Financial Reporting and Accounting Strategy Analysis: ANZ Bank Report

VerifiedAdded on 2020/03/01

|19

|3548

|60

Report

AI Summary

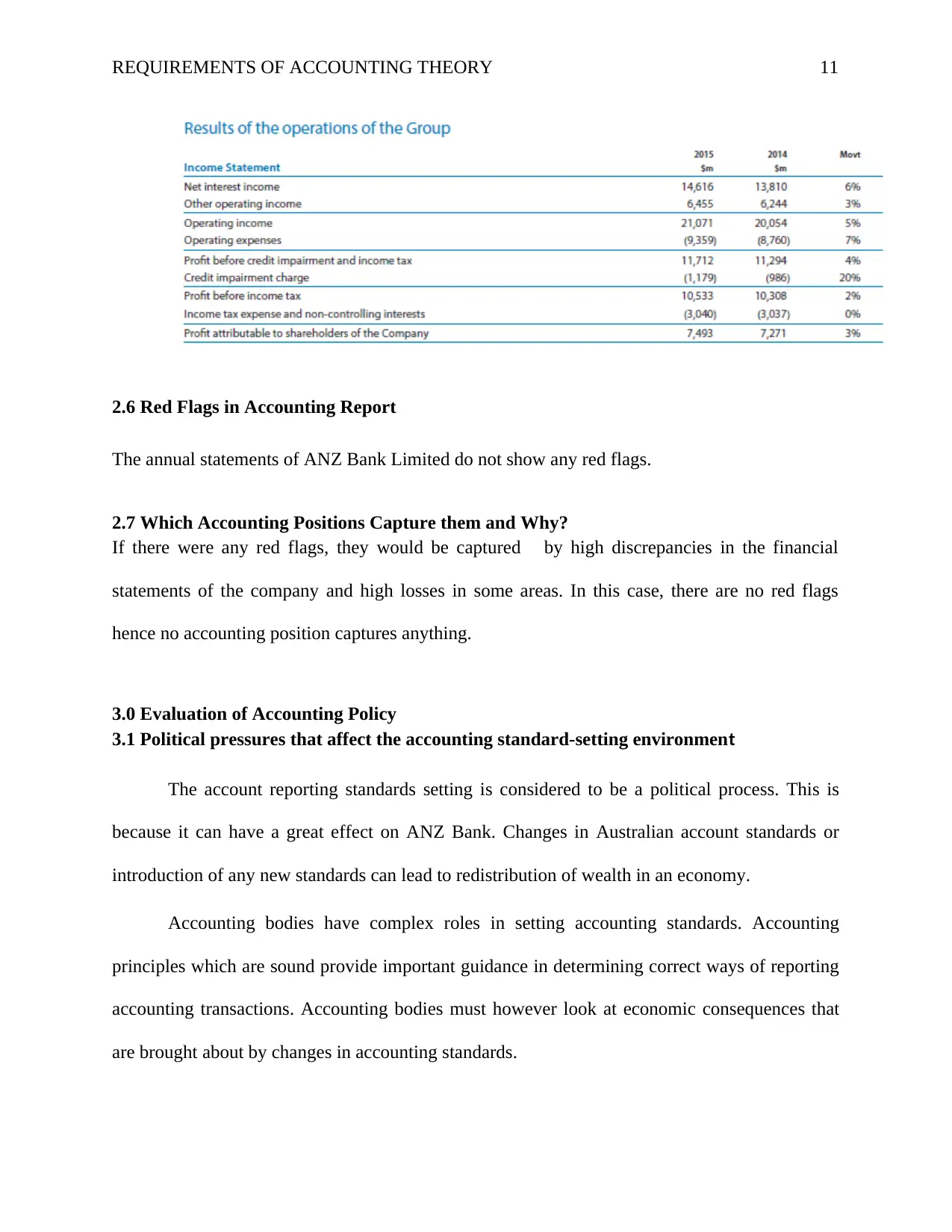

This report provides a detailed analysis of ANZ Bank's accounting strategy and financial reporting practices, examining the bank's approach to financial statements for the years 2015 and 2016. It covers key accounting policies and estimates, including the basis of preparation, income and expense recognition, and income tax. The report assesses the flexibility of these policies, compares them to those of a competitor (Westpac Bank), and evaluates their acceptability, reliability, and relevance. Furthermore, it determines whether the accounting strategy is revealing or hiding information, identifies any red flags, and evaluates the impact of political pressures on accounting standard-setting. The analysis also includes an assessment of ANZ Bank managers' accounting and reporting strategy, evaluating the quality of disclosures and identifying potential red flags, while also considering the bank's compliance with the conceptual framework. The report concludes with an overview of the bank's financial reporting strategy, its strengths, and potential areas for improvement.

Running head: REQUIREMENTS OF ACCOUNTING THEORY 1

Requirements of Accounting Theory

Name:

Institution:

Affiliation:

Requirements of Accounting Theory

Name:

Institution:

Affiliation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REQUIREMENTS OF ACCOUNTING THEORY 2

Executive Summary

Accounting reporting and strategy is very important in any organization. Success can only be

achieved if a company follows the right procedures in policy implementation and reporting, with

regards to accounting. The report looks at one of the most successful banks in Australia and New

Zealand, ANZ Bank and the kind of reporting strategy, which they use. The report has an

introduction, main body, which outlines the strategy that has been used by the bank and then

ends with a conclusion of the same. The report will look into the details of some of the

accounting policies, which have been put in place by ANZ Bank Limited.

Executive Summary

Accounting reporting and strategy is very important in any organization. Success can only be

achieved if a company follows the right procedures in policy implementation and reporting, with

regards to accounting. The report looks at one of the most successful banks in Australia and New

Zealand, ANZ Bank and the kind of reporting strategy, which they use. The report has an

introduction, main body, which outlines the strategy that has been used by the bank and then

ends with a conclusion of the same. The report will look into the details of some of the

accounting policies, which have been put in place by ANZ Bank Limited.

REQUIREMENTS OF ACCOUNTING THEORY 3

Contents

Executive Summary.........................................................................................................................2

1.0 Introduction................................................................................................................................4

2.0 Accounting Policies and Estimates............................................................................................4

2.1 Accounting Policies and Estimates Used...............................................................................4

2.1.1 Basis of Preparation.........................................................................................................4

2.1.2 Recognition of Income....................................................................................................5

2.1.3 Recognition of Expense...................................................................................................6

2.1.4 Income Tax......................................................................................................................6

2.2 Flexibilities of Accounting Policies and Estimates Used by ANZ Bank Limited.................7

2.3 Accounting Policies and Estimates Used by ANZ Bank Competitors..................................7

2.4 If Policies and Estimates are Acceptable...............................................................................8

2.5 Is Accounting Strategy Hiding or Revealing.........................................................................9

2.6 Red Flags in Accounting Report..........................................................................................11

2.7 Which Accounting Positions Capture them and Why?........................................................11

3.0 Evaluation of Accounting Policy.............................................................................................11

3.1 Political pressures that affect the accounting standard-setting environmen........................11

3.2 Implications of organizations making accounting disclosures............................................12

3.3 Understand the Implications of Particular Accounting Disclosures....................................13

4.0 Report on ANZ Bank Managers’ Accounting and Reporting Strategy...................................13

4. 1 Identify Key Accounting Policies.......................................................................................13

4. 2 Assess Accounting Flexibility............................................................................................14

4.3 Evaluate Accounting Strategy..............................................................................................14

4.4 Evaluate the Quality of Disclosure......................................................................................15

4.5 Identify Potential Red Flags.................................................................................................17

5.0 Compliance with Conceptual Framework...............................................................................17

6.0 Conclusion...............................................................................................................................17

6.0 References................................................................................................................................19

Contents

Executive Summary.........................................................................................................................2

1.0 Introduction................................................................................................................................4

2.0 Accounting Policies and Estimates............................................................................................4

2.1 Accounting Policies and Estimates Used...............................................................................4

2.1.1 Basis of Preparation.........................................................................................................4

2.1.2 Recognition of Income....................................................................................................5

2.1.3 Recognition of Expense...................................................................................................6

2.1.4 Income Tax......................................................................................................................6

2.2 Flexibilities of Accounting Policies and Estimates Used by ANZ Bank Limited.................7

2.3 Accounting Policies and Estimates Used by ANZ Bank Competitors..................................7

2.4 If Policies and Estimates are Acceptable...............................................................................8

2.5 Is Accounting Strategy Hiding or Revealing.........................................................................9

2.6 Red Flags in Accounting Report..........................................................................................11

2.7 Which Accounting Positions Capture them and Why?........................................................11

3.0 Evaluation of Accounting Policy.............................................................................................11

3.1 Political pressures that affect the accounting standard-setting environmen........................11

3.2 Implications of organizations making accounting disclosures............................................12

3.3 Understand the Implications of Particular Accounting Disclosures....................................13

4.0 Report on ANZ Bank Managers’ Accounting and Reporting Strategy...................................13

4. 1 Identify Key Accounting Policies.......................................................................................13

4. 2 Assess Accounting Flexibility............................................................................................14

4.3 Evaluate Accounting Strategy..............................................................................................14

4.4 Evaluate the Quality of Disclosure......................................................................................15

4.5 Identify Potential Red Flags.................................................................................................17

5.0 Compliance with Conceptual Framework...............................................................................17

6.0 Conclusion...............................................................................................................................17

6.0 References................................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REQUIREMENTS OF ACCOUNTING THEORY 4

Accounting Reporting Strategy of ANZ Bank

1.0 Introduction

ANZ Bank is one of the most successful banks in Australia and New Zealand. The report

views the annual reports for 2015 and 2016 for the bank and looks at the strategy which the bank

has used in its financial reporting (ANZ, 2017). The report therefore views various accounting

policies and how they have been applied to the organization.

2.0 Accounting Policies and Estimates

2.1 Accounting Policies and Estimates Used

2.1.1 Basis of Preparation

Compliance - The financial statements for ANZ Bank are prepared according to

requirements of the Financial Markets Conduct Act of 2013. The financial statements are in

compliance with Australia’s accepted accounting practices, International Financial Reporting

Standards and any other reporting standards which are applicable (ANZ, 2017).

Estimates and Assumptions – The financial statements have been prepared using

management judgements, estimates and assumptions which affect whatever has been reported.

Measurement – The financial statements have been prepared according to historical case

basis and some assets and liabilities are stated at a fair value. These assets and liabilities are

derivative financial instruments, assets which are available for sale, financial instruments which

have been held for trading and those that have been designated at fair value through profit and

loss.

Accounting Reporting Strategy of ANZ Bank

1.0 Introduction

ANZ Bank is one of the most successful banks in Australia and New Zealand. The report

views the annual reports for 2015 and 2016 for the bank and looks at the strategy which the bank

has used in its financial reporting (ANZ, 2017). The report therefore views various accounting

policies and how they have been applied to the organization.

2.0 Accounting Policies and Estimates

2.1 Accounting Policies and Estimates Used

2.1.1 Basis of Preparation

Compliance - The financial statements for ANZ Bank are prepared according to

requirements of the Financial Markets Conduct Act of 2013. The financial statements are in

compliance with Australia’s accepted accounting practices, International Financial Reporting

Standards and any other reporting standards which are applicable (ANZ, 2017).

Estimates and Assumptions – The financial statements have been prepared using

management judgements, estimates and assumptions which affect whatever has been reported.

Measurement – The financial statements have been prepared according to historical case

basis and some assets and liabilities are stated at a fair value. These assets and liabilities are

derivative financial instruments, assets which are available for sale, financial instruments which

have been held for trading and those that have been designated at fair value through profit and

loss.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REQUIREMENTS OF ACCOUNTING THEORY 5

Rounding – ANZ Bank rounds off its financial statements to the nearest million dollars

unless stated otherwise.

Consolidated Subsidiaries – Consolidated financial statements include all the businesses

in Australia and New Zealand. The equity method of accounting is applied for any associates.

Foreign Currency – The financial statements of ANZ are presented in Australian dollars.

Any foreign currency transactions are converted into the functional currency using the day’s

prevailing exchange rates (ANZ, 2017). Any monetary assets or liabilities that have resulted

from foreign currency are converted at spot rates as at the reporting date. Any differences in

exchange rates are reported in the income statement.

2.1.2 Recognition of Income

Interest Income – This is calculated using the effective interest method. It is based on the

income which is received by ANZ Bank from interest on its assets minus interest that is paid on

liabilities. Assets include loans and mortgages while liabilities include accounts (ANZ, 2017).

Commission and Fees – ANZ Bank’s commission and fees are calculated using the

effective interest method. Commission and fees are gained after provision of various services to

bank customers.

Rounding – ANZ Bank rounds off its financial statements to the nearest million dollars

unless stated otherwise.

Consolidated Subsidiaries – Consolidated financial statements include all the businesses

in Australia and New Zealand. The equity method of accounting is applied for any associates.

Foreign Currency – The financial statements of ANZ are presented in Australian dollars.

Any foreign currency transactions are converted into the functional currency using the day’s

prevailing exchange rates (ANZ, 2017). Any monetary assets or liabilities that have resulted

from foreign currency are converted at spot rates as at the reporting date. Any differences in

exchange rates are reported in the income statement.

2.1.2 Recognition of Income

Interest Income – This is calculated using the effective interest method. It is based on the

income which is received by ANZ Bank from interest on its assets minus interest that is paid on

liabilities. Assets include loans and mortgages while liabilities include accounts (ANZ, 2017).

Commission and Fees – ANZ Bank’s commission and fees are calculated using the

effective interest method. Commission and fees are gained after provision of various services to

bank customers.

REQUIREMENTS OF ACCOUNTING THEORY 6

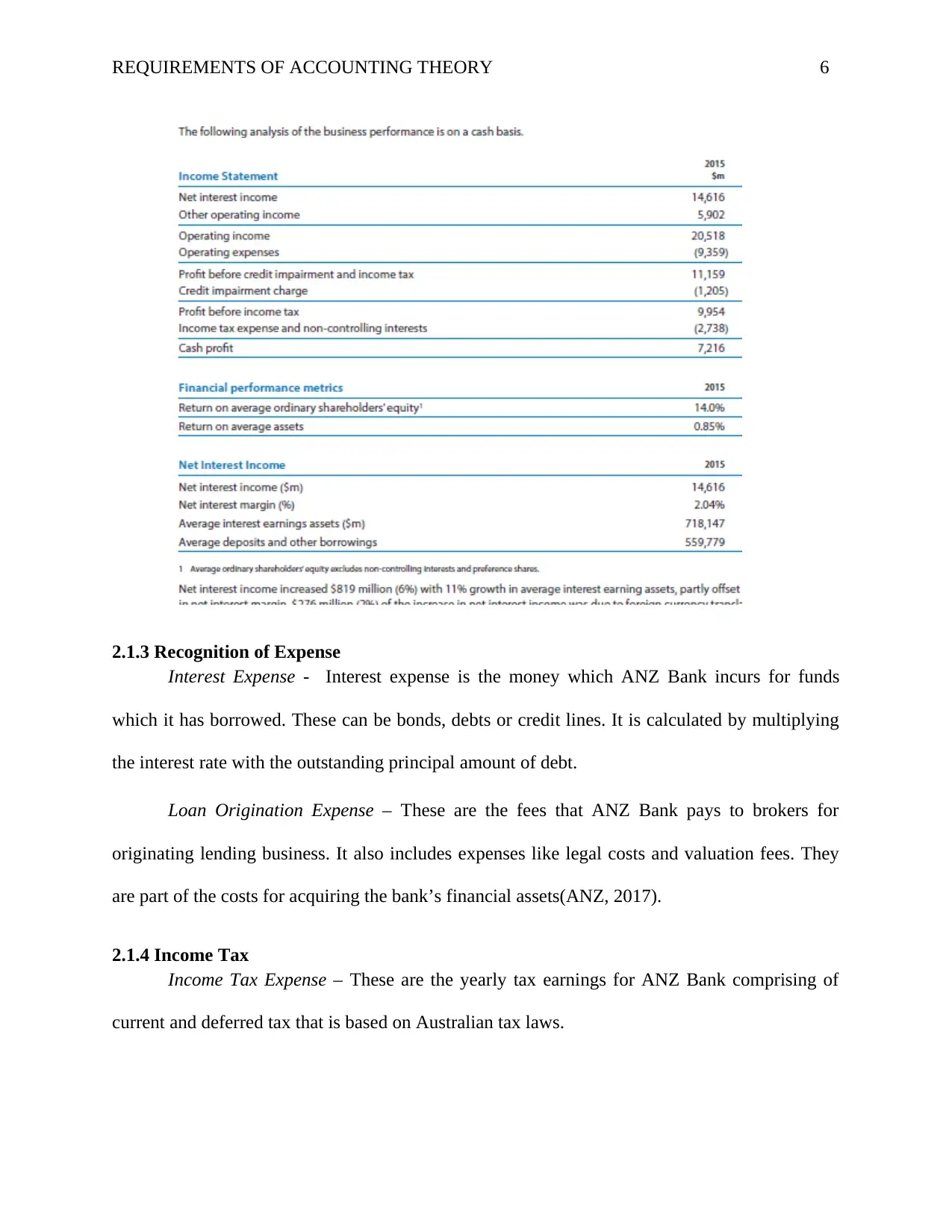

2.1.3 Recognition of Expense

Interest Expense - Interest expense is the money which ANZ Bank incurs for funds

which it has borrowed. These can be bonds, debts or credit lines. It is calculated by multiplying

the interest rate with the outstanding principal amount of debt.

Loan Origination Expense – These are the fees that ANZ Bank pays to brokers for

originating lending business. It also includes expenses like legal costs and valuation fees. They

are part of the costs for acquiring the bank’s financial assets(ANZ, 2017).

2.1.4 Income Tax

Income Tax Expense – These are the yearly tax earnings for ANZ Bank comprising of

current and deferred tax that is based on Australian tax laws.

2.1.3 Recognition of Expense

Interest Expense - Interest expense is the money which ANZ Bank incurs for funds

which it has borrowed. These can be bonds, debts or credit lines. It is calculated by multiplying

the interest rate with the outstanding principal amount of debt.

Loan Origination Expense – These are the fees that ANZ Bank pays to brokers for

originating lending business. It also includes expenses like legal costs and valuation fees. They

are part of the costs for acquiring the bank’s financial assets(ANZ, 2017).

2.1.4 Income Tax

Income Tax Expense – These are the yearly tax earnings for ANZ Bank comprising of

current and deferred tax that is based on Australian tax laws.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REQUIREMENTS OF ACCOUNTING THEORY 7

Current Tax – This is the expected tax for ANZ Bank, which is payable on the taxable

income for the year. It can either be recognised as a liability or asset.

Deferred Tax – ANZ Bank’s deferred tax is shown using the comprehensive tax balance

sheet method

Offsetting - The current and deferred tax assets of ANZ Bank are offset to the level at

which they relate to income tax imposed by Australian Taxation Authority.

2.2 Flexibilities of Accounting Policies and Estimates Used by ANZ Bank Limited

ANZ Bank continuously evaluates its estimates and judgments based on historical

experience and future events that may affect the accounting policies. With regards to credit

provisioning, the bank looks at impairment of loans at each reporting date of the financials. The

credit provisioning is estimated based on historical loss experiences by ANZ bank for its assets

which have same characteristics as the ones in the collective pool. The historical loss experience

is adjusted depending on the current data which can be observed and the events occurring in the

company.

ANZ Bank ensures that the financial instruments are measured at fair value by using

quoted market prices in the active market. If an active market lacks, ANZ bank bases the fair

value on present value estimates. The type of valuation models used by the bank include the

effect of bid/ask spread, counterparty spreads and any other factors that may influence fair value

(ANZ, 2017).Buying and selling of derivatives is used by ANZ Bank to hedge interest rate risk,

currency risk and any other exposures which the bank may face.

2.3 Accounting Policies and Estimates Used by ANZ Bank Competitors

The Competitor looked at is Westpac Bank and their accounting policies are as follows:

Current Tax – This is the expected tax for ANZ Bank, which is payable on the taxable

income for the year. It can either be recognised as a liability or asset.

Deferred Tax – ANZ Bank’s deferred tax is shown using the comprehensive tax balance

sheet method

Offsetting - The current and deferred tax assets of ANZ Bank are offset to the level at

which they relate to income tax imposed by Australian Taxation Authority.

2.2 Flexibilities of Accounting Policies and Estimates Used by ANZ Bank Limited

ANZ Bank continuously evaluates its estimates and judgments based on historical

experience and future events that may affect the accounting policies. With regards to credit

provisioning, the bank looks at impairment of loans at each reporting date of the financials. The

credit provisioning is estimated based on historical loss experiences by ANZ bank for its assets

which have same characteristics as the ones in the collective pool. The historical loss experience

is adjusted depending on the current data which can be observed and the events occurring in the

company.

ANZ Bank ensures that the financial instruments are measured at fair value by using

quoted market prices in the active market. If an active market lacks, ANZ bank bases the fair

value on present value estimates. The type of valuation models used by the bank include the

effect of bid/ask spread, counterparty spreads and any other factors that may influence fair value

(ANZ, 2017).Buying and selling of derivatives is used by ANZ Bank to hedge interest rate risk,

currency risk and any other exposures which the bank may face.

2.3 Accounting Policies and Estimates Used by ANZ Bank Competitors

The Competitor looked at is Westpac Bank and their accounting policies are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REQUIREMENTS OF ACCOUNTING THEORY 8

The financial statements for Westpac are prepared in accordance to the Reserve Bank Act

and Overseas

Judgements, estimates and assumptions are used in the preparation of Westpac’s

accounting statements

Funding valuation adjustment is used in the fair value of derivatives by Westpac

They have a disclosure statement for the year ended September 2014 which is used in

providing guidance to application of offsetting criteria

The financial statements are authorised by board of directors before disclosure

The financial statements are prepared based on principles of historical cost accounting

2.4 If Policies and Estimates are Acceptable

The policies and statements which can be used by ANZ Bank Limited are acceptable

as they are understandable. The information which is given in the company’s annual

statements is well presented and therefore understandable to users. A lot of additional

information is provided in the annual statements and this shoes transparency (Otley, 2016).

The policies and estimates are relevant. The information given in the annual reports

of ANZ bank influences the economic decisions of various stakeholders. All the financials

are presented in the annual report and stakeholders can make decisions based on this on

which strategic direction to take, which areas to improve and what assets the bank can

invest in.

The policies and estimates are also acceptable because they are reliable. The

information presented in ANZ Bank’s financial statements 2015 and 2016 is free of material

The financial statements for Westpac are prepared in accordance to the Reserve Bank Act

and Overseas

Judgements, estimates and assumptions are used in the preparation of Westpac’s

accounting statements

Funding valuation adjustment is used in the fair value of derivatives by Westpac

They have a disclosure statement for the year ended September 2014 which is used in

providing guidance to application of offsetting criteria

The financial statements are authorised by board of directors before disclosure

The financial statements are prepared based on principles of historical cost accounting

2.4 If Policies and Estimates are Acceptable

The policies and statements which can be used by ANZ Bank Limited are acceptable

as they are understandable. The information which is given in the company’s annual

statements is well presented and therefore understandable to users. A lot of additional

information is provided in the annual statements and this shoes transparency (Otley, 2016).

The policies and estimates are relevant. The information given in the annual reports

of ANZ bank influences the economic decisions of various stakeholders. All the financials

are presented in the annual report and stakeholders can make decisions based on this on

which strategic direction to take, which areas to improve and what assets the bank can

invest in.

The policies and estimates are also acceptable because they are reliable. The

information presented in ANZ Bank’s financial statements 2015 and 2016 is free of material

REQUIREMENTS OF ACCOUNTING THEORY 9

error and bias and is not misleading. The information given represents all the financial

events that have taken place in ANZ Bank. The policies and estimates are comparable in

terms of different years and accounting periods hence stakeholders are able to identify

performance trends (Otley, 2016). This can help ANZ Bank know whether it is on the right

strategic path and where the company may be hurting.

2.5 Is Accounting Strategy Hiding or Revealing

The accounting strategy used by ANZ Bank is revealing. This is due to the fact that the

financial statements are comprehensive. The annual statements of ANZ bank contain different

financial reports which give a comprehensive picture of the bank’s status (ANZ, 2016). The

statements are a true reflection of ANZ Bank’s financial activities and give comprehensive

details of how the bank used its finances.

The accounting strategy is relevant and timely. The financial statements are produced in a

timely manner and are relevant to the business. They are also relevant to the stakeholders as they

show the bank’s true financial position. They are produced annually as required by bank

regulation laws.

The accounting strategy is reliable. The bank has made the annual reports public and

easily available to anyone who may want to access them (ANZ, 2016). The bank has provided a

link in their portal where annual reports since 1969 can be found, hence showing that the strategy

used is a revealing one. Stakeholders and shareholders can therefore access this information and

make informed decisions about the position of the bank and how to make their investments.

error and bias and is not misleading. The information given represents all the financial

events that have taken place in ANZ Bank. The policies and estimates are comparable in

terms of different years and accounting periods hence stakeholders are able to identify

performance trends (Otley, 2016). This can help ANZ Bank know whether it is on the right

strategic path and where the company may be hurting.

2.5 Is Accounting Strategy Hiding or Revealing

The accounting strategy used by ANZ Bank is revealing. This is due to the fact that the

financial statements are comprehensive. The annual statements of ANZ bank contain different

financial reports which give a comprehensive picture of the bank’s status (ANZ, 2016). The

statements are a true reflection of ANZ Bank’s financial activities and give comprehensive

details of how the bank used its finances.

The accounting strategy is relevant and timely. The financial statements are produced in a

timely manner and are relevant to the business. They are also relevant to the stakeholders as they

show the bank’s true financial position. They are produced annually as required by bank

regulation laws.

The accounting strategy is reliable. The bank has made the annual reports public and

easily available to anyone who may want to access them (ANZ, 2016). The bank has provided a

link in their portal where annual reports since 1969 can be found, hence showing that the strategy

used is a revealing one. Stakeholders and shareholders can therefore access this information and

make informed decisions about the position of the bank and how to make their investments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REQUIREMENTS OF ACCOUNTING THEORY 10

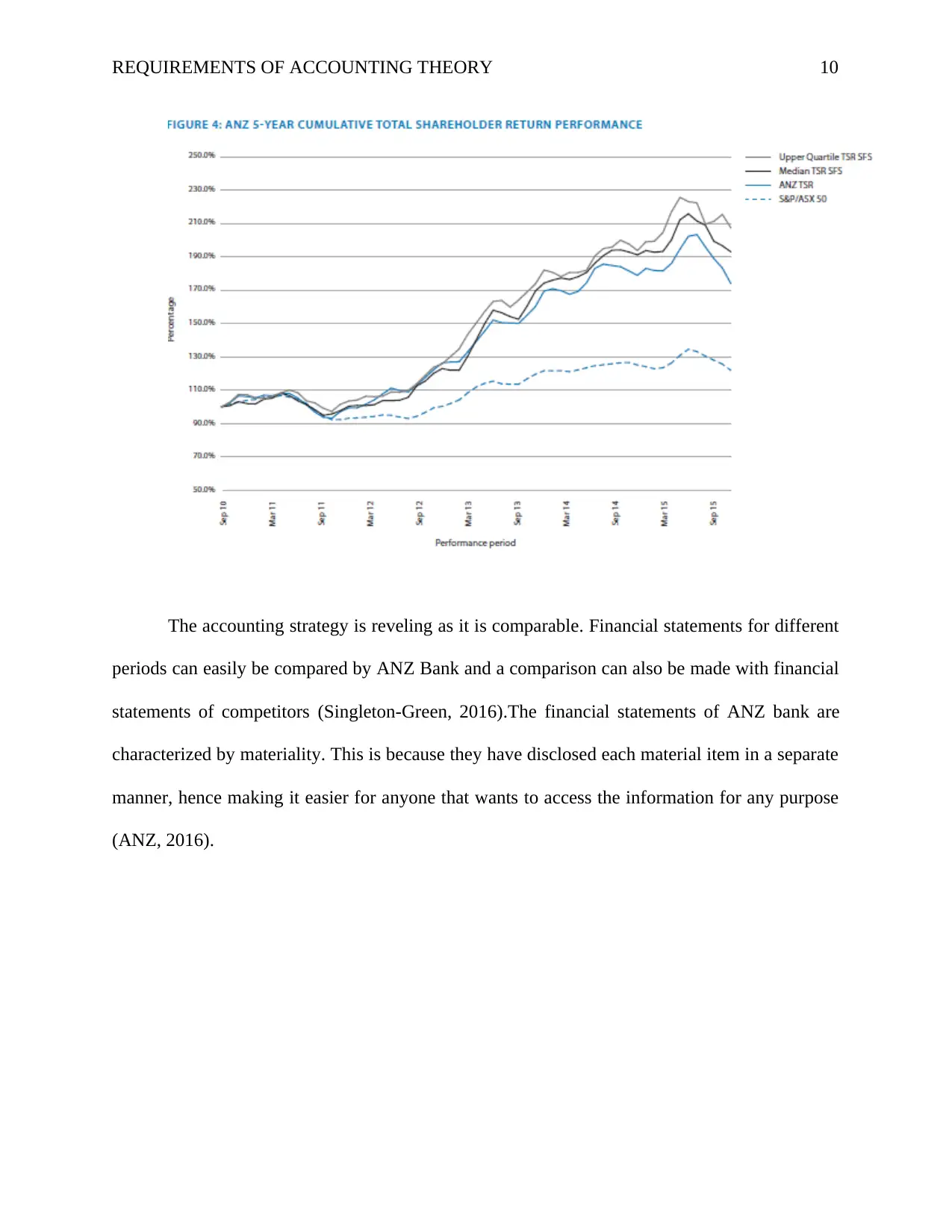

The accounting strategy is reveling as it is comparable. Financial statements for different

periods can easily be compared by ANZ Bank and a comparison can also be made with financial

statements of competitors (Singleton-Green, 2016).The financial statements of ANZ bank are

characterized by materiality. This is because they have disclosed each material item in a separate

manner, hence making it easier for anyone that wants to access the information for any purpose

(ANZ, 2016).

The accounting strategy is reveling as it is comparable. Financial statements for different

periods can easily be compared by ANZ Bank and a comparison can also be made with financial

statements of competitors (Singleton-Green, 2016).The financial statements of ANZ bank are

characterized by materiality. This is because they have disclosed each material item in a separate

manner, hence making it easier for anyone that wants to access the information for any purpose

(ANZ, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REQUIREMENTS OF ACCOUNTING THEORY 11

2.6 Red Flags in Accounting Report

The annual statements of ANZ Bank Limited do not show any red flags.

2.7 Which Accounting Positions Capture them and Why?

If there were any red flags, they would be captured by high discrepancies in the financial

statements of the company and high losses in some areas. In this case, there are no red flags

hence no accounting position captures anything.

3.0 Evaluation of Accounting Policy

3.1 Political pressures that affect the accounting standard-setting environment

The account reporting standards setting is considered to be a political process. This is

because it can have a great effect on ANZ Bank. Changes in Australian account standards or

introduction of any new standards can lead to redistribution of wealth in an economy.

Accounting bodies have complex roles in setting accounting standards. Accounting

principles which are sound provide important guidance in determining correct ways of reporting

accounting transactions. Accounting bodies must however look at economic consequences that

are brought about by changes in accounting standards.

2.6 Red Flags in Accounting Report

The annual statements of ANZ Bank Limited do not show any red flags.

2.7 Which Accounting Positions Capture them and Why?

If there were any red flags, they would be captured by high discrepancies in the financial

statements of the company and high losses in some areas. In this case, there are no red flags

hence no accounting position captures anything.

3.0 Evaluation of Accounting Policy

3.1 Political pressures that affect the accounting standard-setting environment

The account reporting standards setting is considered to be a political process. This is

because it can have a great effect on ANZ Bank. Changes in Australian account standards or

introduction of any new standards can lead to redistribution of wealth in an economy.

Accounting bodies have complex roles in setting accounting standards. Accounting

principles which are sound provide important guidance in determining correct ways of reporting

accounting transactions. Accounting bodies must however look at economic consequences that

are brought about by changes in accounting standards.

REQUIREMENTS OF ACCOUNTING THEORY 12

Political influence can affect ANZ bank as it can affect the outcome of an accounting

process and therefore increase or decrease the bank’s wealth.

Australian accounting regulators are direct political appointments who can make different

decisions which affect wealth allocation between ANZ Bank and its customers. ANZ Bank will

therefore feel that they have undue political pressure if the effect is negative to the bank

(Singleton-Green, 2016).

Political forces in accounting reflect changes in economic, legal and institutional

environments and can assist accounting standards to be moved to the market equilibrium.

Another pressure that ANZ Bank may feel is when special interest groups seek to affect

accounting rules for self-interest hence making them be inefficient.

Political pressure may also be felt when the bank is forced to make adjustments which

may not be proper for the benefit of the selfish gains of few people. This may lead to incorrect

reporting which can negatively affect the bank. Investors may come in and invest in the bank yet

they have used wrong positions in determining the profitability of the bank and also its growth.

3.2 Implications of organizations making accounting disclosures

By ANZ Bank making accounting disclosures it can benefit from new corporate cash.

They can sell stock so that they raise cash and this can only be done successfully if the company

discloses its finances. Through this ANZ Bank will not have to worry about paying back interest

on any loan.

Making disclosures will assist in owner diversification as the owners can diversify their

investments. This is because they will be able to know the true financial position of the

company.ANZ Bank can grow its portfolio further. ANZ Bank will also benefit from increased

Political influence can affect ANZ bank as it can affect the outcome of an accounting

process and therefore increase or decrease the bank’s wealth.

Australian accounting regulators are direct political appointments who can make different

decisions which affect wealth allocation between ANZ Bank and its customers. ANZ Bank will

therefore feel that they have undue political pressure if the effect is negative to the bank

(Singleton-Green, 2016).

Political forces in accounting reflect changes in economic, legal and institutional

environments and can assist accounting standards to be moved to the market equilibrium.

Another pressure that ANZ Bank may feel is when special interest groups seek to affect

accounting rules for self-interest hence making them be inefficient.

Political pressure may also be felt when the bank is forced to make adjustments which

may not be proper for the benefit of the selfish gains of few people. This may lead to incorrect

reporting which can negatively affect the bank. Investors may come in and invest in the bank yet

they have used wrong positions in determining the profitability of the bank and also its growth.

3.2 Implications of organizations making accounting disclosures

By ANZ Bank making accounting disclosures it can benefit from new corporate cash.

They can sell stock so that they raise cash and this can only be done successfully if the company

discloses its finances. Through this ANZ Bank will not have to worry about paying back interest

on any loan.

Making disclosures will assist in owner diversification as the owners can diversify their

investments. This is because they will be able to know the true financial position of the

company.ANZ Bank can grow its portfolio further. ANZ Bank will also benefit from increased

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.