Financial Management Assignment: Share Issuance and Capital Budgeting

VerifiedAdded on 2022/09/28

|18

|3619

|22

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Financial Management assignment, addressing two key questions. The first question focuses on share issuance, analyzing three options with different price rates and calculating the theoretical ex-rights fair value per share and expected EPS. It evaluates the best option for the company, recommending the most beneficial share issuance strategy. The second question delves into capital budgeting, utilizing tools such as ARR, IRR, NPV, and payback period to evaluate the economic feasibility of a machine investment. It provides detailed calculations, discusses the machine's economic viability, and explores the benefits and limitations of various investment appraisal techniques, including NPV and IRR. The assignment offers a practical application of financial concepts and decision-making processes.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 1

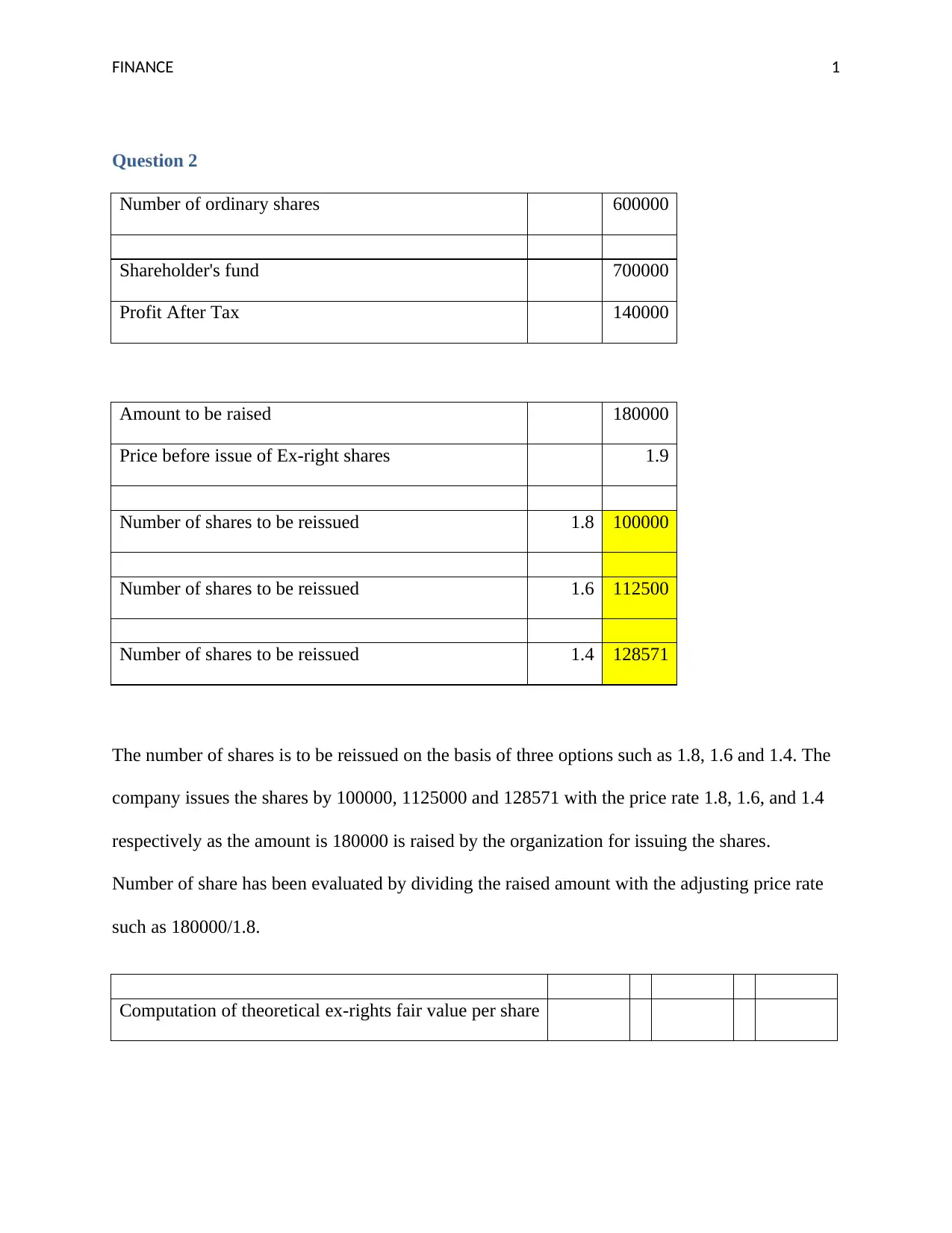

Question 2

Number of ordinary shares 600000

Shareholder's fund 700000

Profit After Tax 140000

Amount to be raised 180000

Price before issue of Ex-right shares 1.9

Number of shares to be reissued 1.8 100000

Number of shares to be reissued 1.6 112500

Number of shares to be reissued 1.4 128571

The number of shares is to be reissued on the basis of three options such as 1.8, 1.6 and 1.4. The

company issues the shares by 100000, 1125000 and 128571 with the price rate 1.8, 1.6, and 1.4

respectively as the amount is 180000 is raised by the organization for issuing the shares.

Number of share has been evaluated by dividing the raised amount with the adjusting price rate

such as 180000/1.8.

Computation of theoretical ex-rights fair value per share

Question 2

Number of ordinary shares 600000

Shareholder's fund 700000

Profit After Tax 140000

Amount to be raised 180000

Price before issue of Ex-right shares 1.9

Number of shares to be reissued 1.8 100000

Number of shares to be reissued 1.6 112500

Number of shares to be reissued 1.4 128571

The number of shares is to be reissued on the basis of three options such as 1.8, 1.6 and 1.4. The

company issues the shares by 100000, 1125000 and 128571 with the price rate 1.8, 1.6, and 1.4

respectively as the amount is 180000 is raised by the organization for issuing the shares.

Number of share has been evaluated by dividing the raised amount with the adjusting price rate

such as 180000/1.8.

Computation of theoretical ex-rights fair value per share

FINANCE 2

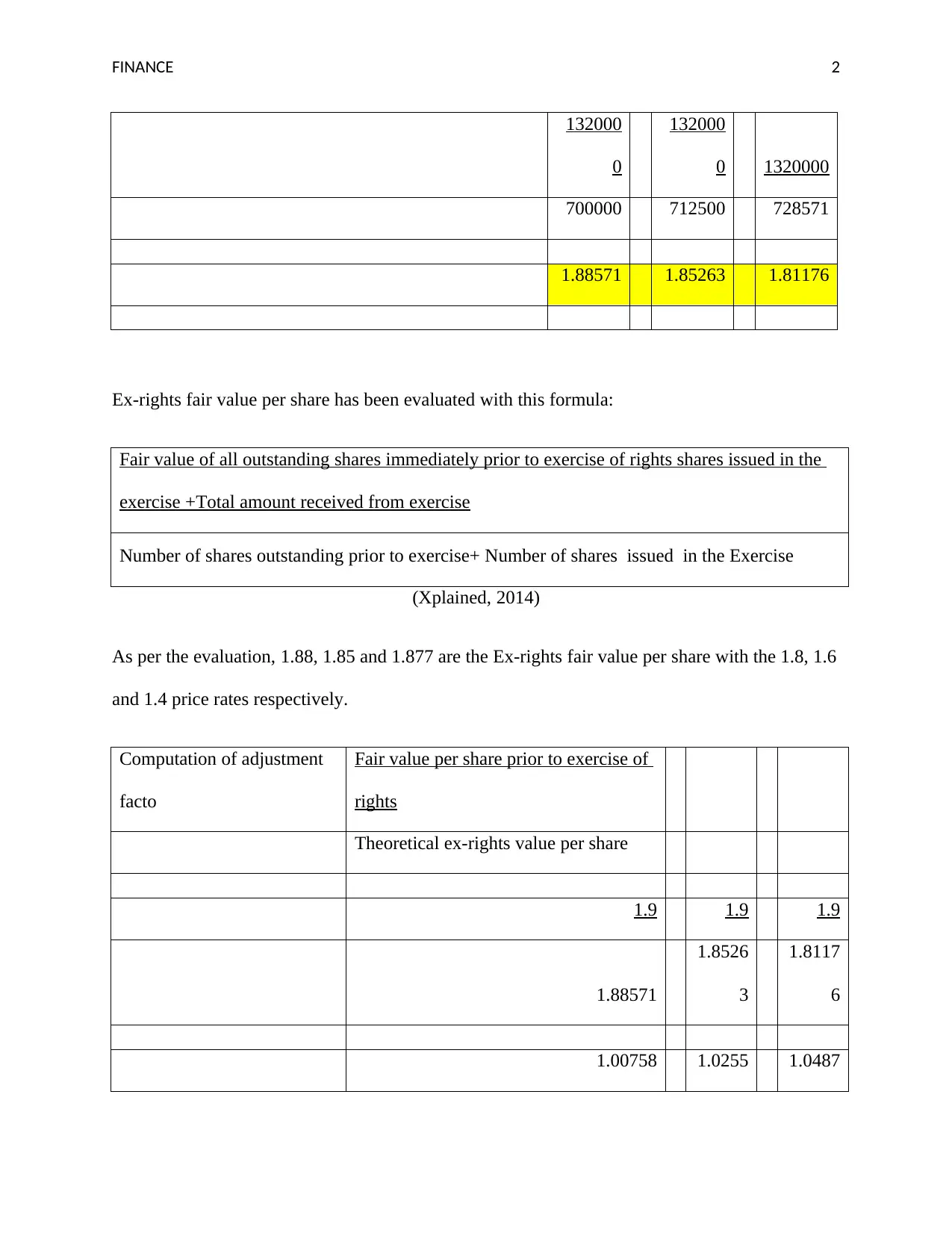

132000

0

132000

0 1320000

700000 712500 728571

1.88571 1.85263 1.81176

Ex-rights fair value per share has been evaluated with this formula:

Fair value of all outstanding shares immediately prior to exercise of rights shares issued in the

exercise +Total amount received from exercise

Number of shares outstanding prior to exercise+ Number of shares issued in the Exercise

(Xplained, 2014)

As per the evaluation, 1.88, 1.85 and 1.877 are the Ex-rights fair value per share with the 1.8, 1.6

and 1.4 price rates respectively.

Computation of adjustment

facto

Fair value per share prior to exercise of

rights

Theoretical ex-rights value per share

1.9 1.9 1.9

1.88571

1.8526

3

1.8117

6

1.00758 1.0255 1.0487

132000

0

132000

0 1320000

700000 712500 728571

1.88571 1.85263 1.81176

Ex-rights fair value per share has been evaluated with this formula:

Fair value of all outstanding shares immediately prior to exercise of rights shares issued in the

exercise +Total amount received from exercise

Number of shares outstanding prior to exercise+ Number of shares issued in the Exercise

(Xplained, 2014)

As per the evaluation, 1.88, 1.85 and 1.877 are the Ex-rights fair value per share with the 1.8, 1.6

and 1.4 price rates respectively.

Computation of adjustment

facto

Fair value per share prior to exercise of

rights

Theoretical ex-rights value per share

1.9 1.9 1.9

1.88571

1.8526

3

1.8117

6

1.00758 1.0255 1.0487

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 3

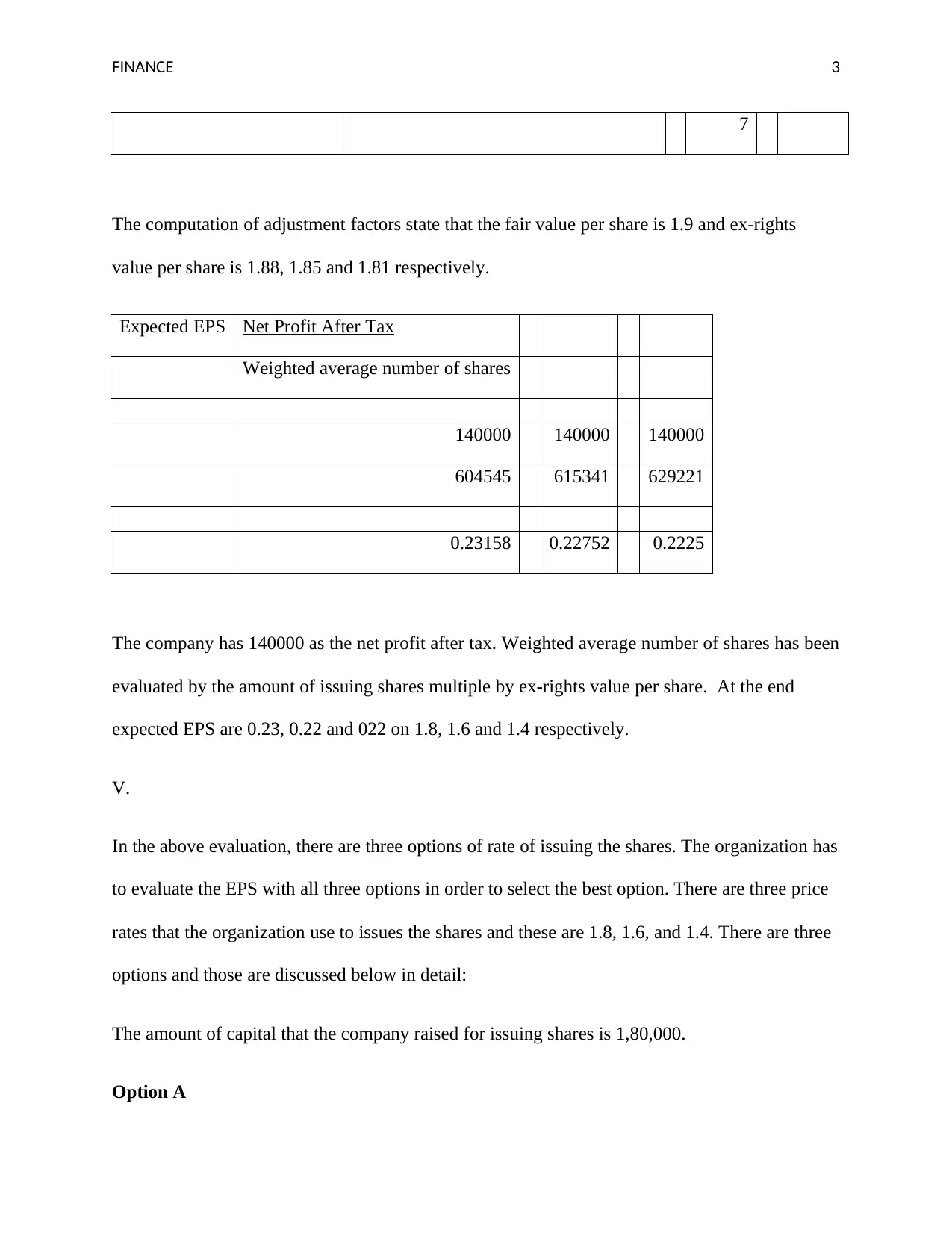

7

The computation of adjustment factors state that the fair value per share is 1.9 and ex-rights

value per share is 1.88, 1.85 and 1.81 respectively.

Expected EPS Net Profit After Tax

Weighted average number of shares

140000 140000 140000

604545 615341 629221

0.23158 0.22752 0.2225

The company has 140000 as the net profit after tax. Weighted average number of shares has been

evaluated by the amount of issuing shares multiple by ex-rights value per share. At the end

expected EPS are 0.23, 0.22 and 022 on 1.8, 1.6 and 1.4 respectively.

V.

In the above evaluation, there are three options of rate of issuing the shares. The organization has

to evaluate the EPS with all three options in order to select the best option. There are three price

rates that the organization use to issues the shares and these are 1.8, 1.6, and 1.4. There are three

options and those are discussed below in detail:

The amount of capital that the company raised for issuing shares is 1,80,000.

Option A

7

The computation of adjustment factors state that the fair value per share is 1.9 and ex-rights

value per share is 1.88, 1.85 and 1.81 respectively.

Expected EPS Net Profit After Tax

Weighted average number of shares

140000 140000 140000

604545 615341 629221

0.23158 0.22752 0.2225

The company has 140000 as the net profit after tax. Weighted average number of shares has been

evaluated by the amount of issuing shares multiple by ex-rights value per share. At the end

expected EPS are 0.23, 0.22 and 022 on 1.8, 1.6 and 1.4 respectively.

V.

In the above evaluation, there are three options of rate of issuing the shares. The organization has

to evaluate the EPS with all three options in order to select the best option. There are three price

rates that the organization use to issues the shares and these are 1.8, 1.6, and 1.4. There are three

options and those are discussed below in detail:

The amount of capital that the company raised for issuing shares is 1,80,000.

Option A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 4

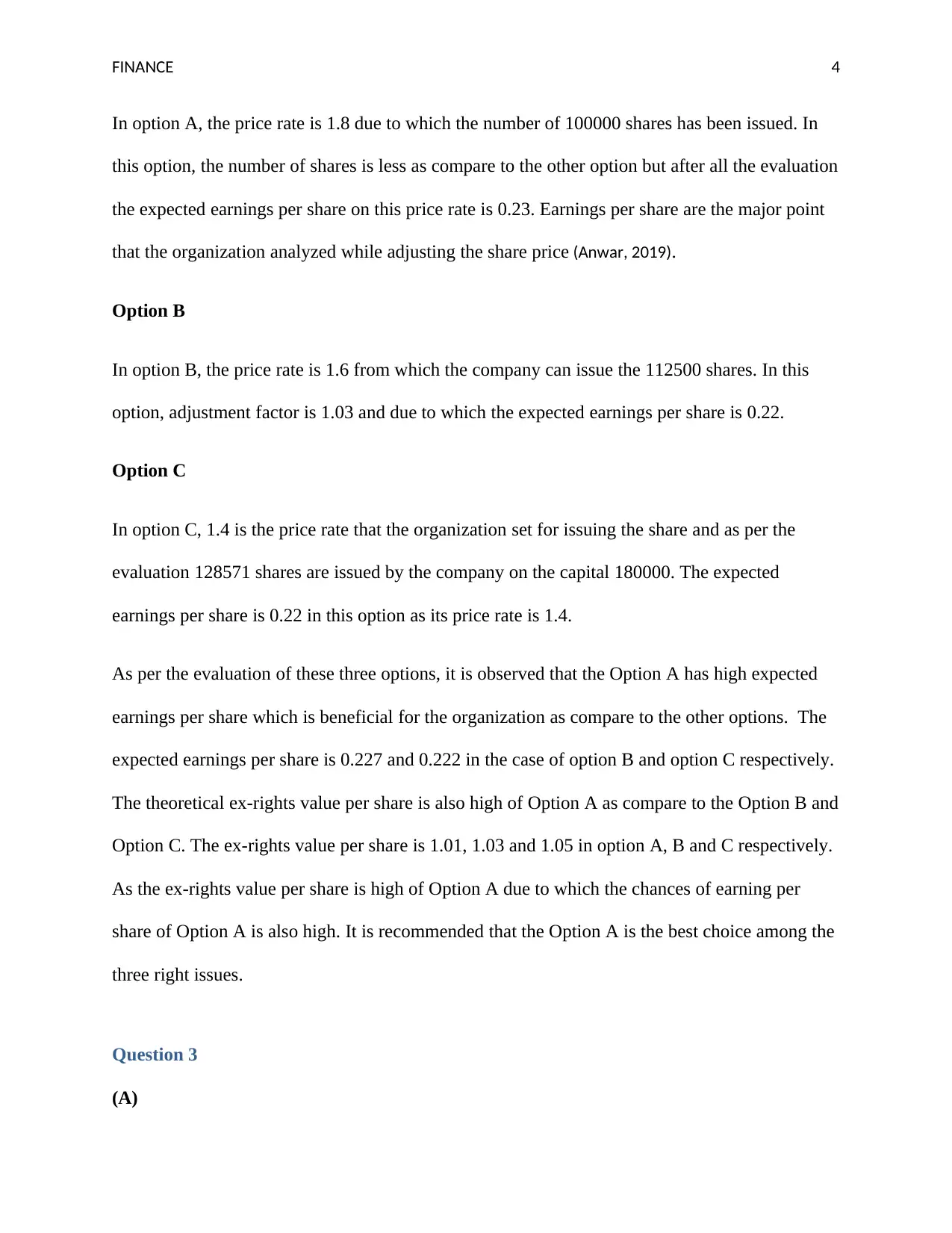

In option A, the price rate is 1.8 due to which the number of 100000 shares has been issued. In

this option, the number of shares is less as compare to the other option but after all the evaluation

the expected earnings per share on this price rate is 0.23. Earnings per share are the major point

that the organization analyzed while adjusting the share price (Anwar, 2019).

Option B

In option B, the price rate is 1.6 from which the company can issue the 112500 shares. In this

option, adjustment factor is 1.03 and due to which the expected earnings per share is 0.22.

Option C

In option C, 1.4 is the price rate that the organization set for issuing the share and as per the

evaluation 128571 shares are issued by the company on the capital 180000. The expected

earnings per share is 0.22 in this option as its price rate is 1.4.

As per the evaluation of these three options, it is observed that the Option A has high expected

earnings per share which is beneficial for the organization as compare to the other options. The

expected earnings per share is 0.227 and 0.222 in the case of option B and option C respectively.

The theoretical ex-rights value per share is also high of Option A as compare to the Option B and

Option C. The ex-rights value per share is 1.01, 1.03 and 1.05 in option A, B and C respectively.

As the ex-rights value per share is high of Option A due to which the chances of earning per

share of Option A is also high. It is recommended that the Option A is the best choice among the

three right issues.

Question 3

(A)

In option A, the price rate is 1.8 due to which the number of 100000 shares has been issued. In

this option, the number of shares is less as compare to the other option but after all the evaluation

the expected earnings per share on this price rate is 0.23. Earnings per share are the major point

that the organization analyzed while adjusting the share price (Anwar, 2019).

Option B

In option B, the price rate is 1.6 from which the company can issue the 112500 shares. In this

option, adjustment factor is 1.03 and due to which the expected earnings per share is 0.22.

Option C

In option C, 1.4 is the price rate that the organization set for issuing the share and as per the

evaluation 128571 shares are issued by the company on the capital 180000. The expected

earnings per share is 0.22 in this option as its price rate is 1.4.

As per the evaluation of these three options, it is observed that the Option A has high expected

earnings per share which is beneficial for the organization as compare to the other options. The

expected earnings per share is 0.227 and 0.222 in the case of option B and option C respectively.

The theoretical ex-rights value per share is also high of Option A as compare to the Option B and

Option C. The ex-rights value per share is 1.01, 1.03 and 1.05 in option A, B and C respectively.

As the ex-rights value per share is high of Option A due to which the chances of earning per

share of Option A is also high. It is recommended that the Option A is the best choice among the

three right issues.

Question 3

(A)

FINANCE 5

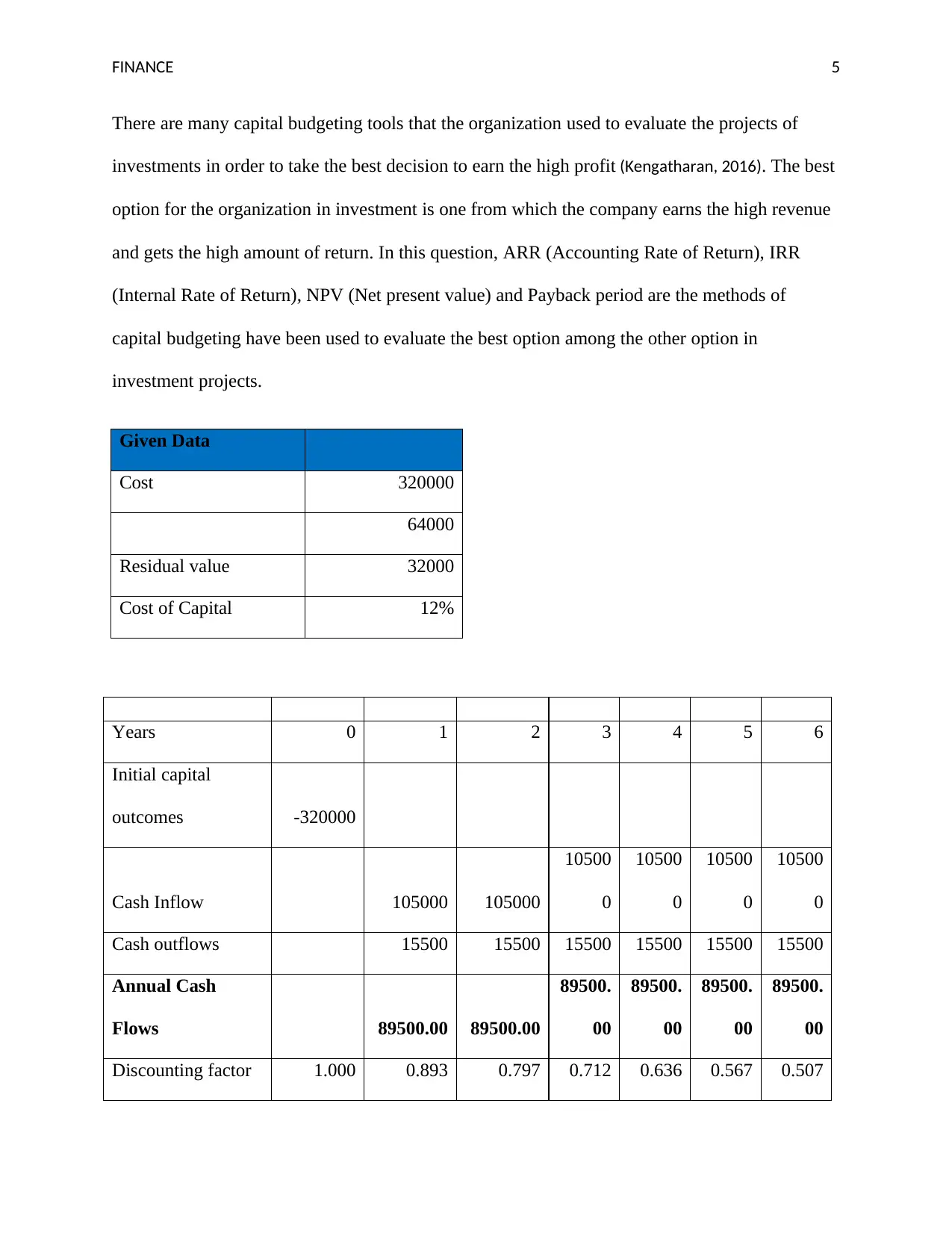

There are many capital budgeting tools that the organization used to evaluate the projects of

investments in order to take the best decision to earn the high profit (Kengatharan, 2016). The best

option for the organization in investment is one from which the company earns the high revenue

and gets the high amount of return. In this question, ARR (Accounting Rate of Return), IRR

(Internal Rate of Return), NPV (Net present value) and Payback period are the methods of

capital budgeting have been used to evaluate the best option among the other option in

investment projects.

Given Data

Cost 320000

64000

Residual value 32000

Cost of Capital 12%

Years 0 1 2 3 4 5 6

Initial capital

outcomes -320000

Cash Inflow 105000 105000

10500

0

10500

0

10500

0

10500

0

Cash outflows 15500 15500 15500 15500 15500 15500

Annual Cash

Flows 89500.00 89500.00

89500.

00

89500.

00

89500.

00

89500.

00

Discounting factor 1.000 0.893 0.797 0.712 0.636 0.567 0.507

There are many capital budgeting tools that the organization used to evaluate the projects of

investments in order to take the best decision to earn the high profit (Kengatharan, 2016). The best

option for the organization in investment is one from which the company earns the high revenue

and gets the high amount of return. In this question, ARR (Accounting Rate of Return), IRR

(Internal Rate of Return), NPV (Net present value) and Payback period are the methods of

capital budgeting have been used to evaluate the best option among the other option in

investment projects.

Given Data

Cost 320000

64000

Residual value 32000

Cost of Capital 12%

Years 0 1 2 3 4 5 6

Initial capital

outcomes -320000

Cash Inflow 105000 105000

10500

0

10500

0

10500

0

10500

0

Cash outflows 15500 15500 15500 15500 15500 15500

Annual Cash

Flows 89500.00 89500.00

89500.

00

89500.

00

89500.

00

89500.

00

Discounting factor 1.000 0.893 0.797 0.712 0.636 0.567 0.507

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 6

@12%

Present Cash Flows -320000

79910.71

429

71348.85

204

63704.

33

56878.

87

50784.

7

45343.

49

Net present Value

47970.95

546

IRR 5%

Payback Period

Years 0 1 2 3 4 5

Cash Inflow

-

320000 89500.00 89500.00 89500.00

89500.0

0 89500.00

Cumulative cash inflow

-

320000 -230500 -141000 -51500 38000 127500

Payback Period 3.58

Average Revenue 89500.00

Average Investment 320000

ARR Average Revenue

Average

Investment

ARR 89500.00

@12%

Present Cash Flows -320000

79910.71

429

71348.85

204

63704.

33

56878.

87

50784.

7

45343.

49

Net present Value

47970.95

546

IRR 5%

Payback Period

Years 0 1 2 3 4 5

Cash Inflow

-

320000 89500.00 89500.00 89500.00

89500.0

0 89500.00

Cumulative cash inflow

-

320000 -230500 -141000 -51500 38000 127500

Payback Period 3.58

Average Revenue 89500.00

Average Investment 320000

ARR Average Revenue

Average

Investment

ARR 89500.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 7

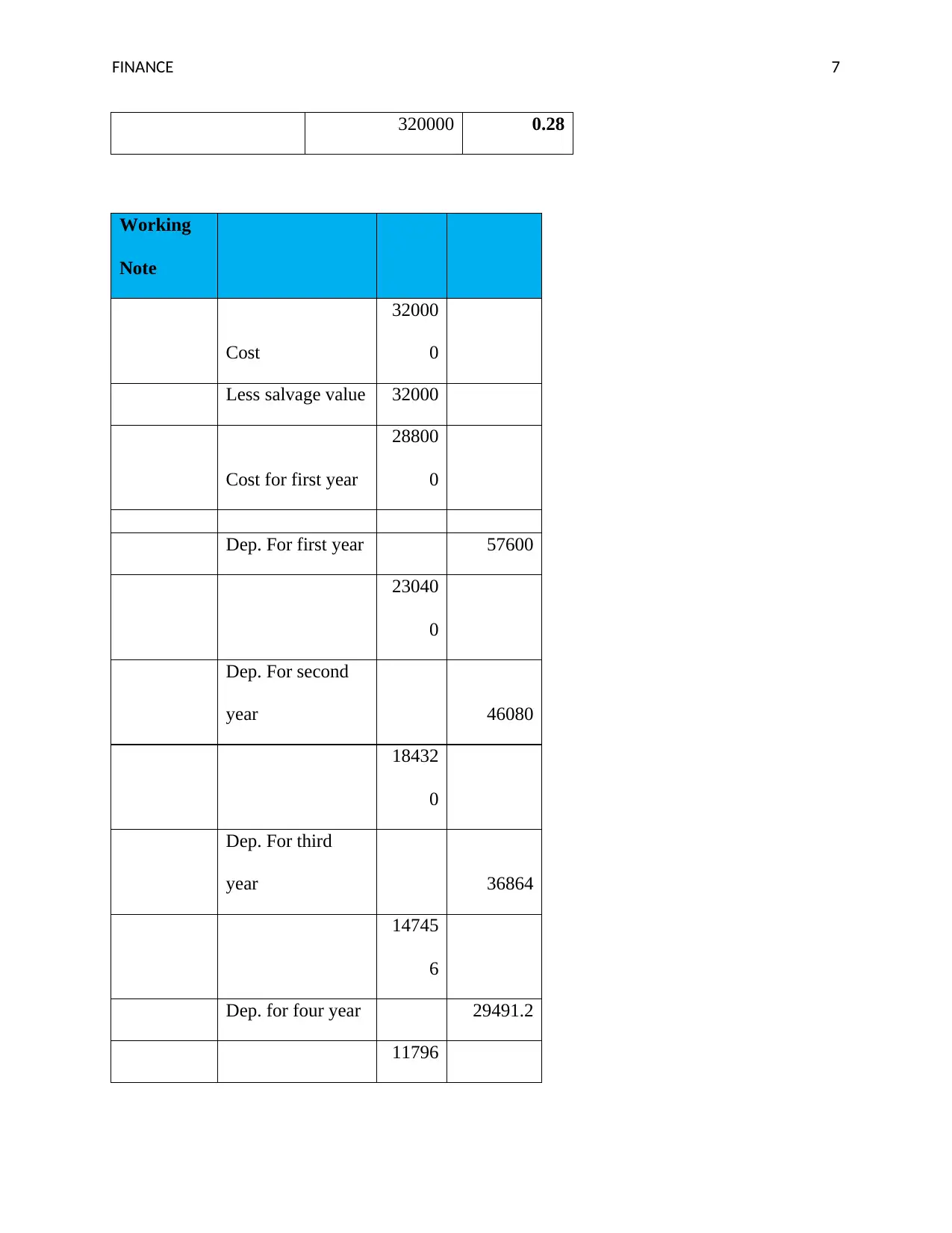

320000 0.28

Working

Note

Cost

32000

0

Less salvage value 32000

Cost for first year

28800

0

Dep. For first year 57600

23040

0

Dep. For second

year 46080

18432

0

Dep. For third

year 36864

14745

6

Dep. for four year 29491.2

11796

320000 0.28

Working

Note

Cost

32000

0

Less salvage value 32000

Cost for first year

28800

0

Dep. For first year 57600

23040

0

Dep. For second

year 46080

18432

0

Dep. For third

year 36864

14745

6

Dep. for four year 29491.2

11796

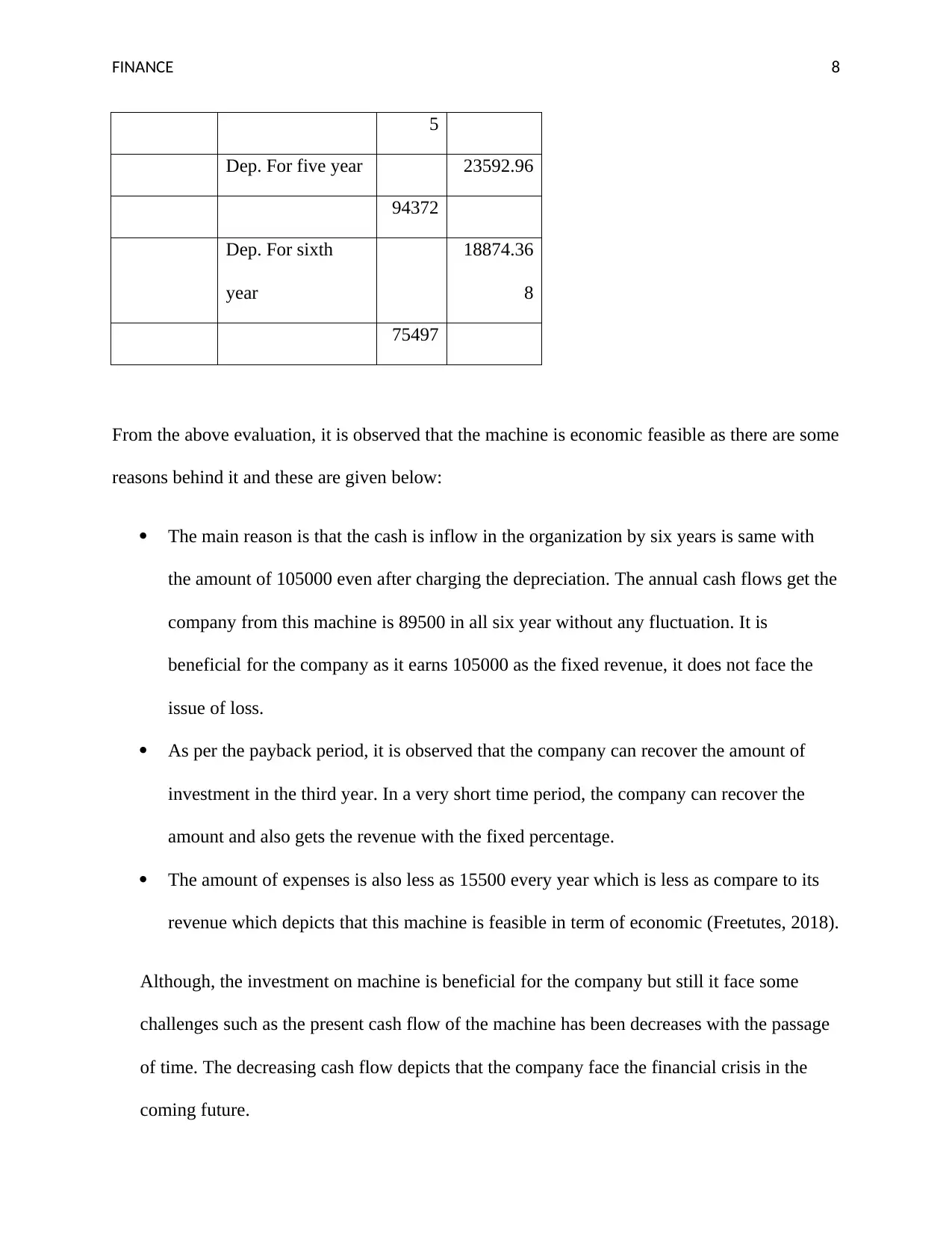

FINANCE 8

5

Dep. For five year 23592.96

94372

Dep. For sixth

year

18874.36

8

75497

From the above evaluation, it is observed that the machine is economic feasible as there are some

reasons behind it and these are given below:

The main reason is that the cash is inflow in the organization by six years is same with

the amount of 105000 even after charging the depreciation. The annual cash flows get the

company from this machine is 89500 in all six year without any fluctuation. It is

beneficial for the company as it earns 105000 as the fixed revenue, it does not face the

issue of loss.

As per the payback period, it is observed that the company can recover the amount of

investment in the third year. In a very short time period, the company can recover the

amount and also gets the revenue with the fixed percentage.

The amount of expenses is also less as 15500 every year which is less as compare to its

revenue which depicts that this machine is feasible in term of economic (Freetutes, 2018).

Although, the investment on machine is beneficial for the company but still it face some

challenges such as the present cash flow of the machine has been decreases with the passage

of time. The decreasing cash flow depicts that the company face the financial crisis in the

coming future.

5

Dep. For five year 23592.96

94372

Dep. For sixth

year

18874.36

8

75497

From the above evaluation, it is observed that the machine is economic feasible as there are some

reasons behind it and these are given below:

The main reason is that the cash is inflow in the organization by six years is same with

the amount of 105000 even after charging the depreciation. The annual cash flows get the

company from this machine is 89500 in all six year without any fluctuation. It is

beneficial for the company as it earns 105000 as the fixed revenue, it does not face the

issue of loss.

As per the payback period, it is observed that the company can recover the amount of

investment in the third year. In a very short time period, the company can recover the

amount and also gets the revenue with the fixed percentage.

The amount of expenses is also less as 15500 every year which is less as compare to its

revenue which depicts that this machine is feasible in term of economic (Freetutes, 2018).

Although, the investment on machine is beneficial for the company but still it face some

challenges such as the present cash flow of the machine has been decreases with the passage

of time. The decreasing cash flow depicts that the company face the financial crisis in the

coming future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 9

(B)

The evaluation has been done by using the methods or techniques of capital budgeting, those are

Payback period, NPV (Net present value) and ARR (Accounting Rate of Return), IRR (Internal

Rate of Return). These methods help to evaluate the economic feasibility of the machine. These

methods have advantages but still there are some difficulties that the organization faces while

using them. The benefits and limitations of these investment appraisal techniques have been

discussed below:

The Net Present Value

Net Present Value defines the difference among the present value of cash inflow and the present

value of cash outflow. This method is used in capital budgeting and investment planning in order

to assess the profitability of a particular project or the option of investment. The positive and

negative Net Present Value defines the different meaning. The positive net present value states

the net profit in an investment and the negative net present value defines the net loss (Berrada,

Loudiyi, and Zorkani, 2017).

Each and every thing has both the aspects such as positive and negative. There are many benefits

and drawbacks of this method and these are discussed below:

Benefits

The main advantage of Net Present Value defines the time value of money

This method help in maximizing the organization value by evaluating the best return on

investment projects and the other capital budgeting activities (Hussain, 2015).

It has been found that the NPV method supports to evaluate the profitability of the project

due to which the company can easily takes the decision regarding the investment. It is

(B)

The evaluation has been done by using the methods or techniques of capital budgeting, those are

Payback period, NPV (Net present value) and ARR (Accounting Rate of Return), IRR (Internal

Rate of Return). These methods help to evaluate the economic feasibility of the machine. These

methods have advantages but still there are some difficulties that the organization faces while

using them. The benefits and limitations of these investment appraisal techniques have been

discussed below:

The Net Present Value

Net Present Value defines the difference among the present value of cash inflow and the present

value of cash outflow. This method is used in capital budgeting and investment planning in order

to assess the profitability of a particular project or the option of investment. The positive and

negative Net Present Value defines the different meaning. The positive net present value states

the net profit in an investment and the negative net present value defines the net loss (Berrada,

Loudiyi, and Zorkani, 2017).

Each and every thing has both the aspects such as positive and negative. There are many benefits

and drawbacks of this method and these are discussed below:

Benefits

The main advantage of Net Present Value defines the time value of money

This method help in maximizing the organization value by evaluating the best return on

investment projects and the other capital budgeting activities (Hussain, 2015).

It has been found that the NPV method supports to evaluate the profitability of the project

due to which the company can easily takes the decision regarding the investment. It is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 10

required for the organization to evaluate the expected return on investment in future so

that it can take the correct decision from the different investment option. Using this

method to assess the profitability of the investment helps to take the better decision in

order to operate the business effectively (Smit, and Trigeorgis, 2017).

Limitations

There are also some disadvantages of using the method of NPV such as estimation of

opportunity cost. It is observed that the organization has to evaluate the opportunity cost

for taking the best decision in investment. The opportunity cost defines the next

beneficial investment project for the company. This cost has been considered at the initial

stages by considered the opportunity cost affects the result in terms of wrong decision. As

per this method, people have two options from which it has to select the best one option

for the company in term of investment. But due to evaluating the two investment option

which is considered as the opportunity cost affects the decision of the company in order

to select option for it (Bora, 2015).

It is determined that the evaluation of Net Present Value is not that easy for a human

being. It requires the professional and well qualified person who can easily evaluate it

with his best knowledge. The company has to hire the well qualified person with the high

compensation so that he performs his job very well. It is observed that the hiring the

qualified person consumes the high cost which affects the net profit of the organization.

The company also has to invest the high amount before starting the project such as on

research and development department. The cost incurred before starting the project

affects the result but ignoring these costs is a difficult task for corporate finance team.

required for the organization to evaluate the expected return on investment in future so

that it can take the correct decision from the different investment option. Using this

method to assess the profitability of the investment helps to take the better decision in

order to operate the business effectively (Smit, and Trigeorgis, 2017).

Limitations

There are also some disadvantages of using the method of NPV such as estimation of

opportunity cost. It is observed that the organization has to evaluate the opportunity cost

for taking the best decision in investment. The opportunity cost defines the next

beneficial investment project for the company. This cost has been considered at the initial

stages by considered the opportunity cost affects the result in terms of wrong decision. As

per this method, people have two options from which it has to select the best one option

for the company in term of investment. But due to evaluating the two investment option

which is considered as the opportunity cost affects the decision of the company in order

to select option for it (Bora, 2015).

It is determined that the evaluation of Net Present Value is not that easy for a human

being. It requires the professional and well qualified person who can easily evaluate it

with his best knowledge. The company has to hire the well qualified person with the high

compensation so that he performs his job very well. It is observed that the hiring the

qualified person consumes the high cost which affects the net profit of the organization.

The company also has to invest the high amount before starting the project such as on

research and development department. The cost incurred before starting the project

affects the result but ignoring these costs is a difficult task for corporate finance team.

FINANCE 11

The Internal Rate of Return

It is also a capital budgeting tool that is used to take the decision for a particular project. In this

method, discounting rate where the total of initial investment and discounted cash inflow is

equivalent to zero. It can be said that it is a discounting rate in which the value of NPV is just

equal to zero. In order to compute the IRR (Internal Rate of Return), it is required to evaluate the

NPV or present cash inflow of all years. The evaluation of IRR is based on the formula of NPV.

The amount of discount rate or cost of capital is multiple with the amount of cash flows. Cash

inflow has been evaluated in order to calculate NPV.

Benefits

Time value of money is major part that is necessary to considered while evaluating the

expected return in future. In this method, time value of money has been considered while

evaluating IRR that helps to estimates the accurate results or returns that the company

gets in future( Clear Tax, 2019).

Another advantage of this method is that it can easily represent in front of mangers. After

the evaluation of IRR, it is easy for the company to display the IRR to represent the

percentage to managers.

It has been seen that this method is not only easy to represent the percentage but it also

easy to assess the rate of return. As compare to the other method, it is easy to evaluate the

internal rate of return.

It helps to take the decision on the basis of rate of return. The managers of the company

evaluate the rate just because of estimation for future plans.

The Internal Rate of Return

It is also a capital budgeting tool that is used to take the decision for a particular project. In this

method, discounting rate where the total of initial investment and discounted cash inflow is

equivalent to zero. It can be said that it is a discounting rate in which the value of NPV is just

equal to zero. In order to compute the IRR (Internal Rate of Return), it is required to evaluate the

NPV or present cash inflow of all years. The evaluation of IRR is based on the formula of NPV.

The amount of discount rate or cost of capital is multiple with the amount of cash flows. Cash

inflow has been evaluated in order to calculate NPV.

Benefits

Time value of money is major part that is necessary to considered while evaluating the

expected return in future. In this method, time value of money has been considered while

evaluating IRR that helps to estimates the accurate results or returns that the company

gets in future( Clear Tax, 2019).

Another advantage of this method is that it can easily represent in front of mangers. After

the evaluation of IRR, it is easy for the company to display the IRR to represent the

percentage to managers.

It has been seen that this method is not only easy to represent the percentage but it also

easy to assess the rate of return. As compare to the other method, it is easy to evaluate the

internal rate of return.

It helps to take the decision on the basis of rate of return. The managers of the company

evaluate the rate just because of estimation for future plans.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.