Quantitative Analysis: Forecasting Future Returns of ANZ Bank Stock

VerifiedAdded on 2023/06/10

|9

|1537

|395

Report

AI Summary

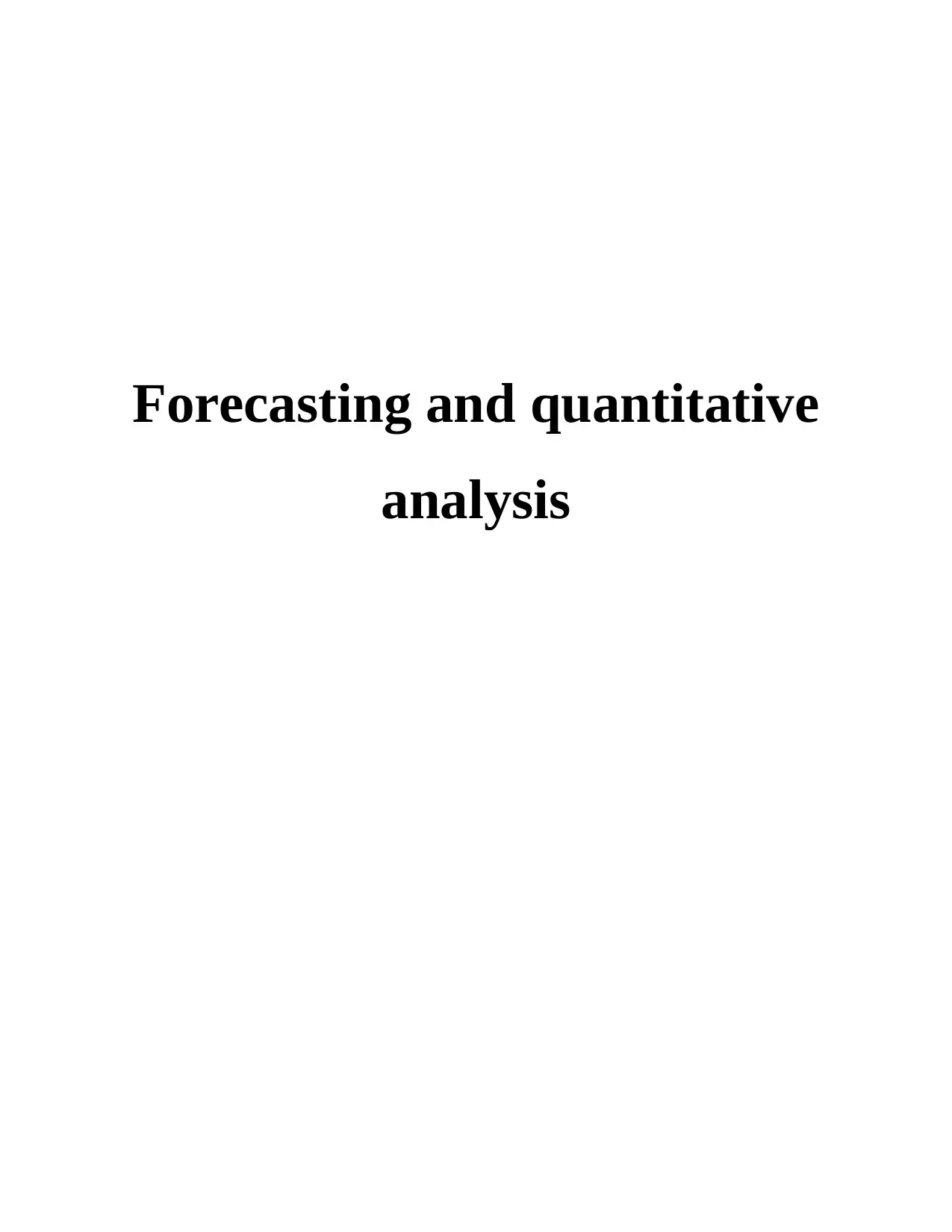

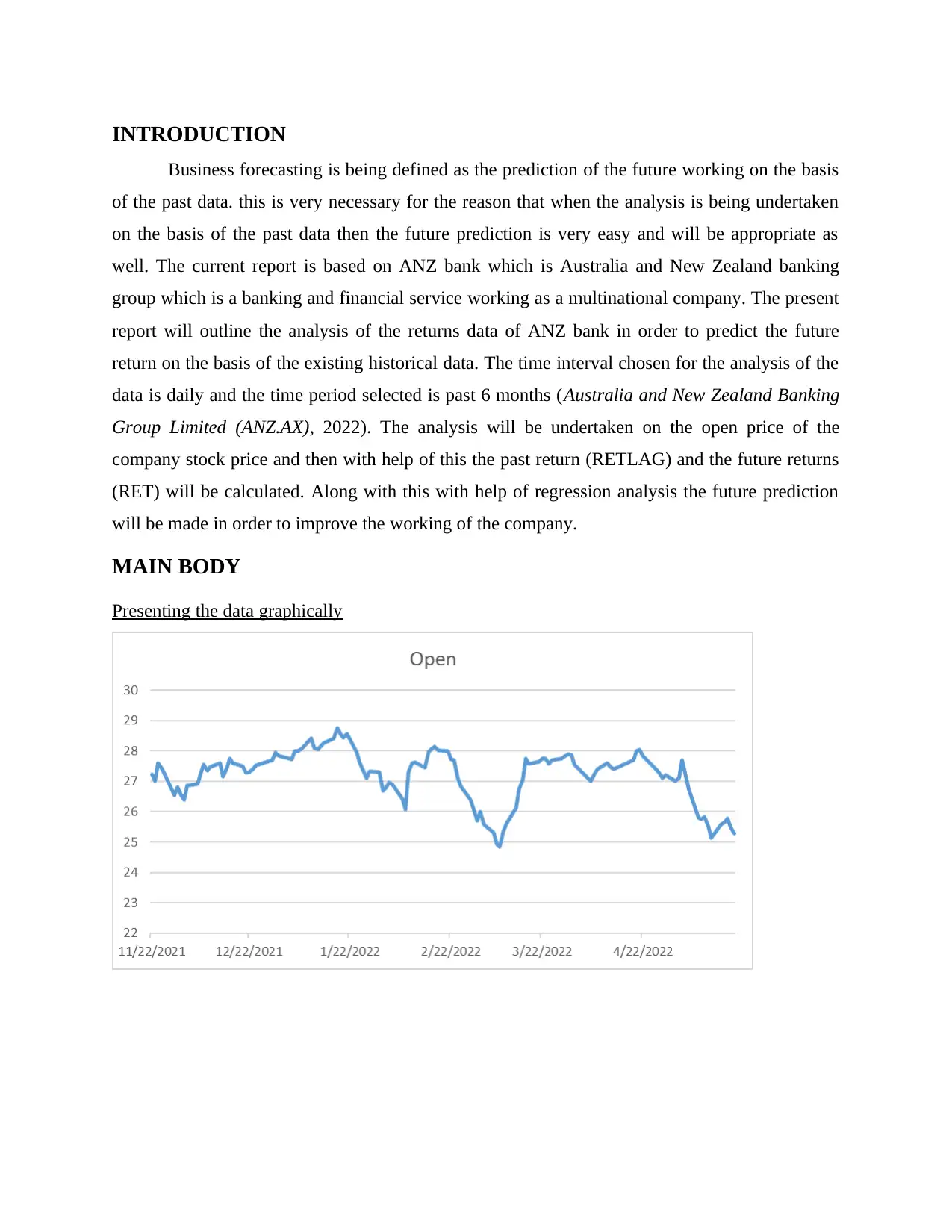

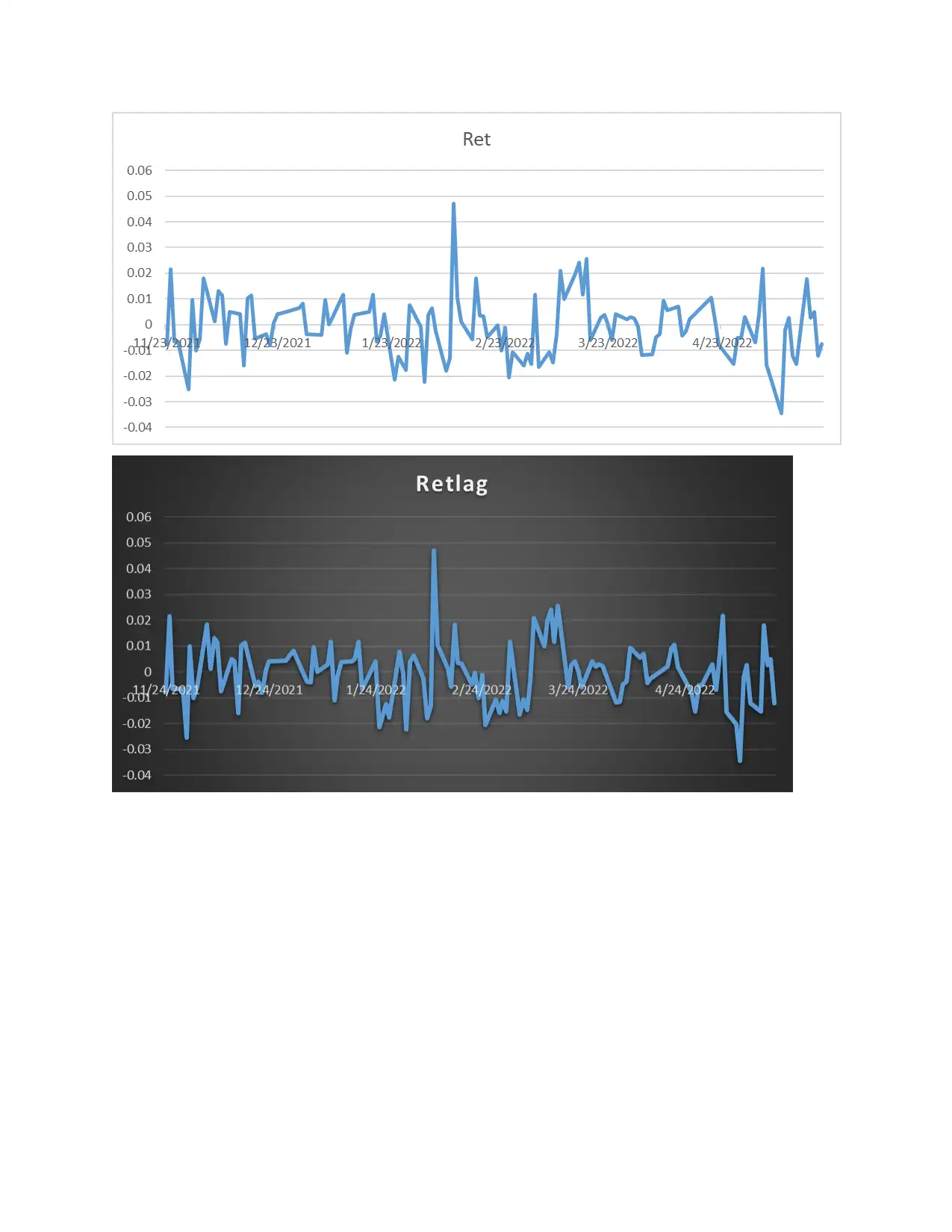

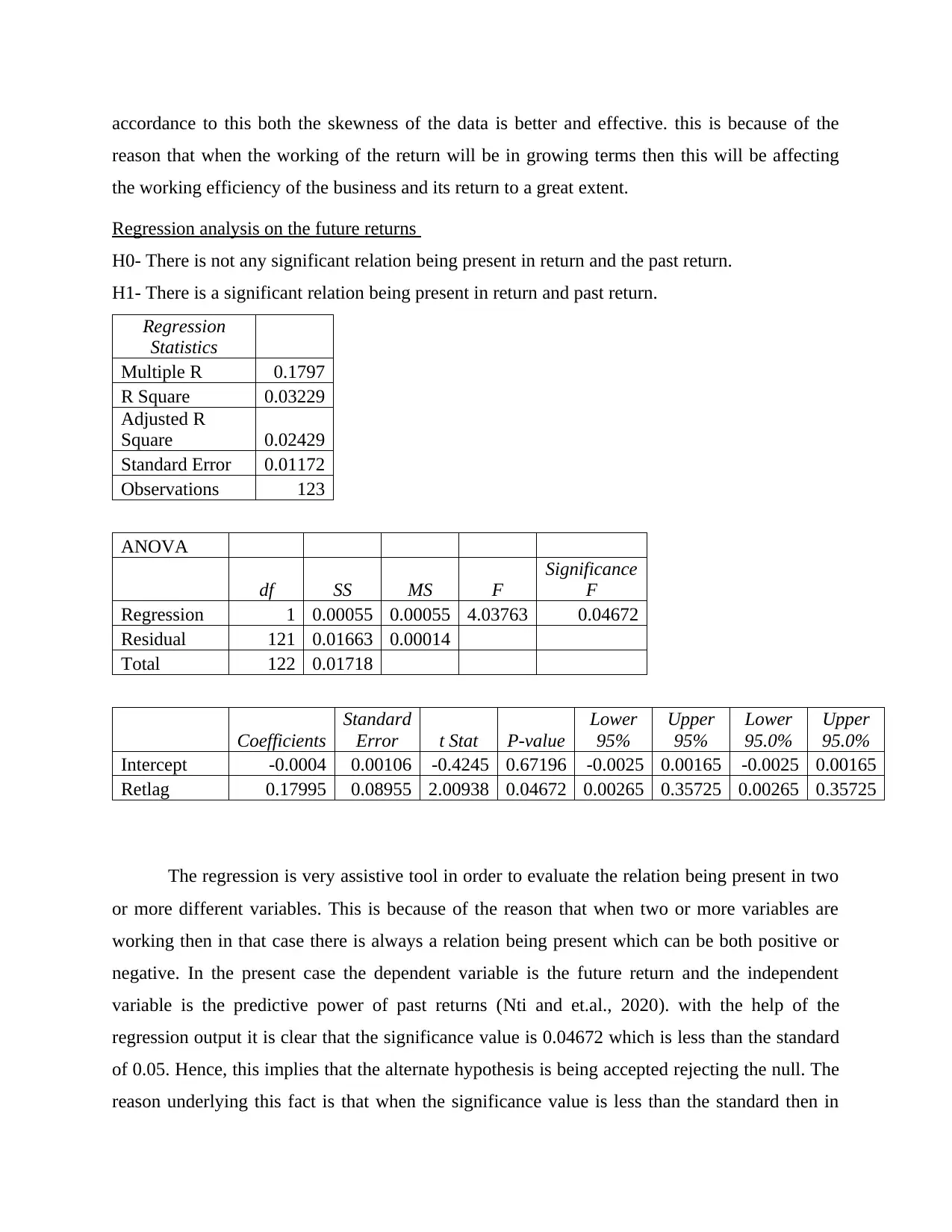

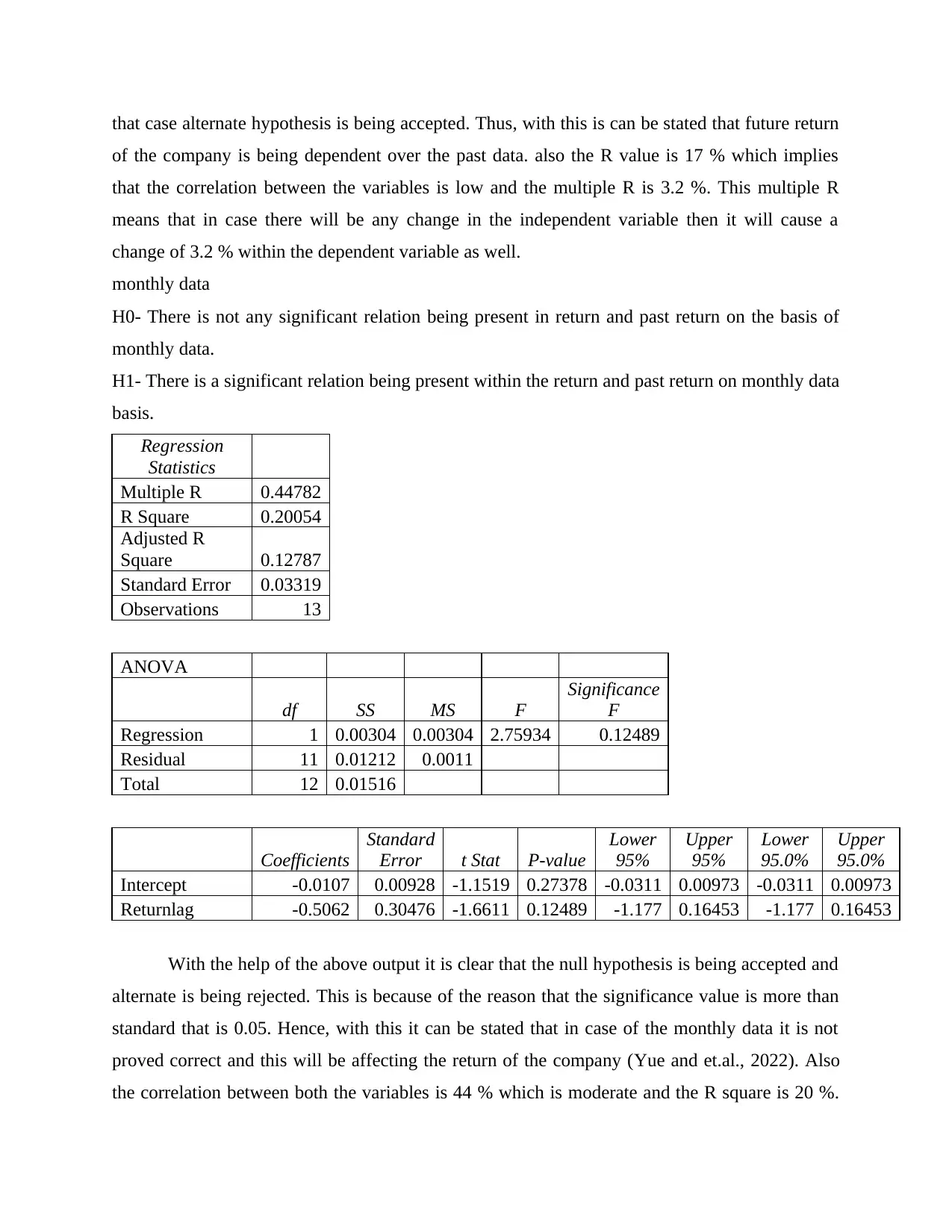

This report provides a quantitative analysis of ANZ Bank's stock returns, focusing on forecasting future performance based on historical data. Utilizing daily stock price data over the past six months, the analysis includes graphical data presentation, descriptive statistics calculation, and regression analysis. The descriptive statistics reveal average daily and monthly returns, standard deviation, and skewness, while the regression analysis assesses the relationship between past and future returns. The findings suggest a significant relationship between past and future returns based on daily data, but not on monthly data. The report concludes with recommendations for ANZ Bank, emphasizing the importance of employing diverse forecasting techniques and analyzing competitor data to enhance working efficiency and returns. This student-contributed document is available on Desklib.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.