Corporate Finance Report: Antofagasta Plc. - Cost of Equity Analysis

VerifiedAdded on 2023/04/07

|13

|2896

|235

Report

AI Summary

This report provides a comprehensive financial analysis of Antofagasta Plc., a Chilean business listed on the London Stock Exchange. It begins by calculating the company's cost of equity using the Capital Asset Pricing Model (CAPM), justifying the data used, including risk-free rate, market return, and beta. The report then calculates the asset beta, explaining the significance of both equity and asset betas in assessing risk. Furthermore, it analyzes Antofagasta's dividend policy over the past five years, using ratios to assess its stability and relation to earnings. Finally, the report critically evaluates the suitability of the CAPM-derived cost of equity for investment appraisal, comparing it to the Dividend Growth Model and discussing their respective strengths and weaknesses for determining the cost of equity.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Author’s Note:

Corporate Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE FINANCE

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Cost of Equity..............................................................................................................................2

Equity Beta and Asset Beta.........................................................................................................4

Dividend Policy of Antofagasta Plc............................................................................................5

Evaluation of Cost of Equity.......................................................................................................6

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Cost of Equity..............................................................................................................................2

Equity Beta and Asset Beta.........................................................................................................4

Dividend Policy of Antofagasta Plc............................................................................................5

Evaluation of Cost of Equity.......................................................................................................6

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................11

2CORPORATE FINANCE

Introduction

Antofagasta Plc. is a Chilean Business that operates in the various sectors in an economy.

The company stands as one of the key conglomerate of Chile whereby the company is having a

major equity participation in Antofagasta Minerals. The company is listed in the London Stock

Exchange and is an important constituent of the FTSE 100 Index. The financial analysis of the

company was conducted thereby covering the various financials of the company. The cost of

equity for the company with the help of the CAPM Model, the equity beta and asset beta for the

company was evaluated. The dividend policy followed by the company in the last five period

was also taken into consideration. Asset Beta and Equity Beta are the two important risk factors

that should be taken into account for computing the various risks associated with a company and

the same was addressed for evaluating the equity and asset risk in contrast to the market. It is

important that there are various techniques and rules applied for evaluating the required rate of

return on equity and the same has been done by including the Dividend Growth Model for

determining the cost of equity1.

Discussion

Cost of Equity

The cost of equity shows the theoretically rate of return that is required by the equity

investors of a company for compensating the undertaken risk borne by investing their equity

capital2. Risk free rate of return, return generated on market index and the beta of the stocks are

some of the important perspective that will be taken into consideration for the purpose of

1 Pedersen, Niels, Sébastien Page, and Fei He. "Asset allocation: Risk models for alternative investments." Financial

Analysts Journal 70.3 (2014): 34-45.

2 Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor sentiment, beta, and the cost of

equity capital." Management Science 62.2 (2015): 347-367.

Introduction

Antofagasta Plc. is a Chilean Business that operates in the various sectors in an economy.

The company stands as one of the key conglomerate of Chile whereby the company is having a

major equity participation in Antofagasta Minerals. The company is listed in the London Stock

Exchange and is an important constituent of the FTSE 100 Index. The financial analysis of the

company was conducted thereby covering the various financials of the company. The cost of

equity for the company with the help of the CAPM Model, the equity beta and asset beta for the

company was evaluated. The dividend policy followed by the company in the last five period

was also taken into consideration. Asset Beta and Equity Beta are the two important risk factors

that should be taken into account for computing the various risks associated with a company and

the same was addressed for evaluating the equity and asset risk in contrast to the market. It is

important that there are various techniques and rules applied for evaluating the required rate of

return on equity and the same has been done by including the Dividend Growth Model for

determining the cost of equity1.

Discussion

Cost of Equity

The cost of equity shows the theoretically rate of return that is required by the equity

investors of a company for compensating the undertaken risk borne by investing their equity

capital2. Risk free rate of return, return generated on market index and the beta of the stocks are

some of the important perspective that will be taken into consideration for the purpose of

1 Pedersen, Niels, Sébastien Page, and Fei He. "Asset allocation: Risk models for alternative investments." Financial

Analysts Journal 70.3 (2014): 34-45.

2 Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor sentiment, beta, and the cost of

equity capital." Management Science 62.2 (2015): 347-367.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE FINANCE

analysis. The risk free rate of return taken into consideration was the average risk free rate

prevailing in the UK, which was around 2%. The return was around 2%, which was applied in

the CAPM Model3. The return generated on the market was considered as the return generated

by the FTSE 100 Index where the return generated by the stock over a period of five-years were

taken into consideration. The return generated by the FTSE 100 index in this five-years of time

was around 6.67%4.

The beta of the stock was taken from the beta book taken from the yahoo finance for the

company. The beta for the stock was calculated to be around 0.98 times which implies that the

return of the stock is closely implied with the return from the index. The derived calculation of

beta also shows that the beta of 0.98 times shows that the stock is comparatively more risky and

volatile5. After getting the desired result for computing the required rate of return on equity the

formula that can be applied for the computation of the same could be as follows:

Cost of Equity = Risk-Free Rate of Return + Beta * (Market Rate of Return - Risk-Free Rate of

Return).

Cost of Equity = 2.00%+ (0.98*(6.67%-2.00%))

Cost of Equity = 6.58%

The cost of equity derived from the model was comparatively close with the market index

and the possible reason could be the 0.98 beta for the stock. The reason behind selecting the data

for average risk free rate was that the same should attribute or reflect the position and scenario of

3 "United Kingdom Government Bond 10Y | 2019 | Data | Chart | Calendar." Tradingeconomics.com. N.p., 2019.

Web. 25 Mar. 2019.

4 "FTSE 100 Index Data." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

5 "Antofagasta Plc Share Price." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

analysis. The risk free rate of return taken into consideration was the average risk free rate

prevailing in the UK, which was around 2%. The return was around 2%, which was applied in

the CAPM Model3. The return generated on the market was considered as the return generated

by the FTSE 100 Index where the return generated by the stock over a period of five-years were

taken into consideration. The return generated by the FTSE 100 index in this five-years of time

was around 6.67%4.

The beta of the stock was taken from the beta book taken from the yahoo finance for the

company. The beta for the stock was calculated to be around 0.98 times which implies that the

return of the stock is closely implied with the return from the index. The derived calculation of

beta also shows that the beta of 0.98 times shows that the stock is comparatively more risky and

volatile5. After getting the desired result for computing the required rate of return on equity the

formula that can be applied for the computation of the same could be as follows:

Cost of Equity = Risk-Free Rate of Return + Beta * (Market Rate of Return - Risk-Free Rate of

Return).

Cost of Equity = 2.00%+ (0.98*(6.67%-2.00%))

Cost of Equity = 6.58%

The cost of equity derived from the model was comparatively close with the market index

and the possible reason could be the 0.98 beta for the stock. The reason behind selecting the data

for average risk free rate was that the same should attribute or reflect the position and scenario of

3 "United Kingdom Government Bond 10Y | 2019 | Data | Chart | Calendar." Tradingeconomics.com. N.p., 2019.

Web. 25 Mar. 2019.

4 "FTSE 100 Index Data." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

5 "Antofagasta Plc Share Price." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE FINANCE

the economy6. The return generated by the market index was taken for a sum of five years of

time frame where the relevant movement in the index was captured with help of the annual

return generated by the stock. The cost of equity derived above is an important measure for

evaluating the effectiveness and minimum return that is required by an investor for the capital

invested.

Equity Beta and Asset Beta

The asset beta or the unlevered beta of a company shows the value of beta for a company

by ignoring the impact of debt or by ignoring the impact of financial leverage in this case. The

asset beta is an important measure that is helpful for determining the risk of the company in an

unlevered form7. The unlevered beta of a company or the asset beta could be calculated with the

equity beta by the following formula:

Asset Beta: Equity Beta/[(1+(1-Tax Rate)*(Debt/Equity)]

Asset Beta: 0.98/[1+(1-0.338)*(1847.9/9438.1)

Asset Beta: 0.868 times.

The equity beta for the company was calculated to be around 0.98 times on the other

hand side the asset beta for the stock was calculated to be around 0.868 times the slight

difference could be well attributed to the lower amount of debt in the financials of the company8.

The financial risk of the business can be well understand with the help of the lower debt that is in

the balance sheet of the company letting the company maintain stable risk. The value of debt in

the financial statement for the company was around $1848 million and the value of equity for the

6 Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor sentiment, beta, and the cost of

equity capital." Management Science 62.2 (2015): 347-367.

7 "Unlevered Beta (Asset Beta) - Formula, Calculation, And Examples." Corporate Finance Institute. N.p., 2019.

Web. 25 Mar. 2019.

8 Buchner, Axel. "The alpha and beta of private equity investments." Available at SSRN 2549705 (2014).

the economy6. The return generated by the market index was taken for a sum of five years of

time frame where the relevant movement in the index was captured with help of the annual

return generated by the stock. The cost of equity derived above is an important measure for

evaluating the effectiveness and minimum return that is required by an investor for the capital

invested.

Equity Beta and Asset Beta

The asset beta or the unlevered beta of a company shows the value of beta for a company

by ignoring the impact of debt or by ignoring the impact of financial leverage in this case. The

asset beta is an important measure that is helpful for determining the risk of the company in an

unlevered form7. The unlevered beta of a company or the asset beta could be calculated with the

equity beta by the following formula:

Asset Beta: Equity Beta/[(1+(1-Tax Rate)*(Debt/Equity)]

Asset Beta: 0.98/[1+(1-0.338)*(1847.9/9438.1)

Asset Beta: 0.868 times.

The equity beta for the company was calculated to be around 0.98 times on the other

hand side the asset beta for the stock was calculated to be around 0.868 times the slight

difference could be well attributed to the lower amount of debt in the financials of the company8.

The financial risk of the business can be well understand with the help of the lower debt that is in

the balance sheet of the company letting the company maintain stable risk. The value of debt in

the financial statement for the company was around $1848 million and the value of equity for the

6 Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor sentiment, beta, and the cost of

equity capital." Management Science 62.2 (2015): 347-367.

7 "Unlevered Beta (Asset Beta) - Formula, Calculation, And Examples." Corporate Finance Institute. N.p., 2019.

Web. 25 Mar. 2019.

8 Buchner, Axel. "The alpha and beta of private equity investments." Available at SSRN 2549705 (2014).

5CORPORATE FINANCE

company was around $9438 for the company. The business risk of the company can be well

understood with the help of the associated business factors like the competition evolving in the

industry, cost factor associated and the revenue for the company which has fallen from the last

year. It is essential that the company must keep the financial risk of the company at a very low

level so that on a overall basis the higher debt does not affect the financial performance and

position of the company. The debt to equity ratio for the company was around 0.19 or 19% that

shows that the company might be using equity and retained earnings as the prime source of

investment. The lower amount of financial leverage was the key reason reflecting the minute

impact in the asset beta of the company. On the one hand side the equity beta of a stock shows

the volatility generated by the stock by taking the market returns and the return generated by the

stock. In the above case as analysed if the beta of the stock is around 0.98 times it reflects that if

the market moves by around 1% then the stock would be moving around by 0.98 times reflecting

high correlation between these two. On the other hand the asset beta of the company shows the

potential impact of the debt on the financial position of the company and how will the change in

the capital structure of the company or the debt financing impact the overall asset beta of the

company.

Dividend Policy of Antofagasta Plc.

The dividend policy of company shows the set of guideline of a company reflecting the

decision of the company in paying of the amount of profits of the company in the form of

dividend to the equity shareholders of the company. The same is important for the perspective of

the analysis reflecting the internal source of funding that is used by the company. The dividend

policy of a company could be well depicted with the help of various policies like the stable

dividend policy, constant dividend policy and the residual dividend policy. The dividends paid

company was around $9438 for the company. The business risk of the company can be well

understood with the help of the associated business factors like the competition evolving in the

industry, cost factor associated and the revenue for the company which has fallen from the last

year. It is essential that the company must keep the financial risk of the company at a very low

level so that on a overall basis the higher debt does not affect the financial performance and

position of the company. The debt to equity ratio for the company was around 0.19 or 19% that

shows that the company might be using equity and retained earnings as the prime source of

investment. The lower amount of financial leverage was the key reason reflecting the minute

impact in the asset beta of the company. On the one hand side the equity beta of a stock shows

the volatility generated by the stock by taking the market returns and the return generated by the

stock. In the above case as analysed if the beta of the stock is around 0.98 times it reflects that if

the market moves by around 1% then the stock would be moving around by 0.98 times reflecting

high correlation between these two. On the other hand the asset beta of the company shows the

potential impact of the debt on the financial position of the company and how will the change in

the capital structure of the company or the debt financing impact the overall asset beta of the

company.

Dividend Policy of Antofagasta Plc.

The dividend policy of company shows the set of guideline of a company reflecting the

decision of the company in paying of the amount of profits of the company in the form of

dividend to the equity shareholders of the company. The same is important for the perspective of

the analysis reflecting the internal source of funding that is used by the company. The dividend

policy of a company could be well depicted with the help of various policies like the stable

dividend policy, constant dividend policy and the residual dividend policy. The dividends paid

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE FINANCE

by the company can be well related with the above policies in order to find out the strategy

followed by the company. While, paying out the dividend growth prospects of the company and

the approach of the management towards, future growth can be well explained with the help of

the above policies9.

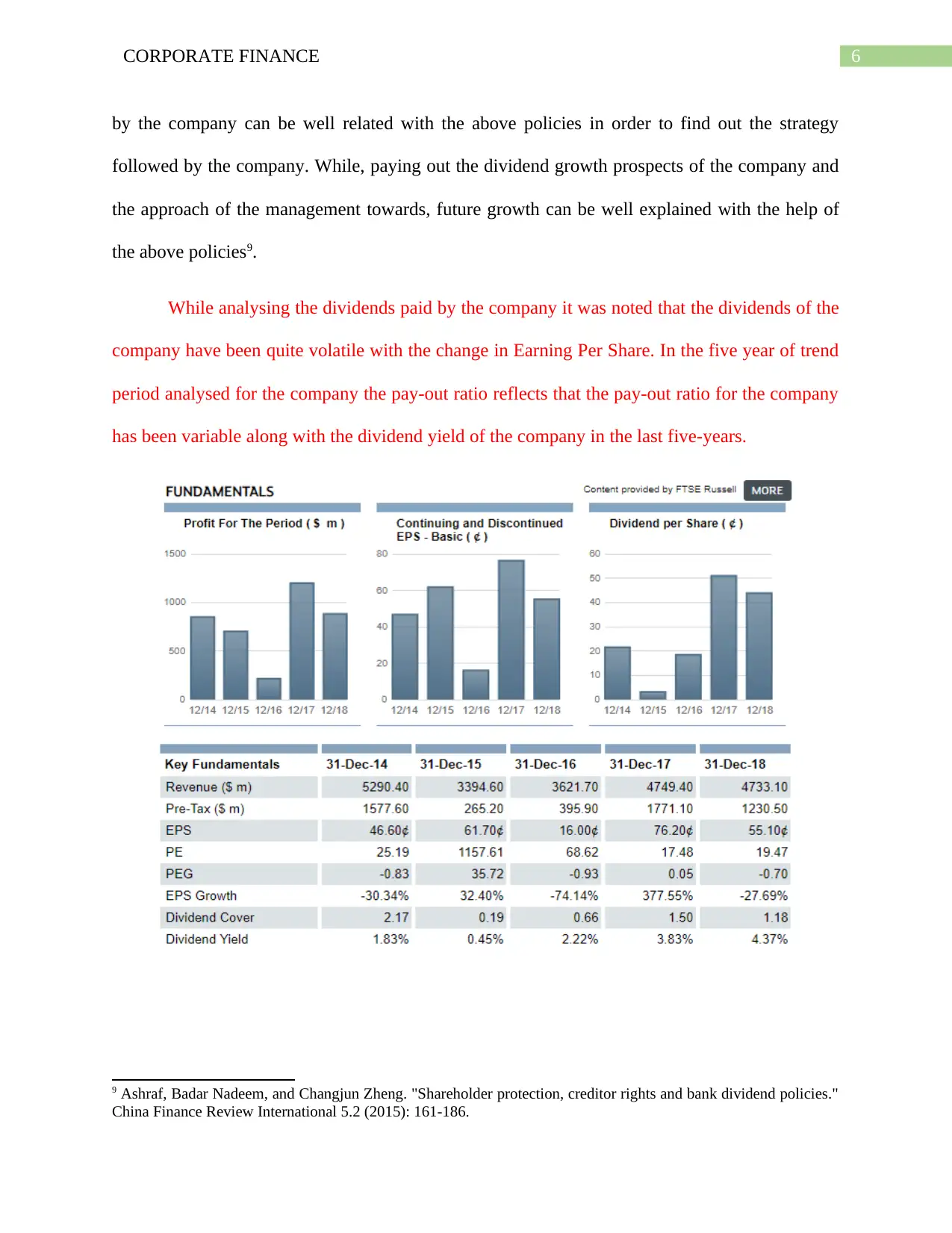

While analysing the dividends paid by the company it was noted that the dividends of the

company have been quite volatile with the change in Earning Per Share. In the five year of trend

period analysed for the company the pay-out ratio reflects that the pay-out ratio for the company

has been variable along with the dividend yield of the company in the last five-years.

9 Ashraf, Badar Nadeem, and Changjun Zheng. "Shareholder protection, creditor rights and bank dividend policies."

China Finance Review International 5.2 (2015): 161-186.

by the company can be well related with the above policies in order to find out the strategy

followed by the company. While, paying out the dividend growth prospects of the company and

the approach of the management towards, future growth can be well explained with the help of

the above policies9.

While analysing the dividends paid by the company it was noted that the dividends of the

company have been quite volatile with the change in Earning Per Share. In the five year of trend

period analysed for the company the pay-out ratio reflects that the pay-out ratio for the company

has been variable along with the dividend yield of the company in the last five-years.

9 Ashraf, Badar Nadeem, and Changjun Zheng. "Shareholder protection, creditor rights and bank dividend policies."

China Finance Review International 5.2 (2015): 161-186.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE FINANCE

The dividend policy of the company has been volatile and the dividend p\yield generated by the

company on the stock has varied significantly in the last five-years. As observed the dividends

for a company may increase even if there is a decline observed in the earnings of the company.

The dividends of the company may not increase at a constant speed and the same might

also would not increase as the growth of earnings also. The above two points are the key and

crucial distinctive feature matches with the stable dividend policy. While paying out the

dividends of a company it is important to consider various business factors and macro-economic

factors reflecting the growth potential and the ability of the company in paying of a stable

dividend policy. If the level of operations and the belief by the management of the company is

high growth perspective than a higher dividend pay-out ratio could be well followed10.

The pay-out ratio maintained by the company in the five-year o trend analysis has always

been greater than 30% reflecting the ability of the company in providing a stable dividend policy.

However, with the changes in the growth perspective and the belief of the management regarding

the company operational plan the dividend has changed fir the company accordingly. The pay-

out ratio of the company was around 31% in the year 2013 reflecting the lowest pay-out ratio for

the company in the trend period analysed for the company. The highest pay-out ratio for the

company was in the year of 2017 when the same was around 67% reflecting a very low growth

prospects about the company as the company might not be having positive NPV projects and

business operations for the purpose of investment.11

10 Alshomaly, Ibrahim, Ra’ed Masa’deh, and Jordan AqabaBranch. "The Capital Assets Pricing Model & Arbitrage

Pricing Theory: Properties and Applications in Jordan." Modern Applied Science 12.11 (2018).

11 "Dividend Information | Antofagasta PLC." Antofagasta.co.uk. N.p., 2019. Web. 25 Mar. 2019.

The dividend policy of the company has been volatile and the dividend p\yield generated by the

company on the stock has varied significantly in the last five-years. As observed the dividends

for a company may increase even if there is a decline observed in the earnings of the company.

The dividends of the company may not increase at a constant speed and the same might

also would not increase as the growth of earnings also. The above two points are the key and

crucial distinctive feature matches with the stable dividend policy. While paying out the

dividends of a company it is important to consider various business factors and macro-economic

factors reflecting the growth potential and the ability of the company in paying of a stable

dividend policy. If the level of operations and the belief by the management of the company is

high growth perspective than a higher dividend pay-out ratio could be well followed10.

The pay-out ratio maintained by the company in the five-year o trend analysis has always

been greater than 30% reflecting the ability of the company in providing a stable dividend policy.

However, with the changes in the growth perspective and the belief of the management regarding

the company operational plan the dividend has changed fir the company accordingly. The pay-

out ratio of the company was around 31% in the year 2013 reflecting the lowest pay-out ratio for

the company in the trend period analysed for the company. The highest pay-out ratio for the

company was in the year of 2017 when the same was around 67% reflecting a very low growth

prospects about the company as the company might not be having positive NPV projects and

business operations for the purpose of investment.11

10 Alshomaly, Ibrahim, Ra’ed Masa’deh, and Jordan AqabaBranch. "The Capital Assets Pricing Model & Arbitrage

Pricing Theory: Properties and Applications in Jordan." Modern Applied Science 12.11 (2018).

11 "Dividend Information | Antofagasta PLC." Antofagasta.co.uk. N.p., 2019. Web. 25 Mar. 2019.

8CORPORATE FINANCE

Evaluation of Cost of Equity

The cost of equity for a company could be well evaluated with the help of various

valuation techniques like by applying the Divided Growth Model or the Capital Asset Pricing

Model. In the case of the Capital Asset Pricing Model the value of equity is calculated with the

help of the factors like the prevailing risk free rate in the economy12. The market risk premium

that can be well calculated with the help of the return generated by market stocks less risk free

rate13. The beta of the stock could be calculated by observing the return given by both the stock

and index. However on the other hand side the Dividend growth model takes various factors on

the basis of assumption like the growth rate of the dividend and the current share price of the

company, which again is based on various market scenario and factors. It is important that the

cost of equity used for analysing the investment project should be such so that the same reflects

the potential return required for taking a certain amount of risk. The growth factors are the main

and important assumption that will be taken into account for the calculation of the required

return from the perspective of the dividend discount model. It is on the forecast and assumption

that varied growth rates can be taken according to the growth and increase in the operations of

the company14. Both the model has its own factors that are taken into account while making the

assumption regarding the input factors included in the model for computation of the required rate

of return on equity. However accuracy and sustainable input factors reflecting the risk associated

12Frazzini, Andrea, and Lasse Heje Pedersen. "Betting against beta." Journal of Financial Economics 111.1 (2014):

1-25.

13 Nhleko, A. S., and C. Musingwini. "Estimating cost of equity in project discount rates using the capital asset

pricing model and Gordon’s wealth growth model." International Journal of Mining, Reclamation and Environment

30.5 (2016): 390-404.

14Lawson, Bradley P., and Dechun Wang. "The earnings quality information content of dividend policies and audit

pricing." Contemporary Accounting Research 33.4 (2016): 1685-1719.

Evaluation of Cost of Equity

The cost of equity for a company could be well evaluated with the help of various

valuation techniques like by applying the Divided Growth Model or the Capital Asset Pricing

Model. In the case of the Capital Asset Pricing Model the value of equity is calculated with the

help of the factors like the prevailing risk free rate in the economy12. The market risk premium

that can be well calculated with the help of the return generated by market stocks less risk free

rate13. The beta of the stock could be calculated by observing the return given by both the stock

and index. However on the other hand side the Dividend growth model takes various factors on

the basis of assumption like the growth rate of the dividend and the current share price of the

company, which again is based on various market scenario and factors. It is important that the

cost of equity used for analysing the investment project should be such so that the same reflects

the potential return required for taking a certain amount of risk. The growth factors are the main

and important assumption that will be taken into account for the calculation of the required

return from the perspective of the dividend discount model. It is on the forecast and assumption

that varied growth rates can be taken according to the growth and increase in the operations of

the company14. Both the model has its own factors that are taken into account while making the

assumption regarding the input factors included in the model for computation of the required rate

of return on equity. However accuracy and sustainable input factors reflecting the risk associated

12Frazzini, Andrea, and Lasse Heje Pedersen. "Betting against beta." Journal of Financial Economics 111.1 (2014):

1-25.

13 Nhleko, A. S., and C. Musingwini. "Estimating cost of equity in project discount rates using the capital asset

pricing model and Gordon’s wealth growth model." International Journal of Mining, Reclamation and Environment

30.5 (2016): 390-404.

14Lawson, Bradley P., and Dechun Wang. "The earnings quality information content of dividend policies and audit

pricing." Contemporary Accounting Research 33.4 (2016): 1685-1719.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE FINANCE

with the company should be taken into account for the purpose of computation of the required

rate of return on equity15.

The key factor in taking the required rate of return via the CAPM model is the selection

of the proper benchmark with which the return of the stock will be regressed with the benchmark

index for getting the beta of the stock. The beta is an important tool in the computation of the

required rate of return for the stock. On the other hand required rate of return via the Gordon

growth model is far more justified in this case where the prevailing share price, dividends paid

by the company and the growth rate would be taken for the purpose of analysis.

Conclusion

The financial valuation of the company was done by taking the financial data of the

company from the year 2013-2018. The dividend discount model and the Capital Asset Pricing

Model was done for valuing the required return by the equity investors. Asset Beta and Equity

beta are the two important components playing an important role in the organisation with the

help of the debt and equity ratio of the company. It was evaluated that the risks and return plays

an important role from the perspective of investment so there should be necessary factors and

conditions that should be taken into account while doing the financial valuation of the company.

On an overall basis the risk associated with the company was found to be comparatively low

when the same was compared with the context of the FTSE 100 index. The moderate volatility

beta stock can be considered a good and sound investment plan as stock can be used in portfolio

for creating value.

15 Firth, Michael, et al. "Institutional stock ownership and firms’ cash dividend policies: Evidence from China."

Journal of Banking & Finance 65 (2016): 91-107.

with the company should be taken into account for the purpose of computation of the required

rate of return on equity15.

The key factor in taking the required rate of return via the CAPM model is the selection

of the proper benchmark with which the return of the stock will be regressed with the benchmark

index for getting the beta of the stock. The beta is an important tool in the computation of the

required rate of return for the stock. On the other hand required rate of return via the Gordon

growth model is far more justified in this case where the prevailing share price, dividends paid

by the company and the growth rate would be taken for the purpose of analysis.

Conclusion

The financial valuation of the company was done by taking the financial data of the

company from the year 2013-2018. The dividend discount model and the Capital Asset Pricing

Model was done for valuing the required return by the equity investors. Asset Beta and Equity

beta are the two important components playing an important role in the organisation with the

help of the debt and equity ratio of the company. It was evaluated that the risks and return plays

an important role from the perspective of investment so there should be necessary factors and

conditions that should be taken into account while doing the financial valuation of the company.

On an overall basis the risk associated with the company was found to be comparatively low

when the same was compared with the context of the FTSE 100 index. The moderate volatility

beta stock can be considered a good and sound investment plan as stock can be used in portfolio

for creating value.

15 Firth, Michael, et al. "Institutional stock ownership and firms’ cash dividend policies: Evidence from China."

Journal of Banking & Finance 65 (2016): 91-107.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE FINANCE

References

1. Pedersen, Niels, Sébastien Page, and Fei He. "Asset allocation: Risk models for

alternative investments." Financial Analysts Journal 70.3 (2014): 34-45.

2. Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor

sentiment, beta, and the cost of equity capital." Management Science 62.2 (2015): 347-

367.

3. "United Kingdom Government Bond 10Y | 2019 | Data | Chart | Calendar."

Tradingeconomics.com. N.p., 2019. Web. 25 Mar. 2019.

4. "FTSE 100 Index Data." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

5. "Antofagasta Plc Share Price." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

6. Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor

sentiment, beta, and the cost of equity capital." Management Science 62.2 (2015): 347-

367.

7. "Unlevered Beta (Asset Beta) - Formula, Calculation, And Examples." Corporate Finance

Institute. N.p., 2019. Web. 25 Mar. 2019.

8. Buchner, Axel. "The alpha and beta of private equity investments." Available at SSRN

2549705 (2014).

9. Ashraf, Badar Nadeem, and Changjun Zheng. "Shareholder protection, creditor rights and

bank dividend policies." China Finance Review International 5.2 (2015): 161-186.

10. Alshomaly, Ibrahim, Ra’ed Masa’deh, and Jordan AqabaBranch. "The Capital Assets

Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan."

Modern Applied Science 12.11 (2018).

References

1. Pedersen, Niels, Sébastien Page, and Fei He. "Asset allocation: Risk models for

alternative investments." Financial Analysts Journal 70.3 (2014): 34-45.

2. Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor

sentiment, beta, and the cost of equity capital." Management Science 62.2 (2015): 347-

367.

3. "United Kingdom Government Bond 10Y | 2019 | Data | Chart | Calendar."

Tradingeconomics.com. N.p., 2019. Web. 25 Mar. 2019.

4. "FTSE 100 Index Data." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

5. "Antofagasta Plc Share Price." Finance.yahoo.com. N.p., 2019. Web. 25 Mar. 2019.

6. Antoniou, Constantinos, John A. Doukas, and Avanidhar Subrahmanyam. "Investor

sentiment, beta, and the cost of equity capital." Management Science 62.2 (2015): 347-

367.

7. "Unlevered Beta (Asset Beta) - Formula, Calculation, And Examples." Corporate Finance

Institute. N.p., 2019. Web. 25 Mar. 2019.

8. Buchner, Axel. "The alpha and beta of private equity investments." Available at SSRN

2549705 (2014).

9. Ashraf, Badar Nadeem, and Changjun Zheng. "Shareholder protection, creditor rights and

bank dividend policies." China Finance Review International 5.2 (2015): 161-186.

10. Alshomaly, Ibrahim, Ra’ed Masa’deh, and Jordan AqabaBranch. "The Capital Assets

Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan."

Modern Applied Science 12.11 (2018).

11CORPORATE FINANCE

11. "Dividend Information | Antofagasta PLC." Antofagasta.co.uk. N.p., 2019. Web. 25 Mar.

2019.

12. Frazzini, Andrea, and Lasse Heje Pedersen. "Betting against beta." Journal of Financial

Economics 111.1 (2014): 1-25.

13. Nhleko, A. S., and C. Musingwini. "Estimating cost of equity in project discount rates

using the capital asset pricing model and Gordon’s wealth growth model." International

Journal of Mining, Reclamation and Environment 30.5 (2016): 390-404.

14. Lawson, Bradley P., and Dechun Wang. "The earnings quality information content of

dividend policies and audit pricing." Contemporary Accounting Research 33.4 (2016):

1685-1719.

15. Firth, Michael, et al. "Institutional stock ownership and firms’ cash dividend policies:

Evidence from China." Journal of Banking & Finance 65 (2016): 91-107.

11. "Dividend Information | Antofagasta PLC." Antofagasta.co.uk. N.p., 2019. Web. 25 Mar.

2019.

12. Frazzini, Andrea, and Lasse Heje Pedersen. "Betting against beta." Journal of Financial

Economics 111.1 (2014): 1-25.

13. Nhleko, A. S., and C. Musingwini. "Estimating cost of equity in project discount rates

using the capital asset pricing model and Gordon’s wealth growth model." International

Journal of Mining, Reclamation and Environment 30.5 (2016): 390-404.

14. Lawson, Bradley P., and Dechun Wang. "The earnings quality information content of

dividend policies and audit pricing." Contemporary Accounting Research 33.4 (2016):

1685-1719.

15. Firth, Michael, et al. "Institutional stock ownership and firms’ cash dividend policies:

Evidence from China." Journal of Banking & Finance 65 (2016): 91-107.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.