ACCT20076 - Activity Based Costing Analysis of Animal Shelter

VerifiedAdded on 2023/06/05

|10

|1664

|458

Report

AI Summary

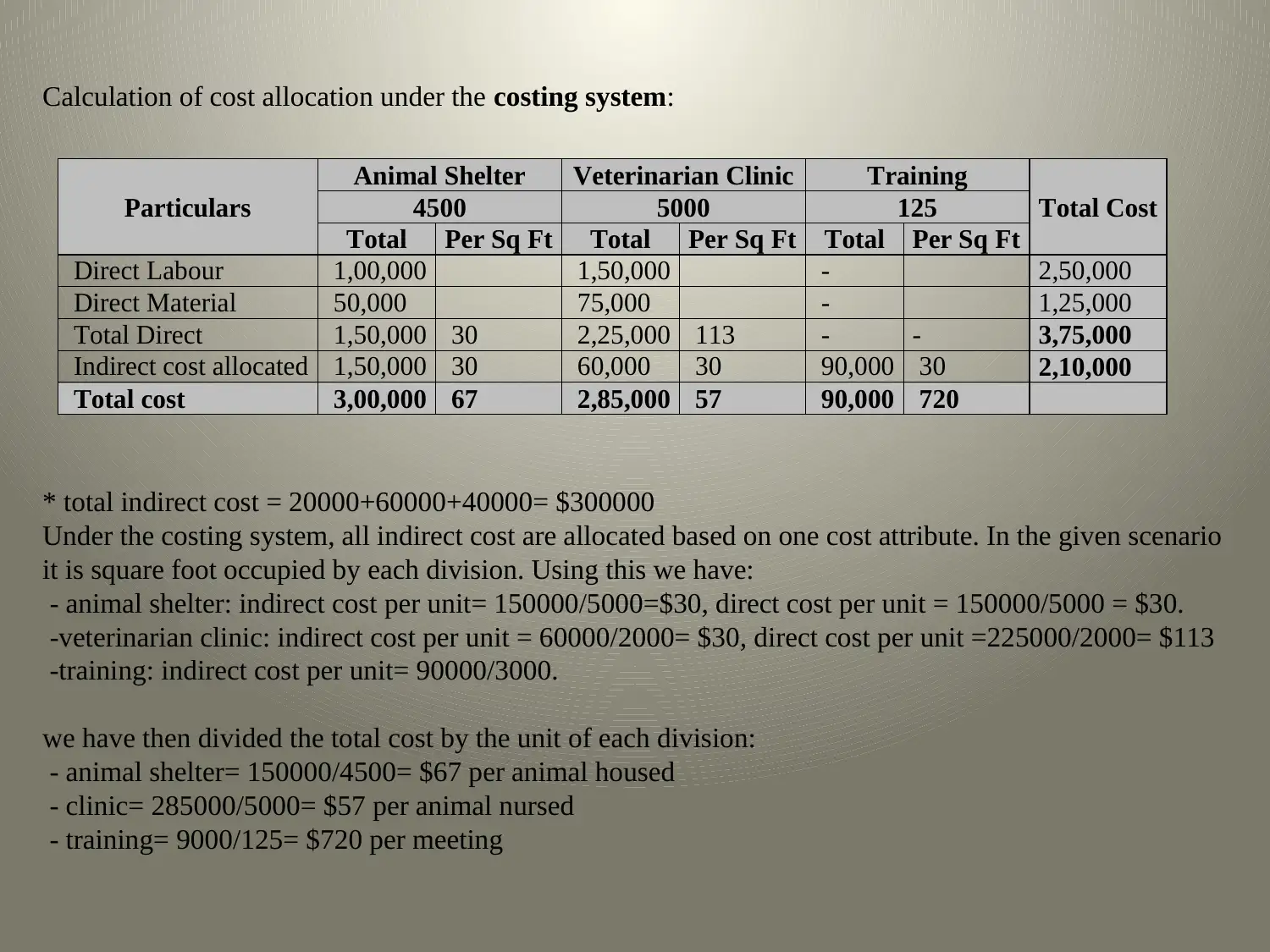

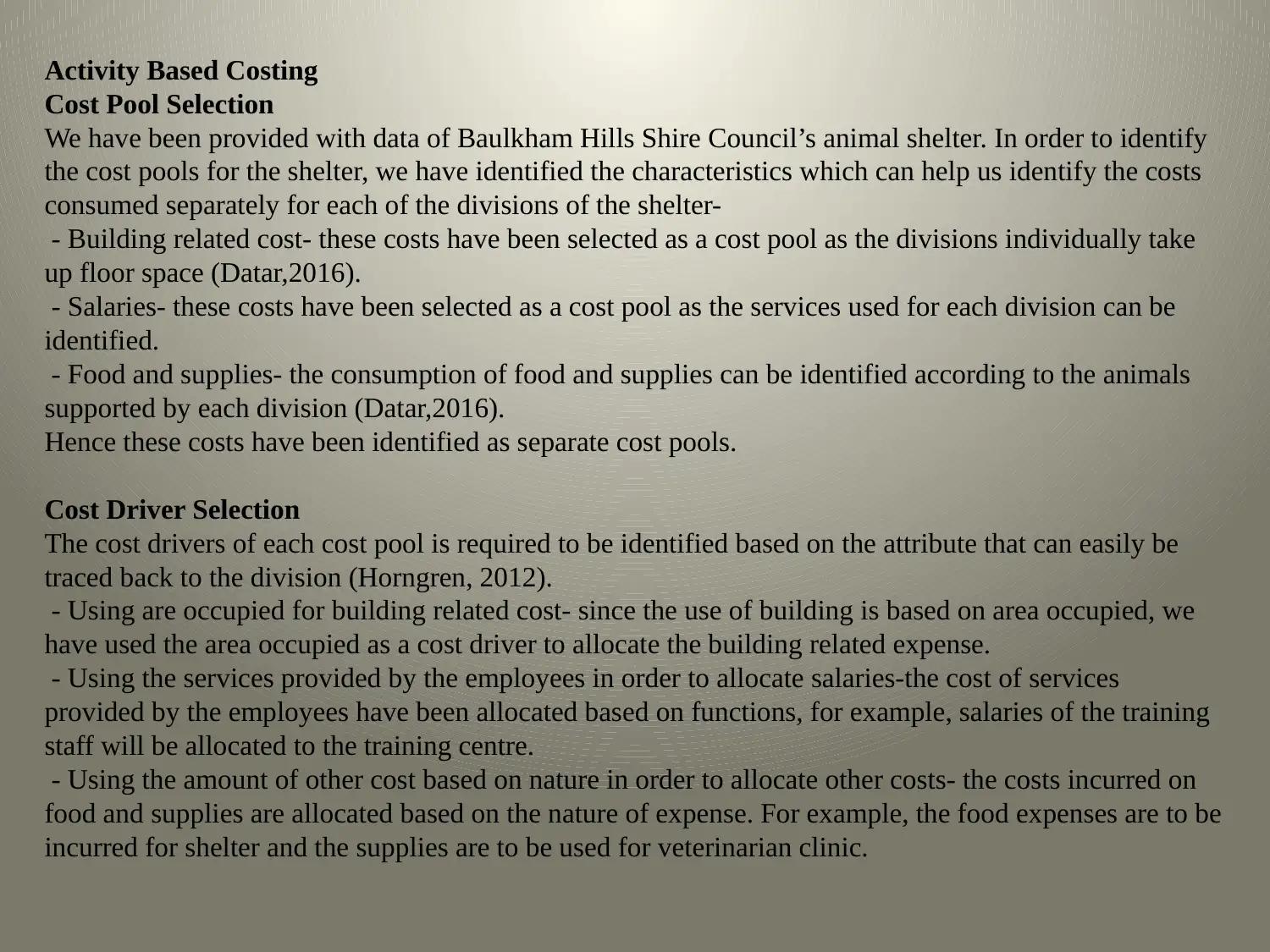

This report presents an analysis of activity-based costing (ABC) applied to an animal shelter, specifically Baulkham Hills Shire Council. It details the application of ABC to the shelter's cost data across three divisions: Animal Shelter, Director and Training, and Veterinarian Clinic. The report identifies cost pools such as building-related costs, salaries, and food and supplies, and assigns cost drivers like area occupied, employee services, and nature of expense. Calculations are performed to allocate costs based on these drivers, revealing the cost per animal housed, cost per family attending training, and cost per animal visit. The report concludes by highlighting the limitations of ABC, such as data collection complexity and the need for trained professionals, while emphasizing its benefits in providing detailed cost insights for better resource allocation and management decision-making. The findings include the cost of sheltering one animal for an entire year is $60, cost for each family attending the classes is $112 and cost incurred on each animal visit is $53 per visit for a year.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.