Contemporary Issues in Accounting: ANZ Limited Standards Report

VerifiedAdded on 2022/07/28

|9

|1789

|32

Report

AI Summary

This report examines ANZ Limited's adherence to contemporary accounting standards, specifically focusing on AASB 9 (Financial Instruments) and AASB 15 (Revenue from Contracts with Customers). It provides an executive summary, introduction, and detailed analysis of the application of these standards, including the classification and measurement of financial assets under AASB 9, and the five-step model for revenue recognition under AASB 15. The report also highlights the company's disclosures related to these standards, including transitional impacts and changes in accounting policies. The conclusion affirms ANZ's compliance with the relevant standards, supported by an auditor's clean report. References to key resources are also included.

CONTEMPORARY ISSUES IN ACCOUNTING

1

CONTEMPORARY

ISSUES IN

ACCOUNTING

1

CONTEMPORARY

ISSUES IN

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ISSUES IN ACCOUNTING

2

Executive summary:

The accounting standards lay down the rules and requirements with regard to accounting that

have to be followed by each company while preparing its financial statements. The company

chosen for this report is ANZ limited and it can be stated that it complies with the accounting

rules and regulations.

2

Executive summary:

The accounting standards lay down the rules and requirements with regard to accounting that

have to be followed by each company while preparing its financial statements. The company

chosen for this report is ANZ limited and it can be stated that it complies with the accounting

rules and regulations.

CONTEMPORARY ISSUES IN ACCOUNTING

3

Contents

Introduction:...............................................................................................................................4

AASB 9 Financial instruments:.............................................................................................4

AASB 15 Revenue from contracts with customers:..............................................................5

Disclosures:................................................................................................................................6

AASB 9 FINANCIAL INSTRUMENTS (AASB 9):............................................................6

AASB 15 revenue from contracts with customers:................................................................6

Conclusion:...............................................................................................................................7

References:............................................................................................................................8

3

Contents

Introduction:...............................................................................................................................4

AASB 9 Financial instruments:.............................................................................................4

AASB 15 Revenue from contracts with customers:..............................................................5

Disclosures:................................................................................................................................6

AASB 9 FINANCIAL INSTRUMENTS (AASB 9):............................................................6

AASB 15 revenue from contracts with customers:................................................................6

Conclusion:...............................................................................................................................7

References:............................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ISSUES IN ACCOUNTING

4

Introduction:

The assignment requires the choosing of a company listed on the ASX and then reporting the

rules and regulations as have been required to be followed by two accounting standards. Then

the disclosures with regard to those 2 chosen accounting standards have been written down.

The company chosen for the purposes of this report is ANZ limited which is a company listed

on ASX and belongs to the industry of banking.

AASB 9 Financial instruments:

The Annual report of the company contains the application of AASB 9 that deals with the financial

instruments.

As per the requirements of the accounting standard, when the financial instruments are recognised initially,

then the financial asset shall be measured at its fair values. And if this is not the case, then the transactions

costs connected with such financial assets shall be attributed directly with the financial asset.

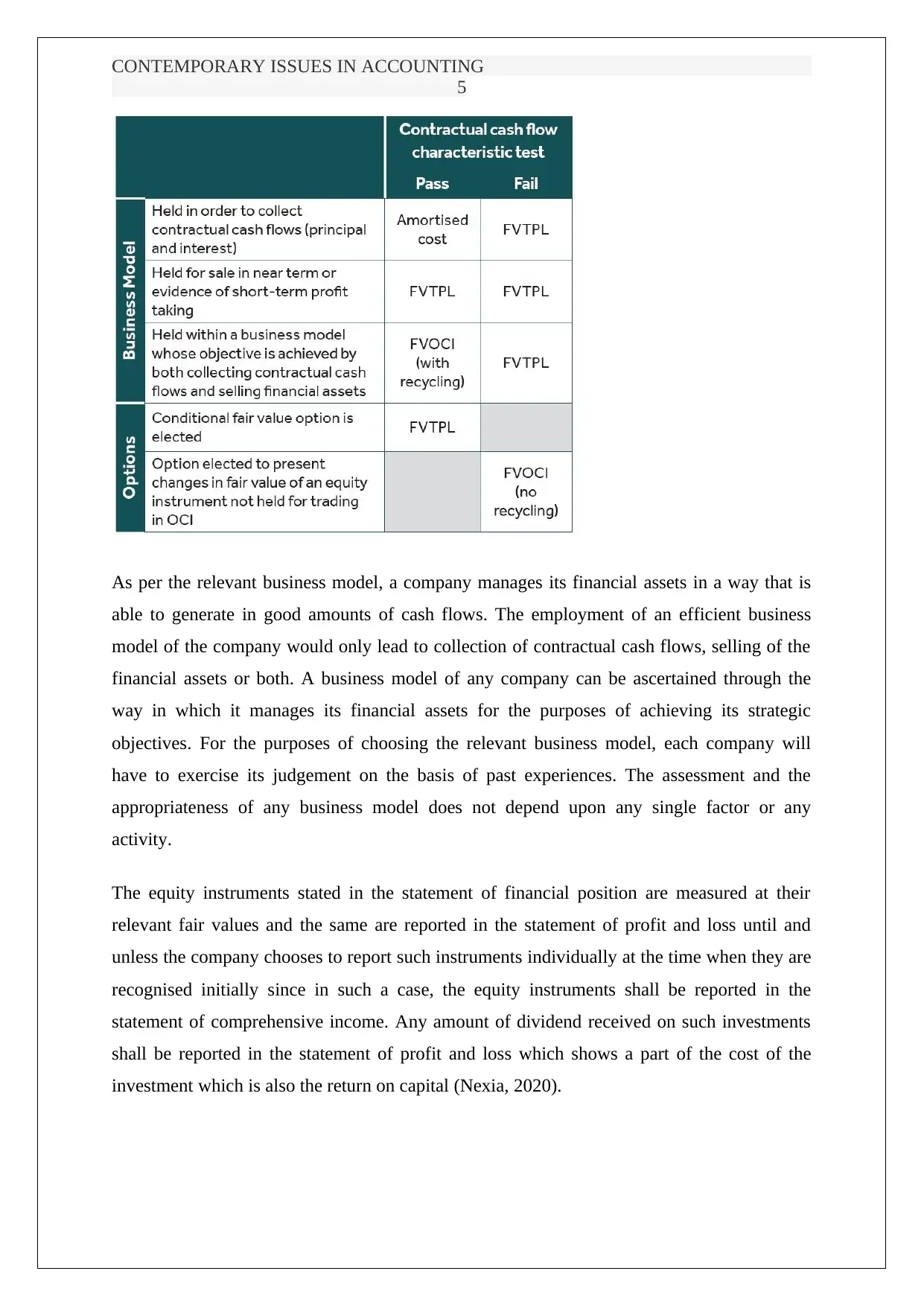

All of the financial assets are reported as per their relevant contractual cash flow characteristics and the

relevant business model under which these are held. The following is the table that summarises the

classification and the subsequent measurement of the financial assets:

4

Introduction:

The assignment requires the choosing of a company listed on the ASX and then reporting the

rules and regulations as have been required to be followed by two accounting standards. Then

the disclosures with regard to those 2 chosen accounting standards have been written down.

The company chosen for the purposes of this report is ANZ limited which is a company listed

on ASX and belongs to the industry of banking.

AASB 9 Financial instruments:

The Annual report of the company contains the application of AASB 9 that deals with the financial

instruments.

As per the requirements of the accounting standard, when the financial instruments are recognised initially,

then the financial asset shall be measured at its fair values. And if this is not the case, then the transactions

costs connected with such financial assets shall be attributed directly with the financial asset.

All of the financial assets are reported as per their relevant contractual cash flow characteristics and the

relevant business model under which these are held. The following is the table that summarises the

classification and the subsequent measurement of the financial assets:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ISSUES IN ACCOUNTING

5

As per the relevant business model, a company manages its financial assets in a way that is

able to generate in good amounts of cash flows. The employment of an efficient business

model of the company would only lead to collection of contractual cash flows, selling of the

financial assets or both. A business model of any company can be ascertained through the

way in which it manages its financial assets for the purposes of achieving its strategic

objectives. For the purposes of choosing the relevant business model, each company will

have to exercise its judgement on the basis of past experiences. The assessment and the

appropriateness of any business model does not depend upon any single factor or any

activity.

The equity instruments stated in the statement of financial position are measured at their

relevant fair values and the same are reported in the statement of profit and loss until and

unless the company chooses to report such instruments individually at the time when they are

recognised initially since in such a case, the equity instruments shall be reported in the

statement of comprehensive income. Any amount of dividend received on such investments

shall be reported in the statement of profit and loss which shows a part of the cost of the

investment which is also the return on capital (Nexia, 2020).

5

As per the relevant business model, a company manages its financial assets in a way that is

able to generate in good amounts of cash flows. The employment of an efficient business

model of the company would only lead to collection of contractual cash flows, selling of the

financial assets or both. A business model of any company can be ascertained through the

way in which it manages its financial assets for the purposes of achieving its strategic

objectives. For the purposes of choosing the relevant business model, each company will

have to exercise its judgement on the basis of past experiences. The assessment and the

appropriateness of any business model does not depend upon any single factor or any

activity.

The equity instruments stated in the statement of financial position are measured at their

relevant fair values and the same are reported in the statement of profit and loss until and

unless the company chooses to report such instruments individually at the time when they are

recognised initially since in such a case, the equity instruments shall be reported in the

statement of comprehensive income. Any amount of dividend received on such investments

shall be reported in the statement of profit and loss which shows a part of the cost of the

investment which is also the return on capital (Nexia, 2020).

CONTEMPORARY ISSUES IN ACCOUNTING

6

The above is an option which is irrevocable and applies only to the equity instruments,

irrespective of the fact whether these are held for the purposes of trading or for a contingent

consideration as a part of the business combination.

With regard to the unlisted equity investments, the company shall measure the investments in

the equity at their relevant costs if these investments do not have quoted price available for

them in the active market and their fair value cannot be reliably measured (as per AASB

139). AASB 9 requires no such condition and these are valued at their respective fair values.

Then the accounting standard requires the use of an impairment model for the financial assets

on a forward looking expected credit loss model. This model requires the use of amortised

costs for the debt instruments or fair value through other comprehensive income approach.

The following are the 3 points of assessment for impairment model:

Simplified approach which shall be applied to the trade receivables

Approach which would be applicable on the loans and debt securities

The approach for the purchased or originated credit impairment (AASB, 2020)

With regard to the requirements of AASB 15 which deals with the contracts with the

customers, the accounting standard states the use of a 5 step model for the purposes of

recognising the revenue and the amount at which the same shall be recognised.

Revenue shall be reported as and when the company transfers all the control over the goods

or the services to the customer and the same has been done at the amount which the company

was expecting to receive (Accru, 2020).

Revenue can be recognised over a period of time if some of the criteria is not met, this is

usually done when it is ascertained that the deferred recognition shall result in a much better

picture of the statement of affairs of the company (AASB, 2020).

The following are the steps of recognition of revenue:

1. Contract identification

2. Performance obligations identification

3. Transaction price determination

6

The above is an option which is irrevocable and applies only to the equity instruments,

irrespective of the fact whether these are held for the purposes of trading or for a contingent

consideration as a part of the business combination.

With regard to the unlisted equity investments, the company shall measure the investments in

the equity at their relevant costs if these investments do not have quoted price available for

them in the active market and their fair value cannot be reliably measured (as per AASB

139). AASB 9 requires no such condition and these are valued at their respective fair values.

Then the accounting standard requires the use of an impairment model for the financial assets

on a forward looking expected credit loss model. This model requires the use of amortised

costs for the debt instruments or fair value through other comprehensive income approach.

The following are the 3 points of assessment for impairment model:

Simplified approach which shall be applied to the trade receivables

Approach which would be applicable on the loans and debt securities

The approach for the purchased or originated credit impairment (AASB, 2020)

With regard to the requirements of AASB 15 which deals with the contracts with the

customers, the accounting standard states the use of a 5 step model for the purposes of

recognising the revenue and the amount at which the same shall be recognised.

Revenue shall be reported as and when the company transfers all the control over the goods

or the services to the customer and the same has been done at the amount which the company

was expecting to receive (Accru, 2020).

Revenue can be recognised over a period of time if some of the criteria is not met, this is

usually done when it is ascertained that the deferred recognition shall result in a much better

picture of the statement of affairs of the company (AASB, 2020).

The following are the steps of recognition of revenue:

1. Contract identification

2. Performance obligations identification

3. Transaction price determination

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ISSUES IN ACCOUNTING

7

4. Transaction price allocation

5. Revenue recognition

Revenue can also be recognised at the point of time when the control of the goods or the

services have been transferred on to the customer.

(Bhattacharya, 2020).

Disclosures:

AASB 9, the company undertaken for review went on to apply the requirements of AASB 9

from October 1, 2018. But these requirements were not applied on the credit requirements

connected with the financial liabilities that was required to be measured at fair value which

was adopted by the group much before, from October 1, 2013. The company also chose to

adopt the requirements of AASC2017-6 which deals with the Australian Accounting

Standards connected with the prepayment feature of the negative compensation from October

1, 2018. The company has been given a choice of accounting policy that the group has

applied during the current year and this is continuance of the application of AASB

139 which deals with the requirements of hedge accounting. The group has chosen to do this

till the time the current project of International Accounting Standard’s Board, Macro hedge

accounting is completed. AASB 9 and AASB 2017-6 deals with the requirements for the

impairment of the financial assets along with the classification and the measurement of the

financial assets and the financial liabilities and general hedge accounting. The details of these

key requirements have been duly stated in the financial assets and the financial liabilities

section listed on pages 125 and 144 respectively. This is then accompanied by the

reconciliation of the transitional impact of adoption of the accounting standard from October

1, 2018 which has been set out under Note 35 of the Annual report.

7

4. Transaction price allocation

5. Revenue recognition

Revenue can also be recognised at the point of time when the control of the goods or the

services have been transferred on to the customer.

(Bhattacharya, 2020).

Disclosures:

AASB 9, the company undertaken for review went on to apply the requirements of AASB 9

from October 1, 2018. But these requirements were not applied on the credit requirements

connected with the financial liabilities that was required to be measured at fair value which

was adopted by the group much before, from October 1, 2013. The company also chose to

adopt the requirements of AASC2017-6 which deals with the Australian Accounting

Standards connected with the prepayment feature of the negative compensation from October

1, 2018. The company has been given a choice of accounting policy that the group has

applied during the current year and this is continuance of the application of AASB

139 which deals with the requirements of hedge accounting. The group has chosen to do this

till the time the current project of International Accounting Standard’s Board, Macro hedge

accounting is completed. AASB 9 and AASB 2017-6 deals with the requirements for the

impairment of the financial assets along with the classification and the measurement of the

financial assets and the financial liabilities and general hedge accounting. The details of these

key requirements have been duly stated in the financial assets and the financial liabilities

section listed on pages 125 and 144 respectively. This is then accompanied by the

reconciliation of the transitional impact of adoption of the accounting standard from October

1, 2018 which has been set out under Note 35 of the Annual report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ISSUES IN ACCOUNTING

8

AASB 15 deals with the revenue from contracts entered into with the customers. The group

had adopted this accounting policy from October 1, 2018. The adoption of this accounting

policy resulted in the change in the accounting policies and adjustments had to be made in the

amounts that were reported in the statement of financial position. This accounting standard

required the identification of some separate performance obligations that were within a

contract and the allocation of the transaction price of the contract from these performance

obligations. The company recognises the revenue once the performance obligations were

satisfied. The standards also provided some guidance on the company acting as the principal

and as an agent that affected the reporting of the revenue on gross or net basis. The

accounting standard provided some transitional provisions that were duly adopted by the

company in full. Under it, the cumulative impact of this standard was recognised as an

adjustment in the statement of retained earnings as on October 1, 2017 along with the

comparative information for the year 2018 was duly restated. The adoption led to the

following changes in the accounting policy:

The trail commission revenue which was reported in the financial accounts at the time

when the products were transferred to the customer would not be reported in the

financial accounts only when it is certain that such revenue would not be reversed in

any of the future periods. This policy led to an increase in the opening balances pf the

assets as on October 1, 2017. There was no impact on the earning per share though.

There were some credit card loyalty costs and other such costs which were deducted

from the operating income in the years but now, the company shall report these as an

operating income and operating expenses. This led to the increase in the operating

income and operating expenses during the year 2018. There was no impact on the

earning per share though (ANZ limited, 2020).

Conclusion:

The company has duly complied with the relevant accounting standards of AASB and AASB

15 which is good. Further, an auditor has also issued a clean report which means that the

financial facts contained in the financial statements of the company represent a true and a fair

picture of the company.

8

AASB 15 deals with the revenue from contracts entered into with the customers. The group

had adopted this accounting policy from October 1, 2018. The adoption of this accounting

policy resulted in the change in the accounting policies and adjustments had to be made in the

amounts that were reported in the statement of financial position. This accounting standard

required the identification of some separate performance obligations that were within a

contract and the allocation of the transaction price of the contract from these performance

obligations. The company recognises the revenue once the performance obligations were

satisfied. The standards also provided some guidance on the company acting as the principal

and as an agent that affected the reporting of the revenue on gross or net basis. The

accounting standard provided some transitional provisions that were duly adopted by the

company in full. Under it, the cumulative impact of this standard was recognised as an

adjustment in the statement of retained earnings as on October 1, 2017 along with the

comparative information for the year 2018 was duly restated. The adoption led to the

following changes in the accounting policy:

The trail commission revenue which was reported in the financial accounts at the time

when the products were transferred to the customer would not be reported in the

financial accounts only when it is certain that such revenue would not be reversed in

any of the future periods. This policy led to an increase in the opening balances pf the

assets as on October 1, 2017. There was no impact on the earning per share though.

There were some credit card loyalty costs and other such costs which were deducted

from the operating income in the years but now, the company shall report these as an

operating income and operating expenses. This led to the increase in the operating

income and operating expenses during the year 2018. There was no impact on the

earning per share though (ANZ limited, 2020).

Conclusion:

The company has duly complied with the relevant accounting standards of AASB and AASB

15 which is good. Further, an auditor has also issued a clean report which means that the

financial facts contained in the financial statements of the company represent a true and a fair

picture of the company.

CONTEMPORARY ISSUES IN ACCOUNTING

9

References:

Aasb.gov.au. 2020. AASB 9 Financial Instruments. [online] Available at:

<https://www.aasb.gov.au/admin/file/content105/c9/AASB9_12-14.pdf> [Accessed 20 April

2020].

Aasb.gov.au. 2020. Revenue From Contracts With Customers. [online] Available at:

<https://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14_COMPsep18_01-

19.pdf> [Accessed 20 April 2020].

Accru. 2020. AASB 15 Summary And Five-Step Model Explained - Accru. [online] Available

at: <https://www.accru.com/2018/08/aasb-15-summary-five-step-model/> [Accessed 20

April 2020].

Anz.com. 2020. Annual Report 2019. [online] Available at:

<https://www.anz.com/content/dam/anzcom/shareholder/ANZ-2019-Annual-Report.pdf>

[Accessed 20 April 2020].

Bhattacharya, S., 2020. New Revenue Standard – Introducing AASB 15. [online] KPMG.

Available at: <https://home.kpmg/au/en/home/insights/2017/04/introducing-aasb-15-revenue-

standard.html> [Accessed 20 April 2020].

nexia.com.au. 2020. AASB 9. [online] Available at:

<https://nexia.com.au/news/accounting/aasb-9-financial-instruments-understanding-the-

basics https://home.kpmg/au/en/home/insights/2017/09/aasb-9-financial-instruments-

transition-practical-guide.html> [Accessed 20 April 2020].

9

References:

Aasb.gov.au. 2020. AASB 9 Financial Instruments. [online] Available at:

<https://www.aasb.gov.au/admin/file/content105/c9/AASB9_12-14.pdf> [Accessed 20 April

2020].

Aasb.gov.au. 2020. Revenue From Contracts With Customers. [online] Available at:

<https://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14_COMPsep18_01-

19.pdf> [Accessed 20 April 2020].

Accru. 2020. AASB 15 Summary And Five-Step Model Explained - Accru. [online] Available

at: <https://www.accru.com/2018/08/aasb-15-summary-five-step-model/> [Accessed 20

April 2020].

Anz.com. 2020. Annual Report 2019. [online] Available at:

<https://www.anz.com/content/dam/anzcom/shareholder/ANZ-2019-Annual-Report.pdf>

[Accessed 20 April 2020].

Bhattacharya, S., 2020. New Revenue Standard – Introducing AASB 15. [online] KPMG.

Available at: <https://home.kpmg/au/en/home/insights/2017/04/introducing-aasb-15-revenue-

standard.html> [Accessed 20 April 2020].

nexia.com.au. 2020. AASB 9. [online] Available at:

<https://nexia.com.au/news/accounting/aasb-9-financial-instruments-understanding-the-

basics https://home.kpmg/au/en/home/insights/2017/09/aasb-9-financial-instruments-

transition-practical-guide.html> [Accessed 20 April 2020].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.