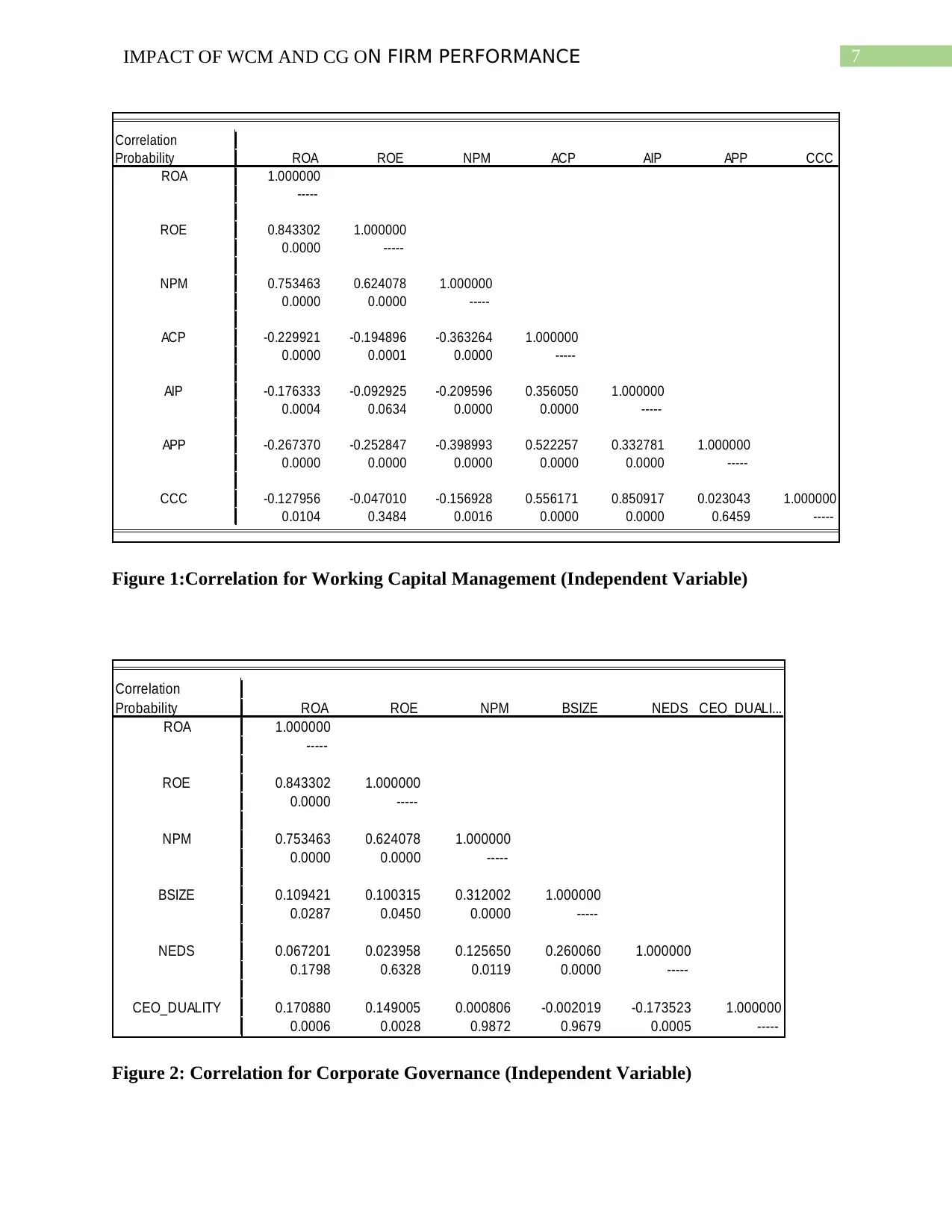

Correlation

Probability ROA ROE NPM ACP AIP APP CCC

ROA 1.000000

-----

ROE 0.843302 1.000000

0.0000 -----

NPM 0.753463 0.624078 1.000000

0.0000 0.0000 -----

ACP -0.229921 -0.194896 -0.363264 1.000000

0.0000 0.0001 0.0000 -----

AIP -0.176333 -0.092925 -0.209596 0.356050 1.000000

0.0004 0.0634 0.0000 0.0000 -----

APP -0.267370 -0.252847 -0.398993 0.522257 0.332781 1.000000

0.0000 0.0000 0.0000 0.0000 0.0000 -----

CCC -0.127956 -0.047010 -0.156928 0.556171 0.850917 0.023043 1.000000

0.0104 0.3484 0.0016 0.0000 0.0000 0.6459 -----

Figure 1:Correlation for Working Capital Management (Independent Variable)

Correlation

Probability ROA ROE NPM BSIZE NEDS CEO_DUALI...

ROA 1.000000

-----

ROE 0.843302 1.000000

0.0000 -----

NPM 0.753463 0.624078 1.000000

0.0000 0.0000 -----

BSIZE 0.109421 0.100315 0.312002 1.000000

0.0287 0.0450 0.0000 -----

NEDS 0.067201 0.023958 0.125650 0.260060 1.000000

0.1798 0.6328 0.0119 0.0000 -----

CEO_DUALITY 0.170880 0.149005 0.000806 -0.002019 -0.173523 1.000000

0.0006 0.0028 0.9872 0.9679 0.0005 -----

Figure 2: Correlation for Corporate Governance (Independent Variable)

Correlation

Probability ROA ROE NPM ACP AIP APP CCC

ROA 1.000000

-----

ROE 0.843302 1.000000

0.0000 -----

NPM 0.753463 0.624078 1.000000

0.0000 0.0000 -----

ACP -0.229921 -0.194896 -0.363264 1.000000

0.0000 0.0001 0.0000 -----

AIP -0.176333 -0.092925 -0.209596 0.356050 1.000000

0.0004 0.0634 0.0000 0.0000 -----

APP -0.267370 -0.252847 -0.398993 0.522257 0.332781 1.000000

0.0000 0.0000 0.0000 0.0000 0.0000 -----

CCC -0.127956 -0.047010 -0.156928 0.556171 0.850917 0.023043 1.000000

0.0104 0.3484 0.0016 0.0000 0.0000 0.6459 -----

Figure 1:Correlation for Working Capital Management (Independent Variable)

Correlation

Probability ROA ROE NPM BSIZE NEDS CEO_DUALI...

ROA 1.000000

-----

ROE 0.843302 1.000000

0.0000 -----

NPM 0.753463 0.624078 1.000000

0.0000 0.0000 -----

BSIZE 0.109421 0.100315 0.312002 1.000000

0.0287 0.0450 0.0000 -----

NEDS 0.067201 0.023958 0.125650 0.260060 1.000000

0.1798 0.6328 0.0119 0.0000 -----

CEO_DUALITY 0.170880 0.149005 0.000806 -0.002019 -0.173523 1.000000

0.0006 0.0028 0.9872 0.9679 0.0005 -----

Figure 2: Correlation for Corporate Governance (Independent Variable)

8IMPACT OF WCM AND CG ON FIRM PERFORMANCE

The Pearson’s correlation coefficient between the independent variable BSIZE with the

dependent variables ROA, ROE and NPM are 0.109, 0.1003 and 0.312 respectively All were

found to be positive and significant at 5% level of significance. The Pearson’s correlation

coefficient between the independent variable NEDS with the dependent variables ROA, ROE

and NPM are 0.067, 0.0239 and 0.125 respectively. Only the correlation with NPM was found

to be positive and significant at 5% level of significance. The Pearson’s correlation coefficient

between the independent variable CEO duality with the dependent variables ROA, ROE and

NPM are 0.170, 0.149 and 0.0008 respectively. All except the correlation with NPM were found

to be significant at 5% level of significance and positive.

Correlation

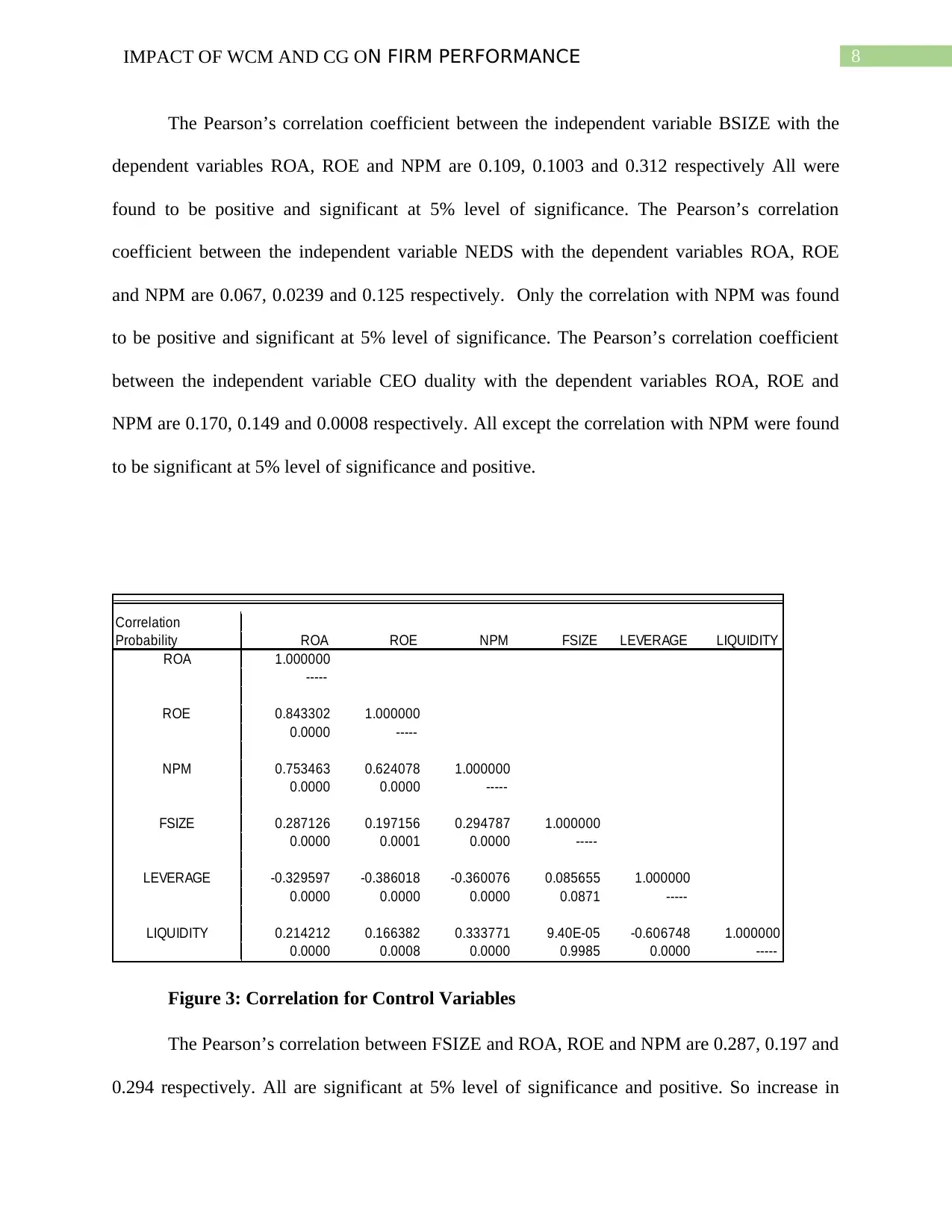

Probability ROA ROE NPM FSIZE LEVERAGE LIQUIDITY

ROA 1.000000

-----

ROE 0.843302 1.000000

0.0000 -----

NPM 0.753463 0.624078 1.000000

0.0000 0.0000 -----

FSIZE 0.287126 0.197156 0.294787 1.000000

0.0000 0.0001 0.0000 -----

LEVERAGE -0.329597 -0.386018 -0.360076 0.085655 1.000000

0.0000 0.0000 0.0000 0.0871 -----

LIQUIDITY 0.214212 0.166382 0.333771 9.40E-05 -0.606748 1.000000

0.0000 0.0008 0.0000 0.9985 0.0000 -----

Figure 3: Correlation for Control Variables

The Pearson’s correlation between FSIZE and ROA, ROE and NPM are 0.287, 0.197 and

0.294 respectively. All are significant at 5% level of significance and positive. So increase in

The Pearson’s correlation coefficient between the independent variable BSIZE with the

dependent variables ROA, ROE and NPM are 0.109, 0.1003 and 0.312 respectively All were

found to be positive and significant at 5% level of significance. The Pearson’s correlation

coefficient between the independent variable NEDS with the dependent variables ROA, ROE

and NPM are 0.067, 0.0239 and 0.125 respectively. Only the correlation with NPM was found

to be positive and significant at 5% level of significance. The Pearson’s correlation coefficient

between the independent variable CEO duality with the dependent variables ROA, ROE and

NPM are 0.170, 0.149 and 0.0008 respectively. All except the correlation with NPM were found

to be significant at 5% level of significance and positive.

Correlation

Probability ROA ROE NPM FSIZE LEVERAGE LIQUIDITY

ROA 1.000000

-----

ROE 0.843302 1.000000

0.0000 -----

NPM 0.753463 0.624078 1.000000

0.0000 0.0000 -----

FSIZE 0.287126 0.197156 0.294787 1.000000

0.0000 0.0001 0.0000 -----

LEVERAGE -0.329597 -0.386018 -0.360076 0.085655 1.000000

0.0000 0.0000 0.0000 0.0871 -----

LIQUIDITY 0.214212 0.166382 0.333771 9.40E-05 -0.606748 1.000000

0.0000 0.0008 0.0000 0.9985 0.0000 -----

Figure 3: Correlation for Control Variables

The Pearson’s correlation between FSIZE and ROA, ROE and NPM are 0.287, 0.197 and

0.294 respectively. All are significant at 5% level of significance and positive. So increase in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9IMPACT OF WCM AND CG ON FIRM PERFORMANCE

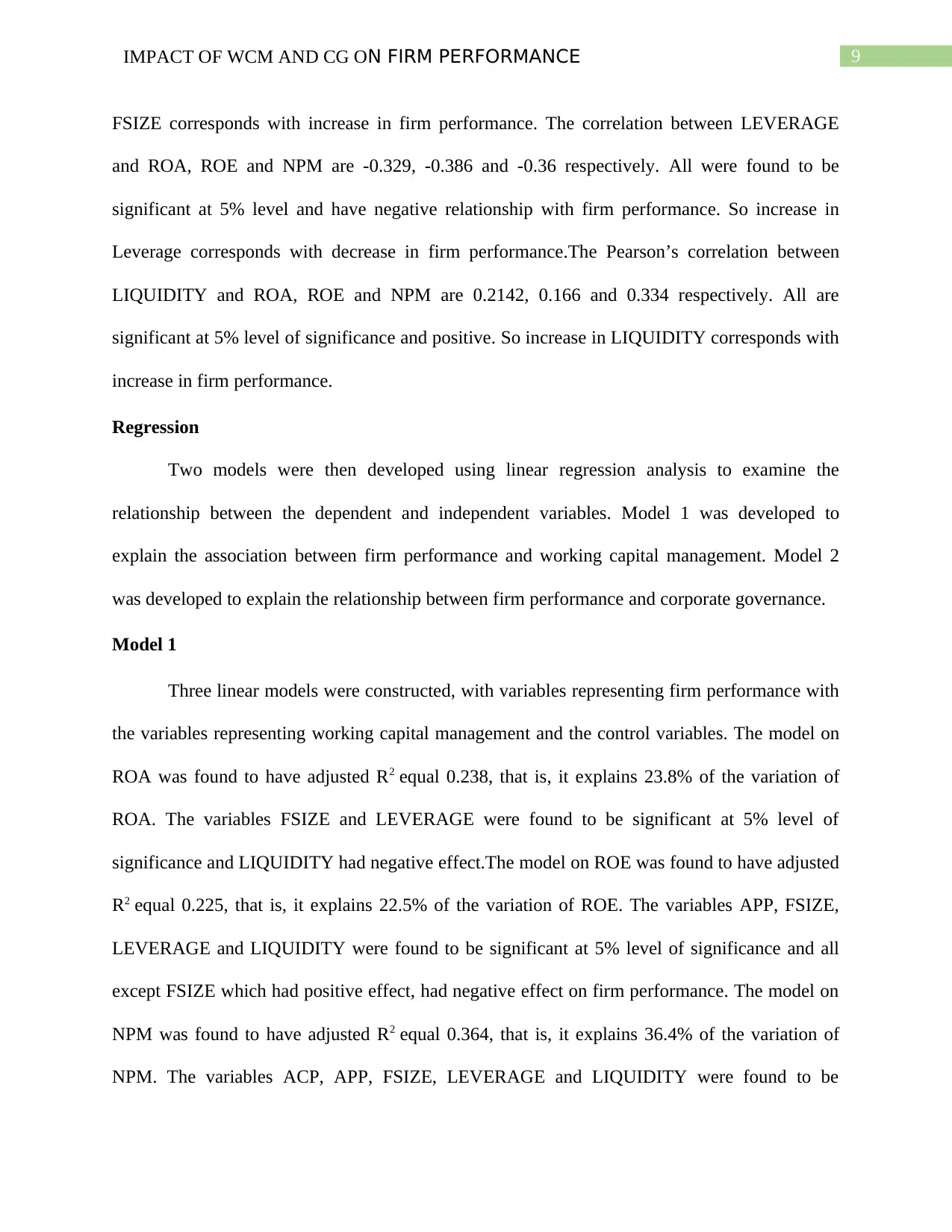

FSIZE corresponds with increase in firm performance. The correlation between LEVERAGE

and ROA, ROE and NPM are -0.329, -0.386 and -0.36 respectively. All were found to be

significant at 5% level and have negative relationship with firm performance. So increase in

Leverage corresponds with decrease in firm performance.The Pearson’s correlation between

LIQUIDITY and ROA, ROE and NPM are 0.2142, 0.166 and 0.334 respectively. All are

significant at 5% level of significance and positive. So increase in LIQUIDITY corresponds with

increase in firm performance.

Regression

Two models were then developed using linear regression analysis to examine the

relationship between the dependent and independent variables. Model 1 was developed to

explain the association between firm performance and working capital management. Model 2

was developed to explain the relationship between firm performance and corporate governance.

Model 1

Three linear models were constructed, with variables representing firm performance with

the variables representing working capital management and the control variables. The model on

ROA was found to have adjusted R2 equal 0.238, that is, it explains 23.8% of the variation of

ROA. The variables FSIZE and LEVERAGE were found to be significant at 5% level of

significance and LIQUIDITY had negative effect.The model on ROE was found to have adjusted

R2 equal 0.225, that is, it explains 22.5% of the variation of ROE. The variables APP, FSIZE,

LEVERAGE and LIQUIDITY were found to be significant at 5% level of significance and all

except FSIZE which had positive effect, had negative effect on firm performance. The model on

NPM was found to have adjusted R2 equal 0.364, that is, it explains 36.4% of the variation of

NPM. The variables ACP, APP, FSIZE, LEVERAGE and LIQUIDITY were found to be

FSIZE corresponds with increase in firm performance. The correlation between LEVERAGE

and ROA, ROE and NPM are -0.329, -0.386 and -0.36 respectively. All were found to be

significant at 5% level and have negative relationship with firm performance. So increase in

Leverage corresponds with decrease in firm performance.The Pearson’s correlation between

LIQUIDITY and ROA, ROE and NPM are 0.2142, 0.166 and 0.334 respectively. All are

significant at 5% level of significance and positive. So increase in LIQUIDITY corresponds with

increase in firm performance.

Regression

Two models were then developed using linear regression analysis to examine the

relationship between the dependent and independent variables. Model 1 was developed to

explain the association between firm performance and working capital management. Model 2

was developed to explain the relationship between firm performance and corporate governance.

Model 1

Three linear models were constructed, with variables representing firm performance with

the variables representing working capital management and the control variables. The model on

ROA was found to have adjusted R2 equal 0.238, that is, it explains 23.8% of the variation of

ROA. The variables FSIZE and LEVERAGE were found to be significant at 5% level of

significance and LIQUIDITY had negative effect.The model on ROE was found to have adjusted

R2 equal 0.225, that is, it explains 22.5% of the variation of ROE. The variables APP, FSIZE,

LEVERAGE and LIQUIDITY were found to be significant at 5% level of significance and all

except FSIZE which had positive effect, had negative effect on firm performance. The model on

NPM was found to have adjusted R2 equal 0.364, that is, it explains 36.4% of the variation of

NPM. The variables ACP, APP, FSIZE, LEVERAGE and LIQUIDITY were found to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10IMPACT OF WCM AND CG ON FIRM PERFORMANCE

significant at 5% level of significance with ACP, APP and LEVERAGE having negative impact

on performance.

Variable

ROA ROE NPM

Coefficien

t t-statistic Coefficien

t t-statistic Coefficien

t t-statistic

ACP -8.60E-05 -1.430584 -0.000149 -1.161535 -0.00043

-

3.709789**

*

AIP -6.52E-05 -1.792878* -4.12E-05 -0.528798 ####### -1.336106

APP -0.000114 -1.798655* -0.000261 -

1.925052** -0.00043

-

3.515686**

*

CCC -6.52E-05 -1.792878* -4.12E-05 -0.528798 ####### -1.336106

FSIZE 0.050856 6.262053**

* 0.083825 4.823157**

* 0.10245 6.585742**

*

LEVERAG

E -0.170914

-

5.800952**

*

-0.493454

-

7.826238**

*

-0.24646

-

4.367088**

*

LIQUIDIT

Y -0.000235 -0.117425 -0.010194 -

2.381511** 0.01119 2.920968**

*

* p < 0.1 ** p <0.05 *** p < 0.01

Table 2: Regression Model 1 Specifications

ROA ROE NPM

Coefficient Prob. Coefficien

t Prob. Coefficient Prob.

R2 0.249599 - 0.237381 - 0.36425 -

Adjusted R2 0.238143 - 0.225738 - 0.35454 -

F-statistics 21.78669 0.0000 20.38824 0.0000 37.5276 0.0000

Table 3: Regression Model 1 Fitness Measures

Model 2

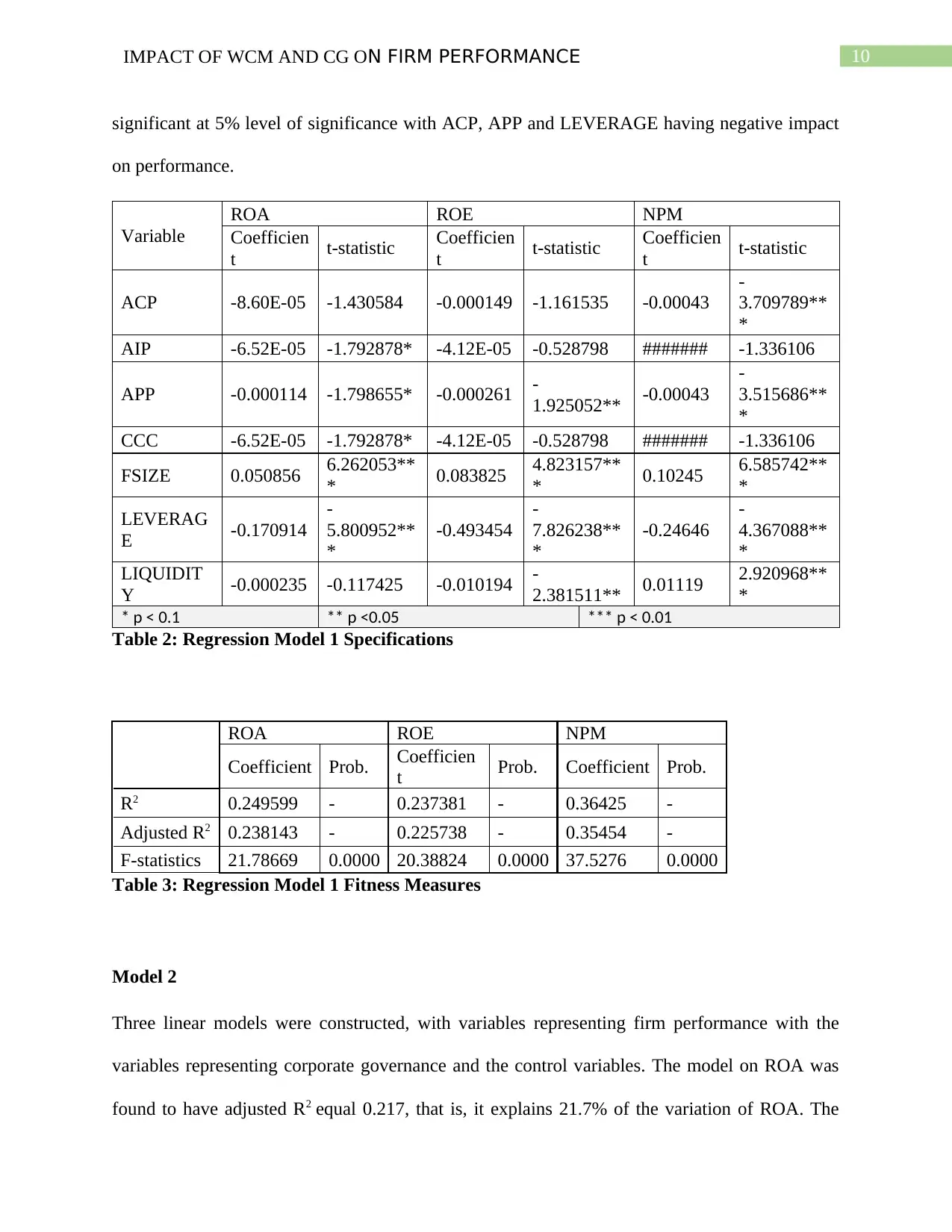

Three linear models were constructed, with variables representing firm performance with the

variables representing corporate governance and the control variables. The model on ROA was

found to have adjusted R2 equal 0.217, that is, it explains 21.7% of the variation of ROA. The

significant at 5% level of significance with ACP, APP and LEVERAGE having negative impact

on performance.

Variable

ROA ROE NPM

Coefficien

t t-statistic Coefficien

t t-statistic Coefficien

t t-statistic

ACP -8.60E-05 -1.430584 -0.000149 -1.161535 -0.00043

-

3.709789**

*

AIP -6.52E-05 -1.792878* -4.12E-05 -0.528798 ####### -1.336106

APP -0.000114 -1.798655* -0.000261 -

1.925052** -0.00043

-

3.515686**

*

CCC -6.52E-05 -1.792878* -4.12E-05 -0.528798 ####### -1.336106

FSIZE 0.050856 6.262053**

* 0.083825 4.823157**

* 0.10245 6.585742**

*

LEVERAG

E -0.170914

-

5.800952**

*

-0.493454

-

7.826238**

*

-0.24646

-

4.367088**

*

LIQUIDIT

Y -0.000235 -0.117425 -0.010194 -

2.381511** 0.01119 2.920968**

*

* p < 0.1 ** p <0.05 *** p < 0.01

Table 2: Regression Model 1 Specifications

ROA ROE NPM

Coefficient Prob. Coefficien

t Prob. Coefficient Prob.

R2 0.249599 - 0.237381 - 0.36425 -

Adjusted R2 0.238143 - 0.225738 - 0.35454 -

F-statistics 21.78669 0.0000 20.38824 0.0000 37.5276 0.0000

Table 3: Regression Model 1 Fitness Measures

Model 2

Three linear models were constructed, with variables representing firm performance with the

variables representing corporate governance and the control variables. The model on ROA was

found to have adjusted R2 equal 0.217, that is, it explains 21.7% of the variation of ROA. The

11IMPACT OF WCM AND CG ON FIRM PERFORMANCE

variables CEO-duality, FSIZE and LEVERAGE were found to be significant at 5% level of

significance. LEVERAGE had a negative effect on ROA where as CEO duality and FSIZE wer

positively related wiith ROA. The model on ROE was found to have adjusted R2 equal 0.2095,

that is, it explains 20.95% of the variation of ROE. The variables CEO-duality, FSIZE,

LEVERAGE and LIQUIDITY were found to be significant at 5% level of significance with the

latter two having negative effect on ROE. The model on NPM was found to have adjusted R2

equal 0.268, that is, it explains 26.8% of the variation of NPM. The variables BSIZE, FSIZE,

LEVERAGE and LIQUIDITY were found to be significant at 5% level of significance and

LEVERAGE had a negative effect on firm performance as measured by the NPM.

Variable

ROA ROE NPM

Coefficien

t t-statistic Coefficien

t t-statistic Coefficien

t t-statistic

BSIZE -0.0026 -1.214889 -0.0026 -0.573722 0.0136 3.197047**

*

NEDs 0.0632 1.605706* 0.0504 0.599288 0.0787 0.992474

CEO-

duality 0.0331 2.900794**

* 0.0496 2.033735** -0.0188 -0.817334

FSIZE 0.0579 6.919709**

* 0.0911 5.105909**

* 0.1021 6.063324**

*

LEVERAG

E -0.1776

-

6.062792**

*

-0.5158

-

8.251913**

*

-0.3043

-

5.161385**

*

LIQUIDIT

Y 0.0003 0.157899 -0.009 -

2.078222** 0.0097 2.374963**

* p < 0.1 ** p <0.05 *** p < 0.01

Table 4: Regression Model 2 Specifications

ROA ROE NPM

Coefficien

t Prob. Coefficient Prob. Coefficient Prob.

R2 0.2294 - 0.2214 - 0.279 -

Adjusted R2 0.2177 - 0.2095 - 0.268 -

F-statistics 19.504 0.0000 18.621 0.000 25.344 0.000

variables CEO-duality, FSIZE and LEVERAGE were found to be significant at 5% level of

significance. LEVERAGE had a negative effect on ROA where as CEO duality and FSIZE wer

positively related wiith ROA. The model on ROE was found to have adjusted R2 equal 0.2095,

that is, it explains 20.95% of the variation of ROE. The variables CEO-duality, FSIZE,

LEVERAGE and LIQUIDITY were found to be significant at 5% level of significance with the

latter two having negative effect on ROE. The model on NPM was found to have adjusted R2

equal 0.268, that is, it explains 26.8% of the variation of NPM. The variables BSIZE, FSIZE,

LEVERAGE and LIQUIDITY were found to be significant at 5% level of significance and

LEVERAGE had a negative effect on firm performance as measured by the NPM.

Variable

ROA ROE NPM

Coefficien

t t-statistic Coefficien

t t-statistic Coefficien

t t-statistic

BSIZE -0.0026 -1.214889 -0.0026 -0.573722 0.0136 3.197047**

*

NEDs 0.0632 1.605706* 0.0504 0.599288 0.0787 0.992474

CEO-

duality 0.0331 2.900794**

* 0.0496 2.033735** -0.0188 -0.817334

FSIZE 0.0579 6.919709**

* 0.0911 5.105909**

* 0.1021 6.063324**

*

LEVERAG

E -0.1776

-

6.062792**

*

-0.5158

-

8.251913**

*

-0.3043

-

5.161385**

*

LIQUIDIT

Y 0.0003 0.157899 -0.009 -

2.078222** 0.0097 2.374963**

* p < 0.1 ** p <0.05 *** p < 0.01

Table 4: Regression Model 2 Specifications

ROA ROE NPM

Coefficien

t Prob. Coefficient Prob. Coefficient Prob.

R2 0.2294 - 0.2214 - 0.279 -

Adjusted R2 0.2177 - 0.2095 - 0.268 -

F-statistics 19.504 0.0000 18.621 0.000 25.344 0.000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.