Accounting Standards and Practices: Annual Report Analysis Project

VerifiedAdded on 2020/07/22

|10

|2247

|31

Report

AI Summary

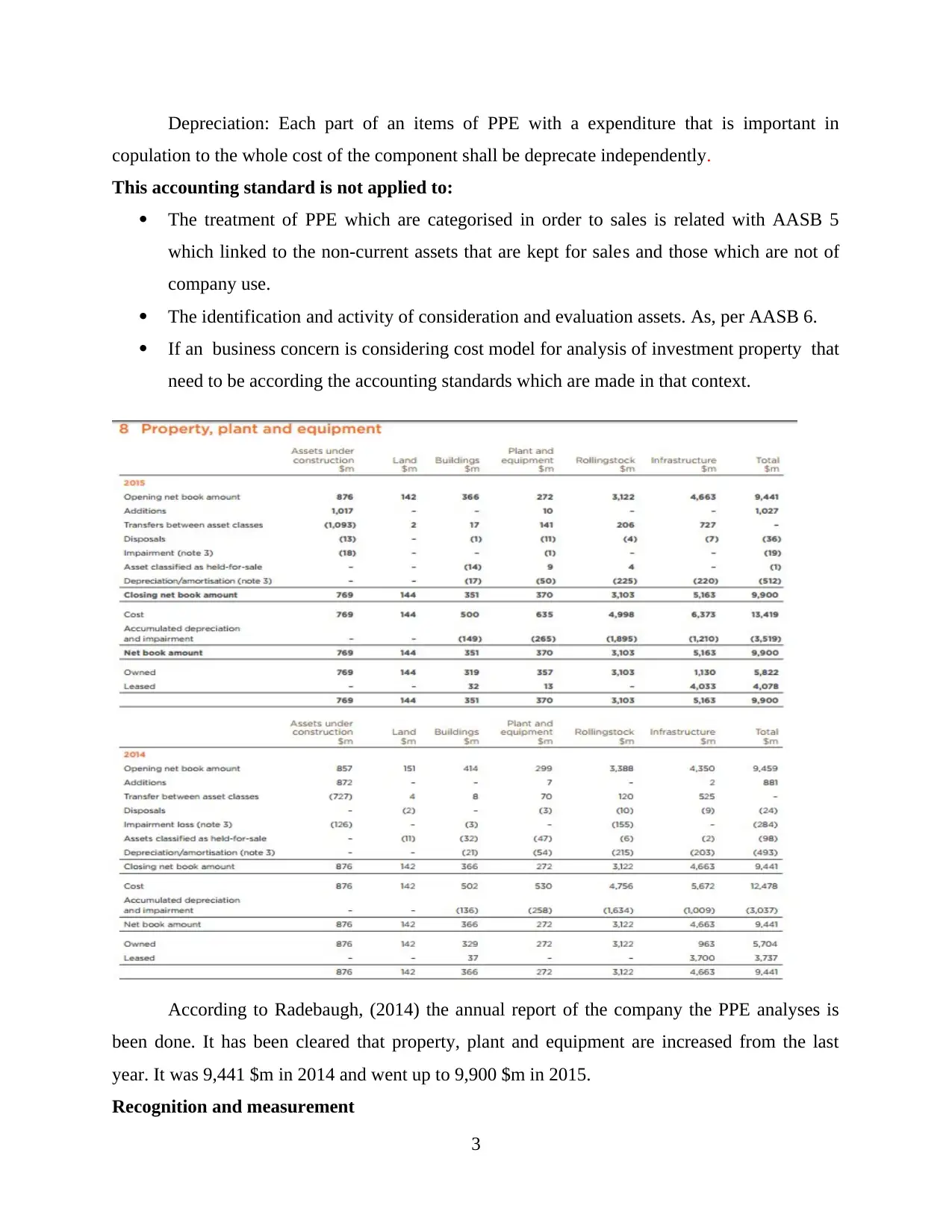

This report delves into the realm of accounting standards and practices, with a particular emphasis on financial reporting and the treatment of Property, Plant, and Equipment (PPE). The report begins by outlining the objectives and characteristics of financial reporting, referencing the conceptual frameworks established by the IASB. It then proceeds to a critical analysis of an annual report, specifically that of Aurizon Holdings Limited, evaluating how the company meets the disclosure requirements of AASB 116 concerning PPE. The analysis includes a review of recognition and measurement principles, depreciation methods, and revaluation techniques. Furthermore, the report critically assesses the extent to which the company's PPE practices satisfy both fundamental and enhancing qualitative characteristics of financial information, such as relevance, faithful representation, comparability, and verifiability. The discussion also covers how PPE disclosures align with the overarching purpose of financial reporting, including the presentation of assets and liabilities, and the impact of these disclosures on stakeholders' decision-making processes. The report concludes with a summary of the key findings and recommendations regarding the application of accounting standards in the context of PPE.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.